BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

New stock market indices are frequently created to track emerging sectors, regional markets, or particular investment strategies. However, some of the recent and notable stock market indices introduced in recent years focus on new trends or themes such as technology, sustainability, and ESG (Environmental, Social, and Governance) factors. Here are a few noteworthy examples:

1. S&P 500 ESG Index (2021)

One of the newer and increasingly popular indices is the S&P 500 ESG Index, launched in 2021. This index tracks the performance of the companies within the S&P 500 that meet certain environmental, social, and governance (ESG) criteria. The S&P 500 ESG Index aims to provide a more sustainable and socially responsible alternative to the traditional S&P 500 index. It excludes companies involved in industries like tobacco, firearms, or fossil fuels, reflecting the growing interest in socially responsible investing.

2. Nasdaq-100 ESG Index (2021)

Another significant ESG-focused index is the Nasdaq-100 ESG Index, also introduced in 2021. This index tracks the Nasdaq-100, which is typically made up of the 100 largest non-financial companies listed on the Nasdaq stock exchange, but it filters those companies to include only those with strong ESG scores. Given the rapid growth of ESG investing, indices like this one are becoming increasingly important for socially-conscious investors.

3. Global X Metaverse ETF Index (2022)

The Global X Metaverse ETF Index, introduced in 2022, is another example of a new market index targeting a specific, emerging sector. This index focuses on companies involved in the development of the metaverse, which encompasses technologies like virtual reality (VR), augmented reality (AR), and other digital experiences. As the concept of the metaverse gains popularity, this index is designed to provide investors with exposure to companies working within this new virtual space.

4. FTSE All-World High Dividend Yield ESG Index (2022)

This is an example of a more niche index, combining high-dividend yield investing with ESG factors. Introduced by FTSE Russell in 2022, this index is designed for investors looking for companies with high dividend yields while also considering sustainability and ethical investment criteria. It is part of a broader trend where investors seek to combine solid financial returns with socially responsible practices.

5. Bitcoin and Digital Assets Indices

As cryptocurrency continues to grow in prominence, more indices focused on digital assets and cryptocurrency have emerged. For instance, the S&P Bitcoin Index and the Nasdaq Crypto Index were created to provide benchmarks for the growing market of cryptocurrencies and blockchain technology companies. These indices help investors track the performance of digital currencies and crypto-related stocks or funds.

Why Are New Indices Created?

New stock market indices are created for several reasons:

Emerging Market Trends: As new sectors like the metaverse, AI, and ESG investing become more relevant, indices are developed to capture the performance of these new areas.

Investor Demand: As investors look for more targeted strategies, whether for ethical investing or to gain exposure to emerging technologies, indices are created to meet those demands.

Financial Innovation: As financial products like ETFs (Exchange-Traded Funds) gain popularity, they require benchmarks or indices to track performance.

Conclusion

While the S&P 500 ESG Index and Nasdaq-100 ESG Index are among the newest mainstream indices focusing on socially responsible investing, there are also many other niche indices targeting rapidly growing sectors like the metaverse, cryptocurrencies, and digital assets. These indices reflect the evolving nature of global markets and the increasing interest in themes such as sustainability and technological innovation. With such rapid change in the financial landscape, it’s likely that even more specialized indices will continue to emerge in the coming years.

Posted on November 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

The Financial Industry Regulatory Authority (FINRA) is a cornerstone of the U.S. financial system, serving as a self-regulatory organization that oversees brokerage firms and their registered representatives. Established in 2007 through the consolidation of the National Association of Securities Dealers (NASD) and the regulatory arm of the New York Stock Exchange, FINRA plays a critical role in maintaining market integrity, protecting investors, and ensuring that the securities industry operates fairly and transparently.

Origins and Mission

FINRA’s creation was driven by the need for a unified regulatory body that could streamline oversight of broker-dealers. Its mission is straightforward yet vital: to safeguard investors and promote market integrity. Unlike government agencies such as the Securities and Exchange Commission (SEC), FINRA is a non-governmental organization, but it operates under the SEC’s supervision. This unique structure allows FINRA to act with agility while still being accountable to federal oversight.

Core Responsibilities

FINRA’s responsibilities are broad and multifaceted.

Licensing and Registration: FINRA ensures that brokers and brokerage firms meet professional standards before they can operate. This includes administering qualification exams such as the Series 7 and Series 63.

Rulemaking and Enforcement: FINRA develops rules that govern broker-dealer conduct and enforces them through disciplinary actions when violations occur.

Market Surveillance: FINRA monitors trading activity across U.S. markets to detect fraud, manipulation, or other irregularities.

Investor Education: Through initiatives like BrokerCheck, FINRA provides investors with tools to research brokers and firms, empowering them to make informed decisions.

Each of these functions contributes to a safer and more transparent marketplace.

Protecting Investors

Investor protection lies at the heart of FINRA’s mission. By enforcing ethical standards and monitoring trading practices, FINRA reduces the risk of misconduct such as insider trading, excessive risk-taking, or misleading investment advice. Its arbitration and mediation services also provide investors with avenues to resolve disputes with brokers outside of lengthy court proceedings. This combination of proactive regulation and accessible dispute resolution strengthens public trust in financial markets.

Challenges and Criticisms

Like any regulatory body, FINRA faces challenges. Critics argue that as a self-regulatory organization, it may be too close to the industry it oversees, raising concerns about conflicts of interest. Others question whether its penalties are sufficient to deter misconduct. Additionally, the rapid evolution of financial technology, cryptocurrency markets, and complex trading algorithms presents new regulatory hurdles. FINRA must continually adapt its rules and surveillance systems to keep pace with innovation.

Impact on the Financial System

Despite these challenges, FINRA’s impact is undeniable. By maintaining standards of conduct and transparency, it helps ensure that capital markets remain efficient and trustworthy. Investors, from individuals saving for retirement to institutions managing billions, rely on FINRA’s oversight to protect their interests. Broker-dealers, meanwhile, benefit from clear rules that create a level playing field and reduce systemic risk.

Conclusion

In summary, FINRA is an essential pillar of the U.S. financial regulatory framework. Its blend of licensing, rulemaking, enforcement, and investor education fosters confidence in the securities industry. While it must continue to evolve in response to technological and market changes, its mission remains constant: protecting investors and promoting integrity. Without FINRA’s presence, the risk of misconduct and instability in financial markets would be far greater. As the financial landscape grows more complex, FINRA’s role will only become more critical in ensuring that markets remain fair, transparent, and resilient.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Role of Volatility Indices in Financial Markets

Volatility is often described as the pulse of financial markets, reflecting the collective emotions of investors as they respond to uncertainty, risk, and opportunity. Among the many tools designed to measure this phenomenon, the CBOE Volatility Index, or VIX, stands out as the most widely recognized. Dubbed the “fear gauge,” the VIX captures market expectations of near-term volatility in the S&P 500, derived from options pricing. Its movements often mirror investor sentiment: rising sharply during periods of crisis and falling when confidence returns. Yet, the VIX is not alone. A family of volatility indices exists across global markets, each offering unique insights into sector-specific or regional risk.

