BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The core idea is simple: annuity taxation depends on the source of the money you receive. Payments from an annuity are made up of two components:

Principle — the money you originally contributed

Earnings — the growth generated inside the annuity

The IRS taxes these two components differently, and the rules shift depending on whether the annuity is qualified or non‑qualified, whether you take lump‑sum withdrawals or periodic payments, and whether you withdraw before or after age 59½.

Qualified vs. Non‑Qualified Annuities

Qualified Annuities

A qualified annuity is funded with pre‑tax dollars, usually through a retirement plan such as a traditional IRA or 401(k). Because the contributions were never taxed, both the principle and the earnings are fully taxable when withdrawn. Every dollar you receive is treated as ordinary income, not capital gains.

This means that when you begin receiving payments, the IRS does not distinguish between principal and earnings. The entire distribution is taxed because none of the money has been taxed before.

Non‑Qualified Annuities

A non‑qualified annuity is funded with after‑tax dollars. You already paid taxes on the principal, so the IRS only taxes the earnings. This is where the exclusion ratio comes into play.

The Exclusion Ratio: How Principle Is Recovered Tax‑Free

For non‑qualified annuities that pay out over time, the IRS uses the exclusion ratio to determine how much of each payment is considered a return of principle and therefore not taxable.

The exclusion ratio is based on:

Your total investment in the contract

The expected return (based on life expectancy or contract terms)

Each payment is split proportionally into:

Non‑taxable return of principle

Taxable earnings

Once you have recovered all of your principle, all remaining payments become fully taxable.

Taxation of Lump‑Sum Withdrawals

If you take money out of a non‑qualified annuity before it is annuitized, the IRS applies the LIFO rule — Last In, First Out. This means:

Earnings come out first and are fully taxable

Principal comes out last and is tax‑free

This rule often surprises people who assume they can withdraw their original contributions tax‑free at any time. With annuities, that is not the case unless the contract has already been annuitized.

Early Withdrawal Penalties

Withdrawals made before age 59½ may trigger a 10% IRS penalty on the taxable portion of the distribution. This applies to:

Earnings from non‑qualified annuities

The entire withdrawal from qualified annuities

The penalty does not apply to the return of principle in a non‑qualified annuity because that portion is not taxable.

Taxation After Annuitization

Once an annuity is converted into a stream of payments, the tax treatment becomes more predictable:

Qualified annuity payments: fully taxable

Non‑qualified annuity payments: partially taxable based on the exclusion ratio

Annuitization spreads the tax burden over time and eliminates the LIFO rule.

Death Benefits and Beneficiary Taxation

Annuity taxation does not end with the owner’s death. Beneficiaries must pay taxes on any earnings they receive, whether as a lump sum or periodic payments. The principal portion remains tax‑free for non‑qualified annuities.

Unlike inherited IRAs, annuities do not offer a step‑up in basis. The original cost basis carries over, which can increase the taxable amount for heirs.

Why the Distinction Matters

Understanding how principal and income are taxed helps you:

Plan retirement income more efficiently

Avoid unexpected tax bills

Decide whether to annuitize or take withdrawals

Evaluate whether a qualified or non‑qualified annuity better fits your goals

The tax structure also affects estate planning, cash‑flow planning, and the timing of withdrawals.

Final Thoughts

The IRS treats annuity principal and earnings differently because annuities blend investment growth with return of your own money. Once you understand which part of your payment is which, the tax rules become far more predictable. The key is recognizing whether your annuity is funded with pre‑tax or after‑tax dollars and how you choose to take distributions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A financial advisor’s draw payment system is a compensation structure that blends stability with performance incentives, giving advisors predictable income while still tying their long‑term earnings to the revenue they generate. It is widely used in brokerage firms, independent advisory practices, and insurance‑based financial services organizations because it helps new or transitioning advisors manage cash flow while they build a client base. Understanding how a draw works, why firms use it, and what trade‑offs it creates is essential for evaluating its fairness and effectiveness.

What a Draw Payment System Is

A draw is an advance on future commissions or advisory fees. Instead of being paid strictly when revenue is earned, the advisor receives a regular, predetermined payment—weekly, biweekly, or monthly—that functions like a salary. Later, when the advisor earns commissions or fees, those earnings are used to “repay” the draw. If the advisor earns more than the draw amount, they receive the excess. If they earn less, the draw may accumulate as a deficit that must be repaid or carried forward.

Firms use several types of draws. A recoverable draw must be paid back through future production, while a non‑recoverable draw functions more like a temporary stipend that the firm does not reclaim. Some firms offer a graduated draw, which decreases over time as the advisor becomes more productive. These variations allow firms to tailor compensation to the advisor’s experience level and the firm’s risk tolerance.

Why Firms Use Draw Systems

The draw system exists because financial advising is a revenue‑driven profession with unpredictable income patterns. New advisors often face months of prospecting before earning meaningful commissions or fees. Without a draw, many would struggle to cover basic living expenses, making the profession inaccessible to anyone without substantial savings.

For firms, the draw system is a way to attract talent without committing to a full salary. It shifts part of the financial risk to the advisor while still providing enough stability to support early‑stage business development. It also aligns incentives: advisors are motivated to produce revenue because their long‑term earnings depend on it.

How Draws Affect Advisor Behavior

A draw system shapes advisor behavior in several ways:

Encourages early productivity — Because the draw must be repaid, advisors feel pressure to generate revenue quickly.

Promotes long‑term client building — Once production exceeds the draw, advisors begin earning true commissions or fees, reinforcing the value of building a strong book of business.

Creates accountability — Firms can track whether advisors are on pace to justify their compensation.

Influences risk‑taking — Advisors may feel pressure to sell products with higher commissions to cover their draw, which can create ethical tensions if not properly supervised.

These behavioral effects are neither inherently good nor bad; their impact depends on firm culture, compliance oversight, and the advisor’s professional judgment.

Advantages for Advisors

A draw system offers several benefits:

Income stability — Advisors can rely on predictable payments while building their client base.

Reduced financial stress — The draw helps cover living expenses during slow periods.

Opportunity for high earnings — Once production exceeds the draw, advisors can earn significantly more than a fixed salary would allow.

Professional runway — The system gives advisors time to develop skills, build relationships, and refine their business model.

For many advisors, the draw is the bridge that makes the early years of the profession survivable.

Advantages for Firms

Firms also benefit from draw systems:

Lower upfront risk — Firms avoid paying full salaries to advisors who may not produce.

Performance alignment — Compensation is tied directly to revenue generation.

Talent attraction — Draws make the profession accessible to candidates who lack financial reserves.

Scalable compensation — Firms can adjust draw levels as advisors grow, reducing support as production increases.

This balance of risk and reward is one reason the draw system remains common across the industry.

Challenges and Criticisms

Despite its advantages, the draw system has drawbacks:

Debt pressure — Recoverable draws can accumulate into large deficits, creating financial stress.

