BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on April 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler CFP™

***

***

Lately, I’ve been hearing the same question from clients and readers alike: “Is Social Security even going to be there in five years?” Fueling this concern is a recent viral comment from Elon Musk, who told Joe Rogan that Social Security is “the biggest Ponzi scheme of all time.” That quote has been repeated in every corner of the internet, stirring up uncertainty and fear.

Elon Musk is a genius, but his brilliance in technology and innovation doesn’t automatically translate into expertise in public policy. When it comes to Social Security, he’s outside his lane. Calling it a Ponzi scheme may make for a great soundbite, but it’s a fundamental mischaracterization.

Social Security is not a Ponzi scheme. Not even close.

A Ponzi scheme is a form of financial fraud that lures investors with the promise of high returns. Instead of earning those returns through legitimate investments, the scheme pays earlier investors using money from newer ones. Eventually, the model collapses when there aren’t enough new participants to keep it going, leaving most people with significant losses. This is what happened to those who trusted Bernie Madoff, operator of one of the worst Ponzi schemes in history. Ponzi schemes are illegal, deceptive, and doomed from the start.

Social Security, in contrast, is a government-run, pay-as-you-go tax program. It’s fully transparent; you know exactly where your money is going. The payroll taxes you and your employer pay are used to provide income to today’s retirees, people with disabilities, and surviving family members of deceased workers. This isn’t a con, it’s a social contract.

So why the confusion? Part of the issue is that Social Security does, on the surface, resemble the flow of a Ponzi scheme: money coming in from the young to support the old. But similarity in structure doesn’t make it fraudulent. The program does not promise high returns, it promises a modest, inflation-adjusted benefit to support people as they age.

Social Security does face challenges. The trust fund reserves, built up during years when payroll taxes exceeded payouts, are projected to run dry around 2033. If Congress does nothing, benefits will need to be cut by about 20%. That’s serious, but it’s a solvency issue, not a scam.

And the solvency issue is fixable. There are numerous bipartisan proposals to shore up the system for the long term, from raising the payroll tax cap to gradually adjusting benefits. These aren’t radical ideas, they’re common-sense repairs. A bipartisan mix of 100 CFPs in a room could work out a solution in two days.

When clients ask me if the system will be around in five years, what they’re really asking is: Can I trust it? Can I trust the government? Can I trust that my years of work and tax payments will mean something in retirement? These are not just policy questions. They are emotional questions based on fear of scarcity and a desire for security. When someone with Elon Musk’s influence wrongly calls Social Security a Ponzi scheme, his attention-grabbing soundbite shakes the emotional foundation of that trust.

If we’re serious about preserving Social Security, let’s start by calling it what it is: a commitment to our elders. A tax-supported promise to care for one another across generations.

Social Security is not a fraud, it’s a shared responsibility based on the kind of society we want and woven into the fabric of American life. Yes, it needs some adjustments, but it’s not broken. Rather than eroding public trust with misleading comparisons, we should be focused on debating public policy and how we can strengthen and sustain the program for future generations.

***

ME-P NOTE: An increase in Social Security benefits is on the horizon, providing a potential financial cushion against rising inflation. The Cost of Living Adjustment (COLA) for 2025 is set at 2.5% monthly, translating to an average annual increase of approximately $600 for beneficiaries. This adjustment is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers. While not guaranteed annually, COLA has historically been implemented in most years due to persistent inflationary trends.

An alternative investment is a financial asset that does not fall into one of the conventional investment categories. Conventional categories include stocks, bonds, and cash. Alternative investments can include private equity or venture capital, hedge funds, managed futures, art and antiques, commodities, and derivatives contracts. Real estate is also often classified as an alternative investment.

QUESTION: But what about a medical, podiatric or dental practice?

***

***

AnAlternate Asset Class Surrogate?

A medical practice is much like an alternative investment [AI], or alternate asset class in, two respects.

First, it provides the work environment that generates personal income which has been considered generous, to date.

Second, it has inherent appreciation and sales value that can be part of an exit (retirement) or succession planning transfer strategy.

Conclusion

So, unlike the emerging thought that offers Social Security payments as a surrogate for an asset classes; or a federally insured AAA bond – a medical practice might also be considered by some folks as an asset class within a well diversified modern investment portfolio.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

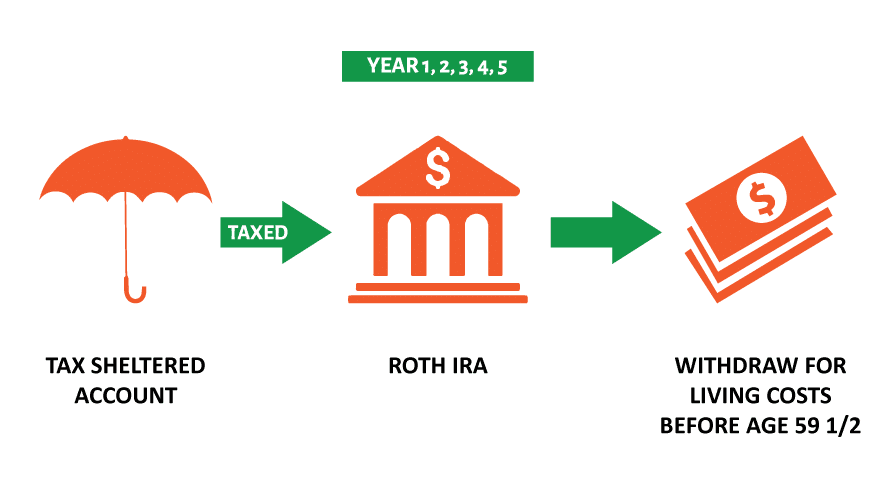

Why would a doctor consider a Roth IRA conversion?

By Staff Reporters

***

***

A Roth conversion involves transferring funds from a traditional retirement account—such as a 401(k), 403(b), or individual retirement account (IRA) funded with pre-tax dollars—into a Roth IRA.

The biggest benefit lies in the tax treatment of the converted funds. Once the funds are in the Roth IRA, future growth of those assets is tax-free. Withdrawals in retirement are also tax-free, assuming they meet certain criteria. As with any strategy, there are important considerations to keep in mind.

When you convert funds to a Roth IRA, the amount converted is taxable income in that tax year. For example, if you convert $100,000 from a traditional IRA to a Roth IRA, that $100,000 will be added to your taxable income in the conversion year.

Converting large amounts can result in a significant tax bill and may push you into a higher tax bracket. Even so, using retirement funds to pay taxes may make sense for those looking to convert large IRAs to reduce their future required minimum distributions (RMDs).

The timing of your Roth conversion matters too. Generally, it’s a good idea to convert when your income is lower—for example, after you’ve retired and before you begin drawing Social Security. You may also choose to convert over the course of several years to spread out the tax impacts. But if you can get comfortable with these considerations, a Roth conversion can provide you with benefits beyond tax-free growth and withdrawals.

Some of these benefits are:

Tax diversification. Having both traditional and Roth accounts allows you to manage your tax liability in retirement. For example, if your income in a given year is higher than expected, you can withdraw from the Roth IRA without increasing your taxable income.

No RMDs. Traditional IRAs and 401(k)s require you to begin taking RMDs at age 73. Roth IRAs have no RMD requirement during your lifetime. With a Roth account, you have more control over your retirement withdrawals and can leave the funds to grow for your heirs.

Benefits for heirs. Roth IRAs can be passed on to beneficiaries, who can inherit the account income tax-free. This means your heirs can enjoy the tax-free growth and withdrawals if the Roth IRA has been held for five years or more—a significant advantage, especially if your beneficiaries are in a higher tax bracket.

