BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: The S&P 500 hit its seventh record close in a row today, its longest win streak since May. The NASDAQ was buoyed by big tech, while the DJIA fell.

Commodities: Oil climbed thanks to a decision by OPEC+ to boost crude production at a more modest rate than experts expected. Gold continued its record run, rising above $3,900 for the first time ever, while bitcoin hovered just below a new all-time high.

Japan and France: Japanese stocks rose after the country elected its first female prime minister, and French stocks dropped after its prime minister quit less than a month into the job.

The ICE 3-Month USD LIBOR interest rate is the average interest rate at which a selection of banks in London are prepared to lend to one another in American dollars with a maturity of 3 months.

The Bank of America US High Yield Constrained Index is a market value-weighted index of all domestic high-yield bonds and Yankee high-yield bonds (issued by a foreign entity and denominated in U.S. dollars), including deferred interest bonds and payment-in-kind securities.

The ICE BofA BB-B US High Yield Constrained Index is composed of U.S. dollar-denominated corporate debt publicly issued in the U.S. market rated BB through B, based on an average of Moody’s, S&P and Fitch ratings, with issuer exposure capped at 2%.

ICE BofA U.S. Convertible Index tracks the performance of publicly issued, exchange-listed US dollar denominated convertible securities of US companies with at least $50 million face amount outstanding and at least one month remaining to the final conversion date. Index constituents are market capitalization-weighted and rebalanced monthly.

ICE BofA ML MOVE Index is a widely used measure of bond market volatility, similar to the VIX Index for stocks. The MOVE Index (also known as the Merrill Lynch Option Volatility Estimate) is a yield-curve-weighted index that tracks the market’s expectation of volatility in the U.S. bond market based on 1-month Treasury options.

ICE Exchange-Listed Preferred & Hybrid Securities Index tracks the performance of exchange-listed US dollar denominated hybrid debt, preferred stock and convertible preferred stock publicly issued by corporations in the US domestic market. Preferred stock and notes must have a minimum amount outstanding of $100 million; convertible preferred stock must have at least $50 million face amount outstanding. Index constituents are market capitalization-weighted subject to certain constraints. The index is re-balanced monthly.

Posted on December 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The winter solstice, also called the hibernal solstice, occurs when either of Earth’s poles reaches its maximum tilt away from the Sun. This happens twice yearly, once in each hemisphere (North and South). For that hemisphere, the winter solstice is the day with the shortest period of daylight and longest night of the year, and when the Sun is at its lowest daily maximum elevation in the sky. Each polar region experiences continuous darkness or twilight around its winter solstice.

Stat: $200 million. That’s how much drug manufacturer Endo Health Solutions paid the federal government for profiting from the opioid crisis and racking up $4 billion in unpaid taxes. (ProPublica)

US stocks bounced back Friday as investors digested key inflation data that showed a deceleration in price increases during the month of November.

The tech-heavy NASDAQ Composite (^IXIC) gained 1%. The Dow Jones Industrial Average (^DJI) added 1.2%, while the S&P 500 (^GSPC) rose 1.1%.

But the rebound wasn’t enough to overcome losses earlier in the week. All three major gauges finished the week lower. The NASDAQ gave up 1.8% while the Dow and the S&P both shed around 2%.

Investors waited for the Magnificent 7 stock reports to begin rolling last evening. The NASDAQ rose to a new high on optimism while the Dow Jones fell, and the S&P 500 split the difference.

Alphabet announced earnings after the bell yesterday, Microsoft and MetaPlatforms reveal their latest quarters today, Amazon and Apple on Thursday afternoon.

The 10-year Treasury yield hit a 4-month high this afternoon before paring back a bit as traders struggle to find a signal in all the market noise.

Oil rebounded a bit from yesterday’s terrible day, though it still ended the trading session lower.

No, I’m not talking about creepy, crawly insects. I’m referring to Standard & Poor’s Depository Receipts (SPDRs, or spiders), a derivative product, which combines many of the advantages of index funds with the superior trading flexibility of common stocks.

Creation

SPDRs were created in January 1993 by the American Stock Exchange. SPDRs are units in a trust holding the S&P 500 securities in proportion to their index weighting and which are adjusted as necessary to track changes made to the index by S&P. They pay quarterly cash dividend distributions based on the accumulated dividends paid by the stocks held in the SPDR trust minus an annual fee of about .19% of principal to cover trust expenses. They trade at approximately one-tenth the value of the index.

Conclusion

And so, your thoughts and comments on this ME-P are appreciated. Do you use SPDRs; why or why not? Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed: And, credible sponsors and like-minded advertisers are always welcomed.

Posted on January 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Four U.S. banks warned of lower interest income for this year on Friday, capping a week of dour commentary from the industry that has been under pressure from high deposit costs. After more than a year of booking strong profits on the back of the high interest they were able to charge on loans, banks are contending with a string of challenges heading into 2024, including weaker loan growth and potentially tougher capital rules.

Markets: Investors saw the S&P 500 and the Dow finished Friday at all-time highs. Soaring tech stocks helped the S&P blow past both intra-day and closing records set in January 2022.

Stock spotlight: Spirit Airlines had a bumpy ride this week. After falling for days, the budget carrier took off when it raised its forecast and said it still believes in the deal for JetBlue to buy it that a judge has blocked. Spirit and JetBlue also filed an appeal to try to save the merger.

Posted on December 31, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

***

The S&P 500 has climbed about 24% in 2023, hovering right around its all-time high. And, the NASDAQ Composite is up 44%, although the tech-heavy index still has some ground to cover before it starts carving out new all-time highs of its own.

Consulting firm McKinsey and Co. has agreed to pay $78 million to settle claims from insurers and health care funds that its work with drug companies helped fuel an opioid addiction crisis. The agreement was revealed late Friday in documents filed in federal court in San Francisco. The settlement must still be approved by a judge.

Under the agreement, McKinsey would establish a fund to reimburse insurers, private benefit plans and others for some or all of their prescription opioid costs. The insurers argued that McKinsey worked with Purdue Pharma – the maker of OxyContin – to create and employ aggressive marketing and sales tactics to overcome doctors’ reservations about the highly addictive drugs. Insurers said that forced them to pay for prescription opioids rather than safer, non-addictive and lower-cost drugs, including over-the-counter pain medication. They also had to pay for the opioid addiction treatment that followed.

Posted on December 7, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Real estate prices continued to cool in September—the first time prices declined for three straight months in nearly four years, which is a big deal. The change was especially noticeable out west.

For example, San Francisco and Seattle experienced the largest percentage decrease (2.9%) from August to September, according to the S&P CoreLogic Case-Shiller Indices. The report, which tracks home price fluctuations, showed “short-term declines and medium-term deceleration” in US housing prices, said Craig Lazarra, S&P Dow Jones Indices managing director.And, Las Vegas, Phoenix, San Diego, and Dallas also saw declines of more than 2%, in contrast to cities like Chicago and New York, where prices fell the least (less than 1%). But even as prices cool, housing overall has grown less affordable since the start of the pandemic—the year-over-year change was 10.6% nationally in September. Pair that with mortgage rate climbs, and you’ve got a market that’s seen a decline in activity for nine straight months. The good news is economists don’t expect things to spiral as far down as they did in ’08.

***

U.S. equities tumbled for a second day, as uncertainty regarding how aggressive the Fed will remain was met with increased recession fears.

Yesterday, the economic calendar was light, with the only notable report showing that the trade deficit widened less than expected. The equity front was also fairly quiet, as AutoZone beat earnings and revenue estimates, and shares of Meta Platforms fell after the Wall Street Journal reported that European Union regulators said the company should not require users to agree to personalized ads based on their online activity.