The importance of volatility indices lies in their ability to quantify uncertainty. Traditional measures such as historical volatility look backward, analyzing past price fluctuations. In contrast, indices like the VIX are forward-looking, reflecting implied volatility based on options markets. This distinction makes them invaluable for traders, portfolio managers, and policymakers. For example, a sudden spike in the VIX often signals heightened fear, prompting investors to hedge positions or reduce exposure to equities. Conversely, a low VIX suggests complacency, though it can also precede unexpected shocks.

Beyond the VIX, other indices provide complementary perspectives. The VXN tracks volatility in the Nasdaq-100, often dominated by technology stocks. Because the tech sector is highly sensitive to innovation cycles and regulatory changes, the VXN can diverge significantly from the VIX, highlighting sector-specific risks. Similarly, the RVX measures volatility in the Russell 2000, offering a window into small-cap stocks that are more vulnerable to domestic economic conditions. Internationally, indices such as the VSTOXX in Europe and India VIX extend this framework globally, allowing investors to compare risk sentiment across regions. Together, these indices form a mosaic of market psychology, enabling a more nuanced understanding of global financial stability.

Volatility indices also play a crucial role in risk management. Derivatives linked to these indices, such as futures and exchange-traded products, allow investors to hedge against sudden downturns. For instance, during the 2008 financial crisis, demand for VIX futures surged as investors sought protection from extreme market swings. More recently, volatility products have become popular among retail traders, though their complexity and tendency to lose value over time make them risky for long-term holding.

Critics argue that volatility indices can be misleading. A low VIX does not guarantee stability, and a high VIX does not always signal disaster. Moreover, the rise of volatility-linked products has occasionally amplified market stress, as seen during the “Volmageddon” event of February 2018, when inverse volatility ETFs collapsed. These episodes underscore the need for caution: volatility indices are powerful tools, but they must be used with a clear understanding of their limitations.

In conclusion, volatility indices such as the VIX serve as vital instruments for gauging investor sentiment and managing risk. They provide a forward-looking measure of uncertainty, complementing traditional metrics and offering insights across sectors and regions. While not infallible, their role in modern finance is undeniable.

For traders, analysts, and policymakers alike, these indices are more than numbers on a screen—they are reflections of the market’s collective psyche, guiding decisions in times of both calm and crisis.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The NASDAQ, short for the National Association of Securities Dealers Automated Quotations, is one of the largest and most influential stock exchanges in the world. Founded in 1971, it was the first electronic stock market, revolutionizing how securities were traded by replacing traditional floor-based systems with computerized trading platforms. This innovation made transactions faster, more transparent, and accessible to a broader range of investors.

Unlike the New York Stock Exchange (NYSE), which historically operated through physical trading floors, the NASDAQ is entirely virtual. It connects buyers and sellers through a sophisticated network of computers, allowing for rapid execution of trades. This digital-first approach has made it particularly attractive to technology companies and growth-oriented firms, earning it a reputation as the go-to exchange for innovative and high-tech businesses.

Companies Listed on the NASDAQ The NASDAQ is home to some of the most prominent and influential companies in the world. Giants like Apple, Microsoft, Amazon, Google (Alphabet), Meta (formerly Facebook), and Tesla all trade on the NASDAQ. These companies are part of the NASDAQ-100, an index that tracks the performance of the 100 largest non-financial companies listed on the exchange. The NASDAQ Composite Index, which includes over 3,000 stocks, provides a broader snapshot of the market’s overall health and direction.

How It Works The NASDAQ operates as a dealer’s market, meaning transactions are facilitated by market makers—firms that stand ready to buy or sell securities at publicly quoted prices. These market makers help maintain liquidity and ensure that trades can be executed efficiently. Prices are determined by supply and demand, and the electronic nature of the exchange allows for real-time updates and high-speed trading.

Significance in the Global Economy The NASDAQ plays a vital role in the global financial system. It provides companies with access to capital by allowing them to issue shares to the public, and it offers investors a platform to buy and sell those shares. The performance of the NASDAQ is often seen as a barometer for the health of the technology sector and, more broadly, the innovation economy. When the NASDAQ rises, it typically signals investor confidence in growth and future earnings; when it falls, it may reflect concerns about economic stability or company performance.

Global Reach and Influence Though based in the United States, the NASDAQ’s influence extends worldwide. Many international companies choose to list on the NASDAQ to gain exposure to U.S. investors and benefit from the prestige associated with being part of a leading global exchange. Its technological infrastructure and regulatory standards make it a model for other exchanges around the world.

In summary, the NASDAQ is more than just a stock exchange—it’s a symbol of innovation, speed, and global connectivity. Its pioneering approach to electronic trading has reshaped the financial landscape, and its roster of companies continues to drive technological progress and economic growth across the globe.

The October 2025 Stock Market Crash: A Perfect Storm of Geopolitics and Investor Panic

The weekend of October 10–12, 2025, marked one of the most dramatic downturns in global financial markets in recent memory. What began as a series of unsettling headlines quickly snowballed into a full-blown market crash, sending shockwaves through economies and portfolios worldwide. This event was not the result of a single catalyst but rather a convergence of geopolitical tensions, speculative excess, and investor psychology.

At the heart of the crisis was a sudden escalation in U.S.–China trade relations. President Donald Trump abruptly canceled a scheduled diplomatic meeting with Chinese President Xi Jinping and announced a sweeping 100% tariff on all Chinese imports. This move reignited fears of a prolonged trade war, reminiscent of the economic standoff that rattled markets in the late 2010s. Investors, already jittery from months of uncertainty, interpreted the announcement as a signal of deteriorating global cooperation and retaliatory economic measures to come.

The impact was immediate and severe. Major U.S. indices plummeted: the S&P 500 dropped 2.7%, the Nasdaq fell 3.6%, and the Dow Jones Industrial Average lost 1.9%. These declines marked the worst single-day performance since April and triggered automatic trading halts in several sectors. The selloff was not confined to the United States; European and Asian markets mirrored the panic, with steep losses across the board.

Compounding the crisis was a massive liquidation in the cryptocurrency market. As traditional assets tumbled, investors rushed to offload digital holdings, leading to the largest crypto wipeout in history. Trillions of dollars in value evaporated within hours, further destabilizing investor confidence and draining liquidity from the broader financial system.

Another underlying factor was growing concern over the valuation of artificial intelligence (AI) stocks. The International Monetary Fund (IMF) had recently issued a warning that the AI sector was exhibiting signs of a speculative bubble, drawing parallels to the dot-com era. With many AI companies trading at astronomical price-to-earnings ratios, the crash exposed the fragility of investor sentiment and the dangers of overexuberance in emerging technologies.

Perhaps most telling was the psychological shift among investors. The weekend saw widespread capitulation, with many choosing to exit the market entirely rather than weather further volatility. This behavior—marked by fear-driven decision-making and herd mentality—is often a hallmark of deeper financial crises. It underscores the importance of trust and stability in maintaining market equilibrium.