Posted on December 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITIONS

By Staff Reporters

***

***

Entitlement programs: From an economic overview or government budgeting perspective, entitlement programs are types of government programs that provide individuals with personal financial benefits (or sometimes special government-provided goods or services) to which an indefinite (but usually large) number of potential beneficiaries have a legal right when they meet specified eligibility requirements. The beneficiaries are normally individuals, but can also be organizations. The most important examples at the federal level in the U.S. include Social Security, Medicare, and Medicaid.

Environmental, Social, Governance (ESG) Criteria: The risk and/or opportunity to a company’s market valuation resulting from environmental, social and governance (ESG) factors. Depending on the sector, environmental and social factors include, but are not limited to, 1) climate change, 2) water stress, 3) product safety and quality (supply chain and manufacturing), 4) cybersecurity and data privacy, and 5) human capital management. Regardless of the sector, governance factors include: 1) business (mis)conduct, 2) board composition, independence and entrenchment, 3) accounting practices, 4) ownership structure, and 5) executive pay-for-sustainability performance alignment.

Environmental, Social, Governance (ESG) Integration: The structural incorporation of financially-relevant information on Environmental, Social and Governance (ESG) factors into the investment decision-making process.

You’ve got a sense of your ideal retirement age. And you’ve probably made certain plans based on that timeline. But what if you’re forced to retire sooner than you expect? Aging baby-boomers, corporate medicine, the medical practice great resignation and/or the pandemic, etc?

Early retirement is nothing new, but it’s clear how much the COVID-19 pandemic has affected an aging workforce. Whether due to downsizing, objections to vaccine mandates, concerns about exposure risks, other health issues, or the desire for more leisure time, the retired general population grew by 3.5 million over the past two years—compared to an annual average of 1 million between 2008 and 2019—according to the Pew Research Center.1 At the same time, a survey conducted by the National Institute on Retirement Security revealed that more than half of Americans are concerned that the COVID-19 pandemic has impacted their ability to achieve a secure retirement.2

***

***

There’s no need to panic, but those numbers make one thing clear, says Rob Williams, managing director of financial planning, retirement income, and wealth management for the Schwab Center for Financial Research. Flexible and personalized financial planning that addresses how you’d cope if you had to retire early can help you make the best use of all your resources.

So – Here are six steps to follow. We’ll use as an example a person who’s seeing if they could retire five years early, but the steps remain the same regardless of your individual time frame.

Step 1: Think strategically about pension and Social Security benefits

For most retirees, Social Security and (to a lesser degree) pensions are the two primary sources of regular income in retirement. You usually can collect these payments early—at age 62 for Social Security and sometimes as early as age 55 with a pension. However, taking benefits early will mean that you get smaller monthly benefits for the rest of your life. That can matter to your bottom line, even if you expect Social Security to be merely the icing on your retirement cake.

On the Social Security website, you can find a projection of what your benefits would be if you were pushed to claim them several years early. But if you’re part of a two-income couple, you may want to make an appointment at a Social Security office or with a financial professional to weigh the potential options.

For example, when you die, your spouse is eligible to receive your monthly benefit if it’s higher than his or her own. But if you claim your benefits early, thus receiving a reduced amount, you’re likewise limiting your spouse’s potential survivor benefit.

If you have a pension, your employer’s pension administrator can help estimate your monthly pension payments at various ages. Once you have these estimates, you’ll have a good idea of how much monthly income you can count on at any given point in time.

***

Step 2: Pressure-test your 401(k)

In addition to weighing different strategies to maximize your Social Security and/or pension, evaluate how much income you could potentially derive from your personal retirement savings—and there’s a silver lining here if you’re forced to retire early.

Rule of 55

Let’s say you leave your job at any time during or after the calendar year you turn 55 (or age 50 if you’re a public safety employee with a government defined-benefit plan). Under a little-known separation-of-service provision, often referred to as the “rule of 55,” you may be able take distributions (though some plans may allow only one lump-sum withdrawal) from your 401(k), 403(b), or other qualified retirement plan free of the usual 10% early-withdrawal penalties. However, be aware that you’ll still owe ordinary income taxes on the amount distributed.

This exception applies only to the plan (including any consolidated accounts) that you were contributing to when you separated from service. It does not extend to IRAs.

4% rule

There’s also a simple rule of thumb suggesting that if you spend 4% or less of your savings in your first year of retirement and then adjust for inflation each year following, your savings are likely to last for at least 30 years—given that you make no other changes to your withdrawals, such as a lump sum withdrawal for a one-time expense or a slight reduction in withdrawals during a down market.

To see how much monthly income you could count on if you retired as expected in five years, multiply your current savings by 4% and divide by 12. For example, $1 million x .04 = $40,000. Divide that by 12 to get $3,333 per month in year one of retirement. (Again, you could increase that amount with inflation each year thereafter.) Then do the same calculation based on your current savings to see how much you’d have to live on if you retired today. Keep in mind that your money will have to last five years longer in this instance.

Knowing the monthly amount your current savings can generate will give you a clearer sense of whether you’ll have a shortfall—and how large or small it might be. Use our retirement savings calculator to test different saving amounts and time frames.

Step 3: Don’t forget about health insurance, doctor!

Nobody wants to spend down a big chunk of their retirement savings on unanticipated healthcare costs in the years between early retirement and Medicare eligibility at age 65. If you lose your employer-sponsored health insurance, you’ll want to find some coverage until you can apply for Medicare.

Your options may include continuing employer-sponsored coverage through COBRA, insurance enrollment through the Health Insurance Marketplace at HealthCare.gov, or joining your spouse’s health insurance plan. You may also find discounted coverage through organizations you belong to—for example, the AARP.

Step 4: Create a post-retirement budget

To make sure your retirement savings will cover your expenses, add up the monthly income you could get from pensions, Social Security, and your savings. Then, compare the total to your anticipated monthly expenses (including income taxes) if you were to retire five years early and are eligible, and choose to file, for Social Security and pension benefits earlier.

Take into account various life events and expenditures you may encounter. You may not pay off your mortgage by the date you’d planned. Your spouse might still be working (which can add income but also prolong certain expenses). Or your children might not be out of college yet.

You’re probably fine if you anticipate that your monthly expenses will be lower than your income. But if you think your expenses would be higher than your early-retirement income, some suggest that you take one or more of these measures:

Retire later; practice longer.

Save more now to fill some of the potential gap.

Trim your budget so there’s less of a gap down the road.

Consider options for medical consulting or part-time work—and begin to explore some of those opportunities now.

To the last point, finding a physician job later in life can be challenging, but certain employment agencies specialize in this area. If you can find work you like that covers a portion of your expenses, you’ll have the option of delaying Social Security and your company pension to get higher payments later—and you can avoid dipping into your retirement savings prematurely.

When you retire early, you have to walk a fine line with your portfolio’s asset allocation—investing aggressively enough that your money has the potential to grow over a long retirement, but also conservatively enough to minimize the chance of big losses, particularly at the outset.

“Risk management is especially important during the first few years of retirement or if you retire early,” Rob notes, because it can be difficult to bounce back from a loss when you’re drawing down income from your portfolio and reducing the overall number of shares you own.

To strike a balance between growth and security, start by making sure you have enough money stashed in relatively liquid, relatively stable investments—such as money market accounts, CDs, or high-quality short-term bonds—to cover at least a year or two of living expenses. Divide the rest of your portfolio among stocks, bonds, and other fixed-income investments. And don’t hesitate to seek professional help to arrive at the right mix.

Many people are unaccustomed to thinking about their expenses because they simply spend what they make when working, Rob says. But one of the most valuable decisions you can make about your life in retirement is to reevaluate where your money is going now.

This serves two aims. First, it’s a reality check on the spending plan you’ve envisioned for retirement, which may be idealized (e.g., “I’ll do all the home maintenance and repairs!”). Second, it enables you to adjust your spending habits ahead of schedule—whichever schedule you end up following. This gives you more control and potentially more income.