Treasury yields finished lower, and the U.S. dollar gained ground, while gold increased slightly.

Crude oil prices added to yesterday’s drop that came amid new restrictions on Russian oil, and after OPEC+ announced that it would leave its production target unchanged.

Stocks in Asia were mostly lower despite China continuing to ease COVID restrictions in some parts of the country, while European stocks fell amid a host of construction PMI data. The international markets also digested the Reserve Bank of Australia’s decision to hike its interest rate by 25 basis points, and its subsequent statement that was less dovish than expected.

Posted on September 30, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Major US indexes plunged after staging a relief rally in the prior session.

UK prime minister Liz Truss stood by proposed tax cuts, despite a chorus of vocal critics.

US Treasury yields hit multi-year highs this week as markets react to growing recession fears.

Stocks recovered from their steepest losses of the day, with the Dow Jones Industrial Average down over 600 points and the NASDAQ lower by nearly 4% at one point in the afternoon. Major indexes still ended deep in the red, though, with the S&P 500 hitting a new closing low for the year.

UK prime minister Liz Truss said that she stood by the government’s plan to cut taxes, which earlier in the week rocked markets and sent the pound falling last week to 37-year lows. Top economists including Paul Krugman, Mohamed El-Erian, and Nouriel Roubini have ripped into the new fiscal policy, warning that it could set UK inflation surging even higher and require more aggressive moves by the central bank, upping the risk of recession.

Posted on September 30, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Are We Experiencing a Bear Market Relief Rally?

***

Maybe yesterday – Not today!

By Staff Reporters

***

A bear market relief rally describes a period inside of a bear market in which prices of stocks temporarily increase during, sometimes quite sharply, before returning to new lows. This rise in prices is typically a short-lived increase, sometimes lasting anywhere from days to months, amidst an overall long-term downward trend in the market.

Posted on September 29, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Domestic Markets: The Dow and the S&P 500 both snapped six-day losing streaks after the Bank of England stepped in to calm investor fears about its teetering markets. That announcement helped crashing bonds recover in a big way, and the 10-year US Treasury yield (which moves inversely to prices) posted its biggest one-day drop since 2009.

Posted on September 24, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. stocks closed sharply lower with the Dow Jones Industrial Average ending at its lowest closing value since November 2020. All three major benchmarks suffered another week of losses as bond yields rose in the wake of the Federal Reserve’s interest rate hike on Wednesday.

The Dow Jones Industrial Average shed 486.27 points, or 1.6%, to close at 29,590.41.

The S&P 500 dropped 64.76 points, or 1.7%, to finish at 3,693.23.

The NASDAQ Composite slid 198.88 points, or 1.8%, to end at 10,867.93.

For the week, the Dow dropped 4% while the S&P 500 slid 4.6% and the NASDAQ tumbled 5.1%, according to Dow Jones Market Data. All three major indexes declined for a second straight week.

Posted on September 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Equity markets declined for the third straight day in the wake of the U.S. Federal Reserve‘s most recent increase to the benchmark interest rate.

The S&P 500 fell 31.94 points, or 0.84%, to 3,757.99, while the Dow Jones Industrial Average declined by 107.1 points, or 0.35%, to 30,076.68. The NASDAQ Composite dropped 153.39 points, or 1.37%, to 11,066.80.

All three indexes are on pace to end the week in the red, as investors worry continued rate hikes meant to combat high inflation, could result in a recession.

Posted on September 20, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. stocks found their solid footing in the final hour of back-and-forth trading after all three major indexes logged their worst week in three months. The S&P 500 climbed about 0.7%, while the Dow Jones Industrial Average rose nearly 200 points, or 0.6%. The tech-heavy NASDAQ gained 0.8%.

In the bond market, the benchmark U.S. 10-year Treasury touched 3.5%, its highest level since 2011, while the 2-year Treasury note inched toward 4%.

Posted on September 16, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Wall Street ended sharply lower today extending its losses in late afternoon trading as a raft of economic data failed to alter the expected course of aggressive tightening by the Federal Reserve amid growing warnings of global recession. The sell-off gathered momentum toward the end of the session, with market leaders including Microsoft Corp, Apple Inc and Amazon.com Inc hitting the tech-laden NASDAQ hardest.

After the bell, FedEx Corp tumbled 14.5% after the package delivery company said its fiscal first-quarter results were hit by global volume softness and it withdrew its financial forecast, saying it expected further deterioration of business conditions. FedEx’s warning sent shares of rival United Parcel Service down 5.7% in extended trade.

Earlier, in the trading session, the benchmark S&P 500 closed a hair above 3,900, seen by many analysts as a key technical support level that has been tested several times over the past two weeks.

Interest rate-sensitive banks helped soften the blue-chip Dow’s decline.

Posted on September 15, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The wobbly trading came as investors weighed another snapshot of inflation. Markets have been on edge about the possibility of a recession after a string of interest rate hikes by the Federal Reserve this year as the central bank fights inflation.

The S&P 500 rose 0.3% after wavering between small gains and losses much of the afternoon. The benchmark index was coming off its biggest drop since June 2020, which ended a four-day winning streak.

The Dow Jones Industrial Average closed 0.1% higher, while the Nasdaq composite rose 0.7%. Smaller company stocks also rose, pushing the Russel 2000 to a 0.4% gain.

Bond yields remained relatively stable after leaping higher on Tuesday. The yield on the two-year Treasury rose to 3.79% from 3.75% late Tuesday, when it soared on expectations for more aggressive interest rate hikes by the Federal Reserve.

The yield on the 10-year Treasury, which helps dictate where mortgages and rates for other loans are heading, held steady at 3.41%.

A report on inflation at the wholesale level showed prices are still rising rapidly, with pressures building underneath the surface, even if overall inflation slowed. It echoed a report on inflation at the consumer level Tuesday, which raised expectations for interest-rate hikes and triggered a rout for markets.

Posted on September 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

Stocks nosedived after a surprising inflation report showed prices rose more than expected last month. All three major averages logged their worst day since June 2020. Technology stocks led the way down, with the NASDAQ Composite plunging 5.2%. Tuesday’s session marks the seventh time this year the NASDAQ slid 4% or more, per data from Bespoke Investment Group. No declines of the same size were recorded last year, while 10 were experienced in 2020.

The S&P 500 sank 4.3%, while the Dow Jones Industrial Average erased 1,300 points, or roughly 4%.

The Bureau of Labor Statistics released its Consumer Price Index (CPI) for August early Tuesday, which showed prices rose 8.3% over the prior year and 0.1% over the prior month. Economists had expected an 8.1% increase in inflation over last year and a decline of 0.1% over the prior month.

Posted on September 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

For Friday, the Dow Jones Industrial Average rose 377.19 points, or 1.19%, to 32,151.71, the S&P 500 gained 61.18 points, or 1.53%, to 4,067.36 and the NASDAQ Composite added 250.18 points, or 2.11%, to 12,112.31. For the week, the Dow advanced 2.7%, the S&P 500 climbed 3.6% and the NASDAQ gained 4.1%. And, U.S. equity funds recorded outflows of $11.5 billion in the week to Wednesday, their largest outflow in 11 weeks, Bank of America Merrill said today. Volume on U.S. exchanges was 9.91 billion shares, compared with the 10.24 billion average for the full session over the last 20 trading days.

***

Commodities: In commodity news, oil traded up 3.1% to $86.16, while gold traded up 0.3% at $1,725.40. Silver traded up 1.1% to $18.65 on Friday while copper rose 0.6% to $3.5490.

