BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Population health has been defined as “the health outcomes of a group of individuals, including the distribution of such outcomes within the group”. It is an approach to health that aims to improve the health of an entire human population or cohort. http://www.HealthDictionarySeries.org

History

In fact, the nominal “father of population health” is colleague and Dean David B. Nash MD MBA of Jefferson Medical School in Philadelphia. And, although I attended Temple University down the street, David still wrote the Foreword to my textbook years later; Financial Management Strategies for Hospitals and Healthcare Organizations [Tools, Techniques, Checklists and Case Studies].

Now age, income, location, race, gender and education are just a few characteristics that differentiate the world’s population. These are called ”disparities” and they have a major impact on people’s lives; especially their healthcare. And, I’ve written about them before. Perform a ME-P “search” for more.

So, it’s only natural that we’re keeping an eye on two major demographic trends: aging baby boomers and maturing Millennials [1982-2002 approximately].

Why it’s important

The impact of large population shifts propagate throughout an economy benefitting certain sectors more than others and influencing a country’s growth prospects; tantalizing investing ideas?

Example:

For example, as baby boomers retire, we’ll likely see higher spending on health care, but less on education and raising children. Likewise, tech-savvy Millennials will likely prioritize consumption on experiences over cars and houses [leading economic indicator].

So, can we profit from these trends?

Assessment

Well maybe – maybe not! Overall economic prospects may not be completely affected by these trends. Spending habits on combined goods and services will shift, rather than rise or decline.

So, be careful. What matters most for your investment success is your demographics and investing according to your personal circumstances and goals [paradox-of-thrift].

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Most all investors and physician executives are aware of the concept of financial beta.

BETA: A Systemic risk measurement benchmark correlating with a change in a specific index.

EXAMPLE: The measure of a stock’s volatility relative to the market, where a beta lower than 1 means the stock is less sensitive than the market as a whole; higher than 1 indicates the stock is more volatile than the market. The healthcare industry is considered to be increasingly volatile and hence possess a higher beta.

An acute care inpatient hospital is a health care organization or “anchor hospital” in which a patient is treated for an acute (immediate and severe) episode of illness or the subsequent treatment of injuries related to an accident or trauma, or during recovery from surgery. Specialized personnel using complex and sophisticated technical equipment and materials usually render acute professional care in a hospital setting. Unlike chronic care, acute care is often necessary for only a short time. Measures of acute health care utilization are represented by three separate rates:

Rate of admissions per 1000 patients.

Average length of stay per admission.

Total days of care per 1000 patients.

***

***

Psychiatric Hospital

A psychiatric hospital (behavioral health, mental hospital, or asylum) specializes in the treatment of patients with mental illness or drug-related illness or dependencies. Psychiatric wards differ only in that they are a unit of a larger hospital.

Specialty Hospital

A specialty hospital is a type of health care organization that has a limited focus to provide treatment for only certain illnesses such as cardiac care, orthopedic or plastic surgery, elder care, radiology / oncology services, neurological care, or pain management cases. These organizations are often owned by doctors who refer patients to them. In recent years, single-specialty hospitals have emerged in various locations in the United States. Instead of offering a full range of inpatient services, these hospitals focus on providing services relating to a single medical specialty or cluster of specialties.

Long-Term Care Hospital

A long-term care hospital is an entity that provides assistance and patient care for the activities of daily living (ADLs), including reminders and standby help for those with physical, mental, or emotional problems. This includes physical disability or other medical problems for 3 months or more (90 days). The criteria of five ADLs may also be used to determine the need for help with the following: meal preparation, shopping, light housework, money management, and telephoning. Other important considerations include taking medications, doing laundry, and getting around outside.

Rural Hospital

The parameters of a rural hospital are determined based on distance. A rural hospital is defined as a hospital serving a geographic area 10 or more miles from the nexus of a population center of 30,000 or more.

More specifically, a rural hospital means an entity characterized by one of the following:

Type A rural hospital—small and remote, has fewer than 50 beds, and is more than 30 miles from the nearest hospital

Type B rural hospital—small and rural, has fewer than 50 beds, and is 30 miles or less from the nearest hospital

Type C rural hospital—considered rural and has 50 or more beds

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Dr. David Edward Marcinko works with doctors, nurses, technicians and healthcare professionals who struggle with professional disillusionment, burnout, financial distress and an unbalanced life–all of which can happen at any stage of a medical career. Through our coaching sessions, medical and healthcare professionals can achieve a more meaningful, purposeful, and flourishing life.

With the PP-ACA, increased compliance regulations and higher tax rates impending from the Biden administration – not to mention the corona pandemic, venture capital based healthcare corporations and telehealth – physicians are more concerned about their retirement and retirement planning than ever before; and with good reason. After payroll taxes, dividend taxes, limited itemized deductions, the new 3.8% surtax on net investment income and an extra 0.9% Medicare tax, for every dollar earned by a high earning physician, almost 50 cents can go to taxes!

Introduction

Retirement planning is not about cherry picking the best stocks, ETFs or mutual funds or how to beat the short term fluctuations in the market. It’s a disciplined long term strategy based on scientific evidence and a prudent process. You increase the probability of success by following this process and monitoring on a regular basis to make sure you are on track.