Step 6: Reevaluate your current spending

For example, if you’re not averse to downsizing, moving to a less expensive home could reduce your monthly mortgage, property tax, and insurance payments while freeing up equity that could also be invested to provide additional monthly income.

“When you are saving for retirement, time is on your side”. You lose that advantage when you’re forced to retire early, but having a backup plan that anticipates the possibility of an early retirement can make the unknowns you face a lot less daunting.

Posted on April 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

DEFINITION: Tax season is the period of time, generally between January 1st and April 15th of each year, when individual taxpayers prepare to report their taxable income to the federal government and, in most cases, to the government of the state in which they live.

Some Year-End Preparation for the Upcoming Tax Filing Season

The filing season for 2023 tax returns us now upon us. A little advance preparation can prevent stressful tax time surprises for doctors and all medical professionals. Here are some important steps you can take now to set yourself up for worry-free tax filing:

Do one last withholding checkup. Time is running out to adjust your paycheck withholding to make sure you have paid enough tax throughout 2023. You can use the online IRS Withholding Estimator tool to make sure your numbers are on track.

If your name changed in 2023, report the change to the Social Security Administration as soon as possible, preferably before the end of the year.

Locate your bank account information, including both your account number and the bank routing number, so you can receive your tax refund by direct deposit.

Watch for year-end income statements, especially in late January and early February. These statements may include W-2 forms, along with 1099-NEC, 1099-MISC, 1099-INT, 1099-G and other 1099 forms. Note that some of these forms may come by mail, while others may be sent to you electronically. Keep all of the forms together and organized.

Organize records for tax deductions and credits. These records may include Form 1095-A (Health Insurance Marketplace Statement), tuition statements (Form 1098-T), medical bills, mortgage interest statements, and home energy improvement or clean vehicle receipts or invoices.

Waiting until the last minute to try to assemble these documents can lead to missing the filing deadline, so start early.

Posted on October 21, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The U.S. government on Friday posted a $1.695 trillion budget deficit in fiscal 2023, a 23% jump from the prior year as revenues fell and outlays for Social Security, Medicare and interest costs on the federal debt rose significantly.

The Treasury Department said the deficit was the largest since a COVID-fueled $2.78 trillion gap in 2021 and marks a major return to ballooning deficits after back-to-back declines during President Joe Biden’s first two years in office. The deficit comes as Biden is asking Congress for $100 billion in new foreign aid and security spending, including $60 billion for Ukraine and $14 billion for Israel, along with funding for U.S. border security and the Indo-Pacific region.

The S&P 500® Index was down 53.84 points (1.3%) at 4,224.16, down 2.4% for the week; the Dow Jones Industrial Average (DJI) was down 286.89 points (0.9%) at 33,127.28, down 1.6% for the week; the NASDAQ Composite was down 202.37 points (1.5%) at 12,983.81, down 3.2% for the week.

The 10-year Treasury note yield was up about 8 basis points at 4.907%.

CBOE’s Volatility Index (VIX) was up 0.26 at 21.71.

Small-cap stocks, which are considered to be more exposed to economic uncertainty, were also soft, as the Russell 2000 Index (RUT) dropped to a 12-month low and was 2.2% lower for the week.

Gold futures rose 2.3% for the week and ended near a three-month high, as the fighting in the Middle East fueled demand for assets considered to be safe havens. Volatility based on the VIX spiked to its highest level since March.

Posted on September 15, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The forecast for next year’s Social Security increase rose to 3.2% from 3% on Wednesday after the government said inflation ticked up in August. Annual inflation in August rose to 3.7%, from 3.2% in July but off a 40-year high of 9.1% in June 2022. Without the volatile food and energy sectors, the so-called “core” inflation rate was 4.3%, down from July’s 4.7%.

***

Illegal drugs are expected to be one of the biggest threats to national security in 2024 as overdose deaths topped 100,000 in the last year, according to the Department of Homeland Security’s annual threat study. In its report released Thursday, DHS said it expects illegal drugs produced in Mexico and sold in the United States will continue to kill more Americans than any other threat.

***

U.S. stocks ended sharply higher and the greenback jumped on Thursday as robust economic data failed to budge expectations that the Federal Reserve will leave its key interest rate unchanged next week. The rally boosted a broad array of assets. All three major stock indexes ended higher, as did all 11 major sectors of the S&P 500. The dollar jumped to a six-month high, 10-year Treasury yields rose, and crude oil futures hit their highest this year, helping energy stocks outperform the broader market.

A spate of economic data released before the opening bell showed energy prices, specifically gasoline, were largely responsible for a hotter-than-expected producer prices print and a consensus-beating retail sales reading.

***

Here is where the major benchmarks ended:

The S&P 500 Index was up 37.66 points (0.8%) at 4,505.10; the Dow Jones Industrial Average was up 331.58 points (1.0%) at 34,907.11; the NASDAQ Composite (COMP) was up 112.47 points (0.8%) at 13,926.05.The 10-year Treasury note yield (TNX) was up about 4 basis points at 4.286%. CBOE’s Volatility Index (VIX) was down 0.69 at 12.79.

Retailers were among the market’s strongest sectors Thursday in the wake of stronger-than-expected August retail sales reported by the Commerce Department. Energy companies also climbed as crude oil futures extended a rally and topped $90 a barrel for the first time since mid-November. Small-cap stocks joined the upswing, with the Russell 2000 Index (RUT) rising nearly 1.5% and ended at a one-week high. Volatility based on the VIX fell under 13.00 and near pre-pandemic levels of early 2020.

Posted on July 16, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

Supplemental Security Income

By Staff Reporters

***

***

Stocks popped 2% this week, as investors expect the Fed to soon pause or dial back interest rates after the release of the June inflation report. Central bankers have raised rates from zero to over 5% since March of last year, a move that led the S&P 500 to shed 20% in 2022.

And yet, No SSI for you!

DEFINITION: Supplemental Security Income (SSI) is a means-tested program that provides cash payments to disabled children, disabled adults, and individuals aged 65 or older who are citizens or nationals of the USA. SSI was created by the Social Security Amendments of 1972 and is incorporated in Title 16 of the Social Security Act The program is administered by the Social Security Administration (SSA) and began operations in 1974.

Individuals or their helpers may start the application for SSI benefits by completing a short form on SSA’s website. SSA staff will schedule an appointment for the individual or helper within 1–2 weeks and complete the process.

SSI was created to replace federal-state adult assistance programs that served the same purpose, but were administered by the state agencies and received criticism for lacking consistent eligibility criteria. The restructuring of these programs was intended to standardize the eligibility requirements and level of benefits. Although administered by SSA, SSI is funded from the U.S. Treasury general funds, not the SS Trust Fund. As of July 2022, the program provides benefits to approximately five million Americans.

The Social Security Administration gives, and the Social Security Administration takes away — at least when it comes to beneficiaries who qualify for Supplemental Security Income (SSI) payments.

July is one of the months when the agency doesn’t issue an SSI check. Because of a quirk in the payment schedule, SSI beneficiaries get two payments in March, June, September and December, while no payments are deposited in January, April, July and October.

Posted on June 29, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The new magic number for retirement is up slightly from last year, when U.S. adults said they believed they needed $1.25 million to retire comfortably, according to new findings from Northwestern Mutual. High-net-worth individuals – those with more than $1 million in investible assets – believe they’ll need $3 million to retire comfortably.

There’s quite a gap, however, between what people have now and what they think they’ll need. The average amount that U.S. adults have saved for retirement is only $89,300, up 3% from $86,869 in 2022, Northwestern Mutual found.

***

Interestingly, more than four in 10 Americans (42%) said they could imagine a time when Social Security no longer exists, according to the research. And yet, people are relying on Social Security to provide 28% of their overall retirement funding. That’s more than personal savings (22%) and equal to retirement savings (28%).

Gen Z and millennials have tempered expectations – they anticipate Social Security will provide 15% and 19% of their overall retirement funding, respectively. That’s a significant drop from what boomers+ say – 38%.