Euro zone: European shares were higher today. The Eurozone’s STOXX 600 gained 1.57%, London’s FTSE 100 rose 1.38%, while Spain’s IBEX 35 Index rose 1.52%. The German DAX gained 1.39%, French CAC 40 rose 1.5% and Italy’s FTSE MIB Index gained 1.85%. Industrial production in France dropped by 1.6% from a month ago in July versus a revised 1.2% increase in June, while industrial production in Spain gained by 5.3% year-over-year in July.

Posted on August 31, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

According to the USBLS, the number of open Job positions ticked up unexpectedly in July, with around 11.2 million jobs available, slightly higher than June’s revised total of 11 million openings, according to the latest Job Openings and Labor Turnover Survey (JOLTS). Economists had expected there to be about 10.5 million jobs added, according to estimates from Refinitiv. The June total was revised up by about 300,000 positions.

Oil closed down almost $6 a barrel with global crude benchmark Brent falling beneath key $100 pricing, after a pro-Tehran television station out of London reported that Iran and the United States have reached a deal to revive a nuclear deal that could legitimately put the Islamic Republic’s oil back on the export market.

Stocks fell again on Wall Street, posting their third loss in a row as traders worry that high interest rates are here to stay for a while. The S&P 500 fell 1.1% bringing its loss in the past three days to 5.1%. The Dow Jones Industrial Average and the NASDAQ also fell. Energy companies fell along with sliding crude oil prices. Technology stocks and industrial companies were also weak. The yield on the 10-year Treasury held steady.

Posted on August 30, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Stocks closed broadly lower on Wall Street yesterday, adding to their hefty losses from last week when the Federal Reserve pledged to keep interest rates high as long as it takes to tame inflation.

The S&P 500 fell 0.7% after wavering between small gains and losses. The Dow Jones Industrial Average fell 0.6% and the NASDAQ composite lost 1%. Smaller company stocks also fell, pulling the Russell 2000 0.8% lower.

The selling was widespread, with technology and health care stocks among the biggest weights on the market. Only energy and utilities stocks rose.

Posted on July 27, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Microsoft (MSFT) – Get Microsoft Corporation Report posted weaker-than-expected fourth quarter earnings as a surging U.S. dollar blunted the impact of overseas demand for its flagship cloud computing division. Microsoft said revenues for Azure, its flagship cloud division, rose 40% from last year, slowing notably from its prior quarter gains in the mid to high 40-percent range as companies pulled back on digital infrastructure spending and the dollar continued its 2022 climb. Overall group revenues rose 12.4% to $51.87 billion for the three months ending in June, Microsoft’s fiscal fourth quarter, missing analysts’ estimates of a $52.45 billion tally and the company’s owned lowered guidance of between $51.94 billion to $54.74 billion. Microsoft’s bottom line rose 2% to $16.7 billion, as adjusted earnings rose 2.7% from last year to $2.23 per share, well shy of the the Street consensus forecast of $2.29 per share. Microsoft had forecast a range of between $2.24 and $2.32 per share in early June.

And, Google’s revenue growth during the past quarter decelerated to its slowest pace in two years as advertisers reined in their spending amid intensifying fears of an economic recession. The regression reported by Google’s corporate parent, Alphabet, is the latest sign that the tailwinds propelling big technology companies during the pandemic have shifted. The array of new challenges facing the industry has already caused the tech-driven NASDAQ composite index to plummet by 26% so far this year. In Alphabet’s case, revenue during the April-June period totaled $69.7 billion, a 13% increase from the same time last year.

On the other hand, Texas Instruments Inc., the maker of chips used in everything from washing machines to satellites, gave a bullish forecast for the current period, countering concern that a slowing economy is hurting demand for electronics. Third-quarter revenue will be $4.9 billion to $5.3 billion. That compares with the $4.94 billion average estimate from analysts. Profit will be as much as $2.51 a share, the company said, ahead of projections.That helped lift the shares 2.6% in extended trading Tuesday and gave a boost to other chip makers, such as Qualcomm Inc.

Posted on July 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The stock markets fell after new data showing U.S. manufacturing activity stalled and the service sector’s pandemic recovery has gone into reverse as a result of high inflation and mounting interest rate hikes, feeding concerns that the Federal Reserve’s efforts to cool decades-high price increases may force the economy into a recession. The Dow Jones Industrial Average fell 138 points, or 0.4%, to close at 31,899, while the S&P 500 fell 0.9% and the tech-heavy NASDAQ 1.9%; for the week, the indexes ended up 2%, 2.5% and 3%, respectively.

US social-media companies also saw more than $130 billion wiped off their stock-market values after disappointing revenue from Snap Inc. and a lackluster report from Twitter Inc. raised new concerns about the outlook for online advertising. The Snapchat parent plummeted 39%, sinking to its lowest level since March 2020. Meanwhile, Facebook parent Meta Platforms Inc. fell 7.6%, Pinterest Inc dropped more than 13%, and Google owner Alphabet Inc. declined 5.6% in its biggest one-day drop since March 2020. Twitter also reported quarterly results on Friday, though Wall Street remains focused on the company’s legal battle with Tesla CEO Elon Musk, who is attempting to withdraw from a deal to buy the company. The stock rose 0.8% on the day.

Posted on July 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

President Biden tested positive for the coronavirus, raising health concerns for the 79-year-old president and underscoring how the virus remains a persistent, if muted, threat in a country trying to put the pandemic in the past.

U.S. Indices

Change

Close

Dow Jones

+162.06

32036.90

NASDAQ

+161.96

12059.61

S&P500

+39.05

3998.95

SCHWAB1000

+129.50

13230.70

Senator Elizabeth Warren along with 22 more Democratic lawmakers are pushing the IRS to create its own free tax filing service. The bill also aims to allow eligible taxpayers to choose a “return-free option,” providing a pre-populated filing. “The average American spends 13 hours and $240 every year to file their taxes — that’s too much time and too much money,” Warren said in a press release. But some tax professionals say it’s not a realistic plan for the overburdened agency.

A case of polio has been identified in an un-vaccinated adult in Rockland County, according to a news release from the New York State Department of Health. The agency confirmed that the infection was transmitted from someone who received the oral polio vaccine, which has not been administered in the United States since 2000. Officials believe the virus may have originated outside the United States, where the oral vaccine is still administered.

he New York Times opinion columnist Paul Krugman published a mea culpa in column form flat out admitting he was wrong for thinking inflation wouldn’t be that bad. In his piece, titled, “I Was Wrong About Inflation,” the economics professor noted that he was on “Team Relaxed” when it came to fears of inflation and acknowledged that was a “very bad call.” Krugman began by recounting the “intense debate among economists about the likely consequences of the American Rescue Plan, the $1.9 trillion package enacted by a new Democratic president and a (barely) Democratic Congress.” He mentioned how he originally didn’t see the massive government spending bill as that dangerous for the economy. “Some warned that the package would be dangerously inflationary; others were fairly relaxed. I was Team Relaxed. As it turned out, of course, that was a very bad call,” he confessed.

Posted on July 21, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

The S&P 500 rose 0.6%, a day after soaring 2.8% for its best day in weeks. The NASDAQ led the market with a 1.6% gain. The Dow Jones Industrial Average added a more modest 0.2%. Smaller company stocks also closed higher. The Russell 2000 rose 28.62 points, or 1.6%, to 1,827.95.

