![]()

Peeling Back the Layers of Fees

By PALADIN [Research & Registry]

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

- PRACTICES: www.BusinessofMedicalPractice.com

- HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

- CLINICS: http://www.crcpress.com/product/isbn/9781439879900

- ADVISORS: www.CertifiedMedicalPlanner.org

- FINANCE: Financial Planning for Physicians and Advisors

- INSURANCE: Risk Management and Insurance Strategies for Physicians and Advisors

- Dictionary of Health Economics and Finance

- Dictionary of Health Information Technology and Security

- Dictionary of Health Insurance and Managed Care

* 8

* 8

Share this:

Filed under: Financial Planning, Investing, Risk Management | Tagged: advisory fees, Investing Expenses, stock broker fees |

Posting Website Fees

Many financial planning websites mention fees, as required, but still remain opaque to potential clients because the advisor whishes to control the discussion and understandably wishes to avoid the website shopper phenomenon. But, s/he can still control the discussion, and still provide transparency, because posting up front pricing information doesn’t mean presenting information in a vacuum!

For example, a 1%/year fee doesn’t have to just be 1%; it can be 1%, compared to an industry average cost of X%, where the average cost of an actively managed mutual fund is Y%. Similarly, it doesn’t have to be a retainer fee of $1,000/year; it can be a retainer fee for less than the cost of a monthly cable bill! And, a financial plan doesn’t cost $2,500; it costs 15 hours of staff time to craft extensive, customized solutions; but saves the doctor-client so much more!

And, if services have a range of potential prices, they might be provided with some insight into the factors that impact the price. Modern young and internet savvy doctors expect this sort of information.

Anonymous

LikeLike

Compensation Issues

The focal point of most Financial Advisor, Planner and/or Insurance Agent disclosure is real or potential conflicts of interest, primarily compensation. There has been a torrential debate within the planning industry regarding which type of compensation is best. At times, the debate has gotten ugly within the industry.

Definitions are blurred, fluid and ill-defined; perhaps intentionally so. Those who receive some level of commission income have taken offense at the assertion made by some that they are somehow less ethical than fee-only advisors.

The fee-only crowd has been accused of being holier-than-thou zealots. All the while both sides of the debate seem to ignore the fact that how an advisor gets paid is completely irrelevant as to whether good advice is being rendered. It makes no more sense to pay a fee for bad advice than to pay a commission for bad advice.

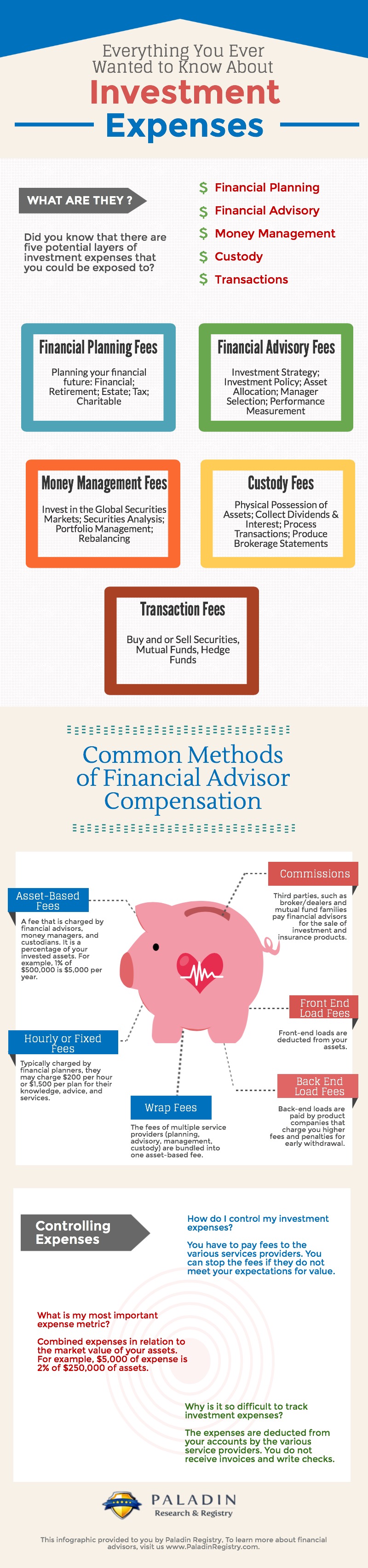

So how do financial planners get paid? Commissions; fees or both!

It is a complex issue best explained in this book.

Ann Miller RN MHA

LikeLiked by 1 person

On Commissions

Commission income has been a cornerstone of the insurance industry financial advice business for decades. The primary advantage of paying on a commission basis is that one is paying on an as needed basis. For instance, when a trade is executed, the commission is charged to facilitate the order. The rate paid will be higher than that charged strictly for execution and a portion of that additional charge goes to the advisor for helping decide whether to execute that trade. A commission is also usually higher for a financial product deemed less viable. Think variable annuities, reverse mortgages or whole life insurance. OR, in healthcare, think subsidies [commissions] for the purchase of electronic medical records [EMRs] or meaningful use [MU] requirements. If a large subsidy or aggressive salesman is needed; the product itself may be suspect.

One of the significant disadvantages of this approach is the focus on transactions. The advisor, working in this capacity as a commissioned stock broker, has the financial incentive to either encourage a client to trade or spend his time with a client that will. It is not uncommon for the best course of action to be no action. This compensation arrangement does not give the advisor the financial incentive to render that advice.

In addition to the transactional bias, a common issue that arises is the use of incentive commissions to generate sales of particular products. The traditional place for this occurrence is with the development of in-house or proprietary products. Most major brokerage firms develop their own mutual funds, or variable annuity products, for instance. As mentioned previously, most major firms are no longer directly compensating brokers for such sales but many continue to use the percentage of proprietary product in calculating bonuses. Further, much of the brokerage firm’s management compensation in the United States is directly linked to proprietary product. Rather than pressuring the broker directly through their paychecks, the management team is given the incentive to push in-house products.

The discount brokerage firms are not immune to the proprietary product push. Instead of proactively pushing their products they will put competing products at a disadvantage within their system. For instance, some on-line brokerages have their own version of an S&P Index fund. The in-house variety can be purchased without a transaction fee, whereas a competitor’s version requires a purchase fee. Despite admonitions to review the prospectus before investing, the on-line firm is betting that the investor will elect the proprietary fund to save the transaction fee even though it typically carries a higher management fee.

Incentive compensation is not the sole domain of proprietary products by any stretch. Most mutual fund companies pay roughly the same level of commission to brokerage funds but many will from time to time offer extra compensation to drive sales. This is common with funds that do not seem to attract much attention (and new investor money) usually due to poor performance.

Hope Rachel Hetico RN MHA CMP™

http://www.CertifiedMedicalPlanner.org

LikeLiked by 1 person

Fees and Commissions (Fee-based)

There is a large percentage of practitioners that use a combination of fees and commissions. Often the term fee-based is used. The varieties of fee-based arrangements are vast. Investment accounts may be managed on a fee-only basis, yet the FA or financial planner may receive a commission for placing an insurance policy. Here we have a fee-only service (investment) but a fee-based planner.

Confusing? It can be – but a good advisor will make clear disclosures to reduce confusion. Another common version is to charge a fee for the preparation of a financial plan with the implementation of the plan resulting in commissions.

Also, some states allow a fee-offset where a fee is determined and any implementation commissions are rebated to the client up to the fee. Excess commissions are retained by the advisor.

The most common ethical abuse of the term fee-only, however, manifests itself in the arena of investment management. A client pays an annual fee but is not made aware that some investments that may be purchased, usually mutual funds, will also pay 12b-1 fees (trail commissions) to the brokerage firm. Despite the commission, the arrangement is presented as fee-only. Anytime the advisor has an FINRA/NASD license, one should ask and be told what role 12b-1s will play in the relationship [get it in writing, too].

The ethical issue is not whether there are real or potential conflicts — there are. These conflicts can arise all by themselves. The ethical consideration is whether and how these issues are disclosed by the advisor and dealt with by both the client and the advisor.

Ultimately, it is the physician-client’s responsibility to determine whether a conflict is clouding the advisor’s recommendations.

Remember fee-based is not the same as fee-only.