Posted on June 20, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The average balance in employer-sponsored savings plans last year was $112,572, well below the $141,542 recorded in 2021. That’s according to the latest annual report, “How America Saves,” from investment firm Vanguard, which serves as record keeper for defined contribution plans that, combined, have nearly 5 million participants with a median age of 43. Such plans include 401(k)s and 403(b)s, as well as a much smaller universe of plans that employers simply put money into for employees and then employees direct how that money is invested.

“Vanguard participants’ average account balances decreased by 20% since year-end 2021, driven primarily by the decrease in equity and bond markets over the year,” according to the report.

And, the numbers look worse if you consider the median balance, which was just $27,376 last year, down from $35,345 in 2021. The median in some ways is a truer read on the state of employees’ retirement savings since it is the middle point — meaning half of accounts have higher balances, and half have lower ones.

***

According to the Social Security Administration, Social Security benefits make up about a third of the income of the elderly. In general, single people depend more heavily on Social Security checks than do married people. In 2023, the average monthly retirement income from Social Security is $1,827.

Keep in mind, though, that your Social Security benefits could be smaller. If you don’t have 35 years of work under your belt when you start claiming benefits, if your earnings were consistently low or if you claim benefits starting at age 62 rather than waiting until your full retirement age (or age 70, if you want maximum benefits), then you can expect a small monthly check. There’s also a gender gap in Social Security income. Women, because they tend to earn less and work for fewer years, draw smaller Social Security checks than men do.

Posted on October 15, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

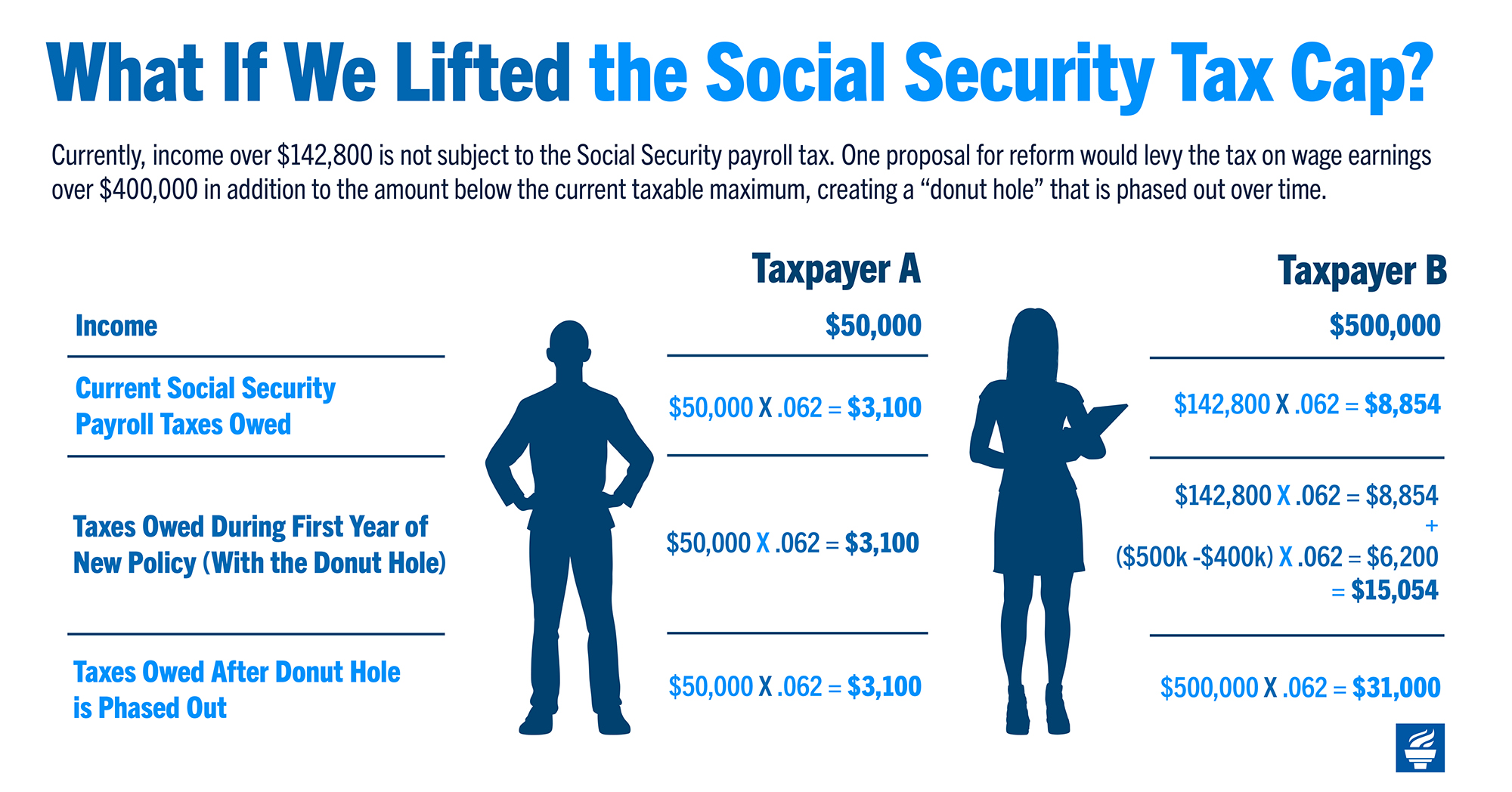

Social Security’s payroll tax cap was raised nearly 9% for 2023, meaning more income will face Social Security taxes next year, but the rise is unlikely to affect the solvency of the trusts underpinning the system.

Citing the increase in average wages, the Social Security Administration said the maximum amount of earnings subject to the Social Security tax (taxable maximum) will increase to $160,200 from $147,000 starting in January. The announcement was part of the release of the cost-of-living adjustment, or COLA. The taxable maximum for 2021 was $142,800.

Citing the increase in average wages, the Social Security Administration said the maximum amount of earnings subject to the Social Security tax (taxable maximum) will increase to $160,200 from $147,000 starting in January.

Posted on October 13, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Social Security just announced an 8.7 percent cost of living adjustment, the largest inflation adjustment to benefits in four decades — a welcome development for millions of older Americans struggling to keep up with fast-rising living costs.

The Dow Jones Industrial Average dropped 500 points at the starting bell, down 1.7% and undercutting its Sept. 30th low. The S&P 500 index sank 2.3% and the NASDAQ composite swooned 3%.

Then Stocks Soared Despite the Hotter-Than-Expected Inflation Report

U.S. equities closed out the day noticeably higher, ending six-straight days of declines, despite the release of today’s key inflation data. The markets seemed to shrug off another hotter-than-expected consumer price inflation (CPI) report, which boosted expectations that the Fed will have to remain aggressive with its monetary policy tightening plans.

Posted on October 13, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Markets: The S&P 500 extended its losing streak to six days yesterday, notching its worst day since November 2020. But, Moderna did not contribute to the decline after news broke it will develop a cancer vaccine with Merck.

***

***

The Social Security Administration is expected to announce a cost of living adjustment, or COLA, of at least 8% today amid a rising inflation rate that has been punishing for Americans on fixed incomes.

The annual adjustment is forecast to be the largest one-time increase since 1981, and the largest experienced by beneficiaries alive today. The nonprofit Senior Citizens League predicts an adjustment coming in at 8.7%, implying that Social Security recipients could see an increase of about $144 starting Jan. 1, 2023. The increase that took effect this year was 5.9%.

