BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

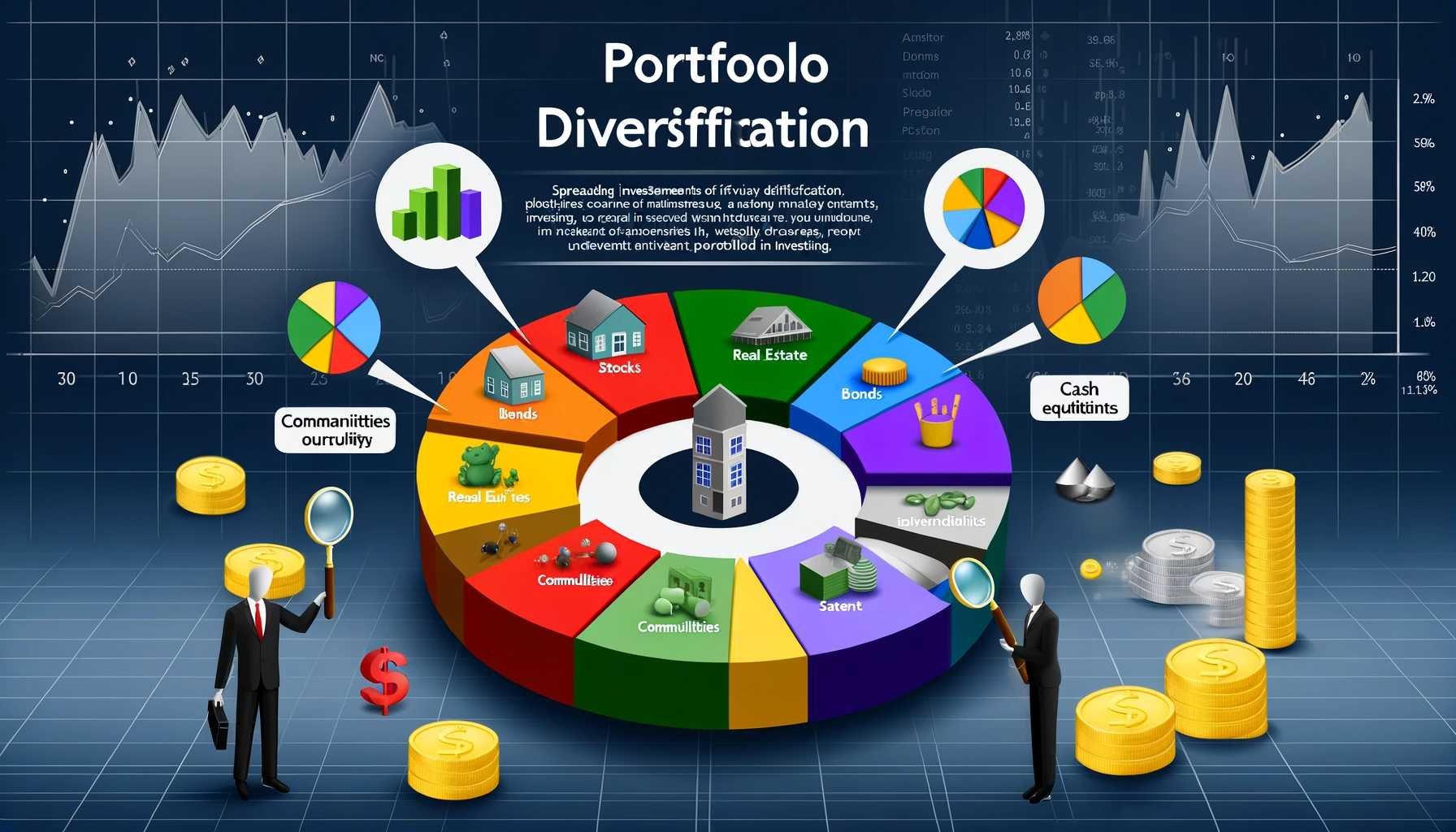

In the world of financial advising, few principles are as foundational—and as misunderstood—as diversification. Clients often come to advisors hoping for bold moves and big wins. Yet the most prudent strategy we offer is not a thrilling stock pick or a market-timing miracle, but a quiet, calculated spread of risk. Diversification, in essence, is the art of saying “sorry” in advance—for not chasing every hot trend, for not going all-in, and for not promising perfection. But it’s also the strategy that earns trust, builds resilience, and delivers long-term value.

Diversification means allocating assets across different sectors, geographies, and investment vehicles to reduce exposure to any single point of failure. For financial advisors, it’s not just a portfolio tactic—it’s a philosophy of humility. It acknowledges that markets are unpredictable, that no one can consistently forecast winners, and that protecting capital is just as important as growing it.

Clients may initially resist this approach. They might question why their portfolio includes lagging sectors or why we’re not doubling down on tech or crypto. This is where our role as educators becomes critical. We explain that diversification isn’t about avoiding risk—it’s about managing it. It’s the reason why, when tech stumbles, healthcare or consumer staples might hold steady. It’s why international exposure can buffer domestic volatility. And it’s why fixed income still matters, even in a rising-rate environment.

The challenge for advisors is that diversification rarely feels heroic. It doesn’t make headlines. It doesn’t deliver overnight gains. Instead, it delivers consistency. It smooths out the ride. It allows clients to sleep at night. And over time, it compounds into something powerful: confidence.

***

***

One of the most effective ways to communicate this is through behavioral coaching. We remind clients that diversification is designed to protect them from their own impulses—from chasing trends, reacting to headlines, or panicking during downturns. It’s a guardrail against emotional investing. And when markets inevitably wobble, diversified portfolios give us the credibility to say, “This is why we planned ahead.”

Moreover, diversification is a relationship tool. It shows clients that we’re not betting their future on a single idea. We’re building something durable. We’re thinking about their retirement, their children’s education, their legacy. And we’re doing it with a strategy that’s built to last.

In short, diversification may feel like an apology to the thrill-seeker in every investor. But it’s also a promise: that we’re here to protect, to guide, and to deliver results that matter—not just today, but for decades to come.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Why It Is Difficult to Be a Part-Time Financial Planner Today

In theory, part-time financial planning offers flexibility and work-life balance, making it an attractive option for professionals seeking reduced hours. However, in practice, the role of a financial planner has evolved into a demanding, full-time commitment. The complexity of financial markets, client expectations, regulatory requirements, and technological advancements make part-time financial planning increasingly difficult to sustain.

One of the primary challenges is client relationship management. Financial planning is deeply personal and trust-based. Clients expect consistent communication, timely updates, and proactive advice. A part-time planner may struggle to maintain the same level of responsiveness as full-time counterparts, especially during volatile market conditions or life-changing events like retirement, divorce, or inheritance. Delayed responses or limited availability can erode client confidence and damage long-term relationships.

***

***

Another obstacle is the rapid pace of financial change. Tax laws, investment products, insurance regulations, and retirement planning strategies are constantly evolving. Staying current requires ongoing education, certifications, and industry engagement. For part-time planners, keeping up with these changes while managing clients and administrative tasks can be overwhelming. Falling behind risks offering outdated or suboptimal advice, which could lead to compliance issues or client dissatisfaction.

