By Staff Reporters

***

US stocks: Rebounded to close firmly higher Tuesday as investors shrugged off hawkish remarks from Federal Reserve Chair Jerome Powell and continued to monitor the war in Ukraine.

The S&P 500 rose 1.1% to 4,511.81, and Dow Jones Industrial Average [DJIA] jumped more than 250 points, or about 0.7%, to 34,807.86. The NASDAQ Composite was up nearly 2% to 14,108.82. The moves come on the back of a choppy session Monday that saw all three indexes cap last week’s winning streak to close lower after Powell signaled the central bank was prepared to act more aggressively to rein in inflation.

***

***

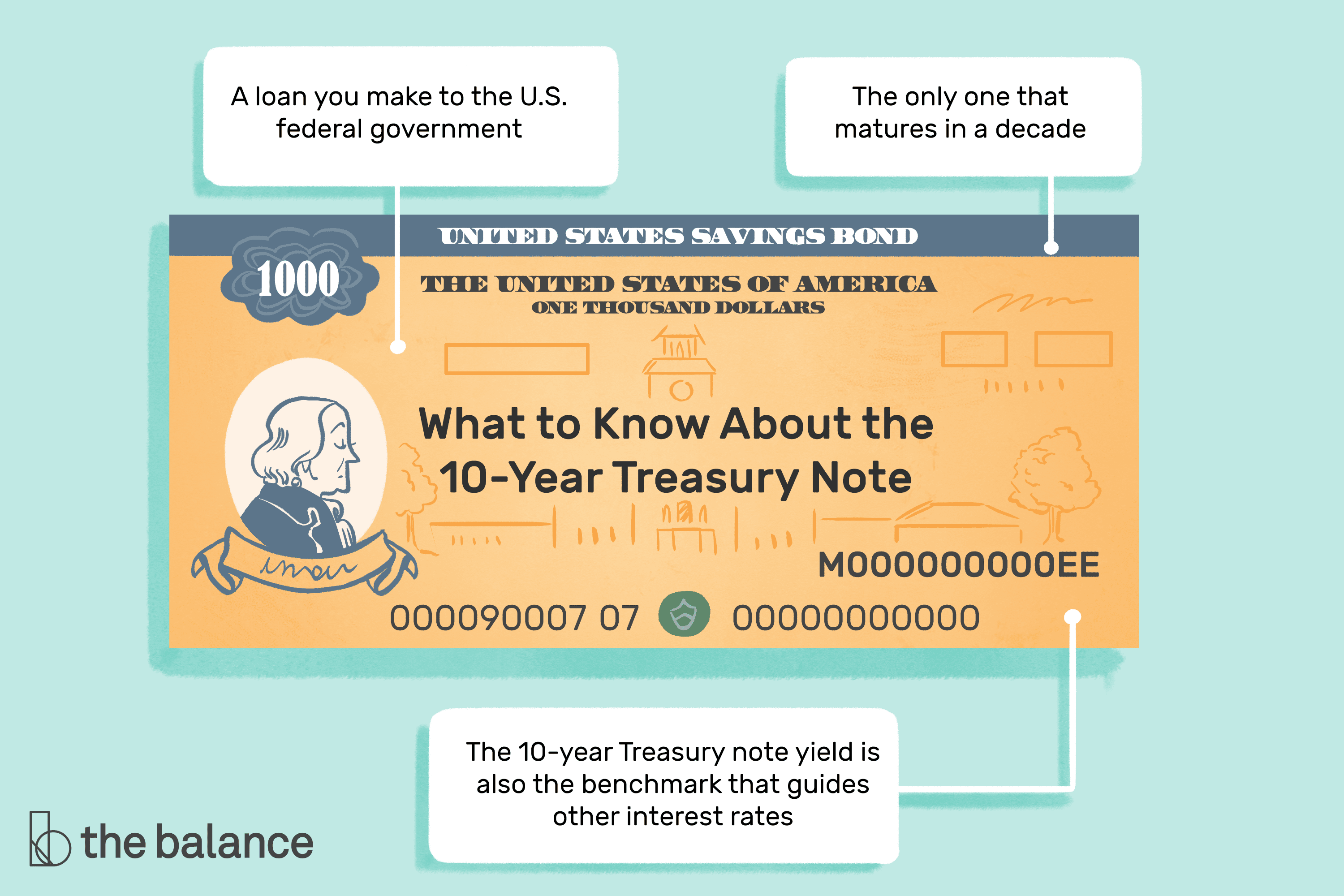

T-Note: Meanwhile, the 10-year U.S. Treasury climbed to yield 2.372%

***

COMMENTS APPRECIATED

Thank You

Subscribe to the Medical Executive-Post

***

***

Share this:

Filed under: Alerts Sign-Up, Investing | Tagged: 10 year treasury note, DJIA, Dow Jones Industrial Average, NASDAQ, T-Note | Leave a comment »