BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Estate planning is essential for everyone, but for doctors it carries unique importance. Physicians often navigate a complex financial landscape shaped by high incomes, significant debt, professional liability, and long‑term career uncertainty. Their assets, responsibilities, and risks differ from those of many other professionals, making a thoughtful estate plan not just advisable but necessary. Estate planning for doctors is ultimately about protecting their families, safeguarding their professional legacy, and ensuring that their hard‑earned wealth is managed according to their wishes.

One of the first reasons estate planning is so critical for doctors is the nature of their financial journey. Many physicians begin their careers burdened with substantial student loan debt. As they progress, their income rises sharply, often creating a rapid shift from financial strain to financial abundance. This transition can lead to a mix of assets—retirement accounts, investment portfolios, real estate, and business interests—that must be coordinated carefully. A will or trust helps ensure these assets are distributed efficiently and according to the doctor’s intentions, rather than being left to state laws that may not reflect their wishes.

Doctors also face professional risks that make asset protection a key part of estate planning. Even with malpractice insurance, physicians may worry about lawsuits or claims that could threaten personal wealth. While estate planning cannot eliminate liability, certain tools—such as irrevocable trusts or careful titling of assets—can help shield property from potential creditors. This is especially important for doctors in high‑risk specialties, where litigation is more common. Protecting assets ensures that a physician’s family is not financially devastated by an unexpected legal challenge.

Another unique consideration for doctors is the possibility of owning a medical practice. Whether a solo practice, partnership, or share in a larger group, this business interest must be addressed in an estate plan. A practice is not just an asset; it is a functioning enterprise with employees, patients, and contractual obligations. A well‑crafted estate plan can outline what happens to the practice if the doctor becomes incapacitated or passes away. This may include succession planning, buy‑sell agreements, or instructions for transferring ownership. Without clear guidance, the practice could face disruption, harming both its value and the people who depend on it.

Estate planning also intersects with the demanding nature of a physician’s schedule. Doctors often work long hours, leaving little time to manage personal financial matters. This can lead to procrastination, even though they may have more to lose by delaying. A comprehensive estate plan provides peace of mind, ensuring that their family is protected even if they haven’t had time to revisit every financial detail. Powers of attorney and advance directives are especially important, as they designate trusted individuals to make financial and medical decisions if the doctor cannot do so.

Family considerations play a major role as well. Many doctors are primary breadwinners, and their families rely heavily on their income. Estate planning ensures that dependents are cared for through life insurance, trusts, and guardianship designations. Trusts can be particularly valuable for physicians who want to provide long‑term financial stability for children, especially if those children are young or have special needs. These tools allow doctors to control how and when assets are distributed, preventing mismanagement and protecting wealth across generations.

Tax planning is another essential component. Physicians often fall into higher tax brackets, and without proper planning, their estates may face significant tax burdens. Strategies such as gifting, charitable planning, and trust creation can help minimize taxes and preserve more wealth for heirs. Doctors who support medical charities or educational institutions may also use estate planning to leave a philanthropic legacy that reflects their values.

Finally, estate planning for doctors is about clarity. Physicians understand the importance of informed decision‑making in their professional lives, and the same principle applies to their personal finances. A clear estate plan reduces confusion, prevents conflict among family members, and ensures that the doctor’s wishes are honored. It transforms uncertainty into structure, allowing loved ones to focus on healing rather than navigating legal and financial chaos.

In the end, estate planning is an act of responsibility and care. For doctors, whose lives revolve around helping others, it is also a way to protect the people they love most. By addressing their unique financial risks, professional obligations, and family needs, physicians can build an estate plan that provides security, preserves their legacy, and reflects the dedication they bring to their work and their lives.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors1738@outlook.com -OR-http://www.MarcinkoAssociates.com

Project management plays a crucial role in strengthening the processes and outcomes of financial planning, transforming what can often be an abstract or reactive activity into a structured, disciplined, and strategically aligned effort. At its core, financial planning involves setting objectives, allocating resources, assessing risks, and monitoring progress over time. These are the same foundational elements that define effective project management, which is why integrating the two fields creates a more coherent and resilient approach to organizational decision‑making. When financial planning is treated as a project rather than a static document, organizations gain clarity, accountability, and adaptability in navigating both short‑term pressures and long‑term goals.

The first major contribution of project management to financial planning is the establishment of clear and measurable goals. Financial objectives—whether related to revenue growth, cost reduction, investment performance, or capital allocation—must be specific and time‑bound to guide meaningful action. Project management frameworks ensure that these goals are not only well‑defined but also aligned with broader organizational strategy. Without this alignment, financial plans risk becoming disconnected from operational realities. By applying structured goal‑setting techniques, such as those used in scope management, financial planners can avoid ambiguity and maintain focus on the outcomes that matter most.

Another essential dimension is resource allocation. Financial planning is fundamentally about deciding how limited resources should be distributed across competing priorities. Project management introduces a systematic approach to evaluating these trade‑offs, ensuring that financial resources, personnel, time, and technology are deployed in ways that support strategic objectives. This structured approach to resource allocation helps organizations avoid overextension, reduce inefficiencies, and maintain a realistic understanding of what can be achieved within given constraints. When financial planning lacks this discipline, organizations may commit to initiatives that exceed their capacity or fail to invest adequately in areas critical to long‑term success.

Risk assessment is another area where project management significantly enhances financial planning. Markets fluctuate, operational costs shift, and unexpected events can disrupt even the most carefully constructed plans. Project management provides tools for identifying risks, estimating their likelihood, and developing contingency strategies. This structured approach to financial risk assessment ensures that organizations are not caught off guard by foreseeable challenges. Instead, they can prepare alternative scenarios, adjust assumptions, and build flexibility into their financial models. This proactive stance reduces vulnerability and supports more confident decision‑making.

Time management also plays a central role in integrating project management with financial planning. Financial goals unfold across months or years, and without a clear timeline, organizations may struggle to track progress or anticipate future needs. Project management techniques, such as milestone mapping and timeline development, help planners visualize when investments will mature, when expenses will peak, and when cash flow may tighten. By applying structured approaches to timeline development, organizations can better coordinate financial activities with operational cycles, regulatory deadlines, and strategic initiatives.

***

***

Beyond these technical contributions, project management enhances financial planning by improving communication and accountability. When financial planning is treated as a project, responsibilities are clearly assigned, expectations are documented, and progress is regularly reviewed. This reduces ambiguity and ensures that stakeholders understand their roles in achieving financial objectives. Transparency increases as well, since project management encourages documentation, reporting, and open dialogue. Stakeholders gain visibility into how decisions are made, how budgets are allocated, and how performance is measured, which strengthens trust and reduces internal conflict.

In practical terms, project management principles appear throughout financial planning activities. Budget development becomes a collaborative process with defined phases and checkpoints. Forecasting incorporates structured data collection and scenario analysis. Capital projects rely on charters, cost‑benefit evaluations, and risk logs. Performance tracking uses dashboards and key indicators to measure progress against the plan. Each of these activities benefits from the discipline and structure that project management provides, ensuring that financial planning is not merely theoretical but actionable and measurable.