Potential conflicts of interest — Advisors may feel pressure to recommend products with higher commissions.

Uneven income — Once the draw period ends, income can fluctuate dramatically.

Advisor turnover — High draw deficits can push advisors out of the industry before they have time to succeed.

These challenges highlight the importance of training, ethical oversight, and realistic production expectations.

The Draw System in a Modern Advisory Environment

As the industry shifts toward fee‑based planning and fiduciary standards, some firms are rethinking draw structures. Fee‑based advisors often experience more stable revenue streams, reducing the need for large draws. At the same time, firms still use draws to support new advisors who are transitioning from other careers or building a client base from scratch.

Hybrid models are emerging, combining modest base salaries with smaller draws and performance bonuses. These structures aim to reduce conflicts of interest while still rewarding productivity.

Closing Thought

A financial advisor’s draw payment system is ultimately a tool for balancing stability and performance. When designed thoughtfully, it supports new advisors, aligns incentives, and helps firms manage risk. When poorly structured, it can create financial pressure and ethical challenges. The key is finding a balance that supports both advisor success and client‑centered service.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Value‑Added Tax, commonly known as VAT, is one of the most widely used forms of taxation in the world. More than 160 countries rely on it as a major source of government revenue, and its influence on economic behavior, public finance, and consumer prices makes it a central feature of modern tax systems. At its core, VAT is a consumption tax applied at each stage of production and distribution, but only on the value added at that stage. This structure distinguishes it from traditional sales taxes and shapes both its advantages and its criticisms.

VAT operates on a deceptively simple principle. Whenever a business sells a good or service, it charges VAT on the sale price. At the same time, it receives a credit for the VAT it paid on its own inputs. The business then remits the difference to the government. Because each firm pays tax only on the value it adds—its contribution to the final product—the system avoids the “tax‑on‑tax” problem that plagued older turnover taxes. This incremental approach creates a transparent chain of taxation that follows a product from raw materials to final consumption.

One of the most significant strengths of VAT is its efficiency. Since the tax is collected in small increments throughout the supply chain, it is harder to evade than a single end‑stage sales tax. Each business has an incentive to keep proper records because it must document the VAT it paid in order to claim credits. This built‑in self‑enforcement mechanism reduces opportunities for fraud and increases the reliability of revenue collection. For governments, this makes VAT a stable and predictable source of income, which is especially valuable in countries with large informal sectors or limited administrative capacity.

VAT is also considered neutral in many respects. Because it taxes consumption rather than income or investment, it does not directly discourage saving or production. Economists often argue that taxing consumption is less distortionary than taxing labor or capital, since it allows individuals and firms to make economic decisions without the same degree of tax‑induced pressure. In theory, VAT encourages long‑term growth by leaving investment incentives intact. This neutrality is one reason why international organizations frequently recommend VAT as a cornerstone of tax reform.

Despite these advantages, VAT is far from universally praised. One of the most persistent criticisms is that it is regressive. Since lower‑income households spend a larger share of their income on consumption, they bear a heavier relative burden under a VAT system. Even though the tax applies uniformly to purchases, its impact is unequal across income groups. Many countries attempt to soften this effect by applying reduced rates or exemptions to essential goods such as food, medicine, or children’s clothing. However, these adjustments complicate the system and can undermine some of its efficiency.

Another challenge lies in the administrative demands of VAT. While the system is self‑policing in theory, it requires businesses to maintain detailed records, file regular returns, and manage complex invoicing requirements. For large firms, these obligations are manageable, but for small businesses they can be burdensome. In developing economies, where many enterprises operate informally or lack accounting capacity, implementing VAT can be particularly difficult. Governments must invest in training, technology, and oversight to ensure compliance, and these investments can be costly.

VAT also influences prices and consumer behavior. Because it is embedded in the cost of goods and services, it can raise the overall price level when introduced or increased. Consumers may feel the impact immediately, even if the tax is not itemized on receipts. Businesses, meanwhile, must decide whether to absorb part of the tax or pass it fully to consumers. In competitive markets, firms often have little choice but to raise prices, which can affect demand. Policymakers must therefore consider the timing and scale of VAT changes carefully to avoid economic shocks.

The political dimension of VAT is equally important. Although it is a powerful revenue tool, it can be unpopular with the public, especially when introduced in countries that previously relied on other forms of taxation. Governments often face resistance from both consumers and businesses, who may view VAT as an added financial burden. Successful implementation typically requires clear communication about how the revenue will be used and why the tax is necessary. When citizens believe that VAT funds essential services—such as healthcare, education, or infrastructure—they may be more willing to accept it.

In recent years, debates about VAT have expanded to include digital goods and cross‑border commerce. As economies become more digital, traditional tax systems struggle to capture value created by online transactions. VAT has had to adapt, with many countries introducing rules that require foreign digital service providers to collect and remit tax. This evolution highlights VAT’s flexibility but also underscores the complexity of administering a tax in a globalized, technology‑driven world.

Ultimately, VAT is a powerful but imperfect instrument. Its design encourages efficiency, transparency, and stable revenue, making it attractive to governments across the globe. At the same time, its regressive nature, administrative demands, and impact on prices create challenges that must be managed carefully. The ongoing debates surrounding VAT reflect broader questions about fairness, economic growth, and the role of taxation in society. As economies continue to evolve, VAT will remain a central topic in discussions about how to fund public services while balancing equity and efficiency.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Net Investment Income Tax (NIIT) occupies a distinctive place in the modern U.S. tax landscape. Introduced as part of the Affordable Care Act, it was designed to generate revenue from higher‑income households by taxing certain forms of unearned income. Although it affects a relatively small portion of taxpayers, its implications reach into investment strategy, tax planning, and broader debates about fairness and economic policy. Understanding how the NIIT works—and why it exists—offers insight into the evolving relationship between tax policy and wealth in the United States.

At its core, the NIIT is a 3.8 percent surtax applied to specific types of investment income for individuals whose modified adjusted gross income exceeds statutory thresholds. These thresholds—$200,000 for single filers and $250,000 for married couples filing jointly—are not indexed for inflation. As a result, over time, more taxpayers may find themselves subject to the tax even if their real purchasing power has not increased. This “bracket creep” is one of the subtle but important features of the NIIT, shaping its long‑term reach.

The tax applies only to “net investment income,” a term that includes interest, dividends, capital gains, rental income, royalties, and passive business income. It does not apply to wages, self‑employment earnings, or distributions from qualified retirement plans. The logic behind this distinction is straightforward: the NIIT targets income derived from wealth rather than labor. In practice, this means that two taxpayers with identical total income may face different NIIT liabilities depending on how much of their income comes from investments versus work.