Posted on August 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

**

Inflation eased off historically high levels in July, raising hopes that a relentless surge in prices may have peaked. Consumer prices increased 8.5% from a year ago, down from a 9.1% annual rise – a 40-year high – in June, according to the Labor Department’s Consumer Price Index. Gasoline prices fell but food and rent continued to march higher. Economists surveyed by Bloomberg had estimated yearly inflation would fall to 8.7%. On a monthly basis, consumer prices were unchanged, compared to a 1.3% rise in June. Core prices, which exclude volatile food and energy items and generally provide a better gauge of future trends, increased 0.3% in July following a 0.7% rise the prior month. That held the annual increase at 5.9% after three straight monthly declines.

And, in a bit of good news for aged Americans, Social Security payments may take their biggest jump in years. The surge could be as high as 10%, which is larger than recent increases in the consumer price index. Social Security carries an official name of the “Old-Age, Survivors, and Disability Insurance (OASDI).” Even the rich can get benefits. The income calculation tops out at a maximum of $142,800.

Once you hit age 62, what’s an investment class that can give you a high guaranteed return with almost no risk; Bonds, Equities, or Commodities?

Nope; it’s social security.

There’s just one catch. You can’t actually get your hands on the money until you’re 70.

The Catch

One of the most common issues for those approaching retirement age is determining the right time to file for Social Security. If you file at age 62, you will receive benefits longer. Yet your monthly benefit for the rest of your life will only be about 75% of the monthly amount you will receive if you file at your full retirement age of 66 to 67. If you wait even longer, the benefit amount is higher still.

Those who are unable to work and don’t have sufficient retirement savings may not have a choice about filing for Social Security early. Those who don’t have a compelling need for early Social Security income may still consider early filing as an option, with the idea of investing the money for their later retirement.

Recent Thoughts

According to a recent article by Karen DeMasters in Financial Advisor magazine, this is not a good choice. She cites research done by William Meyer and William Reichenstein of Social Security Solutions Inc (www.ssanalyzer.com) in Leawood, Kansas.

One big drawback to investing your Social Security benefits is the penalty you pay if you are still working. If, between age 62 and your full retirement age, you earn more than $15,120 a year, your benefits are reduced. So you’d start with a smaller benefit amount, have it cut even further, and not be left with a whole lot to invest.

Even more important, however, is a number that Meyer and Reichenstein emphasize: 8%. This is the amount that your Social Security benefit increases every year between age 62 and 70 that you delay filing. In essence, if you leave your Social Security benefits in the government’s hands instead of investing them yourself, you are guaranteed an 8% annual return on that part of your retirement portfolio. This doesn’t include cost-of-living increases.

Taking early benefits and investing them is only a good idea if you are sure you can get more than an 8% return. Any investment likely to produce a return higher than 8% would come with risks that are unacceptably high for a retirement-age portfolio.

Social Security Risks

There are only two real risks associated with letting your Social Security benefits accumulate until later than age 62.

One is the possibility that Social Security won’t be there when you do retire. Given that the delay is only a few years and that Social Security is now the retirement plan of most Americans, this is extremely unlikely.

The second risk is that you won’t live long enough to collect an amount equal to what you would get if you started benefits early. Unless you are facing a terminal illness, however, chances are that waiting until at least full retirement age is still the wisest option.

Assessment

If your health is good and you don’t need retirement cash immediately, you are far better off to delay filing. Even if you are facing circumstances that might make early retirement a necessity, it’s a good idea to look at all your options and try to find creative ways to put off filing as long as possible.

Once you reach age 62, Social Security is always an option. It gives you a doorway out of the working world any time you really need to take it. But for every year you can delay walking through that door, you gain 8%. That’s an investment return well worth waiting for.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on July 31, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Although the future of Social Security remains in doubt, some congressional lawmakers are ensuring that most Social Security recipients get their money and then some. Sen. Bernie Sanders (I-Vt.) introduced the Social Security Expansion Act (SSEA) in June. The bill would allot $200 more per month for each Social Security recipient — a 12% boost in money, according to CBS News.

So who will receive these Social Security increases?

The people who are currently eligible for Social Security or anyone who turns 62 in 2023, which is the earliest age to collect Social Security, will be eligible to receive the extra $200 a month with their benefits.

***

Now, at present for Social Security, 12.4% is taken out of each paycheck for people earning up to $147,000, with half paid by the employer and half paid by the worker. So, if you make $147,000 or less, you are paying 6.2% into Social Security. If you make, say, $1.47 million, you only pay 0.6% of your income to Social Security.

If the pending new SS bill is approved, the same rate would be taxed on individuals making $250,000 or more. Those making $147,000 or less would continue to pay the same rate as well, with a do-nut hole between the $147,000 and $250,000 — although that $147,000 typically goes up each year, as it is based on average income.

The increased funding — along with a change in the cost-of-living-adjustments (COLA) to the Consumer Price Index for the Elderly (CPI-E) — would help to increase benefits by an estimated $200 per month, or $2,400 per year, which bears out, according to an analysis by the Social Security Administration (SSA).

Posted on July 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. inflation climbed to new 41-year high of 9.1% in June, as gasoline prices surged. Soaring gasoline prices in June drove the rate of U.S. inflation to 9.1%, a nearly 41-year peak. The CPI jumped 1.3% last month to mark the third time in the last four months it’s topped 1%. Economists polled by The Wall Street Journal had forecast a 1.1% advance.

Because of June’s higher-than-expected inflation jump, it’s likely seniors will receive a 10.5% adjustment to their Social Security checks in early 2023, the Senior Citizens League, an advocacy group for older Americans opined.

Nearly a third of job recruiters said they experience extreme stress on a weekly basis because of their work, according to a December survey by human-resources analytics firm Veris Insights. The research found that 77% of high-ranking recruiters are open to changing jobs, along with 65% of HR professionals — a figure that rose 17 percentage points from September to November last year.

And, the S&P 500 slipped 0.5%, and the Dow Jones Industrial Average shed 210 points, or roughly 0.7%, though both indexes pared losses from sharper declines earlier in the day. The NASDAQ Composite closed down 0.2% but was an outlier for much of the session, trading in the green as technology stocks rebounded.

Finally, US Treasury yields were also in focus with the most dramatic moves happening at the front end of the yield curve. The 10-year stood at 3.04% following the CPI print, with 2-year yields rising as high as 3.17%, further inverting the yield curve. The curve “inverts” when yields on shorter-dated Treasuries rise above those of longer-dated ones and have typically preceded recessions on Wall Street.

Posted on June 29, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

Markets: Stocks sagged for the second straight day, with technology chip stocks taking some of the biggest blows. A new consumer report showed that Americans are not confident in the economy, but are confident that inflation will be remain for the next year.

A Social Security official earlier this month said he expects a COLA bump of about 8%, based on the current inflationary trends. But if inflation continues at its current pace — the cost of goods and services in May accelerated to 8.6% — seniors could receive a COLA hike of 10.8% in early 2023, according to a new analysis from the non-partisan Committee for a Responsible Federal Budget. If inflation grinds to a halt over the final months of 2022, seniors would receive a COLA increase of 7.3%, the group predicted.

Ernst and Young (EY), one of the world’s largest auditing firms, has agreed to pay a $100 million SEC fine after admitting hundreds of its accountants have cheated on their ethics exams between 2017 and 2021.

US health officials ramped up their fight against the Monkeypox outbreak, expanding the group eligible to get vaccines and deploying more doses and testing capabilities.

Posted on June 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. personal income rose 0.42% in May, which equates to 5% on an annualized basis. With inflation (8.26% annualized) so much higher than income (5% annualized), consumers have to borrow or dip into savings to continue buying the same amount of goods and services they purchased last year.

And, in a recent survey, Clever found that retirees average only $191,659 saved for retirement. That’s not a lot for what could be a 20- to 30-year time period. This would translate to an annual income of $7,666. On a monthly basis, that’s just $639 — still not a lot when combined with the average Social Security benefit. NOTE: To be fair, that $191,659 is based on a single survey of 1,000 retired Americans. That number may look different across a much larger sample size.