Ultimately, the integration of project management into financial planning supports continuous improvement. Financial planning is cyclical: plans are created, executed, monitored, and adjusted. Project management reinforces this cycle by embedding review points, performance metrics, and lessons‑learned processes. Over time, organizations become more accurate in forecasting, more efficient in resource use, and more resilient in the face of uncertainty. By applying project‑management principles to financial planning, organizations transform financial strategy into a dynamic, adaptive process that supports long‑term stability and success.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

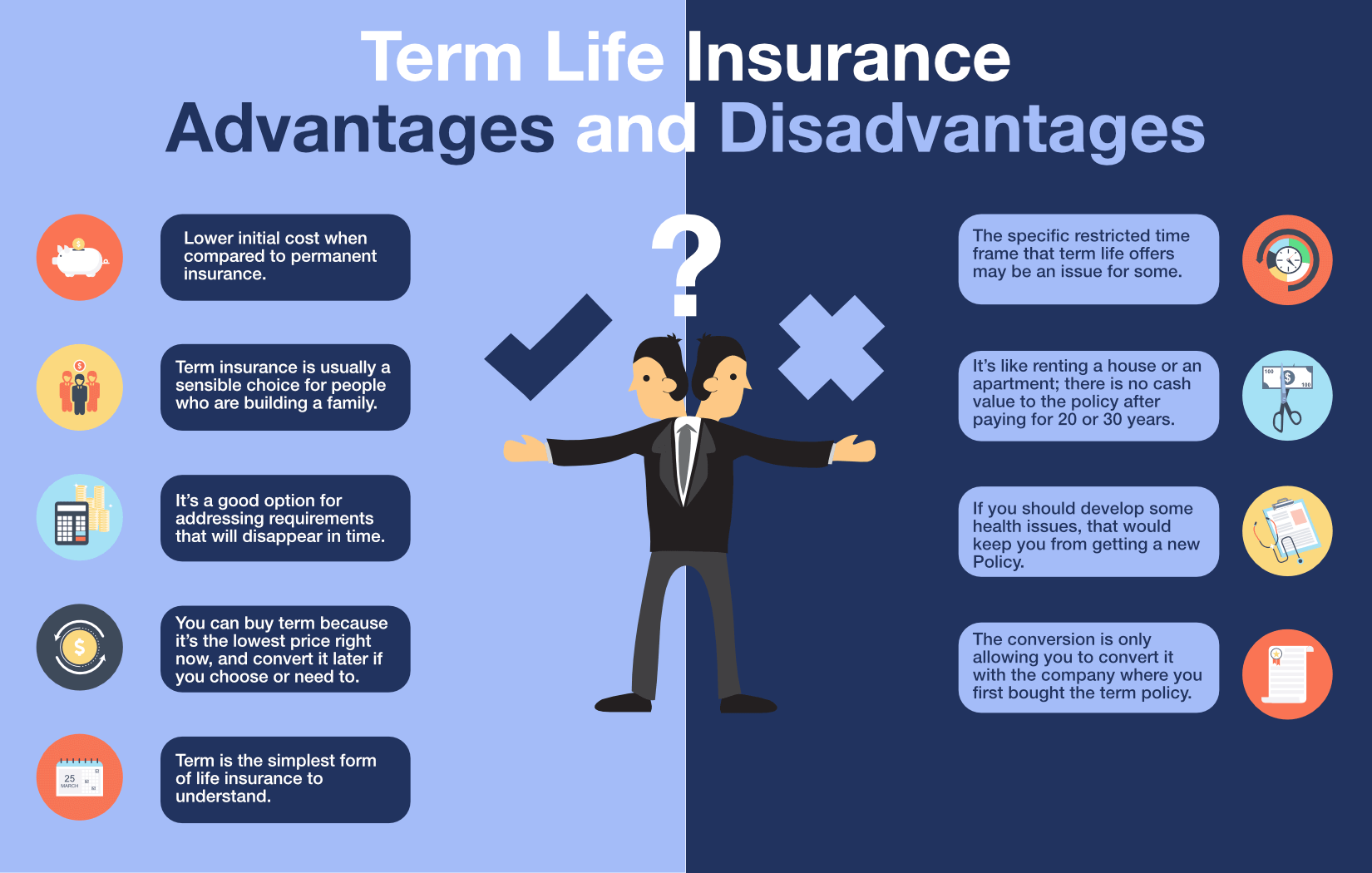

For many people, renting a home or apartment feels like a temporary or transitional stage, something less permanent than homeownership and therefore less in need of formal protection. Yet this assumption often leads renters to overlook one of the most important safeguards available to them: renter’s insurance. While landlords typically carry insurance for the building itself, that coverage does not extend to a tenant’s personal belongings or liability. Renter’s insurance fills that gap, offering a surprisingly robust layer of protection at a relatively low cost. Understanding what renter’s insurance covers, how it works, and why it matters can help renters make informed decisions that protect their financial stability and peace of mind.

At its core, renter’s insurance is designed to protect personal property. Many renters underestimate the value of their belongings, assuming that they do not own enough to justify insurance. But when you add up the cost of furniture, electronics, clothing, kitchenware, and other essentials, the total value can easily reach several thousands of dollars. A single fire, burst pipe, or break‑in could wipe out years of accumulated possessions. Renter’s insurance provides reimbursement for these losses, allowing tenants to replace what was damaged or stolen without bearing the full financial burden. Policies typically cover a wide range of events, including theft, vandalism, smoke damage, and certain types of water damage. For renters who rely on their belongings for work or daily living, this protection can be invaluable.

Another major component of renter’s insurance is liability coverage. This aspect of the policy protects renters if they are found legally responsible for injuries or property damage that occur within their rented space. For example, if a guest slips on a wet floor and suffers an injury, the renter could be held liable for medical expenses or legal fees. Without insurance, these costs could be financially devastating. Liability coverage also extends to accidental damage caused by the renter to someone else’s property. Even a small mishap—like a kitchen fire that spreads to a neighboring unit—can result in significant costs. Renter’s insurance helps shield tenants from these unexpected financial risks, offering a safety net that many people do not realize they need until it is too late.

A lesser‑known but highly valuable feature of renter’s insurance is coverage for additional living expenses. If a rental unit becomes uninhabitable due to a covered event, such as a fire or severe water damage, the policy can help pay for temporary housing, meals, and other necessary expenses. This benefit ensures that renters are not left scrambling for a place to stay or forced to pay out‑of‑pocket for hotel rooms while repairs are underway. In moments of crisis, having this support can make a significant difference in maintaining stability and reducing stress.

One of the most compelling aspects of renter’s insurance is its affordability. Compared to other types of insurance, premiums for renter’s policies are generally low, often costing less per month than a typical streaming subscription. This affordability makes it accessible to a wide range of renters, including students, young professionals, and families. The relatively small investment can yield substantial financial protection, making renter’s insurance one of the most cost‑effective forms of coverage available. For many renters, the peace of mind alone is worth the modest monthly expense.