In Europe, stocks slipped amid worries about whether Russia would restrict supplies of natural gas headed for the region after some maintenance on a key pipeline is scheduled to end. Germany’s DAX fell 0.2%, and French stocks dipped 0.3%. The continent is also preparing for the first increase in interest rates by the European Central Bank in 11 years as it tries to beat back inflation.

And, in the letter to investors, Tesla execs reveal the company has sold 75 percent of its Bitcoin holdings. Last year, Tesla made a $1.5 billion investment in bitcoin and announced that it would accept bitcoin as payment. Tesla started accepting Bitcoin in late March, then abruptly reversed itself in May, just 49 days later. In the latest report, Tesla says the value of its remaining “digital assets” is $218 million, which it had reported at around $1.2 billion in previous quarters.

Finally, Microsoft Corp. is eliminating many open jobs, including in its Azure cloud business and its security software unit, as the economy continues to weaken.

Posted on July 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. inflation climbed to new 41-year high of 9.1% in June, as gasoline prices surged. Soaring gasoline prices in June drove the rate of U.S. inflation to 9.1%, a nearly 41-year peak. The CPI jumped 1.3% last month to mark the third time in the last four months it’s topped 1%. Economists polled by The Wall Street Journal had forecast a 1.1% advance.

Because of June’s higher-than-expected inflation jump, it’s likely seniors will receive a 10.5% adjustment to their Social Security checks in early 2023, the Senior Citizens League, an advocacy group for older Americans opined.

Nearly a third of job recruiters said they experience extreme stress on a weekly basis because of their work, according to a December survey by human-resources analytics firm Veris Insights. The research found that 77% of high-ranking recruiters are open to changing jobs, along with 65% of HR professionals — a figure that rose 17 percentage points from September to November last year.

And, the S&P 500 slipped 0.5%, and the Dow Jones Industrial Average shed 210 points, or roughly 0.7%, though both indexes pared losses from sharper declines earlier in the day. The NASDAQ Composite closed down 0.2% but was an outlier for much of the session, trading in the green as technology stocks rebounded.

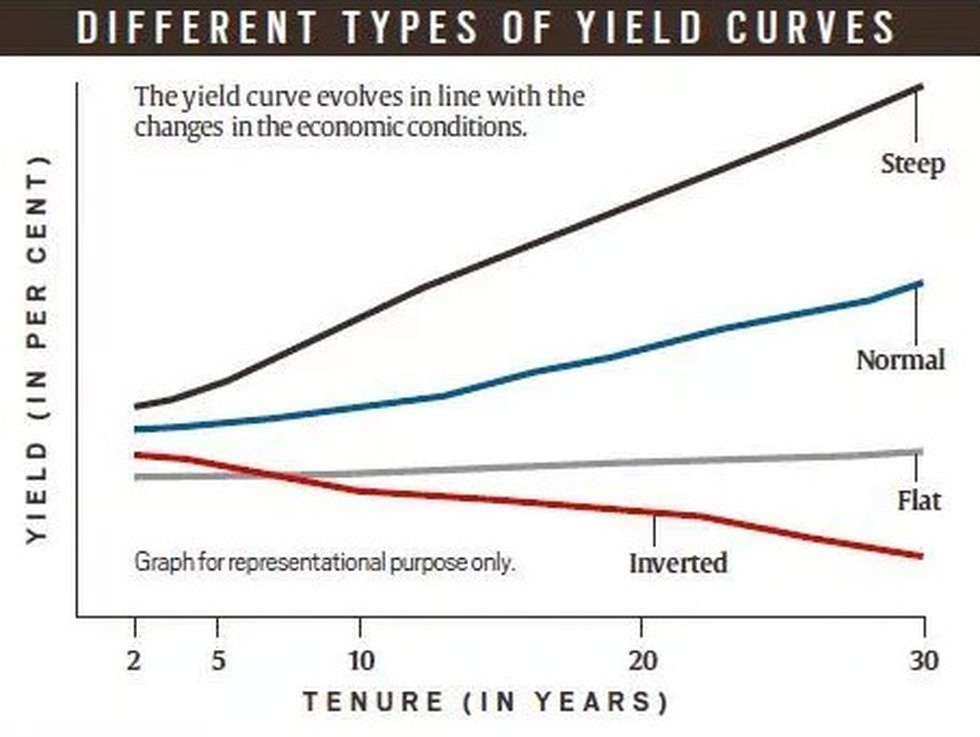

Finally, US Treasury yields were also in focus with the most dramatic moves happening at the front end of the yield curve. The 10-year stood at 3.04% following the CPI print, with 2-year yields rising as high as 3.17%, further inverting the yield curve. The curve “inverts” when yields on shorter-dated Treasuries rise above those of longer-dated ones and have typically preceded recessions on Wall Street.

Posted on July 13, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Morgan Stanley named Eli Gross and Simon Smith as new global co-heads of investment banking, as part of a leadership shakeup at the top of one of Wall Street’s most powerful deals advisory group. The current investment banking heads, Mark Eichorn and Susie Huang were elevated to executive chairs of the division to lead a newly formed group of senior bankers, according to an internal memo seen by Reuters.

The U.S. Bureau of Labor Statistics will release June data from the closely watched Consumer Price Index (CPI) today, which tracks the prices of a basket of daily goods and services. Investors use the CPI as one way to measure inflation, which has hit a 40-year high this year and forced the Federal Reserve to become increasingly hawkish in terms of monetary policy. While CPI data comes out every month, the reading will be watched more closely than normal, as are the current high levels of inflation.

America has decided the pandemic is over. The corona virus has other ideas. The latestomicron offshoot, BA.5, has quickly become dominant in the United States, and thanks to its elusiveness when encountering the human immune system, is driving a wave of cases across the country. The size of that wave is unclear because most people are testing at home or not testing at all. The Centers for Disease Control and Prevention in the past week has reported a little more than 100,000 new cases a day on average. But infectious-disease experts know that wildly underestimates the true number, which may be as many as a million, said Eric Topol, a professor at Scripps Research who closely tracks pandemic trends. Antibodies from vaccines and previous coronavirus infections offer limited protection against BA.5, leading Topol to call it “the worst version of the virus that we’ve seen.”

Posted on July 6, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Euro lost 10% versus the dollar this year and at $1.0238 EUR=EBS is close to the psychologically crucial parity point it last saw in mid-2002. It also hit new seven-year lows versus the Swiss franc and dropped against the sterling and the yen, but few observers are willing to call a bottom yet. Nomura’s analysts cut their euro/dollar target to $0.95 and said parity could be breached as soon as August. Citibank says a move to parity is “inevitable.” However, Nomura said that $0.95 was not that important historically, noting that the euro fell from $1.17 after its creation to $0.82 in October 2002. Extrapolating backwards using its legacy currencies, the euro traded as weak as $0.6444 in February 1985.

On the New York Mercantile Exchange, benchmark U.S. crude oil for August delivery fell $8.93 to $99.50 a barrel, its first dip below $100 since May 11th. Brent crude for September delivery fell $10.73 to $102.70 a barrel.

Finally, the Dow dropped 129.44 points, or 0.4%, to finish at 30,967.82; it had been down more than 700 points at its lows earlier in the session. The S&P 500 gained 6.06 points, or 0.2%, closing at 3,831.39. And, the NASDAQ Composite advanced 194.39 points, or 1.8%, to finish at 11,322.24.

Posted on July 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

Markets: The S&P’s drop of more than 21% was its biggest H1 plunge since 1970. Its second quarter was the worst since Q1 of 2020. And while the S&P is floundering in the bear market, the NASDAQ, which is loaded with tech stocks, has taken an even bigger licking: It’s plunged more than 30% since its peak last November. For example:

Netflix: down 71% YTD (the worst performer in the S&P)

Coinbase: down 81%

Even megacaps like Meta (-52%), Amazon (-38%), and Apple (-25%) haven’t been spared.

