BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

An app, which is short for “application,” is a type of software that can be installed and run on a computer, tablet, smartphone or other electronic devices. An app most frequently refers to a mobile application or a piece of software that is installed and used on a computer. Most apps have a specific and narrow function.

An easy and fairly cheap way for novices to get into investing is to use a robo-advisor. Basically, the funds you contribute will be invested by an algorithm based upon your goals, which are usually determined by taking a survey. This helps keep fees low; the algorithm doesn’t rely on a human expert to make trades, and you don’t have to spend significant amounts of time researching your investments. While this is a good way to start, it may not be the best option in the long run.

Online Brokerage or Investment Apps

More options are becoming available all the time, and they have opened trading to a much larger percentage of the population. That is a great thing, but it’s important to remember that “easier to invest” doesn’t necessarily mean it’s easy to invest well.

Be wary of apps that “gamify” trading and encourage risky choices. Keep in mind that trusted names offer more security, so do your research when you are selecting a platform.

WHAT YOU “MUST KNOW“ ABOUT FINANCIAL ADVISORY FEES

Investment fees still matter despite dropping dramatically over the past several decades due to computer automation, algorithms and artificial intelligence, etc. And, they can make a big difference to your financial health. So, before buying any investment, it’s vital to uncover all real financial advisor and stock broker costs.

1. Up-front salesperson commissions. It is easy to ask; “If I buy this investment today and want to get out tomorrow, how much money do I get back?” If the answer is not “all your money,” the difference is probably upfront fees and commissions. These fees may run as high as 30% of the money invested. If you were to earn 5% a year on the investment, it would take 8 years just to break even.

2. Ongoing advisory fees. These are monthly, quarterly, or annual fees paid to advisors for their investment advice and oversight. This includes working with you to pick the asset classes, set diversification, select a portfolio manager, optimize taxes, re-balance holdings and other periodic tasks.

These fees have many names including wrap fee or investment advisory fees. The normal “rule of thumb” is 1% of assets managed, although fees can range from 0 to 7%. Today, it can even be as low as .5%. It can be charged even if the advisor receives an upfront commission. It can be easy to see, or hidden in the fine print.

3. Additional service fees. Find out specifically what services are included financial advisory fees. Additional fees for financial planning or other services are rarely disclosed. They can range from minimal hand-holding focused on your investments to comprehensive financial planning.

4. Ongoing managerial expense ratio fees. These are incredibly well hidden that you may not see them in your statements or invoices. The only way to know is to read the prospectus or other third party analysis, like Morningstar.com. And, they can vary greatly for the same investment, depending on the class of share you buy.

For example, American Fund’s New Perspective Fund’s expense ratio ranges from 0.45% to 1.54%. The average expense ratio of a mutual fund that invests in stocks is 1.35%. Conversely, the average expense ratio of a Vanguard S&P 500 Fund is 0.10%. The difference of 1.25% is staggering over time.

5. Miscellaneous fees. Some advisors charge $50 – $100 a year per account to open or close an account, and even fees to dollar cost average your funds into the market.

6. Transaction fees. Every time you buy or sell a fund, a fee is typically paid to a custodian. These can range from $5 to hundreds of dollars per transaction.

7. Fee Only: Paid directly by clients for their services and can’t receive other sources of compensation, such as payments from fund providers. Act as a fiduciary, meaning they are obligated to put their clients’ interests first

8. Fee Based: Paid by clients but also via other sources, such as commissions from financial products that clients purchase. Brokers and dealers (or registered representatives) are simply required to sell products that are “suitable” for their clients.