***

***

Despite its benefits, renter’s insurance remains underutilized. Some renters assume that their landlord’s insurance will cover their belongings, not realizing that the landlord’s policy only protects the building structure. Others believe that their possessions are not valuable enough to insure, or they simply have not taken the time to explore their options. Education plays a key role in addressing these misconceptions. When renters understand what is at stake and how renter’s insurance works, they are more likely to recognize its importance and take steps to protect themselves.

Choosing the right renter’s insurance policy involves evaluating personal needs and understanding the different types of coverage available. One important decision is whether to select actual cash value coverage or replacement cost coverage. Actual cash value policies reimburse the depreciated value of items, while replacement cost policies cover the cost of buying new items at current prices. Although replacement cost coverage is typically more expensive, it often provides more meaningful protection, especially for essential items like electronics or furniture. Renters should also consider the policy’s deductible, coverage limits, and any optional add‑ons that may be relevant to their situation.

Ultimately, renter’s insurance is about more than protecting belongings; it is about safeguarding financial well‑being and creating a sense of security. Life is unpredictable, and even the most careful renter cannot control every circumstance. Whether it is a break‑in, a kitchen accident, or a burst pipe, unexpected events can disrupt daily life and lead to significant expenses. Renter’s insurance offers a practical, affordable way to prepare for these possibilities. By investing in a policy, renters take an important step toward protecting themselves, their possessions, and their future stability.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Physicians are entrepreneurial by nature and take great pride in the creation of their businesses. Market pressures are motivating physicians to be proactive and to make informed decisions concerning the future of their businesses. The decision to sell, buy or merge while often financially driven and is inherently an emotional one. Other economic reasons for a practice valuation include changes in ownership, determining insurance coverage for a practice buy-sell agreement or upon a physician owners death, establishing stock options, or bringing in a new partner.

Practice appraisals are also used for legal reasons such as divorce, bankruptcy, breach of contract and minority shareholder complaints. In 2002, the Financial Accounting Standards Board (FASB) issued rules that required certain intangible assets to be valued, such as goodwill. This may be important for practices seeking start-up, service segmentation extensions, or operational funding.

Estate Planning is another reasons for a medical practice appraisal and the considerations that go along with it are discussed here.

***

***

Estate Planning

Medical practice valuation may be required for estate planning purposes. For a decedent physician with a gross estate of more than $1 million, his or her assets must be reported at fair market value on an estate tax return. If lifetime gifts of a medial practice business interest are made, it is generally wise to obtain an appraisal and attach it to the gift tax return.

Note that when a “closely-held” level of value (in contrast to “freely traded,” “marketable,” or “publicly traded” level) is sought, the valuation consultant may need to make adjustments to the results. There are inherent risks relative to the liquidity of investments in closely held, non-public companies (e.g., medical group practice) that are not relevant to the investment in companies whose shares are publicly traded (freely-traded). Investors in closely-held companies do not have the ability to dispose of an invested interest quickly if the situation is called for, and this relative lack of liquidity of ownership in a closely held company is accompanied by risks and costs associated with the selling of an interest said company (i.e., locating a buyer, negotiation of terms, advisor/broker fees, risk of exposure to the market, etc.).

Conversely, investors in the stock market are most often able to sell their interest in a publicly traded company within hours and receive cash proceeds in a few days. Accordingly, a discount may be applicable to the value of a closely held company due to the inherent illiquidity of the investment. Such a discount is commonly referred to as a “discount for lack of marketability.”

Discount for lack of marketability is typically discussed in three categories: (1) transactions involving restricted stock of publicly traded companies; (2) private transactions of companies prior to their initial public offering (IPO); and, (3) an analysis and comparison of the price to earnings (P/E) ratios of acquisitions of public and private companies respectively published in the “Mergerstat Review Study.”

With a non-controlling interest, in which the holder cannot solely authorize and cannot solely prevent corporate actions (in contrast to a controlling interest), a “discount for lack of control,” (DLOC), may be appropriate. In contrast, a control premium may be applicable to a controlling interest. A control premium is an increase to the pro rata share of the value of the business that reflects the impact on value inherent in the management and financial power that can be exercised by the holders of a control interest of the business (usually the majority holders).

Conversely, a discount for lack of control or minority discount is the reduction from the pro rata share of the value of the business as a whole that reflects the impact on value of the absence or diminution of control that can be exercised by the holders of a subject interest.

Several empirical studies have been done to attempt to quantify DLOC from its antithesis, control premiums. The studies include the Mergerstat Review, an annual series study of the premium paid by investors for controlling interest in publicly traded stock, and the Control Premium Study, a quarterly series study that compiles control premiums of publicly traded stocks by attempting to eliminate the possible distortion caused by speculation of a deal.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on January 24, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters.

***

***

A fake job or ghost job is a scam job posting for a non-existent or already filled position. A scam is a dishonest scheme to gain money or possessions from someone fraudulently, especially a complex or prolonged one.

Due to current economic conditions in 2025, there’s been a rise in scams related to job postings and financial relief offers, preying on people’s financial insecurities. Keep your wits about you and be wary of potential fraud in seemingly legitimate opportunities.

For example, an employer may post fake job opening listings for many reasons such as inflating statistics about their industries, protecting the company from discrimination lawsuits, fulfilling requirements by human-resources departments, identifying potentially promising recruits for future hiring, pacifying existing employees that the company is looking for extra help, or retaining desirable employees. They may also use this strategy to gather information regarding their competitors’ wages. And, there is a rising trend in employers promising remote work as “bait,” and it underscores the relative power of the employers in the job market.

GHOST NURSING: The 1982 Movie

A young woman nanny plagued with bad luck travels to Thailand to visit a friend. There, her friend suggests a visit to a sorcerer, which results in her adopting a child ghost/demon who begins to protect her, but matters soon go awry.

Impact on the Healthcare Field

This is not a 44 year old science-fiction movie. Medicine and the healthcare industry isn’t immune to the ghost job phantom trend. Some contingent labor or medical staffing agencies lack ethics and post jobs solely to bolster their database, without any intention of filling those roles. This deceptive practice misleads job seekers and wastes their time, further eroding trust in the hiring process.

If you are a nanny or caregiver, you may have your services listed on an online job site. While this is a great way to find work, it can also open you to ghost scams. One phone scam is to send you an offer of employment. The “employer” sends you a check, and asks you to send them some money to buy assistive care items needed for the job. However, the person you are talking to isn’t really interested in you. After you’ve sent the money, the check will bounce and the “employer” will ghost you and disappear. Not only do you not really have a job, you just sent money to a ghost scammer and will not be reimbursed.