General Surveys

According to a survey from the Employee Benefit Research Institute [EBRI] and Greenwald & Associates; nearly half of workers without a retirement plan were not at all confident in their financial security, compared to 11 percent for those who participated in a plan, according to the 2014 Retirement Confidence Survey (RCS).

In addition, 35 percent of workers have not saved any money for retirement, while only 57 percent are actively saving for retirement. Thirty-six percent of workers said the total value of their savings and investments—not including the value of their home and defined benefit plan—was less than $1,000, up from 29 percent in the 2013 survey. But, when adjusted for those without a formal retirement plan, 73 percent have saved less than $1,000.

Debt is also a concern, with 20 percent of workers saying they have a major problem with debt. Thirty-eight percent indicate they have a minor problem with debt. And, only 44 percent of workers said they or their spouse have tried to calculate how much money they’ll need to save for retirement. But, those who have done the calculation tend to save more.

The biggest shift in the 24 years has been the number of workers who plan to work later in life. In 1991, 84 percent of workers indicated they plan to retire by age 65, versus only 9 percent who planned to work until at least age 70. In 2014, 50 percent plan on retiring by age 65; with 22 percent planning to work until they reach 70.

Physician Statistics

Now, compare and contrast the above to these statistics according to a 2018 survey of physicians on financial preparedness by American Medical Association [AMA] Insurance. The statistics are still alarming:

The top personal financial concern for all physicians is having enough money to retire.

Only 6% of physicians consider themselves ahead of schedule in retirement preparedness.

Nearly half feel they were behind

41% of physicians average less than $500,000 in retirement savings.

Nearly 70% of physicians don’t have a long term care plan.

Only half of US physicians have a completed estate plan including an updated will and Medical directives.

Thoughts to Ponder

And so, to help make your golden years comfortable and worry free, here are ten important retirement questions for all physicians to consider:

How much money do you need to retire?

What is your retirement cash flow?

What is your retirement vision?

How to stay on retirement track?

How to maximize retirement plan contributions such as 401(k) or 403(b)?

How to maximize retirement income from retirement plans?

What are some other retirement plan savings options?

What is your retirement plan and investing style?

What is the role of social security in retirement planning?

How to integrate retirement with estate planning?

The opinion of a competent Certified Medical Planner® can assist.

ASSESSMENT: Your thoughts, comments and input are appreciated.

An important issue facing the world of medicine and health care is the field’s lack of diversity, especially regarding African American doctors. African Americans made up 6% of all physicians in the U.S. in 2008, 6.9% of enrolled medical students in 2013 and 7.3% of all medical school applicants.

The existing literature on the lack of diversity within the medical field emphasizes the role that inclusion would play in closing the health disparities among racial groups and the benefits acquired by African Americans through better patient-doctor interactions and further respect for cultural sensitivity. A large portion of current research regarding Black medical students and education focuses on why minority students do not go into medical school or complete their intended pre-med degrees.

Common notions and conclusions are that many institutions do not properly prepare and support students, who despite drive and desire, may lack adequate high school preparation and may go through additional stress unlike their other peers. Historically Black Colleges and Universities (HBCUs) are institutions that were designed to support African American students by providing an educational learning environment that caters to their unique challenges and cultural understandings. Given that HBCUs have had much success in preparing minority students for STEM fields, and for medical school success more specifically, this article looks at the history of such universities in the context of medical education, their effective practices, the challenges faced by African Americans pursing medical education, and what they can do in the future to produce more Black doctors.

We also highlight the work of Xavier University and Prairie View A&M University, institutions that regularly rank among the top two and top ten producers, respectively, of future African American doctors among colleges and universities.

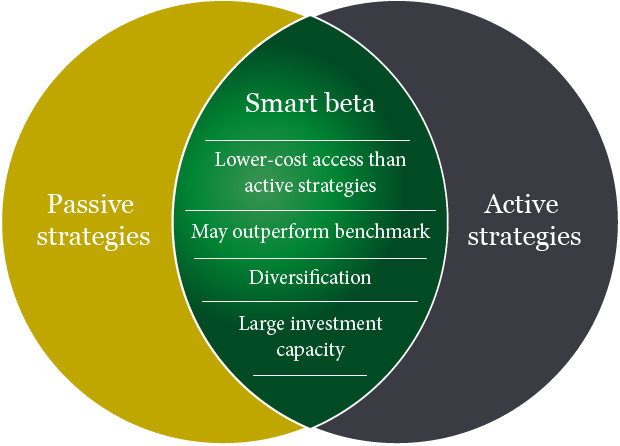

Offering a blend of active and passive styles of management, a smart beta portfolio is low cost due to the systematic nature of its core philosophy – achieving efficiency by way of tracking an underlying index (e.g., MSCI World Ex US). Combining with optimization techniques traditionally used by active managers, the strategy aims at risk/return potentials that are more attractive than a plain vanilla active or passive product.