Regulatory compliance adds another layer of complexity. Financial planners must adhere to strict standards set by organizations like FINRA, the SEC, and state regulators. These include documentation, disclosures, fiduciary responsibilities, and continuing education. Compliance is non-negotiable and time-consuming, regardless of hours worked. Part-time planners face the same scrutiny and liability as full-time professionals, but with fewer hours to manage the workload.

Technology, while a powerful tool, also presents challenges. Clients increasingly expect digital access to their portfolios, real-time updates, and virtual meetings. Managing these platforms requires technical proficiency and regular maintenance. Part-time planners may find it difficult to keep systems updated, troubleshoot issues, or provide tech support, especially if they lack dedicated staff.

Business development is another hurdle. Building and maintaining a client base requires networking, marketing, and referrals. Part-time planners often have limited time to attend events, follow up with leads, or cultivate relationships. This can hinder growth and make it difficult to compete with full-time advisors who are more visible and accessible.

Finally, there’s the issue of income and scalability. Many financial planners earn through commissions, assets under management (AUM), or fee-based models. Part-time work often means fewer clients and lower revenue, which can make it hard to justify the costs of licensing, insurance, software, and office space. Without scale, profitability becomes a challenge.

In conclusion, while the idea of part-time financial planning may seem appealing, the realities of the profession make it difficult to execute effectively. The demands of client care, compliance, education, and business development require consistent attention and availability. Unless the industry adapts to support flexible models, part-time financial planners will continue to face significant barriers to success.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Investment fees still matter for physicians and all of us, despite dropping dramatically over the past several decades due to computer automation, algorithms and artificial intelligence, etc. And, they can make a big difference to your financial health. So, before buying any investment thru a financial advisor, planner, manager, stock broker, etc., it’s vital to understand these two often confusing costs.

***

***

Fee Only: Paid directly by clients for their services and can’t receive other sources of compensation, such as payments from fund providers. Act as a fiduciary, meaning they are obligated to put their clients’ interests first

Fee Based: Paid by clients but also via other sources, such as commissions from financial products that clients purchase. Brokers and dealers (registered representatives) are simply required to sell products that are “suitable” for their clients. Not a fiduciary.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

In the early 1980s, Daniel Kahneman and Amos Tverskey proved in numerous experiments that the reality of decision making differed greatly from the assumptions held by economists. They published their findings in Prospect Theory: An analysis of decision making under risk, which quickly became one of the most cited papers in all of economics.

To understand the importance of their breakthrough, we first need to take a step back and explain a few things. Up until that point, economists were working under a normative model of decision making. A normative model is a prescriptive approach that concerns itself with how people should make optimal decisions. Basically, if everyone was rational, this is how they should act.

Amanda, an RN client, was just informed by her financial advisor that she needed to re-launch her 403-b retirement plan. Since she was leery about investing, she quietly wondered why she couldn’t DIY. Little does her Financial Advisor know that she doesn’t intend to follow his advice, anyway! So, what went wrong?

The answer may be that her advisor didn’t deploy a behavioral economics framework to support her decision-making. One such framework is the “prospect theory” model that boils client decision-making into a “three step heuristic.”

According to colleague Eugene Schmuckler PhD MBA MEd CTS, Prospect theory makes the unspoken biases that we all have more explicit. By identifying all the background assumptions and preferences that clients [patients] bring to the office, decision-making can be crafted so that everyone [family, doctor and patient] or [FA, client and spouse] is on the same page.

1. Simplify choices by focusing on the key differences between investment [treatment] options such as stock, bonds, cash, and index funds.

2. Understanding that clients [patients] prefer greater certainty when it comes to pursuing financial [health] gains and are willing to accept uncertainty when trying to avoid a loss [illness].

3. Cognitive processes lead clients and patients to overestimate the value of their choices thanks to survivor bias, cognitive dissonance, appeals to authority and hindsight biases.

CITE: Jaan E. Sidorov MD [Harrisburg, PA]

Assessment

Much like in healthcare today, the current mass-customized approaches to the financial services industry fall short of recognizing more personalized advisory approaches like prospect theory and assisted client-centered investment decision-making.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

FIVE INVESTING MISTAKES OF DOCTORS; PLUS 1 VITAL TIP

As a former US Securities and Exchange Commission [SEC] Registered Investment Advisor [RIA] and business school professor of economics and finance, I’ve seen many mistakes that doctors must be aware of, and most importantly, avoid. So, here are the top 5 investing mistakes along with suggested guideline solutions.

Mistake 1: Failing to Diversify Investment but Beware Di-Worsification

A single investment may become a large portion of your portfolio as a result of solid returns lulling you into a false sense of security. The Magnificent Seven stocks are a current example:

Apple, up +5,064%% since 1/18/2008

Amazon, up +30,328% since 9/6/2002

Alphabet, up +1,200% since 7/20/2012

Tesla, up +21,713% since 11/16/2012

Meta, up +684% since 2/20/2015

Microsoft, up +22% since 12/21/2023

Nvidia, up +80,797% since 4/15/2005

Guideline: The Magnificent Seven [7] has grown from 9% of the S&P 500 at the end of 2013 to 31% at the end of 2024! That means even if you don’t own them, you’re still very exposed if you have an Index Fund [IF] or Exchange Traded Fund [ETF] that tracks the market. Accordingly, diversification is the only free lunch in investing which can reduce portfolio risk. But, remember the Wall Street insider aphorism that states: “Di-Versification Means Always Having to Say Your Sorry.”

The term “Di-Worsification” was coined by legendary investor Peter Lynch in his book, One Up On Wall Street to refer to over-diversifying an investment portfolio in such a way that it reduces your overall risk-return characteristics. In other words, the potential return rises with an increase in risk and invested money can render higher profits only if willing to accept a higher possibility of losses [1].

A podiatrist can easily fall into the trap of chasing securities or mutual funds showing the highest return. It is almost an article of faith that they should only purchase mutual funds sporting the best recent performance. But in fact, it may actually pay to shun mutual funds with strong recent performance. Unfortunately, many struggle to appreciate the benefits of their investment strategy because in jaunty markets, people tend to run after strong performance and purchase last year’s winners.

Similarly, in a market downturn, investors tend to move to lower-risk investment options, which can lead to missed opportunities during subsequent market recoveries. The extent of underperformance by individual investors has often been the most awful during bear markets. Academic studies have consistently shown that the returns achieved by the typical stock or bond fund investors have lagged substantially.

Guideline: Understand chasing performance does not work.Continually monitor your investments and don’t feel the need to invest in the hottest fund or asset category. In fact, it is much better to increase investments in poor performing categories (i.e. buy low). Also keep in remind rebalancing of assets each year is key. If stocks perform poorly and bonds do exceptionally well, then rebalance at the end of the year. In following this strategy, this will force a doctor into buying low and selling high each year.

Often doctors make their investment decisions under the belief that stocks will consistently give them solid double-digit returns. But the stock markets go through extended long-term cycles.

In examining stock market history, there have been 6 secular bull markets (market goes up for an extended period) and 5 secular bear markets (market goes down) since 1900. There have been five distinct secular bull markets in the past 100+ years. Each bull market lasted for an extended period and rewarded investors.