Impact on the Finance Field

In finance, ghost jobs can appear for various reasons, such as companies wanting to gauge the labor market, fulfill internal posting policies, or maintain a pool of potential candidates. Consulting roles, including those in financial planning, have seen an increase in ghost jobs, with some firms keeping listings open despite slowing hiring activity. The IRS will never ghost call, but your bank might, which makes it harder to figure out if it’s the real deal; or a ghost scam. Plus, it makes sense that your bank would need to confirm your identity to protect your account. If your bank calls and asks you to confirm if transactions are legitimate, feel free to give a yes or no. But don’t give up any more information than that, says Adam Levin, founder of global identity protection and data risk services firm CyberScout and author of Swiped: How to Protect Yourself in a World Full of Scammers, Phishers, and Identity Thieves. Some scammers rattle off your credit card number and expiration date, then ask you to say your security code as confirmation, he says. Others will claim they froze your credit card because you might be a fraud victim, then ask for your Social Security number.

If someone claiming to be your accountant, insurance agent or financial advisor calls and says you have a computer problem with them, just say no and hang up. No one is ‘watching’ your computer for signs of a virus. And, those scammers won’t fix the problem—they’ll make it worse by installing malware or stealing your account information or even money.

Promoters of cryptocurrency and other investments use complex schemes, often enhanced through deepfake videos or AI-manipulated audio, to lend credibility. According to the FBI’s Internet Crime Complaint Center (IC3), victims reported an estimated $3.9 billion in losses from investment fraud in 2024. Promises of “guaranteed returns” or requests for money transfers via crypto wallets are warning signs.

Many targets lack experience in crypto markets, amplifying risk. Do thorough research, consult official resources (like SEC.gov), and use licensed platforms if investing. Treat “sure thing” tips and unsolicited offers as red flags.

***

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on November 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Retirement planning has evolved significantly over the past several decades, with employers and employees seeking solutions that balance security, flexibility, and predictability. Among the various retirement plan options available today, cash balance plans stand out as a hybrid design that combines features of both traditional defined benefit pensions and defined contribution plans. Their unique structure makes them an attractive choice for employers aiming to provide meaningful retirement benefits while maintaining financial predictability.

At their core, cash balance plans are a type of defined benefit plan. Unlike traditional pensions, which promise retirees a monthly income based on years of service and final salary, cash balance plans define the benefit in terms of a hypothetical account balance. Each participant’s account grows annually through two components: a “pay credit” and an “interest credit.” The pay credit is typically a percentage of the employee’s salary or a flat dollar amount, while the interest credit is either a fixed rate or tied to an index such as U.S. Treasury yields. Although the account is hypothetical—meaning the funds are not actually segregated for each employee—the structure provides participants with a clear, understandable statement of their retirement benefit.

One of the primary advantages of cash balance plans is their transparency. Employees can easily track the growth of their account balance, much like they would with a 401(k). This clarity helps workers better understand the value of their retirement benefits and fosters a sense of ownership. Additionally, cash balance plans are portable: when employees leave a company, they can roll over the vested balance into an IRA or another qualified plan, ensuring continuity in retirement savings.

***

***

From the employer’s perspective, cash balance plans offer several benefits as well. Traditional pensions often create unpredictable liabilities, as they depend on factors such as longevity and investment performance. Cash balance plans, by contrast, provide more predictable costs because the employer commits to specific pay and interest credits. This predictability makes them easier to manage and budget for, particularly in industries where workforce mobility is high. Moreover, cash balance plans can be designed to reward long-term employees while still appealing to younger workers who value portability.

Despite these advantages, cash balance plans are not without challenges. Because they are defined benefit plans, employers bear the investment risk and must ensure the plan is adequately funded. Regulatory requirements, including nondiscrimination testing and funding rules, add complexity and administrative costs. Additionally, while cash balance plans are generally more equitable across generations of workers, transitions from traditional pensions to cash balance designs have sometimes sparked controversy, particularly among older employees who may perceive a reduction in benefits.

In recent years, cash balance plans have gained popularity among professional firms, such as law practices and medical groups, as well as small businesses seeking tax-efficient retirement solutions. These plans allow owners and highly compensated employees to accumulate larger retirement savings than would be possible under defined contribution limits, while still providing benefits to rank-and-file workers. As such, they serve as a valuable tool for both talent retention and financial planning.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

For generations, the prevailing belief in healthcare has been that physicians [MD, DO and DPM], with their high salaries and prestige, inevitably retire wealthier than nurses. Yet this assumption overlooks the financial realities of different nursing specialties and the long‑term impact of debt, lifestyle, and retirement planning. In fact, some Registered Nurses (RNs)—particularly Certified Registered Nurse Anesthetists (CRNAs), visiting nurses, and those who participate in structured pay programs like the Baylor plan—can retire richer than physicians. The reasons lie in the interplay of education costs, career flexibility, income potential, and disciplined financial planning.

Education Costs and Debt Burden

One of the most decisive factors shaping retirement wealth is the cost of education. Physicians often spend over a decade in training, including undergraduate studies, medical school, and residency. This path not only delays their earning years but also saddles them with substantial student debt. The median medical school debt in the United States exceeds $200,000, and many physicians spend years paying it down.

By contrast, RNs typically complete their training in two to four years, with advanced practice nurses such as CRNAs requiring graduate‑level education. Even so, their debt burden is far lighter, often less than half of what physicians carry. This difference means nurses can begin earning earlier, save for retirement sooner, and avoid the crushing interest payments that erode physicians’ wealth. A CRNA who starts practicing in their late twenties may already be investing in retirement accounts while a physician is still in residency earning a modest stipend.

Income Potential of Specialized Nurses

While physicians generally earn more annually than nurses, the gap is narrower in certain specialties. CRNAs, for example, are among the highest‑paid nursing professionals, with average salaries often exceeding $200,000 per year. This places them in direct competition with some physician specialties, especially primary care doctors, who may earn similar or even lower salaries.

Visiting nurses also benefit from unique financial advantages. Many work on flexible schedules, contract arrangements, or per‑visit compensation models. This allows them to maximize income while minimizing burnout. By avoiding the overhead costs of private practice and the administrative burdens physicians face, visiting nurses can channel more of their earnings directly into savings and investments.

When combined with lower debt and earlier career starts, these income streams can compound into significant retirement wealth.

The Baylor plan, a structured pay program used by some hospitals, allows nurses to work full‑time hours compressed into fewer days—often weekends—while still receiving full‑time pay and benefits. This arrangement provides several financial advantages. First, it enables nurses to earn competitive wages while freeing up weekdays for additional work, education, or entrepreneurial ventures. Second, it reduces commuting and childcare costs, allowing more income to be saved. Third, the plan often includes robust retirement benefits, such as employer‑matched contributions to 401(k) or pension programs.

Nurses who consistently participate in such structured pay plans can accumulate substantial nest eggs, often surpassing physicians who delay retirement savings due to debt repayment or lifestyle inflation. The Baylor plan highlights the importance of systematic investing: by automating contributions and focusing on long‑term growth, nurses can harness the power of compound interest. A nurse who invests steadily for 35 years may accumulate more wealth than a physician who begins saving late and inconsistently, despite earning a higher salary.

Lifestyle and Work‑Life Balance

Another overlooked factor is lifestyle. Physicians often face grueling schedules, high stress, and the temptation to maintain expensive lifestyles commensurate with their social status. Luxury homes, cars, and vacations can erode their financial base. Nurses, while not immune to lifestyle inflation, often maintain more modest spending habits.

