BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The S&P 500 closed within a hair of a new record yesterday marking an enormous comeback that followed the April announcement of “Liberation Day” tariffs.

Despite a persistent vibe of uncertainty related to US economic policy and geopolitics:

The S&P 500 closed less than 0.1% away from a record high which it notched in February before cratering nearly 20% in April. The index has regained ground in fits and starts since then and briefly surpassed its record in intra-day trading yesterday.

On Monday, the tech-heavy NASDAQ 100 one-upped the broader market and logged its highest-ever close. It came after President Trump said Israel and Iran agreed to a ceasefire, which eased investors’ concerns about a potential oil crisis.

According to Morning Brew, between unresolved geopolitical conflicts and President Trump’s still-unfolding tariff policies, a portfolio manager with Capital Wealth Planning, Kevin Simpson, told CNBC that he was “surprised by the magnitude of the rebound.”

If you are just starting out managing your finances and don’t know where to begin, a financial coach may be a good option for you. They are helpful for someone who wants to become proficient in the basics of finance, from learning how to budget or save money to building an emergency fund or creating a plan for paying off debt. If you have short-term money goals, like saving for a big purchase or just practicing better money habits, a financial coach can help you reach them by working with you to create a plan and holding you accountable. Even more for physicians and most all medical professionals.

Pros and Cons of Working with a Financial Coach A financial coach can have a positive impact on your financial well–being and your life in a number of ways:

Financial coaches see the bigger picture of how you relate to money. They can help you develop better habits, resulting in positive personal growth.

By providing education and encouragement, they can reduce financial stress, confusion, and what it is about money that overwhelms you.

Through accountability and support, they can help you accomplish your goals and help you feel more confident in your finances.

Available 24/7/365.

Modest fees.

At you service. Dr. David Edward Marcinko MBA MEd CMP

Posted on June 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

A June 11th report from global professional services firm Alvarez & Marsal (A&M) predicts that more beneficiaries might soon ditch insurance coverage for options like short-term, limited duration plans or healthcare sharing ministries (HCSMs), which aren’t regulated like health insurance and aren’t required to comply with ACA protections like covering maternity care or pre-existing conditions.

Nvidia extended its winning streak to five days, rising another 1.73% as the AI trade continues to recover.

EchoStar climbed 13.16% after the parent company of Dish TV disclosed that President Trump did in fact prod the FCC to make a deal.

Cyngn soared another 20.07% following a big day of gains after the company that makes self-driving tech for industrial vehicles announced a partnership with Nvidia.

Strong earnings from Nike (more on that later) propelled sporting goods stocks higher today. ONHoldings rose 1.74%, while Dick’s Sporting Goods climbed 3.59%.

Domestic power producers popped on reports that Trump is planning to issue an executive order increasing energy production to meet AI demand. Vistra gained 2.44%, GE Vernova climbed 2.54%, and Vertiv added 2.71%.

What’s down

Coinbase Global ended its winning streak, tumbling 5.77% after GENIUS Act hype propelled the crypto stock skyward all week long. Traders took profits in Circle as well, pushing the stablecoin stock down 15.54%.

Chinese EV maker LiAuto fell 1.93% on its weaker-than-expected deliveries forecast for the second quarter.

Fellow Chinese EV maker Xiaomi stunned markets with reports that it received 240,000 orders for its new SUV within 18 hours of its debut, but shares still sank 4%.

Pony.ai lost 6.31% on a report that Uber is considering helping its founder Travis Kalanick fund his acquisition of the US subsidiary of the Chinese autonomous vehicle company.

Gold miners tumbled while the price of the precious metal fell as investors took a risk-on stance. Newmont lost 4.11%, BarrickMining fell 3.44%, and KinrossGold shed 6.18%.

Today’s trade deal reopens the door for Chinese rare earth imports, bad news for US producers like MPMaterials (down 8.59%) and USA Rare Earth (down 12.14%).

If you’re looking at this tab, chances are you are fed up with your financial brokerage accounts, thinking of finances, investing, retirement or all of the above.

And so, we can help

An investment portfolio second opinion, also called a “ portfolio review,” is an analysis of your financial holdings and associated strategies, allocations, fees and performance to determine whether the most effective instruments and methodologies are being utilized to reach your goals.

No Worries! You may have come to the right place.

E-Mail Ann Miller RN MHA CPHQ for an Initial Appointment: MarcinkoAdvisors@outlook.com

The purpose of this initial appointment is for you to ask a lot of questions to make sure you are comfortable with potentially working with us. It also helps if you are prepared to provide a verbal summary of your current situation.

Here are some questions to consider asking us during your first meeting:

1) Can you tell us about your financial qualifications, experience, education and training; if any?

2) Can you provide some information about your current financial advisory team?

3) On what type of investments do you typically purchase and own?

5) How much do pay your financial management firm?

6) How long have you been working with your current financial management firm?

8) What other services does your financial team provide?

Posted on June 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BY A.I.

***

***

Stocks: The S&P 500 briefly traded a few cents above its February all-time closing high yesterday afternoon, but couldn’t sustain the gain and fell just short at the end of the day. The NASDAQ remains inches away from its record high as well.

Deals: The end of the 90-day tariff pause is less than two weeks away, but the White House said that the July 9th deadline “is not critical.”

Meanwhile, the Treasury Department is doing everything it can to make the dreaded “revenge tax” in the big, beautiful bill irrelevant.

Commodities: Gold and oil had muted moves upward but copper climbed to a three-month high after Goldman Sachs analysts warned of shortages ahead

Posted on June 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Stocks: The S&P 500 and NASDAQ started the day inches away from their all-time highs, but the market rally faltered in mid-afternoon as relief from an Israel/Iran ceasefire faded and investors turned their attention to Friday’s PCE report.

Economy: Speaking of inflation, Jerome Powell stuck to his guns during his second day of congressional testimony, endorsing a wait-and-see mentality. President Trump is apparently tired of waiting, and says he has “3 or 4” candidates in mind to replace Powell.

Commodities: Oil bounced back after posting its biggest two-day decline since 2022.

Although many academics argue that value stocks outperform growth stocks, the returns for individuals investing through mutual funds demonstrate a near match.

Introduction

A 2005 study Do Investors Capture the Value Premium? written by Todd Houge at The University of Iowa and Tim Loughran at The University of Notre Dame found that large company mutual funds in both the value and growth styles returned just over 11 percent for the period of 1975 to 2002. This paper contradicted many studies that demonstrated owning value stocks offers better long-term performance than growth stocks.

The studies, led by Eugene Fama PhD and Kenneth French PhD, established the current consensus that the value style of investing does indeed offer a return premium. There are several theories as to why this has been the case, among the most persuasive being a series of behavioral arguments put forth by leading researchers. The studies suggest that the out performance of value stocks may result from investors’ tendency toward common behavioral traits, including the belief that the future will be similar to the past, overreaction to unexpected events, “herding” behavior which leads at times to overemphasis of a particular style or sector, overconfidence, and aversion to regret. All of these behaviors can cause price anomalies which create buying opportunities for value investors.

Another key ingredient argued for value out performance is lower business appraisals. Value stocks are plainly confined to a P/E range, whereas growth stocks have an upper limit that is infinite. When growth stocks reach a high plateau in regard to P/E ratios, the ensuing returns are generally much lower than the category average over time.