The mechanics of the NIIT involve a comparison between two amounts: net investment income and the excess of modified adjusted gross income over the applicable threshold. The tax is applied to whichever of these two figures is smaller. This structure ensures that the NIIT functions as a surtax on high‑income households without taxing investment income for those below the threshold. It also means that taxpayers with large investment portfolios but modest overall income may avoid the tax entirely, while those with high wages and relatively small investment income may still owe it.

One of the most significant effects of the NIIT is its influence on investment behavior. Because the tax applies to capital gains, it can affect decisions about when to sell appreciated assets. Taxpayers may choose to time sales to avoid pushing their income above the threshold in a given year. Others may shift toward tax‑exempt investments, such as municipal bonds, or toward assets that generate unrealized rather than realized gains. The NIIT therefore becomes not just a revenue tool but a factor shaping the broader investment landscape.

The tax also interacts with other parts of the tax code in ways that can be complex. For example, rental real estate income is generally subject to the NIIT unless the taxpayer qualifies as a real estate professional and materially participates in the activity. Trusts and estates face their own NIIT rules, often reaching the surtax threshold at much lower income levels than individuals. These layers of complexity mean that the NIIT is often a central topic in tax planning for high‑income households, especially those with diverse investment portfolios.

Beyond its technical features, the NIIT reflects broader policy debates about equity and the distribution of tax burdens. Supporters argue that it helps ensure that high‑income individuals contribute a fair share to the cost of public programs, particularly those related to health care. Because investment income is disproportionately concentrated among wealthier households, the NIIT is seen as a way to align tax policy with ability to pay. Critics, however, contend that the tax discourages investment, adds unnecessary complexity, and imposes an additional layer of taxation on income that may already be subject to corporate taxes or other levies.

Despite these debates, the NIIT has become a stable part of the federal tax system. It raises billions of dollars annually and plays a role in funding health‑related initiatives. As discussions about tax reform continue, the NIIT often resurfaces as policymakers consider how best to balance revenue needs with economic incentives. Whether it remains unchanged, is expanded, or is modified in future legislation, the NIIT will continue to shape the financial decisions of high‑income taxpayers and contribute to the ongoing conversation about how the United States taxes wealth.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A concept of tax fairness that states that people with different amounts of wealth or different amounts of income should pay tax at different rates. Wealth includes assets such as houses, cars, stocks, bonds, and savings accounts. Income includes wages, interest and dividends, and other payments.

A business authorized by the IRS to participate in the IRS e-file Program. The business may be a sole proprietorship, a partnership, a corporation, or an organization. Authorized IRS e-file Providers include Electronic Return Originators (EROs), Transmitters, Intermediate Service Providers, and Software Developers. These categories are not mutually exclusive. For example, an ERO can at the same time, be a Transmitter, a Software Developer, or an Intermediate Service Provider, depending on the function being performed.

Assuming all other dependency tests are met, the citizen or resident test allows taxpayers to claim a dependency exemption for persons who are U.S. citizens for some part of the year or who live in the United States, Canada, or Mexico for some part of the year.

Amount that taxpayers can claim for a “qualifying child” or “qualifying relative”. Each exemption reduces the income subject to tax. The exemption amount is a set amount that changes from year to year. One exemption is allowed for each qualifying child or qualifying relative claimed as a dependent.

This allows tax refunds to be deposited directly to the taxpayer’s bank account. Direct Deposit is a fast, simple, safe, secure way to get a tax refund. The taxpayer must have an established checking or savings account to qualify for Direct Deposit. A bank or financial institution will supply the required account and routing transit numbers to the taxpayer for Direct Deposit.

The transmission of tax information directly to the IRS using telephones or computers. Electronic filing options include (1) Online self-prepared using a personal computer and tax preparation software, or (2) using a tax professional. Electronic filing may take place at the taxpayer’s home, a volunteer site, the library, a financial institution, the workplace, malls and stores, or a tax professional’s place of business.

Electronic preparation means that tax preparation software and computers are used to complete tax returns. Electronic tax preparation helps to reduce errors.

The Authorized IRS e-file Provider that originates the electronic submission of an income tax return to the IRS. EROs may originate the electronic submission of income tax returns they either prepared or collected from taxpayers. Some EROs charge a fee for submitting returns electronically.

Free from withholding of federal income tax. A person must meet certain income, tax liability, and dependency criteria. This does not exempt a person from other kinds of tax withholding, such as the Social Security tax.

Amount that taxpayers can claim for themselves, their spouses, and eligible dependents. There are two types of exemptions-personal and dependency. Each exemption reduces the income subject to tax. While each is worth the same amount, different rules apply to each.

A program sponsored by the IRS in partnership with participating states that allows taxpayers to file federal and state income tax returns electronically at the same time.

The federal government levies a tax on personal income. The federal income tax provides for national programs such as defense, foreign affairs, law enforcement, and interest on the national debt.

Provides benefits for retired workers and their dependents as well as for disabled workers and their dependents. Also known as the Social Security tax.

To mail or otherwise transmit to an IRS service center the taxpayer’s information, in specified format, about income and tax liability. This information-the return-can be filed on paper, electronically (e-file).

Determines the rate at which income is taxed. The five filing statuses are: single, married filing a joint return, married filing a separate return, head of household, and qualifying widow(er) with dependent child.

Spending and income records and items to keep for tax purposes, including paycheck stubs, statements of interest or dividends earned, and records of gifts, tips, and bonuses. Spending records include canceled checks, cash register receipts, credit card statements, and rent receipts.

A foster child is any child placed with a taxpayer by an authorized placement agency or by court order. Eligible foster children may be claimed by taxpayers for tax benefits.

Money, goods, services, and property a person receives that must be reported on a tax return. Includes unemployment compensation and certain scholarships. It does not include welfare benefits and nontaxable Social Security benefits.

You must meet the following requirements: 1. You are unmarried or considered unmarried on the last day of the year. 2. You paid more than half the cost of keeping up a home for the year. 3. A qualifying person lived with you in the home for more than half the year (except temporary absences, such as school). However, a dependent parent does not have to live with the taxpayer.

Taxes on income, both earned (salaries, wages, tips, commissions) and unearned (interest, dividends). Income taxes can be levied on both individuals (personal income taxes) and businesses (business and corporate income taxes).

Performs services for others. The recipients of the services do not control the means or methods the independent contractor uses to accomplish the work. The recipients do control the results of the work; they decide whether the work is acceptable. Independent contractors are self-employed.

A person who represents the concerns or special interests of a particular group or organization in meetings with lawmakers. Lobbyists work to persuade lawmakers to change laws in the group’s favor.

An economic system based on private enterprise that rests upon three basic freedoms: freedom of the consumer to choose among competing products and services, freedom of the producer to start or expand a business, and freedom of the worker to choose a job and employer.

You are married and both you and your spouse agree to file a joint return. (On a joint return, you report your combined income and deduct your combined allowable expenses.)