Originally theorized by Harry Markowitz in his work on Modern Portfolio Theory (MPT), smart beta is a response to a question that forms the basis of MPT – how to best construct the optimally diversified portfolio. Smart beta answers this by allowing a portfolio to expand on the efficient frontier (post-cost) of active and passive. As a typical investor owns both the active and index fund, most would benefit from adding smart beta exposure to their portfolio in addition to their existing allocations.

Assessment: The smart beta approach is an arguably perfect intersection between traditional value investing and the efficient market hypothesis. But, is it worth the cost?

Disposablecredit cards are the newest innovation to help reduce fraud and assumed identity scams on e-commerce based websites. As with traditional credit cards, these cards are numbered, but used only once. Then, electronically they are erased so that there is nothing left in the merchant’s database for hackers to steal.

But, in 2014, Congress began looking at new ways to keep personal credit card information safe after several high-profile security breaches at some of America’s top retailers.

WHY? Current credit cards use easy to hack magnetic strip technology from the 1960s. Many consumers want more secure “pin & chip” cards which have been in use in Europe for years. Even though micro-chip technology costs billions to implement, merchants are moving in that direction as they issue new cards to consumers. Most modern polls show nearly half of all people surveyed are extremely concerned about the safety of their personal credit card information.

Burner Cards: Similar to a burner phone or “throwaway” social media account, burner credit cards are temporary, virtual credit cards that are not your “main” credit card. The bank or burner card app will give you a temporary number that links back to your main credit card which you can use for online purchases.

An ANonymousCreditCard provides an extreme degree of privacy and prevents the tracking of your expenses by a spouse, people with bad intentions or government monitoring agencies. It is important to realize that there are plenty of legitimate reasons for wanting to buy something discreetly through an AnonymousCreditCard.

Credit Card Mistakes to Avoid

No number has as far-reaching an impact on your money as your credit scores.

Here are some obstacles, physicians and all of us, should dodge on the road to financial security:

If you are denied a credit card, you have the right to obtain a credit report free from the agency which denied you. Your request must be made in writing and within thirty-sixty days. Consumer credit is governed by the Fair Credit Reporting Act (FCRA). The regulations are issued by and enforced by the Federal Trade Commission. Certain states offer consumers additional rights. Credit reporting agencies are referred to as a “consumer reporting agency”.

No, I’m not talking about creepy, crawly insects. I’m referring to Standard & Poor’s Depository Receipts (SPDRs, or spiders), a derivative product, which combines many of the advantages of index funds with the superior trading flexibility of common stocks.

Creation

SPDRs were created in January 1993 by the American Stock Exchange. SPDRs are units in a trust holding the S&P 500 securities in proportion to their index weighting and which are adjusted as necessary to track changes made to the index by S&P. They pay quarterly cash dividend distributions based on the accumulated dividends paid by the stocks held in the SPDR trust minus an annual fee of about .19% of principal to cover trust expenses. They trade at approximately one-tenth the value of the index.

Conclusion

And so, your thoughts and comments on this ME-P are appreciated. Do you use SPDRs; why or why not? Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed: And, credible sponsors and like-minded advertisers are always welcomed.

Beside market, limit and stop orders, there are some other miscellaneous orders for the physician or guided investor, to know:

A stop limit order is a stop order that, once triggered or activated, becomes a limit order. Realize that it is possible for a stop limit to be triggered and not executed, as the limit price specified by the doctor may not be available.

In addition, there are all or none and fill or kill orders, and even though both require the entire order to be filled, there are distinct differences. An all or none (AON) is an order in which the broker is directed to fill the entire order or none of it.

A fill or kill (FOK) is an order either to buy or to sell a security in which the broker is directed to attempt to fill the entire’ amount of the order immediately and in full, or that it be canceled.

The difference between an all or none and a fill or kill order is that with an all or none order, immediate execution is not required, while immediate execution is a critical component of the fill or kill. Because of the immediacy requirement,

FOK orders are never found on the specialist’s book. Another difference is that AON orders are only permitted for bonds, not stocks, while FOK orders may be used for either.

Also, there exists an immediate or cancel order (IOC), which is an order to buy or sell a security in which the broker is directed to attempt to fill immediately as much of the order as possible and cancel any part remaining. This type of order differs from a fill-or-kill order which requires the entire order to be filled. An IOC order will permit a partial fill. Because of the immediacy requirement, IOC and FOK orders are never found on the specialist’s book.

Long and Short Positions

A long buy position means that shares are for sale from a market makers inventory or owned by the medical investor outright. Market makers take long positions when customers and other firms wish to sell, and they take short positions when customers and other firms want to buy in quantities larger than the market maker’s inventory. By always being ready, willing, and able to handle orders in this way, market makers assure the investing public of a ready market in the securities in which they are interested. When a security can be bought and sold at firm prices very quickly and easily the security is said to have a high degree of liquidity, also known as marketability.

A short position investor seeks to make a profit by participating in the decline in the market price of a security.

Now; let’s see how these terms, long and short, apply to transactions by medical investors [rather than market makers] in the securities markets.

