BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

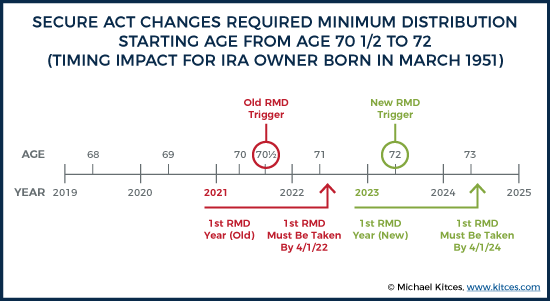

Required Minimum Distributions (RMDs) are mandatory withdrawals from certain retirement accounts that begin at age 73, designed to ensure the IRS collects taxes on previously tax-deferred savings.

Required Minimum Distributions (RMDs) are a critical component of retirement planning in the United States. They represent the minimum amount that retirees must withdraw annually from specific tax-deferred retirement accounts, such as traditional IRAs, 401(k)s, and other qualified plans, once they reach a certain age. As of 2025, individuals must begin taking RMDs at age 73, a change implemented by the SECURE 2.0 Act for those born between 1951 and 1959.

The rationale behind RMDs is rooted in tax policy. Contributions to tax-deferred accounts are made with pre-tax dollars, allowing investments to grow without immediate tax consequences. However, the IRS eventually wants its share. RMDs ensure that retirees begin paying taxes on these funds, preventing indefinite tax deferral. The amount of each RMD is calculated using the account balance at the end of the previous year and a life expectancy factor provided by IRS tables.

Failing to take an RMD can result in steep penalties. Historically, the penalty was 50% of the amount not withdrawn, but recent changes have reduced this to 25%, and potentially 10% if corrected promptly. These penalties underscore the importance of understanding and complying with RMD rules.

Not all retirement accounts are subject to RMDs. Roth IRAs are exempt during the original account holder’s lifetime, and under the SECURE 2.0 Act, Roth 401(k) and Roth 403(b) accounts are also exempt from RMDs while the original owner is alive. However, beneficiaries of these accounts may still face RMD requirements.

***

***

Strategically managing RMDs can help retirees minimize tax impacts and optimize their retirement income. For example, retirees might consider withdrawing more than the minimum in years with lower income to reduce future RMD amounts. Others may choose to convert traditional IRA funds to Roth IRAs before reaching RMD age, thereby reducing future taxable distributions. Additionally, using RMDs to fund charitable donations through Qualified Charitable Distributions (QCDs) can satisfy the RMD requirement while excluding the amount from taxable income.

Timing is also crucial. The first RMD must be taken by April 1 of the year following the year the individual turns 73. Subsequent RMDs must be taken by December 31 each year. Delaying the first RMD can result in two withdrawals in one year, potentially increasing taxable income and affecting Medicare premiums or tax brackets.

In conclusion, RMDs are more than just a tax obligation—they are a planning opportunity. Understanding the rules, calculating the correct amount, and integrating RMDs into a broader retirement strategy can help retirees maintain financial stability and reduce unnecessary tax burdens.

As regulations evolve, staying informed and consulting with financial professionals is essential to make the most of retirement savings.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Yes, you can contribute to both a Roth IRA and a 401(k), provided you don’t exceed annual contribution limits for each account.

Determining whether to contribute to a Roth IRA, 401(k), or both can be an important step in planning for your retirement. Here are the key differences, including tax advantages, employer contributions, and investment options.

Eligibility requirements are the first consideration when contributing to a Roth IRA and a 401(k). For Roth IRA contributions, your eligibility is determined by your income. Specifically, if your modified adjusted gross income (MAGI) exceeds certain thresholds, your ability to contribute to a Roth IRA may be reduced or eliminated. However, there are no income limits for contributing to a 401(k), making it accessible to anyone with earned income.

IRS rules do allow for contributions to both a Roth IRA and a 401(k), provided you adhere to the annual contribution limits for each account.

This means you can take advantage of the higher contribution limits of a 401(k) while also benefiting from the tax-free growth of a Roth IRA. This dual approach can be a strategy for maximizing your retirement savings. The advantages to contributing to both accounts present some key benefits, such as:

Tax diversification in retirement, allowing for better management of taxable income.

Potential reduction of overall tax burden.

Maximization of savings potential by taking full advantage of the benefits each account offers.3

Balancing contributions between a Roth IRA and a 401(k) requires careful planning. You might start by contributing enough to your 401(k) to receive the full employer match, which is essentially free money, if your employer offers this. Once you’ve secured the match, consider maxing out your Roth IRA contributions, if you’re eligible.

If you’re looking at this tab, chances are you are fed up with your financial brokerage accounts, thinking of finances, investing, retirement or all of the above.

And so, we can help

An investment portfolio second opinion, also called a “ portfolio review,” is an analysis of your financial holdings and associated strategies, allocations, fees and performance to determine whether the most effective instruments and methodologies are being utilized to reach your goals.

No Worries! You may have come to the right place.

E-Mail Ann Miller RN MHA CPHQ for an Initial Appointment: MarcinkoAdvisors@outlook.com

The purpose of this initial appointment is for you to ask a lot of questions to make sure you are comfortable with potentially working with us. It also helps if you are prepared to provide a verbal summary of your current situation.

Here are some questions to consider asking us during your first meeting:

1) Can you tell us about your financial qualifications, experience, education and training; if any?

2) Can you provide some information about your current financial advisory team?

3) On what type of investments do you typically purchase and own?

5) How much do pay your financial management firm?

6) How long have you been working with your current financial management firm?

8) What other services does your financial team provide?

An annuity is a contract between you and an insurance company. When you purchase an annuity, you make a lump-sum contribution or a series of contributions, generally each month. In return, the insurance company makes periodic payments to you beginning immediately or at a pre-determined date in the future. These periodic payments may last for a finite period, such as 20 years, or an indefinite period, such as until both you and your spouse are deceased. Annuities may also include a death benefit that will pay your beneficiary a specified minimum amount, such as the total amount of your contributions.

The growth of earnings in your annuity is typically tax-deferred; this could be beneficial as you may be in a lower tax bracket when you begin taking distributions from the annuity.

Warning: A word of caution: Annuities are intended as long-term investments. If you withdraw your money early from an annuity, you may pay substantial surrender charges to the insurance company as well as tax penalties to the IRS and state.

***

***

There are three basic types of annuities — fixed, indexed, and variable

1. With a fixed annuity, the insurance company agrees to pay you no less than a specified (fixed) rate of interest during the time that your account is growing. The insurance company also agrees that the periodic payments will be a specified (fixed) amount per dollar in your account.

2. With an indexed annuity, your return is based on changes in an index, such as the S&P. Indexed annuity contracts also state that the contract value will be no less than a specified minimum, regardless of index performance.

3. A variable annuity allows you to choose from among a range of different investment options, typically mutual funds. The rate of return and the amount of the periodic payments you eventually receive will vary depending on the performance of the investment options you select.

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

WARNING – WARNING

By Staff Reporters

***

***

A “retirement account scam” is a type of online fraud that occurs when a third party administrator (TPA) for retirement investment accounts is tricked into authorizing a money distribution to an imposter posing as the true account holder.

The imposter often starts the scam by calling the TPA, identifying himself or herself as an actual account holder, and requesting a withdrawal distribution form. Once the imposter receives the withdrawal distribution form, the imposter returns the completed form to the TPA. The form is completed with the account holder’s real personal identifying information (PII)—often stolen via schemes, data breaches, and other hacking offenses—and bank account information for an account controlled by the imposter or the imposter’s conspirators.

***

***

After the TPA processes the fraudulent request, the request is forwarded to the investment firm responsible for managing the account holder’s investments, and the funds—often the account holder’s life savings—are then directed to the imposter’s designated bank account.

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Why would a doctor consider a Roth IRA conversion?