For example, if an investor had started investing in stocks either at the top of the markets in 1966 or 2000, future stock market returns would have been exceptionally below average for the proceeding decade. On the other hand, those investors fortunate enough to start building wealth in 1982 would have enjoyed a near two-decade period of well above average stock market returns. They key element to remember is that future historical returns in stocks are not guaranteed. If stock market returns are poor, one must consider that he or she will have to accept lower projected returns and ultimately save more money to make up for the shortfall. For example,

The May 6th, 2010, flash crash, also known as the crash of 2:45, was a United States trillion-dollar stock market plunge which started at 2:32 pm EST and lasted for approximately 36 minutes.

And, investors who have embraced the “buy the dip” strategy in 2025 have been handsomely rewarded, with the S&P 500 delivering its strongest post-pull back returns in over three decades.

According to research from Bespoke Investment Group, the S&P 500 has gained an average of 0.36% in the trading session following a down day so far in 2025. The only year with a comparable performance was 2020, which saw a 0.32% average post-dip gain [2].

The most recent example came on May 27, 2025 when the S&P 500 surged more than 2% after falling 0.7% in the final session before the holiday weekend. The rally was sparked by President Trump’s decision to scale back huge previously threatened tariffs on EU —a recurring catalyst behind many of 2025’s rebound.

Guideline: Beware of projecting forward historical returns. Doctors should realize that the stock markets are inherently volatile and that, while it is easy to rely on past historical averages, there are long periods of time where returns and risk deviate meaningfully from historical averages.

Some doctors believe they are “smarter than the market” and can time when to jump in and buy stocks or sell everything and go to cash. Wouldn’t it be nice to have the clairvoyance to be out of stocks on the market’s worst days and in on the best days?

Using the S&P 500 Index, our agile imaginary doctor-investor managed to steer clear of the worst market day each year from January 1st, 1992 to March 31st, 2012. The outcome: s/he compiled a 12.42% annualized return (including reinvestment of dividends and capital gains) during the 20+ years, sufficient to compound a $10,000 investment into $107,100.

But what about another unfortunate doctor-investor that had the mistiming to be out of the market on the best day of each year. This ill-fated investor’s portfolio returned only 4.31% annualized from January 1992 – March 2012, increasing the $10,000 portfolio value to just $23,500 during the 20 years. The design of timing markets may sound easy, but for most all investors it is a losing strategy.

More contemporaneously on December 18th 2024, the DJIA plummeted 2.5%, while the S&P 500 declined 3% and the NASDAQ tumbled 3.5%

Guideline: If it looks too good to be true, it probably is. While jumping into the market at its low and selling right at the high is appealing in theory, we should recognize the difficulties and potential opportunity and trading costs associated with trying to time the stock market in practice. In general, colleagues are be best served by matching their investment with their time horizon and looking past the peaks / valleys along the way.

Mistake 5: Failing to Recognize the Impact of Fees and Expenses

A free dinner seminar or a polished stock-broker sales pitch may hide the total underlying costs of an investment. So, fees absolutely matter.

The first costing step is determining what the fees actually are. In a mutual fund, these costs are found in the company’s obligatory “Fund Facts”. This manuscript clearly outlines all the fees paid–including up front fees (commissions and loads), deferred sales charges and any switching fees. Fund management expense ratios are also part of the overall cost. Trading costs within the fund can also impact performance.

Here is a list of the traditional mutual fund fees:

Front End Load: The commission charged to purchase a fund through a stock broker or financial advisor. The commission reduces the amount you have available to invest. Thus, if you start with $100,000 to invest, and the advisor charges up to an 8 percent front end load, you end up actually investing $92,000.

Deferred Sales Charge (DSC) or Back End Load: Imposed if you sell your position in the mutual fund within a pre-specified period of time (normally one – five years). It is initiated at a higher start percentage (i.e. as high as 10 percent) and declines over a specific period of time.

Operating Fees: Costs of the mutual fund including the management fee rewarded to the manager for investment services. It also includes legal, custodial, auditing and marketing fees.

Annual Administration Fee: Many mutual fund companies also charge a fee just for administering the account – usually under $100-150 per year.

Guideline: Know and understand all fees.

For example: A 1 percent disparity in fees may not seem like much but it makes a considerable impact over a long time period.

Consider a $100,000 portfolio that earns 8 percent before fees, grows to $320,714 after 20 years if the investor pays a 2 percent operating fee. In comparison, if s/he opted for a fund that charged a more reasonable 1 percent fee, after 20 years, the portfolio grows to be $386,968 – a divergence of over $66,000!

This is the value of passive or index investing. In the case of an index fund, fees are generally under 0.5 percent, thus offering even more savings over a long period of time.

One Vital Tip: Investing Time is on Your Side

Despite thousands of TV shows, podcasts, textbooks, opinions and university studies on investing, it really only has three simple components. Amount invested, rate of return and time. By far, the most important item is time! For example:

Nvidia: if you invested $1,000 in 2009, you’d have $338,103 today.

Apple: if you invested $1,000 in 2008, you’d have $48,005 today.

Netflix: if you invested $1,000 in 2004, you’d have $495,679 today.

Unfortunately, this list of investing mistakes is still being made by many doctors. Fortunately, by recognizing and acting to mitigate them, your results may be more financially fruitful and mentally quieting.

REFERENCES:

1. Lynch, Peter: One Up on Wall Street [How to Use What You Already Know to Make Money in the Market]: Simon and Shuster (2nd edition) New York, 2000.

1. Marcinko, DE; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

2. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York, 2006.

3. Marcinko, DE; Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] CRC Press, New York, 2015.

BIO: As a former university Professor and Endowed Department Chair in Austrian Economics, Finance and Entrepreneurship, the author was a NYSE Registered Investment Advisor and Certified Financial Planner for a decade. Later, he was a private equity and wealth manager

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on May 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP®

***

***

OVER HEARD IN THE FINANCIAl ADVISOR’S LOUNGE

A basic strategy for asset protection is to hold various assets in different entities. Putting real estate, small businesses, and other assets into trusts, corporations, or limited liability companies (LLCs) is effective protection that is relatively easy to put into practice. Not only do I recommend this strategy to clients, I use it myself. Recently, however, I discovered a potential downside.

About 25 years ago, I invested in some rare coins in a corporation I owned and put them into a safe deposit box owned by the corporation. When my business relocated 12 years ago, the safe deposit box billing was not forwarded to the new address and was never paid again. Last year I went to retrieve the coins from the safe deposit box, which I had not visited in 25 years. I discovered the box had been drilled open three years earlier and my collection turned over to the unclaimed property division of the State Treasurer’s office.

I was told getting the coins back would be simple enough. I just needed to verify that I owned the company which owned them by providing the corporation’s tax ID number. However, the corporation no longer existed. I didn’t have a record of its tax ID number. The IRS wouldn’t verify the number without my giving them the address the company had used. That address was a post office box number that I no longer used and couldn’t remember. The state’s position was “no tax ID, no coins.” The only verification of my identity as owner of the corporation was my signature on the bank’s safe deposit box application. Eventually, with the support of bank officers who were willing to swear that I was who I claimed to be, I got my coin collection back. The hassle involved in this process was a reminder of an important component of asset protection. Maintain accurate records so you don’t end up hiding assets from yourself.

***

***

A good start is to create a master file of all the entities that hold your assets. This can be any system that’s easy for you to use: a computer spreadsheet, a set of file folders, or a single paper list. Share it as appropriate with your CPA, attorney, or financial planner. The master list should include the name of each company, its date of incorporation, tax ID number, address, and other relevant information like phone or bank account numbers. Also keep an inventory of the assets each company owns.