When a doctor buys any security – he is said to be taking a long position in that security. This means the investor is an owner of the security. Why does a doctor take a long position in a security? Well, receiving dividend income to make a profit from an increase in the market price is one reason. Once the security has risen sufficiently in price to satisfy the investor’s profit needs, the investor will liquidate his long position, or sell his stock. This would officially be known as a long sale of stock, though few people in the securities business use the label “long sale”. This is the manner in which the above investor had made a profit is the traditional method used; buy low, sell high.

Let’s look at an actual investment in General Motors to investigate this principle further. A medical investor has taken a long position in 100 shares of General Motors stock at a price of $70 per share. This means that the manner in which he can do that is by placing a market order which will be executed at the best “available market price at the time, or by the placing of a buy limit order with a limit price of $70 per share. The investor firmly believes, on the basis of reports that he has read about the automobile industry and General Motors specifically, that at $70 a share, General Motors is a real bargain. He believes that based on its current level of performance, it should be selling for a price of between $80 and $85 per share. But, the doctor investor has a dilemma. He feels certain that the price is going to rise but he cannot watch his computer, or call his broker, every hour of every day. The reason he can’t watch is because patients have to be seen in the office. The only people who watch a computer screen all day are those in the offices of brokerage firms (stock broker registered representatives), and doctor day traders, among others.

In the above example, with a sell limit order, if the doctor investor was willing to settle for a profit of $12 per share, what order would he place at this time? If you said, “sell at $82 good ’til canceled”, you are correct. Why GTC rather than a day order? Because our doctor investor knows that General Motors is probably not going to rise from $70 to $82 in one day. If he had placed an order to sell at $82 without the GTC qualification, his order would have been canceled at the end of this trading day. He would have had to re-enter the order each morning until he got an execution at 82. Marking the order GTC (or open) relieves him of any need to replace the order every morning. Several weeks later, when General Motors has reached $82 per share in the market, his order to sell at 82 is executed. The medical investor has bought at 70 and sold at 82 and realized a $12 per share profit for his efforts.

Let’s suppose that the medical investor, who has just established a $12 per share profit, has evaluated the performance of General Motors common stock by looking at the market performance over a period of many years. Let’s further assume that the investor has found by evaluating the market price statistics of General Motors that the pattern of movement of General Motors is cyclical. By cyclical, we mean that it moves up and down according to a regular pattern of behavior.

Let’s say the investor has observed that in the past, General Motors had repeated a pattern of moving from prices in the $60 per share range as a low, to a high of approximately $90 per share. Further, our investor has observed that this pattern of performance takes approximately 10 to l2 months to do a full cycle; that is, it moves from about 60 to about 90 and back to about 60 within a period of roughly l2 months. If this pattern repeats itself continually, the investor would be well advised to buy the stock at prices in the low to mid 60’s hold onto it until it moves well into the 80’s, and then sell his long position at a profit. However, what this means is that our investor is going to be invested in General Motors only 6 months of each year. That is, he will invest when the price is low and, usually within half a year, it will reach its high before turning around and going back to its low again. How can the doctor-investor make a profit not only on the rise in price of General Motors in the first 6 months of the cycle, but on the fall in price of General Motors in the second half of the cycle? One technique that is available is the use of the short sale.

The Short Sale

If a doctor investor feels that GM is at its peak of $ 90 per share, he may borrow 100 shares from his brokerage firm and sell the 100 shares of borrowed GM at $ 90. This is selling stock that is not owned and is known as a short sale. The transaction ends when the doctor returns the borrowed securities at a lower price and pockets the difference as a profit. In this case, the doctor investor has sold high, and bought low.

Odd Lots

Most of the thousands of buy and sell orders executed on a typical day on the NYSE are in 100 share or multi-100 share lots. These are called round lots. Some of the inactive stocks traded at post 30, the non-horseshoe shaped post in the northwest corner of the exchange, are traded in 70 share round lots due to their inactivity. So, while a round lot is normally 700 shares, there are cases where it could be 10 shares. Any trade for less than a round lot is known as an odd lot. The execution of odd lot orders is somewhat different than round lots and needs explanation.

When a stock broker receives an odd lot order from one of his doctor customers, the order is processed in the same manner as any other order. However, when it gets to the floor, the commission broker knows that this is an order that will not be part of the regular auction market. He takes the order to the specialist in that stock and leaves the order with the specialist. One of the clerks assisting the specialist records the order and waits for the next auction to occur in that particular stock. As soon as a round lot trade occurs in that particular stock as a result of an auction at the post, which may occur seconds later, minutes later, or maybe not until the next day, the clerk makes a record of the trade price.

Every odd lot order that has been received since the last round lot trade, whether an order to buy or sell, is then executed at the just noted round lot price, the price at which the next round lot traded after receipt of the customer’s odd lot order, plus or minus the specialist’s “cut “. Just like everything else he does, the specialist doesn’t work for nothing. Generally, he will add 1/8 of a point to the price per share of every odd lot buy order and reduce the proceeds of each odd lot sale order by 1/8 per share. This is the compensation he earns for the effort of breaking round lots into odd lots. Remember, odd lots are never auctioned but, there can be no odd lot trade unless a round lot trades after receipt of the odd lot order.