By Staff Reporters

***

***

A Roth conversion involves transferring funds from a traditional retirement account—such as a 401(k), 403(b), or individual retirement account (IRA) funded with pre-tax dollars—into a Roth IRA.

The biggest benefit lies in the tax treatment of the converted funds. Once the funds are in the Roth IRA, future growth of those assets is tax-free. Withdrawals in retirement are also tax-free, assuming they meet certain criteria. As with any strategy, there are important considerations to keep in mind.

When you convert funds to a Roth IRA, the amount converted is taxable income in that tax year. For example, if you convert $100,000 from a traditional IRA to a Roth IRA, that $100,000 will be added to your taxable income in the conversion year.

Converting large amounts can result in a significant tax bill and may push you into a higher tax bracket. Even so, using retirement funds to pay taxes may make sense for those looking to convert large IRAs to reduce their future required minimum distributions (RMDs).

The timing of your Roth conversion matters too. Generally, it’s a good idea to convert when your income is lower—for example, after you’ve retired and before you begin drawing Social Security. You may also choose to convert over the course of several years to spread out the tax impacts. But if you can get comfortable with these considerations, a Roth conversion can provide you with benefits beyond tax-free growth and withdrawals.

Some of these benefits are:

Tax diversification. Having both traditional and Roth accounts allows you to manage your tax liability in retirement. For example, if your income in a given year is higher than expected, you can withdraw from the Roth IRA without increasing your taxable income.

No RMDs. Traditional IRAs and 401(k)s require you to begin taking RMDs at age 73. Roth IRAs have no RMD requirement during your lifetime. With a Roth account, you have more control over your retirement withdrawals and can leave the funds to grow for your heirs.

Benefits for heirs. Roth IRAs can be passed on to beneficiaries, who can inherit the account income tax-free. This means your heirs can enjoy the tax-free growth and withdrawals if the Roth IRA has been held for five years or more—a significant advantage, especially if your beneficiaries are in a higher tax bracket.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

QUESTION:Can I invest my Individual Retirement Account [IRA] in a Hedge Fund?

This is up to the manager, but there is no legal restriction on a hedge fund accepting individual retirement account (IRA) assets. IRA accounts are not well suited for funds that make extensive use of leverage, however. In such cases, the fund is likely to generate significant amounts of unrelated business taxable income (UBTI) – profits of the fund attributable to the use of leverage. The holder of an IRA account must pay taxes on UBTI, even if the UBTI was generated in an IRA account.

But, today’s hedge funds may or may not use leverage. Many hedge funds are not hedged at all, but rather are just specialized versions of regular long stock portfolios. If such funds do not use much leverage, IRA investors will not encounter much difficulty with UBTI and should not hesitate in considering these funds.

In considering whether to accept IRA money, hedge fund managers must consider several factors. If the only type of retirement money accepted by the hedge funds is IRA money, then the manager has no limit on how much retirement money the fund can accept. If, however, there are other types of retirement money invested in the fund, such as pension funds, IRA money will be counted towards a total of 25 percent of fund assets that can be invested in retirement accounts before the fund becomes subject to the Employment Retirement Income Security Act of 1974 (ERISA). Funds subject to ERISA regulations face a heavy administrative burden and more restrictions than most fund managers like.

Finally, IRA distributions from a hedge fund are subject to the standard 20 percent withholding unless the funds are directly rolled over to other qualified plans.

Posted on January 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The U.S. Department of Labor reported a 0.4% increase in the monthly CPI after seasonal adjustment, overshooting the forecast of 0.3% and the previous value of 0.3%. On an annual basis, inflation climbed to 2.9%, up from 2.7% in November, the highest rate since July 2024.

US stocks ripped higher on Wednesday as high hopes for bank earnings paid off and a crucial consumer inflation update showed key prices increased less than expected in December.

The benchmark S&P 500 (^GSPC) popped more than 1.8%, while the Dow Jones Industrial Average (^DJI) rose more than 1.6%, or over 700 points. Meanwhile, the tech-heavy NASDAQ Composite (^IXIC) soared 2.5%.

Stocks took a leg higher after the Consumer Price Index (CPI) showed progress toward the Fed’s 2% inflation target in December. Prices climbed 0.2% month-on-month on a “core” basis, which strips out the more volatile costs of food and gas, an easing from November’s 0.3% gain. Over last year, core CPI rose 3.2%.

Capital One is being sued by the US government’s consumer watchdog agency for “cheating millions of consumers” and not paying more than $2 billion in interest to holders of its high-interest savings accounts.

As of January 1st 2025, beneficiaries enrolled in Part D prescription drug plans will have their out-of-pocket spending capped at $2,000 for the year. This new policy was part of President Joe Biden’s 2022 Inflation Reduction Act (IRA), which included other drug pricing measures such as capping the cost of insulin at $35 per month for seniors.

But only a small share of Medicare enrollees will benefit from the cap, according to an analysis from nonprofit organization AARP’s Public Policy Institute, as most don’t spend more than $2,000 annually on their medications after hitting their deductible (which is up to $590 for standard plans in 2025). Beneficiaries spent an average of $400 to $500 per year as of 2022, the Hill reported, citing data from the US Department of Health and Human Services (HHS).

It’s good to have money stashed in the stock market when the market is doing well. The number of people with at least $1 million in their 401(k) and IRA accounts jumped 12% in the second quarter 2024, according to a report from Fidelity Investments, largely tracking the market’s gain during that period. It’s the third straight quarter of growth in $1+ million accounts and close to a record high.

But start saving now, because building a hard-boiled nest egg through retirement accounts takes time: The average age of a 401(k) millionaire is 59, Fidelity said.

Posted on September 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

All U.S. and Canadian markets will be closed in observance of Labor/Labour Day.

There will be no Pre-Market or After Hours trading sessions.

Any trades placed on Friday, August 30, 2024, will settle on Tuesday, September 3, 2024.

Requests to move money (MoneyLink, wire transfers, check requests, and IRA distributions) received after the standard cut-off times on Friday, August 30, 2024, will not be processed until Tuesday, September 3, 2024.

Posted on July 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The S&P 500 broke above 5,500 yesterday and stayed there for the first time in market history, notching yet another all-time high for the index—its 32nd this year alone. With so much bullishness it’s understandable that investors may be wondering if we’re at the top yet, but chartists suggests gains tend to beget gains. The bulls have too much momentum to stop now—and if/when the FOMC cuts rates later this year, it seems likely that we’ll see more all-time highs in 2024? Any thoughts.

The Biden administration has awarded $206.3 million of funding to clinician training programs across 42 universities and provider organizations to bolster the nation’s geriatrics care workforce. Programs will be able to integrate geriatrics training into primary care and will work to educate older adults’ families on their care needs. Health and Human Services, in its announcement, noted that primary care providers are a crucial source of care for much of the aging population.

As Walmart shutters its primary care clinics, the retail giant inked a deal to sell its MeMD telehealth business to health tech startup Fabric. Fabric provides a telemedicine platform for a range of customers, including provider groups, with the goal of improving the clinician and patient experience, as well as operational efficiency. The acquisition will expand its provider network, add virtual behavioral health to the company’s services and build on Fabric’s employer and payer solutions.

And…The U.S. Supreme Court has overturned the Chevron deference, stripping power from federal agencies to interpret and enforce regulations. Courts no longerhave to defer to reasonable agency interpretations. One healthcare attorney told Fierce Healthcare he predicts the Centers for Medicare & Medicaid Services will be under a microscope from the courts going forward, and there will be more scrutiny towards provider reimbursement cuts, drug pricing regulation and the Inflation Reduction Act.

The S&P 500 index®(SPX)rose 28.01 points (0.51%) to 5,537.02; the Dow Jones Industrial Average® ($DJI) fell 23.85 points (-0.1%) to 39,308.00; the NASDAQ Composite® ($COMP) gained 159.54 points (0.9%) to 18,188.30.

