Dr. David Edward Marcinko; MBA MEd

SPONSOR: http://www.MarcinkoAssociates.com

***

***

A physician‑focused financial plan is a specialized approach to personal financial management designed to address the unique challenges, opportunities, and career patterns that medical professionals experience. While the core principles of financial planning—budgeting, saving, investing, and risk management—apply to everyone, physicians face circumstances that make a generic plan insufficient. Long training periods, delayed earnings, high student debt, demanding work schedules, and complex compensation structures all shape the financial lives of doctors. A physician‑focused financial plan recognizes these realities and provides a tailored roadmap that supports both long‑term stability and personal well‑being.

One of the defining features of a physician’s financial journey is the delayed start to earning a full income. Most physicians spend more than a decade in education and training, often accumulating significant student loan debt while earning modest resident salaries. A physician‑focused financial plan begins by acknowledging this imbalance between early‑career income and debt. It helps physicians understand repayment options, prioritize high‑interest loans, and choose strategies that align with their career goals and lifestyle. This early planning is essential because the decisions made during residency can influence financial outcomes for decades.

Another key element of a physician‑focused financial plan is managing the transition from training to practice. This period often brings a dramatic increase in income, but it also introduces new financial responsibilities. Physicians may face relocation costs, licensing fees, malpractice insurance, and the need to establish emergency savings. Without a structured plan, the sudden jump in earnings can lead to lifestyle inflation—spending that rises as quickly as income. A tailored financial plan helps physicians create intentional habits, allocate new income wisely, and build a foundation for long‑term wealth rather than short‑term consumption.

Compensation structures in medicine also require specialized planning. Many physicians receive income from multiple sources, such as base salaries, bonuses, call pay, or production‑based incentives. Some work as employees, while others operate as independent contractors or partners in a practice. Each arrangement carries different tax implications, retirement plan options, and insurance needs. A physician‑focused financial plan helps navigate these complexities by clarifying how income is taxed, identifying opportunities for tax‑advantaged savings, and ensuring that physicians take full advantage of employer‑sponsored benefits or self‑employed retirement plans.

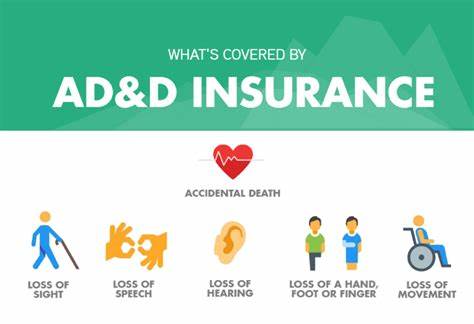

Risk management is another area where physicians have distinct needs. Because their income is often high and their work can be physically and emotionally demanding, protecting their earning potential is critical. Disability insurance, for example, is especially important for physicians, as an injury or illness could prevent them from practicing in their specialty. A physician‑focused financial plan evaluates the appropriate level of coverage, the importance of “own‑occupation” definitions, and the role of supplemental policies. Life insurance, malpractice coverage, and asset protection strategies also play a central role in safeguarding a physician’s financial future.

***

***

Investing is a major component of any financial plan, but physicians often face unique considerations. Their late start in earning means they have fewer years to build retirement savings, making efficient investing essential. A physician‑focused plan helps determine appropriate asset allocation, risk tolerance, and long‑term strategies that account for the physician’s career stage and goals. It also addresses common pitfalls, such as overly conservative investing due to fear of market volatility or overly aggressive investing to “catch up.” The goal is to create a balanced, disciplined approach that supports sustainable growth.

Tax planning is another area where physicians benefit from specialized guidance. High incomes can push physicians into top tax brackets, making tax‑efficient strategies especially valuable. A physician‑focused financial plan explores opportunities such as maximizing retirement contributions, using health savings accounts, evaluating charitable giving strategies, and considering the tax implications of practice ownership. Thoughtful tax planning can significantly increase long‑term wealth by reducing unnecessary liabilities.

Work‑life balance and burnout are also important considerations in a physician‑focused financial plan. Physicians often work long hours and face intense pressure, which can influence financial decisions. A well‑designed plan supports not only financial goals but also personal well‑being. It helps physicians align their spending with their values, plan for meaningful time off, and create financial flexibility that allows for career changes, reduced hours, or early retirement if desired. In this way, the plan becomes a tool for enhancing quality of life, not just accumulating wealth.

Estate planning is another essential component. Physicians often accumulate significant assets over their careers, and a tailored plan ensures that these assets are protected and distributed according to their wishes. This includes creating wills, establishing trusts, designating beneficiaries, and planning for potential estate taxes. These steps provide peace of mind and protect loved ones from unnecessary complications.

Ultimately, a physician‑focused financial plan is a comprehensive, personalized strategy that addresses the financial realities of a medical career. It integrates debt management, income planning, risk protection, investing, taxes, and long‑term goals into a cohesive framework. More importantly, it recognizes that physicians are not just high‑earning professionals—they are individuals with demanding careers, personal aspirations, and unique financial pressures. By providing clarity, structure, and confidence, a physician‑focused financial plan empowers doctors to build secure, fulfilling lives both inside and outside the exam room.

COMMENTS APPRECIATED

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR- http://www.MarcinkoAssociates.com

Like, Refer and Subscribe

***

***

Share this:

Filed under: "Ask-an-Advisor", "Doctors Only", Accounting, economics, finance, Financial Planning, iMBA, Inc., Insurance Matters, Investing, Marcinko Associates, Taxation | Tagged: david marcinko | Leave a comment »