Moreover, growth stocks tend to lose more in bear markets. In the last two major bear markets, growth stocks fared far worse than value. From January 1973 until late 1974, large growth stocks lost 45 percent of their value, while large value stocks lost 26 percent. Similarly, from April 2000 to September 2002, large growth stocks lost 46 percent versus only 27 percent for large value stocks. These losses, academics insist, dramatically reduce the long-term investment returns of growth stocks.

***

***

However, the study by Houge and Loughran reasoned that although a premium may exist, investors have not been able to capture the excess return through mutual funds. The study also maintained that any potential value premium is generated outside the securities held by most mutual funds. Simply put, being growth or value had no material impact on a mutual fund’s performance.

Listed below in the table are the annualized returns and standard deviations for return data from January 1975 through December 2002.

Index Return SD

S&P 500 11.53% 14.88%

Large Growth Funds 11.30% 16.65%

Large Value Funds 11.41% 15.39%

Source: Hough/Loughran Study

The Hough/Loughran study also found that the returns by style also varied over time. From 1965-1983, a period widely known to favor the value style, large value funds averaged a 9.92 percent annual return, compared to 8.73 percent for large growth funds. This performance differential reverses over 1984-2001, as large growth funds generated a 14.1 percent average return compared to 12.9 percent for large value funds. Thus, one style can outperform in any time period.

However, although the long-term returns are nearly identical, large differences between value and growth returns happen over time. This is especially the case over the last ten years as growth and value have had extraordinary return differences – sometimes over 30 percentage points of under performance.

This table indicates the return differential between the value and growth styles since 1992.

YEARLY RETURNS OF GROWTH/VALUE STOCKS

Year

Growth

Value

1992

5.1%

10.5%

1993

1.7%

18.6%

1994

3.1%

-0.6%

1995

38.1%

37.1%

1996

24.0%

22.0%

1997

36.5%

30.6%

1998

42.2%

14.7%

1999

28.2%

3.2%

2000

-22.1%

6.1%

2001

-26.7%

7.1%

2002

-25.2%

-20.5%

2003

28.2%

27.7%

2004

6.3%

16.5%

2005

3.6%

6.1%

2006

10.8%

20.6%

2007

8.8%

1.5%

2008

-38.43%

-36.84%

2009

37.2%

19.69%

2010

16.71%

15.5%

2011

2.64%

0.39%

2012

15.25%

17.50%

Source: Ibbottson.

Between the third quarter of 1994 and the second quarter of 2000, the S&P Growth Index produced annualized total returns of 30 percent, versus only about 18 percent for the S&P Value Index. Since 2000, value has turned the tables and dramatically outperformed growth. Growth has only outperformed value in two of the past eight years. Since the two styles are successful at different times, combining them in one portfolio can create a buffer against dramatic swings, reducing volatility and the subsequent drag on returns.

Assessment

In our analysis, the surest way to maximize the benefits of style investing is to combine growth and value in a single portfolio, and maintain the proportions evenly in a 50/50 split through regular rebalancing. Research from Standard & Poor’s showed that since 1980, a 50/50 portfolio of value and growth stocks beats the market 75 percent of the time.

Conclusion

Due to the fact that both styles have near equal performance and either style can outperform for a significant time period, a medical professional might consider a blending of styles. Rather than attempt to second-guess the market by switching in and out of styles as they roll with the cycle, it might be prudent to maintain an equal balance your investment between the two.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

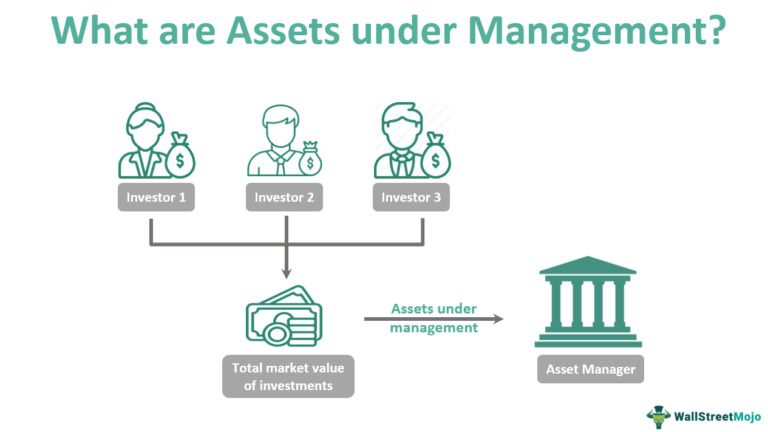

Assets under management (AUM) is a significant parameter in the financial world. It answers financial questions like – how many investments does a company manage? What is the net value of the investments that the company manages? Finally, how many investors have trusted their assets with the company? The higher the answer to these three questions, the more glory to the company.

A wealthy investor who is not concerned by higher fees but wants maximum returns of their asset will probably choose an asset manager based on its AUM. Thus, the AUM indicates the financial performance of the firm. Also, based on the funds under management, the firm collects fees from other clients.

So, what are the investments which qualify as AUM? Any liquid asset of the investor they have entrusted the asset manager with monitoring and control. For example, bank deposits, cash balances, equity shares, bonds, mutual funds, and other investments.

What are the services an asset manager provides to their clients? The most important function is decision-making. With the constant fluctuations and rapid movements in the market, an asset manager has to make decisions about holding or selling an investment. The firm communicates with the investors and advises them about the necessary action.

Once the decision is taken, the firm acts on the decision, i.e., the investor does not have to enter the field. In addition, the asset management company will buy, sell, and make any other transactions on behalf of the investor. Finally, the firm also renders services like accounting, tax reporting, proxy voting (equity shares), client reporting, and other financial services.

What are Assets Under Advisement?

Assets under advisement refer to assets on which your firm provides advice or consultation but for which your firm does either does not have discretionary authority or does not arrange or effectuate the transaction. Such services would include financial planning or other consulting services where the assets are used for the informational purpose of gaining a full perspective of the client’s financial situation, but you are not actually placing the trade.

Assets under advisement could also be those which you monitor for a client on a non-discretionary basis, where you may make recommendations but where the client is the party responsible for arranging or effecting the purchase or sale. A common example of this scenario is when an adviser reviews a participant’s 401(k) allocations. If the adviser does not have the authority or ability to effect changes in the portfolio, these assets are likely considered assets under advisement rather than regulatory assets under management.

Assets under advisement are permitted to be disclosed on Form ADV Part 2A as a separate asset figure from the assets under management. There is no requirement to disclose the assets under advisement figure, but some advisers opt to include the figure to give prospective clients a more complete picture of the firm’s responsibilities. If you choose to report your assets under advisement, be sure to make a clear distinction between this figure and your regulatory assets under management.