The 10-year Treasury note yield (TNX) dropped seven basis points to 4.36%.

The CBOE Volatility Index® (VIX) held steady at 12.09.

What’s up

Tesla rose yet another 6.54% as investors continue to celebrate stronger-than-expected delivery numbers. Much like the company’s self-driving mode, this stock can’t stop.

Nvidia rose 4.57%, with the bulls seemingly beating profit-taking bears heading into the holiday.

MGM Resorts popped 2.24% after BTIG analysts gave the company a “buy” rating and a price target 20% higher than shares trade for today.

Quest Diagnostics rose 3.11% after announcing it will acquire fellow laboratory service provider LifeLabs for $985 million.

What’s down

First Foundation plummeted 23.81% after the bank announced it will raise $225 million to shore up a balance sheet burdened by commercial real estate loans.

Constellation Brands fell 3.76% after the alcoholic beverage maker reported stronger than expected earnings but missed Wall Street’s expectations on revenue.

Simulations Plus slid 14.87% after it reported strong third-quarter earnings but announced it’s cutting its dividend.

CureVac popped then dropped 6.59% after GSKbought the rights to the smaller pharma company’s Covid-19 and flu vaccines for $1.6 billion.

Posted on May 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Don’t Leave Yourself Unprotected

By Nicholas Efthemis CFP®

The largest concern facing physicians today is how to protect their wealth against the proliferation of malpractice claims and extraordinarily high jury verdicts. Malpractice insurance has become so expensive that physicians are greatly reducing their coverage.

Even worse, some carriers are dropping physicians that have poor claims history. When meeting with physicians my message is a simple one. Take action and do so now. Constructing a complete asset protection plan is the single most critical step towards attaining financial freedom. Physicians work hard and long hours to create wealth, and are potentially one medical malpractice claim or general negligence claim away from financial catastrophe. Detailing every asset protection strategy is beyond the scope of this article, however I will review some important concepts you should know.

Good asset protection will prevent lawsuits. Conversely, the more personal assets that remain unprotected the more likely an attorney is willing to go after you. In fact, a physician with very high malpractice coverage and unprotected assets has a target on his back. This can be avoided through lower policy limits and a complete Asset Protection Plan.

What is the Best Asset Protection Plan?

The best Asset Protection Plan for a physician or any high net worth client removes all assets from the client’s name. The worst plan has all the assets in the client’s name. You will need to work with a specialized attorney to find the ideal plan for you. In many cases your largest asset are the funds in your retirement plan or IRA. The good news is that creditors cannot reach ERISA qualified plan assets. Common ERISA plans include:

1. 401(k) 403(b) Plan

2. Profit Purchase Plan

3. Money Purchase Plan

4. New Comparability Plans

5. Defined Benefit Plan

Keep in mind IRAs are not considered ERISA qualified plans and have no federal protection from creditors. Many individual states have protected IRAs in part or in full. In my state, New York, IRAs are fully protected. If you live in a state where they are not you should seriously consider moving the money into an ERISA qualified plan. This can be accomplished even if you are retired.

What about my house?

It is never a good idea, from an asset protection standpoint to own property in just your name. If you get sued the property is almost entirely at risk. Owning the marital home jointly with your spouse can be effective. You will protect the home from each other’s individual creditors (though not joint creditors). You should not title many assets as tenants by the entirety for several reasons. Physicians suffer a higher divorce rate than the already high national average of fifty percent. Should a divorce occur you will have ensured the spouse will receive half of that asset. Also, you do nothing to protect the asset against joint creditors.

How should my other assets be held?

You will need to consult a specialized asset protection attorney. Most effective plans involve the use of a corporate structure, limited liability company, or family limited partnership. Keep in mind that the entity you choose will have its own unique asset protection and tax consequences.

Sole proprietorships and partnerships are the worst way to own a business. If a sole proprietor is found negligent in his duties for the business that injures a third person, the sole proprietor is personally liable. If a product or employee harm a third person or someone is harmed on the premises, the sole proprietor is personally liable. With a partnership you have all of the above risks coupled with a partner who can cause you even more liability.

Limited Liability Companies (LLCs), Family Limited Liability Companies (FLLCs) and Family Limited Partnerships (FLPs) are the most commonly used tools by asset protection specialists today. A creditor attempting to obtain assets of a debtor when the assets are in a LLC will likely have very limited success. In fact, a charging order is the only remedy a court can give a creditor. A charging order does not allow creditors to sell assets of the LLC or force distributions of income. It also cannot transfer interest in the LLC to the creditor. A creditor who obtains a charging order against an LLC may in fact receive a K-1 for income they never did and may never receive.

What should I consider holding in an LLC?

I advise my physician clients to consider holding rental real estate, after tax investment accounts, planes, boats and any personal assets of value in an LLC. Unless you are single and your home is titled in your name alone, the marital home may not be a good candidate for transfer to an LLC. By doing so, you forego the capital gains exemption of $250,000 per spouse. Brokerage accounts can be owned by an LLC, and when constructed correctly you will have full ability to invest as you desire. The investments within the account would then be protected. Assets such as planes and boats may be best held in their own LLCs to protect the rest of your estate from their unique risk profiles.

Example:

Personal Residence $750,000 Tenants by the entirety

Vacation Property $300,000 LLC #1

Investment Account $900,000 LLC #1

401 (k) 2,400,000 ERISA plans are federally protected

Boat $55,000 LLC #2

Assessment

The topic of asset protection is vast and complicated, but I hope to break out additional topics such as off-shoring, accounts receivable leveraging, fiduciary duties, and insurance in subsequent articles. My hope is that I have given you enough ideas and motivation to act now. You cannot wait until there is an issue. It is critical that your financial planner, attorney and accountant are all very knowledgeable on asset protection. Do not rely on a generalist to navigate such a complex yet critical issue.

About the Author:

Nicholas Efthemis is a Certified Financial Planner™ who helps physicians plan wisely and live fully by creating a financial plan that helps them focus on their medical practice and live a better life.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

***

***

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on April 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stat: 740. That’s how many employees Nike will lay off at its Oregon HQ before the end of June. In February, Nike CEO John Donahoe informed employees of the company’s plan to reduce 2% of its workforce, which would mean around 1,600 employees in total. (USA Today)

Let’s say you leave your job at any time during or after the calendar year you turn 55 (or age 50 if you’re a public safety employee with a government defined-benefit plan). Under a little-known separation-of-service provision, often referred to as the “rule of 55,” you may be able take distributions (though some plans may allow only one lump-sum withdrawal) from your 401(k), 403(b), or other qualified retirement planfree of the usual 10% early-withdrawal penalties. However, be aware that you’ll still owe ordinary income taxes on the amount distributed. This exception applies only to the plan (including any consolidated accounts) that you were contributing to when you separated from service. It does not extend to IRAs.

The S&P 500 index rose 59.95 points (1.2%) to 5,070.55; the Dow Jones Industrial Average gained 263.71 points (0.7%) to 38,503.69; the NASDAQ Composite® ($COMP) surged 245.33 points (1.6%) to 15,696.64.

The 10-year Treasury note yield (TNX) decreased about 2 basis points to 4.602%.

The CBOE Volatility Index® (VIX) fell 1.25 to 15.69.

Similar to Monday, chipmakers were among the market’s strongest areas, carrying the Philadelphia Semiconductor Index (SOX) to a 2.2% advance. Retailers and communication services shares were also strong. The Dow Jones Utility Index ($DJU) gained for the fifth straight day and ended at its highest level in over three months. The Russell 2000® Index (RUT) surged nearly 2%.

Posted on September 13, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

REMINDER

***

***

Starting in 2026, high-income earners over the age of 50 who make more than $145,000 can no longer make catch-up contributions to regular 401(k)s. Instead, those catch-ups will head to Roth accounts. That carries significant tax implications.

