BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Yes, you can contribute to both a Roth IRA and a 401(k), provided you don’t exceed annual contribution limits for each account.

Determining whether to contribute to a Roth IRA, 401(k), or both can be an important step in planning for your retirement. Here are the key differences, including tax advantages, employer contributions, and investment options.

Eligibility requirements are the first consideration when contributing to a Roth IRA and a 401(k). For Roth IRA contributions, your eligibility is determined by your income. Specifically, if your modified adjusted gross income (MAGI) exceeds certain thresholds, your ability to contribute to a Roth IRA may be reduced or eliminated. However, there are no income limits for contributing to a 401(k), making it accessible to anyone with earned income.

IRS rules do allow for contributions to both a Roth IRA and a 401(k), provided you adhere to the annual contribution limits for each account.

This means you can take advantage of the higher contribution limits of a 401(k) while also benefiting from the tax-free growth of a Roth IRA. This dual approach can be a strategy for maximizing your retirement savings. The advantages to contributing to both accounts present some key benefits, such as:

Tax diversification in retirement, allowing for better management of taxable income.

Potential reduction of overall tax burden.

Maximization of savings potential by taking full advantage of the benefits each account offers.3

Balancing contributions between a Roth IRA and a 401(k) requires careful planning. You might start by contributing enough to your 401(k) to receive the full employer match, which is essentially free money, if your employer offers this. Once you’ve secured the match, consider maxing out your Roth IRA contributions, if you’re eligible.

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Why would a doctor consider a Roth IRA conversion?

By Staff Reporters

***

***

A Roth conversion involves transferring funds from a traditional retirement account—such as a 401(k), 403(b), or individual retirement account (IRA) funded with pre-tax dollars—into a Roth IRA.

The biggest benefit lies in the tax treatment of the converted funds. Once the funds are in the Roth IRA, future growth of those assets is tax-free. Withdrawals in retirement are also tax-free, assuming they meet certain criteria. As with any strategy, there are important considerations to keep in mind.

When you convert funds to a Roth IRA, the amount converted is taxable income in that tax year. For example, if you convert $100,000 from a traditional IRA to a Roth IRA, that $100,000 will be added to your taxable income in the conversion year.

Converting large amounts can result in a significant tax bill and may push you into a higher tax bracket. Even so, using retirement funds to pay taxes may make sense for those looking to convert large IRAs to reduce their future required minimum distributions (RMDs).

The timing of your Roth conversion matters too. Generally, it’s a good idea to convert when your income is lower—for example, after you’ve retired and before you begin drawing Social Security. You may also choose to convert over the course of several years to spread out the tax impacts. But if you can get comfortable with these considerations, a Roth conversion can provide you with benefits beyond tax-free growth and withdrawals.

Some of these benefits are:

Tax diversification. Having both traditional and Roth accounts allows you to manage your tax liability in retirement. For example, if your income in a given year is higher than expected, you can withdraw from the Roth IRA without increasing your taxable income.

No RMDs. Traditional IRAs and 401(k)s require you to begin taking RMDs at age 73. Roth IRAs have no RMD requirement during your lifetime. With a Roth account, you have more control over your retirement withdrawals and can leave the funds to grow for your heirs.

Benefits for heirs. Roth IRAs can be passed on to beneficiaries, who can inherit the account income tax-free. This means your heirs can enjoy the tax-free growth and withdrawals if the Roth IRA has been held for five years or more—a significant advantage, especially if your beneficiaries are in a higher tax bracket.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

QUESTION:Can I invest my Individual Retirement Account [IRA] in a Hedge Fund?

This is up to the manager, but there is no legal restriction on a hedge fund accepting individual retirement account (IRA) assets. IRA accounts are not well suited for funds that make extensive use of leverage, however. In such cases, the fund is likely to generate significant amounts of unrelated business taxable income (UBTI) – profits of the fund attributable to the use of leverage. The holder of an IRA account must pay taxes on UBTI, even if the UBTI was generated in an IRA account.

But, today’s hedge funds may or may not use leverage. Many hedge funds are not hedged at all, but rather are just specialized versions of regular long stock portfolios. If such funds do not use much leverage, IRA investors will not encounter much difficulty with UBTI and should not hesitate in considering these funds.

In considering whether to accept IRA money, hedge fund managers must consider several factors. If the only type of retirement money accepted by the hedge funds is IRA money, then the manager has no limit on how much retirement money the fund can accept. If, however, there are other types of retirement money invested in the fund, such as pension funds, IRA money will be counted towards a total of 25 percent of fund assets that can be invested in retirement accounts before the fund becomes subject to the Employment Retirement Income Security Act of 1974 (ERISA). Funds subject to ERISA regulations face a heavy administrative burden and more restrictions than most fund managers like.

Finally, IRA distributions from a hedge fund are subject to the standard 20 percent withholding unless the funds are directly rolled over to other qualified plans.

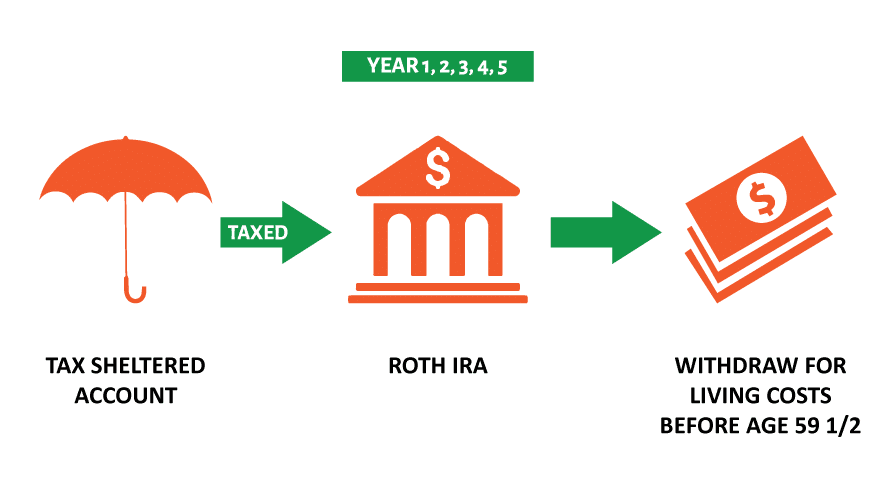

Last week, ProPublica published the story of how PayPal co-founder and tech investor Peter Thiel was able to turn a Roth IRA initially worth around $2,000 into a jaw-dropping $5 billion tax-free retirement stash in just 20 years.