A “suitable” investment is defined by FINRA as one that fits the level of risk that an investor is willing and able, as measured by personal financial circumstances, to take on. The Financial Industry Regulatory Authority is a private American corporation that acts as a Self Regulatory Organization (SRO) that regulates member stock brokerage firms and exchange markets. These criteria must be met. It is not enough to state that an investor has a risk-friendly investment profile. In addition, they must be in a financial position to take certain chances with their money. It is also necessary for them to

A hedge fund is a limited partnership of private investors whose money is managed by professional fund managers who use a wide range of strategies; including leveraging [debt] or trading of non-traditional assets [real-estate, collectible, commodities, cyrpto-currency, etc] to earn above-average returns. Hedge funds are considered a risky alternative investment and usually require a high minimum investment or net worth. This person is known as an “accredited investor” or “Regulation D” investor by the US Securities Exchange Commission and must have the following attributes:

A net worth, combined with spouse, of over $1 million, not including primary residence

An income of over $200,000 individually, or $300,000 with a spouse, in each of the past two years

Choose the fee structure. The fee structure should align with your needs. Consider the type of advice you seek, the number of times needed and the complexity of your financial situation. You can always negotiating tactics are free to ask for a better deal.

Compare fees. It is essential to research and compare different fees. Be sure to read the fine print for details or costs that are not a base fee.

Robo-advisors: For simple investment goals, with little specificity, robo-advisors may be a cost-effective option. They charge lower fees than conventional financial advisors and provide an automated, algorithmic approach to managing your investments.

Assessment

The average cost of working with a human financial advisor in 2024 was 0.5% to 2.0% of assets managed, $200 to $400 per hourly consultation, a flat fee of $1,000 to $3,000 for a one-time service, and/or a 3% to 6% commission fee on the product types sold.

When ruminating over financial advisory fees; read and understand the contract with disclosures, do not sign a confidentiality or non-disclosure agreement, and do not waive your right to a lawsuit. According to colleague Dr. Charles F. Fenton IIII JD, forced legal settlements almost always favor the advisor over the client.

2. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

3. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

SO – HOW MUCH IS A “FINANCIAL ADVISOR” REALLY WORTH?

This blog holds a rather uncomplimentary opinion of financial advisors, and the financial services and brokerage industry as a whole; deserved, or not? The entire site hints at this attitude as well, in favor of a going it alone or ME, Inc investing when possible. Nevertheless, it is reasonable to wonder how much boost in net-returns might an educated and informed, fee transparent and honest, fiduciary focused “financial advisor” add to a clients’ investment portfolio; all things being equal [ceteris paribus].

And, can it be quantified?

Well, according to Vanguard Brokerage Services®, perhaps as much as 3%? In a decade long paper from the Valley Forge, PA based mutual fund and ETF giant, Vanguard said financial advisors can generate returns through a framework focused on five wealth management principles:

• Being an effective behavioral coach: Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value added: up to 1.50%).

• Applying an asset location strategy: The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value added: from 0% to 0.75%).

• Employing cost-effective investments: This component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value added: up to 0.45%).

• Maintaining the proper allocation through rebalancing: Over time, as investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value added: up to 0.35%).

• Implementing a spending strategy: As the retiree population grows, an advisor can help clients make important decisions about how to spend from their portfolios. (Potential value added: up to 0.70%).

Source: Financial Advisor Magazine, page 20, April 2014.

Assessment

However, Vanguard notes that while it’s possible all of these principles could add up to 3% in net returns for clients, it’s more likely to be an intermittent number than an annual one because some of the best opportunities to add value happen during extreme market lows and highs when angst or giddiness [fear and greed] can cause investors to bail on their well-thought-out investment plans.

And, is the study applicable to doctors and allied healthcare providers? Doe Vanguard have a vested interest in the topic. What about fee based versus fee-only financial advice?

Conclusion

Finally, recognize the plethora of other financial planning life-cycle topics addressed in this ME-P were not included in the Vanguard investment portfolio-only study a decade ago.

And what about today with contemporaneous internet advising, chat-rooms, linkedin, robo-advisors, reddit and the like?

Posted on February 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dan Ariely PhD

THE IRRATIONAL ECONOMIST

***

***

Of course you don’t need a human financial advisor … until you do. Today, we’ve had unfettered internet access to a wide range of investments, opinions and models for at least two decades. So, why the bravado to go it alone; fifteen positive years for equities, since 2009! Yet, the DJIA, S&P 500 and NASDAQ just plunged and plummeted today!

The financial advisor’s role is to remove the human element and emotion from investing decisions for something as personal as your wealth. Emotion drives the retail investor to sell low (fear) and buy high (greed). This is the reason why the average equity returns for retail investors is less than half of the S&P 500’s returns.