Ruja Ignatova promised her cryptocurrency, OneCoin, would become the next Bitcoin. The only problem: It didn’t exist. The FBI today added the Bulgarian-born Ignatova—accused of defrauding investors out of approximately $4.1 billion in a fake cryptocurrency scheme—to its most-wanted list. The 41-year-old has been on outstanding since October 2017, just days after a warrant was issued for her arrest in the U.S. In a press release, the FBI called OneCoin a “massive fraud scheme” and offered up to $100,000 for information leading to Ignatova’s arrest.

The U.S. Securities and Exchange Commission rejected a proposal from Grayscale to list a spot Bitcoin ETF on the NYSE Arca exchange, setting up a potential legal battle with the country’s biggest digital asset manager. The SEC said Grayscale’s request for an ETF listing, which it proposed as a conversion of its popular Grayscale Bitcoin Trust GBTC, didn’t meet the regulator’s standard of being “designed to prevent fraudulent and manipulative acts and practices” and “to protect investors and the public interest.” Grayscale said it would challenge the SEC’s decision in court, arguing that its approval of ETF’s that hold Bitcoin futures should “logically (make it) comfortable with ETFs that hold that same asset.”

Posted on June 27, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Predictions: The stock market could surge 7% this week as quarter-end re-balancing leads to a buying spree in equities, according to JPMorgan. The bank expects re-balancing trades to favor equities after a year-to-date decline of nearly 20%. “Next week’s re-balance is important since equity markets were down significantly over the past month, quarter and six-month time periods.”

Markets: With the S&P having plunged nearly 18% this year, expect W. Buffett to preach the value of value stocks (aka steady, non-flashy public companies). By one measure, they’re on track to beat growth stocks by the widest margin in more than two decades, according to the WSJ.

Global economy: Russia defaulted on its foreign-currency sovereign debt for the first time since the Bolshevik Revolution in 1918 after failing to pay bondholders $100 million worth of interest by the end of a 30-day grace period. The default marks the beginning of a complex legal journey for bondholders, but it’s not expected to have any major consequences for the Russian economy, which has already been battered by Western sanctions.

Posted on June 26, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

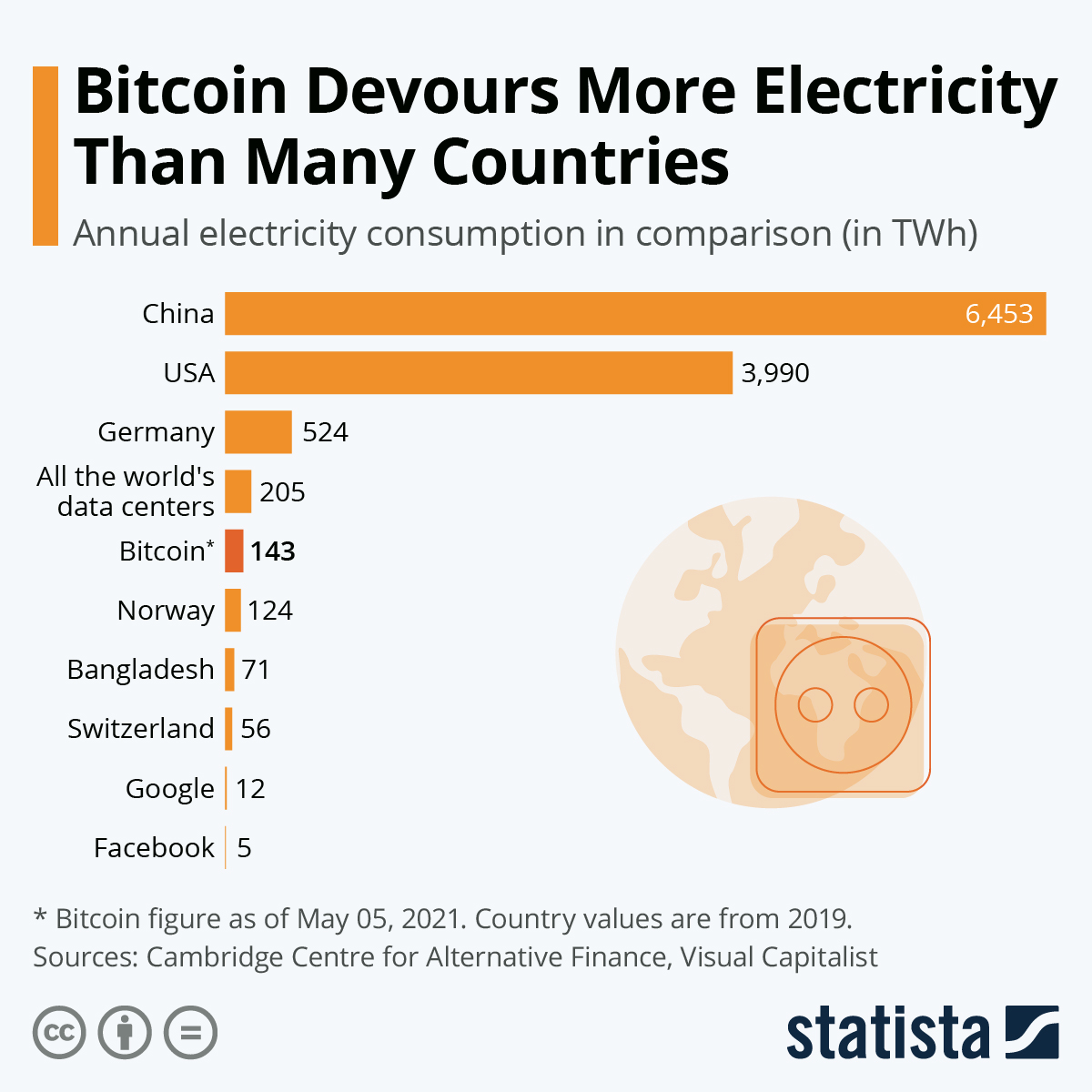

Bitcoin’s energy hunger, which has alarmed environmentalists and consumer advocates concerned about pollution and utility prices, comes from the process of mining new tokens. Bitcoin miners earn new tokens by validating transactions through an inherently energy-inefficient process, using specialized machines to solve complex puzzles. All that computing by all those machines has led to an energy appetite rivaling that of entire nations. Bitcoin’s annualized energy consumption has fallen from about 204 terawatt-hours (TWh) per year on June 11th to around 132 TWh per year on June 23rd. But even though its electricity use has plunged, it’s still very high — roughly equivalent to the amount of electricity Argentina uses in a single year.

Editor’s Note: Incidentally, colleague Mike Burry MD, the Scion Asset Management boss has also compared the crypto boom to the dot-com and housing bubbles, and cautioned that retail buyers of meme stocks and crypto are barreling towards the “mother of all crashes.” – DE Marcinko

Markets: Finally, and according to preliminary data, the S&P 500 gained 116.98 points, or 3.08%, to end at 3,912.71 points, while the NASDAQ Composite gained 380.21 points, or 3.38%, to 11,612.40. The Dow Jones Industrial Average rose 839.93 points, or 2.70%, to 31,505.59.

Posted on June 25, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

W. Buffett’s Berkshire Hathaway purchased roughly 9.5 million shares of Occidental over the past week at a cost of nearly $530 million, according to a new regulatory filing late on Wednesday. Buffett’s investing conglomerate now owns roughly 152 million shares of Occidental—a 16.3% stake worth nearly $8.5 billion that makes Berkshire by far and away the largest shareholder in the energy giant.