Visiting nurses, in particular, enjoy flexibility that allows them to balance work with personal life. This reduces burnout and healthcare costs while enabling consistent employment into later years. By living within their means and prioritizing savings, nurses can accumulate wealth steadily without the financial pitfalls that sometimes accompany physician lifestyles.

Retirement Wealth Beyond Salary

Retirement wealth is not solely determined by annual income. It is shaped by debt management, savings discipline, investment strategies, and lifestyle choices. Nurses who leverage high‑paying specialties like anesthesia, flexible arrangements like visiting nursing, and structured programs like the Baylor plan can outperform physicians in these areas.

Consider two professionals: a physician earning $250,000 annually but burdened by $200,000 in debt and high living expenses, and a CRNA earning $200,000 with minimal debt and disciplined savings. Over decades, the CRNA may accumulate more net wealth, retire earlier, and enjoy greater financial security.

Conclusion

The assumption that physicians always retire richer than nurses is outdated. While physicians command higher salaries, their delayed earnings, heavy debt, and lifestyle pressures often undermine long‑term wealth. Nurses, particularly CRNAs, visiting nurses, and those who participate in structured pay programs like the Baylor plan, can retire wealthier by combining lower debt, earlier savings, competitive incomes, and disciplined financial planning.

Ultimately, retirement wealth is not about prestige but about strategy. Nurses who recognize this truth and act accordingly may find themselves enjoying more financial freedom than the very physicians they once assisted.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Here’s a risk to your financial health that may surprise you!

By Rick Kahler CFP™

There are two reasons for this.

First, we tend to trust and rely on people we know.

Second, research finds that humans have a deep-seated desire to meet the needs of others, so “helping” a relative or friend get started in their financial sales career is just human nature. Unfortunately, brokerage and insurance companies know this. They train their new agents that the easiest sales to make when getting started are to relatives and friends.

Any time I find an ill-advised financial product a client has purchased from a relative or friend, I cringe, anticipating the client’s resistance to canceling it. Regardless of how bad the advice was or how outrageous the fees of an investment product may be, the deeper the relationship the more difficulty there will be in changing course.

***

***

Here’s a typical example

Jim and Sofia, two young professionals, married at around the same time Jim’s uncle went to work for a financial services company. The uncle sold Jim a $250,000 Variable Universal Life (VUL) policy with a $500 monthly premium. Jim and Sofia were happy, thinking they had made a prudent choice to start saving for retirement and help out a relative at the same time.

When Sofia became pregnant, the couple decided to engage a fee-only financial planner. She found they were under insured to provide for a family and also that the VUL policy was incredibly expensive and ill-advised for their needs. She recommended canceling the VUL policy with its $500 monthly premium, instead paying $300 monthly for two $1 million term life insurance policies and putting $200 a month into a tax-free Roth IRA.

Sofia and Jim told this to their uncle, who was “shocked” at the planner’s “poor advice.”

He contended that any competent financial planner would know a person needs permanent insurance as a foundation to “raise their child in the case of a premature death, fund their retirement, pay estate taxes and just like a Roth, it is tax free.”

Sadly, the uncle was unwilling to admit that $250,000 of insurance wouldn’t be enough to raise their child, fund their retirement, and pay estate taxes; nor was it truly tax free. He also didn’t mention that he had a vested interest in their keeping the policy. While he probably earned 55% to 100% of the first year’s commission, it is common practice that an agent will also receive 10-15% of the annual premium from years 2-10.

***

***

Sofia and Jim agreed with the financial planner’s recommendation. They could see the sense in having $1 million of insurance on each of them instead of $250,000 on just Jim for almost half the price, plus the tax-free growth of $200 a month in the Roth IRA.

Yet they didn’t follow the planner’s advice, because they didn’t want to upset their uncle. They chose to weaken their financial health, plus risk the well-being of their family if one of them died prematurely, in order to enrich their uncle for fear of offending him.

This happens more frequently than you would think. And it isn’t limited to life insurance. I’ve seen clients invest in a variety of “opportunities,” based on advice from a family member, that were not in their best interest.

Assessment

Next time a friend or family member offers to sell you a financial product or give you some great advice, you may want to do yourself a favor and decline. If you really want to help them out, invite them over for dinner.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, urls and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Posted on October 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelsen CFA

***

***

One of the biggest hazards of being a professional money manager is that you are expected to behave in a certain way.

One of the biggest hazards of being a professional money manager is that you are expected to behave in a certain way: You have to come to the office every day, work long hours, slog through countless emails, be on top of your portfolio (that is, check performance of your securities minute by minute), watch business TV and consume news continuously, and dress well and conservatively, wearing a rope around the only part of your body that lets air get to your brain. Our colleagues judge us on how early we arrive at work and how late we stay. We do these things because society expects us to, not because they make us better investors or do any good for our clients.

Somehow we let the mindless, Henry Ford–assembly-line, 8:00 a.m. to 5:00 p.m., widgets-per-hour mentality dictate how we conduct our business thinking. Though car production benefits from rigid rules, uniforms, automation and strict working hours, in investing — the business of thinking — the assembly-line culture is counterproductive. Our clients and employers would be better off if we designed our workdays to let us perform our best.

Investing is not an idea-per-hour profession; it more likely results in a few ideas per year. A traditional, structured working environment creates pressure to produce an output — an idea, even a forced idea. Warren Buffett once said at a Berkshire Hathaway annual meeting: “We don’t get paid for activity; we get paid for being right. As to how long we’ll wait, we’ll wait indefinitely.”

How you get ideas is up to you. I am not a professional writer, but as a professional money manager, I learn and think best through writing. I put on my headphones, turn on opera and stare at my computer screen for hours, pecking away at the keyboard — that is how I think. You may do better by walking in the park or sitting with your legs up on the desk, staring at the ceiling.

I do my best thinking in the morning. At 3:00 in the afternoon, my brain shuts off; that is when I read my emails. We are all different. My best friend is a brunch person; he needs to consume six cups of coffee in the morning just to get his brain going. To be most productive, he shouldn’t go to work before 11:00 a.m.

And then there’s the business news. Serious business news that lacked sensationalism, and thus ratings, has been replaced by a new genre: business entertainment (of course, investors did not get the memo). These shows do a terrific job of filling our need to have explanations for everything, even random events that require no explanation (like daily stock movements). Most information on the business entertainment channels — Bloomberg Television, CNBC, Fox Business — has as much value for investors as daily weather forecasts have for travelers who don’t intend to go anywhere for a year.

Yet many managers have CNBC, Fox or Bloomberg TV/Internet streaming on while they work.

“THE INVESTOR’S CHIEF problem—even his worst enemy—is likely to be himself.” So wrote Benjamin Graham, the father of modern investment analysis.

With these words, written in 1949, Graham acknowledged the reality that investors are human. Though he had written an 800 page book on techniques to analyze stocks and bonds, Graham understood that investing is as much about human psychology as it is about numerical analysis.