You must be married. This method may benefit you if you want to be responsible only for your own tax or if this method results in less tax than a joint return. If you and your spouse do not agree to file a joint return, you may have to use this filing status.

Used to provide medical benefits for certain individuals when they reach age 65. Workers, retired workers, and the spouses of workers and retired workers are eligible to receive Medicare benefits upon reaching age 65.

When the amount of a credit is greater than the tax owed, taxpayers can only reduce their tax to zero; they cannot receive a “refund” for any excess nonrefundable credit.

Allow taxpayers to “sign” their tax returns electronically. The PIN, a five-digit self-selected number, ensures that electronically submitted tax returns are authentic. Most taxpayers can qualify to use a PIN.

Taxes on property, especially real estate, but also can be on boats, automobiles (often paid along with license fees), recreational vehicles, and business inventories.

Benefits that cannot be withheld from those who don’t pay for them, and benefits that may be “consumed” by one person without reducing the amount of the product available for others. Examples include national defense, streetlights, and roads and highways. Public services include welfare programs, law enforcement, and monitoring and regulating trade and the economy.

To be a qualifying child, the dependent must meet eight tests: (1) relationship, (2) age, (3) residence, (4) support, (5) citizenship or residency, (6) joint return, (7) qualifying child of more than one person, and (8) dependent taxpayer.

There are tests that must be met to be a qualifying relative, they are: (1) not a qualifying child, (2) member of household or relationship, (3) citizenship or residency, (4) gross income, (5) support, (6) joint return, and (7) dependent taxpayer.

If your spouse died in 2010, you can use married filing jointly as your filing status for 2010 if you otherwise qualify to use that status. The year of death is the last year for which you can file jointly with your deceased spouse. You may be eligible to use qualifying widow(er) with dependent child as your filing status for two years following the year of death of your spouse. For example, if your spouse died in 2010, and you have not remarried, you may be able to use this filing status for 2011 and 2012. This filing status entitles you to use joint return tax rates and the highest standard deduction amount (if you do not itemize deductions). This status does not entitle you to file a joint return.

Compensation received by an employee for services performed. A salary is a fixed sum paid for a specific period of time worked, such as weekly or monthly.

Similar to Social Security and Medicare taxes. The self-employment tax rate is 15.3 percent of self-employment profit. The self-employment tax is calculated on Schedule SE—Self-Employment Tax. The self-employment tax is reported on Form 1040, U.S. Individual Income Tax Return.

If on the last day of the year, you are unmarried or legally separated from your spouse under a divorce or separate maintenance decree and you do not qualify for another filing status.

Provides benefits for retired workers and their dependents as well as for the disabled and their dependents. Also known as the Federal Insurance Contributions Act (FICA) tax.

Develops software for the purposes of (1) formatting electronic tax return information according to IRS specifications, and/or (2) transmitting electronic tax return information directly to the IRS.

For dependency test purposes, support includes food, clothing, shelter, education, medical and dental care, recreation, and transportation. It also includes welfare, food stamps, and housing provided by the state. Support includes all income, taxable and nontaxable.

Interest income that is not subject to income tax. Tax-exempt interest income is earned from bonds issued by states, cities, or counties and the District of Columbia.

The amount of tax that must be paid. Taxpayers meet (or pay) their federal income tax liability through withholding, estimated tax payments, and payments made with the tax forms they file with the government.

Money and goods received for services performed by food servers, baggage handlers, hairdressers, and others. Tips go beyond the stated amount of the bill and are given voluntarily.

Taxes on economic transactions, such as the sale of goods and services. These can be based on a set of percentages of the sales value (ad valorem-sales taxes), or they can be a set amount on physical quantities (“per unit”-gasoline taxes).

The concept that people in different income groups should pay different rates of taxes or different percentages of their incomes as taxes. “Unequals should be taxed unequally.”

A system of compliance that relies on individual citizens to report their income freely and voluntarily, calculate their tax liability correctly, and file a tax return on time.

This provides free income tax return preparation for certain taxpayers. The VITA program assists taxpayers who have limited or moderate incomes, have limited English skills, or are elderly or disabled. Many VITA sites offer electronic preparation and transmission of income tax returns.

Compensation received by employees for services performed. Usually, wages are computed by multiplying an hourly pay rate by the number of hours worked.

Money, for example, that employers withhold from employees paychecks. This money is deposited for the government. (It will be credited against the employees’ tax liability when they file their returns.) Employers withhold money for federal income taxes, Social Security taxes and state and local income taxes in some states and localities.

Philanthropy is often celebrated as a noble endeavor, allowing wealthy individuals to contribute to societal welfare. However, beneath its altruistic veneer, philanthropic giving can also function as a strategic financial tool—particularly as a form of tax shelter. This duality raises important questions about equity, influence, and the role of private wealth in shaping public outcomes.

At its core, a tax shelter is any legal strategy that reduces taxable income. In the case of philanthropy, the U.S. tax code allows individuals to deduct charitable donations from their taxable income, often up to 60% depending on the type of donation and recipient organization. For billionaires and high-net-worth individuals, this can translate into substantial tax savings. For example, donating appreciated stock or real estate not only earns a deduction for the full market value but also avoids capital gains taxes that would have been incurred through a sale.

One common vehicle for such giving is the donor-advised fund (DAF). These funds allow donors to make a charitable contribution, receive an immediate tax deduction, and then distribute the money to charities over time. While DAFs offer flexibility and convenience, critics argue they enable donors to delay actual charitable impact while still reaping tax benefits. In some cases, funds sit idle for years, raising concerns about whether the public good is truly being served.

Private foundations present another avenue for tax-advantaged giving. By establishing a foundation, donors can retain significant control over how their money is spent, often employing family members or influencing policy through grantmaking. While foundations are required to distribute a minimum of 5% of their assets annually, this threshold is relatively low, and administrative expenses can count toward it. This means that a large portion of foundation assets may remain invested, growing tax-free, while only a fraction is used for charitable work.

Beyond financial mechanics, philanthropic tax shelters raise ethical and democratic concerns. When wealthy individuals use charitable giving to reduce their tax burden, they effectively shift resources away from public coffers—funds that could support schools, infrastructure, or healthcare. Moreover, philanthropy allows donors to direct resources according to personal priorities, which may not align with broader societal needs. This privatization of public influence can undermine democratic decision-making and perpetuate inequality.

In conclusion, while philanthropic giving can yield positive social outcomes, it also serves as a powerful tax shelter for the wealthy. The challenge lies in balancing the benefits of private generosity with the need for transparency, accountability, and equitable tax policy. As debates over wealth concentration and tax reform intensify, reexamining the role of philanthropy in public finance becomes increasingly urgent. Only by addressing these complexities can society ensure that charitable giving truly serves the common good.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Required Minimum Distributions (RMDs) are mandatory withdrawals from certain retirement accounts that begin at age 73, designed to ensure the IRS collects taxes on previously tax-deferred savings.