Finally, amid rising inflation rates and slowing demand, tech and crypto companies cut more jobs in May than in the previous four months combined, according to out placement firm Challenger, Gray & Christmas. There were 4,044 job cuts in the tech industry compared to about 500 through the first four months of the year and the most in one month since December 2020. Crypto and other companies in the fintech industry cut 1,619 jobs in May, compared to 440 in January through April.

Posted on December 13, 2016 by Dr. David Edward Marcinko MBA MEd CMP™

By Vanguard Services

Infographic on Social Security Taxation

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

When it comes to being financially prepared for retirement, Chinese women are the most confident women in the world. In fact, they are almost twice as confident as their US counterparts.

The Survery

This conclusion comes from a 2014 global survey, the Aegon Retirement Readiness Index. It found that the percentage of women saying they are very confident or extremely confident about retirement is 42% in China, 35% in India, 29% in Brazil, 22% in the US, and 18% in Canada.

The survey included responses from 16,000 employees and retirees in 15 countries, half of whom were women. About 62% of the women were married, 52% had some higher education, and 80% took an active role in managing the household finances.

The Insights

Several aspects of this survey really caught my attention:

I was puzzled that only two developed countries—the US and Canada—made the top five. The first three—China, India, and Brazil—were emerging markets with little or no social safety nets in place.

Even more notable is that, in the US and Canada, the number of women who do not feel prepared to retire (38% in the US and 36% in Canada) is almost twice as high as the number that are confident about retirement.

And more notable yet is that the bottom five includes three developed countries with strong social safety nets. In France, Japan, and Spain, less than 6% of women reported retirement confidence, while 60% or higher said they had no confidence.

It seems puzzling that the countries with large social safety nets spawned less retirement confidence than did developed countries with little or no safety net. Why isn’t it the opposite? Why aren’t women in countries where government plays a big part in retirement income more confident?

The Answer?

Therein may lay the answer. Possibly because of the lack of government retirement programs, people in the emerging market countries like China, India, and Brazil realize they cannot count on anyone but themselves in retirement. They know they must begin saving a significant amount of their income, starting early in life, to be able to sustain themselves in retirement. A failure to do so will result in them literally being “thrown out onto the street” or into the “poor house.” As harsh as that may sound to our Western ears, the reality must be a powerful motivator.

***

***

The Reality

This reality was brought home to me by two people I met on visits to China and India. One Chinese woman in her 20’s told me she saved a third of her income. She said, “People in America don’t need to save. China doesn’t have the social safety nets you have.” Part of surviving in their society is to learn money skills and how to save early in life for emergencies and retirement. A man I met in India told me much the same story; he had his retirement fully funded by age 45.

In the US and most other developed countries, government programs like Social Security have become the retirement plan of the masses. Yet the majority of women in developed countries don’t seem to find comfort in those programs.

However, neither do they save like their emerging market counterparts. In fact, 56% of Americans live hand to mouth, according to a 2005 survey of retirement savings for baby boomers and others, by Sharon A. Devaney and Sophia T. Chiremba, reported at the US Bureau of Labor Statistics [USBLS].

Assessment

What might motivate women globally to gain confidence in their retirement preparedness? I don’t know. But based on the results of this survey, the answer won’t be found in more government programs.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

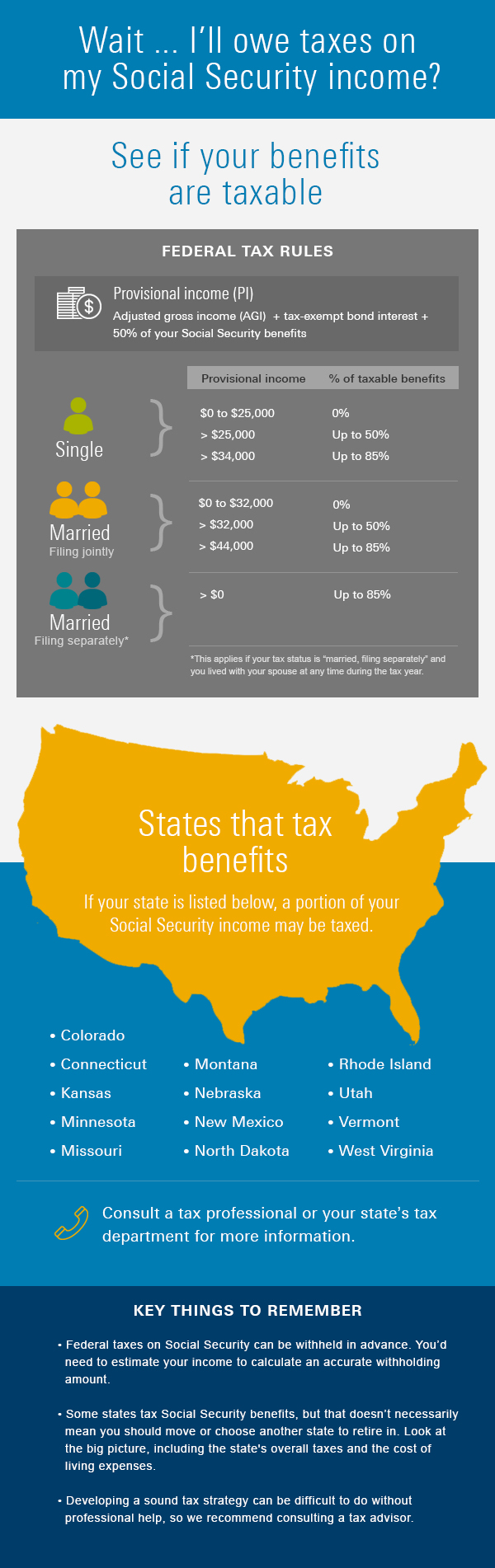

If Social Security is your only source of income, it is unlikely that your monthly benefit is subject to taxation.

However, people like doctors and other medical professionals with substantial income outside of Social Security may have to pay federal income taxes on their benefits. In fact, it is possible that as much as 85 percent of your Social Security payout is taxable.

The Determination

To determine whether you are required to pay taxes on your benefit, the first step is to determine what the federal government deems your “combined income.” Your “combined income” is one-half of your Social Security benefit, plus all other income received during the year. Other income might include wages earned, capital gains recognized, dividends and interest collected, pension benefits received, and IRA funds distributed during the year.

Example:

For instance, consider a retired couple that receives an annual pension benefit of $20,000, takes an IRA distribution in the amount of $10,000, and receives $15,000 in Social Security benefits. This couple’s other income would total $30,000 (the pension and the IRA distribution). One-half of the Social Security benefit, or $7,500 would then be added to the other income to create a “combined income” of $37,500.

If a couple filing a joint tax return has a “combined income” of less than $32,000 ($25,000 for individuals), then all Social Security benefits are free of taxation. However, if the figure is between $32,000 and $44,000 ($25,000 and $34,000 for individuals), then as much as 50 percent of the Social Security benefit may be taxable. Further, if the “combined income” is greater than $44,000 ($34,000 for individuals), than as much as 85 percent of the Social Security payout may be taxable.

The “Combined Income” Threshold

So should couples do everything necessary to keep their “combined income” below $32,000 (the 50 percent threshold), or even $44,000 (the 85 percent threshold)? Fortunately, the tax system is progressive, meaning that just because a couple might fall in the bracket causing as much as 50 percent of their Social Security benefit to be taxable, not all of their benefit is necessarily taxed as such.

Example:

For instance, our sample couple with a “combined income” of $37,500 might be concerned that they are paying taxes on 50 percent of their Social Security benefit because that is the bracket they fall in. This would cause half of their $15,000 Social Security benefit, or $7,500, to be taxable. Fortunately, it is only the $5,500 of benefits received that pushes the couple’s “combined income” over and above the $32,000 threshold that is actually considered 50 percent taxable. As a result, only $2,750 (half of the $5,500 of “combined income” over the $32,000 threshold) of Social Security benefits is taxable. In this instance, the taxpayers are only paying taxes on 18 percent ($2,750/$15,000) of their Social Security benefits.