Once you’ve created a master list, it’s essential to keep it up to date as you buy or sell assets, close companies, or transfer ownership. Set up a system, as well, to remind yourself of tasks like filing tax returns, completing minutes of annual meetings, and paying the annual safe deposit box rent. Make your record-keeping easier by eliminating unnecessary complications.

For example, you probably don’t need a separate address for each trust, corporation, or LLC. Instead of creating a separate company for each asset, you might consider grouping smaller assets within one entity. I’d suggest first discussing the pros and cons with an attorney or financial planner. For larger assets like real estate, I do recommend holding each one separately.

When I talk to clients about asset protection, I mention that part of the price we pay for it is an increase in paperwork. It’s easy to accept that idea with casual good intentions. The case of my reclaimed coin investment is a good reminder of the importance of keeping up with that paperwork. If we don’t, we might protect ourselves right out of access to our own assets.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

I want to invest with a manager that has the skills to “hedge” a portfolio, but I do not wish to mix my money with other investors as in a hedge fund.

QUESTION:Can I hire hedge fund managers to manage my account separately?

Some hedge fund managers do take the time to recruit and manage separate accounts, with or without the help of referring brokers.

However, before long the administrative burden of managing so many separate accounts can become quite significant. Hence, the minimums for such separate accounts are generally much higher than if one were to invest in the manager’s hedge fund.

The best feature of these separate accounts is that potentially every aspect of the investment account, including fees, is negotiable. Other features include greater transparency and increased liquidity, since separately managed accounts can often be shut down on short notice.

Investors must be aware, however, that for practical purposes the portfolio manager generally will buy and sell the same securities in the separately managed accounts that the portfolio manager buys and sells in the hedge fund, yet the expenses incurred by the investor will likely be higher.

Financial Advisor, Planner and Insurance Agent Information

By Staff Reporters

***

***

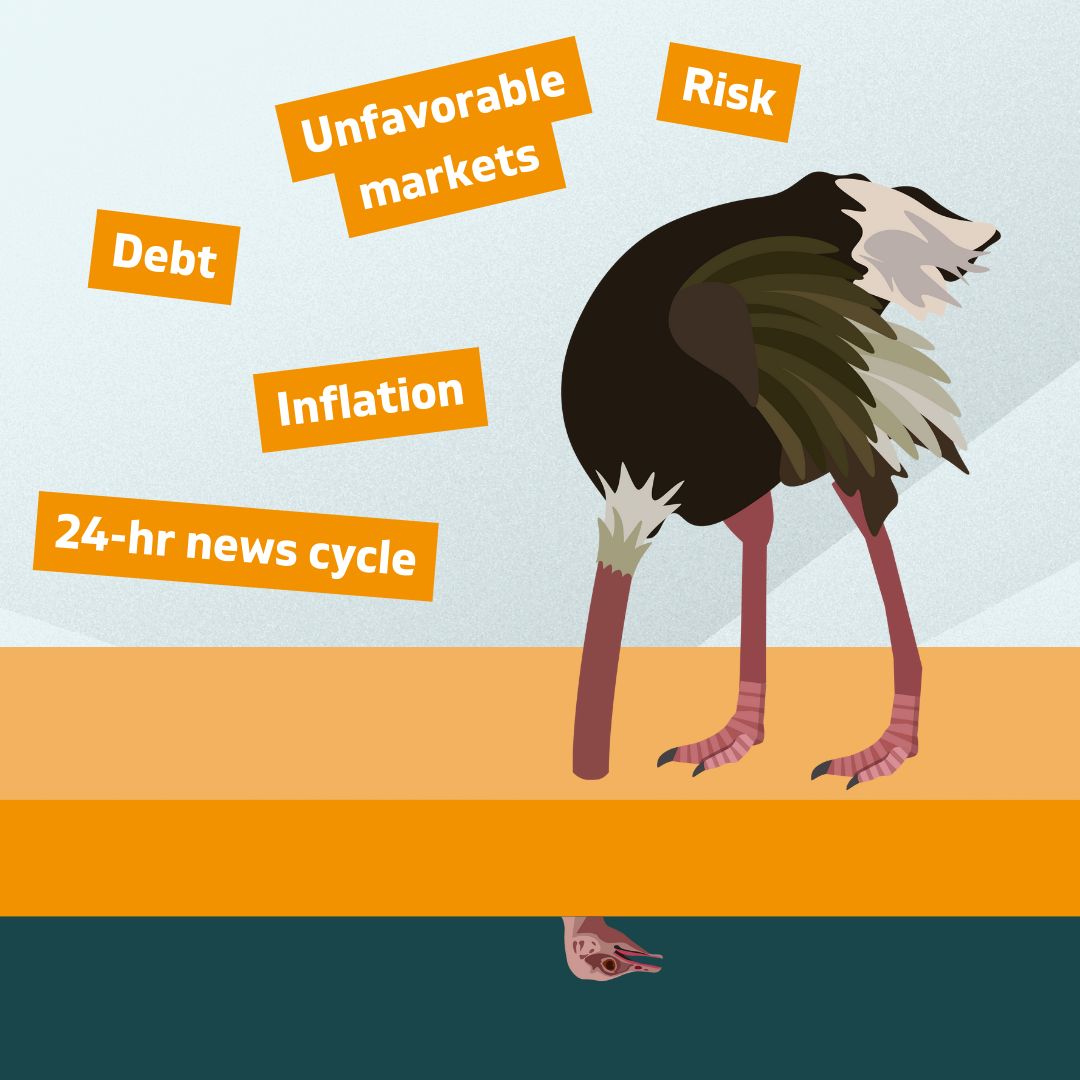

Ostrich Bias is a behavioral phenomenon describing the tendency of individuals to avoid or ignore information that they perceive as negative or threatening. This term is derived from the popular but inaccurate belief that ostriches bury their heads in the sand when faced with danger, even though they do not exhibit such behavior.

Evidence: There is neuro-scientific evidence of the ostrich effect. Sharot et al. (2012) investigated the differences in positive and negative information when updating existing beliefs. Consistent with the ostrich effect, participants presented with negative information were more likely to avoid updating their beliefs; wills, estate plans, investment portfolios, and insurance policies, etc..

Moreover, they found that the part of the brain responsible for this cognitive bias was the left IFG – inferior frontal gyrus – by disrupting this part of the brain with TMS – transcranial magnetic stimulation – participants were more likely to accept the negative information provided.

EXAMPLE: The Ostrich Bias can cause someone to avoid looking at their bills, because they’re worried about seeing how far behind they are on home mortgage payments, credit cards, education or auto loans, etc.

COMMENTS APPRECIATED

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on April 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHA CPHQ CMP™

***

***

Finally … Fiduciary second investing and financial planning opinions right here!

Telephonic or electronic advice for medical professionals that is:

Objective, affordable, medically focused and financially personalized

Rendered by a pre-screened financial consultant for doctors and medical professionals

Offered on a pay-as-you-go basis, by phone or secure e-mail transmission

The iMBA Discussion Forum™ is a physician-to-financial advisor telephone or e-mail portal that connects independent financial professionals to doctors, nurses or healthcare executives desiring affordable and unbiased financial planning advice.