Gary

LikeLike

FEES

This is a hot topic so please allow me to weigh in:

[a] Hourly rate

The hourly rate method [$100-250/hr] has a similar advantage to a commissioned approach, namely you only pay when you want to. This is an appropriate way to address a project need or to get a second opinion or spot check of a particular situation. It does not seem to foster good long-term relationships and few planners work exclusively on this basis. The obvious conflict arises from the incentive to take as much time as possible to do the work requested or to create work and the resulting billable hours. A more subtle issue is that this method of compensation may not promote good communications between planner and client. At times, a client may be hesitant to call with questions or requests for fear of a bill. Conversely, the advisor may be hesitant to bill for time spent for fear of aggravating a client.

More problematic is the reliance on the doctor-client to determine when work is needed. Here, the client engages the advisor when the client perceives the need. The client may not be the best person to determine a need exists. Typically, the client will feel compelled to hire an advisor when there is a problem. This diminishes a significant benefit to hiring help – preventing problems from occurring in the first place.

Often, a well-designed financial plan is ineffective due to poor execution or the outright failure to implement. Without an ongoing compensation arrangement, there is not necessarily an incentive to assure proper implementation of the advice rendered. In a way this is akin to the criticism of the commissioned approach. The advisor only has a financial incentive to spend his time on those that are ready to pay.

[b] Flat rate

The flat fee approach has many of the same advantages of the hourly method when applied to a project or second opinion situation. Again, however, ongoing attention is not in the cards. Annual retainers can address this flaw to a degree and ongoing service can be obtained.

There are two important downsides to this approach. First, is the opposite problem from that of hourly rates. With a flat fee, the incentive is to complete the work as quickly as possible and cut corners. The second downside comes into play with the delivery of investment management services. Here, performance has no bearing on the rewards to the advisor. It is this fact that has led to a percentage of assets as the most prevalent form of compensation in the planning community.

Sinclair

LikeLike

Annual percentage of assets Method

Sinclair – In theory, the percentage of assets method is the fairest when providing investment management services. Under this method the advisor retains a percentage of the assets managed. With all of the fee approaches it makes no difference which particular securities are selected, the compensation to the advisor is the same. The percentage method, however, changes this slightly in that the result of the selection does impact compensation. If the investments appreciate, the advisor gets a raise, if the values decline, the advisor gets a pay cut. Still h/she gets a percent on the original corpus for which s/he had no input. So this is not really; share the gain, share the pain, as postulated. While many believe this is a better alignment of advisor and client interests; others do not and consider it ridiculously expensive.

Financial advisors do love this model however, because it is like an annuity; cash keeps coming into the firm monthly which is good for cash flow; especially when provided by a TAMP. Moreover, the fees are automatically deduced from the client’s account; often in a less than fully transparent fashion. This business model is also valuated more than the traditional commission model which must earn the fee, on each and every transaction.

The most significant conflict arises from what to do with a particular sum of money. An advisor has an incentive to recommend that an inheritance be invested rather than applied to outstanding debts, pay off a home-mortgage, or to start a business, for instance. Only if the advisor manages the money does s/he get paid.

Example:

A medical professional considering the DIY approach (along with a proper education to do so with focused expert advice, prn) versus hiring an asset manager at the going rate (let’s say 1% a year), ought to think of the long-term cost of this decision. A 7% returns due to paying the adviser 1% a year vs 8% returns make a huge difference over an investing career.

For a doctor investing $100K a year for 30 years, the difference is $1.9M ($11.3M vs $9.4M). Some may suggest this $1.9 Million Dollar difference is awfully expensive handholding; even with quarterly meetings.

Bently

LikeLike

Percentage of Net-Worth Method

Basing the fee on net worth instead of assets managed, the retirement of debt for instance, does not alter the fee as much because the effect on net worth is substantially equal to putting the funds in an investment account. This method is not free of conflict and shares two issues with the percentage of assets.

Both methods work against the use of funds on a current basis. The more a household spends or gives to family or charity, the less there is to manage and the lower the net worth.

To a degree there is an incentive to be more aggressive in order to increase the value of an investment account or a household net worth. By being bold, a good result can increase the assets managed and the resulting fee income to the advisor.

This potential problem is mitigated to a point by the fact that being bold in the investment world does not always pay off. Stocks in particular do go down substantially from time to time. Such an event translates to a pay cut.

Creighton

LikeLike