Getting Granular

Now suppose our imaginary couple received not $15,000 in total Social Security benefits, but $15,000 each, leading to a total benefit of $30,000. Assuming the same $20,000 pension benefit and $10,000 IRA distribution, the couple’s “combined income” would now be $45,000 (half of the $30,000 in Social Security benefits received plus the $30,000 of other income).

This provides another illustration of how the progressive tax system prevents higher-income taxpayers from feeling the need to do everything they can to get their “combined income” under the $44,000 threshold just to avoid the 85 percent bracket. First, a “combined income” of $45,000 clearly fills the entire 50 percent bracket of $32,000 – $44,000. Consequently, the entire $12,000 of Social Security benefits received within that range will be 50 percent taxable (or $6,000 of benefits received will be taxable). Additionally, another $1,000 of benefits over and above the $44,000 threshold will be 85 percent taxable, meaning another $850 of benefits are taxed. This means a total of $6,850 ($6,000 from the 50 percent taxable bracket, and $850 from the 85 percent taxable bracket) of Social Security benefits received will be taxable. Still, however, of the $30,000 of Social Security payments received by our couple, only 23 percent ($6,850/$30,000) ends up being taxable.

Taking this one step further, we can deduce that income outside of a Social Security benefit (the combination of pension benefits, IRA distributions, capital gains, etc) must be greater than $44,000 for there to even be a possibility that as much as 85% of a Social Security benefit would be taxable. If this other income portion of the “combined income” is less than $44,000, then at least some of our Social Security benefit will fall in the 50 percent threshold, if not the 0 percent threshold.

The Calculations

Here is a useful calculator to determine the taxability of your Social Security benefit.

The point of this exercise is twofold. First, understanding the factors that may cause a Social Security benefit to be more or less taxable provides us with an advantage from a financial planning perspective. Second, it is important to realize that just because our “combined income” passes a threshold causing some of our Social Security benefit to be taxable doesn’t mean that the resulting tax liability is catastrophic.

Assessment

In fact, once realizing that the increase in tax liability from having some additional income is so inconsequential, some retirees may be more likely to spend and enjoy their retirement, which is the point of financial planning in the first place.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Lost in the hoopla over the government shutdown, defunding Obamacare, and raising the debt ceiling are some proposals contained in President Obama’s budget that will have a significant impact on retirees, inheritors, and savers.

Most of the President’s proposals are aimed at enforcing higher taxes on savers who maximize their retirement plans. This is a way to raise revenue for government entitlement programs, like subsidies for health insurance, Medicare, and Social Security.

Retirement and Retirees

Back from last year is his proposal to cap contributions to IRA’s and 401(k)’s when the balance reaches a level determined by a set formula which is tied to interest rates. The proposal sets the cap at $3.4 million initially. As interest rates rise, the cap will lower. When a saver’s IRA balance hits the cap, he or she will not be allowed to make further contributions to any retirement plan.

This will mostly affect savers who terminate employment and roll large accumulations from profit-sharing plans and lump-sum distributions from defined benefit plans into their IRA’s. It will shut down their ability to save into the future.

Taxes and Inheritors

The President has yet another plan to end tax-deductible contributions for upper income earners. Only 28% of a contribution would be deductible for any taxpayer whose bracket exceeds 28%. For a taxpayer in the highest bracket, this means a tax increase of about 50%.

Another of the President’s proposals would end the ability of anyone other than a spouse to inherit a tax-deferred IRA. Under the proposal, all non-spouses inheriting an IRA would have five years to terminate the IRA and pay income taxes on the distributions. This proposal really impacts Roth IRA conversions, as most parents convert traditional IRA’s to Roths with the intention of leaving their children a non-taxable sum of money that can continue to grow tax free during their lifetime. If the President’s proposal passes, many older savers will discover that the intentions behind their Roth conversions have been nullified.

Forced Savings and Savers

While President Obama wants to cap what successful savers can stash away in retirement plans, he also wants to force employees to save for retirement. Employers will be required to open IRA’s for every employee and to fund the plan at a minimum of 3% of the employee’s pay, unless the employee specifically opts out. The employee can contribute more than 3%, up to the $5,000 cap for those under 50 and $6,000 for those over 50.

Of course, savvy savers and ME-P readers know most of us need to be saving 20% to 50% of our salaries, depending on our ages, so saving just 3% of pay won’t amount to much in the way of retirement income.

Good News

On the positive side, the President wants to end required minimum distributions on IRA balances under $75,000. This will reduce some paperwork for savers with smaller IRA’s who are not making withdrawals.

Typically, most retirees with small IRA’s are those with less savings anyway, who need to take withdrawals from their IRA’s to make ends meet. So it’s doubtful this rule change will have much impact.

Finally, the President proposes letting inherited non-spousal IRA’s enjoy the same benefit of a 60-day rollover window on any distribution, similar to what they can do with a non-inherited IRA. This will simply eliminate a lot of confusion, as most people don’t understand the 60-day rollover provision does not include inherited IRA’s.

[US Federal Government Shut-Down]

Assessment

Of course, whether any or all of these proposals make it into law is anyone’s guess. Anyone whose retirement and estate planning includes saving in IRA’s will want to keep an eye on these provisions as the budget moves through Congress.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

“The Feds Want Your Retirement Accounts.” This was the headline of a February 22 post on the American Thinker blog recently forwarded to me by a reader. Normally I hit delete on articles warning of some type of impending financial doom. I read this one, since Argentina confiscated its citizens’ retirement accounts shortly before I first visited there in 2009.

The Feds Want Your Retirement Accounts

According to the article, in 2007 a professor of economic policy from the New School for Social Research, Theresa Ghilarducci, wrote a paper calling for the US government to eliminate private retirement accounts. She suggested confiscating the assets in those accounts and replacing them with a “Guaranteed Retirement Account” (GRA) guaranteeing a return of 3%, which is essentially another program like Social Security.

This is basically what Argentina did one year later.

I brushed aside Argentina’s action as the quirky behavior of a third world “banana republic.” Such confiscation would never happen in a developed country like the US.

Nationalizing Private Retirement Accounts

Today, I am not as nonchalant about the prospect of nationalizing private retirement accounts. While I still believe it’s unlikely, I don’t completely rule it out as right-fringe conspiracy lunacy. The dramatic fall of our economic freedom from third in the world to 18th in 10 short years should give any US citizen pause. Even since 2009 we’ve seen a significant shift in public preference toward a government-controlled economy versus a market economy.

Does that mean we should stop funding our IRAs and 401(k)s and start stuffing gold coins into coffee cans? I don’t think so.

###

###

A Favored Vehicle

I still favor retirement accounts and personally fund mine to the maximum. I recommend that most wealth accumulators do the same. Roth IRAs, where the proceeds are distributed tax-free, are especially attractive vehicles in which to store investments. However, they are only as good as our government’s word.

Certainly, we can point to a number of circumstances where the US government did renege on its promises. One example was the Tax Simplification Act of 1986, signed into law by President Reagan, where Congress penalized real estate investors by retroactively changing the laws. A second instance, engineered by President Obama, was the unconstitutional confiscation of GM bondholders’ collateral which was handed over to the unions. Such acts do make me pause and wonder if I am being naïve.

A Sovereign Government

Yet a sovereign government that issues its own currency has no need to confiscate financial assets of citizens if the currency is sound. As long as the government can find vendors to accept its currency in exchange for goods and services, there is no need to take citizens’ assets. All it needs to do is create new currency.

If a government with a sound currency would confiscate assets, the reason would almost certainly be to redistribute wealth. However, any country that starts taking the assets of its citizens will not be considered politically stable and will not have a sound currency for long. Other countries, corporations, and individuals will become reluctant to accept its currency.