Required Minimum Distributions (RMDs) are a critical component of retirement planning in the United States. They represent the minimum amount that retirees must withdraw annually from specific tax-deferred retirement accounts, such as traditional IRAs, 401(k)s, and other qualified plans, once they reach a certain age. As of 2025, individuals must begin taking RMDs at age 73, a change implemented by the SECURE 2.0 Act for those born between 1951 and 1959.

The rationale behind RMDs is rooted in tax policy. Contributions to tax-deferred accounts are made with pre-tax dollars, allowing investments to grow without immediate tax consequences. However, the IRS eventually wants its share. RMDs ensure that retirees begin paying taxes on these funds, preventing indefinite tax deferral. The amount of each RMD is calculated using the account balance at the end of the previous year and a life expectancy factor provided by IRS tables.

Failing to take an RMD can result in steep penalties. Historically, the penalty was 50% of the amount not withdrawn, but recent changes have reduced this to 25%, and potentially 10% if corrected promptly. These penalties underscore the importance of understanding and complying with RMD rules.

Not all retirement accounts are subject to RMDs. Roth IRAs are exempt during the original account holder’s lifetime, and under the SECURE 2.0 Act, Roth 401(k) and Roth 403(b) accounts are also exempt from RMDs while the original owner is alive. However, beneficiaries of these accounts may still face RMD requirements.

***

***

Strategically managing RMDs can help retirees minimize tax impacts and optimize their retirement income. For example, retirees might consider withdrawing more than the minimum in years with lower income to reduce future RMD amounts. Others may choose to convert traditional IRA funds to Roth IRAs before reaching RMD age, thereby reducing future taxable distributions. Additionally, using RMDs to fund charitable donations through Qualified Charitable Distributions (QCDs) can satisfy the RMD requirement while excluding the amount from taxable income.

Timing is also crucial. The first RMD must be taken by April 1 of the year following the year the individual turns 73. Subsequent RMDs must be taken by December 31 each year. Delaying the first RMD can result in two withdrawals in one year, potentially increasing taxable income and affecting Medicare premiums or tax brackets.

In conclusion, RMDs are more than just a tax obligation—they are a planning opportunity. Understanding the rules, calculating the correct amount, and integrating RMDs into a broader retirement strategy can help retirees maintain financial stability and reduce unnecessary tax burdens.

As regulations evolve, staying informed and consulting with financial professionals is essential to make the most of retirement savings.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Sudden Money Paradox: When Wealth Disrupts Instead of Liberates

The “Sudden Money Paradox” refers to the counterintuitive reality that receiving a large financial windfall—whether through inheritance, lottery winnings, business sales, or legal settlements—can lead to emotional turmoil, poor decision-making, and even financial ruin. While most people assume that sudden wealth guarantees security and happiness, the paradox reveals that it often destabilizes lives instead.

At the heart of this paradox is the psychological shock that accompanies a dramatic change in financial status. Sudden wealth can trigger a cascade of emotions: excitement, guilt, anxiety, and confusion. Recipients may feel overwhelmed by the responsibility of managing their newfound resources, especially if they lack financial literacy or a support system. The windfall can also disrupt one’s sense of identity. Someone who previously lived modestly may struggle to reconcile their new status with their values, relationships, and lifestyle. This identity dissonance can lead to impulsive decisions, such as extravagant spending, quitting a job prematurely, or giving away money without boundaries.

Financial mismanagement is a common consequence of sudden wealth. Without a plan, recipients may fall prey to scams, make poor investments, or underestimate tax obligations. The phenomenon known as “Sudden Wealth Syndrome” describes the psychological stress and behavioral pitfalls that often follow a windfall. Studies show that lottery winners and professional athletes frequently go bankrupt within a few years of receiving large sums. The paradox lies in the fact that the very thing meant to provide freedom—money—can instead create chaos.

***

***

Relationships also suffer under the weight of sudden wealth. Friends and family may treat the recipient differently, leading to feelings of isolation or mistrust. Requests for financial help can strain bonds, and recipients may struggle to set boundaries. The paradox deepens when generosity becomes a source of conflict rather than connection.

Experts like Susan Bradley, founder of the Sudden Money® Institute, emphasize that financial transitions require more than technical advice—they demand emotional intelligence and structured support. Her work highlights the importance of pausing before making major decisions, assembling a transition team of advisors, and creating a personal vision for the money. These steps help recipients align their financial choices with their values and long-term goals.

Ultimately, the Sudden Money Paradox teaches that wealth is not just a numerical asset—it’s a psychological and relational force. Navigating it successfully requires self-awareness, education, and guidance. When approached thoughtfully, sudden money can be a catalyst for growth and purpose. But without preparation, it risks becoming a burden disguised as a blessing.

This paradox challenges society’s assumptions about wealth and reminds us that financial well-being is as much about mindset and meaning as it is about money itself.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Modigliani-Miller Theorem asserts that under ideal market conditions, a firm’s value is unaffected by its capital structure—that is, whether it is financed by debt or equity. This principle revolutionized corporate finance and remains foundational in understanding how firms make financing decisions.

The Modigliani-Miller Theorem (M&M), developed by economists Franco Modigliani and Merton Miller in 1958, is a cornerstone of modern corporate finance. It posits that in a world of perfect capital markets—where there are no taxes, transaction costs, bankruptcy costs, or asymmetric information—the value of a firm is independent of its capital structure. In other words, whether a company is financed through debt, equity, or a mix of both does not affect its overall market value.

The theorem is built on two key propositions. Proposition I states that the total value of a firm is invariant to its financing mix. This implies that investors can replicate any desired capital structure on their own, making the firm’s choice irrelevant. Proposition II addresses the cost of equity: as a firm increases its debt, the risk to equity holders rises, and so does the required return on equity. However, this increase offsets the benefit of cheaper debt, keeping the overall cost of capital constant.

Initially, the M&M Theorem was criticized for its unrealistic assumptions. Real-world markets are far from perfect—companies face taxes, bankruptcy risks, and information asymmetries. Recognizing this, Modigliani and Miller later revised their model to include corporate taxes. In this modified version, they showed that debt financing can create value because interest payments are tax-deductible, effectively reducing a firm’s taxable income and increasing its value.

***

***

Despite its limitations, the M&M Theorem has profound implications. It provides a benchmark for evaluating the impact of financing decisions and helps isolate the effects of market imperfections. For instance, it explains why firms might prefer debt in a tax-heavy environment or avoid it when bankruptcy costs are high. It also underpins the concept of arbitrage in financial markets, suggesting that investors can create homemade leverage to mimic corporate strategies.

In practice, the theorem guides corporate managers, investors, and policymakers. Managers use it to assess whether changes in capital structure will truly enhance shareholder value or merely shift risk. Investors rely on its logic to understand the trade-offs between debt and equity. Policymakers consider its insights when designing tax codes and regulations that influence corporate behavior.