In the decades since Graham’s passing, an entire field has emerged at the intersection of psychology and finance. Known as behavioral finance, its pioneers include Daniel Kahneman, Amos Tversky and Richard Thaler. Together, they and their peers have identified countless human foibles that interfere with our ability to make good financial decisions. These include hindsight bias, recency bias and overconfidence, among others. On my bookshelf, I have at least as many volumes on behavioral finance as I do on pure financial analysis, so I certainly put stock in these ideas.

At the same time, I think we’re being too hard on ourselves when we lay all of these biases at our feet. We shouldn’t conclude that we’re deficient because we’re so susceptible to biases. Rather, the problem is that finance isn’t a scientific field like math or physics. At best, it’s like chaos theory. Yes, there is some underlying logic, but it’s usually so hard to observe and understand that it might as well be random. The world of personal finance is bedeviled by paradoxes, so no individual—no matter how rational—can always make optimal decisions.

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just last year.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.”

In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.

Yourmedical practice. Your personal goals. Your financial plan. Our experienced confirmation guide.

***

***

When you know exactly where you are today, have a vision of where you want to be tomorrow, and have trusted counsel at your side, you have already achieved so much success. Marcinko Associates works to keep you at that level of confidence every day. We use a comprehensive economic process to uncover what’s most important to you and then develop a financial strategy that gives you the highest probability of achieving your monetary goals.

We assess, plan, and opine for your success

To accurately see where you are today, chart a strategic path to your goals and help you make the most informed decisions to keep you on financial track, our key services for physicians and high net worth medical clients include:

Investment Portfolio Review

Fee, Charge and Cost Review

Comprehensive Financial Planning

Insurance Reviews

Estate Planning

Investment and Asset Management Second Opinions

We take a deep dive into your financial retirement plans

Physicians and dental employers now have options for how to design and deliver retirement benefits and we can help you make the best choice for your healthcare business. Our services for retirement plans include:

Fee, Charges & Fiduciary Review

Portfolio Analysis

Single Employer Retirement Plan Advisory

Retirement Plans Risk Analysis

Capital Funding and Financing

Business Planning and Practice Valuations

Career Development

and more!

We take a broad and balanced look at your financial life life

We coordinate our recommendations with your other advisors, including attorneys, accountants, insurance professionals and others, to ensure each decision is consistent with your goals and overall strategy. For example, through our partnerships we offer physician colleagues deeper expanded advisory services, like:

Classic Definition: Research from Ernst-Young [Nikhil Lele and Yang Shim] uncovered a chasm between how consumer patients think they’re doing financially, and the actual state of their finances. Even more striking, their study suggested that improving consumers’ financial health will become one of the top imperatives in reframing consumer financial services.

Modern Circumstance: For example, the study asked consumers to rate their own financial health, and 83 percent rated themselves “good,” “very good” or “excellent.” Now, contrast this figure with what is known about their actual situation:

60 percent of Americans say they are financially stressed.

56 percent of Americans have less than $10,000 saved for retirement.

40 million American families have no retirement savings at all.

40 percent of Americans are not prepared to meet a $400 short-term emergency.

Paradox Example: Fortunately, even though the vast majority of consumers rate themselves as financially healthy, the study found that most still want to improve. Importantly for health economists, the attractive 25-34 and 35-49 year-old age groups were most likely to be extremely or very interested in improving their financial and economic health.

Paradox Example: Massively affluent consumer patients are even more interested in improving this paradox than their mass market counterparts.

If you are just starting out managing your finances and don’t know where to begin, a financial coach may be a good option for you. They are helpful for someone who wants to become proficient in the basics of finance, from learning how to budget or save money to building an emergency fund or creating a plan for paying off debt. If you have short-term money goals, like saving for a big purchase or just practicing better money habits, a financial coach can help you reach them by working with you to create a plan and holding you accountable. Even more for physicians and most all medical professionals.

Pros and Cons of Working with a Financial Coach A financial coach can have a positive impact on your financial well–being and your life in a number of ways:

Financial coaches see the bigger picture of how you relate to money. They can help you develop better habits, resulting in positive personal growth.

By providing education and encouragement, they can reduce financial stress, confusion, and what it is about money that overwhelms you.

Through accountability and support, they can help you accomplish your goals and help you feel more confident in your finances.

Available 24/7/365.

Modest fees.

At you service. Dr. David Edward Marcinko MBA MEd CMP

A psychological paradox is a figure of speech that can seem silly or contradictory in form, yet it can still be true, or at least make sense in the context given.

This is sometimes used to illustrate thoughts or statements that differ from traditional ideas. So, instead of taking a given statement literally, an individual must comprehend it from a different perspective. Using paradoxes in speeches and writings can also add wit and humor to one’s work, which serves as the perfect device to grab a reader or a listener’s attention and/or persuade them to action, sales and closing statements. But paradoxes for the financial sector can be quite difficult to explain by definition alone, which is why it is best to refer to a few examples to further your understanding.

One good psychological paradox example is The Paradox of Thrift which suggests that while saving money is generally considered a prudent financial behavior, excessive saving during times of economic downturn can actually hinder economic recovery. When consumers collectively reduce their spending and increase their savings, it creates a decrease in aggregate demand. This reduction in demand can lead to lower production levels, job losses, and ultimately a decline in economic output. In other words, what may be individually rational behavior (financial saving) can have negative consequences for the overall economy.

The following paradoxical contradictions will help financial advisors guide clients to close more sales to the benefit of both.

____

In the intricate world of finance sales, advisors are often at the crossroads of various paradoxes that challenge client decision-making. While the journey towards financial security involves calculated strategies, it’s the nuanced understanding of paradoxes that can help the advisor close more sales.

____

But, what seems trueabout money often turns out to be false, according to colleague Finance Professor John Goodell, PhD from the University Akron:

The more we try to trade our way to profits, the less likely we are to profit.

The more boring an investment—think index funds—the more exciting the long-run performance will probably be.

The more exciting an investment—name your latest Wall Street concoction, Special Purpose Acquisition Company [SPAC] or anything crypto—the less exciting the long-term results typically are.

The only certainty is uncertainty and the only constant is change. Today’s market decline will eventually become a bull market, and today’s market leaders will eventually yield to other stocks.

Big market trends play a huge role in investment results, and yet trying to time macroeconomic cycles or guess which market sectors will outperform is a fool’s errand. Many big market rotations are set in motion by something wholly unanticipated, like a virus pandemic or a war.

To be happy when wealthy, we also need to be happy with far less money. The fact is, above a relatively modest income level, no amount of extra money will change our level of happiness. More money might even make us miserable, as many lottery winners have discovered.

The more we hate an investing trait—or any trait for that matter—the more likely it is that we’re resisting seeing that trait in ourselves. It’s what Carl Jung MD called the Shadowof Undesirable Personality Aspects that we hide from ourselves. Do prospects get irritated listening to your unsolicited financial advice? There’s a good chance that you often give unsolicited financial advice but don’t like to admit it.

