MEDICAL EXECUTIVE-POST – TODAY’S NEWSLETTER BRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

http://www.MedicalBusinessAdvisors.com

SPONSORED BY: Marcinko & Associates, Inc.

***

http://www.MarcinkoAssociates.com

| Daily Update Provided By Staff Reporters Since 2007. How May We Serve You? |

| © Copyright Institute of Medical Business Advisors, Inc. All rights reserved. 2025 |

REFER A COLLEAGUE: MarcinkoAdvisors@outlook.com

SPONSORSHIPS AVAILABLE: https://medicalexecutivepost.com/sponsors/

ADVERTISE ON THE ME-P: https://tinyurl.com/ytb5955z

Your Referral Count -0-

***

CITE: https://www.r2library.com/Resource

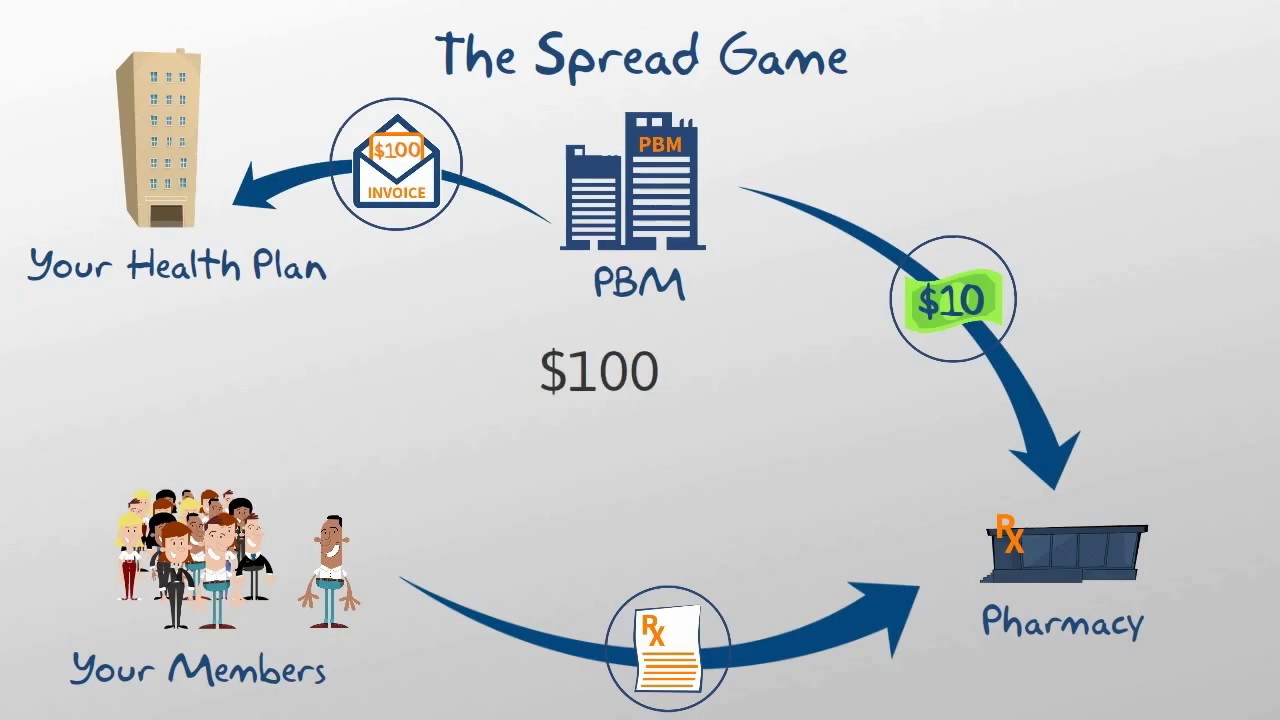

CVS has threatened to close 23 pharmacies in Arkansas after the state passed a law banning companies that own pharmacy benefit managers (PBMs) from also operating pharmacies starting in 2026.

CITE: https://tinyurl.com/2h47urt5

What’s up stocks

- Kraft Heinz jumped 2.53% following a WSJ report it was preparing to break itself up (but not back to Kraft and Heinz).

- Companies in the drone sector rose after the Pentagon introduced measures to supercharge production and deployment. Red Cat rose 26.40%, AeroVironment 11.04%, and Kratos Defense & Security Solutions 11.76%.

- Performance Food Group jumped 4.84% to a record after reportedly being eyed by US Foods Holding for a takeover. A combined company would become the top foodservice distributor in the US with combined sales of ~$100 billion.

- AMC Entertainment popped 11% on an upgrade from Wedbush. It’s tired of IMAX hogging the Brew Markets spotlight…

What’s down stocks

- Delta (-0.23%) and United (-4.34%) took a breather after their big celebration on Thursday post-Delta earnings.

- Penn Entertainment got hit 7.62% when gaming revenue for Iowa and Indiana came in soft.

- Sunrun’s up-and-down week ended…down, with the solar stock falling 7%.

CITE: https://tinyurl.com/tj8smmes

Stat: $10 billion. That’s how much Merck is paying to buy UK-based biopharmaceutical Verona Pharma. (CNBC)

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

COMMENTS APPRECIATED

PLEASE SUBSCRIBE: MarcinkoAdvisors@outlook.com

Thank You

***

***

***

***

EDUCATIONAL TEXTBOOKS: https://tinyurl.com/4zdxuuwf

***

Share this:

Filed under: Drugs and Pharma, Ethics, Information Technology, Investing, Marcinko Associates, Recommended Books, Sponsors | Tagged: CVs, DJIA, DOW, Marcinko, Merck, NASDAQ, PBMs, S&P 500, textbooks, VIX | Leave a comment »