In conclusion, the October 2025 stock market crash was a multifaceted event driven by geopolitical shocks, speculative risk, and emotional contagion. It serves as a stark reminder of how interconnected and fragile global markets have become. As policymakers and investors assess the damage, the focus must shift toward restoring confidence, recalibrating risk, and ensuring that future growth is built on sustainable foundations rather than speculative fervor.

COMMENTS APPRECIATED

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Buying or selling stocks requires access to one of the major exchanges, such as the New York Stock Exchange (NYSE) or the National Association of Securities Dealers Automated Quotations (NASDAQ). To trade on these exchanges, you must be a member of the exchange or belong to a member firm. Member firms and many individuals who work for them are licensed as brokers or broker-dealers by the Financial Industry Regulatory Authority (FINRA).

And so, a stockbroker executes orders in the market on behalf of clients. A stockbroker may also be known as a registered representative or investment advisor. Most stockbrokers work for a brokerage firm and handle transactions for several individual and institutional customers. Stockbrokers are often paid on commission, although compensation methods vary by employer.

Remember: SBs work for their firm and not the client. Stock brokers are not fiduciaries.

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

The Dow Jones Industrial Average (DJIA), often referred to simply as “the Dow,” is one of the oldest and most well-known stock market indices in the world. It was created in 1896 by Charles Dow, the co-founder of The Wall Street Journal, and is designed to represent the performance of the broader U.S. stock market, specifically focusing on 30 large, publicly traded companies. These companies are considered leaders in their respective industries and serve as a barometer for the overall health of the U.S. economy.

The Composition of the DJIA

The DJIA includes 30 companies, which are selected by the editors of The Wall Street Journal based on various factors such as market influence, reputation, and the stability of the company. These companies represent a wide array of sectors, including technology, finance, healthcare, consumer goods, and energy. Notably, the companies chosen for the DJIA are not necessarily the largest companies in the U.S. by market capitalization, but rather those that are most indicative of the broader economy. Some of the prominent companies listed in the DJIA include names like Apple, Microsoft, Coca-Cola, and Johnson & Johnson.

However, the list of 30 companies is not static. Over time, companies may be added or removed to reflect changes in the economic landscape. For example, if a company experiences significant decline or no longer represents a leading sector, it might be replaced with another company that better reflects modern economic trends. This periodic reshuffling ensures that the DJIA continues to be a relevant measure of economic activity.

How the DJIA is Calculated

The DJIA is a price-weighted index, which means that the value of the index is determined by the share price of the component companies, rather than their market capitalization. To calculate the DJIA, the sum of the stock prices of all 30 companies is divided by a special divisor. This divisor adjusts for stock splits, dividends, and other corporate actions to maintain the integrity of the index over time. The price-weighted method means that higher-priced stocks have a greater impact on the movement of the index, regardless of the overall size or economic weight of the company.

For instance, if a company with a higher stock price like Apple experiences a significant change in value, it will influence the DJIA more than a company with a lower stock price, even if the latter has a larger market capitalization. This makes the DJIA somewhat different from other indices, like the S&P 500, which is weighted by market cap and gives more weight to larger companies in terms of their economic impact.

Significance of the DJIA

The DJIA is widely regarded as a barometer of the U.S. stock market’s performance. Investors and analysts closely monitor the movements of the Dow to gauge the overall health of the economy. When the DJIA rises, it generally suggests that investors are optimistic about the economic outlook and that large companies are performing well. Conversely, when the DJIA falls, it often signals economic uncertainty or a downturn in market conditions.

Despite being a narrow index, with only 30 companies, the DJIA holds substantial sway in financial markets. It is widely covered in the media and is often cited in discussions about the state of the economy. In fact, the performance of the DJIA is considered a key indicator of investor sentiment and economic confidence.

However, the DJIA has its limitations. Since it only includes 30 companies, it does not necessarily represent the broader market or capture the performance of smaller companies. Other indices, like the S&P 500, which includes 500 companies, offer a more comprehensive view of the market’s performance.

Conclusion

The Dow Jones Industrial Average is a key metric for understanding the state of the U.S. economy and the stock market. Although it has evolved over the years, it continues to provide valuable insights into the performance of large, influential companies. While it is not a perfect reflection of the market as a whole, the DJIA remains one of the most important and widely recognized indices in global finance. Through its historical significance and its role in shaping market sentiment, the Dow has cemented its place as a cornerstone of financial analysis.

Posted on October 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: The S&P 500 hit its seventh record close in a row today, its longest win streak since May. The NASDAQ was buoyed by big tech, while the DJIA fell.

Commodities: Oil climbed thanks to a decision by OPEC+ to boost crude production at a more modest rate than experts expected. Gold continued its record run, rising above $3,900 for the first time ever, while bitcoin hovered just below a new all-time high.

Japan and France: Japanese stocks rose after the country elected its first female prime minister, and French stocks dropped after its prime minister quit less than a month into the job.

Stocks: The Russell 2000 went 967 days without hitting a new record high until Thursday. But, it looks like it will have to keep waiting for the next one—the small-cap-focused index fell, even as the DJIA, NASDAQ and S&P 500 rose to new closing highs on Friday.* Bonds: 2-year yields and 10-year yields both hit two-week intra-day highs even after the FOMC cut interest rates, indicating that traders still aren’t sure how the economy will perform in the months ahead. Commodities: Arabica futures fell on reports that lawmakers will introduce a bipartisan bill to exempt coffee from tariffs.

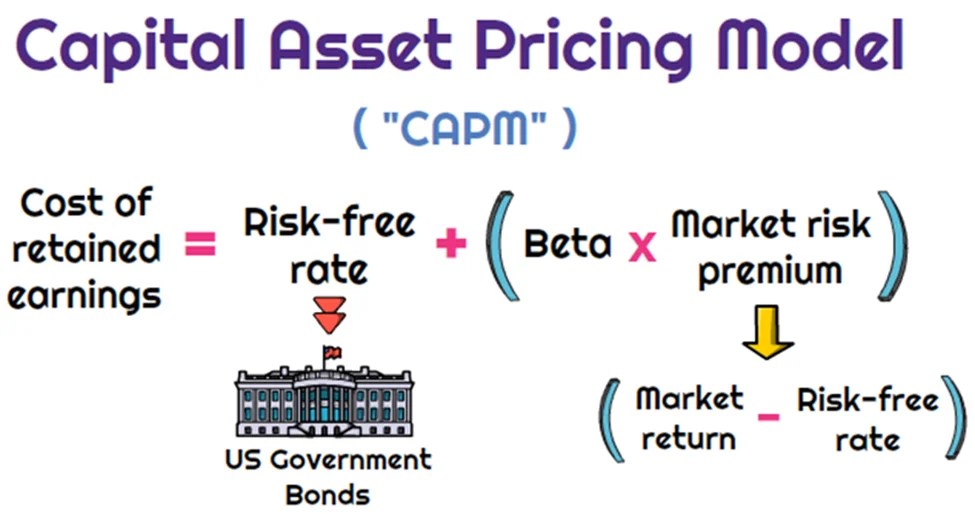

Dr. Harry Markowitz is credited with developing the framework for constructing investment portfolios based on the risk-return tradeoff. William Sharpe, John Lintner, and Jan Mossin are credited with developing the Capital Asset Pricing Model (CAPM).