Medical professionals and healthcare executives can now receive direct access to pre-screened iMBA professionals in the areas of Investing, Financial Planning, Asset Allocation, Portfolio Management, Insurance, Mortgage and Lending, Human Resources, Retirement Planning and Employee Benefits. To assist our medical professional and healthcare executive members, we can be contracted with per-minute or per-project fees, and contacted by client phone, email or secure instant messaging.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on March 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

ByJ. Chris Miller JD

***

***

Your personal and financial life is constantly changing. Significant changes always necessitate the need to review your life. However, a few key events trigger the need to review your estate plan. If any of the events below have occurred since you reviewed your estate plan, see a competent adviser to help you achieve your goals.

Birth of a child or grandchild.

Death of a spouse, beneficiary, guardian, trustee or personal representative.

Marriage of you or your children.

Divorce. (Review beneficiary designations and asset titling)

Move out of state. An estate is settled under the laws of the state in which the decedent resided. Certain provisions of a will that are valid in one state may not be in another.

Change in estate value. A large increase or decrease in the size of an estate may greatly affect some of the strategies that were implemented.

Changes in business. Starting, buying or selling a medical practice or other business has an impact on your estate. The addition or death of a business owner will cause a review.

Tax law changes. EGTRRA has dramatically changed the way we plan for estate taxes. It is important to note that only planning for estate taxes has been effected. Estate planning involves much more than just the motivation to reduce or eliminate taxes. Assuring that your family is financially taken care of, that children have the opportunity to go to college, that your debts are paid, that charitable desires are achieved, provisions for a needy child, proper selection of a guardian, the list goes on. Please do not use the new law as an excuse to not plan your estate.

***

OVERHEARD IN THE FINANCIAL ADVISOR’S LOUNGE

From my perspective, estate planning is a team sport, and lawyers rely on financial advisers all the time to spot issues for clients. We do not share the opinion that non-lawyers are incapable of giving good advice.

The desire for security and feelings of insecurity are the same thing.

The idea of security, financial or otherwise, is an illusion; human life is inherently insecure. But, this doesn’t mean we shouldn’t be prudent with risk and diligent financial planning with strategies like saving and investing.

However, according to colleague Eugene Schmuckler PhD, MBA,MEd seeking security is like many things; the more you try to grasp and obsess about financial security, the more quickly you will reach a point of diminishing returns. You will feel increasingly less secure at a certain point.

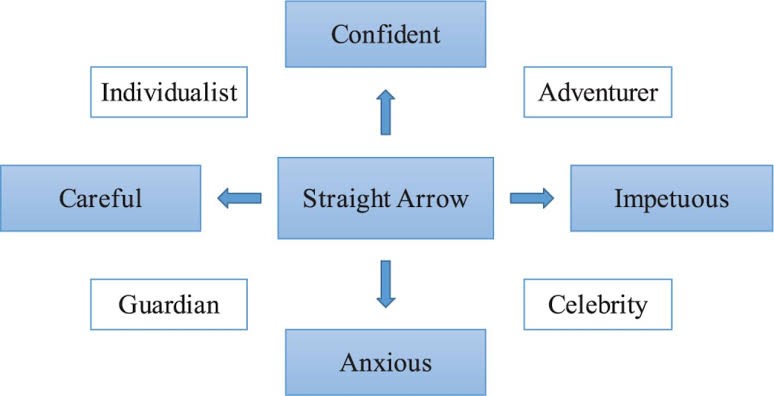

Fund managers Tom Bailard, Larry Biehl and Ron Kaiser identified five types of investors, each type characterized by their investment preferences and actions. These 5 types are: Individualists, Adventurers, Celebrities, Guardians and Straight Arrows. Key to the different categories is their different attitude to seeking professional financial advice. Defined below:

Individualists have faith in their own investment abilities so do not approach a financial adviser. But they are also cautious.

Adventurers are what may be called high rollers, in that they like big bets, tend not to diversify and are happy to put all their eggs in one basket. They, too, are unlikely to seek financial advice.

Celebrities tend to follow the crowd in investment terms but are aware of their lack of expertise so frequently consult advisers.

Guardians are fearful of losing money, thus prefer rock-solid investments such as government bonds. They, too, are likely to seek professional investment advice.

Straight Arrows exhibit some of the characteristics of individualists and some of adventurers.

A certified financial planner (CFP®) helps individuals plan their financial futures. CFPs are not focused only on investments; they help their clients achieve specific long-term financial goals, such as saving for retirement, buying a house, or starting a college fund for their children.

To become a CFP®, a person must complete a course of study and then pass a two-part examination. The exam covers wealth management, tax palnning, insurance, retirement planning, estate planning, and other basic personal finance topics. These topics are all important for someone seeking to help clients achieve financial goals.

Chartered Financial Analyst (CFA)

A CFA, on the other hand, conducts investing in larger settings, normally for large investment firms on both the buy side and the sell side, mutual funds or hedge funds. CFAs can also provide internal financial analysis for corporations that are not in the investment industry. While a CFP® focuses on wealth management and planning for individual clients, a CFA focuses on wealth management for a corporation.

To become a CFA, a person must complete a rigorous course of study and pass three examinations over the course of two or more years. In addition, the candidate must adhere to a strict code of ethics and have four years of work experience in an investment decision-making setting.

(“Informed Voice of a New Generation of Fiduciary Advisors for Healthcare”)

For most lay folks, personal financial planning typically involves creating a personal budget, planning for taxes, setting up a savings account and developing a debt management, retirement and insurance recovery plan. Medicare, Social Security and Required Minimal Distribution [RMD] analysis is typical for lay retirement. Of course, we can assist in all of these activities, but lay individuals can also create and establish their own financial plan to reach short and long-term savings and investment goals.

But, as fellow doctors, we understand better than most the more complex financial challenges doctors can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

Posted on December 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Beneficial Ownership Information

By Staff Reporters

***

***

Small business owners face severe penalties if they don’t report to the federal government by year’s end. And, thousands of businesses may not realize they are subject to a new reporting process mandated under the Corporate Transparency Act, which went into effect in January 2024. Even lawyers, doctors, financial advisors and accountants are affected; along with “mom and pop”business owners.

For most eligible businesses, the filing deadline is Jan. 1, 2025, according to the U.S. Chamber of Commerce. “Those who fail to file by this deadline — or fail to update this information if needed — could face up to two years imprisonment and fines up to $10,000, in addition to civil penalties of up to $591 per day,” the U.S. Chamber of Commerce website reads.

The law was created “to combat illicit activity including tax fraud, money laundering and financing for terrorism by capturing more ownership information for specific U.S. businesses operating in or accessing the country’s market,” the chamber website explained.

A paradox is a logic and self-contradictory statement or a statement that runs contrary to one’s expectation. It is a statement that, despite apparently valid reasoning from true or apparently true premises, leads to a seemingly self-contradictory or a logically unacceptable conclusion. A paradox usually involves contradictory-yet-interrelated elements that exist simultaneously and persist over time. They result in “persistent contradiction between interdependent elements” leading to a lasting “unity of opposites”.

***

And so, as we plan for our financial future thru a New Year Resolution for 2025, it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

According to Adam Grossman, here are seven [7] of the paradoxes that can bedevil financial decision-making, clients and financial advisors, alike:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds. More:https://tinyurl.com/285vftx4

There’s the paradox that the stock market may appear over valued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as the recent 2024 election results attest.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

Posted on September 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Dubious Financial Specialists?

By Rick Kahler MS CFP®

Even if you work with a financial planner, there are times you may also need the services of a financial specialist such as an attorney, accountant, or insurance agent.

Conflicted

In a situation where the specialist’s advice may seem to conflict with the suggestions of your financial planner, as a rule the specialist always has the last word. After all, they are the experts. Their particular knowledge is the reason your generalist financial planner recommended consulting them in the first place.

Occasionally, however, a specialist’s recommendations may not be in your best interest. Most are skilled professionals who are very good at their jobs and provide a great service to their clients in moving the financial planning process forward.

However, as in any profession, there are exceptions.

One example of this is when a specialist’s knowledge doesn’t adequately cover the particular needs of a client’s situation.

Another example is a specialist who has a conflict of interest because of receiving commissions for the sale of financial products.

Both of these may be more likely to occur when specialists are chosen less because of their skills and more because of a prior relationship with the client.

While most specialists are open to listening to another point of view, acknowledging errors, or learning new information, some are not. It’s those specialists who lack needed knowledge and are unwilling to admit errors that cause financial planners to lose sleep.

A Choice

If a planner disagrees with the client’s specialist and says so, this can put the client in a difficult and unenviable position of having to choose between two trusted professionals, one of whom may have some incorrect information.

Unfortunately, the client usually doesn’t have the training or knowledge to know which. If the client is forced to side with one professional against the other, at best this damages the ongoing ability of the professionals to work together and at worst it finds the client firing one or both.

Planners who choose to keep silent about the disagreement and defer to the specialist can save face as well as retain working relationships with both the client and the specialist. They can only hope that the apparent poor advice the specialist has given the client works out in the long run.

Most planners I know will weigh the severity of the issue, as well as the strength of the client’s relationships with them and the specialist, when deciding how forcefully to oppose poor advice. If the consequences are significant, many financial planners will risk losing their relationship with the client to point out a specialist’s error.

***

***

To Do List

What can you do to encourage your planner to level with you if one of your specialists is giving you advice that doesn’t serve you well?

I don’t have a definitive answer to this difficult question.

One thing I can suggest is that communication is essential. It’s important that you fully and openly explore any disagreement a planner expresses, no matter how insignificant it sounds.

My second suggestion is to minimize the chances of getting poor advice in the first place. Avoid anyone who might have a conflict of interest, especially if they receive commissions for selling you something. Don’t assume a professional you’ve worked with in other areas is qualified for this particular concern.

Assessment

Make sure your planner has thoroughly researched the specialist’s expertise, and don’t be afraid to ask questions about anything you don’t fully understand. Partner with your financial planner to choose a specialist carefully in the beginning, and you increase the likelihood that all of you will be able to work effectively as a team.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Did you know that Federal and state laws require Registered Investment Advisors [RIAs] be held to a fiduciary standard? To satisfy this extremely high legal standard, an advisor must act solely in the best interest of the client, even if that interest is in conflict with the advisor’s own financial interests. Investment Advisors [IAs] must disclose any conflict, or potential conflict, to the client prior to and throughout a business engagement. Investment Advisors must fully disclose, in writing, how they are compensated. In addition, most adopt a Code of Ethics to ensure that fiduciary obligations are achieved.

Brokers or Advisors

Unfortunately, not all “financial advisors” work for federally or state-registered investment advisory firms. Many so-called financial advisors are registered representatives, better known as stock-brokers, and are employed by brokerage firms [broker-dealers]. Generally, these registered representatives [RRs] need not comply with the fiduciary duty standard that is owed when you are dealing with a registered investment advisory firm. Because broker-dealers are not necessarily acting in your best interest, the SEC [remember what a fine job former Commissioner Chris Cox did for investors in the Bernie Madoff incident?] and FINRA [NASD] require them to add the following disclosure to your client agreement.

Disclosure

Read this disclosure, and decide if this is the type of relationship you want to dictate your financial security:

“Your account is a brokerage account and not an advisory account. Our interests may not always be the same as yours. Please ask us questions to make sure you understand your rights and our obligations to you, including the extent of our obligations to disclose conflicts of interest and to act in your best interest. We are paid both by you and, sometimes, by people who compensate us based on what you buy. Therefore, our profits, and our salespersons’ compensation, may vary by product and over time.”

Disclaimers

If this disclaimer appears in agreements you are signing, or have already signed, you should ask questions of your advisor. S/he’s probably a broker. Obtain complete disclosure about how he or she is compensated, and where his or her first loyalties lie. Then decide if the relationship is in your best interest [Source: www.focusonfiduciary.com NAPFA Consumer Education Foundation]. Also, consider mediation and arbitration clauses very carefully. Do not wave your rights to litigation. Your patients do not; and neither should you!

Assessment

I am a doctor, former stock-broker, registered-rep, certified financial planner and licensed insurance agent who decided there must be a better way to help physician colleagues. As a health economist, and Founder of www.CertifiedMedicalPlanner.org I’ve believe I’ve found that way.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

As a former certified financial planner for almost 15 years, I was surprised to recently receive the following unedited e-mail correspondence.

Dear Marcinko,

If you are clever, have a way with people, or are a born salesperson, then becoming financial advisor could be your ticket to paradise.

Maybe not exactly paradise, but you could definitely have a ticket to a rewarding career. If you’re thinking about starting out as a new financial advisor – you may already be half the way there.

Why?

Because it’s an occupation where your life challenges will give you the understanding and empathy needed to work with your clients. Have you ever been in the position where you had to figure out a budget for your children’s education? Or manage an over extended credit card? These life situations will aid an individual on the path to become a financial consultant.

Requirements to Be a Financial Advisor

Even though a formal education is not a necessity to become financial adviser, it helps if you’ve taken certain courses.

What degree do you need to become a financial advisor? A bachelor’s degree in Finance, Economics, Accounting, Commerce, Business or Marketing would be a good start. A degree won’t assure you of a startling career but it may help get your foot in the door.

Rumor has it that a degree in psychology is also an asset as financial advising is as much about counseling as it is about advising. There are a plethora of people with all sorts of emotional entanglements around their financial lives.

Licenses

So, what licenses do you need to be a financial advisor? Some companies will assist a newbie in the financial advisory business and place them into a special program that will help them to obtain the required regulatory licenses such as a Series 66, this license permits them to vend annuities and mutual funds. It’s also possible to manage your own training. You can take part-time courses in order to qualify for the CFP (Certified Financial Planner) exam.

There are roughly over 286 universities and colleges that will assist you in preparing for the CFP exam. How long does it take to become a financial advisor? In order to qualify for the exam you will also need three years full-time working experience with a financial planning establishment.

Statistics state that over 40% regularly fail this all important exam. It’s worth the time and effort as with this certification you are deemed as a certified financial planner and demand a higher salary.

Assessment

Hot tip: Stay away from insurance companies for financial employment. They’ll insist that you sign everyone including the dog and your grandmother. Then get rid of you if you don’t procure sufficient business. Banks are better they will bring in the clients for you.

Conclusion

And so, your thoughts and comments on this ME-P are appreciated. Are financial advisors true professionals; or a truely professional sales force?