No, of course you don’t need a human financial advisor … until you do.

Many physician investors who trade through online brokerage accounts assume they have a direct connection to the securities markets.

But, they don’t. When you press “enter,” your order is sent over the Internet to your broker – who in turn decides which market to send it to for execution. A similar process occurs when you call your broker to place a trade.

While trade execution is usually seamless and quick, it does take time. And prices can change quickly, especially in fast-moving markets. Because price quotes are only for a specific number of shares, MD investors may not always receive the price they saw on their screen or the price their broker quoted over the phone. By the time your order reaches the market, the price of the stock could be slightly – or very – different.

Note:No SEC regulations require a trade to be executed within a set period of time. But if firms advertise their speed of execution, they must not exaggerate or fail to tell investors about the possibility of significant delays.

Tip:To avoid buying or selling a stock at a price higher or lower than you wanted, place a limit order rather than a market order. A limit order is an order to buy or sell a security at a specific price. A buy limit order can only be executed at the limit price or lower, and a sell limit order can only be executed at the limit price or higher. When you place a market order, you can’t control the price at which your order will be filled.

Example: You want to buy the stock of a “hot” IPO that was initially offered at $9, but don’t want to end up paying more than $20 for the stock. Place a limit order to buy the stock at any price up to $20. By entering a limit order rather than a market order, you will not be caught buying the stock at $90 and then suffering immediate losses as the stock drops later in the day or the weeks ahead.

Caution: Your limit order may never be executed because the market price may quickly surpass your limit before your order can be filled. But by using a limit order you also protect yourself from buying the stock at too high a price.

Dr. Gary L. Bode was Chief Executive Officer of Comprehensive Practice Accounting, Inc., a firm specializing in providing tax solutions to medical professionals. Originally, he was a board certified podiatrist and managing partner of a multi-office medical practice for a decade before earning his Master of Science degree in Accounting from the University of North Carolina. He then served as Chief Financial Officer [CFO] for a private mental healthcare facility. Today, Dr. Bode is a nationally known Certified Public Accountant, financial author, educator, and speaker. Areas of expertise include producing customized managerial accounting reports, practice appraisals and valuations, restructurings, and innovative financial accounting as well as proactive tax positioning and tax return preparation for healthcare facilities. He has been quoted in Newsweek.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on March 15, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By a Computer [FIN-TECH]

[By Rick Kahkler CFP®]

If Ken Fisher is right, in the future you will be talking to a computer about your asset allocation and loving every minute of it.

Fisher has built Fisher Asset Management into the largest fee-only investment advisory firm in the US, with over $100 billion under management. Speaking at the Investment News Innovation Summit in New York City on April 17, 2019, he said, “We need to get machines talking to people in a way that is more human than human.”

If you view “talking to machines” mostly in terms of using four-letter words when your computer locks up, you might be skeptical.

Fisher explained there are six personality profiles that fit almost every investor. “When you (or a machine) knows what they are, then you deal with them according to their profile.” In Ken’s thinking, machines will be able to spot the profile and then, using an algorithm free of human error, interact with the customer in a manner superior to a human advisor. He sees this happening within the next ten years.

I asked him, “What happens to the human advisors when machines talk to your customers better than a human?” Ken replied, “I don’t know the answer to that question,” suggesting that people will need to gain new skills and move on to the next thing. “You can’t keep doing the same thing you were before or you will be out of luck.”

As shocking as this idea is to investment advisors, it’s not at all far-fetched. In an “Axios AM Deep Dive” article on April 6, 2019, Mike Allen quoted Axios Future Editor Steve LeVine as saying that Millennials (those born between 1981 and 1996) will be the first generation to fully face the new age of automation, which could wipe out jobs faster than the economy creates new ones.

Like most before them, many Millennials have taken entry level, minimum wage jobs. Allen suggests that, unlike prior generations, they may not find much of a ladder up from there. Part of that is because of the aftermath of the great recession and part is because technology and globalization have reduced middle-wage jobs.

The median income of younger Millennials is $21,000, according to the AXIOS article. Contrast that to the median wage of $84,000 for statisticians and financial analysts, both of which have high concentrations of older Millennials.

It’s those $84,000 a year jobs that Fisher thinks will be done better by machines. If this happens, it will disrupt the financial services industry in spectacular fashion.

Danielle Fava of TD Ameritrade didn’t agree that human investment advisors will become obsolete in ten years. She does see voice digital assistants making email obsolete. She also believes that artificial intelligence will “enhance the conversations advisors are having with their clients,” rather than replace the human advisor.

***

***

While staring my professional demise in the face in ten years, I drew solace from knowing I am nearing the end of my career. Another fact that should comfort some financial professionals is the difference between investment advisors and analysts (like those who work for Ken Fisher) and financial planners. Investment advising is relatively easy; that’s why a machine may be able to do it all in ten years. Also, investment advice comprises only a small fraction of what financial planners do. It will take a really, really smart machine to integrate all the complex aspects of someone’s financial picture into a sensible plan.

Assessment

So maybe ten years from now a machine will flawlessly figure out your asset allocation. But it may be another ten years before your financial planner is a machine, and maybe another 50 before a machine can do financial therapy.

Posted on October 16, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

“Increases in the shelter, food, and medical care indexes were the largest of many contributors to the monthly seasonally adjusted all items increase.”—Bureau of Labor Statistics’s Consumer Price Index Summary

According to Betterment, one of the world’s largest robo-advisors, whose consumer-facing investment offerings make virtually no use of machine learning. [Emerging Tech]

Posted on May 22, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

[By Staff Reporters]

The concept of a self-taught and student motivated, but automated outcomes driven classroom may seem like a nightmare scenario for those who are not comfortable with computers.

Now everyone can breathe a sigh of relief, because the Institute of Medical Business Advisors just launched an “automated” final examination review protocol that requires no programming skill whatsoever.

In fact, everything is designed to be very simple and easy to use. Once a student’s examination “blue-book” is received, computerized “robotic reviewers” correct student assignments and quarterly test answers. This automated examination model lets the robots correct tests and exams, while the students concentrate on guided self-learning.

According to Eugene Schmuckler PhD MBA MEd, Dean of the CERTIFIED MEDICAL PLANNER® professional designation and certification program,

“This option allows the modern adult-learner save both time and money as s/he progresses toward the ultimate goal of board certification as a CMP® mark holder.”

The trend is growing and iMBA, Inc., is leading the way.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