Critics argue that the theorem oversimplifies complex financial realities. Behavioral factors, agency problems, and market frictions often distort the neat predictions of M&M. Nonetheless, its elegance and clarity make it a vital tool for financial analysis. It encourages a disciplined approach to capital structure, reminding decision-makers to focus on fundamentals rather than financial engineering.

In conclusion, the Modigliani-Miller Theorem remains a foundational theory in finance. While its assumptions may not hold in the real world, its core message—that value stems from a firm’s operations, not its financing choices—continues to shape how we think about corporate value and financial strategy.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Retirement planning has evolved significantly over the past several decades, with employers and employees seeking solutions that balance security, flexibility, and predictability. Among the various retirement plan options available today, cash balance plans stand out as a hybrid design that combines features of both traditional defined benefit pensions and defined contribution plans. Their unique structure makes them an attractive choice for employers aiming to provide meaningful retirement benefits while maintaining financial predictability.

At their core, cash balance plans are a type of defined benefit plan. Unlike traditional pensions, which promise retirees a monthly income based on years of service and final salary, cash balance plans define the benefit in terms of a hypothetical account balance. Each participant’s account grows annually through two components: a “pay credit” and an “interest credit.” The pay credit is typically a percentage of the employee’s salary or a flat dollar amount, while the interest credit is either a fixed rate or tied to an index such as U.S. Treasury yields. Although the account is hypothetical—meaning the funds are not actually segregated for each employee—the structure provides participants with a clear, understandable statement of their retirement benefit.

One of the primary advantages of cash balance plans is their transparency. Employees can easily track the growth of their account balance, much like they would with a 401(k). This clarity helps workers better understand the value of their retirement benefits and fosters a sense of ownership. Additionally, cash balance plans are portable: when employees leave a company, they can roll over the vested balance into an IRA or another qualified plan, ensuring continuity in retirement savings.

***

***

From the employer’s perspective, cash balance plans offer several benefits as well. Traditional pensions often create unpredictable liabilities, as they depend on factors such as longevity and investment performance. Cash balance plans, by contrast, provide more predictable costs because the employer commits to specific pay and interest credits. This predictability makes them easier to manage and budget for, particularly in industries where workforce mobility is high. Moreover, cash balance plans can be designed to reward long-term employees while still appealing to younger workers who value portability.

Despite these advantages, cash balance plans are not without challenges. Because they are defined benefit plans, employers bear the investment risk and must ensure the plan is adequately funded. Regulatory requirements, including nondiscrimination testing and funding rules, add complexity and administrative costs. Additionally, while cash balance plans are generally more equitable across generations of workers, transitions from traditional pensions to cash balance designs have sometimes sparked controversy, particularly among older employees who may perceive a reduction in benefits.

In recent years, cash balance plans have gained popularity among professional firms, such as law practices and medical groups, as well as small businesses seeking tax-efficient retirement solutions. These plans allow owners and highly compensated employees to accumulate larger retirement savings than would be possible under defined contribution limits, while still providing benefits to rank-and-file workers. As such, they serve as a valuable tool for both talent retention and financial planning.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Taxation is a cornerstone of modern governance, providing the financial resources necessary for governments to deliver public services, maintain infrastructure, and support social programs. While paying taxes is a legal obligation, individuals and businesses often seek ways to reduce their tax burden. This pursuit gives rise to two distinct concepts: tax avoidance and tax evasion. Though they may sound similar, the difference between them is profound, hinging on legality, ethics, and consequences.

Tax avoidance refers to the use of lawful strategies to minimize tax liability. It involves taking advantage of deductions, exemptions, credits, and other provisions explicitly allowed by tax laws. For example, individuals may contribute to retirement accounts, claim mortgage interest deductions, or invest in tax-free municipal bonds. Businesses may structure operations to benefit from tax incentives or credits designed to encourage innovation, sustainability, or job creation. In essence, tax avoidance is legal tax planning—a way to reduce obligations while staying within the boundaries of the law.

***

***

By contrast, tax evasion is illegal. It involves deliberately misrepresenting or concealing information to avoid paying taxes. Common forms of evasion include underreporting income, overstating deductions, hiding assets offshore, or falsifying records. Unlike avoidance, which is permitted and often encouraged, evasion constitutes fraud against the government. The consequences are severe: individuals and corporations found guilty of tax evasion may face hefty fines, penalties, and even imprisonment.

The distinction between the two lies in compliance versus deception. Tax avoidance complies with the letter of the law, even if it sometimes exploits loopholes. Tax evasion, however, breaks the law outright. This difference is critical not only legally but also ethically. While avoidance is lawful, aggressive avoidance strategies—especially by wealthy individuals or multinational corporations—can raise moral questions. Critics argue that such practices undermine fairness, shifting the tax burden onto ordinary citizens. Governments often respond by reforming tax codes to close loopholes and ensure equity.

Tax evasion, on the other hand, is universally condemned. It erodes trust in the tax system, deprives governments of essential revenue, and places greater strain on compliant taxpayers. Moreover, evasion can damage reputations, leading to loss of credibility and public backlash for businesses or individuals caught engaging in fraudulent practices.

In summary, tax avoidance is legal and strategic, while tax evasion is illegal and punishable. Both aim to reduce tax liability, but they differ fundamentally in method and consequence. Avoidance leverages lawful opportunities provided by tax codes, whereas evasion relies on deception and concealment. Understanding this distinction is vital for taxpayers, as crossing the line from avoidance into evasion can result in serious legal and financial repercussions. Ultimately, responsible tax planning requires not only knowledge of the law but also an awareness of ethical considerations, ensuring that efforts to minimize taxes do not compromise legality or fairness.

The Evolving Landscape of Broker-Dealer Recruitment

Broker-dealer recruitment has become a dynamic and competitive arena within the financial services industry. As firms vie for top talent, the strategies and incentives used to attract and retain financial advisors have evolved significantly. In an environment shaped by regulatory changes, technological innovation, and shifting advisor expectations, broker-dealers must continuously refine their recruitment approaches to remain competitive and relevant.

At the heart of broker-dealer recruitment is the pursuit of experienced financial advisors who bring with them established client relationships and significant assets under management. These advisors are highly sought after because they can generate immediate revenue and enhance a firm’s market presence. According to recent industry reports, firms like LPL Financial, Commonwealth, and Cetera have ramped up their recruitment efforts by investing in platform enhancements, rebranding initiatives, and technology upgrades to appeal to both seasoned professionals and the next generation of advisors.

One of the most significant trends in broker-dealer recruitment is the emphasis on value-added services. Advisors today are not merely looking for the highest payout or signing bonus; they are increasingly drawn to firms that offer robust support systems, including compliance assistance, marketing resources, and advanced technology platforms. Broker-dealers that can demonstrate a commitment to advisor growth and client service excellence are more likely to attract top-tier talent.