Please review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure. Are financial advisors true professionals, or a professional sales force?

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

As a financial advisor for more than 15 years, it has been my experience that many doctors who require assistance in developing a comprehensive personal financial plan also need help with implementing any investment planning recommendations. While perhaps not so true before the “flash-crash” of 2008-09, the issue seems especially true today as retirement portfolios have been decimated, and the specter of healthcare reform is no longer just a threat but a political reality. The mindset of hubris has been replaced by a tone of fear in many medical colleagues.

The Financial Advisors

Physician investors who develop an investment plan may use a competent financial advisor [FA] or other specialist in the investment area. A financial advisor can help clients understand their current financial situations and develop strategies for achieving their goals. Other FAs are specialists that help clients design and implement plans for investing. Still others use a more comprehensive approach to the entire financial planning process with extreme degrees of healthcare specificity

These Certified Medical Planners™ are fiduciaries at all times and put client needs first as registered investment advisors [RIAs], not commissioned sales agents or mere stock-brokers despite often confusing monikers.

Implementation

Implementation may be accomplished using professionally managed portfolios and mutual funds. The following shows how a plan may be implemented with an advisor assisting the physician-investor. The process may include:

• Developing investment policy and strategies

• Selecting and implementing managed portfolios and mutual funds

• Evaluating performance on a periodic basis

• Periodically reviewing and adjusting the investment plan as required

Note: The advisor may provide all of the investment services, or the physician investor may use other advisors in the process.

Example:

A financial planner has developed a number of financial planning recommendations for a client. One recommendation is to develop a written investment plan, review current investments, and implement changes. The planner has recommended an investment advisor experienced in selecting and monitoring managed portfolios and mutual funds. The financial planner will meet with the client and advisor initially and once each year to monitor the plan.

Example:

A financial planner has developed a financial plan for a client. The financial planner specializes in developing investment policy but not in implementing investments. The financial planner will use asset allocation software and develop a written long-term plan for the client. The doctor-client will work with a major brokerage firm to implement the plan using managed portfolios and mutual funds. The financial planner will monitor the brokerage firm and help the client evaluate performance.

Example:

A financial planner has developed a financial plan for a physician-client and will assist the client in developing asset allocation strategies. The planner has extensive knowledge in implementing the asset allocation strategies using managed portfolios and mutual funds. The planner will select and monitor the choices. The planner will provide the client with a quarterly performance report and meet with the client every six months to review the plan and strategies.

Assessment

Understanding the above is more critical than ever as physician-income continues to shrink going forward in the era of healthcare reform.

Conclusion

And so, your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Do you seek professional assistance with your investing needs, or do you go-it-alone; why or why not? Then, subscribe to the ME-P. It is fast, free and secure.

Speaker:If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com and http://www.springerpub.com/Search/marcinko

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Posted on April 29, 2009 by Dr. David Edward Marcinko MBA MEd CMP™

Checklist for Financial Planners

[By Staff Reporters]

The following will enable the financial planner to assist the client in choosing a nursing home.

The Checklist

1. Review the client’s requirements. An assisted-living facility may suffice instead of a true nursing home, which is required by the frail and elderly needing daily medical care.

2. Pick a location close to home and relatives. Frequent visits are crucial, not only to combat loneliness but also to ensure resident receives proper attention.

3. Read inspection report (state survey). If the financial planner encounters difficulties in obtaining a current report, he or she should assume that the home has something to hide. Don’t expect perfection. Nursing homes provide a difficult service for difficult residents. If a home is unresponsive to inquiry regarding items in a report, assume a similar response to concerns about the quality of care being provided in the future.

4. Tour the facility on an unannounced basis at different times on different days. Stroll through corridors and look and listen. Trust senses and instincts. Items to consider should include:

· Appearance of residents’ rooms. Outward decor of facility can be misleading, so the planner should inspect the residents’ rooms. To what extent can the rooms be personalized? If rooms are shared, how are good roommate matches made?

· Smells. High-quality homes have no lingering stench of urine or air freshener to cover up bad care and unusually high incidences of incontinence due to lack of attention by staff.

· Safety hazards. Be especially aware of items in corridors that can be obstacles to those with unsteady gait and poor eyesight.

· Sufficient staff members who are pleasant and respectful to residents. Are staff members responsive to residents’ needs? Are staff members warm in their interactions with all residents, even those requiring the heaviest supervision? Are aides helping residents with walking or exercise of their arms and legs?

· Residents’ attitudes toward facility’s service. Talk with residents and staff to determine attitudes toward the facility’s service. Does the facility have a family counsel to provide it with input?

· Grooming. A clear sign of neglect is failure to keep residents clean, well dressed, and well groomed.

· Physical restraints. Nursing homes that have eliminated restraints also have improved quality of life and more social contact among residents. Ties, belts, vests, and high bed rails are an easy but unsatisfactory solution to managing residents. Count number of residents that are restrained; ask what percentage are restrained and why.

· Food. Visit at meal time and sample the food to make sure it is palatable. The setting for meals should be attractive and pleasant, and food should be served at the proper temperature. Staff should be available to help residents who are not able to feed themselves. Review menus and determine the amount of concern for nutrition.

· Activities. A wide variety of activities should be provided, and the participation level should be high. Bored residents in front of a television may be a sign of a home’s failure to stimulate its residents.

· Dignity. Residents should be handled in ways that respect their dignity. For example, are residents properly clothed in public?

· Bed sores. Bed sores are a sign of poor care. Review inspection reports and see if they are mentioned, or talk to residents or their families about this topic.

· Special care units. Such units are often used as an expensive marketing device. The special care units may not be designed well and may indicate a lack of outdoor facilities.

5. Review the facility’s policy on medical care. Will residents be seen by their personal doctors or by staff physicians? Does the home have good infection control and immunization plans? What sort of access to dentists and eye doctors is there?

6. Perform financial analysis. The planner should gain a complete understanding of what the client’s and/or his or her family’s financial commitments are and how they will be met.

· Determine the financial strength of the nursing home, particularly if client funds are to be advanced.

· Consider a single lifetime payment in lieu of monthly rental payments.

· Consider exclusions in contract. For example, nursing home insurance coverage should include loss of personal property and personal injury.

· Determine what services the client will require, what is covered under the facility’s general fee, and what services are provided for an extra fee. Determine what the extra fee will be for each additional service that will be required. Family members should not agree to pay these charges because this could delay Medicaid funding.

· Analyze pricing structure in general and what the pattern of increases in fees has been.

· Determine residents’ rights in eviction proceedings for nonpayment of rent, in returning to nursing home after hospital stay, and in having Medicaid make payments on behalf of resident.

· Determine residents’ rights to appeal decisions and what the appeal procedures are.

7. Obtain and check references, including families of current residents, local hospitals, doctors, and government agencies, particularly the ombudsman at state departments for aging.

Assessment

What have we missed?

Conclusion

In any case, early planning is the key to supporting both your kids’ futures and your retirement. Making logical college funding decisions, rather than emotional ones, creates a win/win for everyone.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on April 19, 2009 by Dr. David Edward Marcinko MBA MEd CMP™

Marcinko Predates Basu – Joins in on Promoting Same

[By Ann Miller; RN, MHA]

Executive Director

Editor’s Note:

We cut and pasted this verbatim anonymous comment, obtained from the trade magazine – Financial Advisor [FA] online – for its pointed charges important to the currently contentious topic of CFP mark status. Although emotional, and borderline abusive, it may represent more reality; than not.

The Letter

Liars and Frauds

Grossly Incompetent

Conveniently Stupid

Simply Unethical

The bulk of the commentary seems to focus on ethics and fiduciary duty to clients. It does not now, nor has ever existed. Fiduciary:

“As fiduciaries, financial planners must make fair and complete disclosure of all material facts and must employ reasonable care to avoid misleading their clients. The utmost good faith is required in all their dealings. Simply put, fiduciaries must exhibit the highest form of trust, fidelity and confidence, and are expected to act in the best interest of their clients at all times.”

The bulk of planner’s violate this tenet and always have. A fiduciary MUST be legal. The idea that one is practicing ethically while never being legal is an affront to any rational person. Or; shall we simply say a “prudent man” at as minimum.

As a fact, about 35 states require licensing that planners don’t want to hear about, never mind adhere to. California – with 8,000 CFPs – has only ONE that is fully licensed and legal to offer comprehensive fee services. Where is the outrage from CFP®s regarding this – and what the other 35 states demand?

A Conspiracy?

Nothing at all: The Board has actively engaged in a conspiracy of silence regarding such duty. NAPFA is a joke and always has been regarding high standards. Yet not one CFP® apparently even cares. That is being a fiduciary? It goes further. The UC system in California was also made aware of this deception more than a decade ago – yet did nothing. The illegal planners/instructors were left to “instruct and guide” new planners to the same level of illegality and fraud. You simply have a wholesale violation of integrity and honesty permeates the educational system and no one cares. I am not sure California Lutheran knows of the deception either. I doubt it. Does that make the lack of integrity and knowledge any the less worse? No.

You have to know what is required legally to perform a function. Every commentator would immediately notify regulators if a physician or attorney was practicing illegally. Yet; nothing here. Is this a double standard by CFPs etc, all to allow themselves a free pass from licensing? Sure.

Every officer, director and most staff members of the Board since Bob Goss has been aware of the fraud. All on formal written record since 1995, at the very least. Not one CFP® in this commentary venue has even bothered to address illegal and unethical activity- yet while extolling the virtues of the organization and themselves. What about the New Disciplinary Board Members? Are they not aware of the breach? If not, why not. Incompetency? If they do now, then why have they done nothing? Conveniently stupid – worse?

Steven Covey noted:

“Integrity means avoiding any communication that is deceptive, full of guile or beneath the dignity of people. A lie is any communication with intent to deceive. Whether we communicate with words or behavior, if we have integrity, our intent cannot be to deceive.”

FA is also aware of the lies and deception and at least has allowed this discussion. But to have further commentary from Board officers extolling the virtues of their standards and the highest integrity is disingenuous at best and a fraud at its worst.

Shame

Shame on all of you for not forcing the issue – of being a true fiduciary? But then again, worse yet, we have these same organizations and people deceptively going to Congress to instill this level of a breach of duty to the American public. Yet, hardly an outcry because the deception is so good and because members would benefit. So we have a benefit by deception.

“it is a lot easier to talk about your ethics than to live up to them.”

The standards might be fine. But who cares if they do not have to be adhered to. Is that not the real question?

Contrary to the above and CFP BoS requirements, the Certified Medical Planner program demands a college degree [with verifiable proof], a written and signed statement of legal fiduciary accountability at all times, and CEs consisting of a published dissertation, not mere annual lucre www.CertifiedMedicalPlanner.org

The CMP™ Experience

Now, in as much as I am the ED for our CMP™ online program, I vet most applications. The prioritized reasons for matriculation rejection are: 1] unwillingness / inability to accept fiduciary status while blaming it on BDs, 2] lack of at least an undergraduate college degree, and 3] absolute “panic” regarding our writing and publication requirements.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Speaker:If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.comor Bio: www.stpub.com/pubs/authors/MARCINKO.htm

Subscribe Now:Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Posted on March 8, 2009 by Dr. David Edward Marcinko MBA MEd CMP™

Deciding What Works?

[By Staff Reporters]

Another way of asking the above titled question might be, “Is it smart for a doctor’s household to build savings while they are getting out of debt?”

Financial Priorities

In the first instance, the doctor already has debt and would be increasing the terms of any loans by deferring some of the payments to savings, which is equivalent to borrowing the same amount.

In the second instance, the doctor would be taking on debt to save more money. The answer is that it makes sense to borrow money for investment purposes only if the financial gains derived from the investment are larger than the financial benefits of paying off the debt. But, who can know for sure?

Assuming that a medical professional has more debt than needed, and doesn’t make contributions to a retirement account, the concern becomes: [1] should he/she make minimum payments to the debt and contribute to a retirement account; or [2] should he/she make the maximum payments toward the debt or loans, etc?

Downside Risks

It is important to understand the downside risks of a lower payment strategy. Just as stocks return more than bonds due to their higher risk, the lower payment strategy returns more because of its’ higher risk. Taking on debt to finance an investment is riskier than paying off debt for a number of reasons.

First, the US economy may continue its’ current depressionary spiral, and investments and savings could disappear as financial institutions fail. This would leave the doctor with debt that he or she could not service.

Second, the rate-of-return required to decide whether or not to borrow for investment purposes may not be achieved, leaving the doctor in worse financial shape than if he or she had just paid off the debt.

Assessment

Ultimately, the doctor must decide if the added risks are worth the possible gain. But, the services of a fiduciary financial advisor may also be required. However, some doctors may not be ready to receive the sort of “tough-love” required in this case.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on February 10, 2009 by Dr. David Edward Marcinko MBA MEd CMP™

Using Financial Advisors with Increased Safety

[By Dr. David Edward Marcinko; MBA, CMP™]

Following the Bernie Madoff investment scheme, and related financial industry scandals, here are seven “red-flags” that should have alerted physician-investors to proceed with extreme caution. Always consider them before making an investment with any financial advisor [FA], registered representative [RR] or financial advisory firm, regardless of reputation, size, referral recommendation or so-called industry certifications and designations. In other words, according to Robert James Cimasi; MHA, AVA, and a Certified Medical Planner™ from Health Capital Consultants LLC, of St. Louis, MO;” trust no one and paddle your own canoe.”

Red Flags of Cautious Investing

As a former insurance agent, financial advisor, registered representative, investment advisor and Certified Financial Planner™ for more than a decade, the existence of any one of the following items may be a “red-flag” of caution to any investor:

Acting as its’ own custodian, clearance firm or broker-dealer, etc.

Lack of a well-known accounting firm review with regular reporting.

Unreliable or sporadic written performance reports.

Rates-of-return that don’t seem to track industry benchmarks.

Seeming avoidance of regulatory oversight, transparency or review.

Lack of recognized written fiduciary accountability in favor of lower brokerage “sales suitability” standards.

No Investment Policy Statement [IPS].

Assessment

Let a word to the wise be sufficient going forward. But, in hindsight, a healthy dose of skepticism might have prevented this situation in the first place. As is the usual case, fear and greed often seem to rule the day. Just as there is no such thing as safe sex – just safer sex – there is no thing as safe intermediary investing. But, exercising some common sense will surely make investing with any financial advisor much safer. It’s like a condom for your money.