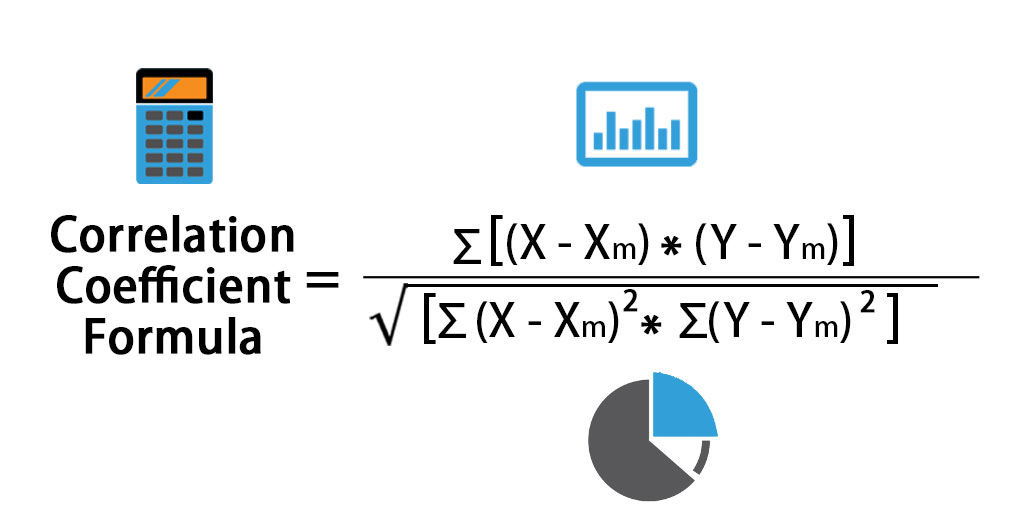

Correlation measures the relationship between two investments–the higher the correlation, the more likely they are to move in the same direction for a given set of economic or market events. Correlation, in the finance and investment industries, is a statistic that measures the degree to which two securities move in relation to each other. Correlations are used in advanced portfolio management, computed as the correlation coefficient which has a value that must fall between -1.0 and +1.0.

So if two securities are highly positively correlated, they will move in the same direction the vast majority of the time. Negatively correlated investments do the opposite–as one security rises, the other falls, and vice versa. No correlation means there is no relationship between the movement of two securities–the performance of one security has no bearing on the performance of the other.

Correlation is an important concept for portfolio diversification--combining assets with low or negative correlations can improve risk-adjusted performance over time by providing a diversity of payouts under the same financial conditions.

here are many ways for a doctor, osteopath, podiatrist or dentist to financially invest. Traditionally, this meant picking individual stocks and bonds. Today, there are many other ways to purchase securities en mass. For example:

MUTUAL FUND: A regulated investment company that manages a portfolio of securities for its shareholders.

Open End Mutual Funds: An investment company that invests money in accordance with specific objectives on behalf of investors. Fund assets expand or contract based on investment performance, new investments and redemptions. Trade at Net Asset Value or the price the fund shares scheduled with the US Securities and Exchange Commission (SEC) trade. NAV can change on a daily basis. Therefore, per-share NAV can, as well.

Closed End Mutual Funds: Older than open end mutual funds and more complex. A CEMF is an investment company that registers shares SEC regulations and is traded in securities markets at prices determined by investments. Shares of closed-end funds can be purchased and sold anytime during stock market hours. CEMF managers don’t need to maintain a cash reserve to redeem or / repurchase shares from investors. This can reduce performance drag that may otherwise be attributable to holding cash. CEMFs may be able to offer higher returns due to the heavier use of leverage [debt]. They are subject to volatility, less liquid than open-end funds, available only through brokers and may sells at a heavily discount or premium to [NAV] determined by subtracting its liabilities from its assets. The fund’s per-share NAV is then obtained by dividing NAV by the number of shares outstanding. .

Sector Mutual Funds: Sector funds are a type of mutual fund or Exchange-Traded Fund (ETF) that invests in a specific sector or industry such as technology, healthcare, energy, finance, consumer goods, or real estate. Sector funds focus on a particular industry, allowing investors to gain targeted exposure to specific market areas. The goal is to outperform the overall market by investing in companies within a specific sector that is expected to perform well. However, they are also more susceptible to market fluctuations and specific sector risks, making them a more specialized and potentially higher-risk investment option.

EXCHANGE TRADED FUNDS: ETFs are a type of fund that owns various kinds of securities, often of one type. For example, a stock ETF holds stocks, while a bond ETF holds bonds. One share of the ETF gives buyers ownership of all the stocks or bonds in the fund. If an ETF held 100 stocks, then those who owned the fund would own a stake – albeit a very tiny one – in each of those 100 stocks.

ETFs are typically passively managed, meaning that the fund usually holds a fixed number of securities based on a specific preset index of investments. These are tax efficient. In contrast, many mutual funds are actively managed, with professional investors trying to select the investments that will rise and fall.

The Standard & Poor’s 500 Index is perhaps the world’s best-known index, and it forms the basis of many ETFs. Other popular indexes include the Dow Jones Industrial Average and the National Association of Securities Dealers Automated Quotations [NASDAQ] Composite Index.

ETFs based on these funds are called Index Funds and just buy and hold whatever is in the index and make no active trading decisions. ETFs trade on a stock exchange during the day, unlike mutual funds that trade only after the market closes. With an ETF you can place a trade whenever the market is open and know exactly the price you’re paying for the fund.

INDEX FUNDS: Index funds mirror the performance of benchmarks like the DJIA. These passive investments are an unimaginative way to invest. Passive index funds tracking market benchmarks accounted for just 21% of the U.S. equity fund market in 2012. By 2024, passive index funds had grown to about half of all U.S. fund assets. This rise of passive funds has come as they often outperform their actively managed peers. According to the widely followed S&P Indices Versus Active (SPIVA) scorecards, about 9 out of 10 actively managed funds didn’t match the returns of the S&P 500 benchmark in the past 15 years.

ASSESSMENT

Investing in individual stocks is psychologically and academically different than investing in the above funds, according to psychiatrist and colleague Ken Shubin-Stein MD, MPH, MS, CFA who is a professor of finance at the Columbia University Graduate School of Business When you buy shares of a company, you are putting all your eggs in one basket. If the company does well, your investment will go up in value. If the company does poorly, your investment will go down. Fund diversification helps reduce this risk.

CONCLUSION

Investing in the above fund types will help mitigate single company security risk.

References:

1. Fenton, Charles, F: Non-Disclosure Agreements and Physician Restrictive Covenants. In, Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. Productivity Press, New York, 2015.

Readings:

1. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017

2. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

4. Shubin-Stein, Kenneth: Unifying the Psychological and Financial Planning Divide [Holistic Life Planning, Behavioral Economics, Trading Addiction and the Art of Money]. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

We make second investment portfolio opinions affordable

Approximately 1 million allopathic physicians, 150,000 dentists, 200,000 osteopaths, 15,000 podiatrists and 6 million nurses often find it difficult to get an unbiased and fiduciary second opinion on their retirement or brokerage accounts. By offering second opinions for a flat fee, the monetary barriers that prevented colleagues from receiving a second opinion in the past have been removed.

We make second investment portfolio opinions convenient

Here’s how we work: you book an initial appointment with us, answer a few preliminary questions and email us your portfolio information. We then provide a second opinion. It is then up to you to incorporate or not.

We make second investment portfolio opinions timely

Financial markets, jobs and colleague age change like the weather. It is not always okay to wait a week, year or more, to seek a professional second financial portfolio opinion. You need to receive an opinion now. That’s where we come in. We are standing by, ready to take your email [MarcinkoAdvisors@outlook.com] and schedule a free initial consultation within two or three days, or less.