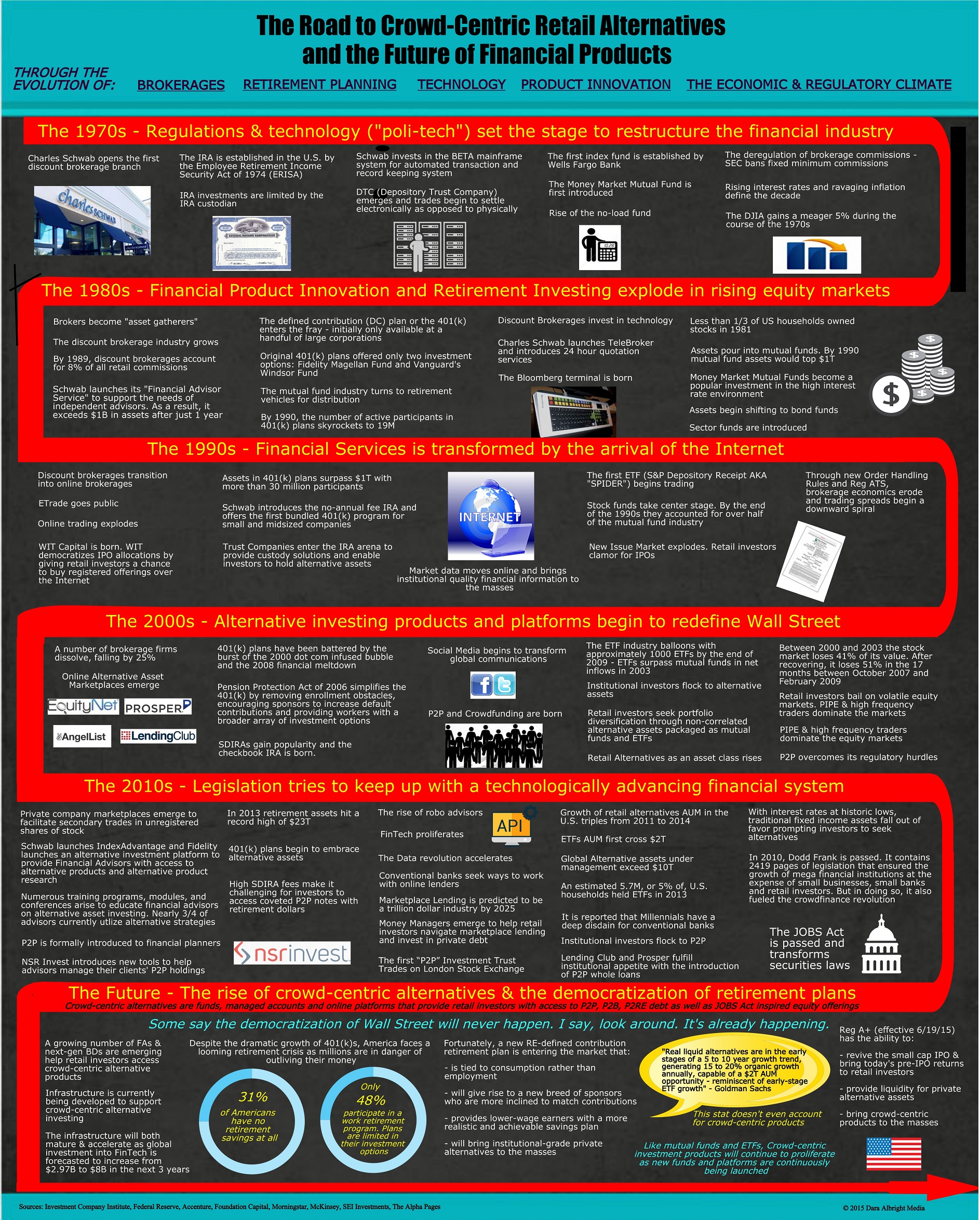

In simpler times, American workers relied on pensions to secure their retirement. Those who desired a supplement to their pension income opted to save during their pre-retirement years. Like television stations, investment options were primarily limited to three main providers. Instead of being bogged down with choices, savers essentially had their pick of placing money in interest bearing savings accounts, stocks or bonds. With the exception of occasionally having to get up from the sofa to change the television channel, life was pretty uncomplicated.

Then the 70s arrived – bringing a rash of polyester and laying the groundwork for sweeping changes throughout the financial system.

Ever since, our capital markets have been in a perpetual state of transformation fueled by innovations in brokerage services, advisory tools, investment products, retirement plans, financial technology and shifts in both the political as well as economic climate. The confluence of these evolutions – as depicted in the infographic below – continues to not only redefine retail investing, but America’s entire retirement framework.

During the past four and a half decades the brokerage business has moved online, slashed commissions and turned its commission-based securities salespeople into asset gatherers. As the number of brokerage firms steadily declined, online alternative asset marketplaces began to rise.

The IRA and 401(k) transformed America’s retirement structure as pension plans became less and less prevalent. These new retail retirement vehicles fed the mutual fund business, and in tandem both industries ballooned into multi trillion dollar markets.

Tools were developed that would enable financial advisors to navigate across a growing number of asset classes and help ensure the proper diversification of retail portfolios. These advisory resources also contributed to the proliferation of new asset classes and retirement accounts.

Legislative changes coupled with technological achievement led to the democratization of both financial products as well as market data. This “poli-tech” dynamic not only furthered the growth of conventional asset classes, it inspired a host of innovative online investing platforms, lending models, equity financing structures and the creation of new asset classes.

A groundswell of investment products

Over the years, a groundswell of investment products has been engineered for the mass market resulting in the flow of retail dollars across money markets, mutual funds and ETFs. Particularly during the recent years, as interest rates reached historic lows and equity markets became excessively volatile, there has been an upsurge of interest in uncorrelated alternative assets.