Sectors: Sectors like utilities, consumer staples, and real estate helped push the market higher yesterday. Today, however, we could see a lot spicier action. Index provider FTSE Russell is re-balancing its stock benchmarks, which will send investors scrambling to trade an estimated $112 billion just before the market closes. Among other tweaks it’s making, Russell will now label Meta, Netflix, and PayPal as “value” stocks.

Markets:

The Dow Jones Industrial Average DJIA, +2.68% gained 823.32 points, or 2.7%, to close at 31,500.68, its largest daily percentage gain since May 4.

The S&P 500 SPX jumped 116.01 points, or 3.1%, to finish at 3,911.74, its biggest daily percentage gain since May 18, 2020.

The NASDAQ Composite COMP, +3.34% surged 375.43 points, or 3.3%, to end at 11,607.62, its largest daily percentage gain since May 13.

For the week, the Dow booked a 5.4% gain, while the S&P 500 climbed 6.5% and the NASDAQ jumped 7.5%, according to Dow Jones Market Data. The Dow and S&P 500 each saw their biggest weekly gain since late May, while the NASDAQ had its best week since March.

Posted on June 20, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

CELEBRATE JUNETEENTH

The Markets: Can an extra day of rest change the market’s fortune?

As the Fed has escalated its fight against inflation, the S&P has fallen for 10 weeks out of the last 11. And not even American blue-chip firms have been spared from the carnage.

The Dow Jones Industrial Average closed below 30,000 for the first time since January 2021.

Posted on June 19, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Recession fears overtook the S&P 500 a day after the Fed meeting, reversing gains seen midweek.

The S&P 500 has been higher only 43.5% of all trading days in 2022, a gloomy marker, according to Bespoke Investment Group.

Meanwhile, it said the Fed is facing a “policy error” in focusing on headline inflation that’s swayed by high gas prices.

This year’s dismal performance in US equities worsened this week as a post-Fed rally fizzled and investors cemented the S&P 500 to one of its shabbiest mid-year showings in decades, all taking place with poor economic data piling up.

***

Goldman Sachs’ President John Waldron admitted at a June 2 conference that this is “among—if not the most—complex, dynamic environments” that he’s ever experienced. As a result, investment banks and economists are split on what the most likely outcome will be for the U.S. economy moving forward. Deutsche Bank has argued since April that we’re headed for a “major” recession, but Morgan Stanley’s CEO James Gorman said on Monday the odds of even a minor recession are more like 50-50.

Bank of America believes we will most likely avoid a recession altogether and instead face “extended weakness,” while the economist and Nobel laureate Paul Krugman appeared to side with more optimistic Fed officials arguing that we could be headed for a ”goldilocks” scenario, where economic growth slows enough to cool inflation without instigating a recession.

Posted on June 18, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

Per history, Bank of America’s Global Investment Strategy chief investment officer, Michael Hartnett, pointed out that the average peak-to-trough bear-market decline is 37.3% over a span of 289 days. Matching that pattern would put the end of current pain on Oct. 19th, 2022. This happens to mark the 35th anniversary of Black Monday, as the stock-market crash of 1987 is widely known. And according to statistical averages, the S&P 500 will likely bottom at 3,000.

Despite rising slightly, the S&P just posted its worst week since March 2020. Even energy stocks, one of the lone bright spots in the market, have taken a beating during this higher interest-rate era

The FDA just authorized two Covid-19 vaccines, Pfizer and Moderna, for kids under five—a year and a half after vaccines were approved for adults 16+.

Posted on June 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

For the domestic markets, the S&P 500 closed down 151 points, or 3.88%. It’s down nearly 22% since January. The Dow was down 876 points (2.79%) and the NASDAQ dropped 530 points (4.68%). And, investors were disappointed to learn that inflation is moving in the wrong direction. U.S. consumer prices surged 8.6% year-over-year in May, to a fresh 40-year high, led by higher prices for energy, food and housing.

For the first time in history, a gallon of regulargasoline now costs $5 on average nationwide, according to AAA, and experts predict gas prices could average $6 a gallon by August.

Moreover, nearly 70% of leading economists expect the US to tumble into a recession as the country grapples with inflation. In a Financial Times poll, the bulk of economists said they expect a recession to be declared in the first half of 2023. The poll comes after US inflation soared to 8.6% in May, outstripping economists’ expectations and piling the pressure on the Fed.

Finally, S&P Global says a 20% decline in the S&P 500 on a closing basis from its previous peak is all it takes to define a bear market. Which means that this bear market is already more than five months old, since the S&P 500 all-time high came on January 3rd, 2022.

Posted on June 13, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Blake Lemoine, an engineer for Google’sresponsible AI organization, described an AI system that he has been working on since last fall as sentient, with a perception of, and ability to express thoughts and feelings that was equivalent to a human child. He was promptly suspended.

Earnings Are Under Threat. Companies from Target to Microsoft have warned their results will be lower than expected, while analysts have trimmed earnings forecasts across industries. Investors will get further clarity next month when companies begin reporting results for the second quarter.

The S&P is in a historic slump having fallen in nine out of the past 10 weeks for just the third time since 1980. And cryptocurrencies, which trade 24/7, tumbled following another red-hot inflation report.

Posted on May 31, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Since the year began, the iconic Dow Jones Industrial Average entered correction territory with a decline of greater than 10%, while the S&P 500 (very briefly, on an intra-day basis) and NASDAQ Composite both pushed into a bear market. The latter has endured a peak-to-trough drop of as much as 31% in six months.

Terra launched a new version of its failed luna cryptocurrency, which plunged to $0. At its height, the old luna — “luna classic” — had a circulating supply of over $40 billion. The revived luna token is already trading on exchanges but its price is crashing.

Oil prices rose to a two-month high over the holiday weekend, while the average cost of a gallon of gas in the US hit a record of $4.62.

Americans say it takes exactly $2.2 million in net worth to be considered “wealthy,” according to a new Charles Schwab study. The figure is up slightly from 2021, when it sat at $1.9 million, but down from a pre-pandemic “wealthy” high of $2.6 million in 2019. The average net worth it takes to be “financially comfortable” sat at $774,000 in 2022 and is up from $624,000 in 2021, but down from a pre-pandemic high of $1.4 million in 2018.

Posted on May 27, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Twitter shares moved firmly higher after Tesla CEO Elon Musk added another $6.25 billion in equity to the financing package in his $44 billion takeover bid.

And, Tesla shares moved higher after Musk closed out a margin loan linked to his $44 billion takeover of Twitter , although gains were capped by a price target cut from analysts at Jefferies.

In March, the House of Representatives voted 414-5 in favor of the Securing a Strong Retirement Act of 2022. If passed by the Senate, and then signed into law by President Joe Biden, the act could represent a massive economic policy shift regarding retirement savings and investment. Now, the next generation known as the SECURE Act 2.0, expands on the original SECURE Act and includes provisions to boost the required minimum distribution (RMD) age from 72 to 75 over time, broaden automatic enrollment in retirement plans, and enhance 403(b) plans.

The DJIA rose for its fifth straight day, as the S&P and NASDAQ are poised to snap their seven-week losing streaks. Retailers are upbeat as shares of Macy’s, Dollar Tree, and Dollar General all soared after exceeding expectations and forecasting positive outlooks. But, Microsoft, Meta, Uber, and Nvidia slowed hiring, and Netflix and Robinhood recently laid off staff. SoftBank’s Vision Fund posted its worst annual loss as a result of the tech downturn.