CAPM is an economic model based upon the idea that there is a single portfolio representing all investments (i.e., the market portfolio) at the point of the optimal portfolio on the Capital Market Line (CML) and a single source of systematic risk, beta, to that market portfolio. The resulting conclusion is that there should be a “fair” return investors should expect to receive given the level of risk (beta) they are willing to assume.

The excess return, or return above the risk-free rate, that may be expected from an asset is equal to the risk-free return plus the excess return of the market portfolio times the sensitivity of the asset’s excess return to the market portfolio excess return. Beta, then, is a measure of the sensitivity of an asset’s returns to the market as a whole. A particular security’s beta depends on the volatility of the individual security’s returns relative to the volatility of the market’s returns, as well as the correlation between the security’s returns and the markets returns.

While a stock may have significantly greater volatility than the market, if that stock’s returns are not highly correlated with the returns of the overall market (i.e., the stock’s returns are independent of the overall market’s returns), then the stock’s beta would be relatively low. A beta in excess of 1.0 implies that the security is more exposed to systematic risk than the overall market portfolio, and likewise, a beta of less 1.0 means that the security has less exposure to systematic risk than the overall market.

MPT has helped focus investors on two extremely critical elements of investing that are central to successful investment strategies.

First, MPT offers the first framework for investors to build a diversified portfolio. Furthermore, an important conclusion that can be drawn from MPT is that diversification does in fact help reduce portfolio risk.

Thus, MPT approaches are generally consistent with the first investment rule of thumb, “understand and diversify risk to the extent possible.”

Additionally, the risk/return tradeoff (i.e., higher returns are generally consistent with higher risk) central to MPT based strategies has helped investors recognize that if it looks too good to be true, it probably is.

Passive Investing

Passive investing is a monetary plan in which an investor invests in accordance with a pre-determined strategy that doesn’t necessitate any forecasting of the economy or an individual company’s prospects. The primary premise is to minimize investing fees and to avoid the unpleasant consequences of failing to correctly predict the future. The most accepted method to invest passively is to mimic the performance of a particular index. Investors typically do this today by purchasing one or more ‘index funds’. By tracking an index, an investor will achieve solid diversification with low expenses.

An ivestor could potentially earn a higher rate of return than an investor paying higher management fees. Passive management is most widespread in the stock markets. But with the explosion of exchange traded funds on the major exchanges, index investing has become more popular in other categories of investing. There are now literally hundreds of different index funds.

Passive management is based upon the Efficient Market Hypothesis theory. The Efficient Market Hypothesis (EMH) states that securities are fairly priced based on information regarding their underlying cash flows and that investors should not anticipate to consistently out-perform the market over the long-term.

The Efficient Market Hypothesis evolved in the 1960s from the Ph.D. dissertation of Eugene Fama. Fama persuasively made the case that in an active market that includes many well-informed and intelligent investors, securities will be appropriately priced and reflect all available information. If a market is efficient, no information or analysis can be expected to result in out-performance of an appropriate benchmark. There are three distinct forms of EMH that vary by the type of information that is reflected in a security’s price:

Weak Form

This form holds that investors will not be able to use historical data to earn superior returns on a consistent basis. In other words, the financial markets price securities in a manner that fully reflects all information contained in past prices.

Semi-Strong Form

This form asserts that security prices fully reflect all publicly available information. Therefore, investors cannot consistently earn above normal returns based solely on publicly available information, such as earnings, dividend, and sales data.

Strong Form

This form states that the financial markets price securities such that, all information (public and non-public) is fully reflected in the securities price; investors should not expect to earn superior returns on a consistent basis, no matter what insight or research they may bring to the table.

While a rich literature has been established regarding whether EMH actually applies in any of its three forms in real world markets, probably the most difficult evidence to overcome for backers of EMH is the existence of a vibrant money management and mutual fund industry charging value-added fees for their services.

The notion of passive management is counterintuitive to many investors. Passive investing proponents follow the strong market theory of EMH. These proponents argue several points including;

In the long term, the average investor will have a typical before-costs performance equal to the market average. Therefore the standard investor will gain more from reducing investment costs than from attempting to beat the market over time.

The efficient-market hypothesis argues that equilibrium market prices fully reflect all existing market information. Even in the case where some of the market information is not currently reflected in the price level, EMH indicates that an individual investor still cannot make use of that information. It is widely interpreted by many academics that to try and systematically “beat the market” through active management is a fools game.

Not everyone believes in the efficient market. Numerous researchers over the previous decades have found stock market anomalies that indicate a contradiction with the hypothesis. The search for anomalies is effectively the hunt for market patterns that can be utilized to outperform passive strategies. Such stock market anomalies that have been proven to go against the findings of the EMH theory include;

Low Price to Book Effect

January Effect

The Size Effect

Insider Transaction Effect

The Value Line Effect

All the above anomalies have been proven over time to outperform the market. For example, the first anomaly listed above is the Low Price to Book Effect. The first and most discussed study on the performance of low price to book value stocks was by Dr. Eugene Fama and Dr. Kenneth R. French. The study covered the time period from 1963-1990 and included nearly all the stocks on the NYSE, AMEX and NASDAQ. The stocks were divided into ten subgroups by book/market and were re-ranked annually. In the study, Fama and French found that the lowest book/market stocks outperformed the highest book/market stocks by a substantial margin (21.4 percent vs. 8 percent). Remarkably, as they examined each upward decile, performance for that decile was below that of the higher book value decile. Fama and French also ordered the deciles by beta (measure of systematic risk) and found that the stocks with the lowest book value also had the lowest risk.

Today, most researchers now deem that “value” represents a hazard feature that investors are compensated for over time. The theory being that value stocks trading at very low price book ratios are inherently risky, thus investors are simply compensated with higher returns in exchange for taking the risk of investing in these value stocks. The Fama and French research has been confirmed through several additional studies. In a Forbes Magazine 5/6/96 column titled “Ben Graham was right–again,” author David Dreman published his data from the largest 1500 stocks on Compustat for the 25 years ending 1994. He found that the lowest 20 percent of price/book stocks appreciably outperformed the market.

One item a medical professional should be aware of is the strong paradox of the efficient market theory. If each investor believes the stock market were efficient, then all investors would give up analyzing and forecasting. All investors would then accept passive management and invest in index funds. But if this were to happen, the market would no longer be efficient because no one would be scrutinizing the markets. In actuality, the efficient market hypothesis actually depends on active investors attempting to outperform the market through diligent research.