The competitive nature of the industry has also led to the rise of aggressive recruitment tactics, including lucrative transition packages and equity offers. While these financial incentives can be effective, they are increasingly being supplemented by strategic differentiators such as flexible affiliation models, access to alternative investment platforms, and opportunities for practice acquisition or succession planning.

Moreover, the recruitment landscape is being reshaped by broader economic and regulatory forces. The implementation of Regulation Best Interest (Reg BI) and the ongoing impact of high interest rates have prompted advisors to reassess their affiliations and seek firms that provide clarity, stability, and strategic guidance. Broker-dealers that proactively address these concerns and offer transparent, advisor-centric solutions are better positioned to succeed in the recruitment race.

In conclusion, broker-dealer recruitment is no longer just about offering the biggest check. It is about creating a compelling value proposition that resonates with advisors’ professional goals and personal values. Firms that invest in technology, culture, and advisor support—while remaining agile in response to industry trends—will be best equipped to attract and retain the talent necessary for long-term success.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Yourmedical practice. Your personal goals. Your financial plan. Our experienced confirmation guide.

***

***

When you know exactly where you are today, have a vision of where you want to be tomorrow, and have trusted counsel at your side, you have already achieved so much success. Marcinko Associates works to keep you at that level of confidence every day. We use a comprehensive economic process to uncover what’s most important to you and then develop a financial strategy that gives you the highest probability of achieving your monetary goals.

We assess, plan, and opine for your success

To accurately see where you are today, chart a strategic path to your goals and help you make the most informed decisions to keep you on financial track, our key services for physicians and high net worth medical clients include:

Investment Portfolio Review

Fee, Charge and Cost Review

Comprehensive Financial Planning

Insurance Reviews

Estate Planning

Investment and Asset Management Second Opinions

We take a deep dive into your financial retirement plans

Physicians and dental employers now have options for how to design and deliver retirement benefits and we can help you make the best choice for your healthcare business. Our services for retirement plans include:

Fee, Charges & Fiduciary Review

Portfolio Analysis

Single Employer Retirement Plan Advisory

Retirement Plans Risk Analysis

Capital Funding and Financing

Business Planning and Practice Valuations

Career Development

and more!

We take a broad and balanced look at your financial life life

We coordinate our recommendations with your other advisors, including attorneys, accountants, insurance professionals and others, to ensure each decision is consistent with your goals and overall strategy. For example, through our partnerships we offer physician colleagues deeper expanded advisory services, like:

In the early 1980s, Daniel Kahneman and Amos Tverskey proved in numerous experiments that the reality of decision making differed greatly from the assumptions held by economists. They published their findings in Prospect Theory: An analysis of decision making under risk, which quickly became one of the most cited papers in all of economics.

To understand the importance of their breakthrough, we first need to take a step back and explain a few things. Up until that point, economists were working under a normative model of decision making. A normative model is a prescriptive approach that concerns itself with how people should make optimal decisions. Basically, if everyone was rational, this is how they should act.

Amanda, an RN client, was just informed by her financial advisor that she needed to re-launch her 403-b retirement plan. Since she was leery about investing, she quietly wondered why she couldn’t DIY. Little does her Financial Advisor know that she doesn’t intend to follow his advice, anyway! So, what went wrong?

The answer may be that her advisor didn’t deploy a behavioral economics framework to support her decision-making. One such framework is the “prospect theory” model that boils client decision-making into a “three step heuristic.”

According to colleague Eugene Schmuckler PhD MBA MEd CTS, Prospect theory makes the unspoken biases that we all have more explicit. By identifying all the background assumptions and preferences that clients [patients] bring to the office, decision-making can be crafted so that everyone [family, doctor and patient] or [FA, client and spouse] is on the same page.

1. Simplify choices by focusing on the key differences between investment [treatment] options such as stock, bonds, cash, and index funds.

2. Understanding that clients [patients] prefer greater certainty when it comes to pursuing financial [health] gains and are willing to accept uncertainty when trying to avoid a loss [illness].

3. Cognitive processes lead clients and patients to overestimate the value of their choices thanks to survivor bias, cognitive dissonance, appeals to authority and hindsight biases.

CITE: Jaan E. Sidorov MD [Harrisburg, PA]

Assessment

Much like in healthcare today, the current mass-customized approaches to the financial services industry fall short of recognizing more personalized advisory approaches like prospect theory and assisted client-centered investment decision-making.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP™

***

***

When Maria needed $400,000 for a down payment on a new home, her broker at a large Wall Street firm offered a solution: “Don’t sell investments and trigger capital gains. Just take out a margin loan.”

A margin loan is a line of credit from a brokerage firm, secured by the client’s investment portfolio. It offers quick access to cash with no immediate tax consequences and minimal paperwork. But the convenience comes at a cost. As of mid-2025, margin loan interest rates range from 6.25% to over 11%.

Margin loan recommendations are often presented by brokers as tax-savvy strategies that allow clients to access “tax-free” cash while keeping their portfolios intact. In many cases, however, the math benefits the advisor more than the investor. The cost of borrowing often exceeds what an investor is likely to earn by holding on.

For example, let’s assume an interest rate of 7.5% on Maria’s $400,000 margin loan. While borrowing delayed the payment of $20,000 in capital gains tax, she will eventually have to pay that tax anyway unless she holds the investments until her death. Two years later, with portfolio returns of 4% annually, she had earned around $32,000 from the $400,000 in investments she might have sold. Meanwhile, she had paid $60,000 in interest—leaving her some $28,000 worse off. That’s without factoring in ongoing interest payments, or the risks of a margin call if the investments securing the loan drop in value.

Why do advisors keep recommending margin loans? Because selling investments reduces the portfolio size and the advisor’s fee. Borrowing keeps the portfolio intact and the compensation unchanged—while the firm receives additional income from interest on the loan. In some cases, advisors suggest using margin loans to buy more investments, increasing both the portfolio and the fee they collect.

None of this is illegal. But when the borrowing cost is higher than expected returns and the advisor benefits financially, the ethics are questionable. The client takes the risk, while the advisor keeps the revenue.

This kind of conflict appears more often in portfolios where compensation is tied to asset volume and the company’s primary culture rewards gathering assets over delivering unbiased advice. By contrast, fee-only financial planning and investment advisors typically operate on simpler hourly, flat, or tiered fee structures. Their compensation doesn’t depend on whether a client borrows, sells, or holds. The culture of the firm focuses on conflict-free advice aligned with the client’s best interest.

Wall Street brokers are often held to a fiduciary standard, but structure still matters. In 2024 the SEC reported their examinations of brokers would continue to focus on advisor recommendations unduly influenced by the company’s compensation and incentives.