This is the case in Argentina, where the currency is devaluing at 30% a year. Nobody wants Argentinian pesos. In response, the government outlawed owning foreign currency; Argentinians cannot legally own more than 100 US dollars.

Assessment

The US is certainly not to that point. In the meantime, what should investors do?

Nothing. I will continue to fully fund my retirement plans and hold a globally diversified portfolio invested in a wide array of assets. I will, however, continue to cast a watchful eye toward the strength of the US dollar, the CPI, and our tax and economic policy. As my father often says, “Never say never.”

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on December 21, 2012 by Dr. David Edward Marcinko MBA MEd CMP™

Definition of Chain-Weighted CPI

By Dr. David Edward Marcinko MBA

An alternative BLS measurement for the Consumer Price Index (CPI), removing the biases associated with new products, changes in quality and discounted prices.

The chain weighted CPI incorporates the average changes in the quantity of goods purchased, along with standard pricing effects. This allows the chain weighted CPI to reflect situations where customers shift the weight of their purchases from one area of spending to another.

The chain weighted CPI incorporates changes in both the quantities and prices of products. For example, let’s examine clothing purchases between two years. Last year you bought a sweater for $40 and two t-shirts at $35 each. This year, two sweaters were purchased at $35 each and one t-shirt for $45.

Standard CPI calculations would produce an inflation level of 13.64%

((1 x 35 + 2 x 45)/ (1 x 40 + 2 x 35)) =1.1364

The chain weighted approach estimates inflation to be 4.55%

((2 x 35 + 1 x 45)/ (1 x 40 + 2 x 35)) =1.0455.

Using the chain weighted approach reveals the impact of a customer purchasing more sweaters than t-shirts.

What is the C-CPI-U and when did the Bureau of Labor Statistics (BLS) begin publishing it?

BLS began publishing the Chained Consumer Price Index for All Urban Consumers effective with the release of July 2002 CPI data. Designated the C-CPI-U, the index supplements the existing indexes already produced by the BLS: the CPI for All Urban Consumers (CPI-U) and the CPI for Urban Wage Earners and Clerical Workers (CPI-W).

The C-CPI-U employs a formula that reflects the effect of substitution that consumers make across item categories in response to changes in relative prices.

What is substitution and substitution bias? And does the C-CPI-U eliminate it?

Traditionally, the CPI was considered an upper bound on a cost-of-living index in that the CPI did not reflect the changes in consumption patterns that consumers make in response to changes in relative prices.

Since January 1999, a geometric mean formula has been used to calculate most basic indexes within the CPI; this formula allows for a modest amount of substitution within item categories as relative price changes.

The geometric mean formula, though, does not account for consumer substitution taking place between CPI item categories. For example, pork and beef are two separate CPI item categories. If the price of pork increases while the price of beef does not, consumers might shift away from pork to beef. The C-CPI-U is designed to account for this type of consumer substitution between CPI item categories. In this example, the C-CPI-U would rise, but not by as much as an index that was based on fixed purchase patterns.

With the geometric mean formula in place to account for consumer substitution within item categories, and the C-CPI-U designed to account for consumer substitution between item categories, any remaining substitution bias would be quite small.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

No, this isn’t a bad joke. It takes one thousand millions to make one billion. That’s a huge difference. And, how many doctors have arrived there?

A Political “Hot-Button”

Over the past couple of years, especially during the presidential election, one of the hot-button issues has been whether the wealthy are paying “their fair share” in taxes. A great deal of the media coverage and political rhetoric, from President Obama on down, has lumped “millionaires and billionaires” together.

That makes as much sense as putting a housecat and a tiger into the same cage and saying they’re just the same.

Who Wants to be a Billionaire?

The first issue to clarify is the definition of “millionaire” and “billionaire.” Is it someone with a net worth of $1 million or $1billion, or is it someone earning a million or a billion in a year?

According to wild.answers.com, only 80,000 Americans make $1 million or more a year. I couldn’t find a source listing how many people make over $1 billion a year, but I can guess. If you earned 6% on your investments, you would need a net worth of about $16 billion to provide an annual income of $1 billion. According to Forbes (March 2012), only 40 people in the entire world have a net worth of over $16 billion. Obviously, all those references we keep hearing to billionaires must refer to net worth, not income.

This is in line with the Merriam Webster dictionary, which defines millionaire (or billionaire) as “a person whose wealth is estimated at a million (or billion) or more.”

The Life-Style

What kind of lifestyle can you have with a net worth of a million as opposed to a billion dollars? Experts tell us the most reasonable sustainable withdrawal rate is 3%. That means your $1 million will provide $30,000 a year. Adding in Social Security of $18,000 a year means a millionaire can retire on an income of $48,000 a year. If you need assisted living, in-home care, or nursing home care in your later years, which at today’s rates cost a minimum of around $84,000 a year, you’ll be spending down your principal.

Three percent of $1 billion, on the other hand, will give you a retirement income of $30 million a year. At that rate, you could probably get by without bothering to file for Social Security.

Aiming High

Accumulating $1 million over a lifetime is certainly possible for middle-class earners who are willing to live on less than they make. If you started saving about $1,750 a month at age 25, you’d have your million by age 65. That’s about the same as a married couple each maximizing their 401(k) contributions.

To accumulate $1 billion by age 65, on the other hand, if you started at age 25 you’d need to save a mere $21 million a year.

Equating a millionaire with a billionaire is the same as equating the population of Rapid City, South Dakota (70,000) to the combined populations of California, Texas, and Virginia (70,000,000). There is simply no comparison.

Rich?

The point here is that in today’s world, a millionaire, especially one who is retired, isn’t “rich.” Accumulating a net worth of $1 million dollars by age 65 is a completely reasonable and achievable goal for anyone wanting a comfortable and secure retirement.

Assessment

Lumping “millionaires and billionaires” together might roll off the tongue with a rhythm that makes a nice sound bite. That doesn’t mean it makes sense. For anyone willing to do the math, the comparison is ludicrous. There’s a world of difference in earnings, wealth, and potential lifestyle in those extra three zeroes.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

Now, we admit that we’ve not paid much attention to Social Security because we are all still far from being eligible for it, and at the ME-P, we assume it won’t be here for us.

The Book

Nevertheless, when Jim published a new book A Social Security Owner’s Manual, we took the opportunity to learn more about Social Security.

And, we think, so should all medical professionals and their financial advisors.

Assessment

Jim provides expert guidance for retirement, education funding, and income tax issues, too. In addition to this all this, you’ll find Jim’s writings all around the internet, as he is a regular contributor to Forbes.com, TheStreet.com, and FiGuide. Several other sites also republish his work.

Conclusion

Your thoughts and comments on social security and this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Posted on August 26, 2011 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

From Expert Voices

By C. Eugene Steuerle PhD [Institute Fellow and Richard B. Fisher Chair, The Urban Institute]

By Stephanie Rennane [University of Maryland]

For August 2011

Reforms to Medicare and Social Security will likely be debated over the next few months as the new “super committee” formed by the debt ceiling agreement works to develop its long-term deficit reduction plan.

The Essay

In this essay, Dr. Eugene Steuerle and Stephanie Rennane help to inform this debate by presenting findings from their newly updated analysis showing that seniors retiring today can expect to receive dramatically more in entitlement program benefits during retirement than they contributed to the programs while working.

For example, the average Medicare beneficiary can expect $3 in benefits for every $1 paid in payroll taxes.

The authors posit that the magnitude of the resources involved when viewing these programs in tandem over a lifetime gives policymakers new impetus and flexibility to develop coordinated entitlement reforms that promote a coherent, equitable and sustainable support system for current and future generations of seniors.

Conclusion

And so, your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Posted on November 2, 2010 by Dr. David Edward Marcinko MBA MEd CMP™

The CRFB Speaks

By Children’s Home Society of Florida Foundation