Here is where the major benchmarks ended yesterday:

The S&P 500® Index (SPX) was down 25.56 points (0.6%) at 4,461.90; the Dow Jones Industrial Average (DJIA) was down 17.73 points at 34,645.99; the NASDAQ Composite was down 144.28 points (1.0%) at 13,773.61.

The 10-year Treasury note yield (TNX) was down about 2 basis points at 4.272%.

CBOE’s Volatility Index (VIX) was up 0.42 at 14.22.

While tech was the weakest performing sector Tuesday, consumer discretionary and communication services shares were also lower. Energy shares led sector gainers Tuesday as oil prices continued to rise.

The Philadelphia Oil Service Index (OSX) gained more than 2% and ended at its highest level since April 2019. WTI crude futures, the U.S. benchmark, extended gains to near $90 a barrel after OPEC, in a report, slightly increased its forecasts for global consumption in 2023 and 2024.

Posted on August 30, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

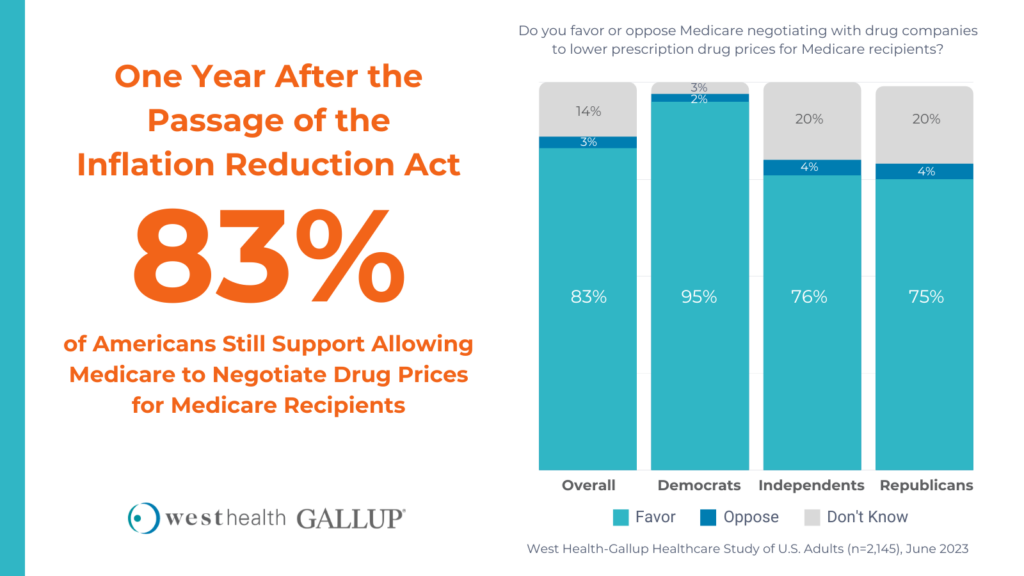

President Joe Biden’s signature Inflation Reduction Act (IRA), signed into law last year, allows the Medicare health program for Americans aged 65 and over to negotiate prices for some of its most costly drugs.

Medicines on the list include Merck & Co’s diabetes drug Januvia, Eliquis rival Xarelto from Johnson & Johnson, and AbbVie’s leukemia treatment Imbruvica. Other drugs on the list include Amgen’s rheumatoid arthritis drug Enbrel, Boehringer Ingelheim and Eli Lilly’s diabetes drug Jardiance, J&J’s arthritis and Crohn’s disease medicine Stelara and insulin from Novo Nordisk.

***

Here is where the major benchmarks ended:

The S&P 500® Index (SPX) was up 64.32 points (1.5%) at 4,497.63; the Dow Jones Industrial Average (DJIA) was up 292.69 points (0.9%) at 34,852.67; the NASDAQ Composite was up 238.63 points (1.7%) at 13,943.76.

The 10-year Treasury note yield (TNX) was down about 10 basis points at 4.112%.

CBOE’s Volatility Index (VIX) was down 0.62 at 14.46.

Technology, Communications Services and Retail shares were among the market’s strongest performers Tuesday. Energy stocks also climbed behind continued strength in crude oil futures, which closed at a two-week high.

The U.S. Dollar Index (DXY) fell along with expectations that interest rates will remain elevated.

Posted on August 4, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Internal Revenue Service is allowing people who inherited an individual retirement account after 2019 to skip a required minimum distribution [RMD] this year, but most still must empty the account within 10 years. The IRS issued the new guidance last week.

There has been confusion surrounding the rules for inherited IRAs ever since the Secure Act of 2019 eliminated the so-called “stretch IRA” for most non-spouse beneficiaries. The old rules had allowed beneficiaries of inherited IRAs to stretch their required minimum distributions over their own lifetimes, permitting decades of tax-free or tax-deferred growth in some cases.

Under the Secure Act of 2019, most non-spouse beneficiaries must now empty their inherited IRA by the end of the 10th year following the original owner’s death. When the law was first passed, experts interpreted it to mean that all the money could be withdrawn in year 10 if so desired, said Ed Slott, CPA and founder of IRAHelp.com

Yet in early 2022, the IRS proposed stricter rules that would apply to someone who inherited an IRA from a person who had already begun taking RMDs; in that case, the recipient must continue taking distributions on an annual schedule. In other words, if the RMD tap had already been turned on, Slott said, it couldn’t be turned off following the original owner’s death, and beneficiaries had to keep withdrawing every year and paying income tax on the amount withdrawn.

Posted on April 17, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

A LAST MINUTE REMINDER

By Staff Reporters

***

***

Tax Day arrives Tuesday, April 18, 2023 as America’s small businesses are worried their own government will treat them like suspected criminals, even as they hire workers, raise wages and strengthen their communities. And, do not forget that Monday the 17th is the last day deadline for 2022 IRA and HSA contributions.

***

G-7 holds its annual summit in Japan. Ministers from the Group of Seven countries have arrived at a Japanese hot spring resort town for a rejuvenating soak and to discuss the world’s most pressing geopolitical challenges, such as China’s aggression toward Taiwan, the war in Ukraine, and climate change. Japan has ramped up security after an apparent smoke bomb was thrown at the prime minister on Saturday.

More companies report earnings. Investors will be poring over reports from Tesla, Netflix, Bank of America, Goldman Sachs, American Express, and dozens of other firms this week for clues on how corporate America is faring in these confusing economic times.

Posted on January 7, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

New medicines launched by US drug makers reached a median price of $222,003 last year, according to Reuters. These astronomical prices were fueled by three very-expensive gene therapies approved by the FDA. In fact, one of them, from Hemgenix, costs $3.5 million, making it the most expensive drug ever.

Congress did cap annual drug price increases via the Inflation Reduction Act, but that doesn’t cover the cost of new medications. Drug-makers, meanwhile, say the cost of their drugs doesn’t reflect what patients pay out-of-pocket for them.

A Required Minimum Distribution (RMD) is an amount of money the IRS requires you to withdraw from most retirement accounts, beginning at age 72. Due to the Coronavirus Aid, Relief, and Economic Security (CARES) Act, RMDs were not required in 2020, but RMDs are required in 2021 and each year after. RMDs can be an important part of your retirement income strategy.

Posted on October 2, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Most likely to have an identity crisis: The Inflation Reduction Act

After a seemingly endless will-they-or-won’t-they make a deal dance, Democrats passed their signature piece of legislation, the Inflation Reduction Act, without Republican support.

The 755-page climate, tax, and healthcare package does a lot of things: It establishes a 15% minimum tax on megacorporations, boosts funding for the IRS, allows Medicare to negotiate prescription drug prices, offers $260 billion in tax credits for renewable energy projects, and more. One thing it likely won’t do: reduce inflation. Despite the name, the law’s impact on rising prices through 2023 is expected to be “negligible.”