To meet the mounting demand, a wave of retail alternative products entered the market. According to McKinsey, retail alternatives will soon account for almost 50% of total retail revenues. Furthermore, Goldman Sachs believes that retail alternatives are in the early stages of a 5-10 year growth trend – reminiscent of early-stage ETF growth and capable of becoming a $2T AUM opportunity.

As financial advisors were becoming acquainted with a growing number of retail alternative products packaged through mutual funds and ETFs, a new niche of alternatives known as crowd-centric alternatives had been gaining popularity – particularly among institutional and internet savvy retail investors.

These crowd-centric alternatives – designed to bring non-correlated yield and pre-IPO equity growth to mainstream investors’ portfolios – are made up of public as well as private funds, managed accounts and online platforms that provide investors with access to peer-to-peer, peer-to-business and peer-to-real estate debt as well as JOBS Act inspired equity offerings.

While momentum continues to build for crowd-centric alternatives, an interesting phenomenon has been brewing in the retirement plan industry. Flaws in the current IRA and 401(k) structures as well as the social security system have legislators as well as economists scrambling to prevent a looming retirement crisis. Thus far, none of the publicly proposed solutions even begin to scratch the surface of the predicament. That is until now.

Fortunately, a soon-to-be-unveiled RE-defined contribution retirement plan will resolve inherent issues by 1) unleashing a new generation of plan sponsors more inclined to match contributions, 2) providing lower-wage earners with a more realistic and achievable savings plan, and by 3) bringing higher yielding institutional-grade alternatives to the masses. (A new white paper: “The RE-defined Contribution Plan: Powering Economic Growth While Preventing a National Retirement Crisis” will be released shortly)

Fascinatingly, the RE-defined contribution plan and crowd-centric alternative assets have the potential to power one another’s expansion in much the same way that the IRA, 401(k) and mutual fund industry fueled each other’s massive growth in prior decades.

***

***

Crowd-centric alternatives

While the existing statistics for retail alternatives are staggering, none of the forecasters have even accounted for crowd-centric alternatives. If history is any guide, crowd-centric alternatives are about to catapult the retail alternative industry to unforeseen heights – particularly given the following key factors:

The surfacing of a more proficient retirement vehicle that accommodates alternative investing;

The introduction of new tools designed to assist financial advisors in managing their client’s crowd-centric holdings;

A growing number of financial advisors and next-gen BDs emerging to help retail investors access crowd-centric alternative products;

The prolific growth of marketplace lending;

Traditional offline private debt businesses migrating online;

The influx of P2P, P2B, P2RE managed products;

The maturation of the infrastructure to support crowd-centric alternative investing;

Venture capital is pouring into fintech (projected to nearly triple in the next 3 years). This will enthuse innovation and lead to greater sophistication of products, platforms and infrastructure;

The implementation of additional key components of the JOBS Act will inspire the creation of new investment products for the masses as well as provide liquidity for private alternatives.

Assessment

Although I cannot promise that polyester and orange shag carpets won’t make a comeback, I can absolutely guarantee that financial services will continue to evolve through the progression of new ideas, products, tools and technology.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Health professionals are small business owners who need to apply their self-discipline tactics in establishing and operating successful practices. Talented trainees are leaving the medical profession because they fail to balance the cost of attendance against a realistic business and financial plan. Principles like budgeting, saving, and living below one’s means, in order to make future investments for future growth, asset protection, and retirement possible are often lacking. This textbook guides the medical professional in his/her financial planning life journey from start to finish. It ranks a place in all medical school libraries and on each of our bookshelves.

Dr. Thomas M. DeLauro DPM [Professor and Chairman – Division of Medical Sciences, New York College of Podiatric Medicine]

Posted on July 10, 2015 by Dr. David Edward Marcinko MBA MEd CMP™

What are your chances?

[By staff reporters]

In an increasingly digital world the workforce is becoming more automated than ever before. In this decade we’ve faced the challenge of interactive POS systems impacting the retail employment sector, but what industries are next?

Understanding the future of your job role can help you plan your career path more effectively, and decide if it’s time to change direction.