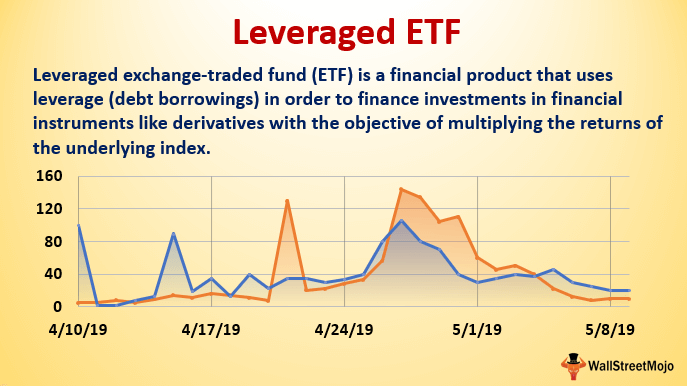

Leveraged ETFs have received tremendous media attention and are proving to be extremely popular with both individual and institutional investors. There are hundreds of leveraged ETFs, covering virtually every asset class and industry sector. The majority are double-leveraged, but there’s a sizeable group of triple-leveraged ETFs.

For professional investors, leveraged ETFs are useful in statistical arbitrage, short-term tactical strategies, and for use as short-term hedges without the need to roll futures. For individual investors, leveraged ETFs are alluring because of the potential for higher returns.

Now, some physicians and Uninformed investors might assume that the leverage returns are generated on a continuous basis, so that if an underlying index is up 5% for a month, the double-leveraged ETF will be up 10% for the same month; if the index is up 10% for 6 months, the ETF will be up 20%, and so forth. That is absolutely not the case. The leverage is determined on a daily basis and the returns for any other period usually will not be double or triple the underlying index.

In order for the leveraged funds to achieve appropriate levels of assets so they can provide their implied leverage, they have to rebalance daily. In the case of an ETF providing long 2-times leveraged exposure, they would typically attain exposure to a notional set of assets equal to 2 times their NAV.

Example: An example would be an ETF that takes in 100 units in assets that does a swap with a counterparty to provide exposure to 200 units in performing assets. The rebalancing activity of these funds will almost always be in the same direction as the market.

In essence, a leveraged ETF is essentially marked to market every night. It starts with a clean slate the next day, almost as if the previous day had not existed. This process produces daily leverage results. However, over time, the compounding of this reset can potentially vary the performance of the fund versus its underlying benchmark. This can result in either greater or lesser degrees of final leverage over individual holding periods.

Financial ratio analysis typically involves the calculation of ratios that are financial and operational measures representative of the financial status of a clinic or medical practice enterprise. These ratios are evaluated in terms of their relative comparison to generally established industry norms, which may be expressed as positive or negative trends for that industry sector. The ratios selected may function as several different measures of operating performance or financial condition of the subject entity.

Common types of financial indicators that are measured by ratio analysis include:

Liquidity. Liquidity ratios measure the ability of an organization to meet cash obligations as they become due, i.e., to support operational goals. Ratios above the industry mean generally indicate that the organization is in an advantageous position to better support immediate goals. The current ratio, which quantifies the relationship between assets and liabilities, is an indicator of an organization’s ability to meet short-term obligations. Managers use this measure to determine how quickly assets are converted into cash.

Activity. Activity ratios, also called efficiency ratios, indicate how efficiently the organization utilizes its resources or assets, including cash, accounts receivable, salaries, inventory, property, plant, and equipment. Lower ratios may indicate an inefficient use of those assets.

Leverage.Leverage ratios, measured as the ratio of long-term debt to net fixed assets, are used to illustrate the proportion of funds, or capital, provided by shareholders (owners) and creditors to aid analysts in assessing the appropriateness of an organization’s current level of debt. When this ratio falls equal to or below the industry norm, the organization is typically not considered to be at significant risk.

Profitability. Indicates the overall net effect of managerial efficiency of the enterprise. To determine the profitability of the enterprise for bench marking purposes, the analyst should first review and make adjustments to the owner(s) compensation, if appropriate. Adjustments for the market value of the “replacement cost” of the professional services provided by the owner are particularly important in the valuation of professional medical practices for the purpose of arriving at an ”economic level” of profit.

The selection of financial ratios for analysis and comparison to the organization’s performance requires careful attention to the homogeneity of data. Bench marking of intra-organizational data (i.e., internal bench marking) typically proves to be less variable across several different measurement periods.

However, the use of data from external facilities for comparison may introduce variation in measurement methodology and procedure. In the latter case, use of a standard chart of accounts for the organization or recasting the organization’s data to a standard format can effectively facilitate an appropriate comparison of the organization’s operating performance and financial status data to survey results.

Posted on August 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Update on Some Interesting and Important Financial Calculations

By Timothy J. McIntosh MBA CFP® MPH

By Dr. David Edward Marcinko MBA MEd CMP™

By Jeffrey S. Coons PhD CFA

-INTRODUCTION-

Performance measurement, like an annual physical, is an important feedback loop to monitor progress towards the goals of the medical professional’s investment program. Performance comparisons to market indices and/or peer groups are a useful part of this feedback loop, as long as they are considered in the context of the market environment and with the limitations of market index and manager database construction.