The case for passive investing and in favor of the EMH is that a preponderance of active managers do actually underperform the markets over time. The latest study by Standard and Poor’s (S&P) confirms this fact. S&P recently compared the performance of actively-managed mutual funds to passive market indexes twice per year. The 2012 S&P study indicated that indexes were once again outperforming actively-managed funds in nearly every asset class, style and fund category. The lone exception in the 2012 report was international equity, where active outperformed the index that S&P chose. The study examined one-year, three-year and five-year time periods. Within the U.S. equity space, active equity managers in all the categories failed to outperform the corresponding benchmarks in the past five year period. More than 65 percent of the large-cap active managers lagged behind the S&P 500 stock index. More than 81 percent of mid-cap mutual funds were outperformed by the S&P MidCap 400 index.

Lastly, 77 percent of the small-cap mutual funds were outperformed by the S&P SmallCap 600 index. U.S. bond active managers fared no better that equity managers over a five year period. More than 83 percent of general municipal mutual funds under-performed the S&P National AMT-Free Municipal Bond index, 93 percent of government long-term funds under-performed the Barclays Long Government index, nearly 95 percent of high yield corporate bond funds under-performed the Barclays High Yield index. Although the performance measurements for index investing are very strong, many analysts find three negative elements of passive investing;

Downside Protection: When the stock market collapses like in 2008, an index investor will assume the same loss as the market. In the case of 2008, the S&P 500 stock index fell by more than 50 percent, offering index investors no downside protection.

Portfolio Control: An index investor has no control over the holdings in the fund. In the event that a certain sector becomes over-owned (i.e. technology stocks in 2000), an index investor maintains the same weight as the index.

Average Returns: An index investor will never have the opportunity to outperform the market, but will always follow. Although the markets are very efficient, an investor can perhaps take advantage of market anomalies and invest with those managers who have maintained a long-term performance edge over the respective index.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Stocks: The NASDAQ rose to its fifth record high of the week, while the S&P 500 and the Dow sank late in the day as investors turned their attention to the FOMC meeting next week.

Bonds: While equities climbed all week long, the bond market has been sending signals that weak economic data really isn’t great news.

Commodities: Oil rallied after President Trump expressed his growing frustration with Vladimir Putin and threatened further energy and financial sanctions. Meanwhile, the US may ask its G7 counterparts to apply 100% tariffs against China and India for purchasing Russian crude.

Posted on September 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Stocks: Markets slowed along yesterday with the S&P 500 and NASDAQ buoyed after a pivotal antitrust ruling for Alphabet pushed big tech stocks higher across the board.

Bonds: The 30-year Treasury pushed 5% yesterday as traders fret about the Fed’s independence and the odds of interest rate cuts.

Commodities: Oil sank on reports that OPEC+ is contemplating increasing its crude output next month, while gold reached yet another new record high as uncertainty swirling around the future of tariffs continued to rise. JPMorgan analysts now think the precious metal could climb as high as $4,250 by the end of next year.

Posted on August 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Technology: Fears of an A.I. bubble continue to climb after MIT published a report that 95% of companies using generative A.I. programs have nothing to show for it, despite pouring billions of dollars into this space.

Stocks: Another day of technology stocks selling off pulled the S&P 500 and NASDAQ lower yesterday, with investors rotating out of some of the hottest names and sectors in the market.

FOMC Drama: President Trump demanded the resignation of Fed Governor Lisa Cook for allegations of mortgage fraud. Meanwhile, the minutes from the July FOMC meeting revealed a growing divide between central bankers.

Posted on August 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: The Dow climbed thanks to UnitedHealth and Warren Buffett while the rest of the market sank as the stock rally slowed. But, despite Friday’s decline, both the S&P 500 and NASDAQ wrapped up winning weeks.

Bonds: Both 10-year and 2-year Treasury yields continued to climb after Thursday’s PPI reading and Friday’s consumer confidence and retail sales data.

Commodities: All eyes were on Anchorage, Alaska as President Trump concluded talks with President Putin—discussions that will be crucial for crude’s future.

There’s an aspect to retirement that many physicians do not plan for … the transition from work and practice to retirement. Your work has been an important part of your life. That’s why the emotional adjustments of retirement may be some of the most difficult ones.

For example, what would you like to do in retirement? Your retirement vision will be unique to you. You are retiring to something not from something that you envisioned. When you have more time, you would like to do more traveling, play golf or visit more often, family and friends. Would you relocate closer to your kids? Learn a new art or take a new class? Fund your grandchildren’s education? Do you have philanthropic goals? Perhaps you would like to help your church, school or favorite charity? If your net worth is above certain limits, it would be wise to take a serious look at these goals. With proper planning, there might be some tax benefits too. Then you have to figure how much each goal is going to cost you.

If you have a list of retirement goals, you need to prioritize which goal is most important. You can rate them on a scale of 1 to 10; 10 being the most important. Then, you can differentiate between wants and needs. Needs are things that are absolutely necessary for you to retire; while wants are things that still allow retirement but would just be nice to have.

Recent studies indicate there are three phases in retirement, each with a different spending pattern [Richard Greenberg CFP®, Gardena CA, personal communication]. The three phases are:

The Early Retirement Years. There is a pent-up demand to take advantage of all the free time retirement affords. You can travel to exotic places, buy an RV and explore forty-nine states, go on month-long sailing vacations. It’s possible during these years that after-tax expenses increase during these initial years, especially if the mortgage hasn’t been paid off yet. Usually the early years last about ten years until most retirees are in their 70’s.

Middle Years. People decide to slow down on the exploration. This is when people start simplifying their life. They may sell their house and downsize to a condo or townhouse. They may relocate to an area they discovered during their travels, or to an area close to family and friends, to an area with a warm climate or to an area with low or no state taxes. People also do their most important estate planning during these years. They are concerned about leaving a legacy, taking care of their children and grandchildren and fulfilling charitable intent. This a time when people spend more time in the local area. They may start taking extension or college classes. They spend more time volunteering at various non-profits and helping out older and less healthy retirees. People often spend less during these years. This period starts when a retiree is in his or her mid to late 70’s and can last up to 20 years, usually to mid to late-80’s.

Late Years. This is when you may need assistance in our daily activities. You may receive care at home, in a nursing home or an assisted care facility. Most of the care options are very expensive. It’s possible that these years might be more expensive than your pre-retirement expenses. This is especially true if both spouses need some sort of assisted care. This period usually starts when the retiree is their 80’s; however they can sometimes start in the middle to the late 70’s.

***

***

[A] Planning issues – early career

Most retirement lifestyle issues do not have to be addressed at this point. Keeping a healthy, balanced lifestyle will help to ensure a more productive retirement. This is the time to focus on the financial aspects of retirement planning.

[B] Planning issues – mid career

If early retirement is a major objective, start thinking about activities that will fill up your time during retirement. Maintaining your health is more critical, since your health habits at this time will often dictate how healthy you will be in retirement

[C] Planning issues – late career

Three to five years before you retire, start making the transition from work to retirement.

Try out different hobbies;

Find activities that will give you a purpose in retirement;

Establish friendships outside of the office or hospital;

Discuss retirement plans with your spouse.

If you plan to relocate to a new place, it is important to rent a place in that area and stay for few months and see if you like it. Making a drastic change like relocating and then finding you don’t like the new town or state might be very costly mistake. The key is to gradually make the transition.

For physicians, like most folks, retirement is the stage in life when one chooses to leave the workforce and live off sources of income or savings that do not require active work. The age at which a person retires, their lifestyle during retirement, and the way they fund that lifestyle, will vary from one person to the next, depending on individual preferences and financial planning. Usually it is age 65.

Some doctors may opt for early retirement to enjoy their hobbies and travel, while others may continue working part-time to stay engaged and supplement their income. Effective retirement planning often involves a combination of savings, investments, and possibly pension benefits to ensure a comfortable and secure post-work life.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stocks: Investors cheered the news of an EU & US trade deal over the weekend, pushing the S&P 500 above 6,400 for the first time ever. But the index gave up most of its gains late in the day as attention turned to a huge week of data ahead (more on that in a minute).

Trade: Today was the first day of discussions between US and Chinese negotiators in Stockholm to keep the trade war truce alive. Elsewhere, President Trump foresees a baseline 15% to 20% tariff rate for the rest of the world.

Commodities: Gold fell as trade deal hopes heightened investors’ risk appetite, while oil spiked higher after Trump gave Russia a 10- to 12-day deadline to sign a truce with Ukraine.

According to Bloomberg, 83% of the S&P 500 companies that have reported earnings have outpaced Wall Street’s estimates, putting the index on pace for its best season of beats since the second quarter of 2021.

Posted on July 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

UnitedHealth confirmed it’s being investigated. The healthcare giant said in a securities filing that it’s cooperating with the Justice Department in civil and criminal investigations following recent reports from the Wall Street Journal that the DOJ was looking into the company’s Medicare billing practices. WSJ reported that UnitedHealth had added unnecessary diagnoses to Medicare patients’ records that increased payments. It’s the latest setback for a company that ousted its CEO in May after its stock price cratered.

Tesla arrested its latest decline and gained 3.52% on the news that it will roll out its new robotaxi program in San Francisco as soon as this weekend.

Deckers Outdoor, the maker of Hoka and Ugg shoes, soared 11.35% on the back of stronger-than-expected earnings thanks to impressive international sales.

Newmont climbed 6.89% after a quarter of surging gold prices helped propel the miner’s earnings to new heights.

Managed care provider Centene added 6.09% despite marked declines in its Medicaid and Medicare membership, as well as soaring costs.

BostonBeer rose 6.54% as shareholders raised a toast to management’s effort to keep tariff costs low.

What’s down

Intel fell 8.53% on the news that it’s cutting costs by laying off 15% of its workforce and scaling back its chip foundry plans.

Puma plummeted 15.67% after the European footwear company warned of the high cost of tariffs.

Charter Communications plunged 18.49% in its worst day of trading ever after reporting that it lost 117,000 broadband subscribers last quarter. It was so bad that other cable stocks like Comcast sank 4.78% and Altice lost 9.46%.

Lyft announced it’s rolling out new autonomous shuttles, but shares still fell 0.56% as shareholders realized it’s just trying to keep up with Uber.

Posted on July 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: President Trump said there’s a “50/50 chance” of a deal with the EU ahead of next week’s deadline. Investors decided they like those odds, and pushed the NASDAQ and S&P 500 to yet another new closing record high—in fact, the S&P 500 set a new record every day this week. Meanwhile, trade deal talks with Brazil have reportedly stalled.

Commodities: Oil fell to a three-week low today as Iran signaled a willingness to come to the negotiating table with European powers for nuclear talks.

Hopes of trade deals and less need for a safe haven investment pushed gold prices lower.

Posted on July 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stat: $3+ million. That’s how much Medicare and Medicare Advantage drug plans have been ordered to pay for “inappropriately delaying or denying” services in the first four months of this year—more than the past four years combined, one analysis finds. (Healthcare Dive)

BloomEnergy popped 22.95% on the news that it made a deal with Oracle to provide the tech company’s AI data centers with power.

Enterprise software maker ServiceNow jumped 4.16% on management’s promise of more AI growth ahead.

West Pharmaceutical Services soared 22.78% on the news that demand for GLP-1 products remains strong.

What’s down

IBM dropped 7.62% despite beating analysts expectations on the top and bottom lines last quarter. Shareholders didn’t like to hear management warn of slowing software sales.

UnitedHealth Group fell 4.76% on reports that the health insurer is cooperating with the DOJ’s investigation into its Medicare billing practices.

Tough day for airlines: AmericanAirlines sank 9.62% after lowering its forward guidance, and SouthwestAirlines lost 11.16% after missing analyst earnings estimates.

Luxury goods maker LVMH sank 3.66% after sales fell 4% last quarter as the high-fashion industry gets hit with tariff turmoil.

UnionPacific fell 4.43% after it confirmed it’s in talks to acquire smaller rival NorfolkSouthern, which also lost 0.81%.

HoneywellInternational beat-and-raised earnings last quarter, but the stock still stumbled 6.18% lower.

Stocks: Investors were pleased to hear about the trade deal with Japan yesterday and reports of an agreement with the EU coming soon kept the stock rally alive through market close. The S&P 500 notched its 12th new closing record this year, and the NASDAQ ended the day above 21,000 for the first time.

Bonds: Treasury yields rose a bit after an auction of 20-year notes was met with strong demand, indicating investor appetite for longer-term US debt.

Commodities: Oil inched higher while gold edged lower as investors hedge their bets in anticipation of more trade deals before the August 1st deadline.

Stocks: The multi-day rally wavered this afternoon as investors turned their attention to big tech earnings tomorrow. The S&P 500 closed at a record high, while the NASDAQ finally broke its hot streak.

FOMC: Treasury Secretary Scott Bessent sees no reason for Jerome Powell to step down, while President Trump tempered his outrage against the Fed chair. Instead, well-known economist Mohamed El-Erian took up the gauntlet.

Trade: Bessent said China may get an extension to make a true trade deal, while promising a “rash of trade deals” in the coming days. Speaking of, Trump declared the US has made a deal with the Philippines capping import levies at 19%.

Posted on July 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets lost steam late in the trading session yesterday as investors awaited more earnings announcements, with the DJIA tumbling into the red. But the S&P 500 managed to end the day above 6,300 for the first time ever, while the NASDAQ enjoyed its sixth consecutive record close

FOMC: Over the weekend,President Trump disputed reports that Treasury Secretary Scott Bessent talked him out of firing Jerome Powell. Meanwhile, Bessent said that the entire Federal Reserve should be put under review.

Trade: Commerce Secretary Howard Lutnick reiterated that August 1st will be the “hard deadline” for countries to make a deal with the US. Both negotiations and tensions with the EU are ramping up as Trump threatens to slap the bloc with 30% levies.

Posted on July 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

“Crypto Week” got back on track after House GOP lawmakers convinced the holdouts in their party to help advance a series of crypto-friendly bills.

Crypto: Although bitcoin fell after the president signed the GENIUS Act into law, ether rose to its highest price in six months today, while enthusiasm for the new legislation pushed total crypto assets above $4 trillion.