Posted on May 21, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

“The Big Short” celebrity investor and colleague Michael Burry MD recently disclosed that he is short Apple stock. Could he be right about AAPL dipping even further from here? Famous hedge fund manager Michael Burry, the real-life character in “The Big Short”, became famous for his short position on subprime CDOs ahead of the 2008 crash. This time, he is shorting Apple stock. The bombshell news has come recently via a 13F filing released by Burry’s hedge fund.

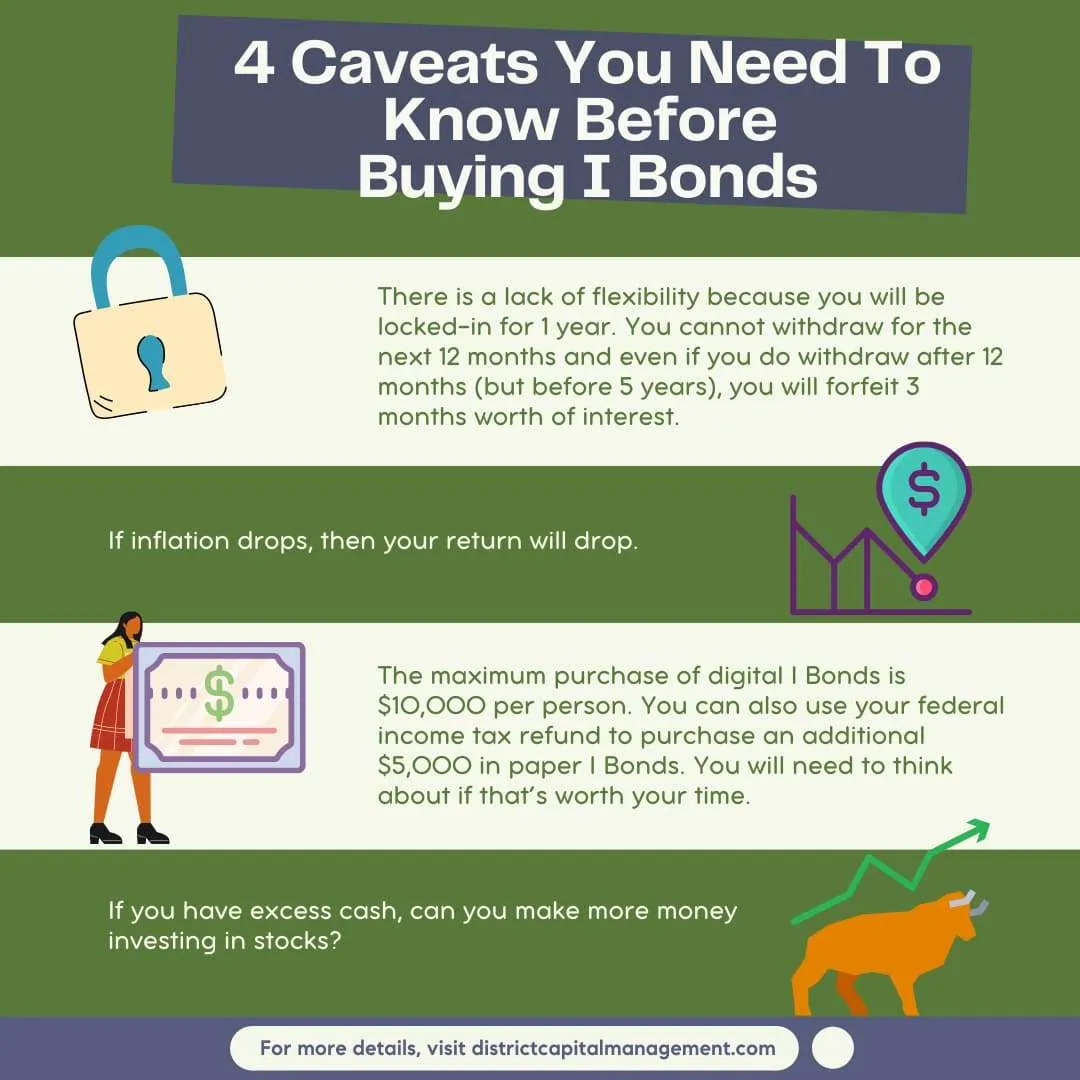

People searching for a respite from inflation have flooded the Treasury Department phone lines and website to try to buy Series I savings bonds, causing much longer waits than usual. It’s the latest example of outdated government computer systems causing anguish for Americans. On May 2nd, the Treasury Department announced that the inflation-protected I bonds will earn 9.62 percent interest at least until the end of October. A day later, TreasuryDirect, the website that people have to use to purchase the bonds, crashed.

Finally, Wall Street rumbled to the edge of a bear market after another drop for stocks briefly sent the S&P 500 more than 20% below its peak set early this year. The S&P 500 index, which sits at the heart of most workers’ 401(k) accounts, was down as much as 2.3% for the day before a furious comeback in the final hour of trading sent it to a tiny gain of less than 0.1%. It finished 18.7% below its record, set on January 3rd. The tumultuous trading capped a seventh straight losing week, its longest such streak since the dot-com bubble was deflating in 2001.

Posted on May 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Until recently, giga-cap technology stocks like Apple (NASDAQ: AAPL) and Microsoft (NASDAQ: MSFT) had large avoided the full brunt of the bear market in the NASDAQ, even as smaller companies lost 50% to 80% or more of their value.

However, over the past couple of months, some of the largest companies in the market, including Meta Platforms (NASDAQ: FB), Netflix (NASDAQ: NFLX), and Amazon.com (NASDAQ: AMZN), started to move sharply lower. Those big-name moves put a bigger dent in market capitalization-weighted benchmarks.

BroaderMarkets: But, the good news is that stocks surged on the best day for the NASDAQ since November 2020. The bad news is the S&P is now in its longest weekly losing streak since 2011, and the Dow’s weekly losing streak is its longest since 2001.

Posted on May 12, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Carvana, the fast-growing used-car seller based in Tempe, announced its plans to lay off 2,500 employees – more than 10% of its workforce – as losses mount. The company, which operates a network of high-profile vehicle “vending machines” including one at Loop 202 and Scottsdale Road, said the move was designed to “better align staffing and expense levels with sales volumes.” Carvana reported a $506 million loss in its first quarter ending March 31st, well above red ink of $82 million during the same stretch of 2021, despite a 56% jump in revenue to $3.5 billion and a 14% increase in vehicles sold.

And, new inflation data scared some investors, who continued to dump riskier assets like cryptocurrencies amid the ongoing market selloff: The price of Bitcoin fell up to 7%, to around $29,000, according to Coin Metrics, before paring back losses. The price of the Terra (LUNA) cryptocurrency has fallen by more than 99 per cent, wiping out the fortunes of crypto investors. Terra, which ranked among the top 10 most valuable cryptocurrencies, dropped below $1 on Wednesday, having peaked close to $120 last month.

The Dow Jones Industrial Average fell 215 points, or 0.7%, to 31,949 after swinging between gains and losses after the opening bell.

The S&P 500 shed 46 points, or 1.2%, to 3,954.

The NASDAQ Composite fell 296 points, or 2.5%, to 11,445.

The national average for a gallon of gas surged to $4.40, the highest price recorded by AAA since it began keeping track in 2000 (though lower when adjusted for inflation than the high-water mark in July 2008, when gas was $5.36 per gallon in today’s dollars).