The story is even more remarkable because Congress created the Roth IRA in 1997 to encourage middle-class Americans to save for their golden years. Most Americans have struggled to do even that; the average account was worth about $39,000 in 2018. But Thiel and other billionaires have managed to turn their mundane Roths into giant onshore tax shelters.

Thiel was able to launch his Roth into the stratosphere through a complicated strategy involving the purchase of nonpublic stock at bargain prices — the kind of deal most people can’t access. Experts say it risked running afoul of rules designed to prevent IRAs from becoming illegal tax shelters. (Thiel’s spokesman didn’t respond to questions.)

Other ultrawealthy Americans have used different means to build Roths worth tens or hundreds of millions of dollars. Senate Finance Chairman Ron Wyden is now looking at how to end the use of the Roth as “yet another tax dodge that allows mega millionaires and billionaires to avoid paying taxes.”

How are they able to do it while you can’t? Check out our explainer of one way the Roth works for the ultrawealthy and not for you.

Whether you do contract work or have your own small business, tax deductions for the self-employed physician consultant and/or medical executive or nurse consultant, etc., can add up to substantial tax savings.

With self-employment comes freedom, responsibility, and a lot of expense. While most self-employed people celebrate the first two, they cringe at the latter, especially at tax time. They might not be aware of some of the tax write-offs to which they are entitled.

When it comes time to file your returns, don’t hesitate to claim the benefits you get for being the boss. As a self-employed success story, you’ve earned them.

FORM 1099NEC: Form 1099 NEC is one of several IRS tax forms used in the United States to prepare and file an information return to report various types of income other than wages, salaries, and tips. The term information return is used in contrast to the term tax return although the latter term is sometimes used colloquially to describe both kinds of returns.

“Many times an overlooked deduction is educational expenses. If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Individual Retirement Plans (IRAs)

One of the best tax write-offs for the self-employed physician consultant is a retirement plan. A person with no employees can set up an individual 401 (k). “You can contribute $19,500 in 2021 as a 401(k) deferral, plus 25 percent of net income.”

If you have employees, consider a SIMPLE (Savings Incentive Match Plan for Employees) IRA—an IRA-based plan that gives small employers a simplified method to make contributions to their employees’ retirement. As of 2021, an employee may defer up to $13,500 and employees over 50 may contribute an additional $3,000.

“A third retirement plan is Simplified Employee Pension IRA (SEP IRA).” The employer may contribute the lesser of 25 percent of income or $58,000 in 2021. If the employer has eligible employees, an equal percentage of their income must be contributed.

Recall that retirement plans are “absolutely the No. 1 tax deduction. The government is helping fund retirement.”

Business use of home or dwelling

Now, most self-employed taxpayers’ businesses start as home-based businesses. These people need to know portions of business costs are deductible and so “It is very important that you keep track of expenses relating to your housing costs.”

If your gross income from your business exceeds your total expenses, then you can deduct all of your expenses related to the business use of your home. If your gross income is less than your total expenses, your deduction will be limited to the difference between your gross income and the sum of all business expenses you would pay if the business was not in your home. Those expenses could include telephone lines, the Internet, and other costs to do business.

You must also have a home office that is truly used for work and the Internal Revenue Service may require you to document this.

***

Deducting automobile expenses

If you travel for business, even short distances within your own city, you may deduct the dollar value of business miles traveled on your tax return. The taxpayer may file the actual expense s/he incurred, or use the standard mileage rate prescribed by the IRS, which is 56 cents as of 2021. The IRS allowable mileage rates should be checked every year as they can change.

“If you decide to use actual car expenses, be sure to include payments, depreciation, registration, insurance, garage rent, licenses, repairs and maintenance, and parking and toll fees.” AND, “If you decide to use the standard mileage rate, it would be in your best interest to keep a log—daily, weekly or monthly—of miles driven to distinguish personal use from business use.”

Depreciation of property and equipment

Some self-employed people may purchase property and equipment for a business. If they expect that property to last longer than one year, it should be depreciated on the tax return.

Claims regarding property, according to the IRS, must meet the following criteria: You must own the property and it must be used or held to generate income. The property should have an estimated useful life, meaning you should be able to guess how long you can generate income with it. It may not have a useful life of one year or less, and may not be purchased and disposed of in the same year.

Certain repairs on property used for business may also be deducted.

Educational expenses

Any educational expense is potentially tax-deductible.

“Many times an overlooked deduction is educational expenses. “If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Think about any books, web courses, local college courses, or other classes or materials that you have purchased to improve your job or business. It’s easy to forget a work-related webinar or business e-book that was purchased online, so remember to save e-receipts.

Also recall that subscriptions to trade or professional publications and donations to business organizations, both of which are frequently necessary for the continuation and growth of your business.

Other areas to explore

Other deductions that can be easily missed are advertising and promotional expenses, banking fees, and air, bus, or train fare. Restaurant meals and other entertainment costs may be written off as long as they are necessary business expenses.

And, consider health insurance premiums, which in most cases represent a credit rather than a tax deduction. “A credit goes directly against one’s taxes, rather than a reduction of income.”

Regardless of which expenses you discover that you may write off, the most important thing is to keep accurate records throughout the year. Save receipts, including e-mail receipts, and file or log them so you have easy access to them at tax time. Not only does keeping receipts, mileage logs, and other expense records make filing taxes easier, but it also facilitates a system that allows you to track changes from year to year.

***

Long-term tax-saving strategies

Don’t just look at last-minute write-offs when considering self-employment tax deductions. Think about laying down some long-term strategies for money savings from year to year—particularly if you are a high earner.