On August 16, 2022, one week after Congress passed the Inflation Reduction Act of 2022 (IRA), President Joseph Biden signed the bill into law. The broad bill, which covers healthcare, taxes, and climate change, had been passed around Congress in assorted versions with varying support for months, but under the specter of a record 40-year-high inflation rate, congressional Democrats ultimately came together to pass the IRA; no Republicans voted for the bill.

The IRA aims, among other things, to fight against ever-increasing healthcare costs, by lowering prescription drug prices and extending federal health insurance subsidies. (Read more…)

Posted on August 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The US Senate passed their climate, health and tax package, including nearly $80 billion in funding for the IRS.

The Inflation Reduction Act allocates $79.6 billion to the agency over the next 10 years, with more than half of the money going to enforcement, with the IRS aiming to collect more from corporate and high-net-worth tax dodgers.

The remainder of the funding is earmarked for operations, taxpayer services, technology, development of a direct free e-file system and more. Collectively, those improvements are projected to bring in $203.7 billion in revenue from 2022 to 2031, according to recent estimates from the Congressional Budget Office.

The biggest revenue-raiser of the IRA is a 15% minimum tax on corporations with profits of $1 billion or more, which is expected to generate $258 billion over 10 years. This addresses the problem of the rampant tax dodging among large companies that has mostly benefited wealthy shareholders and executives. The bill includes a 1% excise tax on companies’ stock buybacks, raising an estimated additional $74 billion. This will discourage corporations from siphoning resources into share repurchases that largely benefit shareholders and executives with stock-based pay. Those resources could instead go toward worker wages or other productive investments. And the bill would boost IRS enforcement to ensure the ultra-rich pay.

Finally, the Inflation Reduction Act would also extend a tax limitation on pass-through businesses for two more years. The limitation on how businesses can use losses to reduce taxes is supposed to expire at the start of 2027. A pass-through or flow-through business is one that reports its income on the tax returns of its owners. That income is taxed at their individual income tax rates. Examples of pass-throughs include sole proprietorships, some limited liability companies, partnerships and S-corporations.

Posted on May 4, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

In this podcast, host Dara Albright and guest, Eric Satz, Founder and CEO of Alto IRA, discuss how modern Self-Directed IRAs (SDIRAs) are democratizing retirement planning by providing all Americans with the ability to add non-correlated alternative asset classes to tax-advantaged accounts.

The single greatest – and free – investment tool is also disclosed.

***

Discussion highlights include:

How SDIRAs offer wealth building opportunities for “not-yet accredited investors”;

How SDIRAs have evolved to accommodate micro-sized alternative investments;

Why alternative assets belong in retirement vehicles;

Three reasons most retirement savers are underweighted in non-correlated assets;

Trading cryptocurrencies without tax consequences;

Why RIAs are looking to ALTO for clients’ crypto allocation;

Whether you do contract work or have your own small business, tax deductions for the self-employed physician consultant and/or medical executive or nurse consultant, etc., can add up to substantial tax savings.

With self-employment comes freedom, responsibility, and a lot of expense. While most self-employed people celebrate the first two, they cringe at the latter, especially at tax time. They might not be aware of some of the tax write-offs to which they are entitled.

When it comes time to file your returns, don’t hesitate to claim the benefits you get for being the boss. As a self-employed success story, you’ve earned them.

FORM 1099NEC: Form 1099 NEC is one of several IRS tax forms used in the United States to prepare and file an information return to report various types of income other than wages, salaries, and tips. The term information return is used in contrast to the term tax return although the latter term is sometimes used colloquially to describe both kinds of returns.

“Many times an overlooked deduction is educational expenses. If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Individual Retirement Plans (IRAs)

One of the best tax write-offs for the self-employed physician consultant is a retirement plan. A person with no employees can set up an individual 401 (k). “You can contribute $19,500 in 2021 as a 401(k) deferral, plus 25 percent of net income.”

If you have employees, consider a SIMPLE (Savings Incentive Match Plan for Employees) IRA—an IRA-based plan that gives small employers a simplified method to make contributions to their employees’ retirement. As of 2021, an employee may defer up to $13,500 and employees over 50 may contribute an additional $3,000.

“A third retirement plan is Simplified Employee Pension IRA (SEP IRA).” The employer may contribute the lesser of 25 percent of income or $58,000 in 2021. If the employer has eligible employees, an equal percentage of their income must be contributed.

Recall that retirement plans are “absolutely the No. 1 tax deduction. The government is helping fund retirement.”

Business use of home or dwelling

Now, most self-employed taxpayers’ businesses start as home-based businesses. These people need to know portions of business costs are deductible and so “It is very important that you keep track of expenses relating to your housing costs.”

If your gross income from your business exceeds your total expenses, then you can deduct all of your expenses related to the business use of your home. If your gross income is less than your total expenses, your deduction will be limited to the difference between your gross income and the sum of all business expenses you would pay if the business was not in your home. Those expenses could include telephone lines, the Internet, and other costs to do business.

You must also have a home office that is truly used for work and the Internal Revenue Service may require you to document this.

***

Deducting automobile expenses

If you travel for business, even short distances within your own city, you may deduct the dollar value of business miles traveled on your tax return. The taxpayer may file the actual expense s/he incurred, or use the standard mileage rate prescribed by the IRS, which is 56 cents as of 2021. The IRS allowable mileage rates should be checked every year as they can change.

“If you decide to use actual car expenses, be sure to include payments, depreciation, registration, insurance, garage rent, licenses, repairs and maintenance, and parking and toll fees.” AND, “If you decide to use the standard mileage rate, it would be in your best interest to keep a log—daily, weekly or monthly—of miles driven to distinguish personal use from business use.”

Depreciation of property and equipment

Some self-employed people may purchase property and equipment for a business. If they expect that property to last longer than one year, it should be depreciated on the tax return.

Claims regarding property, according to the IRS, must meet the following criteria: You must own the property and it must be used or held to generate income. The property should have an estimated useful life, meaning you should be able to guess how long you can generate income with it. It may not have a useful life of one year or less, and may not be purchased and disposed of in the same year.

Certain repairs on property used for business may also be deducted.

Educational expenses

Any educational expense is potentially tax-deductible.

“Many times an overlooked deduction is educational expenses. “If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Think about any books, web courses, local college courses, or other classes or materials that you have purchased to improve your job or business. It’s easy to forget a work-related webinar or business e-book that was purchased online, so remember to save e-receipts.

Also recall that subscriptions to trade or professional publications and donations to business organizations, both of which are frequently necessary for the continuation and growth of your business.

Other areas to explore

Other deductions that can be easily missed are advertising and promotional expenses, banking fees, and air, bus, or train fare. Restaurant meals and other entertainment costs may be written off as long as they are necessary business expenses.

And, consider health insurance premiums, which in most cases represent a credit rather than a tax deduction. “A credit goes directly against one’s taxes, rather than a reduction of income.”

Regardless of which expenses you discover that you may write off, the most important thing is to keep accurate records throughout the year. Save receipts, including e-mail receipts, and file or log them so you have easy access to them at tax time. Not only does keeping receipts, mileage logs, and other expense records make filing taxes easier, but it also facilitates a system that allows you to track changes from year to year.

***

Long-term tax-saving strategies

Don’t just look at last-minute write-offs when considering self-employment tax deductions. Think about laying down some long-term strategies for money savings from year to year—particularly if you are a high earner.

“Accountants typically tell you what you have to pay but they don’t always tell you strategies to reduce your payments.”

To reduce your gross taxable income, consider setting up a defined-benefit pension plan. This plan is based on your age and income: The older you are and the higher your earnings, the more you are allowed to contribute. An alternative plan is an age-weighted profit-sharing plan, which is similar and can benefit those who have several employees.

Another strategy for high-earning business owners who own their own building through a limited liability company or similar business structure is to pay themselves rent. This rent is used to pay down the mortgage, but it is also considered a business expense for tax purposes.

Self-employed professionals required to have liability insurance should consider setting up their own insurance company. A captive insurance company is one that insures the risks of the business—or businesses, in the case of a cooperative. Its premiums can be tax-deductible.

But, if money accumulates and claims are minimal, the money taken out is taxable under capital gains. This is not a retirement strategy, but that it can save you money by allowing you to “pay yourself” instead of an insurance company and still deduct the premiums.

Assessment

With any of these more complicated, long-term strategies, consult with a business attorney, CPA/EA or financial planner to ensure you have the best plan possible for your business.

Here are eight things to keep in mind as you prepare to file your 2021 taxes.

1. Income tax brackets have shifted a bit

There are still seven tax rates, but the income ranges (tax brackets) for each rate have shifted slightly to account for inflation. For 2021, the following rates and income ranges apply:

Tax rate

Taxable income brackets:Single filers

Taxable income brackets:Married couples filing jointly (and qualifying widows or widowers)

10%

$0 to $9,950

$0 to $19,900

12%

$9,951 to $40,525

$19,901 to $81,050

22%

$40,526 to $86,375

$81,051 to $172,750

24%

$86,376 to $164,925

$172,751 to $329,850

32%

$164,926 to $209,425

$329,851 to $418,850

35%

$209,426 to $523,600

$418,851 to $628,300

37%

$523,601 or more

$628,301 or more

Source: Internal Revenue Service

2. The standard deduction has increased slightly

After an inflation adjustment, the 2021 standard deduction has increased slightly to $12,550 for single filers and married couples filing separately and $18,800 for single heads of household, who are generally unmarried with one or more dependents. For married couples filing jointly, the standard deduction has risen to $25,100.

3. Itemized deductions remain the same

For most filers, taking the higher standard deduction is more practical and saves the hassle of keeping track of receipts. But if you have enough tax-deductible expenses, you might benefit from itemizing.

The following rules for itemized deductions haven’t changed much for 2021, but they’re still worth pointing out.

State and local taxes: The deduction for state and local income taxes, property taxes, and real estate taxes is capped at $10,000.

Mortgage interest deduction: The mortgage interest deduction is limited to $750,000 of indebtedness. But people who had $1,000,000 of home mortgage debt before December 16, 2017, will still be able to deduct the interest on that loan.

Medical expenses: Only medical expenses that exceed 7.5% of adjusted gross income (AGI) can be deducted in 2021.

Charitable donations: The cash donation limit of 100% of AGI remains in place for 2021, if donations were made to operating charities.1

Miscellaneous deductions: No miscellaneous itemized deductions are allowed.

4. IRA and 401(k) contribution limits remain the same

The traditional IRA and Roth contribution limits in 2021 remain the same as in 2020. Individuals can contribute up to $6,000 to an IRA, and those age 50 and older also qualify to make an additional $1,000 catch-up contribution. If you’re able to max out your IRA, consider doing so—you may qualify to deduct some or all of your contribution.

The 2021 contribution limit for 401(k) accounts also stays at $19,500. If you’re age 50 or older, you qualify to make an additional $6,500 catch-up contribution as well.

5. You can save a bit more in your health savings account (HSA)

For 2021, the max you can contribute into an HSA is $3,600 for an individual (up $50 from 2020) and $7,200 for a family (up $100). People age 55 and older can contribute an extra $1,000 catch-up contribution.

To be eligible for an HSA, you must be enrolled in a high-deductible health plan (which usually has lower premiums as well). Learn more about the benefits of an HSA.

6. The Child Tax Credit has been expanded

For 2021, the American Rescue Plan Act (ARPA) has temporarily modified the Child Tax Credit requirements and amounts for household incomes below $75,000 for single filers and $150,000 for married filing jointly.

First, the ARPA has raised the age limit for dependents from 16 to 17. In addition, the child tax credit has increased from $2,000 to $3,000 for children age 6 through 17 and up to $3,600 for children under 6. If your income exceeded the above limits but was below $200,000 for single filers or $400,000 for joint filers, you’ll receive the standard child tax credit of $2,000 per child.

The IRS began sending monthly advance Child Tax Credit payments to eligible families in July and sent its last advance in December. If your dependent didn’t qualify for the child tax credit, you may still qualify for up to $500 of tax credits under the “credit for other dependents” (see IRS Publication 972 for more details). Tax credits, which reduce the tax you owe dollar for dollar, are generally better than deductions, which reduce your taxable income.

7. The alternative minimum tax (AMT) exemption has gone up

Until the AMT exemption enacted by the Tax Cuts and Jobs Act expires in 2025, the AMT will continue to affect mostly households with incomes over $500,000. Still, the AMT has investment implications for some high earners.

For 2021, the AMT exemptions are $73,600 for single filers and $114,600 for married taxpayers filing jointly. The phase-out thresholds are $1,047,200 for married taxpayers filing a joint return and $523,600 for all other taxpayers.

8. The estate tax exemption is even higher

The estate and gift tax exemption, which is indexed to inflation, has risen to $11.7 million for 2021. But the now-higher exemption is set to expire at the end of 2025, meaning it could be essentially cut in half at that time if Congress doesn’t act.

The annual gift exclusion, which allows you to give money to your loved ones each year without incurring any tax liability or using up any of your lifetime estate and gift tax exemption, stays at $15,000 per recipient.

Don’t get caught off guard

As you prepare to file your taxes for 2021, here are a few additional items to consider.

If you’re not retired, the 10% early withdrawal penalty that was waived for retirement account distributions in 2020 has been reinstated for 2021.

If you’re age 72 or older, make sure you’ve taken your required minimum distribution (RMD) from your retirement accounts or else you face a 50% penalty on any undistributed funds (unless it’s your first RMD, in which case, you can wait until April 1, 2022).

If you haven’t contributed to your retirement accounts already, now is the time. Review your earnings for the year and take advantage of any deductions that can lower your tax bill. Also, keep an eye on Washington for any last-minute tax changes that could affect your return before you file. Tax season will be here before you know it, and it’s never too early to start preparing.

1Operating charities, or qualifying public charities, are defined by Internal Revenue Code section 170(b)(1)(A). You can use the Tax Exempt Organization Search tool on IRS.gov to check an organization’s eligibility.

If you’re a physician looking to get ahead on planning for retirement, you’re likely familiar with individual retirement accounts, or IRAs. An IRA is a tax-advantaged vehicle that helps you grow your retirement savings. Roth IRAs are particularly attractive, because you don’t pay taxes on withdrawals in retirement.

There’s one problem: you can’t contribute to a Roth IRA directly if you make above a certain income. A backdoor IRA, though, can solve your problem by allowing you to convert a traditional IRA into a Roth.

Here’s how it works:

First, place your contribution in a traditional IRA—which has no income limits.

Then, move the money into a Roth IRA using a Roth conversion.

But make sure you understand the tax consequences before using this strategy.

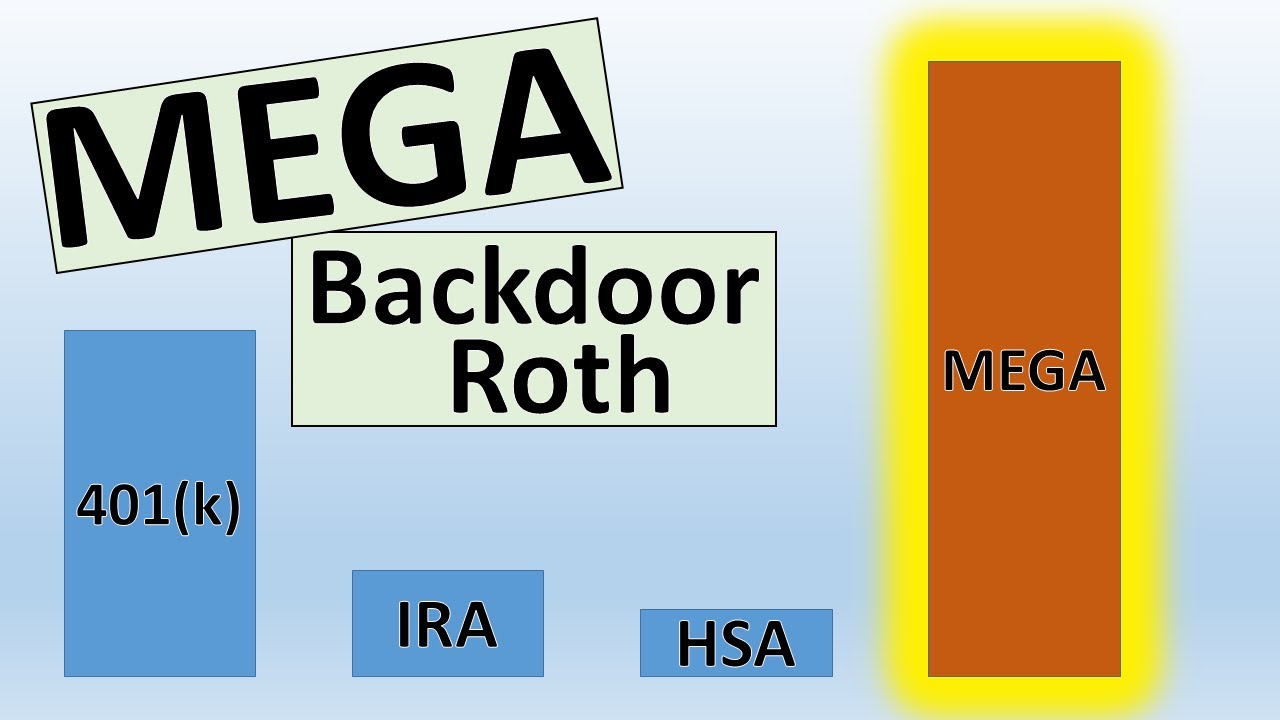

The mega backdoor Roth allows you to put up to $38,500 in a Roth IRA or Roth 401(k) in 2021, on top of the regular contribution limits for those accounts. If you have a Roth 401(k) at work (and the plan allows for the mega option as described below), generally you can choose whether the final destination of your mega contributions is the Roth 401(k) or a Roth IRA. If your employer offers only a traditional 401(k), then your mega contributions would end up in a Roth IRA.

Here’s a quick summary of what you need to have in place for the ideal mega backdoor Roth strategy:

A 401(k) plan that allows “after-tax contributions.” After-tax contributions are a separate bucket of money from your traditional and Roth 401(k) contributions. About 43% of 401(k) plans allow after-tax contributions, according to a 2017 survey of large and midsize employers by consulting firm Willis Towers Watson.

Your employer offers either in-service distributions to a Roth IRA — that is, you can take money out of the 401(k) plan while you’re still working at the company — or lets you move money from the after-tax portion of your plan into the Roth 401(k) part of the plan. If you’re not sure, ask your human resources department or plan administrator.

You’ve got money left over to save, even after maxing out your regular 401(k) and Roth IRA contributions.

Taking a distribution from a tax qualified retirement plan, such as a 401(k), prior to age 59 1/2 is generally subject to a 10 percent early withdrawal tax penalty.

However, the IRS rule of 55 may allow you to receive a distribution after attaining age 55 (and before age 59 1/2 ) without triggering the early penalty if your plan provides for such distributions.

The distribution would still be subject to an income tax withholding rate of 20 percent, however. (If it turns out that 20 percent is more than you owe based on your total taxable income, you will get a refund after filing your yearly tax return.)

An IRA in which distributions continue after the primary beneficiary’s death.

For an IRA to be inherited, the primary beneficiary must have already been receiving the required minimum distribution; the distributions either continue or are re-calculated based upon the secondary beneficiary’s life expectancy.

If the secondary beneficiary is the widow(er) of the primary beneficiary, she/he may roll over the inherited IRA into her/his own IRA without penalty.

One personal investing strategy is to place more conservative investments (those with lower expected returns) in a tax-deferred traditional IRA, 401-k, 403-b or similar, and more aggressive (higher-earning) assets in a taxable brokerage account or Roth IRA.

WHY? Each account is thus working hard but in very different ways.

HOW? The conservative funds in the traditional IRA or retirement accounts would fill any needs for safety as they grow more slowly – and the higher tax rate won’t take out as big of a bite.

Meanwhile, the more aggressive funds in a taxable brokerage accounts would grow more quickly, but be taxed at a lower rate.

Assessment: Any thoughts?

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Posted on July 24, 2018 by Dr. David Edward Marcinko MBA MEd CMP™

Three More Critical Mistakes to Avoid

By Rick Kahler CFP®

Previously, I discussed two critical IRA mistakes, based on information I learned from Jeff Levine of Fully Vested Advice, Inc., at the 2018 spring conference of the National Association of Personal Financial Advisors. This week I will cover three more.

1. Failing to understand beneficiary options on inherited IRAs. You may well be among the millions of Americans, most of them spouses, who will inherit IRAs. Knowing the options you have can save you thousands of dollars in benefits and taxes.

Spouses have the right to remain as a beneficiary of the plan or roll it over into their own IRA. Which to choose depends upon the age of the person who has died, and the age and financial needs of the beneficiary. The “99% rule” says beneficiaries under age 59½ should retain the plan as an inherited IRA; those over 59½ should roll it over. The “1%” scenario is when the deceased spouse was over age 70½ and the beneficiary is more than 11 years younger. A rollover is best if the beneficiary doesn’t need any IRA distributions until after age 59½.

Another option for IRA owners is to name a trust as the beneficiary of the IRA. Levine suggests not doing this if you can accomplish your goals without it. But there are many cases when a trust will accomplish things that giving the IRA outright to a beneficiary won’t do. Estate planning attorney Ilene McCauley, from Scottsdale, AZ, says some of those instances are when you want to protect the IRA from a divorce of a beneficiary or guarantee that the proceeds go to your children when your spouse dies or remarries. McCauley recommends using a living trust as the IRA beneficiary rather than a testamentary trust established through a will.

2. Not understanding the RMD aggregation rules. These are widely misunderstood even by advisors. Levine asked the group of about 50 advisors this question: “If a 72-year-old client had two traditional IRAs, two 401ks, and two 403bs, how many RMD checks would need to be issued?” Only three advisors got the right answer—four. You can aggregate the RMDs from the two traditional IRA accounts and take the combined RMD out of just one account. You can do the same with the two 401k accounts. But with the 403b accounts you must take the RMD separately from each account. You can’t aggregate them or you face penalties and taxes.

3. Not doing periodic reviews of IRA beneficiaries. It’s important to review your IRA beneficiaries regularly. This is especially crucial when a beneficiary dies or you get remarried. For example, assume you want your employer’s retirement plan to go to your children upon your death. You remarry, but don’t have your new spouse sign a disclaimer waiving rights to your retirement plan. If you die after one year of marriage your new spouse, not your children, inherits the employer’s retirement plan funds.

The reverse is true with an IRA or a 403b. Let’s assume you listed your kids as the beneficiaries on either of these accounts. If you remarry and want the proceeds to go to your new spouse but you forget to sign a change of beneficiary form, there is no one-year rule as there is with an employer’s plan. Your kids , not your spouse, will inherit the account.

Assessment

The bottom line is that, to get the most benefit from a retirement plan, you need to do your homework and seek appropriate advice. The money you save by avoiding IRA mistakes can make a big difference in your security and standard of living in retirement.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Posted on July 18, 2018 by Dr. David Edward Marcinko MBA MEd CMP™

Avoid These 2 Mistakes

By Rick Kahler CFP®

Investing through an IRA is a foundational method of retirement saving. Opening and contributing to an individual retirement account is not hard. That doesn’t mean IRAs are simple and easy to understand.