Inherent to performance comparisons is the reality that portfolios taking greater risk will tend to out-perform less risky investments during bullish phases of a market cycle, but are also more likely to under-perform during the bearish phase. The reason for focusing on performance comparisons over a full market cycle is that the phases biasing results in favor of higher risk approaches can be balanced with less favorable environments for aggressive approaches to lessen/eliminate those biases.

So, as physicians and other investors, can we eliminate the biases of the market environment by adjusting performance for the risk assumed by the portfolio? While several interesting calculations have been developed to measure risk-adjusted performance, the unfortunate answer is that the biases of the market environment still tend to have an impact even after adjusting returns for various measures of risk.

However, medical professionals and their advisors will have many different risk-adjusted return statistics presented to them, so understanding the Sharpe ratio, Treynor ratio, Jensen’s measure or alpha, Morningstar star ratings, etc. and their limitations should help to improve the decisions made from the performance measurement feedback loop.

[a] The Treynor Ratio

The Treynor ratio measures the excess return achieved over the risk free return per unit of systematic risk as identified by beta to the market portfolio. In practice, the Treynor ratio is often calculated using the T-Bill return for the risk-free return and the S&P 500 for the market portfolio.

[b] The Sharpe Ratio

The Sharpe ratio, named after CAPM pioneer William F. Sharpe, was originally formulated by substituting the standard deviation of portfolio returns (i.e., systematic plus unsystematic risk) in the place of beta of the Treynor ratio. Thus, a fully diversified portfolio with no unsystematic risk will have a Sharpe ratio equal to its Treynor ratio, while a less diversified portfolio may have significantly different Sharpe and Treynor ratios.

***

8

***

[c] The Jensen Alpha Measure

The Jensen measure, named after CAPM research Michael C. Jensen, takes advantage of the CAPM equation discussed in the Portfolio Management section to identify a statistically significant excess return or alpha of a portfolio. The essential idea is that to investigate the performance of an investment manager you must look not only at the overall return of a portfolio, but also at the risk of that portfolio.

For instance, if there are two mutual funds that both have a 12 percent return, a lucid investor will want the fund that is less risky. Jensen’s gauge is one of the ways to help decide if a portfolio is earning the appropriate return for its level of risk. If the value is positive, then the portfolio is earning excess returns. In other words, a positive value for Jensen’s alpha means a fund manager has “beat the market” with his or her stock picking skills compared with the risk the manager has taken.

[d] Database Ratings

The ratings given to mutual funds by databases, such as Morningstar, and various financial magazines are another attempt to develop risk-adjusted return measures. These ratings are generally based on a ranking system for funds calculated from return and risk statistics.

A popular example is Morningstar’s star ratings, representing a weighting of three, five and ten year risk/return ratings. This measure uses a return score from cumulative excess monthly fund returns above T-Bills and a risk score derived from the cumulative monthly return below T-Bills, both of which are normalized by the average for the fund’s asset class. These scores are then subtracted from each other and funds in the asset class are ranked on the difference. The top 10 percent receive five stars, the next 22.5 percent get four stars, the subsequent 35 percent receive three stars, the next 22.5 percent receive two stars, and the remaining 10 percent get one star.

***

***

Assessment

Unfortunately, these ratings systems tend to have the same problems of consistency and environmental bias seen in both non-risk adjusted comparisons over 3 and 5 year time periods and the other risk-adjusted return measures discussed above. The bottom line on performance measurement is that the medical professional should not take the easy way out and accept independent comparisons, no matter how sophisticated, at face value. Returning to our original rules-of-thumb, understanding the limitations of performance statistics is the key to using those statistics to monitor progress towards one’s goals.

This requires an understanding of performance numbers and comparisons in the context of the market environment and the composition/construction of the indices and peer group universes used as benchmarks.

Another important rule-of-thumb is to avoid projecting forward historical average returns, especially when it comes to strong performance in a bull market environment. Much of an investment or manager’s performance may be environment-driven, and environments can change dramatically.

Channel Surfing

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input.

ABOUT

Timothy J. McIntosh is Chief Investment Officer and founder of SIPCO. As chairman of the firm’s investment committee, he oversees all aspects of major client accounts and serves as lead portfolio manager for the firm’s equity and bond portfolios. Mr. McIntosh was a Professor of Finance at Eckerd College from 1998 to 2008. He is the author of The Bear Market Survival Guideand the The Sector Strategist. He is featured in publications like the Wall Street Journal, New York Times, USA Today, Investment Advisor, Fortune, MD News, Tampa Doctor’s Life, and The St. Petersburg Times. He has been recognized as a Five Star Wealth Manager in Texas Monthly magazine; and continuously named as Medical Economics’ “Best Financial Advisors for Physicians since 2004. And, he is a contributor to SeekingAlpha.com., a premier website of investment opinion. Mr. McIntosh earned a Bachelor of Science Degree in Economics from Florida State University; Master of Business Administration (M.B.A) degree from the University of Sarasota; Master of Public Health Degree (M.P.H) from the University of South Florida and is a CERTIFIED FINANCIAL PLANNER® practitioner. His previous experience includes employment with Blue Cross/Blue Shield of Florida, Enterprise Leasing Company, and the United States Army Military Intelligence.

Dr. Jeffrey S. Coons is the Co-Director of Research at Manning & Napier Advisors, Inc. with primary responsibilities focusing on the measurement and management of portfolio risk and return relative to client objectives. This includes providing analysis across every aspect of the investment process, from objectives setting and asset allocation to on-going monitoring of portfolio risk and return. Dr. Coons is also member of the Investment Policy Group, which establishes and monitors secular investment trends, macroeconomic overviews, and the investment disciplines of the firm. Dr. Coons holds a doctoral degree in economics from Temple University, graduated with distinction from the University of Rochester with a B.A. in Economics, holds the designation of Chartered Financial Analyst, and is one of the employee-owners of Manning and Napier.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on July 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Update on Some Interesting and Important Financial Calculations

By Timothy J. McIntosh MBA CFP® MPH

By Dr. David Edward Marcinko MBA MEd CMP™

By Jeffrey S. Coons PhD CFA

-INTRODUCTION-

Performance measurement, like an annual physical, is an important feedback loop to monitor progress towards the goals of the medical professional’s investment program. Performance comparisons to market indices and/or peer groups are a useful part of this feedback loop, as long as they are considered in the context of the market environment and with the limitations of market index and manager database construction.

Inherent to performance comparisons is the reality that portfolios taking greater risk will tend to out-perform less risky investments during bullish phases of a market cycle, but are also more likely to under-perform during the bearish phase. The reason for focusing on performance comparisons over a full market cycle is that the phases biasing results in favor of higher risk approaches can be balanced with less favorable environments for aggressive approaches to lessen/eliminate those biases.

So, as physicians and other investors, can we eliminate the biases of the market environment by adjusting performance for the risk assumed by the portfolio? While several interesting calculations have been developed to measure risk-adjusted performance, the unfortunate answer is that the biases of the market environment still tend to have an impact even after adjusting returns for various measures of risk.

However, medical professionals and their advisors will have many different risk-adjusted return statistics presented to them, so understanding the Sharpe ratio, Treynor ratio, Jensen’s measure or alpha, Morningstar star ratings, etc. and their limitations should help to improve the decisions made from the performance measurement feedback loop.

[a] The Treynor Ratio

The Treynor ratio measures the excess return achieved over the risk free return per unit of systematic risk as identified by beta to the market portfolio. In practice, the Treynor ratio is often calculated using the T-Bill return for the risk-free return and the S&P 500 for the market portfolio.

[b] The Sharpe Ratio

The Sharpe ratio, named after CAPM pioneer William F. Sharpe, was originally formulated by substituting the standard deviation of portfolio returns (i.e., systematic plus unsystematic risk) in the place of beta of the Treynor ratio. Thus, a fully diversified portfolio with no unsystematic risk will have a Sharpe ratio equal to its Treynor ratio, while a less diversified portfolio may have significantly different Sharpe and Treynor ratios.

***

8

***

[c] The Jensen Alpha Measure

The Jensen measure, named after CAPM research Michael C. Jensen, takes advantage of the CAPM equation discussed in the Portfolio Management section to identify a statistically significant excess return or alpha of a portfolio. The essential idea is that to investigate the performance of an investment manager you must look not only at the overall return of a portfolio, but also at the risk of that portfolio.

For instance, if there are two mutual funds that both have a 12 percent return, a lucid investor will want the fund that is less risky. Jensen’s gauge is one of the ways to help decide if a portfolio is earning the appropriate return for its level of risk. If the value is positive, then the portfolio is earning excess returns. In other words, a positive value for Jensen’s alpha means a fund manager has “beat the market” with his or her stock picking skills compared with the risk the manager has taken.

[d] Database Ratings

The ratings given to mutual funds by databases, such as Morningstar, and various financial magazines are another attempt to develop risk-adjusted return measures. These ratings are generally based on a ranking system for funds calculated from return and risk statistics.

A popular example is Morningstar’s star ratings, representing a weighting of three, five and ten year risk/return ratings. This measure uses a return score from cumulative excess monthly fund returns above T-Bills and a risk score derived from the cumulative monthly return below T-Bills, both of which are normalized by the average for the fund’s asset class. These scores are then subtracted from each other and funds in the asset class are ranked on the difference. The top 10 percent receive five stars, the next 22.5 percent get four stars, the subsequent 35 percent receive three stars, the next 22.5 percent receive two stars, and the remaining 10 percent get one star.

***

***

Assessment

Unfortunately, these ratings systems tend to have the same problems of consistency and environmental bias seen in both non-risk adjusted comparisons over 3 and 5 year time periods and the other risk-adjusted return measures discussed above. The bottom line on performance measurement is that the medical professional should not take the easy way out and accept independent comparisons, no matter how sophisticated, at face value. Returning to our original rules-of-thumb, understanding the limitations of performance statistics is the key to using those statistics to monitor progress towards one’s goals.