Talen Energy soared 24.48% on the news that the independent energy producer is acquiring two new power plants.

InteractiveBrokers surged 7.77% after the broker increased the number of customer accounts by 32% last quarter as traders played market volatility.

Speaking of trading, CharlesSchwab gained 2.87% after opening more than 1 million new brokerage accounts last quarter gave it a 23% boost in trading revenue.

Burberry popped 4.42% thanks to a turnaround in the luxury goods maker’s business, including a 4% increase in American sales last quarter.

Quantumscape continued to climb yet again, rising another 7.65% as investors pour money into the battery maker.

Invesco jumped 15.28% on reports that the asset manager is asking shareholders of its popular QQQ fund to let it revamp its fund structure to increase fee revenue.

Crypto companies continued to have a great week as key legislation passed its final barrier in Congress. Coinbase climbed 2.2%, RobinhoodMarkets rose 4.07%, and GalaxyDigital gained 4.19%.

What’s down stocks

Netflix fell 5.1% after the streaming giant reported a strong quarter but warned that its operating margin will take a hit in the second half of the year.

Sarepta Therapeutics plunged 35.94% after the biotech reported a third patient death during its Phase 1 study of its new gene therapy.

AmericanExpress sank 2.35% despite a strong quarter of spending among cardholders that helped the credit card company notch record quarterly revenue.

Markets: Stocks slid lower today even as a preliminary survey revealed that consumer sentiment hit its highest point since February, while inflation expectations fell to pre-tariff levels. The selloff deepened on reports that President Trump wants 15% to 20% tariffs against the EU, though the NASDAQ managed to eke out a win.

Crypto: Although bitcoin fell after the president signed the GENIUS Act into law, ether rose to its highest price in six months today, while enthusiasm for the new legislation pushed total crypto assets above $4 trillion.

Posted on July 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Lucid exploded 36.24% higher on the news that the EV maker is partnering with Uber to roll out the ridesharing company’s new robotaxis.

PepsiCo popped 7.45% thanks to a strong quarter for the snack and soda giant, while shareholders cheered the details of its turnaround plan.

UnitedAirlines may have missed Wall Street’s revenue forecast, but its profits were enough to impress investors. Shares rose 3.11%.

Reports that Union Pacific is thinking about acquiring a rival sent shares of fellow train operators CSX and NorfolkSouthern up 3.73% and 3.65%, respectively.

Sarepta Therapeutics soared 19.53% after the biotech announced it will lay off 500 employees and restructure its entire business.

Quantumscape continued its hot streak, rising yet another 19.82% thanks to its recent battery breakthrough.

Speaking of hot streaks, OpenDoorTechnologies rose another 10.74% as retail traders pour into what is quickly becoming the next big meme stock.

Stocks down

GE Aerospace crushed earnings expectations and raised its fiscal guidance, but it still wasn’t enough to impress investors, who pushed shares of the engine maker down 2.10%.

USBancorp sank 1.03% after revenue and net interest income missed forecasts last quarter.

AbbottLaboratories beat on both top and bottom line guidance, but still fell 8.53% after the pharma company narrowed its fiscal forecasts.

President Trump is expected to sign an executive order in the coming days designed to help make private-market investments more available to U.S. retirement plans, according to people familiar with the matter. The order would instruct the Labor Department and the Securities and Exchange Commission to provide guidance to employers and plan administrators on including investments like private assets in 401(k) plans.

Stocks: Markets started the day on a high note thanks to a fifth straight decline in weekly initial jobless claims and surprisingly strong monthly retail sales. The NASDAQ hit its 10th record closing high of 2025 and the S&P 500 hit its ninth high.

Commodities: Lithium prices popped around the globe after the Chinese government ordered domestic producer Zangge Mining to halt operations. Plus, the US is reportedly set to impose 93.5% tariffs on Chinese imports of graphite, a key component.

Posted on July 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

US measles cases have reached a 33-year high. A little more than halfway into 2025, the US has reported 1,288 measles cases, marking the highest yearly total since 1992, according to data from the Centers for Disease Control and Prevention.

VC powerhouse and diehard Tolkien fan Peter Thiel revealed he’s taken a 9% stake in bitcoin miner BitMine Immersion Technologies. Shares popped 12.11%, while fellow miners that have also recently invested in ether soared in tandem: SharpLinkGaming added 29.03%, and BitDigital gained 19.45%.

In fact, most crypto stocks had a good day thanks to renewed optimism that Crypto Week isn’t over in Congress. MicroStrategy climbed 3.07% and MARAHoldings jumped 3.62%.

Johnson & Johnson rose 6.19% after the consumer goods giant reported impressive earnings last quarter and raised its forward guidance.

BrightHouseFinancial popped 6.23% on reports that the insurer may be bought by private equity firm Aquarian Holdings.

Tesla gained 3.50% after the EV maker revealed the new six-seat Model Y it will begin selling in China this fall.

What’s down

ASML dropped 8.33% after the chipmaker warned that growth might be completely flat next year.

Ford fell 2.85% on the news that the automaker is recalling nearly 700,000 crossover SUVs due to fuel leaks.

GrabAGun Digital Holdings, the online gun seller backed by Donald Trump, Jr., made its market debut today. Investor reception was scathing, and the stock slid 24.19%.

Though Medicaid cuts in the Trump administration’s budget bill shocked hospitals, providers may start singing its praises after learning they’re due for a pay bump next year. On Monday, the Centers for Medicare and Medicaid Services (CMS) shared its proposed 2026 physician fee schedule, which determines Medicare payments based on the amount of resources in provider services like office visits, hospice, diagnostic testing, ambulance care, and more.

Posted on July 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The consumer price index, a broad-based measure of goods and services costs, increased 0.3% on the month, putting the 12-month inflation rate at 2.7%, the Bureau of Labor Statistics reported Tuesday. The numbers were right in line with the Dow Jones consensus. Excluding volatile food and energy prices, core inflation picked up 0.2% on the month, with the annual rate moving to 2.9%, also matching the respective estimates.

The Trump administration has launched a probe into drone imports. Drones use polysilicon, a key ingredient for solar panels, and tariffs on the material could help boost profitability for domestic manufacturers like FirstSolar, which rose 6.90%.

National Fuel Gas rose 5.65% after the energy company caught a rare double upgrade from Bank of America analysts, who like the energy company’s improved productivity.

Stocks down

BlackRock fell 5.86% after the world’s largest asset manager reported that a single client pulled $52 billion last quarter.

It wasn’t a great day for other big banks: WellsFargo sank 5.43% after cutting its 2025 net interest income guidance, while JPMorgan Chase lost 0.74% despite beating sales and profit estimates.

Albertsons tumbled 5.02% even though the grocer reported a solid quarter thanks to strong pharmacy sales and digital revenue.

Newmont dropped 5.71% on the news that CFO Karyn Ovelmen is leaving the gold miner.