The more we learn about investing, the more we realize we don’t know anything. We should just buy index funds and instead spend our time worrying about stuff we can actually control.

The more an investor is convinced he’s right, the more likely he is to be wrong. Short sellers, in particular, are likely to succumb to this paradoxical trap.

The more options we have, the less satisfied we’ll be with each one. This is the Paradox of Choice; revised. Anyone who has spent hours “optimizing” his or her portfolio knows this all too well. Its close cousin is information overload, another frustration paradox when investing.

The more afraid we are of losing money, the more likely we are to take unwitting risks that lose us money. Sitting in cash seems wise during market selloffs. But the truth is, none of us can reliably time the market. Pull up any chart of the stock market over any period longer than a decade and you’ll see that the riskiest decision is sitting in cash, which gets destroyed by inflation.

The more we think about our investments and look at our financial accounts, the more likely we are to damage our results by buying high because of greed and selling low because of fear. It can pay to look away.

ASSESSMENT

How should you respond to these financial paradoxes? As you plan for your own financial future, as well as your own client prospecting endeavors, embrace the concept of “loosely held views.”

In other words, make financial and client acquisitions plans, but continuously update your views, question your assumptions and paradoxes and rethink your priorities. Years of experience with clients certainly support the futility of trying to help them change their financial behavior by telling them what they “should” know or do.

CONCLUSION

Remember, it is far more useful to listen to client beliefs, fears and goals, and to suggest options and offer encouragement to help them discover their own path toward financial well-being. Then, incentivize them with knowledge of the above psychological paradoxes to your mutual success!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Marcinko, DE and Hetico, HR: Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2016.

Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York. 2006

Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2015.

Alternatively Weighted Exchange Traded Funds are designed to track an index that is constructed based on criteria other than market capitalization (the methodology used for most traditional indexes).

Instead, alternatively weighted indexes select and weight securities based on other factors, such as growth, valuation, and price momentum, among others. Examples include:

Invesco S&P 500 Equal Weight ETF (NYSEARCA: RSP)

SPDR Technology ETF (NYSEARCA: XNTK)

First Trust NYSE Arca Biotechnology Index Fund (NYSEARCA: FBT)

Amplify Online Retail ETF (NASDAQ: IBUY)

iShares MSCI USA Equal Weighted ETF (NYSEARCA: EUSA)

FIVE INVESTING MISTAKES OF DOCTORS; PLUS 1 VITAL TIP

As a former US Securities and Exchange Commission [SEC] Registered Investment Advisor [RIA] and business school professor of economics and finance, I’ve seen many mistakes that doctors must be aware of, and most importantly, avoid. So, here are the top 5 investing mistakes along with suggested guideline solutions.

Mistake 1: Failing to Diversify Investment but Beware Di-Worsification

A single investment may become a large portion of your portfolio as a result of solid returns lulling you into a false sense of security. The Magnificent Seven stocks are a current example:

Apple, up +5,064%% since 1/18/2008

Amazon, up +30,328% since 9/6/2002

Alphabet, up +1,200% since 7/20/2012

Tesla, up +21,713% since 11/16/2012

Meta, up +684% since 2/20/2015

Microsoft, up +22% since 12/21/2023

Nvidia, up +80,797% since 4/15/2005

Guideline: The Magnificent Seven [7] has grown from 9% of the S&P 500 at the end of 2013 to 31% at the end of 2024! That means even if you don’t own them, you’re still very exposed if you have an Index Fund [IF] or Exchange Traded Fund [ETF] that tracks the market. Accordingly, diversification is the only free lunch in investing which can reduce portfolio risk. But, remember the Wall Street insider aphorism that states: “Di-Versification Means Always Having to Say Your Sorry.”

The term “Di-Worsification” was coined by legendary investor Peter Lynch in his book, One Up On Wall Street to refer to over-diversifying an investment portfolio in such a way that it reduces your overall risk-return characteristics. In other words, the potential return rises with an increase in risk and invested money can render higher profits only if willing to accept a higher possibility of losses [1].

A podiatrist can easily fall into the trap of chasing securities or mutual funds showing the highest return. It is almost an article of faith that they should only purchase mutual funds sporting the best recent performance. But in fact, it may actually pay to shun mutual funds with strong recent performance. Unfortunately, many struggle to appreciate the benefits of their investment strategy because in jaunty markets, people tend to run after strong performance and purchase last year’s winners.

Similarly, in a market downturn, investors tend to move to lower-risk investment options, which can lead to missed opportunities during subsequent market recoveries. The extent of underperformance by individual investors has often been the most awful during bear markets. Academic studies have consistently shown that the returns achieved by the typical stock or bond fund investors have lagged substantially.

Guideline: Understand chasing performance does not work.Continually monitor your investments and don’t feel the need to invest in the hottest fund or asset category. In fact, it is much better to increase investments in poor performing categories (i.e. buy low). Also keep in remind rebalancing of assets each year is key. If stocks perform poorly and bonds do exceptionally well, then rebalance at the end of the year. In following this strategy, this will force a doctor into buying low and selling high each year.

Often doctors make their investment decisions under the belief that stocks will consistently give them solid double-digit returns. But the stock markets go through extended long-term cycles.

In examining stock market history, there have been 6 secular bull markets (market goes up for an extended period) and 5 secular bear markets (market goes down) since 1900. There have been five distinct secular bull markets in the past 100+ years. Each bull market lasted for an extended period and rewarded investors.

For example, if an investor had started investing in stocks either at the top of the markets in 1966 or 2000, future stock market returns would have been exceptionally below average for the proceeding decade. On the other hand, those investors fortunate enough to start building wealth in 1982 would have enjoyed a near two-decade period of well above average stock market returns. They key element to remember is that future historical returns in stocks are not guaranteed. If stock market returns are poor, one must consider that he or she will have to accept lower projected returns and ultimately save more money to make up for the shortfall. For example,

The May 6th, 2010, flash crash, also known as the crash of 2:45, was a United States trillion-dollar stock market plunge which started at 2:32 pm EST and lasted for approximately 36 minutes.

And, investors who have embraced the “buy the dip” strategy in 2025 have been handsomely rewarded, with the S&P 500 delivering its strongest post-pull back returns in over three decades.

According to research from Bespoke Investment Group, the S&P 500 has gained an average of 0.36% in the trading session following a down day so far in 2025. The only year with a comparable performance was 2020, which saw a 0.32% average post-dip gain [2].

The most recent example came on May 27, 2025 when the S&P 500 surged more than 2% after falling 0.7% in the final session before the holiday weekend. The rally was sparked by President Trump’s decision to scale back huge previously threatened tariffs on EU —a recurring catalyst behind many of 2025’s rebound.

Guideline: Beware of projecting forward historical returns. Doctors should realize that the stock markets are inherently volatile and that, while it is easy to rely on past historical averages, there are long periods of time where returns and risk deviate meaningfully from historical averages.

Some doctors believe they are “smarter than the market” and can time when to jump in and buy stocks or sell everything and go to cash. Wouldn’t it be nice to have the clairvoyance to be out of stocks on the market’s worst days and in on the best days?