There are rare situations where a margin loan may be appropriate. A client with large unrealized gains might use a short-term margin loan to minimize taxes. An elderly investor might borrow tax-free rather than sell assets that will receive a step-up in basis at their death. Even in those cases, the math must be exact and the client must clearly understand the risks, including the possibility of a margin call.

If your advisor recommends a margin loan, especially to buy more investments, ask strong questions. What’s the interest rate? What return is realistic? What are the tax consequences of selling? How does this affect the advisor’s income?

In a high-rate, low-return environment, margin loans rarely favor the client. The exceptions are narrow. The risks are significant. And the conflict of interest is measurable.

Sometimes the smartest move is the simplest: sell what you need, pay the tax, and leave leverage out of your plan.

Also called “qualified” or “statutory” stock options, ISOs are considered tax-advantaged stock options based on U.S. tax law. With ISOs, the spread (the difference between the award price and the fair market value) will count as income for the alternative minimum tax (AMT) in the year you exercise your options.

Example: If you exercise and hold the shares for more than one year past the exercise date and more than two years past the original grant date, the sale of the stock becomes a qualifying disposition, and any realized profit is typically taxed at the long-term capital gains rate. If you sell earlier, the spread will be taxed at your ordinary income tax rate.

ISOs vs. NSOs: What’s the difference?

There are two types of employee stock options: statutory and nonstatutory. They can also be referred to as qualified and nonqualified, respectively. ISOs are statutory (qualified) and differ from nonstatutory (nonqualified) stock options (NSOs) in a few key ways:

Eligibility. ISOs are issued only to employees, whereas NSOs can be granted to outside service providers like advisors, board directors or other consultants. Typically, mainly senior executives or key employees are given ISOs, as a company is not required to offer ISOs to all employees.

Tax perks. ISOs have more compelling tax treatment compared with NSOs.

Bettors are currently able to deduct 100% of their gambling losses, so they only pay taxes on their winnings. But starting next year, only 90% of gambling losses will be deductible.

So, if a professional gambler wins $100,000, then loses $100,000 that same year, according to the New York Times:

In 2025, that gambler would owe taxes on $0.

In 2026, that gambler would owe taxes on $10,000.

Bettors could even end up paying taxes if they finished the year with a net loss.

Posted on May 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP®

***

***

OVER HEARD IN THE FINANCIAl ADVISOR’S LOUNGE

A basic strategy for asset protection is to hold various assets in different entities. Putting real estate, small businesses, and other assets into trusts, corporations, or limited liability companies (LLCs) is effective protection that is relatively easy to put into practice. Not only do I recommend this strategy to clients, I use it myself. Recently, however, I discovered a potential downside.

About 25 years ago, I invested in some rare coins in a corporation I owned and put them into a safe deposit box owned by the corporation. When my business relocated 12 years ago, the safe deposit box billing was not forwarded to the new address and was never paid again. Last year I went to retrieve the coins from the safe deposit box, which I had not visited in 25 years. I discovered the box had been drilled open three years earlier and my collection turned over to the unclaimed property division of the State Treasurer’s office.

I was told getting the coins back would be simple enough. I just needed to verify that I owned the company which owned them by providing the corporation’s tax ID number. However, the corporation no longer existed. I didn’t have a record of its tax ID number. The IRS wouldn’t verify the number without my giving them the address the company had used. That address was a post office box number that I no longer used and couldn’t remember. The state’s position was “no tax ID, no coins.” The only verification of my identity as owner of the corporation was my signature on the bank’s safe deposit box application. Eventually, with the support of bank officers who were willing to swear that I was who I claimed to be, I got my coin collection back. The hassle involved in this process was a reminder of an important component of asset protection. Maintain accurate records so you don’t end up hiding assets from yourself.

***

***

A good start is to create a master file of all the entities that hold your assets. This can be any system that’s easy for you to use: a computer spreadsheet, a set of file folders, or a single paper list. Share it as appropriate with your CPA, attorney, or financial planner. The master list should include the name of each company, its date of incorporation, tax ID number, address, and other relevant information like phone or bank account numbers. Also keep an inventory of the assets each company owns.

Once you’ve created a master list, it’s essential to keep it up to date as you buy or sell assets, close companies, or transfer ownership. Set up a system, as well, to remind yourself of tasks like filing tax returns, completing minutes of annual meetings, and paying the annual safe deposit box rent. Make your record-keeping easier by eliminating unnecessary complications.

For example, you probably don’t need a separate address for each trust, corporation, or LLC. Instead of creating a separate company for each asset, you might consider grouping smaller assets within one entity. I’d suggest first discussing the pros and cons with an attorney or financial planner. For larger assets like real estate, I do recommend holding each one separately.

When I talk to clients about asset protection, I mention that part of the price we pay for it is an increase in paperwork. It’s easy to accept that idea with casual good intentions. The case of my reclaimed coin investment is a good reminder of the importance of keeping up with that paperwork. If we don’t, we might protect ourselves right out of access to our own assets.

Posted on May 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

Markets: After stomach-churning ups and downs this spring, the stock market calmed down last week with all three major indexes holding steady and closing just a bit lower. This week, investors will be glued to the details of the trade agreement with China, an inflation report, and more earnings.

Breaking News Overnight: After talks in Switzerland this weekend, the US and China agreed to a large reduction in tariffs on each other. The US is lowering its tariffs on China from 145% to 30%, while China is lowering its tariffs on the US from 125% to 10%. The new tariff rates will be in effect for 90 days while the two sides continue talking.

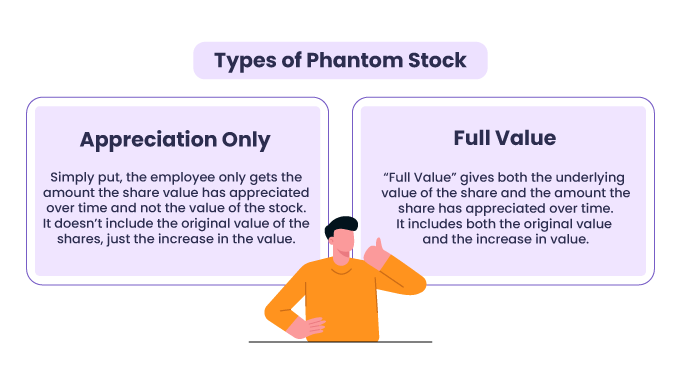

Phantom equity is an increasingly popular tool within businesses, particularly startups and private companies, for incentivizing employees without diluting ownership. It allows firms to reward key personnel by linking compensation to the company’s performance, aligning employee interests with those of shareholders.

Basic Mechanisms of Phantom Equity

Phantom equity operates as a contractual agreement offering employees a simulated stake in the business without issuing actual stock. This arrangement appeals to companies aiming to maintain control over their equity structure while providing performance-based incentives. The benefits mimic stock ownership, such as dividends and capital appreciation, without the complexities of transferring actual shares.