We make second investment portfolio opinions accurate

Fiduciary and non-sales orientated second opinions have the power to change financial lives in the long term. We’ve seen it happen many times. What characterizes a good second opinion? Three things: the opinion must be individualized to your investment portfolio[s], informed and results-oriented. That’s the informed fiduciary approach we take. We are colleagues and look forward to working with you.

Posted on June 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On May 13th, 2025, the CMS Center for Medicare & Medicaid Innovation (CMMI) introduced a new strategic plan for its models going forward. After ending four payment models early and canceling two not-yet-implemented models in March 2025, the agency had promised to release a new strategy. Nearly two weeks later, CMMI released that strategy, as well as a preliminary evaluation of, and changes to, one of its core payment models.

This Health Capital Topics article will review CMMI’s recent actions and what initial indications these actions provide. (Read more…)

Many doctors are surprised to learn of an alternative investment known as a hedge fund, pooled investment vehicle or private investment fund. Unlike mutual funds, they can be structured in many ways. However, these funds cannot be marketed or advertised, but they are far from illegal or illicit.

In fact, physicians were among the early investors in one the most successful hedge funds. Warren Buffett got his start in 1957 running the Buffett Partnership, a hedge fund not open to the public. His first appearance as a money manager was before a group of physicians in Omaha, Nebraska. Eleven decided to invest some money with him. A few then followed into Berkshire Hathaway Inc, now among the most highly valued companies in the world.

And, more recently, Scion Asset Management® LLC, is a private investment firm founded and led by my eloquent colleague Michael J. Burry, MD and featured in the movie, The Big Short. Other hedge fund mangers of note include: George Soros, Carl Icahn, Ken Griffin, David Tepper, John Paulson and Bill Ackman.

A hedge fund is a limited partnership of private investors whose money is managed by professional fund managers who use a wide range of strategies; including leveraging [debt] or trading of non-traditional assets [real-estate, collectible, commodities, cyrpto-currency, etc] to earn above-average returns. Hedge funds are considered a risky alternative investment and usually require a high minimum investment or net worth. This person is known as an “accredited investor” or “Regulation D” investor by the US Securities Exchange Commission and must have the following attributes:

A net worth, combined with spouse, of over $1 million, not including primary residence

An income of over $200,000 individually, or $300,000 with a spouse, in each of the past two years

The hurdle rate is part of the fund manager’s performance incentive compensation. Also known as a “benchmark,” it is the amount, expressed in percentage points an investor’s capital must appreciate before it becomes subject to a performance incentive fee. Podiatrists should view the hurdle rate as a form of protection or the fee arrangement.

The hurdle rate benchmarks a single year’s performance and may be considered mutually exclusive of any other year, or the hurdle rate may compound each year. The former case is more common. In the latter case, a portfolio manager failing to attain a hurdle rate in the first year will find the effective hurdle rate considerably higher during the second year.

Once a fund manager attains the hurdle rate, the investor’s capital account may be charged a performance incentive fee only on the performance above and beyond the hurdle rate. Alternatively, the account may be charged a performance fee for the entire level of performance, including the performance required to attain the hurdle rate. Other variations on the use of the hurdle rate exist, and are limited only by the contract signed between the fund manager and the investor. The hurdle rate is not generally a negotiating point, however.

Example: A fund charges a performance fee with a 6 percent hurdle rate, calculated in mutually exclusive manner. A podiatrist places $100,000 with the fund. The first year’s performance is 5 percent. The doctor therefore owes no performance fee during the first year because the portfolio manager did not attain the hurdle rate. During year two, the portfolio manager guides the fund to a 7 percent return. Because the hurdle rate is mutually exclusive of any other year, the portfolio manager has attained the 6 percent hurdle rate and is entitled to a performance fee.

High Water Mark

Some hedge funds feature a “high water mark” provision known as a ”loss-carry forward.” As with the hurdle rate, the high water mark is a form of protection. It is an amount equal to the greatest value of an investor’s capital account, adjusted for contributions and withdrawals. The high water mark ensures that the manager charges a performance incentive fee only on the amount of appreciation over and above the high water mark set at the time the performance fee was last charged. The current trend is for newer funds to feature this high water mark, while older, larger funds may not feature it.

Example: A fund charges a 20 percent performance fee with a high water mark but no hurdle rate. A podiatrist contributes $100,000 to the fund. During the first year, the hedge fund manager grows that capital account to $110,000 and charges a 20 percent performance fee, or $2,000. The ending capital account balance and high water mark is therefore $108,000. During year two, the account falls back to $100,000, but the high water mark remains $108,000. During year three, in order for the manager to charge a performance fee, the manager must grow the capital account to a level above $108,000.

Claw Back Provision

Rarely, a hedge fund may provide investors with a “claw back” provision. This term results in a refund to the investor of all or part of a previously charged performance fee if a certain level of performance is not attained in subsequent years. Such refunds in the face of poor or inadequate performance may not be legal in some states or under certain authorities.

ASSESSMENT

Managers of hedge funds, like colleague Dimitri Sogoloff MBA who is the CEO of Horton Point investment-technology firm, often aim to produce returns that are relatively uncorrelated with market indices and are consistent with investors’ desired level of risk.

While hedging may reduce some risks overall, they cannot all be eliminated. According to a report by the Hennessee Group, hedge funds were approximately one-third less volatile between 1993 and 2010.

For a podiatrist who already holds mutual funds and/or individual stocks and bonds, a hedge fund may provide diversification and reduce overall portfolio risk. Consider investing in them with care.

2. Burry, Michael, J: Hedge Funds [Wall Street Personified]. In, Marcinko, DE and Hetico, HR: Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

3. Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. Productivity Press, New York, 2015.

4. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

WHAT YOU “MUST KNOW“ ABOUT FINANCIAL ADVISORY FEES

Investment fees still matter despite dropping dramatically over the past several decades due to computer automation, algorithms and artificial intelligence, etc. And, they can make a big difference to your financial health. So, before buying any investment, it’s vital to uncover all real financial advisor and stock broker costs.

1. Up-front salesperson commissions. It is easy to ask; “If I buy this investment today and want to get out tomorrow, how much money do I get back?” If the answer is not “all your money,” the difference is probably upfront fees and commissions. These fees may run as high as 30% of the money invested. If you were to earn 5% a year on the investment, it would take 8 years just to break even.

2. Ongoing advisory fees. These are monthly, quarterly, or annual fees paid to advisors for their investment advice and oversight. This includes working with you to pick the asset classes, set diversification, select a portfolio manager, optimize taxes, re-balance holdings and other periodic tasks.

These fees have many names including wrap fee or investment advisory fees. The normal “rule of thumb” is 1% of assets managed, although fees can range from 0 to 7%. Today, it can even be as low as .5%. It can be charged even if the advisor receives an upfront commission. It can be easy to see, or hidden in the fine print.

3. Additional service fees. Find out specifically what services are included financial advisory fees. Additional fees for financial planning or other services are rarely disclosed. They can range from minimal hand-holding focused on your investments to comprehensive financial planning.