Using the S&P 500 Index, our agile imaginary doctor-investor managed to steer clear of the worst market day each year from January 1st, 1992 to March 31st, 2012. The outcome: s/he compiled a 12.42% annualized return (including reinvestment of dividends and capital gains) during the 20+ years, sufficient to compound a $10,000 investment into $107,100.

But what about another unfortunate doctor-investor that had the mistiming to be out of the market on the best day of each year. This ill-fated investor’s portfolio returned only 4.31% annualized from January 1992 – March 2012, increasing the $10,000 portfolio value to just $23,500 during the 20 years. The design of timing markets may sound easy, but for most all investors it is a losing strategy.

More contemporaneously on December 18th 2024, the DJIA plummeted 2.5%, while the S&P 500 declined 3% and the NASDAQ tumbled 3.5%

Guideline: If it looks too good to be true, it probably is. While jumping into the market at its low and selling right at the high is appealing in theory, we should recognize the difficulties and potential opportunity and trading costs associated with trying to time the stock market in practice. In general, colleagues are be best served by matching their investment with their time horizon and looking past the peaks / valleys along the way.

Mistake 5: Failing to Recognize the Impact of Fees and Expenses

A free dinner seminar or a polished stock-broker sales pitch may hide the total underlying costs of an investment. So, fees absolutely matter.

The first costing step is determining what the fees actually are. In a mutual fund, these costs are found in the company’s obligatory “Fund Facts”. This manuscript clearly outlines all the fees paid–including up front fees (commissions and loads), deferred sales charges and any switching fees. Fund management expense ratios are also part of the overall cost. Trading costs within the fund can also impact performance.

Here is a list of the traditional mutual fund fees:

Front End Load: The commission charged to purchase a fund through a stock broker or financial advisor. The commission reduces the amount you have available to invest. Thus, if you start with $100,000 to invest, and the advisor charges up to an 8 percent front end load, you end up actually investing $92,000.

Deferred Sales Charge (DSC) or Back End Load: Imposed if you sell your position in the mutual fund within a pre-specified period of time (normally one – five years). It is initiated at a higher start percentage (i.e. as high as 10 percent) and declines over a specific period of time.

Operating Fees: Costs of the mutual fund including the management fee rewarded to the manager for investment services. It also includes legal, custodial, auditing and marketing fees.

Annual Administration Fee: Many mutual fund companies also charge a fee just for administering the account – usually under $100-150 per year.

Guideline: Know and understand all fees.

For example: A 1 percent disparity in fees may not seem like much but it makes a considerable impact over a long time period.

Consider a $100,000 portfolio that earns 8 percent before fees, grows to $320,714 after 20 years if the investor pays a 2 percent operating fee. In comparison, if s/he opted for a fund that charged a more reasonable 1 percent fee, after 20 years, the portfolio grows to be $386,968 – a divergence of over $66,000!

This is the value of passive or index investing. In the case of an index fund, fees are generally under 0.5 percent, thus offering even more savings over a long period of time.

One Vital Tip: Investing Time is on Your Side

Despite thousands of TV shows, podcasts, textbooks, opinions and university studies on investing, it really only has three simple components. Amount invested, rate of return and time. By far, the most important item is time! For example:

Nvidia: if you invested $1,000 in 2009, you’d have $338,103 today.

Apple: if you invested $1,000 in 2008, you’d have $48,005 today.

Netflix: if you invested $1,000 in 2004, you’d have $495,679 today.

Unfortunately, this list of investing mistakes is still being made by many doctors. Fortunately, by recognizing and acting to mitigate them, your results may be more financially fruitful and mentally quieting.

REFERENCES:

1. Lynch, Peter: One Up on Wall Street [How to Use What You Already Know to Make Money in the Market]: Simon and Shuster (2nd edition) New York, 2000.

1. Marcinko, DE; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

2. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York, 2006.

3. Marcinko, DE; Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] CRC Press, New York, 2015.

BIO: As a former university Professor and Endowed Department Chair in Austrian Economics, Finance and Entrepreneurship, the author was a NYSE Registered Investment Advisor and Certified Financial Planner for a decade. Later, he was a private equity and wealth manager

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on June 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

A POD (Payable on Death) or TOD (Transfer on Death) account is a type of bank account where the account owner names a beneficiary to receive the account assets when the owner dies.

Key points about these accounts include:

Beneficiaries can be anyone, including minors, non-U.S. citizens, and organizations.

The beneficiary needs to provide a certified copy of the deceased’s death certificate to the bank or brokerage firm.

The assets are transferred immediately upon the account owner’s death.

Probate avoidance: By sidestepping probate, POD and TOD accounts streamline the distribution of assets post-death, allowing beneficiaries to gain access to these funds with greater speed.

Simplicity: Setting up these accounts is generally straightforward, often requiring just the completion of a form at the bank or brokerage firm.

No additional cost: There’s usually no cost to establish these accounts, aligning with the needs of individuals seeking a cost-effective method of transferring assets.

Cons

Joint ownership complexity. When an account is jointly owned, the beneficiary of the account won’t receive the assets until the surviving owner(s) die. The same applies to accounts owned in states with tenancy by the entirety for married couples.

Naming alternative beneficiaries: These accounts do not allow for the nomination of alternative beneficiaries if the primary beneficiary or beneficiaries predecease the account owner. This could lead to the assets being subjected to probate if the primary beneficiary is no longer alive at the time of the account holder’s death.

Transfers only happen after death: These accounts stipulate that the person must pass away before the beneficiary can access the funds – a restriction that could prove troublesome if the beneficiary requires access to these assets during the account holder’s life or if the account owner becomes incapacitated during their lifetime.

Many doctors are surprised to learn of an alternative investment known as a hedge fund, pooled investment vehicle or private investment fund. Unlike mutual funds, they can be structured in many ways. However, these funds cannot be marketed or advertised, but they are far from illegal or illicit.

In fact, physicians were among the early investors in one the most successful hedge funds. Warren Buffett got his start in 1957 running the Buffett Partnership, a hedge fund not open to the public. His first appearance as a money manager was before a group of physicians in Omaha, Nebraska. Eleven decided to invest some money with him. A few then followed into Berkshire Hathaway Inc, now among the most highly valued companies in the world.

And, more recently, Scion Asset Management® LLC, is a private investment firm founded and led by my eloquent colleague Michael J. Burry, MD and featured in the movie, The Big Short. Other hedge fund mangers of note include: George Soros, Carl Icahn, Ken Griffin, David Tepper, John Paulson and Bill Ackman.

A hedge fund is a limited partnership of private investors whose money is managed by professional fund managers who use a wide range of strategies; including leveraging [debt] or trading of non-traditional assets [real-estate, collectible, commodities, cyrpto-currency, etc] to earn above-average returns. Hedge funds are considered a risky alternative investment and usually require a high minimum investment or net worth. This person is known as an “accredited investor” or “Regulation D” investor by the US Securities Exchange Commission and must have the following attributes: