Dr. David Edward Marcinko; MBA MEd

SPONSOR: http://www.HealthDictionarySeries.org

***

***

Why It Matters More Than Ever

Every April, Financial Literacy Month invites people to pause and take a closer look at their relationship with money. It’s a moment to reflect on how we earn, spend, save, borrow, and plan for the future. While the idea may sound simple, the impact of financial literacy reaches far beyond balancing a checkbook or clipping coupons. It shapes the stability of households, the resilience of communities, and the long‑term health of the economy. In a world where financial decisions grow more complex each year, dedicating a month to strengthening financial understanding is not just symbolic—it’s essential.

At its core, financial literacy is the ability to understand and effectively use financial skills. These skills include budgeting, saving, investing, managing credit, and planning for retirement. Yet many people enter adulthood without a strong foundation in these areas. Schools often treat personal finance as an optional topic rather than a core life skill, and families may avoid discussing money altogether. As a result, people frequently learn through trial and error, sometimes making costly mistakes that follow them for years. Financial Literacy Month aims to break that cycle by encouraging education, conversation, and empowerment.

One of the most important themes of the month is budgeting, the backbone of financial stability. A budget is more than a spreadsheet—it’s a plan that reflects priorities. When people understand how to track income and expenses, they gain control over their financial lives. They can identify wasteful habits, set realistic goals, and make intentional choices. Budgeting also helps reduce stress. Money is one of the most common sources of anxiety, and uncertainty often fuels that stress. A clear budget replaces uncertainty with clarity, giving people a sense of direction.

Another key focus is saving, especially for emergencies. Life is unpredictable. A car breaks down, a medical bill arrives, or a job suddenly disappears. Without savings, these events can spiral into debt or financial crisis. Financial Literacy Month encourages people to build an emergency fund—ideally enough to cover several months of expenses. Even small, consistent contributions can create a safety net that protects against hardship. Saving is not just about preparing for the worst; it’s also about creating opportunities. Whether it’s buying a home, starting a business, or pursuing education, savings open doors.

Credit management is another crucial topic highlighted during the month. Credit can be a powerful tool when used wisely, enabling people to buy homes, finance education, or start companies. But mismanaging credit can lead to high-interest debt and long-term financial strain. Understanding how credit scores work, how interest accumulates, and how to avoid predatory lending practices empowers people to make informed decisions. Financial Literacy Month encourages individuals to check their credit reports, dispute errors, and develop strategies to improve their credit health.

