Should I Stay … or … Should I Go?

By Guy P. Jones CFP® www.guypjones.com

Many ME-P readers may remember the song by the same name released in 1982 by English punk band, The Clash.

Many ME-P readers may remember the song by the same name released in 1982 by English punk band, The Clash.

If you do and you were in your late 20’s or early 30’s then, you are probably asking the same question about your hospital, medical clinic or employer-sponsored retirement plans, 401k, 403b, 457b and the like, right now.

History

Since the 401k was introduced back in 1978, it has been promoted as the “holy grail” of retirement savings vehicles, mostly by the mutual fund companies that it favors. Since the introduction of the 401k, there has been a gradual, yet steady, decline in employer-sponsored pension plans by private sector employers to the point that they are almost nonexistent.

Unless you work for a very large company or work in the public sector, your pension plan was phased out a long time ago. This has thrust a myriad of decisions regarding retirement planning on a workforce that is ill prepared to make the proper choices as to appropriate investment options. They therefore have relied on their employer to choose for them. In doing so, we now have a retirement system that is fraught with poor performing, high-cost, limited-choice, loss-incurring investment options.

Another Option?

But, wait, what if there was another, better option for some of you? What would you do if you were suddenly handed a “Get Outta Jail Free Card” from your employer-sponsored retirement plan? Well, guess what, you just have! It’s called an “In-Service Distribution” or “In-Service Transfer” to an Individual Retirement Account (IRA).

So what exactly is an In-Service Distribution or In-Service Transfer?

An In-Service Distribution allows workers to empty their 401(k) accounts once they hit 59½. This means that they can take cash out, pay any ordinary income taxes due and spend what’s left. The same goes for participants in government and not-for-profit savings plans like 403b, 457b, and TSP accounts. Or, they can roll all the money into an IRA without paying tax now which is an In-Service Transfer.

Need to Know:

- You first have to determine if your employer-sponsored plan even permits in-service distributions or transfers. It is determined by what was written in your company summary plan description.

- Many plans permit workers to take out or rollover to an IRA when you reach 59½, but some plans also permit in-service distributions for those under the age of 59½. This permits them to get in-service distributions of money rolled over from previous plans, employer (but not employee) pretax contributions, employee after-tax contributions, and account earnings. If they spend the cash, instead of rolling it over, they will owe an extra 10% penalty on the taxable amount.

- In doing an In-Service Transfer, you must make sure the rollover is to an IRA. In doing so, you avoid IRS taxation (and possibly penalties) on this money.

- Some plans have already pre-approved this option and in many cases can process the in-service distribution or transfer to an IRA right over the phone. Other plans require the completion of some paperwork which then has to be signed by your employer.

[The Retired Doctor’s Lounge]

What Funds are eligible for In-Service Distributions or In-Service Transfers?

When you decide to rollover money from your current employer-sponsored plan to your own IRA while still employed, here are the funds that will be available, subject to the summary plan description:

- Your employer contributions including match and profit sharing

- Your personal after-tax contributions

- Your pre-tax contributions when you reach age 59½.

Reasons to Do an In-Service Distribution or In-Service Transfer

- Unlimited Control — With an IRA, you are the account owner and have more control over your assets, more control over the investment choices, and are free from the restrictions of your employer-sponsored plan.

- Diversification — Most employer-sponsored plans offer limited investment options. Conversely, IRAs enable you to choose virtually any investment option including individual stocks, bonds, ETFs, mutual funds, real estate and precious metals. This flexibility can help you better diversify your retirement assets to meet your individual investment goals.

- Beneficiary Options — IRAs allow non-spouse beneficiaries to stretch distributions from an IRA over their lifetimes. This type of beneficiary distribution option not only results in greater distributions over their lifetime, but also enables the beneficiary to minimize the taxes owed on the distributions. This is not available in most employer-sponsored plans, which may limit distribution choices for your beneficiaries.

- Income Tax Withholding — Employer-sponsored plans have a mandatory 20% withholding tax on any cash distributions from the plan whereas IRAs allow you to choose whether you want tax withheld or not.

- ROTH IRA Conversion Option — Since 2010, any one regardless of their income can convert a Traditional pre-tax IRA to a ROTH IRA where future earnings are tax-free. In addition, you are now permitted to roll 401(k) money directly into a Roth IRA. Income taxes would be due, but not the 10% IRS penalty for pre-59½ withdrawals. If you want to do a gradual conversion of your traditional IRA to a ROTH IRA to minimize taxes, this would be another benefit to getting it out of the employer plan into an IRA now.