“Accountants typically tell you what you have to pay but they don’t always tell you strategies to reduce your payments.”

To reduce your gross taxable income, consider setting up a defined-benefit pension plan. This plan is based on your age and income: The older you are and the higher your earnings, the more you are allowed to contribute. An alternative plan is an age-weighted profit-sharing plan, which is similar and can benefit those who have several employees.

Another strategy for high-earning business owners who own their own building through a limited liability company or similar business structure is to pay themselves rent. This rent is used to pay down the mortgage, but it is also considered a business expense for tax purposes.

Self-employed professionals required to have liability insurance should consider setting up their own insurance company. A captive insurance company is one that insures the risks of the business—or businesses, in the case of a cooperative. Its premiums can be tax-deductible.

But, if money accumulates and claims are minimal, the money taken out is taxable under capital gains. This is not a retirement strategy, but that it can save you money by allowing you to “pay yourself” instead of an insurance company and still deduct the premiums.

Assessment

With any of these more complicated, long-term strategies, consult with a business attorney, CPA/EA or financial planner to ensure you have the best plan possible for your business.

Here are eight things to keep in mind as you prepare to file your 2021 taxes.

1. Income tax brackets have shifted a bit

There are still seven tax rates, but the income ranges (tax brackets) for each rate have shifted slightly to account for inflation. For 2021, the following rates and income ranges apply:

Tax rate

Taxable income brackets:Single filers

Taxable income brackets:Married couples filing jointly (and qualifying widows or widowers)

10%

$0 to $9,950

$0 to $19,900

12%

$9,951 to $40,525

$19,901 to $81,050

22%

$40,526 to $86,375

$81,051 to $172,750

24%

$86,376 to $164,925

$172,751 to $329,850

32%

$164,926 to $209,425

$329,851 to $418,850

35%

$209,426 to $523,600

$418,851 to $628,300

37%

$523,601 or more

$628,301 or more

Source: Internal Revenue Service

2. The standard deduction has increased slightly

After an inflation adjustment, the 2021 standard deduction has increased slightly to $12,550 for single filers and married couples filing separately and $18,800 for single heads of household, who are generally unmarried with one or more dependents. For married couples filing jointly, the standard deduction has risen to $25,100.

3. Itemized deductions remain the same

For most filers, taking the higher standard deduction is more practical and saves the hassle of keeping track of receipts. But if you have enough tax-deductible expenses, you might benefit from itemizing.

The following rules for itemized deductions haven’t changed much for 2021, but they’re still worth pointing out.

State and local taxes: The deduction for state and local income taxes, property taxes, and real estate taxes is capped at $10,000.

Mortgage interest deduction: The mortgage interest deduction is limited to $750,000 of indebtedness. But people who had $1,000,000 of home mortgage debt before December 16, 2017, will still be able to deduct the interest on that loan.

Medical expenses: Only medical expenses that exceed 7.5% of adjusted gross income (AGI) can be deducted in 2021.

Charitable donations: The cash donation limit of 100% of AGI remains in place for 2021, if donations were made to operating charities.1

Miscellaneous deductions: No miscellaneous itemized deductions are allowed.

4. IRA and 401(k) contribution limits remain the same

The traditional IRA and Roth contribution limits in 2021 remain the same as in 2020. Individuals can contribute up to $6,000 to an IRA, and those age 50 and older also qualify to make an additional $1,000 catch-up contribution. If you’re able to max out your IRA, consider doing so—you may qualify to deduct some or all of your contribution.

The 2021 contribution limit for 401(k) accounts also stays at $19,500. If you’re age 50 or older, you qualify to make an additional $6,500 catch-up contribution as well.

5. You can save a bit more in your health savings account (HSA)

For 2021, the max you can contribute into an HSA is $3,600 for an individual (up $50 from 2020) and $7,200 for a family (up $100). People age 55 and older can contribute an extra $1,000 catch-up contribution.

To be eligible for an HSA, you must be enrolled in a high-deductible health plan (which usually has lower premiums as well). Learn more about the benefits of an HSA.

6. The Child Tax Credit has been expanded

For 2021, the American Rescue Plan Act (ARPA) has temporarily modified the Child Tax Credit requirements and amounts for household incomes below $75,000 for single filers and $150,000 for married filing jointly.

First, the ARPA has raised the age limit for dependents from 16 to 17. In addition, the child tax credit has increased from $2,000 to $3,000 for children age 6 through 17 and up to $3,600 for children under 6. If your income exceeded the above limits but was below $200,000 for single filers or $400,000 for joint filers, you’ll receive the standard child tax credit of $2,000 per child.

The IRS began sending monthly advance Child Tax Credit payments to eligible families in July and sent its last advance in December. If your dependent didn’t qualify for the child tax credit, you may still qualify for up to $500 of tax credits under the “credit for other dependents” (see IRS Publication 972 for more details). Tax credits, which reduce the tax you owe dollar for dollar, are generally better than deductions, which reduce your taxable income.

7. The alternative minimum tax (AMT) exemption has gone up

Until the AMT exemption enacted by the Tax Cuts and Jobs Act expires in 2025, the AMT will continue to affect mostly households with incomes over $500,000. Still, the AMT has investment implications for some high earners.

For 2021, the AMT exemptions are $73,600 for single filers and $114,600 for married taxpayers filing jointly. The phase-out thresholds are $1,047,200 for married taxpayers filing a joint return and $523,600 for all other taxpayers.

8. The estate tax exemption is even higher

The estate and gift tax exemption, which is indexed to inflation, has risen to $11.7 million for 2021. But the now-higher exemption is set to expire at the end of 2025, meaning it could be essentially cut in half at that time if Congress doesn’t act.

The annual gift exclusion, which allows you to give money to your loved ones each year without incurring any tax liability or using up any of your lifetime estate and gift tax exemption, stays at $15,000 per recipient.

Don’t get caught off guard

As you prepare to file your taxes for 2021, here are a few additional items to consider.

If you’re not retired, the 10% early withdrawal penalty that was waived for retirement account distributions in 2020 has been reinstated for 2021.

If you’re age 72 or older, make sure you’ve taken your required minimum distribution (RMD) from your retirement accounts or else you face a 50% penalty on any undistributed funds (unless it’s your first RMD, in which case, you can wait until April 1, 2022).

If you haven’t contributed to your retirement accounts already, now is the time. Review your earnings for the year and take advantage of any deductions that can lower your tax bill. Also, keep an eye on Washington for any last-minute tax changes that could affect your return before you file. Tax season will be here before you know it, and it’s never too early to start preparing.

1Operating charities, or qualifying public charities, are defined by Internal Revenue Code section 170(b)(1)(A). You can use the Tax Exempt Organization Search tool on IRS.gov to check an organization’s eligibility.

If you’re a physician looking to get ahead on planning for retirement, you’re likely familiar with individual retirement accounts, or IRAs. An IRA is a tax-advantaged vehicle that helps you grow your retirement savings. Roth IRAs are particularly attractive, because you don’t pay taxes on withdrawals in retirement.

There’s one problem: you can’t contribute to a Roth IRA directly if you make above a certain income. A backdoor IRA, though, can solve your problem by allowing you to convert a traditional IRA into a Roth.

Here’s how it works:

First, place your contribution in a traditional IRA—which has no income limits.

Then, move the money into a Roth IRA using a Roth conversion.

But make sure you understand the tax consequences before using this strategy.

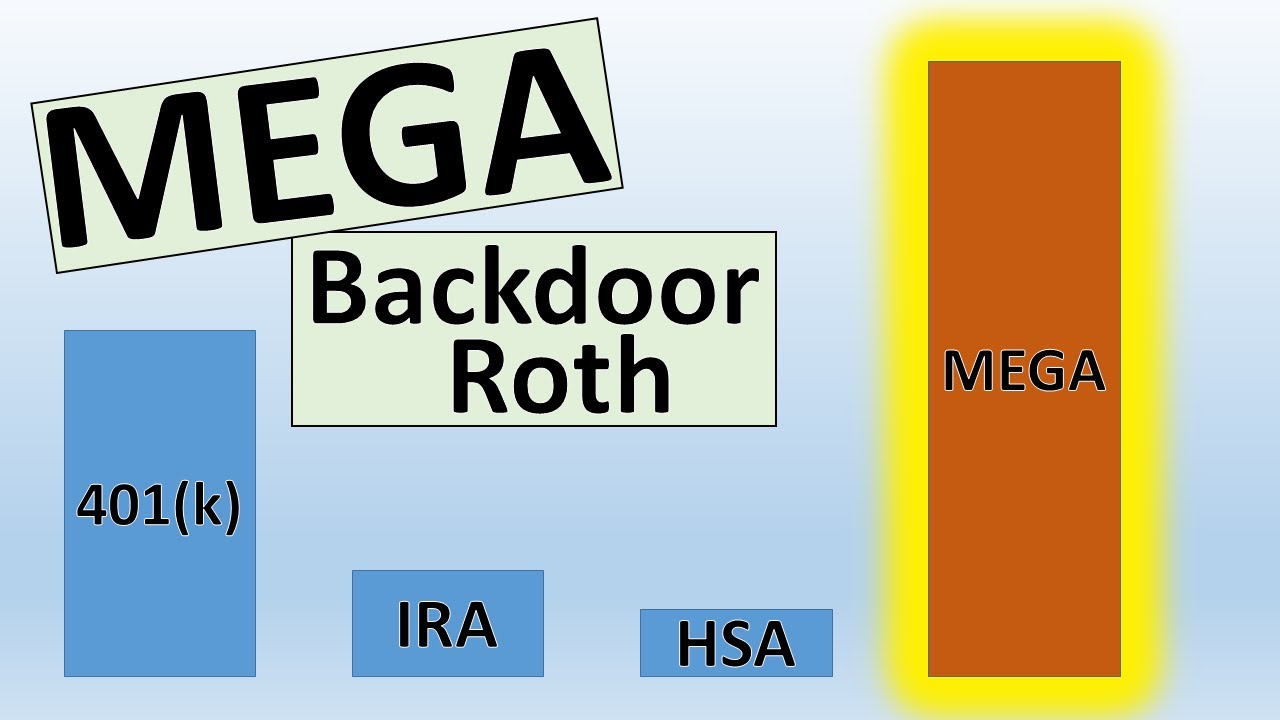

The mega backdoor Roth allows you to put up to $38,500 in a Roth IRA or Roth 401(k) in 2021, on top of the regular contribution limits for those accounts. If you have a Roth 401(k) at work (and the plan allows for the mega option as described below), generally you can choose whether the final destination of your mega contributions is the Roth 401(k) or a Roth IRA. If your employer offers only a traditional 401(k), then your mega contributions would end up in a Roth IRA.

Here’s a quick summary of what you need to have in place for the ideal mega backdoor Roth strategy:

A 401(k) plan that allows “after-tax contributions.” After-tax contributions are a separate bucket of money from your traditional and Roth 401(k) contributions. About 43% of 401(k) plans allow after-tax contributions, according to a 2017 survey of large and midsize employers by consulting firm Willis Towers Watson.

Your employer offers either in-service distributions to a Roth IRA — that is, you can take money out of the 401(k) plan while you’re still working at the company — or lets you move money from the after-tax portion of your plan into the Roth 401(k) part of the plan. If you’re not sure, ask your human resources department or plan administrator.

You’ve got money left over to save, even after maxing out your regular 401(k) and Roth IRA contributions.

Taking a distribution from a tax qualified retirement plan, such as a 401(k), prior to age 59 1/2 is generally subject to a 10 percent early withdrawal tax penalty.

However, the IRS rule of 55 may allow you to receive a distribution after attaining age 55 (and before age 59 1/2 ) without triggering the early penalty if your plan provides for such distributions.

The distribution would still be subject to an income tax withholding rate of 20 percent, however. (If it turns out that 20 percent is more than you owe based on your total taxable income, you will get a refund after filing your yearly tax return.)

An IRA in which distributions continue after the primary beneficiary’s death.

For an IRA to be inherited, the primary beneficiary must have already been receiving the required minimum distribution; the distributions either continue or are re-calculated based upon the secondary beneficiary’s life expectancy.

If the secondary beneficiary is the widow(er) of the primary beneficiary, she/he may roll over the inherited IRA into her/his own IRA without penalty.

Posted on September 9, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

ALERT FOR PHYSICIANS AND ALL INVESTORS

***

1. You can trade actively in a Roth IRA

Some physician investors may be concerned that they can’t actively trade in a Roth IRA. But there’s no rule from the IRS that says you can’t do so. So you won’t get in legal trouble if you do.

But there may be some extra fees if you trade certain kinds of investments. For example, while brokers won’t charge you if you trade in and out of stocks and most ETFs on a short-term basis, many mutual fund companies will charge you an early redemption fee if you sell the fund. This fee is usually assessed only if you’ve owned the fund for fewer than 30 days.

2. Any gains are tax-free – forever

The ability to avoid taxes on your investments is an incredible benefit. You’ll be able to escape – perfectly legally – taxes on dividends and capital gains. Not surprisingly, this superpower makes the Roth IRA very popular, but to enjoy its benefits, you must abide by a few rules.

The Roth IRA limits you to a $6,000 maximum annual contribution (for 2021), and you won’t be able to withdraw earnings from the account until retirement age (59 1/2) or later and after owning the account for at least five years. However, you can withdraw your contributions to the account without being taxed at any time, but you won’t be able to replace those contributions later.

Many traders use margin in their accounts. With a margin loan, the broker extends you capital to invest beyond what you actually own. It’s a useful tool, especially if you’re trading frequently. Unfortunately, margin loans are not available in IRA accounts.

For frequent traders the ability to trade on margin is not just about magnifying your returns. It’s also about having the ability to sell a position and immediately buy another. In a cash account (like a Roth IRA), you have to wait for a transaction to settle, and that takes a couple days. In the meantime you’re unable to trade with that money even though it’s credited to your account.

PLUS A FOURTH RULE

4. You don’t get to deduct losses

If you’re trading in a taxable brokerage account, you’ll get a tax write-off if you make a losing investment. Some investors even make sure they’re getting the largest write-off they can using a process called tax-loss harvesting. They scoop up that benefit and then even repurchase the stock or fund later (after 30 days) if they think it’s poised to rise in the future.

But if you’re trading in a Roth IRA, you won’t get the ability to write off losses. Changes to the tax code in 2017 eliminated the ability to claim any benefit from losses in an IRA account.

One personal investing strategy is to place more conservative investments (those with lower expected returns) in a tax-deferred traditional IRA, 401-k, 403-b or similar, and more aggressive (higher-earning) assets in a taxable brokerage account or Roth IRA.

WHY? Each account is thus working hard but in very different ways.

HOW? The conservative funds in the traditional IRA or retirement accounts would fill any needs for safety as they grow more slowly – and the higher tax rate won’t take out as big of a bite.

Meanwhile, the more aggressive funds in a taxable brokerage accounts would grow more quickly, but be taxed at a lower rate.

Assessment: Any thoughts?

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Posted on November 25, 2018 by Dr. David Edward Marcinko MBA MEd CMP™

More on Retirement Planning

By Rick Kahler CFP®

If your employer offers a 401(k) or other retirement plan, contributing to that plan is a foundation of your retirement savings. However, as you approach retirement age, you might consider moving some of your retirement funds out of your employer’s plan and into an IRA at a custodian like TD Ameritrade or Fidelity; etc.

Such a rollover is often done when you leave an employer, though many employers give you the option of keeping your retirement account with them. What isn’t popularly understood is that you also can do a rollover while you’re still employed, as long as you are over 59 ½.

Why Rollover?

One reason to consider leaving your employer’s plan is that most of them have higher overall fees than an IRA, especially if you choose from low-cost index mutual funds or exchange traded funds from a company like Vanguard or Dimensional Fund Advisors. It’s not uncommon to save up to 1% annually by making a rollover into these mutual funds.

However, the costs of an IRA are not always cheaper. If you have a Thrift Savings Plan (TSP) through the federal government, the total costs are .03% a year. This is far cheaper than the average equity fund that charges 1.3% or even Vanguard and DFA that charge .09% on some funds.

The disadvantage with a TSP, like most employer plans, is their very limited investment options. The TSP offers about six options. Most 401(k)s will offer several times that—still a pittance compared with the 13,000 available at most discount brokers.

Another reason for a rollover is what happens when you retire and need to withdraw funds from your account. You can withdraw money from an IRA at any time without penalty after age 59 ½, but withdrawing money from a past employer’s 401(k) plan will require jumping through a few more hoops.

One issue that surprises most people is that the required minimum distributions (RMD) rules are reversed for employer plans. A RMD is never required with a Roth IRA. However, a RMD must be taken from a Roth 401(k) when you turn 70 ½. For this reason I recommend you roll over a Roth 401(k) before you turn 70 ½. The flip side of this is that when you turn 70 ½ you do have to take RMDs from a traditional IRA, but you do not from a traditional 401(k). Only a committee could have made up these rules.

The new tax code has made charitable giving less tax advantageous. However, if you are over 70 ½, you can give to charity tax-free from your IRA via a qualified charitable distribution (QCD). Employer plans don’t allow QCDs.

Another advantage of IRAs is that you can consolidate a number of employer accounts into one IRA. You can also withdraw funds from an IRA at any age without penalty for college expenses, which you cannot do from an employer plan.

Yet, another big advantage to an IRA is the ability to do Roth conversions, which cannot be done with an employer’s plan. It’s especially important to do such conversions before turning 70 ½ when your RMDs and Social Security benefits (assuming you wait until 70) kick in and raise your taxable income and possibly your tax bracket. Taking advantage of lower tax brackets prior to age 70 to convert part of traditional IRAs to Roths can lower your RMDs, which lower your tax liability, and let some of your retirement funds grow tax free forever.

***

***

Assessment

Done properly, a rollover from an employer’s plan to an IRA is free of any tax consequences. However, it’s important to evaluate the advantages and disadvantages carefully before you act.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

The President has fired the first warning shot indicating that politicians are eying the tax advantages of the Roth IRA. For years I’ve strongly encouraged maximum funding of Roth IRAs & 401(k)s.

Physician-Clients have sometimes expressed concern that politicians would someday retroactively change the rules and strip the plans of their tax advantages. I’ve seen that concern as a possibility (for example, in 2008 Argentina confiscated the assets in IRAs and 401(k)s and replaced them with less than desirable Argentinian Government Bonds), but not much of a probability.

With the introduction of the President’s 2016 budget, the probability of losing some Roth IRA tax benefits has increased.

Each February the President submits a budget to Congress which is about far more than spending requests. It also contains scores of proposed changes to existing tax laws. One such proposal in the current budget would eliminate two tax advantages of the Roth IRA.

The first change would require required minimum distributions (RMDs) for Roth IRAs as well as traditional IRAs.

Currently, one of the benefits of a Roth IRA is not having to take RMDs. At age 70 1/2, owners of traditional IRAs are required withdraw a certain percentage annually, often around 4%. They must pay the tax due and, if they don’t need the funds for living expenses, must invest the remainder in a taxable account. The RMD denies them the option of leaving the money in the tax-deferred environment of the IRA and further compounding.

Under the President’s proposal, owners of Roth IRAs will need to start withdrawing funds annually at age 70 1/2. While there won’t be any taxes due because contributions to Roths are post-tax, it will remove the funds from the tax-free environment, decreasing future returns by up to 40%. That’s a big deal.

The second proposed change would eliminate tax-deferred inheritance of IRAs (sometimes called “stretch IRAs) for anyone except spouses. All other inherited IRAs would need to be dissolved and the funds distributed and taxed within five years after death. This will really impact Baby Boomers counting on their parents’ IRAs to assist them with their own retirement needs.

Other budget proposals would also end Roth conversions to any after-tax IRAs, limiting them to IRAs where the contributions were before taxes. This would prohibit taxpayers with earnings above the traditional and Roth IRA threshold from making non-deductible contributions to a traditional IRA and then doing a Roth conversion.

The final proposal would limit new IRA contributions for total retirement savings totaling over $3.4 million. This includes the aggregate total of IRAs, 401(k)s, and any other pension plan balances. Once the total reaches $3.4 million at the end of the tax year, no new contributions are possible.

***

***

Capping IRA Growth?

To many Americans, especially the youth, this looks like a cap they will never see in their lifetime. Yet consider what $3.4 million will be worth in purchasing power 40 years from now, when today’s 30-year-olds will have to start RMDs. If inflation maintains its historical average of 3%, in 40 years $3.4 million will have the purchasing power of just over $1 million today. If someone wants to be assured they will never run out of money in retirement, $1 million only provides $30,000 a year of retirement income.

Capping IRA growth is another big deal.

Assessment

These are a few of the tax changes proposed by the President’s budget. The chances for any to become law in 2016 are remote, given that Congress is currently controlled by Republicans. However, the proposals do signal the current thinking of lawmakers. In considering their retirement planning, taxpayers would be advised to pay attention to such signals.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

1. Consider establishing an employee stock ownership plan (ESOP).

If you own a clinic or medical practice or business and need to diversify your investment portfolio, consider establishing an ESOP. ESOP’s are the most common form of employee ownership in the U.S. and are used by companies for several purposes, among them motivating and rewarding employees and being able to borrow money to acquire new assets in pretax dollars. In addition, a properly funded ESOP provides you with a mechanism for selling your shares with no current tax liability. Consult a specialist in this area to learn about additional benefits.

2. Make sure there is a succession plan in place.

Have you provided for a succession plan for both management and ownership of your medical practice, clinic or business in the event of your death or incapacity? Many business owners or physician-executives wait too long to recognize the benefits of making a succession plan. These benefits include ensuring an orderly transition at the lowest possible tax cost. Waiting too long can be expensive from a financial perspective (covering gift and income taxes, life insurance premiums, appraiser fees, and legal and accounting fees) and a non-financial perspective (intra-family and intra-company squabbles).

3. Consider the limited liability company (LLC) and limited liability partnership (LLP) forms of ownership.

These entity forms should be considered for both tax and non-tax reasons.

4. Avoid nondeductible compensation.

Compensation can only be deducted if it is reasonable. Recent court-decisions have allowed physician executives or business owners to deduct compensation when (1) the corporation’s success was due to the shareholder-employee, (2) the bonus policy was consistent, and (3) the corporation did not provide unusual corporate prerequisites and fringe benefits.

5. Purchase corporate owned life insurance (COLI).

COLI can be a tax-effective tool for funding deferred executive compensation, funding clinic or company redemption of stock as part of a succession plan, and providing many employees with life insurance in a highly leveraged program. Consult your insurance and tax advisers when considering this technique.

6. Consider establishing a SIMPLE retirement plan.

If you have no more than 100 employees and no other qualified plan, you may set up a Savings Incentive Match Plan for Employees (SIMPLE) into which an employee may contribute up to $12,500 per year if you’re under 50 years old and $15,500 a year if you’re over 50 in 2015. As an employer, you are required to make matching contributions. Talk with a benefits specialist to fully understand the rules and advantages and disadvantages of these accounts.

***

***

7. Establish a Keogh retirement plan before December 31st.

If you are self-employed and want to deduct contributions to a new Keogh retirement plan for this tax year, you must establish the plan by December 31st. You don’t actually have to put the money into your Keogh(s) until the due date of your tax return. Consult with a specialist in this area to ensure that you establish the Keogh or Keoghs that maximize your flexibility and your annual contributions.

8. Section 179 expensing.

Businesses and medical practices may be able to expense up to $25,000 in 2015 for equipment purchases of qualifying property placed in service during the filing year, instead of depreciating the expenditures over a longer time period. The limit is reduced by the amount by which the cost of Section 179 property placed in service during the tax year 2015 exceeds $200,000.

9. Don’t forget deductions for health insurance premiums.

If you are self-employed (or are a partner or a 2-percent S corporation shareholder-employee) you may deduct 100 percent of your medical insurance premiums for yourself and your family as an adjustment to gross income. The adjustment does not reduce net earnings subject to self-employment taxes, and it cannot exceed the earned income from the business under which the plan was established. You may not deduct premiums paid during a calendar month in which you or your spouse is eligible for employer-paid health benefits.

10. Review whether compensation may be subject to self-employment taxes.

If you are a sole proprietor, an active partner in a partnership, or a manager in a limited liability company, the net earned income you receive from the entity may be subject to self-employment taxes.

11. Don’t overlook minimum distributions at age 70½ and rack up a 50 percent penalty.

Minimum distributions from qualified retirement plans and IRAs must begin by April 1 of the year after the year in which you reach age 70½. The amount of the minimum distribution is calculated based on your life expectancy or the joint and last survivor life expectancy of you and your designated beneficiary. If the amount distributed is less than the minimum required amount, an excise tax equal to 50 percent of the amount of the shortfall is imposed.

12. Don’t double up your first minimum distributions and pay unnecessary income and excise taxes.

Minimum distributions are generally required at age seventy and one-half, but you are allowed to delay the first distribution until April 1 of the year following the year you reach age seventy and one-half. In subsequent years, the required distribution must be made by the end of the calendar year. This creates the potential to double up in distributions in the year after you reach age 70½. This double-up may push you into higher tax rates than normal. In many cases, this pitfall can be avoided by simply taking the first distribution in the year in which you reach age 70½.

***

***

13. Don’t forget filing requirements for household employees.

Employers of household employees must withhold and pay social security taxes annually if they paid a domestic employee more than $1,900 a year in 2015 (same as 2014). Federal employment taxes for household employees are reported on your individual income tax return (Form 1040, Schedule H). To avoid underpayment of estimated tax penalties, employers will be required to pay these taxes for domestic employees by increasing their own wage withholding or quarterly estimated tax payments. Although the federal filing is now required annually, many states still have quarterly filing requirements.

14. Consider funding a nondeductible regular or Roth IRA.

Although nondeductible IRAs are not as advantageous as deductible IRAs, you still receive the benefits of tax-deferred income. Note, the income thresholds to qualify for making deductible IRA contributions, even if you or your spouse is an active participant in a employer plan, are increasing.

The $100,000 income test for converting a traditional IRA to a ROTH IRA was permanently eliminated in 2010, allowing anyone to complete the conversion.

You can withdraw all or part of the assets from a traditional IRA and reinvest them (within 60 days) in a Roth IRA. The amount that you withdraw and timely contribute (convert) to the Roth IRA is called a conversion contribution. If properly (and timely) rolled over, the 10 percent additional tax on early distributions will not apply. However, a part or all of the distribution from your traditional IRA may be included in gross income and subjected to ordinary income tax.

Caution: You must roll over into the Roth IRA the same property you received from the traditional IRA. You can roll over part of the withdrawal into a Roth IRA and keep the rest of it. However, the amount you keep will generally be taxable (except for the part that is a return of nondeductible contributions) and may be subject to the 10 percent additional tax on early distributions.

15. Calculate your tax liability as if filing jointly and separately.

In certain situations, filing separately may save money for a married couple. If you or your spouse is in a lower tax bracket or if one of you has large itemized deductions, filing separately may lower your total taxes. Filing separately may also lower the phase out of itemized deductions and personal exemptions, which are based on adjusted gross income. When choosing your filing status, you should also factor in the state tax implications.

16. Avoid the hobby loss rules.

If you choose self-employment over a second job to earn additional income, avoid the hobby loss rules if you incur a loss. The IRS looks at a number of tests, not just the elements of personal pleasure or recreation involved in the activity.

17. Review your will and plan ahead for post-mortem tax strategies.

A number of tax planning strategies can be implemented soon after death. Some of these, such as disclaimers, must be implemented within a certain period of time after death. A number of special elections are also available on a decedent’s final individual income tax return. Also, review your will as the estate tax laws are influx and your will may have been written with differing limits in effect. In 2015, estates of $5,430,000 (up from $5,340,000 in 2014) are exempt from the estate tax with a 40 percent maximum tax rate (made permanent starting in tax year 2013).

18. Check to see if you qualify for the Child Tax Credit.

A $1,000 tax credit is available for each dependent child (including stepchildren and eligible foster children) under the age of 17 at the end of the taxable year. The child credit generally is available only to the extent of a taxpayer’s regular income tax liability. However, for a taxpayer with three or more children, this limitation is increased by the excess of Social Security taxes paid over the sum of other nonrefundable credits and any earned income tax credit allowed to the taxpayer. For 2015 (as in previous years), the income threshold is $3,000.

For more information concerning these financial planning ideas, please call or email us.

Dr. Gary L. Bode was Chief Executive Officer of Comprehensive Practice Accounting, Inc., a firm specializing in providing tax solutions to medical professionals. Originally, he was a board certified podiatrist and managing partner of a multi-office medical practice for a decade before earning his Master of Science degree in Accounting from the University of North Carolina. He then served as Chief Financial Officer [CFO] for a private mental healthcare facility. Today, Dr. Bode is a nationally known Certified Public Accountant, financial author, educator, and speaker. Areas of expertise include producing customized managerial accounting reports, practice appraisals and valuations, restructurings, and innovative financial accounting as well as proactive tax positioning and tax return preparation for healthcare facilities. He has been quoted in Newsweek.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 19, 2014 by Dr. David Edward Marcinko MBA MEd CMP™

Weighing the Costs

[By Lon Jefferies MBA CFP®]

As an informed investor and reader of this ME-P, you’re likely familiar with the difference between a traditional IRA/401(k) and a Roth IRA/401(k).

While the traditional account enables you to postpone taxes on both the income invested and its growth until the funds are withdrawn, a Roth account does not provide an initial tax benefit but investment growth is tax free. So which is better?

Let’s answer the question with some simple math. Suppose an investor in the 25 percent federal tax bracket invests $1,000 of pre-tax income, obtains an 8 percent annual return over the next 10 years, and is still in the 25 percent tax bracket in the future. Would this investor profit more investing in a traditional or a Roth account?

As the chart below illustrates, the investor in this scenario would end up with the exact same amount in either a traditional or a Roth account.

So does the decision to invest in a traditional or Roth retirement account not matter? Not so fast.

Constant Tax Rate

Traditional

Roth

Initial Tax Bill (25%)

$0

$250

Invested Amount (after-tax)

$1,000

$750

Future Investment Value

$2,159

$1,619

Future Tax Bill (25%)

$540

$0

After-Tax Value in 10 Years

$1,619

$1,619

Lower Tax Bracket in Future

Let’s assume our investor will have a reduced income when she retires in 10 years, causing her to be in the 15 percent tax bracket in the future. Perhaps the worker is in her prime earning years and will have less income during retirement. In this scenario, due to the up-front 25 percent tax bill, investing the funds in a Roth would lead to the same after-tax value of $1,619. But investing the funds in a traditional account would allow the full $1,000 to experience growth for 10 years, with a reduced future tax bill of 15 percent, leaving $1,835 of after-tax value in the account. This investor would benefit from delaying taxes into the future when she would be in a lower tax bracket.

Lower Tax Rate in the Future

Traditional

Roth

Initial Tax Bill (25%)

$0

$250

Invested Amount (after-tax)

$1,000

$750

Future Investment Value

$2,159

$1,619

Future Tax Bill (15%)

$324

$0

After-Tax Value in 10 Years

$1,835

$1,619

Higher Tax Bracket in Future

On the other hand, if the investor was in the 15 percent tax bracket this year but expected to be in the 25 percent bracket during retirement (potentially a young employee expecting his earnings to rise), paying taxes now at 15 percent would allow $850 to be invested, which after 10 years of 8 percent growth would be worth $1,835 tax free.

Higher Tax Rate in the Future

Traditional

Roth

Initial Tax Bill (15%)

$0

$150

Invested Amount (after-tax)

$1,000

$850

Future Investment Value

$2,159

$1,835

Future Tax Bill (25%)

$540

$0

After-Tax Value in 10 Years

$1,619

$1,835

Roth Advantages

What if you expect to pay a comparable tax rate both now and in the future? A Roth account offers several advantages in this scenario.

First, as taxes have already been paid on a Roth account, the government doesn’t require investors to take required minimum distributions (RMDs) from these accounts, whereas RMDs are required from traditional retirement accounts beginning at age 70½. Without RMDs, Roth accounts can grow tax free for the investor’s entire lifespan.

Additionally, upon death, Roth accounts pass to an investor’s heirs without any tax liability, while those who inherit a traditional retirement account must pay taxes on the assets.

***

***

Second, money withdrawn from a traditional retirement account before the investor is 59½ may be subject to a 10 percent penalty. Yet contributed funds to a Roth account (but not the growth on the contributed funds) can be withdrawn at any time without penalty. While withdrawing funds before retirement isn’t advisable, the added liquidity of the Roth account can prove useful in emergencies.

Finally, even if your income is expected to remain constant, investing in a Roth account allows you to lock in your taxes at today’s rate as opposed to taking the risk that national tax rates might be raised in the future.

If you’re unsure how your future tax bracket will compare to your current rate, diversify. Nothing prevents you from having both a traditional and a Roth retirement account. This not only allows you to hedge your bets, but puts you in a position during retirement to take distributions from your tax-deferred account in low-income years and from the tax-free account in years when you are in a high tax bracket.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Maximum annual IRA contribution (age 50 and over): $6,500

Maximum annual 401(k), 403(b), and 457 salary-deferral limit (under age 50): $17,500

Maximum annual 401(k), 403(b), and 457 salary-deferral limit (age 50 and over): $23,000

Maximum annual additions limit under defined contribution plan (example: SEP): $51,000

Maximum SIMPLE salary-deferral limit (under age 50): $12,000

Maximum SIMPLE salary-deferral limit (age 50 and over): $14,500

Additionally, the deduction for taxpayers making contributions to a traditional IRA is phased out for singles who are covered by a workplace retirement plan and have a modified adjusted gross income between $59,000 and $69,000.

For married couples filing jointly in which the spouse who makes the IRA contribution is covered by a workplace retirement plan, the income phase-out range is $95,000 to $115,000.

For an IRA contributor who is not covered by a workplace retirement plan and is married to someone who is covered, the deduction is phased out if the couple’s income is between $178,000 and $188,000.

Assessment

Finally, the AGI phase-out range for singles making contributions to a Roth IRA is $112,000 to $127,000.

For married couples filing jointly, the income phase-out range is $178,000 to $188,000.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

Posted on November 19, 2012 by Dr. David Edward Marcinko MBA MEd CMP™

The IRS Announces Major Changes

By Children’s Home Society of Florida Foundation

In IR 2012 77 (18 Oct 2012), the IRS announced multiple pension adjustments for 2013:

1. Elective Deferral – An individual with a 401(k) or 403(b) plan may defer income up to $17,500.

2. Catch-Up Contributions – Individuals age 50 and older may contribute an additional amount of $5,500 to a 401(k) or 403(b).

3. IRA Phase-Out – Contributions to a traditional IRA are phased out for individuals with a workplace retirement plan and modified adjusted gross incomes from $59,000 to $69,000. For married couples where the contributing spouse is covered by a workplace retirement plan, the phase-out range is $95,000 to $115,000. If the married couple IRA owner is not covered by a workplace plan, the phase-out range is $178,000 to $188,000.

4. Roth IRA Contributions – Taxpayers who are married may make Roth IRA contributions with a phase-out AGI of $178,000 to $188,000. Singles and heads of household have a phase-out range of $112,000 to $127,000.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

:strip_icc():format(webp)/what-is-the-rule-of-55-2894280-v1-fa6b42c5a8f647e8aa5776a550c121a5-1fc39bd85b914af9b2682601f2cefdf6.png)