Finally, the US federal government’s budget deficit has shrunk by some $1.57 trillion so far this fiscal year, driven by record receipts from a strong economy and a slowdown in spending as pandemic-era programs fade.

Posted on May 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Bitcoinis now almost 50% off its all-time high. If bitcoin is a store of value, it certainly hasn’t proven itself yet. With bitcoin’s price falling below $30,000 for the first time since July 2021, at least 40% of bitcoin investors are underwater.

***

***

Markets: The S&P fell below 4,000 points for the first time in more than a year as inflation concerns trampled a day down on Wall Street. Big Tech companies lost more than $1 trillion in market value over the past three trading sessions alone.

Posted on May 9, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Last night, the Dow Jones Industrial Average futures lost 191 points, down 0.6%, while the S&P 500 futures declined 0.8% and NASDAQ Composite futures fell 0.9%.

Crude oil futures (West Texas Intermediate) fell 0.2%, to $109.54 a barrel.

Tiger Global, the hedge fund with the most investments in private billion-dollar startups, is going through one of the worst stretches of any hedge fund in history, falling 44% so far this year and 15% in April alone.

This week’s notableeconomic events include: On Tuesday, the National Federation of Independent Business releases its Small Business Optimism Index for April. On Wednesday, the Bureau of Labor Statistics reports the consumer price index for April. On Thursday, the BLS releases the producer price index for April, and the Department of Labor reports initial jobless claims for the week ended on May 7. On Friday, the University of Michigan releases its Consumer Sentiment Index for May.

Posted on May 6, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Markets: After booming stocks had their worst day of the year because of raging inflation, slowing economic growth, and a potential recession.

Crypto: Bitcoin and other major cryptos like ethereum also tumbled in the aftermath of the FOMC announcement. They’ve typically tracked the performance of growth stocks, which have gotten hammered on the prospect of higher interest rates.

***

Almost every major online retailer reporting earnings with signs of a decline:

Wayfair shares cratered nearly 26% yesterday after announcing that its active customer count dropped 23.4% from a year ago.

Bed Bath & Beyond reported an 18% nosedive in online sales.

Etsy and eBay shares both dropped by double digits yesterday after giving weak guidance for the current quarter.

At least five senior executives from Meta’s fledgling e-commerce division have fled in the last six months.

Shopify shares plummeted about 15% on Thursday after posting much lower-than-expected earnings.

Posted on April 30, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

DEFINITION:

In finance, a stock index, or stock market index, is an index that measures a stock market, or a subset of the stock market, that helps investors compare current stock price levels with past prices to calculate market performance.

The Dow Jones Industrial Average DJIA, -2.77% dropped 939.18 points, or 2.8%, to close at 32,977.21.

The S&P 500 SPX, -3.63% dropped 155.57 points, or 3.6%, to finish at 4,131.93, re-entering correction territory.

The NASDAQ Composite COMP, -4.17% shed 536.89 points, or 4.2%, to end at 12,334.64.

Ironically, on Thursday, the Dow rose 614.46 points, or 1.9%, while the S&P 500 gained 2.5% and the NASDAQ Composite jumped 3.1%. The Dow and S&P 500 marked their best daily percentage climbs since March 9, while the NASDAQ saw its best day since March 16th, according to Dow Jones Market Data.

For the week, the Dow dropped 2.5%, the S&P 500 slumped 3.3% and the tech-laden NASDAQ lost 3.9%. In April, the Dow fell 4.9%, the S&P 500 tumbled 8.8% and the NASDAQ plunged 13.3%.

SCM: Supply chain bottlenecks are still stinging corporate giants. With China locking down cities at the first trace of Covid, American companies whose products are made in Chinese factories aren’t able to fulfill orders. Apple said Thursday that it would face up to $8 billion in losses due to restrictions in Shanghai.

Posted on April 27, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Dow Jones Industrial Average fell 809 points, or 2.4 percent today, as investors sold stock amidst concerns of coming recession.

The Dow faced a significant decline since trading opened. By the market’s close, it had reached one of its lowest closing values in the past year. Similar declines were observed on other market indices – including the S&P 500, which fell by 2.8 percent, and the NASDAQ Composite (comprising technology company stock), which lost 4 percent of its value.

The National Review and most experts ascribed the loss to stocks by big technology companies, whose increases in value have come to represent a sizeable portion of market indices. Alphabet, Apple, Microsoft, and Twitter all declined by several points. Each of these companies was due to present earnings reports after the close of trading, which investors did not expect to bode well.

Alphabet, in particular, announced slower sales growth and a drop in earnings from ad-revenue on Google and its other platforms. Netflix, which reported a decline in subscribers on Friday, had previously experienced a 30 percent decline in its stock price amounting to a loss of $54 billion.

Posted on April 25, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

After last week’s sharp decline, the S&P is down 5.7% so far in April and is on track for its worst monthly drop since March 2020, when the spreading COVID-19 pandemic blasted stocks.

And, battered U.S. stocks are facing a potentially painful stretch in the weeks ahead as hawkish Federal Reserve policy, rising bond yields, geopolitical uncertainty and the corporate earnings season fuel investor unease. For example:

REPORTINGCOMPANIES:

Monday: Germany business climate; Earnings from PepsiCo and Whirlpool

Tuesday: US consumer confidence; Earnings from 3M, General Electric, JetBlue, UPS, Warner Bros. Discovery, Alphabet, General Motors, Mondelez, Microsoft and Visa

Wednesday: Earnings from Boeing, Harley-Davidson, Kraft Heinz, Spotify, Ford Motor, Mattel, Meta and PayPal

Thursday: Bank of Japan policy decision; US first quarter GDP; Earnings from Caterpillar, Altria, Domino’s Pizza, Mastercard, Twitter, Amazon, Apple, Intel, Roku and Robinhood

Friday: Europe first quarter GDP and inflation data; US personal income and spending data; PCE Price Index; Earnings from ExxonMobil and Chevron

One measure of investor anxiety, the CBOE Volatility Index, known as Wall Street’s fear gauge, on Friday notched its largest one-day gain in about five months to close at a five-week high of 28.21.

The S&P 500 dropped and erased earlier gains. The Dow Jones Industrial Average also turned lower. The NASDAQ fell more than 2% and extended losses when the tech-heavy index was weighed down by a slide in Netflix. Meanwhile, Tesla (TSLA) shares rose after the electric vehicle-maker handily exceeded expectations in its fiscal first-quarter results.

***

***

Treasury bond yields climbed after Federal Reserve Chair Jerome Powell suggested the case for front-loading interest rate hikes with 50 basis-point increases in order to quickly address persistent inflationary pressures. San Francisco Federal Reserve President Mary Daly also suggested in an interview with Yahoo Finance that she would back a larger-than-typical 50 basis point interest rate hike following the Fed’s May meeting given current price pressures.

China: The nation’s securities regulator issued investor guidance for the country’s giant social security fund, just as the benchmark CSI 300 Index was heading toward the lowest level since June 2020.

Posted on April 21, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Markets: Yesterday was a tale of two markets. The Dow, which is home to blue-chip corporations like P&G, gained, while the NASDAQ, comprised of tech stocks, fell. Netflix is now the worst performing stock in the S&P this year.

Covid: The DOJ appealed a judge’s ruling that overturned a federal mask mandate for transportation. The move came at the suggestion of the CDC, which determined that people should still wear masks in indoor public transportation settings.

Homes: The median existing-home price in the US hit an all-time high of $375,300 in March, up 15% from the year before. With surging mortgage rates and higher home prices, the average borrower is paying ~38% more than they would have for the same home a year ago, according to Realtor.com.