Using NPR’s handy calculator you can see just how safe your job is from the robots. To save you some time we’ve listed the top industries and their rankings

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 14, 2015 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David E. Marcinko MBA

If you have some eggs about to expire, or a car that has problems, you can turn to an online community to find some solutions. But, what if you have a financial issue, like what to do with a windfall or how to invest for a kids’ college tuition, and need help?

Ramirez finds that “for the armchair experts … weighing in on these questions pro bono is all in a day’s work. They are generally affable, seemingly trustworthy, and largely convincing.” But, one professor of personal finance sees a problem: “Six people suggest six different things to do—now what do I do?

Professor Speak

First of all, who are these people that are answering this plea? Are they professionals? Are they certified financial planners? Do they have any idea what they’re talking about?”

Others say the peer-review part of crowdsourced advice is its most valuable aspect.

“Compare this to a traditional financial advisor. If you’re in here asking about what to invest your retirement into, and I’m suggesting funds that personally enrich me, I’ll get called out on it.”

Left unsaid, but surely true, is how investors will increasingly turn to sites like this to validate their advisors’ advice, or learn why they should change advisors.

***

***

***

Assessment

First we had crowd sourced funding, then crowd sourced medicine … and now crowd sourced investing! Prudent, or NOT?

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on April 22, 2015 by Dr. David Edward Marcinko MBA MEd CMP™

Machines will Rule … Soonest?

[By Dr. David Edward Marcinko MBA CMP™]

Machines beat humans at chess. Machines can pilot airplanes to land at O’Hare; or on Mars. There is now a machine that beats the best of us at Jeopardy.

And, many predict that an Artificial Intelligent medical clinician is ten years away.

Just think tele-medicine and tele-health.

And, no one will use a biological doctor in twenty five years. Then, of course, enter the singularity*.

Innovation

I’m not sure who said it first, but this quote has been floating around Twitter lately:

“In 2015 Uber, the world’s largest taxi company owns no vehicles, Facebook the world’s most popular media owner creates no content, Alibaba, the most valuable retailer has no inventory, and Airbnb, the world’s largest accommodation provider owns no real estate.”

Assessment

Fundamental assumptions about what is needed to be a successful doctor, financial advisor, or other business has changed in just the last few years.

So – I ask MD and FA colleagues – will you keep up professionally, or fall behind? What are the ethical implications of these technology innovations; if any?

***

[Vanguard’s “Robo Advisor” – Good for Clients but Bad for Advisors?]

The technological singularity is the hypothesis that accelerating progress in technologies will cause a runaway effect wherein artificial intelligence will exceed human intellectual capacity and control, thus radically changing civilization in an event called “the singularity”.[1] Because the capabilities of such an intelligence may be impossible for a human to comprehend, the technological singularity is an occurrence beyond which events may become unpredictable, unfavorable, or even unfathomable.[2]

The first use of the term “singularity” in this context was by mathematician John von Neumann. In 1958, regarding a summary of a conversation with von Neumann, Stanislaw Ulam described “ever accelerating progress of technology and changes in the mode of human life, which gives the appearance of approaching some essential singularity in the history of the race beyond which human affairs, as we know them, could not continue”.[3] The term was popularized by science fiction writer Vernor Vinge, who argues that artificial intelligence, human biological enhancement, or brain–computer interfaces could be possible causes of the singularity.[4] Futurist Ray Kurzweil cited von Neumann’s use of the term in a foreword to von Neumann’s classic The Computer and the Brain.

Proponents of the singularity typically postulate an “intelligence explosion”,[5][6] where superintelligences design successive generations of increasingly powerful minds, that might occur very quickly and might not stop until the agent’s cognitive abilities greatly surpass that of any human.

Kurzweil predicts the singularity to occur around 2045[7] whereas Vinge predicts some time before 2030.[8] At the 2012 Singularity Summit, Stuart Armstrong did a study of artificial general intelligence (AGI) predictions by experts and found a wide range of predicted dates, with a median value of 2040. Discussing the level of uncertainty in AGI estimates, Armstrong said in 2012, “It’s not fully formalized, but my current 80% estimate is something like five to 100 years.”[9]

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

{kind=link}