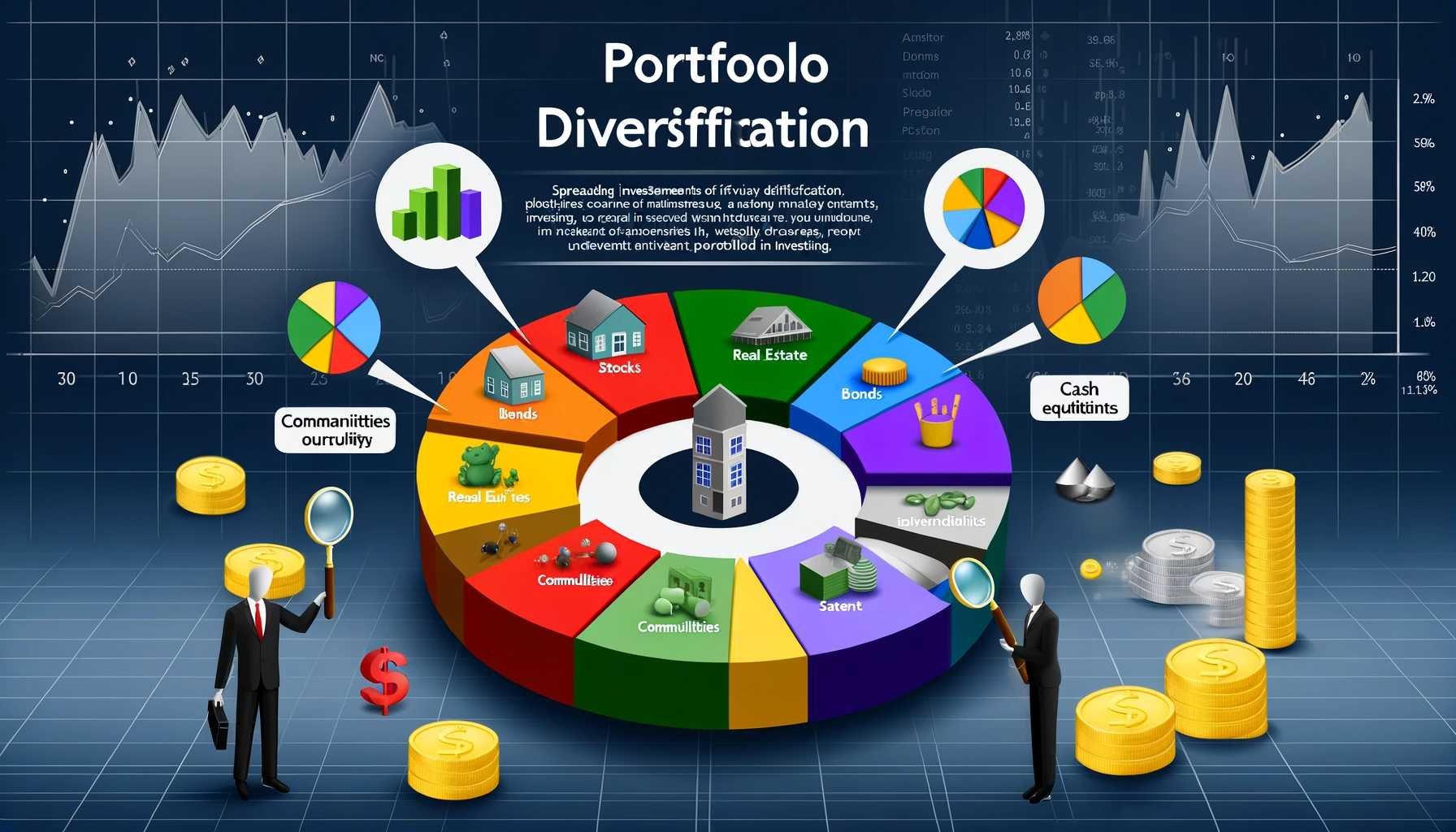

In recent years, investing has become more accessible, but also more confusing. Apps and online platforms have made it easy for anyone to buy stocks or cryptocurrencies with a few taps. While this accessibility is exciting, it also increases the risk of impulsive decisions. Financial Literacy Month emphasizes the importance of understanding risk, diversification, and long-term planning. Investing is not about chasing quick wins; it’s about building wealth steadily over time. Learning the basics helps people avoid emotional decisions and focus on strategies that align with their goals.

Beyond individual skills, the month also highlights broader issues such as financial inequality and access. Not everyone has the same opportunities to learn about money or build wealth. Communities with fewer resources often face higher barriers, from limited access to banking services to a lack of financial education programs. Financial Literacy Month encourages organizations, schools, and policymakers to address these gaps. When financial knowledge becomes more accessible, communities become stronger and more resilient.

Technology also plays a growing role in financial literacy. Digital tools can help people track spending, automate savings, and learn new concepts through interactive platforms. However, technology also introduces new challenges, such as online scams and data privacy concerns. Financial Literacy Month encourages people to stay informed about digital risks and to use technology thoughtfully. Being financially literate today means understanding not only traditional money management but also the digital landscape that surrounds it.

Ultimately, the purpose of Financial Literacy Month is empowerment. Money touches every part of life—housing, healthcare, education, relationships, and retirement. When people understand how to manage their finances, they gain confidence and independence. They can make choices that align with their values and build a future that feels secure. Financial literacy is not about becoming wealthy; it’s about gaining the knowledge to navigate life’s financial challenges with clarity and purpose.

COMMENTS APPRECIATED

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR- http://www.MarcinkoAssociates.com

Like, Refer and Subscribe

***

***

Share this:

Filed under: finance, Financial Planning, Marcinko Associates | Tagged: April, david marcinko, finance, financial literacy month | Leave a comment »