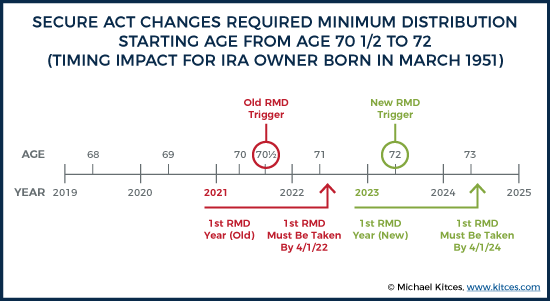

- Required Minimum Distributions — By getting your money out of the employer plan, you can do a conversion to a ROTH IRA to eliminate having to take RMDs starting at age 70½. RMDs affect the taxability of your Social Security benefits and by eliminating them, the taxation on your social security would be reduced.

- Protect IRAs from Investment Losses — Generally, what is offered in employer qualified plans are mutual funds which can and will lose money in the event of a market decline. By doing an in-service transfer to an IRA, you can choose options that will protect these funds from investment losses, lock in gains, and create an income stream that you can never outlive.

###

[Physician Retirement Funds]

Drawbacks to doing an In-Service Distribution or In-Service Transfer

- Age limitations — with employer plans, they allow participants who stop working at age 55 or older to take distributions without the 10% IRS penalty. In an IRA, you can’t take distributions until age 59½ without incurring the 10% penalty. If you plan to retire before age 59½, you may want to preserve penalty-free access to your retirement funds by not moving all of your 401(k) assets to an IRA before retirement

- Net Unrealized Appreciation (NUA) — tax treatment is not an option for distributions from IRAs. Therefore, if you hold highly appreciated company stock in your employer-sponsored plan, the transfer of that stock to an IRA eliminates any ability you may have to take advantage of NUA tax treatment.

- Creditor protection — while IRAs now have federal bankruptcy protection, other IRA creditor protection is still determined by state laws. Texas affords unlimited bankruptcy protection of IRA assets from creditors. Qualified plan assets continue to have broad federal creditor protection.

- New contributions to your existing plan — taking an in-service distribution may affect your ability to contribute to your employer-sponsored plan. Be sure to consult with your plan provider or employer HR department before implementing this.

- Cost — fees related to having your own IRA could be more costly than the investment options inside the 401k, although this can be controlled by careful selection of IRA options.

- After-tax dollars — after tax dollars are generally segregated in a qualified plan, and can often be distributed separately. If you move after-tax money into an IRA, that money becomes part of the non-deductible “basis” of the IRA and will not be separately accessible. To avoid paying tax again on your IRA “basis” when you take an IRA distribution, you must maintain careful records of the “basis” in your IRAs. This can become more of an issue in regards to doing a Roth IRA Conversion.

- Loans — loans are permissible through your employer plan, generally up to 50% of the account balance not to exceed $50,000. These loans can be paid back over a 5 year period or 10 years if used to purchase a home. Loans are not permitted in IRAs or ROTH IRAs.

Assessment

So, if this is so great then why doesn’t everyone take advantage of doing an in-service distribution or in-service transfer? The biggest reason is that employers don’t want plan participants to know about it or exercise this option. The second reason is that people don’t understand it or think that by transferring money out of their plan, they will incur tax and/or penalties. Make sure you go through the facts with a professional or your 401(k) company to understand the rules.

Nobody can be certain when the next market meltdown will be. With many Boomers now approaching retirement, you have to keep your eye on what will be the bulk of your retirement assets.

For my part as a financial professional, if your plan allows in-service distributions or transfers and you were debating whether to get out of your employer plan, I would give you the same advice that Jennie gave Forrest Gump when he was being chased by the bullies: RUN FORREST, RUN!!

The Author

Guy P. Jones & Associates

- 21 Stone Creek Place

- The Woodlands, TX 77382

- 832-677-1692

- 281-605-5370 fax

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Health Dictionary Series: http://www.springerpub.com/Search/marcinko

Practice Management: http://www.springerpub.com/product/9780826105752

Physician Financial Planning: http://www.jbpub.com/catalog/0763745790

Medical Risk Management: http://www.jbpub.com/catalog/9780763733421

Hospitals: http://www.crcpress.com/product/isbn/9781439879900

Physician Advisors: www.CertifiedMedicalPlanner.org

Filed under: Retirement and Benefits | Tagged: 401(k), 403(b), 457b, bonds, Employer-Sponsored Retirement Plans, ETFs, Guy P. Jones, In-Service Transfer, individual retirement account, IRA Conversion Options, Mutual Funds, precious metals., real-estate, Required Minimum Distributions, stocks, TSP accounts | 1 Comment »