National Association of Personal Financial Advisors

I was reminded of this at the 2018 spring conference of the National Association of Personal Financial Advisors, where I attended a workshop by Jeff Levine of Fully Vested Advice, Inc., on “10 Critical IRA Mistakes.”

Top on his list of mistakes was failing to make charitable contributions out of your IRA when you are over 70½. These are called Qualified Charitable Distributions (QCDs). Here is why giving to charity directly from your IRA is a good idea.

For traditional IRAs, at age 70½ you must begin to withdraw required minimum distributions (RMDs) whether you want to or not. An RMD is taxable at ordinary income rates. Further, if you make a charitable donation and you are over age 65, you now must have over $13,300 of itemized deductions per person to get any portion of it deductible. By donating out of your IRA, you can reduce your RMD by an amount equal to your charitable gift. This makes your charitable gift 100% deductible and lowers your adjusted gross income, which can also help lower your Medicare premiums.

Here’s an example

Assume you are age 71, give $9,000 a year to charity, your property taxes on your home are $2,500, you are in the 22% tax bracket, and your RMD is $10,000. Without planning you will take your $10,000 RMD and pay $2,200 of income tax on it. Since you only have $11,500 in itemized deductions you will take the standard deduction of $13,300.

If instead you contribute $9,000 to charity out of your IRA, you reduce your taxable RMD from $10,000 to $1,000, slashing your tax liability on it from $2,200 to $220. The savings of $1,980 would cover most of your property tax.

If you make a QCD like this, it’s essential to inform your tax preparer. There is no required written evidence from your IRA custodian that your RMD needs to be offset by the amount of your gift. It’s your responsibility to tell your accountant so they report the correct reduced amount of the RMD on your tax return.

In Bankruptcy

Another significant source of mistakes is the complex asset protection rules for IRAs and retirement plans. Protection differs between bankruptcy and non-bankruptcy creditor actions.

In bankruptcy, all employer plans (ERISA), SEP and SIMPLE IRAs, and rollovers from retirement plans to IRAs are 100% protected from creditors. Amounts you personally contributed to traditional and Roth IRAs are protected up to a total of $1,283,025. However, inherited IRAs are not covered. You can see why it’s important to keep traditional, rollover and inherited IRAs in separate IRA accounts.

To make it even more complicated, different rules apply if creditors sue in non-bankruptcy proceedings. ERISA plans are 100% protected in all states. All IRAs are 100% protected in most states, except California, Georgia, Maine, Mississippi, Nebraska, South Dakota, and Wyoming, where they have limited to no protection.

Solo 401(k), SEP IRA, and SIMPLE IRA plans are fully protected from non-bankruptcy proceedings in about half of the states. The others, including South Dakota, have limited or no protection. If you live in one of these states and have a Solo 401(k), SEP, or SIMPLE, you want to roll it into an IRA as soon as circumstances allow.

Assessment

Mistakes like the two described here can be costly. To avoid them, especially if your circumstances are at all complex, it’s wise to get tax and IRA withdrawal advice from qualified financial advisors.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Posted on November 8, 2017 by Dr. David Edward Marcinko MBA MEd CMP™

Mandatory RMDs

By Rick Kahler CFP®

Planning is important for all things financial, including retirement, which is inevitable no matter how far into the future it may seem. The financial decisions you make in your 20s through your 60s will greatly impact the quality of your lifestyle during retirement. Social Security and family won’t be enough to get you through 30 years of retirement. If you haven’t worked for a branch of government, you will rely heavily on income you’ve stashed in 401(k)s and IRAs.

Traditional IRAs

One of the big advantages of a traditional IRA or 401(k) is being able to save pre-tax dollars and let them grow tax deferred until you need them. Hopefully, when you take the distributions in retirement, you will be in a lower tax bracket than when you made the contribution. The downside is that traditional IRA funds become 100% taxable when you withdraw them.

Deferrals

Deferring distributions from your IRA only works until age 70½, when you’ll be forced to take money out whether you want to or not. This is called a Required Minimum Distribution, or RMD. If, at age 70½, you don’t need to withdraw funds to live on but are faced with an annual RMD, there are several things you can do to minimize your tax hit.

The easiest is don’t stop earning an income if you have a substantial 401(k). Employees are not required to take RMDs when they are still working, even part-time. This only applies to your employer’s 401(k). You will need to take RMDs from personal IRAs or 401(k)s and IRAs from previous employer plans.

***

***

However, if you plan ahead you may be able to bypass this. If you have IRAs that are rollovers from previous 401(k)s, your employer may allow you to roll them into your current plan. By consolidating previous qualified employer plans into your current plan, you can defer taking an RMD until you quit working.

If you give to charities, you can give any portion or all of your RMD to a charity and not pay any taxes on the distribution. This can really save you a lot of money if you are currently giving to charities out of taxable accounts. When you turn 70½, simply redirect your charitable giving from taxable accounts to your IRA. You can give up to $100,000 annually without paying taxes on those distributions.

Another strategy we use commonly with clients is converting traditional IRA funds to Roth IRAs. Money in a Roth is not subject to RMDs. Of course, the downside is that you must pay taxes on the funds converted from your traditional IRA to a Roth.

For a conversion to make financial sense, two important factors must apply. You generally want to do a Roth conversion when your current tax bracket is lower than you anticipate it will be in the future. The most obvious scenario here is when you delay Social Security until age 70 and you are currently in a 10% or 15% tax bracket. It’s highly possible that Social Security and RMDs all kicking in at the same time may put you into the 25% tax bracket. Moving as much money at the 15% bracket prior to age 70 can make a lot of sense. It’s also important that the money to pay the taxes needs to come from a taxable account.

Assessment

As with all financial strategies that are crammed into a 600-word article, there are variations and nuances I am not able to go into. If you think one of these strategies may apply to you, don’t try it on your own. First get advice from a competent tax advisor or financial professional.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, urls and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Contact: MarcinkoAdvisors@msn.com

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, I.T, business and policy management ecosystem.

I recently learned about an unexpected response to the new Department of Labor rule which mandates that all financial advisors and brokers act as fiduciaries (that is, in the best interest of the consumer) when dealing with customers’ retirement plans.

This means brokers will be discouraged from selling high fee and commission products to a customer’s IRA or similar retirement plan. The ruling may force many brokers to revamp for IRA products that have lower fees and commissions.

The Survey

However, according to a J. D. Power survey as reported in Financial Planning, customers are not happy with their brokers charging them lower fees. While the survey found that the clients of fee-only advisors were “generally more satisfied with what they pay their firm,” it also found that commission-based clients are going to leave in droves if their advisors switch to a lower-cost, fee-only model.

Let me get this straight

A broker who until now has owed no fiduciary duty to the customer, and who sells high fee and commission products to that customer, will now be forced by their company to place the consumer’s interest first. When dealing with the customer’s IRA, the broker cannot receive commissions and can only earn a lower fee. The broker places a low-fee product in the client’s IRA.

The result?

The client is so upset they will take their business to another firm.

According to J. D. Powers, that is correct. Their survey says around 60% of the customers of brokerage firms that may have to switch to fee-only when dealing with customer’s IRAs will “probably” or “definitely” take their business to another firm.

***

***

I am imagining the following conversation between a customer and a broker

Broker:

“Because of the new DOL regulations I can no longer sell you a high fee and commission variable annuity to be owned by your IRA. To comply with the ruling, my company has eliminated the 7% upfront commission on this annuity; we will now charge you a 1% annual fee. They also reduced the annual management expenses from 3% to 1%. Plus, now any advice I give you or product I recommend must be in your best interests.”

Customer:

“So you are eliminating the upfront 7% commission and replacing that with a 1% annual fee, which means 7% more of my money immediately goes to work for me in the investment, right?”

Broker:

“That’s right.”

Customer: