BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A. I.

***

***

A trio of scientists — two of them American and one Japanese — have won the Nobel Prize in Medicine for their discoveries concerning peripheral immune tolerance, a mechanism by which the body helps prevent itself from attacking its own tissues instead of foreign invaders.

Mary E. Brunkow, Fred Ramsdell and Shimon Sakaguchi will share the prize for discoveries that “launched the field of peripheral tolerance, spurring the development of medical treatments for cancer and autoimmune diseases,” the Nobel Assembly said in a news release. The trio will now share the prize money of 11 million Swedish kronor (nearly $1.2 million).

Posted on October 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

UNITED STATES GOVERNMENT SHUTS DOWN

***

By Health Capital Consultants, LLC

***

***

With hours to go until the midnight deadline on September 30th, 2025 to fund the government, lawmakers appear deadlocked over whether certain healthcare provisions should be included in the temporary funding bill.

Should this deadlock continue, the federal government will shut down beginning today October 1st and remain shut down until that deadlock is resolved.

This Health Capital Topics article provides an update on the developing saga. (Read more…)

Posted on September 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Dear Medical Executive-Post Readers and Subscribers

***

HISTORY OF LABOR DAY

The first Labor Day holiday was celebrated on Sept. 5th, 1882, in New York City, in accordance with the plans of the Central Labor Union. President Grover Cleveland signed a law on June 28th, 1894, that made the first Monday in September of each year a national holiday, according to the Department of Labor.

***

***

MY SEPTEMBER HEALTH RE-SET

To give my health a boost after Labor Day, I’m taking a complete break from alcohol, sugar, cookies, ice cream, coffee and tea for the entire month of September. Besides that, I’ll also prioritize sleep and increase my exercise from 7 to at least 10 times [hours] a week. This will allow me to focus on my diet and mental well-being. It’s essentially a month of health and wellness rejuvenation.

I’ve chosen to focus on alcohol and sugar because I want to challenge the idea that moderate drinking is part of a healthy lifestyle. In reality, only those who maintain a healthy lifestyle can afford to enjoy alcohol in moderation. But, sugar is everywhere and must be minimized for Type II diabetes and weight control.

Moreover, the long-term and excessive intake of sugary beverages and refined sugars can negatively impact your overall caloric intake and create a domino effect on your health. For example, excess sugar in the body can turn into fat deposits and lead to fatty liver disease.

A low sugar diet can help you lose weight and also help you manage and/or prevent diabetes, heart disease and stroke, reduce inflammation, and even improve your mood and the health of your skin. That’s why the low sugar approach is a key tenet of other well-known healthy eating patterns, such as the Mediterranean diet and the DASH diet.

QUESTION: And so, do you also commit to such “factory resets” now and then? Please comments.

Do, enjoy the Labor Day Weekend, Bar-B-Ques with friends, family and colleagues. And, I hope you continue to find the Medical Executive-Post useful!

Many thanks for your likes and referrals. Dr. David Edward Marcinko MBA MEd CMP [Editor and Chief]

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

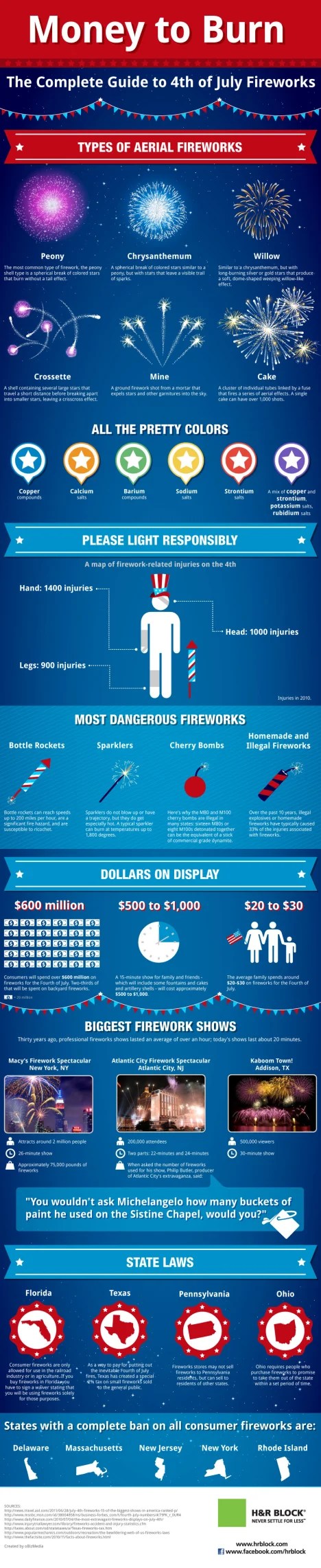

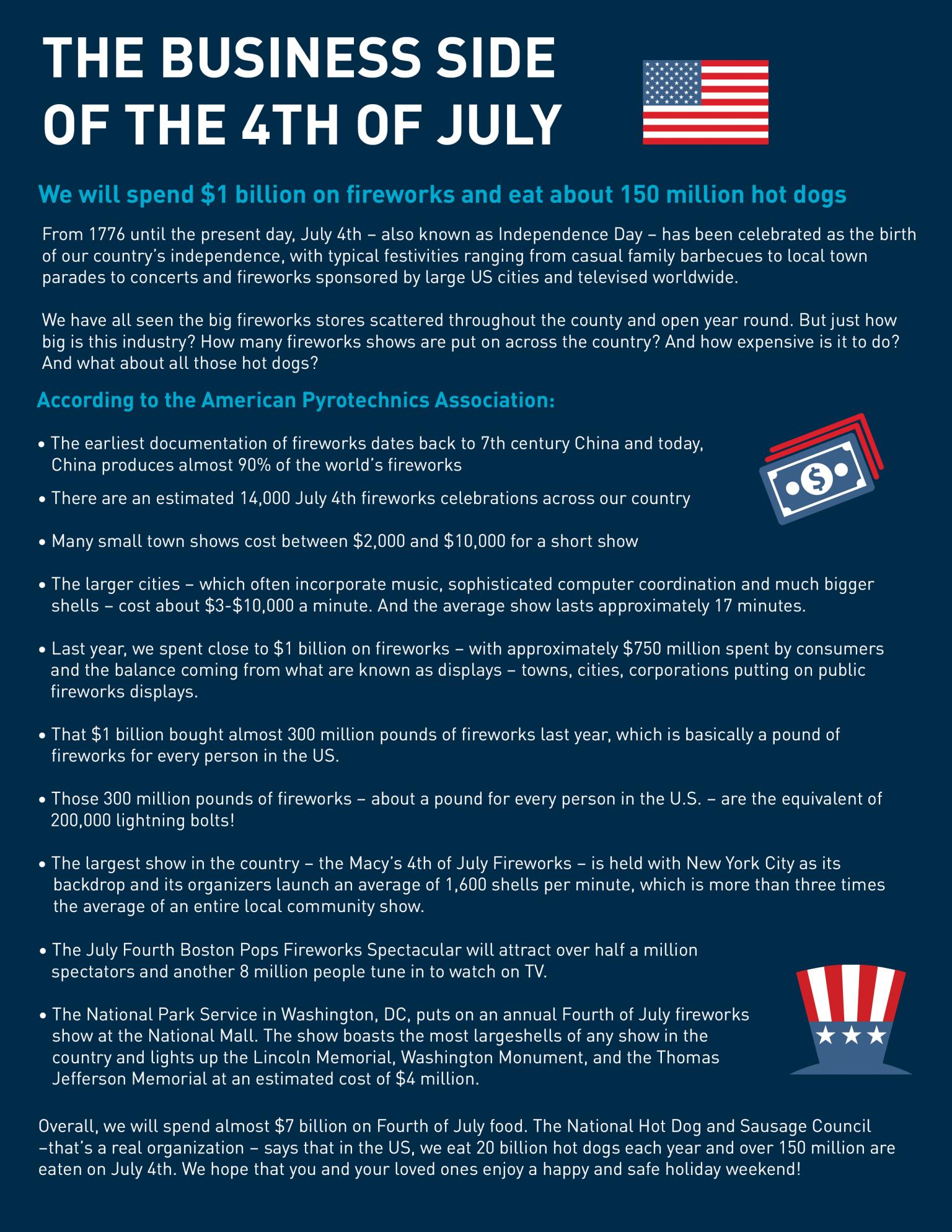

Posted on July 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

Happy Fourth of July! It’s a good day to avoid the emergency department, so leave the fireworks shows to the pros—and perhaps use your extra hands to double-fist some BBQ instead.

If you’re looking at this tab, chances are you are fed up, burned out, seeking a better work-life balance, looking for a new non-clinical career, thinking of retirement, or all of the above. Perhaps you are just looking to regain the joy and meaning in your medical career. No worries! You may have come to the right place.

We work only with doctors, dentists, podiatrists, nurses, technicians and healthcare providers who struggle with personal and professional disillusionment, burnout, financial distress and an unbalanced life – all of which can happen at any stage of a medical career.

Through our coaching sessions, medical and healthcare professionals and colleagues can achieve a more meaningful, purposeful, and financially flourishing life.

Posted on May 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

U.S. stock futures declined after the S&P 500 notched its longest winning streak in more than 20 years last week. Dow Jones Industrial Average futures were down around 280 points, or 0.7%, as of 11 p.m. Eastern. S&P 500 futures and NASDAQ-100 futures were off about 0.8%.

The labor market stayed strong. The US added 177,000 jobs in April, while unemployment stayed steady at 4.2%, new Labor Department data shows. That was slightly less job growth than the month before, but still more than expected, and it shows a resilient labor environment even as the president’s introduction of tariffs roiled the stock and bond markets and raised concerns about a recession. President Trump celebrated the news in a Truth Social post that once again urged the Fed to cut interest rates.

Markets: Stocks soared like a balloon whose string a toddler couldn’t keep hold of yesterday. Unexpectedly strong jobs data for last month and reports that China is open to trade talks helped push the S&P 500 to its longest winning streak in more than 20 years (more on that later), erasing the losses from recent tariff turmoil. On its own impressive streak is Netflix, which hit an all-time high and finished its 11th day in the green for its longest positive run ever.

Crude oil futures dropped more than 3% Sunday after OPEC+ agreed to accelerate production increases for a second straight month in June by 411K bbl/day.

U.S. WTI crude (CL1:COM) for June delivery recently traded -3.4% at $56.28/bbl and July Brent crude (CO1:COM) -3.2% at $59.34/bbl, with both front-month contracts touching their lowest levels since April 9th.

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

There’s often a disconnect between physicians, insurance agents and financial advisors and the patients and clients they’d like to serve. Both might ostensibly share the same goal but there’s often a big difference in perspective. Advisors / Physicians and would-be clients / patients likely have different communication styles, especially in an age where technology has greatly changed the way we talk with one another. Their expectations and priorities can also often dramatically diverge. Those structural gaps can hinder collaboration and trust.

To bridge this divide, you must understand how prospective clients and patients think nowadays and be able to adjust your M.A.S. approach accordingly.

THE BASICS

Marketing is the business process of identifying, anticipating and satisfying patient’s, client’s or customers’ needs and wants. It is your unique value proposition or strategic competitive advantage. Marketers can direct product to other businesses or directly to consumers. But, we believe it is actually your strategic competitive advantage [SCA] which differentiates yourself from competitors. It is the “moat” around your business.

Advertising is a marketing communication that employs an openly sponsored, non-personal message to promote or sell a product, service or idea. Sponsors of advertising are typically businesses wishing to promote their products or services. Advertising is communicated through various mass media outlet, including traditional media such as newspapers, magazines, television, radio, outdoor advertising or direct mail; and new media such as search results, blogs, social media, websites or text messages. The actual presentation of the message in a medium is referred to as an advertisement, or “ad” or advert for short. But, we believe that is simply how you disseminate your strategic competitive advantage [SCM] to potential clients.

Sales close the deal and collects money. Sales are activities related to selling or the number of goods or services sold in a given targeted time period. The seller, or the provider of the goods or services, completes a sale in response to an acquisition, appropriation, requisition, or a direct interaction with the buyer at the point of sale. There is a passing of title (property or ownership) of the item, and the settlement of a price, in which agreement is reached on a price for which transfer of ownership of the item will occur. The seller, not the purchaser, typically executes the sale and it may be completed prior to the obligation of payment. In the case of indirect interaction, a person who sells goods or service on behalf of the owner is known as a salesman or saleswoman or salesperson, but this often refers to someone selling goods in a store/shop, in which case other terms are also common, including salesclerk, shop assistant, and retail clerk.

***

***

DERIVATIVE THOUGHTS

Public Relations [PR] is differentiated than advertising from in that an advertiser pays for and has control over the message. It differs from personal selling in that the message is non-personal, i.e., not directed to a particular individual. We pay for advertising but pray for public relations. But public relations are not controllable but it is free, while advertising is not. PR suggests that “good news or bad news”; just spell the name correctly

Change Management is the discipline that guides how we prepare, equip and support individuals to successfully adopt to change in order to drive organizational success and outcomes.

Crisis Management is the precautions and identification of threats to an organization and its stakeholders, and the methods used by the organization to deal with these threats.

MODERNITY NOW

CRM stands for Customer Relationship Management, which is a system for managing all interactions with current and potential customers, clients or patients. The goal is simple: improve relationships to grow your business or medical practice. CRM technology helps companies stay connected to customers, streamline processes, and improve profitability.

When people talk about CRM, they’re usually referring to a CRM system: software that helps track each interaction you have with a prospect, patient or customer. That can include sales calls, treatment plans or service interactions, marketing e-mails, and more. CRM tools can unify customer and company data from many sources and even use Artificial Intelligene [AI] to help better manage relationships across the entire customer – patient lifecycle – spanning departments described in the M.A.S. basics, above.

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

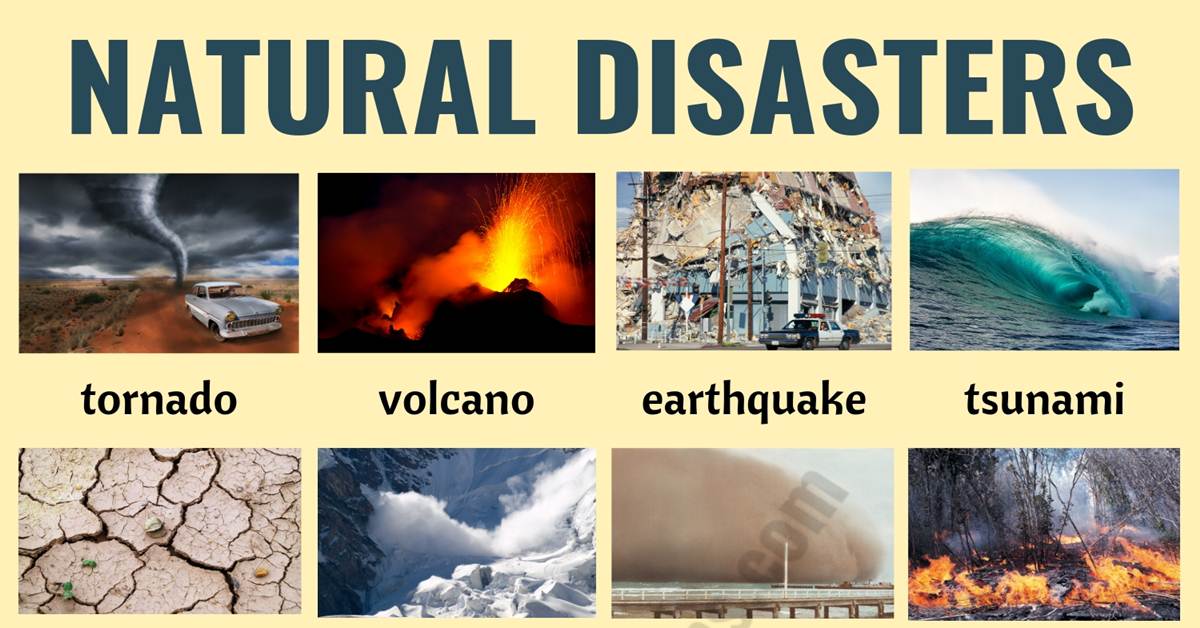

Natural Disaster Insurance

Protecting accumulated assets by insuring them against the wrath of Mother Nature

Most homeowners’ insurance policies do not cover damages arising from floods or earthquakes. If a home, or any other real property like a vacation home or beach condo, is in an area subject to floods or earthquakes, consider the value of purchasing insurance that covers such catastrophes.

Take the time to review your homeowners’ policy, making sure that it will repair or replace your roof if damaged by hail, and will apply in the event of high winds, rather than only in tornadoes. The key to the maintenance of any type of insurance is to anticipate all of the possible calamities, and then to decide whether you can afford to lose the assets exposed to those calamities.

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and Morning Brew

***

***

Microsoft is celebrating its 50th birthday this week looking like a formerly washed up A-lister who’s suddenly rebounded and getting Oscar noms again.

Ever since Bill Gates and Paul Allen huddled in a garage in 1975 to start a company that’d define the experience of sitting in front of a boxy white PC monitor, Microsoft has had an uneven run. But after years of getting roasted for Internet Explorer, it now seems to be back on top—even briefly beating Apple as the world’s most valuable public company last year.