4. Ongoing managerial expense ratio fees. These are incredibly well hidden that you may not see them in your statements or invoices. The only way to know is to read the prospectus or other third party analysis, like Morningstar.com. And, they can vary greatly for the same investment, depending on the class of share you buy.

For example, American Fund’s New Perspective Fund’s expense ratio ranges from 0.45% to 1.54%. The average expense ratio of a mutual fund that invests in stocks is 1.35%. Conversely, the average expense ratio of a Vanguard S&P 500 Fund is 0.10%. The difference of 1.25% is staggering over time.

5. Miscellaneous fees. Some advisors charge $50 – $100 a year per account to open or close an account, and even fees to dollar cost average your funds into the market.

6. Transaction fees. Every time you buy or sell a fund, a fee is typically paid to a custodian. These can range from $5 to hundreds of dollars per transaction.

7. Fee Only: Paid directly by clients for their services and can’t receive other sources of compensation, such as payments from fund providers. Act as a fiduciary, meaning they are obligated to put their clients’ interests first

8. Fee Based: Paid by clients but also via other sources, such as commissions from financial products that clients purchase. Brokers and dealers (or registered representatives) are simply required to sell products that are “suitable” for their clients.

A “suitable” investment is defined by FINRA as one that fits the level of risk that an investor is willing and able, as measured by personal financial circumstances, to take on. The Financial Industry Regulatory Authority is a private American corporation that acts as a Self Regulatory Organization (SRO) that regulates member stock brokerage firms and exchange markets. These criteria must be met. It is not enough to state that an investor has a risk-friendly investment profile. In addition, they must be in a financial position to take certain chances with their money. It is also necessary for them to

A hedge fund is a limited partnership of private investors whose money is managed by professional fund managers who use a wide range of strategies; including leveraging [debt] or trading of non-traditional assets [real-estate, collectible, commodities, cyrpto-currency, etc] to earn above-average returns. Hedge funds are considered a risky alternative investment and usually require a high minimum investment or net worth. This person is known as an “accredited investor” or “Regulation D” investor by the US Securities Exchange Commission and must have the following attributes:

A net worth, combined with spouse, of over $1 million, not including primary residence

An income of over $200,000 individually, or $300,000 with a spouse, in each of the past two years

Choose the fee structure. The fee structure should align with your needs. Consider the type of advice you seek, the number of times needed and the complexity of your financial situation. You can always negotiating tactics are free to ask for a better deal.

Compare fees. It is essential to research and compare different fees. Be sure to read the fine print for details or costs that are not a base fee.

Robo-advisors: For simple investment goals, with little specificity, robo-advisors may be a cost-effective option. They charge lower fees than conventional financial advisors and provide an automated, algorithmic approach to managing your investments.

Assessment

The average cost of working with a human financial advisor in 2024 was 0.5% to 2.0% of assets managed, $200 to $400 per hourly consultation, a flat fee of $1,000 to $3,000 for a one-time service, and/or a 3% to 6% commission fee on the product types sold.

When ruminating over financial advisory fees; read and understand the contract with disclosures, do not sign a confidentiality or non-disclosure agreement, and do not waive your right to a lawsuit. According to colleague Dr. Charles F. Fenton IIII JD, forced legal settlements almost always favor the advisor over the client.

2. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

3. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

If you’re looking at this tab, chances are you are fed up, burned out, seeking a better work-life balance, looking for a new non-clinical career, thinking of retirement, or all of the above. Perhaps you are just looking to regain the joy and meaning in your medical career. No worries! You may have come to the right place.

We work only with doctors, dentists, podiatrists, nurses, technicians and healthcare providers who struggle with personal and professional disillusionment, burnout, financial distress and an unbalanced life – all of which can happen at any stage of a medical career.

Through our coaching sessions, medical and healthcare professionals and colleagues can achieve a more meaningful, purposeful, and financially flourishing life.

Posted on June 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On April 11th, 2025, the Centers for Medicare & Medicaid Services (CMS) released its proposed rules for the payment and policy updates for the Medicare inpatient prospective payment system (IPPS) and long-term care hospital prospective payment system (LTCH PPS) for fiscal year (FY) 2026.

This Health Capital Topics article will discuss the proposed rule and the implications for stakeholders. (Read more…)

50% tariffs on steel and aluminum went into effect today. To celebrate, President Trump hopped on Truth Social to put China’s President Xi on blast ahead of an expected call between the two heads of state. And, Temu lost 58% of its daily users thanks to tariffs.

The president also pushed Jerome Powell to “LOWER THE RATE” following terrible private sector job numbers. Stocks are seemingly immune to tough trade talk and interest rate rants at this point, but bond yields sank on fears of slower economic growth.

The US dollar slipped, propelling gold higher as investors sought safety.

Posted on June 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

A recent joint report by the National Association of Accountable Care Organizations (NAACOS) and Innovaccer Inc., a healthcare artificial intelligence (AI) company, found tangible evidence that the U.S. healthcare delivery system is indeed moving toward value-based care (VBC).

Fifteen years after the passage of the Patient Protection and Affordable Care Act (ACA), which promoted VBC through the advent of ACOs and other alternative payment models, there is finally evidence that providers are actually moving in that direction.

This Health Capital Topics article reviews the joint report on “The State and Science of Value-based Care 2025.”(Read more…)

Life planning and behavioral finance as proposed for physicians and integrated by the Institute of Medical Business Advisors Inc., is unique in that it emanates from a holistic union of personal financial planning, human physiology and medical practice management, solely for the healthcare space. Unlike pure life planning, pure financial planning, or pure management theory, it is both a quantitative and qualitative “hard and soft” science, with an ambitious economic, psychological and managerial niche value proposition never before proposed and codified, while still representing an evolving philosophy. Its’ first-mover practitioners are called Certified Medical Planners™.

Financial Life Planning is an approach to financial planning that places the history, transitions, goals, and principles of the client at the center of the planning process. For the financial advisor or planner, the life of the client becomes the axis around which financial planning develops and evolves.

Financial Life Planning is about coming to the right answers by asking the right questions. This involves broadening the conversation beyond investment selection and asset management to exploring life issues as they relate to money.

Financial Life Planning is a process that helps advisors move their practice from financial transaction thinking, to life transition thinking. The first step is aimed to help clients “see” the connection between their financial lives and the challenges and opportunities inherent in each life transition.

But, for informed physicians, life planning’s quasi-professional and informal approach to the largely isolate disciplines of financial planning and medical practice management is inadequate. Today’s practice environment is incredibly complex, as compressed economic stress from HMOs managed care, financial insecurity from insurance companies, ACOs and VBC, Washington DC and Wall Street; liability fears from attorneys, criminal scrutiny from government agencies, and IT mischief from malicious electronic medical record [eMR] hackers. And economic bench marking from hospital employers; lost confidence from patients; and the Patient Protection and Affordable Care Act [PP-ACA] more than a decade ago. All promote “burnout” and converge to inspire a robust new financial planning approach for physicians and most all medical professionals.

The iMBA Inc., approach to financial planning, as championed by the Certified Medical Planner™ professional certification designation program, integrates the traditional concepts of financial life planning, with the increasing complex business concepts of medical practice management. The former topics are presented in this textbook, the later in our recent companion text: The Business of Medical Practice [Transformational Health 2.0 Skills for Doctors].

***

***

For example, views of medical practice, personal lifestyle, investing and retirement, both what they are and how they may look in the future, are rapidly changing as the retail mentality of medicine is replaced with a wholesale and governmental philosophy. Or, how views on maximizing current practice income might be more profitably sacrificed for the potential of greater wealth upon eventual practice sale and disposition.

Or, how the ultimate fear represented by Yale University economist Robert J. Shiller, in The New Financial Order: Risk in the 21st Century, warns that the risk for choosing the wrong profession or specialty, might render physicians obsolete by technological changes, managed care systems or fiscally unsound demographics. OR, if a medical degree is even needed for future physicians?

Say, what medical license?

Dr. Shirley Svorny, chair of the economics department at California State University, Northridge, holds a PhD in economics from UCLA. She is an expert on the regulation of health care professionals who participated in health policy summits organized by Cato and the Texas Public Policy Foundation. She argues that medical licensure not only fails to protect patients from incompetent physicians, but, by raising barriers to entry, makes health care more expensive and less accessible. Institutional oversight and a sophisticated network of private accrediting and certification organizations, all motivated by the need to protect reputations and avoid legal liability, offer whatever consumer protections exist today.

Yet, the opportunity to revise the future at any age through personal re-engineering, exists for all of us, and allows a joint exploration of the meaning and purpose in life. To allow this deeper and more realistic approach, the informed transformation advisor and the doctor client, must build relationships based on trust, greater self-knowledge and true medical business management and personal financial planning acumen.

[A] The iMBA Philosophy

As you read this ME-P website, we hope you will embrace the opportunity to receive the focused and best thinking of some very smart people. Hopefully, along the way you will self-saturate with concrete information that proves valuable in your own medical practice and personal money journey. Maybe, you will even learn something that is so valuable and so powerful, that future reflection will reveal it to be of critical importance to your life. The contributing authors certainly hope so.

At the Institute of Medical Business Advisors, and thru the Certified Medical Planner™ program, we suggest that such an epiphany can be realized only if you have extraordinary clarity regarding your personal, economic and [financial advisory or medical] practice goals, your money, and your relationship with it. Money is, after only, no more or less than what we make of it.

Ultimately, your relationship with it, and to others, is the most important component of how well it will serve you.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on May 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP®

***

***

OVER HEARD IN THE FINANCIAl ADVISOR’S LOUNGE

A basic strategy for asset protection is to hold various assets in different entities. Putting real estate, small businesses, and other assets into trusts, corporations, or limited liability companies (LLCs) is effective protection that is relatively easy to put into practice. Not only do I recommend this strategy to clients, I use it myself. Recently, however, I discovered a potential downside.

About 25 years ago, I invested in some rare coins in a corporation I owned and put them into a safe deposit box owned by the corporation. When my business relocated 12 years ago, the safe deposit box billing was not forwarded to the new address and was never paid again. Last year I went to retrieve the coins from the safe deposit box, which I had not visited in 25 years. I discovered the box had been drilled open three years earlier and my collection turned over to the unclaimed property division of the State Treasurer’s office.

I was told getting the coins back would be simple enough. I just needed to verify that I owned the company which owned them by providing the corporation’s tax ID number. However, the corporation no longer existed. I didn’t have a record of its tax ID number. The IRS wouldn’t verify the number without my giving them the address the company had used. That address was a post office box number that I no longer used and couldn’t remember. The state’s position was “no tax ID, no coins.” The only verification of my identity as owner of the corporation was my signature on the bank’s safe deposit box application. Eventually, with the support of bank officers who were willing to swear that I was who I claimed to be, I got my coin collection back. The hassle involved in this process was a reminder of an important component of asset protection. Maintain accurate records so you don’t end up hiding assets from yourself.

***

***

A good start is to create a master file of all the entities that hold your assets. This can be any system that’s easy for you to use: a computer spreadsheet, a set of file folders, or a single paper list. Share it as appropriate with your CPA, attorney, or financial planner. The master list should include the name of each company, its date of incorporation, tax ID number, address, and other relevant information like phone or bank account numbers. Also keep an inventory of the assets each company owns.

Once you’ve created a master list, it’s essential to keep it up to date as you buy or sell assets, close companies, or transfer ownership. Set up a system, as well, to remind yourself of tasks like filing tax returns, completing minutes of annual meetings, and paying the annual safe deposit box rent. Make your record-keeping easier by eliminating unnecessary complications.

For example, you probably don’t need a separate address for each trust, corporation, or LLC. Instead of creating a separate company for each asset, you might consider grouping smaller assets within one entity. I’d suggest first discussing the pros and cons with an attorney or financial planner. For larger assets like real estate, I do recommend holding each one separately.

When I talk to clients about asset protection, I mention that part of the price we pay for it is an increase in paperwork. It’s easy to accept that idea with casual good intentions. The case of my reclaimed coin investment is a good reminder of the importance of keeping up with that paperwork. If we don’t, we might protect ourselves right out of access to our own assets.

Posted on May 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

Stock markets are coming off their worst week since April as President Trump’s tariff threats on Europe and Apple revived trade war jitters. The president has since delayed tariff threats on the EU, giving European stocks a boost yesterday, while Wall Street had the day off for Memorial Day.

No such relief appears to be coming for Apple, which has fallen 8% so far this month, and is the only Magnificent Seven member in the red for May, per FactSet.

Most individual physician portfolios are simply a list of stocks. Doctors with such lists usually know the cost of each position and when they acquired it. It is not unusual to find inherited low cost stocks in the account that have been held for many years.

When you inherit securities, a new cost basis is established (the price of the stock on the date of death or six months later—the executor of the estate makes this determination). Even though there would be no capital gain liability if the stock were sold immediately after date of death, most people simply don’t do anything, just hold the stock. Of course taxes should be considered when selling securities but the investment merit should be the overriding factor.

***

***

Doctor and Accountant Opinions

In a personal communication, Mr. L. Eddie Dutton, CPA said, “First make an investment decision and if it fits into the tax plan, so much the better. Doctors often wonder where they will get the money to pay the taxes. I say to get it from the sale of the appreciated stock and cry all the way to the bank with your profit.”

Dr. Ernest Duty MD, a very successful private investor advises “Ask yourself this question: If you had the money instead of the stock, would you buy the stock? If your answer is ‘Yes’ then, hold on to the stock but if you say ‘No, I wouldn’t buy that stock today’ then, sell it” [personal communication].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: E-MAILCONTACT: MarcinkoAdvisors@outlook.com

When New York-based Zocdoc was founded back in 2007, the idea was to help patients get off the phone, founder and CEO Oliver Kharraz told Healthcare Brew. The company created a website that helps patients find clinicians who fit their needs in their area and are under their insurance, and books appointments online.

But on May 1st, Zocdoc launched a new product to get people back on the phone: an artificial intelligence (AI) voice agent called Zo. Zo helps people book doctor appointments 24/7—but instead of speaking with a person, patients speak with an AI voice that is trained to meet their needs.

“Until recently, we didn’t do the phone because the experience on the phone was just so miserable,” Kharraz said. “Now you can actually have a consistent experience, where the AI can pick up after the first ring an unlimited number of times concurrently [and] have a natural conversation with you.”