Posted on July 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Drug and medical device companies paid at least $13.2 billion to medical professionals in 2024, according to CMS data released June 30th. There’s been steady growth in these payments over the last few years, which include everything from research payments to free meals to promotional or conference fees. Drug and medical device companies paid out $13.1 billion in 2023, $13.1 in 2022, and $12.6 in 2021. If you’re a medical provider, you’ve probably gotten one of those perks from a drug or medical device company and thought it wouldn’t affect your decision-making.

But research suggests physicians are more likely to prescribe drugs from companies that pay them, with some studies specifically associating this with drugs that are costlier to patients. “Really well-trained people who affirm an oath to do no harm can be influenced, and are,” Neil Jay Sehgal, associate professor of health systems and population health at the University of Washington School of Public Health, told Healthcare Brew.

Bitcoin is booming, and crypto stocks climbed along with it. MicroStrategy rose 3.86%, RobinhoodMarkets added 1.67%. and Coinbase gained 1.80%.

Boeing rose 1.64% on preliminary reports that investigators have found no evidence of malfunction in the plane that crashed in India last month. Engine-maker GEAerospace also gained 2.71%.

Warner Bros Discovery climbed 2.39% thanks to a strong opening weekend for the new Superman movie.

Autodesk popped 5.05% on the news that it is not pursuing an acquisition of rival software maker PTC. PTC fell 1.25%.

Kenvue, the company behind Band Aids and Listerine, gained 2.18% after kicking its CEO to the curb.

PayPal climbed 3.55% despite the news that JPMorgan will start charging the fintech fees for access to customer data.

Stocks Down

Starbucks sank 1.60% on news that employees will have to return to the office four days a week. Shareholders were also unimpressed with the coffee giant’s new secret menu.

Synopsys stumbled 1.74% after getting regulatory approval from Chinese authorities to acquire software designer Ansys for $35 billion. Ansys rose 3.03% on the news.

Waters plunged 13.81% on the news that it will merge with Becton Dickinson’s bioscience and diagnostic solutions business in a $17.5 billion deal.

RivianAutomotive lost 2.15% thanks to a downgrade from Guggenheim analysts, who forecast soft sales for the automaker’s latest models.

Posted on July 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets shrugged off President Trump’s weekend threat of 30% levies against the EU and Mexico, as well as his proposed 100% secondary tariffs against Russia today. Stocks eked out a win across the board, with the NASDAQ climbing to a new record close.

Commodities: Oil prices fell while gold took a breather, but the big winner was orange juice futures, which hit a four-month high thanks to Trump’s promise of 50% tariffs on all imports from Brazil. Coffee prices also climbed.

Stocks: The major Wall Street stock indexes languished. The S&P pulled back from its record high to close the week just a bit lower, but the NASDAQ managed to post a gain across the week.

Crypto: Bitcoin hit a new high-water mark above $118,000. Next week, July 14th, Congress hosts “Crypto Week” to discuss regulating the industry in a growth-oriented manner.

Commodities: Silver rose to its highest level since 2011, and it’s been even hotter than gold. The metal is up ~27% this year. Oil, meanwhile, ticked higher on speculation that President Trump will place more sanctions on Russia early next week.

Posted on July 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

CVS has threatened to close 23 pharmacies in Arkansas after the state passed a law banning companies that own pharmacy benefit managers (PBMs) from also operating pharmacies starting in 2026.

Kraft Heinz jumped 2.53% following a WSJ report it was preparing to break itself up (but not back to Kraft and Heinz).

Companies in the drone sector rose after the Pentagon introduced measures to supercharge production and deployment. Red Cat rose 26.40%, AeroVironment 11.04%, and Kratos Defense & Security Solutions 11.76%.

Performance Food Group jumped 4.84% to a record after reportedly being eyed by US Foods Holding for a takeover. A combined company would become the top foodservice distributor in the US with combined sales of ~$100 billion.

AMC Entertainment popped 11% on an upgrade from Wedbush. It’s tired of IMAX hogging the Brew Markets spotlight…

What’s down stocks

Delta (-0.23%) and United (-4.34%) took a breather after their big celebration on Thursday post-Delta earnings.

Penn Entertainment got hit 7.62% when gaming revenue for Iowa and Indiana came in soft.

Sunrun’s up-and-down week ended…down, with the solar stock falling 7%.

Posted on July 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

US measles cases have reached a 33-year high. A little more than halfway into 2025, the US has reported 1,288 measles cases, marking the highest yearly total since 1992, according to data from the Centers for Disease Control and Prevention.

Cereal legend WK Kellogg popped 30.57% after chocolate giant Ferrero agreed to acquire it for north of $3 billion.

Tesla (+4.73%) continued to rebound from its plunge on Monday. Elon Musk said that Tesla’s robotaxi service would expand into the Bay Area “probably in a month or two” and that his AI chatbot Grok is coming to Tesla vehicles by next week.

Estée Lauder gained 6.32% after Bank of America slapped a buy rating on the stock, implying a 27% upside from Wednesday’s closing price.

ProKidney continued its remarkable rally, rising another 19.35%, after the biotech announced positive trial results for its diabetes treatment. It’s gone from a penny stock to a $1.55 billion market cap in the past four days.

Copper companies Freeport-McMoRan (+3.51%) and Southern Copper (+2.34%) gained thanks to Trump’s announcement that copper tariffs would begin on August 1.

Stocks down

Biotech partners Ultragenyx (-25.11%) and Mereo BioPharma Group (-42.52%) plunged after issuing a disappointing update on their trial of a treatment for a rare genetic bone condition.

Vertiv, the maker of liquid cooling equipment,declined 5.96% when Amazon said it was rolling out a new liquid cooling system for its AI servers.

Hydro Flask owner Helen of Troy tumbled 22.71% after reporting a $450 million loss in its fiscal first quarter. CEO Brian Grass said “tariff-related impacts” were its Achilles heel.

Autodesk fell 6.89% after Bloomberg reported on Wednesday it was weighing a takeover of rival engineering software company PTC.

Posted on July 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Hims & Hers Health gained 4.62% after announcing it will sell generic semaglutide in Canada when Novo Nordisk’s patent for Ozempic and Wegovy expires in January.

Merck shareholders applauded its move to buy respiratory drugmaker Verona Pharma for $10 billion, sending its stock up 2.88%.

Rhythm Pharmaceuticals popped 36.63% thanks to a promising new trial for its oral obesity treatment.

AES, a renewable power company that counts Microsoft among its clients, jumped 19.87% after Bloomberg reported it was considering a sale.

Fashion names Ralph Lauren (+2.10%) and Coach owner Tapestry (+3.31%) hit record highs.

Stocks down

WPP cut its guidance and watched its stock fall 18.11% as a result. The ad giant is dealing with a laundry list of challenges, from AI disrupting the industry to clients spending less to finding a new CEO.

Medical device maker RxSight plunged 37.84% after slashing its full-year revenue forecast.

T-Mobile ticked 1.55% lower after getting a downgrade from KeyBanc, which said its weakness in fiber internet would prevent it from catching up to rival AT&T.

Mobileye, which makes self-driving tech and was spun out of Intel, fell 7.08% when Intel said it was selling 45 million shares.

Posted on July 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.