The tech giant can not only boast bonanza earnings, it also feels like a purveyor of the next big thing again, leading in the AI race through its partnership with OpenAI.

Windows washed

In the 1990s, it felt like Microsoft’s computer geeks were the overlords of tech. Windows powered most PCs, Internet Explorer became the go-to browser, and proficiency in Office tools became standard resume skills. But in the following decade, the company slept on internet tech and smartphones, ceding ground to Apple, Alphabet, and Meta.

It responded by going into midlife crisis mode, aka blowing cash on a series of questionable acquisitions to stay hip. That…didn’t help. By the 2010s, only grandparents could be reached @hotmail.com, Windows phones were a rarity, and no one used Bing as a verb.

When Gates stepped away from running the company in 2000, its new CEO Steve Ballmer grew its revenue threefold by the end of his tenure in 2013. He spearheaded Microsoft’s foray into gaming with the Xbox console and started its blockbuster cloud computing product Azure. But Microsoft’s profit growth slowed dramatically thanks to a massive cash bleed from its shopping spree.

It dropped $6.3 billion on the owner of ad tech platforms aQuantive to compete with Google’s ad business in 2007, only to write it off as a dud five years later.

The company burned at least $8 billion trying to make Windows phones a bigger force by buying Nokia’s cellphone division in 2014.

Microsoft paid $8.5 billion for Skype in 2011, which must’ve made it extra painful to announce that it was sunsetting the video calling service this winter.

***

***

Cash-slinging comeback kid

When it blew out forty candles in 2015, the tech giant was looking past its prime. The stock was trading at around $35 a share, well below its $58 peak in 1999. Its net profit for the year was $12 billion. But investors who held on until now were rewarded with shares going for $374 on its birthday this week after the company reported a net profit of $88 billion in the last financial year.

Much of the revenue now comes from its Azure cloud computing business, which has been boosted by the booming AI industry ravenous for server power.

When Microsoft’s current CEO Satya Nadella stepped into the role in 2014, he doubled down on Azure to make Microsoft into a B2B behemoth selling computing power to tech companies.

It is now the world’s second largest cloud provider after Amazon Web Services, with a 21% market share, according to Synergy Research Group.

Microsoft also bought some businesses that didn’t fail, including LinkedIn—the thought leadership hub with a user base that has soared to 1 billion since the 2016 acquisition. It also owns GitHub, the leading code-sharing platform for software developers. And in its biggest purchase yet, it snagged gaming IP giant Activision Blizzard that owns Call of Duty and World of Warcraft for a whopping $68 billion in 2022, hoping to make itself a dominant caterer to the Xbox joystick-wielding crowd.

It’s an AI company now

The not-quite-acquisition that really got Microsoft its groundbreaker’s glitz back was pouring $13 billion into OpenAI.

Having gotten in on the ground floor of the AI boom, Microsoft is harnessing OpenAI’s models to power its CoPilot AI agent, which it embedded into its Office tools and Teams app. This pits it against other tech giants betting that AI agents automating tasks will be the biggest in-cubicle revolution since Excel.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

***

The Hedge Fund manager I am considering is a Registered Investment Adviser [RIA]

QUESTION: What is a Registered Investment Advisor?

If the fund manager is an entity, then any individual you deal with will be a registered investment adviser representative. If the fund manager is an individual, then that individual is a registered investment adviser. In either case, the designation implies several steps have been taken.

In order to become a registered investment adviser, an individual must register for and pass the Series 65 Uniform Investment Adviser Law Exam, a three-hour, 130-question computer-based exam administered by the North American Securities Administrators Association. Topics covered include economics and analysis, investment vehicles, investment recommendations and strategies, and ethics and legal guidelines. A passing score is 70 percent or higher.

Once an individual has passed the Series 65, he or she must then apply via Form ADV to become a registered investment adviser. This application is made to either a state authority or to the SEC, depending on the adviser’s assets under management. If assets under management exceed $30 million, then the adviser must register with the SEC.

Form ADV consists of two parts. Part I provides general information to the regulatory authority. Part II is designed to be distributed to potential clients, and includes disclosure of a decent amount of information about the adviser. If the manager is a registered investment adviser, then you should expect to receive as part of the offering documentation either a current copy of Part II of the adviser’s Form ADV or a brochure that contains all the current information in Part II of Form ADV.

In addition to filing Form ADV and paying a small fee, the registered investment adviser becomes subject to extra administrative/regulatory burden as well as capital adequacy requirements that state the Adviser must maintain certain net worth levels.

By and large, because of the extra administrative burden as well as restrictions on certain activities, hedge fund managers attempt to avoid registering as investment advisers. Whether such managers can or cannot avoid such registration is largely dependent upon the state in which the manager operates. In California, for instance, hedge fund managers must register as investment advisers. In New York, such registration is not necessary. Not surprisingly, hedge fund managers located in California are rare, while they are quite plentiful in New York.

Posted on March 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

[Reviewing Terms, Conditions and Selling Agreements]

By Dr. Charles F. Fenton III JD

***

***

Dealing with many issues concerning the actual contract that affect the purchase or sale of a medical practice can be daunting. For example, this chapter will not deal with issue of determining whether or not a physician should retire. Nor will it determine the proper Fair Market Value [FMV] of the practice. However, physicians may be assisted in both instances by a medically focused financial advisor, or valuation specialist. [AVA, CPA-CVA, Certified Medical Planner™; etc] working in conjunction with an experience health care contract attorney to act as an advocate and determine certain contingencies that might occur, and protect him/her from them.

THE PARTIES

The first determination is whether the party at interest is an individual, group of individuals, or an entity (such as a partnership, limited liability partnership, limited partnership, limited liability company, or corporation – whether an S corporation, C corporation or a professional corporation). In many instances, even if the party at interest is an individual is an entity, the individual or individuals behind the entity should be made parties to the agreement.

From the buyer’s perspective, the purchase of a medical practice is a highly person-oriented business. The practice value depends much upon the personality of the current treating physicians. If the current treating physicians are also the owners of the entity, then binding those individuals (especially as applies to the restrictive covenant) is of primary importance.

If the current treating physicians are not owners of the entity, but rather employees, then a determination of whether they will continue in their same positions or whether the buyer will be taking over the treatment of patients becomes the prime focus. If the current treating physicians will be continuing in their same positions, then their current employment contract must be reviewed to determine whether the rights of the seller will accrue to the buyer.

If the rights of the seller will not accrue to the buyer, then the Purchase and Sale Agreement must have a provision that makes the continued employment of those current-treating physicians a condition to consummation of the sale. In such instances, the new employment agreement might be an exhibit to the main agreement and executed contemporaneously with the main agreement.

If the current treating physicians will not be continuing in their same position and if the purchaser will be assuming treatment of the patients, then the main agreement must provide for the dissolution of the employment agreement and provision must be made for restricting the ability of those physicians from competing with the buyer. If the employment contract with the seller contains a restrictive covenant, then the buyer must ensure that such covenants will accrue to the buyers benefit. Otherwise, the buyer should insist that those physicians sign restrictive covenants. In such an instance, a portion of the purchase price may need to be allocated towards the consideration for those restrictive covenants and paid directly to those physicians.

DATE OF AGREEMENT AND CLOSING DATE

In general, it usually does not matter when the agreement is dated. It should usually be dated once all the terms are agreed to and the parties desire to bind each other and to be bound. In certain instance, the parties may have reached an agreement, but certain issues (such as the obtaining of a state license to practice medicine) may be outstanding. In such a case, then an option can be given by either the seller or the buyer to bind the other to sell or buy the practice upon exercise of the option. Giving an option can also push the agreement date into the future. The option will usually be given with token consideration (e.g., one hundred dollars) and will have a fixed expiration date (e.g., thirty to ninety days).

The determination of the closing date is more important than the date that the agreement is dated. Just like in the purchase of a house where certain issues (such as obtaining a mortgage and home inspection) must occur before closing, in the purchase of a practice, there may be certain issues which require time to undertake before the actual transfer can be consummated. For example, the buyer may still need to obtain financing or the landlord may need to approve the assignment of the lease.

RECITALS

The recitals – or “whereas” clauses – traditionally enunciate the reasons the parties are entering into the agreement. In the sale of the practice the recitals may simply state that the buyer wishes to buy the practice and the seller wishes to sell the practice. Yet, there is a modern growing tendency among contract attorneys to eliminate the “whereas” clauses as some attorneys feel that such language is antiquated. In such instances, the agreement will simply have a paragraph or two delineation of the “Purpose” of the agreement.

ARTICLES, SECTIONS, AND PARAGRAPHS

The agreement will often be divided and numbered in some logical fashion, either into articles, sections, paragraphs, or a combination of these. The reason for doing so is twofold. First, it allows ready reference to the numbered paragraph, and secondly it allows the agreement to be divided and grouped in logical associations.

BINDING THE PARTIES

The first paragraph of the first article will often bind the seller to sell and the buyer to buy the practice under the terms of the agreement. The rest of the agreement simply spells out those terms.

WHAT IS PURCHASED?

The agreement must disclose the items which are being transferred and the items which are not considered part of the agreement. This section should be crystal clear, so that anybody reading the contract (and hence a court which may be called upon to enforce the contract) and not privy to the preliminary negotiations will know what is part of the agreement and what is not part of the agreement.

[1] Sale of Stock vs. Sale of Assets

In most cases, well-informed financial advisors [FAs] will recommend that the buyer solely purchase the assets of the practice and not the stock of the practice. By purchasing selected assets, the buyer is ensured that he will not become responsible for the known or unknown liabilities of the corporation. In prior days, avoiding purchasing the stock of the corporation was a wise recommendation.

However, with the advent of managed care, the purchase of the stock of the corporation can provide the new practitioner with certain competitive advantages. It may take a new practitioner three to nine months to get onto enough managed care panels to make the practice profitable. Purchase of the stock of the corporation ensures the new practitioner of acquiring the Federal Tax Identification Number [TIN], Personal Identification Number [PIN], Drug Enforcement Agency [DEA], Centers for Medicare and Medicaid [CMS], Global Location Number [GLN] , National Provider Identifier [NPI], HIE-Form 834 transmission number, Durable Medical Equipment Number [DME] etc, of the corporate entity. Since most managed care corporations identify providers by the Federal TIN, purchase of the stock of the corporation should allow the new practitioner to be enrolled on managed care panels in a shorter period of time.

[2] Items Purchased

Items purchased often lists the tangible and intangible property of the seller which will be transferred to the buyer. Such items often include:

A detailed inventory of the tangible assets to be purchased;

A detailed listing of the inventory of the practice;

The names and addresses of all of the patients of record treated by the seller;

The patient medical records maintained by seller;

The computer records maintained by seller;

All licenses, permits, accreditation and franchises issued by any federal, state, municipal, or quasi-government authority relating to the use, maintenance or operation of the practice, running to or in favor of seller, but only to the extent that they are accepted by buyer;

All of sellers’ right, title, and interest in and to all real estate and equipment leases, if any, services agreements, employment and professional service contracts relating to the practice but only to the extent that the foregoing are accepted by buyer;

Assignment of lease should be attached and be incorporated to the agreement;

All existing telephone numbers used in connection with the operation of the practice and all yellow page advertising of the practice; and

The goodwill of the practice, which includes seller’s assistance and cooperation in transfer of all sellers’ rights and interests in the practice to buyer and any other intangible assets of the practice not listed in any other category.

Certain items purchased, such as [paper or electronic] medical records, governmental licenses, fax, email, website and telephone numbers have special considerations as discussed below.

[3] Medical Records

The seller should protect its future need to use the transferred patient medical records. In the current managed care environment, providers are subject to strict scrutiny. Even after leaving practice the provider may find himself subject to a government or third party audit or subject to a medical malpractice lawsuit. Therefore, the provider should ensure that the contract allows for him to take future possession of the specific medical record(s) of the practice in order to mount an appropriate defense.

[4] Governmental Licenses

Certain government licenses and permits may be nontransferable. These would include items such as the federal and state employer identification numbers, as these are unique to seller as a corporate entity. Likewise, other items unique to seller include Medicare identification numbers, Medicaid identification numbers, NPIs and UPINs. The buyer would have to purchase the stock of the corporation order to acquire such items, which is another advantage of a stock transaction versus an asset transaction. Likewise, some local business licenses may or may not be transferable.

[5] Telephone and Fax Numbers, Website URLs and Twitter [X] Accounts, etc

Transference of the telephone numbers often requires that a special local telephone company form authorizing transfer of the telephone numbers to the buyer. Often the new owner of the telephone number will also become liable for any current yellow page advertisement monthly fees. It is the same with an URL or website or e-mail address or office Twitter X account, etc.

[6] Items Not Purchased

Items not purchased or “excluded items” often list the personal items of the parties or of the employees of the parties. Such items would often include:

All cash on hand or on deposit;

All accounts receivable generated prior to the closing date;

All prepaid expenses, utility deposits, tax rebates, insurance claims, credits due from suppliers and other allowances after Closing Date;

The personal effects, including but not limited to photographs, diplomas, uniforms, books, mementos, memorabilia, personally owned art and any personal property owned by them;

Life insurance, disability insurance, and disability buy-out insurance on seller;

Motor vehicles used in connection with the practice;

Any or all tangible-intangible assets used in conjunction with another practice of seller; and

All other assets owned by seller other than those specifically described as items purchased.

The exact items transferred will often depend upon the prior negotiations of the parties. For example, the parties may have agreed that the accounts receivable will be transferred with the practice. In such an instance, the accounts receivable will be listed as an item to be purchased.

PURCHASE PRICE AND TERMS

The price of the transaction (or the value of the practice) is often the one item that is aggressively negotiated between the parties. That is because both the buyer and the seller are overly concerned with “how much?” As this chapter demonstrates, there are a lot more details that go into the negotiation and final contract than just the price. The buyer or seller would be doing themselves a disservice to consider the other factors simply “lawyer details.” Many additional terms of the agreement should be considered by one side or the other as “walk-way” conditions. The party that fully adheres to their additional terms is likely to find the other party capitulating to them. This is because the other party will most likely be fixated on the price.

The purchase price should be delineated in the agreement. Furthermore, the method of payment of the purchase price should be delineated. Although the usual method of payment would be cash, there are other methods available as well.

Cash payment can be made by an official bank cashier’s check, by a certified check, by deposit of funds into an escrow account, or by other method agreed upon by the parties.

Non-cash type transactions include loan agreements and exchanges. Exchanges can provide certain tax benefits if the exchange is a “like kind” exchange. A like kind exchange would occur when parties swap practices. For example, a group practice might have several offices. As part of the breakup of the group, the parties might exchange their stock of one office for all of the stock of another office. Like kind exchanges have strict guidelines that must be adhered to or the tax advantages will disappear. The reader is cautioned to get current legal and financial advice prior to the time of exchange.

It is in the seller’s best interest to get all cash at the time of closing. Then the seller can walk away and not worry about the success or failure of his predecessor. The seller will not have to worry about collecting periodic payments. The seller will not have to worry about placing the buyer in default or about eventually having to repossess the practice and begin to practice medicine at that office again. If a seller repossesses a practice, the buyer may have driven the patients away or lost the managed care contracts (why else would the buyer not be able to honor the loan agreement?). So the repossessed practice will have a significantly lower market value – if it is even marketable at that time.

On the opposite end of the spectrum, it is in the buyer’s best interest to get long and lean loan terms. First, by getting loan terms, the buyer will often have to come up with much less initial capital. Second, because of the discussion in the preceding paragraph, the seller has a vested interest in ensuring that the buyer succeeds once the practice changes hands.

If the transaction involves a seller-financed loan, then the agreement should specify the terms. Additionally, a separate loan agreement and security agreement should be attached as exhibits to the agreement. Finally, in order to perfect the security agreement, the lien should be recorded at the local courthouse in accordance to local rules and customs.

***

***

ALLOCATION OF PURCHASE PRICE

The final purchase price will actually be the amalgamation of various assets of the practice. Those assets include the tangible and intangible assets. The tangible assets include the hard assets (such as computers, treatment tables, chairs and furniture, DME and x-ray machines, etc) and the soft assets (such as Q-tips, paper and cotton balls). The intangible assets will include going concern value, goodwill, and the value of any restrictive covenant.

The parties should delineate the allocation of the purchase price amongst those various categories to reach a mutual best fit with the potential tax obligations. The buyer is the one who should strive to make the allocation fit his needs as best as possible.

Generally, the sale of the assets will be ordinary income to the seller and taxed at the seller’s usual rate. The buyer will be able to depreciate the purchased items. However, the characterization of those assets and the allocated portion of the purchase price will determine how much can be depreciated and over what time period the items can be depreciated.

As a general rule, soft assets can be depreciated fully in the year of purchase. Generally, hard assets can be depreciated over a three to seven year time period, depending upon the class of the asset. Also, under Section §179, a certain dollar amount can be “expensed” or deducted in the year of purchase. The sooner and the faster that the assets can be deducted the less current taxes that the buyer will be required to pay. However, intangible assets generally must be deducted over a 15-year period. This prolongs the tax benefits of any payments characterized as such.

Nonetheless, purchase of the assets results in better tax consequences that purchase of the stock of the practice. When stock is purchased, there is no depreciation allowance allocated in the current or subsequent years. Instead, the cost of the stock becomes the “basis” of the buyer in the practice. Any gain or loss from that basis will only have tax benefits or tax consequences in the year that the stock is sold or becomes worthless.

Because of the tax consequences of the characterization of the allocations of the purchase price, it is important that the agreement delineate the portion of the practice price which is allocated to each category. Each party should further agree never to claim a different allocation in any future tax filings. Generally, the soft and hard assets will be valued at their current actual cash value. In no event should the purchase price allocated to the soft and hard assets exceed the actual initial cost that the seller paid for the item. The only exception to the foregoing would be if the sale involved the transfer of an appreciable asset.

LEASE ASSIGNMENT

The agreement should provide that upon closing that the seller will assign the lease to the buyer. The buyer then acquires possession of the premises and assumes responsibility for the lease payments.

Sellers often do not understand that even though they do not practice at the leased premises and even though the buyer is making the lease payments, that the seller still remains liable to the landlord under the original lease. Usually this does not present a problem for the seller. But if the buyer abandons the premises or stops making the lease payments, then the landlord will look to the seller for the lease payments through the expiration of the lease.

If the seller has signed a restrictive covenant, then the seller may find himself in the unenviable position of making lease payments for the premises and prohibited from practicing at the premises. The seller should protect himself from this possibility. Therefore, the seller should ensure that the original agreement contains a provision that if the seller becomes liable under the lease that the seller can enter onto the premises, take possession of the practice and the practice assets and can practice medicine at the location until the seller’s liabilities are extinguished.

INDEMNIFICATION AND EXCLUSION/INCLUSION OF LIABILITIES

During the sale of a medical practice, each party will have certain liabilities that the other party should not assume and should not be required to assume. A mutual indemnification clause will act to ensure that each party remains liable for its own liabilities.

In a medical practice, the most common liability is a claim of medical malpractice against the provider. The seller has an interest in insuring that he is not liable for any claim brought by a patient that resulted after he leaves the practice and the buyer has an interest in insuring that she is not liable for any claim brought by a patient that resulted before she acquired the practice.

There are other areas of liability in the sale of a medical practice that may not be readily apparent. These include premise liability (e.g., slip and fall claims), employment claims (e.g., unemployment liability, sexual harassment, discrimination, and wrongful termination claims), tax claims (e.g., unpaid employment taxes and income or sales tax liabilities), and third party payer claims (e.g., Medicare recoupment claims). Consult your insurance agent to determine whether you can obtain insurance coverage to limit your liability under these clauses.

Medical practitioners should understand the full risk of signing an indemnification or hold harmless clause. If a claim is brought against the other party, then the party giving indemnification can be forced to pay any judgment or settlement incurred by that other party. The party giving indemnification can even be required to pay the other party’s attorney bills. This is an important point that the reader should consider carefully: Even if the other party successfully defends a claim, the indemnifying party can be held liable for the other party’s attorney’s fees. Since attorney fees can mount up rapidly, the indemnifying party can find itself responsible for thousands or even tens or thousands of dollars of attorneys’ fees.

If at all possible, one should never sign an indemnification agreement, whether in the sale of a medical practice, a managed care contract, or even a home security monitoring contract. Sometimes, one has no choice but to assume the risk and sign the contract. If at all possible, one should strive to sign such clauses in a corporate capacity and not in an individual capacity. If that is not possible, then seek insurance to minimize the risk. Indemnification clauses and the potential unlimited risk that they pose is one reason why the professional should undertake a carefully planned asset protection program.

***

***

OTHER FACTORS AND CLAUSES

[A] Integration

As a general rule, once parties have seen fit to put their agreement in writing, then no prior oral agreement regarding the same subject is binding. A paragraph stating that the written agreement contains the entire understanding of the parties simply reflects this rule of contract construction. Such a paragraph also places the parties on notice that any oral representation of the other party that has not been placed in the contract will be worthless.

[B] Construction

At times a court may hold any ambiguities in a contract against the party that prepared the agreement or that had the agreement prepared for them. If the party on the other side of the contract is an individual that was not represented by counsel and especially if that party has had very little business experience (such as a physician or medical provider recently in practice), courts are much more likely to hold ambiguities against the drafter of the agreement.

A paragraph regarding the construction of the agreement and stating that the agreement was formed from negotiation (as opposed to a “take-it-or-leave-it” proposition) can identify for any court constructing the contract that the court should not hold any ambiguities against the drafter. After all, even with negotiated contracts, one party or the other draws up the agreement.

[C] Choice of Law

In the United States today, it is common for parties in different states to have business dealings with each other. Likewise, in the sale of a medical practice, the buyer may begin negotiations in one state and then move to the practice state after consummation of the sale. In a similar vein, following the sale the buyer may move to another state.

In most cases, the various state laws should be similar on the contractual issues involved in the sale of a medical practice. However, a statement in the contract identifying the state whose laws will govern the contract will eliminate one possible source of dispute involving a side issue to the contract. In the vast majority of contracts, the laws of the state where the practice is physically located should be chosen by the parties to govern the contract

[D] Choice of Venue

Just like providing for choice of law, a side issue to the contract can be eliminated by choosing ahead of time the venue to resolve any conflicts that may arise. The venue is simply the place where the conflict will be decided. In most cases, the parties should choose the trial court of the county in which the practice is located.

[E] Survival of Obligations

An agreement to purchase a medical practice contains two aspects. First is the transference of the practice assets in exchange for the purchase price. Second are the various other terms, such as preservation of the medical records. By providing that these obligations survive the closing, each party is assured that the other party will not claim that the actual closing of the agreement extinguished the rights of the parties under the agreement.

[F] No Waiver Clause

A provision providing that a party does not waive its rights unless such a waiver is committed to writing allows a party to be a “nice guy” without risking its future rights. In some instances, if a party does not insist upon full compliance by the other party, then the first party may be considered to have waived its rights and may have no recourse against the other party.

There may be instances when the forbearance to exercise a right under the contract will benefit both parties. For example, if the buyer cannot pay the seller an installment on time, the seller may agree to extend the time for payment of that installment. The no waiver clause allows the seller to refuse to extend the time for payment of a future installment. Without the clause the buyer might be able to argue that the seller had waived its future rights to timely payments.

[G] Notices

There may be various reasons under the contract why one party may need to give a notice to the other party. Most often such notice will be that a party is claiming that the other is in breach of some provision of the agreement.

By specifying the address and method of delivery of any notice, the sending party can be assured that a court will rule that the receiver had actual or constructive notice.

Such a provision should also provide that one type of notice would be a change of address. Such a change of address notification would then supersede the address delineated in the agreement.

In most cases, the agreement should provide that the counsel to the party would receive a copy of any notice. This accomplishes two goals. First, there is a greater likelihood that the receiving party would receive actual notice. If the receiving party had moved and had failed to provide notice of the change of address, then the party’s counsel would have received the notice. Secondly, the party’s counsel would have received the notice in a timely manner and could take any immediate action that may be necessary.

[H] Severability Clause

A severability clause helps to ensure that if one provision is held by a court to be illegal or unenforceable, then the offending clause will be stricken from the agreement and the parties will be held to the agreement without the clause.

Without a severability clause, if a court finds that one provision of the agreement illegal or unenforceable, then the court has the power to strike down the entire agreement. Although even with a severability clause a court could strike down the entire agreement, the severability clause tells the court that the intent of the parties was that only the offending clause be stricken and essentially asks the court to honor the parties’ intent.

[I] Further Assurances Clause

After execution of the agreement, the parties may discover that certain other documents are necessary to complete the transaction. Unless such documents materially change the meaning and purpose of the agreement, a further assurance clause requires the party of parties to execute and deliver the document.

***

***

CLOSING – SETTLEMENT

The closing or settlement date should be chosen for a mutually time and place. Generally the date will be between 30 and 90 days from the execution of the agreement. This will allow the buyer and the seller adequate time to complete any conditions precedent to closing. At closing, the buyer will tender to the seller the agreed upon funds and will execute any loan and security agreements required under the purchase and sale agreement. If the restrictive covenant also contains a buyer’s covenant, then the buyer will execute that document. The seller will deliver to the buyer a bill of sale for the assets of the practice, will execute the restrictive covenant, will deliver the keys to the practice, and will surrender the assets and the premises to the buyer. Both the buyer and the seller will execute the lease assignment.

Many of the provisions of the agreement will survive the closing. This includes any agreement to prorate expenses not allocated in at the closing, the restrictive covenant agreement, the indemnifications, and any seller’s right maintained in the medical records.

TRANSITION

Both the seller and the buyer have certain interests to protect after the closing which would require the seller to stay with the practice for a period of time following the closing. The seller may have ongoing treatment plans with certain patients (such as post-operative follow-up treatment). The agreement should specify that the seller be allowed to continue at the practice location for the purpose of finishing such treatment plans. Although the buyer may be fully capable of completing such treatment plans, both the buyer and seller should be cognizant that the patient may claim abandonment. Allowing the seller to complete treatment plans in progress will mitigate against any perceived or actual claims of abandonment.

The buyer will want to require the seller to stay with the practice for a certain period of time, usually between three to six months. During that time, the seller will act to introduce the buyer to the current patients and the buyer will begin treatment of any new patients to the practice. In this way, the transition will appear smooth and natural to the current patients.

Of course, during the transition period, the seller will have the right to be paid by the buyer. To avoid misunderstanding, the method of payment should be reduced to writing. Usually the rate of compensation will be the profit margin percentage of the practice allocated to all income collected from the seller’s efforts during the time period in question. An astute negotiator might be able to require the seller to function during the transition period as an implicit condition for the payment of the practice price.

RESTRICTIVE COVENANTS

As part of the purchase price the buyer is paying for intangible assets of the practice. A medical practice is a highly individual based business. The practice depends in large part upon the reputation of the selling physician. For that reason, the buyer must ensure that the seller cannot use that highly individualized asset to compete against the practice for which she has just paid a high sum. The restrictive covenant protects this interest of the buyer.

A restrictive covenant actually contains several covenants to protect the buyer’s interests. These include not only the obvious covenant not to compete, but also a covenant regarding financial interests, a covenant regarding solicitations, and a covenant regarding proprietary information.

The first covenant is the covenant not to compete. In this covenant, the seller agrees not to compete with the practice in the geographic area during the time term of the agreement. This covenant prohibits the seller from actually practicing or from practicing indirectly. For example, the seller could not set up a clinic within the geographic area during the time period and employ a nurse practitioner to treat patients under his medical license.

The next covenant would be the covenant regarding financial interests. In this covenant, the seller is prohibited from investing in a competing business (i.e., medical practice), within the geographic area during the time period. This provision prevents the seller from investing in such a medical practice, even if he does not directly treat patients at that location.

The third covenant would be the covenant regarding solicitation. In this covenant the seller agrees not only to refrain from contacting patients of the practice during the time period, but also to refrain from contacting employees of the practice. If the seller maintains another office location which will not be sold, then the seller should ensure that the agreement provides that the seller is allowed to treat patients which find themselves to that practice location. Otherwise, the seller may be liable for patient abandonment and may also violate managed care contracts.

A final covenant would be a covenant regarding proprietary information. Simply by the fact of operating the practice, the seller has obtained certain proprietary information about the practice. This includes patient lists, accounting information, managed care contracts, and forms and handbooks. The seller should be prohibited from using such knowledge to the detriment of the practice.

[A] Time and Distance

The time and distance covered by the restrictive covenants must be reasonable. If either the time or distance is unreasonable, then a court might strike down the entire restrictive covenant.

A reasonable time is usually between two to five years. A two-year time period should be the minimum that the buyer should insist upon. The purpose of the time period is to allow sufficient time for the practice patients to consider the buyer as their “doctor” and to lose confidence in the selling doctor. For that reason, any time period over five years is likely to be considered an unreasonable restraint.

On the other hand, a reasonable distance depends upon many individual factors. A reasonable distance in an urban area like New York City would most likely be completely unreasonable in rural areas, such as rural Iowa. In most metropolitan areas, a five to ten mile radius from the practice location is likely to be considered reasonable. In rural areas, an entire county or even several contiguous counties may be considered reasonable. The main determination of the reasonableness of the distance factor is the total area from which the practice draws its patients.

Most practice management software programs allow for delineation of the practice patient base determined by zip code. That will provide the parties a starting point from which to negotiate the distance factor of the restrictive covenant.

[B] Buyer’s Covenants

The restrictive covenant should also contain buyer’s covenants, although it may seem counterintuitive that the buyer, having paid the seller tens of thousands of dollars for the practice, should be required to sign buyer’s covenants. However, a buyer’s covenant is an important part of the restrictive covenant. Under the purchase agreement, the seller might retain the right to repossess the practice, the practice assets, and the premises. This is most likely to happen when the seller finances the purchase price and the buyer defaults on the payments. It can also happen when the seller assigns the lease to the buyer and the buyer either abandons the premises or otherwise causes a default under the lease. The seller then remains liable as principle under the lease.

For those reasons, the restrictive covenant should provide that if the seller is required to enter onto the premises and take possession of the practice, then the Seller is relieved of his obligations under the restrictive covenants and the buyer now becomes bound by those same obligations. Such buyer’s covenants will prevent the buyer from abandoning the practice and then setting up a nearby competing practice.

CORPORATE RESOLUTION

Most medical practices being sold are corporate entities. If the transaction is a sale for stock, then the transaction is between private parties – the buyer paying cash and the seller transferring the stock.

However, in those cases where the buyer is purchasing the assets of the corporate practice, then the corporation must take certain prerequisite steps. Generally, a corporation, through its officers and directors, is prohibited from selling significant assets without permission of the shareholders.

For that reason, a shareholder meeting must be held and the shareholders at that meeting must approve a resolution allowing the officers and directors to sell significant assets of the corporation.

ASSESSMENT

The contract regarding the sale of a medical practice is the final agreement of the parties. Such a contract should only be executed after sufficient investigation into the practice and upon consultation with proficient professionals, including attorneys, accountants, FAs and practice management consultants. Understanding the basic terms and conditions of a contract regarding the sale of a medical practice is the first step in successfully negotiating the best agreement possible. Before one can negotiate for a certain provision, one must first be aware of the possibility of such a provision and its possible ramifications.

So, what else can FAs and consultants do to help plan properly for the sale of a medical practice, physician succession planning, and this major life liquidity event? Some experience FAs suggest constructing a “dry run template analysis” so the doctor can envision what life will be like after the sale, and what their corresponding financial needs might be. When the practice is sold, life is very different because many expenses that the practice paid become expenses the doctor now must pay. And so, the use of an astute financial advisor, practice valuation specialist, and healthcare contract attorney is highly advised.

CONCLUSION

As we have seen, the purchase price of a medical practice, although am important part of any sale, should only be considered one element of the negotiations. There are many clauses and provisions of a contract regarding the sale of the medical practice, which if not negotiated favorably should be considered factors to initiate the party to walk away from the sale.

Boundy, Charles: Business Contracts Handbook Gower Pub, NY 2010

Fenton, CF: Contracts Regarding the Sales of a Medical Practice. Financial Planning for Physicians and Healthcare Professionals; Aspen Publishers, New York, NY, 2003.

Hekman, K: Buying, Selling & Merging a Medical Practice. Keneth Hekman, New York 2008.

Walker, Lewis: The Ultimate Transition. Financial Advisor, page 33, 2014.

Schatzki, M: Negotiation Speak: Winning Words and Phrases for Sales, Purchasing, Contract and Other Business Negotiations – All the Dialogue and Skills You Need to Come Out Ahead, Dynamic Negotiations, Chicago, IL 2009.

UCC, Commercial Contracts and Business Law Blog: LexisNexis 2010.

Posted on March 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters and FTC

***

***

Surveillance pricing is a broad term to describe the practice of linking pricing to individualized consumer data.

Companies employing it might use algorithms, personal information, and AI to set a price for their goods based on everything from where you live to your age to your browsing or credit history. The practice, sometimes called dynamic pricing or personalized pricing, is growing increasingly common, but isn’t completely new.

In 2012, the travel website Orbitz began directing people on Macs to higher hotels after realizing they often had more purchasing power. It stopped the practice after the Wall Street Journalreported on it.

Is surveillance pricing the same thing as surge pricing?Yes and no.

You might know about surge pricing from the last time you tried to call an Uber during a rainstorm. As demand skyrockets for a ride share, so does the price. This is one kind of surveillance pricing, but what the FTC is targeting appears more specific. The FTC said its probe concerns “when the pricing is based on surveillance of an individual’s personal characteristics and behavior.”

Is surveillance pricing bad?

The FTC opened its probe into companies using surveillance pricing because it’s worried about the risks it might pose to consumers

“Firms that harvest Americans’ personal data can put people’s privacy at risk. Now firms could be exploiting this vast trove of personal information to charge people higher prices,” FTC Chair Lina M. Khan said in a statement. “Americans deserve to know whether businesses are using detailed consumer data to deploy surveillance pricing, and the FTC’s inquiry will shed light on this shadowy ecosystem of pricing middlemen.”

The FTC is looking into four major areas of the practice: types of products being offered, data collection, customer and sales information, and impacts on consumers and prices.

Many Americans, it fears, don’t know when their data is being harvested and how it is affecting what they pay. “Consumers may now be subjected to surveillance pricing when they shop for anything, big or small, online or in person: a house, a car, even their weekly groceries,” the FTC said.

The FTC sent the orders for more information to Accenture, Bloomreach, Chase, Mastercard, McKinsey & Co., Pros, Revionics, and Task.

“Advancements in machine learning make it cheaper for these systems to collect and process large volumes of personal data, which can open the door for price changes based on information like your precise location, your shopping habits, or your web browsing history,” the FTC wrote.

Posted on March 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

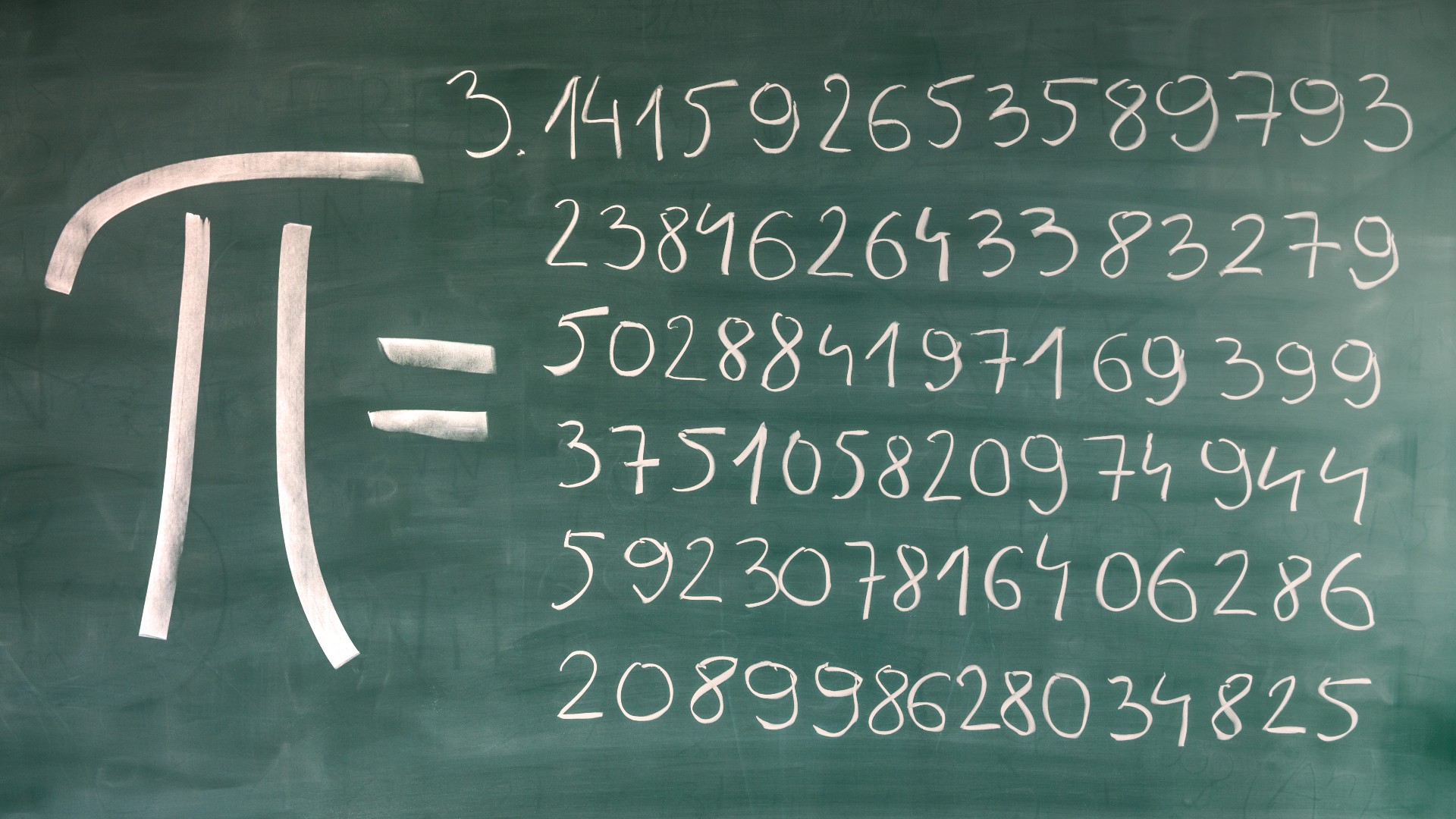

What is Pi?

Pi is the ratio of the circumference of a circle to its diameter, or approximately 3.14.

What is Pi Day?

Pi Day occurs on March 14, because the date is written as 3/14 in the United States. If you’re a serious math geek, celebrate the day exactly at 1:59 a.m. or p.m. so you can reach the first six numbers of pi, 3.14159.

Posted on March 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

March 6th is National Dentist Day, a day to celebrate the men and women who keep our chompers chomping, our gnashers gnashing, and our whites pearly.

Dentists (DDS/DMD) are doctors who specialize in oral health. It’s their job to prevent, diagnose, and treat oral diseases, monitor the growth of our teeth and jaws, and perform surgical procedures on our teeth and mouths!

Dental health is integral to our overall health, so today we salute them not just for keeping our teeth looking good, but keeping our bodies in tip-top shape.

Posted on February 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

February is National Cancer Prevention Month. While life can become unpredictable with challenges and setbacks like a cancer diagnosis, there are many things you can do today to reduce your risk of developing this illness. So, the experts at Mary Bird Perkins Cancer Center recommend the following

LIFESTYLE HABITS

Eat healthy: Eating well-balanced meals that include fruits and vegetables, whole grain foods, low or non-fat dairy products, and limited red or processed meats can all help reduce cancer risks.

Exercise: Aim for at least 150 minutes of moderate-intensity or 75 minutes of vigorous-intensity activity each week. Physical activity lowers stress hormones, improves the immune system, and is associated with living a long, healthy life. Regular participation in physical activity has been linked to a decreased risk of colon, breast, lung, and endometrial cancer.

Maintain a healthy weight: Try to achieve and maintain a healthy weight throughout your life.

Avoid tobacco: Don’t smoke or use smokeless tobacco.

Limit alcohol: Drink alcohol in moderation, if at all.

Posted on February 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

SAVE A LIFE

By Dr. David Edward Marcinko MBA MEd and Staff Reporters

***

***

Did you know more than 23,000 children experience cardiac arrest outside of the hospital each year?

Learn CPR today so you can be ready and become a part of the Nation of Lifesavers. Because no one, especially our most precious ones, should face a life-changing moment alone.

Posted on February 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Complimentary Glow Effect is when something looks better simply because it’s next to something else that’s attractive. It’s like standing next to a supermodel to get a boost to your own appearance.

Marketers use this all the time by pairing products with glamorous images to make them more appealing. It’s a visual trick that our brains fall for every time.

So, according to colleague Dan Ariely PhD, the next time you’re tempted by a shiny new gadget, remember: it might just be basking in the complimentary glow of clever marketing.

Posted on February 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A vexing phenomenon is plaguing the labor market. “Ghost jobs” refer to listings by employers that either aren’t real or have already been filled but never lead to an actual hire. This is frustrating not only to job seekers but also to the Federal Reserve, which is trying to steer the economy to a stable place.

People should be aware of how to distinguish a ghost job posting from a real job posting so they can avoid the disappointment and anticipation of hearing back from a job that never existed.

The warning signs you applied for a ‘ghost job’:

Job opening was posted over 30 days ago

There is no time stamp on the original post

Re-posted role

A vague job description that doesn’t include salary or location

Posted on February 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Cognitive bias is a pattern of thinking in humans that, although flawed, is repeated mindlessly, sometimes resulting in irrational behavior and decisions. Dental personnel need to understand how cognitive biases impact both their patients and their team members. Left unchecked, these automatic associations can cause grave mistakes and injuries, and result in real harm.

This course is designed to help dental team members recognize their own biases and see the need to introspect and self-regulate to change them.

Dr. David Edward Marcinko works with doctors, nurses, technicians and healthcare professionals who struggle with professional disillusionment, burnout, financial distress and an unbalanced life–all of which can happen at any stage of a medical career. Through our coaching sessions, medical and healthcare professionals can achieve a more meaningful, purposeful, and flourishing life.

U.S. Markets will be closed for Martin Luther King Jr. Day this Monday

The U.S. Markets will be closed on Monday, January 20th, 2025. Please be aware that, when making transactions after 4 p.m. EST on Friday, January 17th, 2025, you will receive the closing price as of Tuesday, January 21st 2025.

Martin Luther King Jr. Day is observed in the United States on the third Monday of January. This year coincides with the inauguration of President-elect Donald Trump.

Banks and government offices

Martin Luther King Jr. Day is a federal holiday, which means banks will be closed and government services as well, such as city offices, animal services, administrative offices of the police department, and administrative offices of fire department.

The U.S. Postal Service will not operate on Monday, along with other shipping services.

Posted on December 31, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Is the Stock Market Open or Closed on New Year’s Eve?

Bond markets will close early at 2 p.m. Eastern on Tuesday, while the New York Stock Exchange and the NASDAQ Stock Market will hold regular hours from 9:30 a.m. to 4 p.m. Eastern. Over-the-counter markets, where securities trade over a broker-dealer network rather than a major exchange, will keep normal hours.

Is the Stock Market Open or Closed on New Year’s Day?

Both the U.S. bond and stock markets will be closed in observance of New Year’s Day. Over-the-counter markets will be shut, too.

What About International Markets?

Foreign exchanges, such as the London Stock Exchange, the Euronext Paris, the Stock Exchange of Hong Kong, the Shanghai Stock Exchange, and the Tokyo Stock Exchange, will be closed on Wednesday, January 1st.

Will Banks and Post Offices Be Open?

Federal Reserve banks and United States Post Service locations will be closed in observance of New Year’s Day.

Today marks the anniversary of the 1941 attack on Pearl Harbor, which led to the US entering World War II

***

***

Strategically situated between the US West Coast and the Asia-Pacific region, Pearl Harbor remains an important site to the US military 83 years after the attack. Pearl Harbor is home to one of the Navy’s four public shipyards, and it’s the largest industrial employer in Hawaii (they do maintenance on nuclear submarines there).

The Navy’s other three public shipyards are located in Portsmouth, NH; Norfolk, VA; and Bremerton, WA.

Posted on December 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

On November 1, 2024, CMS released its Outpatient Prospective Payment System (OPPS) and Ambulatory Surgical Center (ASC) Payment System Final Rule for calendar year 2025. The rule finalizes payment updates, revises current programs, and establishes new standards to address the ongoing maternal health crisis.

This Health Capital Topics article discusses the key OPPS changes and updates included in the Final Rule. (Read more…)

Posted on November 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A “wave of inclement weather through the eastern two-thirds of the country” could throw travel into chaos this week, according to the Weather Prediction Center. TSA predicts 30 million people will fly over the holiday, an 11.5% increase from last year, putting a strain on a US aviation system struggling to keep up with demand.

One positive? Thanksgiving gas prices could be the cheapest they’ve been since 2020. Whether you’re flying, driving, taking the train, or awaiting the arrival of those who are, here are some tips to get through the next few days with minimal stress.

Posted on November 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

November 13th, 2024

***

***

World Kindness Day is an international holiday first introduced in 1998 by the World Kindness Movement.

The holiday is devoted to promoting kindness throughout the world, understanding the positive potential of large and small acts of kindness, and unifying together as human beings.

Posted on November 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

FREE SAMPLES

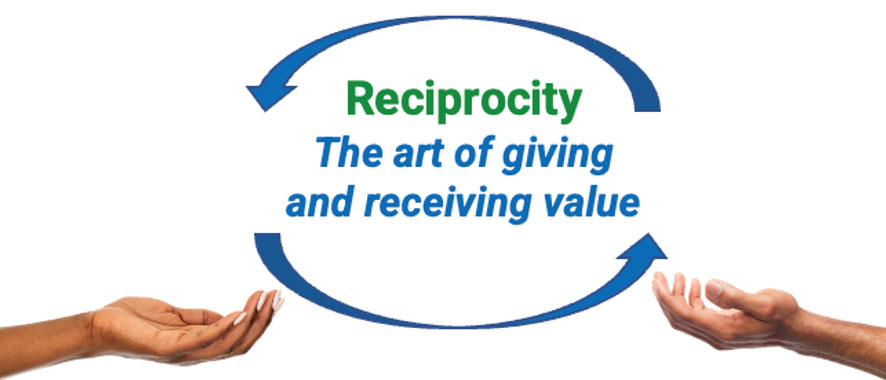

The Art of Giving – And Receiving – Value!

By Staff Reporters

***

***

Imagine you’re at a party, and someone hands you a drink. Your first instinct? Find something to give back. This is [sales] reciprocity in action – our built-in psychological urge to repay kindness.

According to colleague Dan Ariely PhD, it’s like a cosmic balance sheet in our brains, ensuring we don’t owe anyone a favor. This is why companies give out free samples. They’re not just being nice; they know you’ll feel a pang of guilt if you walk away without buying something.

THINK: Free financial planning dinner seminar and prospecting event. That’s you – the Sales Prospect!

So, next time someone does you a favor, remember: it’s not just seller kindness, it’s science!

Posted on October 14, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

U.S. stock markets, including the New York Stock Exchange and the NASDAQ remain open and follow a regular schedule today.

The bond markets will be closed, however.

***

***

Stocks ended last week on a high note, closing out their fifth straight week of gains. The Dow was pushed to yet another new all-time high by strong earnings from JPMorgan, while the S&P 500 was in the green and rose to its own record close, and the NASDAQ clawed its way out of the red by early Friday afternoon.

Bond yields took a breather, falling below 4.1% thanks to a better-than-expected PPI report that helped offset inflation fears that had re-arisen after a worse-than-expected CPI report.

Gold rose as well on PPI news, since the data pointed to a better chance of more rate cuts ahead.

Oil fell a bit but gained over the last two weeks on geopolitical tensions and destruction in the Gulf of Mexico following the two major hurricanes.

Posted on October 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Kamala Harris announced a plan to broaden Medicare to cover home healthcare for the first time in an effort to help the “sandwich generation” of Americans who are taking care of both their children and their parents.

WeightWatchers said it will offer cheaper copycat versions of Novo Nordisk’s weight loss drug, Wegovy.

Reddit gained 0.31% thanks to Jefferies analysts, who debuted their coverage of the social media stock with a “buy” rating, praising the company’s AI potential.

Biogen climbed 1.90% after the FDA gave its treatment for kidney transplant patients a special Breakthrough Therapy Designation.

Cruise stocks sailed higher today, in spite of the oncoming hurricane in the Gulf of Mexico. Norwegian Cruise Line, Carnival, and Royal Caribbean popped 10.91%, 7.05%, and 5.26%, respectively, on upgrades from Citi analysts.

Astera Labs jumped 15.60% after it debuted a new family of data center switches built specifically for AI.

Helen of Troy soared 17.88% thanks to a stronger-than-expected earnings report from the struggling consumer goods manufacturer.

Arcadium Lithium continued to rocket higher today after mining behemoth Rio Tinto announced it’s buying the lithium miner for $5.85 per share. Arcadium shares rose 30.90%.

Stocks down

Boeing just can’t catch a break: Talks with striking machinists broke down and the airplane manufacturer withdrew its recent contract offer. Shares sank 3.41% on the news.

US-traded shares of German life sciences company Bayer dropped 6.96% after a US court decided it will hear arguments that products from Bayer brand Monsanto allegedly harmed people.

Trump Media & Technology Group finally settled down after a wild rally following a wild rally in Pennsylvania featuring Elon Musk, falling 5.64% today.

The S&P 500® index (SPX) rose 40.91 points (0.71%) to 5,792.04, a new record-high close; the Dow Jones Industrial Average® ($DJI) added 431.63 points (1.03%) to 42,512.00, also a new closing high; and the NASDAQ Composite® ($COMP) increased 108.70 points (0.60%) to 18,291.62.

The 10-year Treasury note yield (TNX) climbed three basis points to 4.06%, the highest since late July.

In 2023, about 36% of Hispanic or Latino candidates waiting for a transplant received one, compared to 58% of non-Hispanic white candidates, according to the US Department of Health and Human Services Office of Minority Health.

Stat: $1.8 trillion. That eye-watering number is the federal budget deficit as of September 30th, according to the Congressional Budget Office. Higher interest rates, and increases in Social Security and Medicare, are driving the budget gap. (the Wall Street Journal)

Posted on October 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

By Staff Reporters

***

***

STOCKHOLM (AP) — Two scientists won the Nobel Prize in physiology or medicine on Monday for their discovery of microRNA, tiny bits of genetic material that offer a way for scientists to control what’s happening in our cells and that could lead to new ways of detecting and treating diseases including cancer. The work by Americans Victor Ambros and Gary Ruvkun is “proving to be fundamentally important for how organisms develop and function,” according to a panel that awarded the prize in Stockholm.