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

I want to invest with a manager that has the skills to “hedge” a portfolio, but I do not wish to mix my money with other investors as in a hedge fund.

QUESTION:Can I hire hedge fund managers to manage my account separately?

Some hedge fund managers do take the time to recruit and manage separate accounts, with or without the help of referring brokers.

However, before long the administrative burden of managing so many separate accounts can become quite significant. Hence, the minimums for such separate accounts are generally much higher than if one were to invest in the manager’s hedge fund.

The best feature of these separate accounts is that potentially every aspect of the investment account, including fees, is negotiable. Other features include greater transparency and increased liquidity, since separately managed accounts can often be shut down on short notice.

Investors must be aware, however, that for practical purposes the portfolio manager generally will buy and sell the same securities in the separately managed accounts that the portfolio manager buys and sells in the hedge fund, yet the expenses incurred by the investor will likely be higher.

Posted on May 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Coinbase under investigation – Hit with ransom attack

Coinbase’s wild week got much wilder when the New York Times reported that the SEC has been looking into whether the crypto exchange misstated the size of its user base in securities filings. Per the New York Times, the investigation started under President Biden and has continued under President Trump.

The subject of the investigation appears to be Coinbase’s claim in past disclosures and marketing materials that it has 100 million “verified users.” A company spokesperson said it no longer reports that metric and the investigation should not continue.

The report came days after Coinbase joined the S&P 500, and just hours after it said it could lose $400 million following a recent hack by “rogue overseas” agents looking to steal customer data.

Financial Advisors and Financial Planners Usually Aren’t Millionaires

According to the most recent data from the Bureau of Labor Statistics (BLS), financial advisors had a median annual salary of $99,580 in 2023, which is significantly higher than the national average of $65,470. Of course, salaries of financial advisors can differ significantly by their location and level of expertise. The client’s profile may also have an impact on their compensation. But, many are not rich.

This is unfortunate. Financial advisors and Financial planners don’t rank among the millionaire professions in Thomas J. Stanley and William D. Danko’s book The Millionaire Next Door. Many work as salaried employees rather than entrepreneurs, lacking the scalable income potential of business owners who reinvest profits.

Stanley and Danko also stressed frugality, a challenge for advisors pressured to flaunt success—think luxury cars or upscale offices—making them “income-statement affluent” rather than “balance-sheet affluent.”

The truth is that a Financial Advisors’ success isn’t measured in client returns. Instead it is measured in their ability to gather assets and retain clients. In other words; Financial Advisors do not need to be good with money.

Financial Advisors need to be good with marketing, advertising, sales and people.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

My medical practice has a small self-directed pension plan with profit sharing features.

QUESTION: Can my medical practice’s retirement plan invest in a hedge fund?

Such a pension fund falls under a category called self-directed “plan” assets.

Among the rules are that each participant in the plan counts toward the 100 investor maximum under which most hedge funds operate, that each plan participant be a fully accredited investor, and that the hedge fund keep investments such as pension plans and other funds covered under ERISA to less than 25 percent of total assets under management.

Cognitive science is the interdisciplinary study of the mind and cognition. According to linguistics Professor Mackenzie H. Marcinko PhD, it combines various aspects from neuroscience, computer science, psychology, philosophy, linguistics, anthropology, and other fields, into a comprehensive study on the nature of intelligence.

Linguistics is the scientific study of language and its structure, including the study of morphology, syntax, phonetics, and semantics. Specific branches of linguistics include sociolinguistics, dialectology, psycholinguistics, computational linguistics, historical-comparative linguistics and applied linguistics.

Now, language and linguistics are closely related fields of study but they have distinct focuses.

Language refers to the system of communication used by humans, encompassing spoken, written, and signed forms. It is a means of expressing thoughts, ideas, and emotions.

On the other hand, linguistics is the scientific study of language itself. It examines the structure, sounds, meaning, and evolution of languages, as well as how they are acquired and used by individuals and communities.

While language is a broader concept that encompasses various forms of communication, linguistics delves into the intricate details and mechanics of language, aiming to understand its underlying principles and patterns.

Posted on May 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Oak Street Health, headquartered in Chicago and a wholly-owned subsidiary of CVS Health since 2023, has agreed to pay $60 million to resolve allegations that it violated the False Claims Act by paying kickbacks to third-party insurance agents in exchange for recruiting seniors to Oak Street Health’s primary care clinics.

The Anti-Kickback Statute prohibits anyone from offering or paying, directly or indirectly, any remuneration — which includes money or any other thing of value — to induce referrals of patients or to provide recommendations of items or services covered by Medicare, Medicaid and other federally funded programs. Under the Medicare Advantage (MA) Program, also known as Part C, Medicare beneficiaries have the option to obtain their health care through privately-operated insurance plans known as MA plans. Some MA Plans contract with health care providers, including Oak Street Health, to provide their plan members with primary care services.

The United States alleged that, in 2020, Oak Street Health developed a program to increase patient membership called the Client Awareness Program. Under the Program, third-party insurance agents contacted seniors eligible for or enrolled in Medicare Advantage and delivered marketing messages designed to generate interest in Oak Street Health. Agents then referred interested seniors to an Oak Street Health employee via a three-way phone call, otherwise known as a “warm transfer,” and/or an electronic submission.

In exchange, Oak Street Health paid agents typically $200 per beneficiary referred or recommended. These payments incentivized agents to base their referrals and recommendations on the financial motivations of Oak Street Health rather than the best interests of seniors. The settlement resolves allegations that, from September 2020 through December 2022, Oak Street Health knowingly submitted, and caused the submission of, false claims to Medicare arising from kickbacks to agents that violated the Anti-Kickback Statute.

Posted on May 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

I’ve received emails from readers asking my thoughts on DeepSeek. I need to start with two warnings. First, the usual one: I’m a generalist value investor, not a technology specialist (last week I was analyzing a bank and an oil company), so my knowledge of AI models is superficial. Second, and more unusually, we don’t have all the facts yet.

But this story could represent a major step change in both AI and geopolitics.

Here’s what we know:

DeepSeek—a year-old startup in China that spun out of a hedge fund—has built a fully functioning large language model (LLM) that performs on par with the latest AI models. This part of the story has been verified by the industry: DeepSeek has been tested and compared to other top LLMs. I’ve personally been playing with DeepSeek over the last few days, and the results it spit out were very similar to those produced by ChatGPT and Perplexity—only faster.

This alone is impressive, especially considering that just six months ago, Eric Schmidt (former Google CEO, and certainly no generalist) suggested China was two to three years behind the U.S. in AI.

But here’s the truly shocking—and unverified—part: DeepSeek claims they trained their model for only $5.6 million, while U.S. counterparts have reportedly spent hundreds of millions or even billions of dollars. That’s 20 to 200 times less.

The implications, if true, are stunning. Despite the U.S. government’s export controls on AI chips to China, DeepSeek allegedly trained its LLM on older-generation chips, using a small fraction of the computing power and electricity that its Western competitors have. While everyone assumed that AI’s future lay in faster, better chips—where the only real choice is Nvidia or Nvidia—this previously unknown company has achieved near parity with its American counterparts swimming in cash and datacenters full of the latest Nvidia chips. DeepSeek (allegedly) had huge compute constraints and thus had to use different logic, becoming more efficient with subpar hardware to achieve a similar result.

In other words, this scrappy startup, in its quest to create a better AI “brain,” used brains where everyone else was focusing on brawn—it literally taught AI how to reason.

Posted on May 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

I am back from what has become over the past two decades an annual pilgrimage to Omaha.

What’s fascinating about this trip is that it has everything and nothing to do with Warren Buffett. The main event that draws everyone to Omaha – the Berkshire Hathaway (BRK) annual meeting – is actually the least important part. I could have watched the shareholder meeting livestreamed on YouTube from the comfort of my living room couch.

The emergence of the Berkshire phenomenon reminds me of China’s manufacturing evolution. China initially attracted capital because of its cheap labor. But over time, China took this capital and plowed it into infrastructure. Factories were built next to each other, each specializing in certain areas. A specialized ecosystem emerged.

Today, Chinese labor is no longer cheap. It’s been replaced by automation, and now China is a powerhouse for manufacturing anything and everything.

The transformation that the BRK weekend has undergone followed a similar progression. Initially, the only way to absorb Buffett and Munger’s wisdom was to come to Omaha, as the event was not streamed. But then something interesting happened. The BRK weekend attracted people who shared the same value system, and friendships were formed. A variety of smaller events began to be scheduled throughout the same weekend across Omaha, and an equally specialized ecosystem emerged.

The shareholder meeting began to be streamed about ten years ago, but that has had no impact on attendance. This is one reason why I think Buffett is at peace with the idea of no longer presiding at the meeting – people will still come to Omaha the weekend before Mother’s Day. The BRK weekend now features dozens of excellent events.

I spoke at several, including an investing panel at Creighton University, alongside the wonderful Bob Robotti, a die-hard value investor who runs Robotti & Co. I’ve known Bob for years – at 72, he exhibits the same enthusiasm for stocks as someone decades younger – and this panel was an excellent example of what the BRK Omaha ecosystem has produced.

Bob and I have very different approaches to value investing. He loves cyclical businesses, while I generally shun them. Bob mentioned that he’d buy a very cheap business run by a mediocre manager, while I would not touch it with a ten-foot pole.

There is absolutely nothing wrong with either approach; indeed, there is an important lesson in it. Your investment philosophy and process have to fit your personality and your EQ. In my case, I get nervous (and thus irrational) when I own companies run by imbeciles who don’t have either skin or soul in the game. But the great thing about the BRK weekend is that I learn from Bob every time I spend time with him. He’s a thoughtful and genuinely kind human being.

From the outside, the BRK weekend may seem like a place where people simply want to learn how to get and stay rich. But this gathering transcends value investing and capitalism and genuinely celebrates human values. People (like me) bring their kids to this event. And just like at the main event, at the Q&A breakfast I hosted for my readers, many questions centered on life rather than investing.

My first Omaha reader meetup fit around a small restaurant table. This year, to my surprise, 450 people packed into a venue with standing-room only. I answered questions on every imaginable topic for just over two hours, and by the end I was exhausted.

This gave me even greater admiration for Buffett, who is four decades my senior, yet still fielded questions for four solid hours. I was delighted to hear Warren give a similar answer to one I had given the day before when asked what advice he’d give to graduating students: “Don’t worry too much about starting salaries and be very careful who you work for because you will take on the habits of the people around you.”

(Incidentally, we are going to host our next Q&A Breakfast on May 1, 2026. You can sign up for it here. It’s free, but I suggest you sign up early, as it fills up fast.)

I also participated (as I have for over a decade) in an investing panel at YPO (Young President Organization) in the beautiful Holland Performance Art Center with Tom Gaynor, CEO of Markel (often described as a baby Berkshire Hathaway) and Lawrence Cunningham. Lawrence authored perhaps the most important book about Buffett, The Essays of Warren Buffett, masterfully editing Warren’s annual letters into a cohesive volume. This year’s panel was one of those occasions where I found myself listening intently to my fellow panelists instead of speaking more.

Lawrence has met Greg Abel – Buffett’s designated successor – and feels optimistic about him. He’s probably right – this was one of Buffett’s most crucial decisions, which he did not make lightly. Yet I can’t imagine sitting for four hours listening to Greg Abel. I am sure he is a brilliant CEO, but he’s neither Buffett nor Munger – few individuals possess so much worldly wisdom and communicate it with such clarity and humor.

This brings me to the point of this note: the dramatic (yet not unexpected) announcement that Buffett is stepping down as CEO of BRK at the end of the year.

Before I comment on this, let me tell you a story. Imagine you have been watching a soap opera for 17 years. You arrive dutifully every year to watch every episode in person. And then you miss the last five minutes of the explosive finale before it goes off the air. This is what happened to me when Buffett announced his retirement as CEO.

A few minutes before noon, while Buffett was answering a question I’d heard before and appeared to be winding down, I suggested we slip out early for lunch to avoid the crowds. When we came back, I discovered that the meeting had gone on until 1 pm, and just before it ended, Buffett announced that he would step down at the end of the year. Seventeen years of watching Warren speak and I missed the most dramatic moment of all, followed by a five-minute standing ovation.

I think Buffett has engineered his exit brilliantly. He will still remain chairman, and even before the announcement he was not managing BRK’s day-to-day operations. As a collection of hundreds of companies that often have absolutely nothing in common with each other, BRK is already highly decentralized. Buffett’s main contribution has been capital allocation.

Giving up the CEO title while he’s still alive means Buffett has brought in his replacement in an orderly way and created a smooth transition. But I have a feeling that on January 1, 2026, when Greg Abel officially becomes CEO, nothing will really change, and Warren will continue doing what he’s been doing for as long as he can. If Buffett is able – he’ll be 95 – he’ll still drive to the office and stop by McDonald’s for a breakfast sandwich (there’s a lot of wisdom in finding pleasure in little things). His son Howard Buffett will become chairman after Warren, with his only job being to preserve the culture. I’ve been asked what I think of BRK stock. We bought the stock during the pandemic. It has done better than I expected, in part because of the strong performance of Apple, which was BRK’s largest holding. But BRK today is an unexciting investment at its current price. In all honesty, it is a conglomerate with some good and some merely okay businesses.

As a consumer, I get a (small) glimpse into how BRK businesses are being run by visiting Dairy Queen. BRK owns DQ, and I love their soft-serve ice cream (though I only eat it when I travel). My favorite part of research!

DQ has (or maybe had) a strong brand and operates on a capital-light model as a franchisor. But most stores I have visited looked like they have been neglected and need fresh paint. To be sure, I understand the limitations of this “analysis,” and DQ overall amounts to a rounding error on BRK’s financials. But little things often reveal much about big things.

BRK’s big businesses, from what I can glean through their financials, are not particularly well managed – GEICO and BNSF (railroad) have definitely been undermanaged lately. BNSF is not nearly as efficient as its competitors that embraced precision railroading, and until recently GEICO was losing market share to Progressive.

BRK’s reinsurance business, a significant source of BRK’s profitability, is run by the extraordinary Ajit Jain. Ajit is in his 70s and unfortunately it seems he is not in great health. Is his replacement going to shoot the lights out, like he did? We don’t know. But Ajit is probably more important to BRK today than Buffett.