This requires an understanding of performance numbers and comparisons in the context of the market environment and the composition/construction of the indices and peer group universes used as benchmarks.

Another important rule-of-thumb is to avoid projecting forward historical average returns, especially when it comes to strong performance in a bull market environment. Much of an investment or manager’s performance may be environment-driven, and environments can change dramatically.

Channel Surfing

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register.

ABOUT

Timothy J. McIntosh is Chief Investment Officer and founder of SIPCO. As chairman of the firm’s investment committee, he oversees all aspects of major client accounts and serves as lead portfolio manager for the firm’s equity and bond portfolios. Mr. McIntosh was a Professor of Finance at Eckerd College from 1998 to 2008. He is the author of The Bear Market Survival Guideand the The Sector Strategist. He is featured in publications like the Wall Street Journal, New York Times, USA Today, Investment Advisor, Fortune, MD News, Tampa Doctor’s Life, and The St. Petersburg Times. He has been recognized as a Five Star Wealth Manager in Texas Monthly magazine; and continuously named as Medical Economics’ “Best Financial Advisors for Physicians since 2004. And, he is a contributor to SeekingAlpha.com., a premier website of investment opinion. Mr. McIntosh earned a Bachelor of Science Degree in Economics from Florida State University; Master of Business Administration (M.B.A) degree from the University of Sarasota; Master of Public Health Degree (M.P.H) from the University of South Florida and is a CERTIFIED FINANCIAL PLANNER® practitioner. His previous experience includes employment with Blue Cross/Blue Shield of Florida, Enterprise Leasing Company, and the United States Army Military Intelligence.

Dr. Jeffrey S. Coons is the Co-Director of Research at Manning & Napier Advisors, Inc. with primary responsibilities focusing on the measurement and management of portfolio risk and return relative to client objectives. This includes providing analysis across every aspect of the investment process, from objectives setting and asset allocation to on-going monitoring of portfolio risk and return. Dr. Coons is also member of the Investment Policy Group, which establishes and monitors secular investment trends, macroeconomic overviews, and the investment disciplines of the firm. Dr. Coons holds a doctoral degree in economics from Temple University, graduated with distinction from the University of Rochester with a B.A. in Economics, holds the designation of Chartered Financial Analyst, and is one of the employee-owners of Manning and Napier.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on July 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Significance Often Under Appreciated

By Dr. David Edward Marcinko; MBA, MEd, CMP™

[Publisher-in-Chief]

As some MedicalExecutive-Post readers and subscribers are aware, hospitals that filed bankruptcy a decade ago include: a two-hospital system in Honolulu; one in Pontiac, MI; Trinity Hospital in Erin, Tennessee; Century City Doctors Hospital in Beverly Hills, and four hospital system Hospital Partners of America, in Charlotte. Today,

one can only wonder about the impact of Incurred But Not Reported claims on their plight?

IBNR Definition

According to the www.CertifiedMedicalPlanner.org, an IBNR claim is a concept that signifies healthcare services have been rendered but not invoiced or recorded by the healthcare provider, clinic, hospital, or organization.

Cause and Affect

IBNRs are usually the result of a commercial prospective payment risk contract between managed care organizations and healthcare providers, an IBNR claim refers to the estimated cost of medical services for which a claim has not been filed, or monitored by an IBNR collection systems or control sheet.

IBNR Types

More formally, IBNRs are a financial accounting of all services that have been performed but, as a result of a short period of time or “lag,” have not been invoiced or recorded. The medical services that will not be collected should be accounted for using the following accrued but not recorded (ABNR) entry:

Debit — accrued payments to medical providers or healthcare entity

Credit — IBNR accrual account

Example:

An example of an IBNR is hospital Coronary Artery Bypass Graft [CABG] surgery for a managed care plan member. Out of the capitated or prospective payment funds, the surgeon and/or healthcare organization has to pay for all related physical and respirator therapy, and rehabilitation services, as well as ancillary providers, drugs, and durable medical equipment [DME], as contractually obligated. This may also include complication diagnosis and extensive follow-up treatment.

Accordingly, the health plan will not be completely billed until several weeks, months, or quarters later or even further downstream in the reporting year after the patient is discharged. In order to accurately project the health plan’s financial liability, however, the health plan and hospital must estimate the cost of care based on past expenses.

Accounting Cost Controls

Since the identification and control of costs are paramount in financial healthcare management, an IBNR reserve fund (an interest bearing account) must be set up for claims that reflect services already delivered but, for whatever reason, not yet reimbursed.

From the accounting perspective, IBNR is accrued as an expense and is related as a short-term liability each fiscal month or accounting period.

Otherwise, the organization may not be able to pay the claim, if the associated revenue has already been spent. The proper handling of these “bills in the pipeline” is crucial for proactive providers and health organizations that are exploring arrangements that put them in the role of adjudicating claims or operating in a sub-capitated system.

###

###

Assessment

IBNRs are especially important with newer patients who may be sicker than prior norms.

Recoverables that hospitals post as part of their large reserve charges are also, in many cases, IBNR losses. They may be recorded as IBNR claims on their balance sheets. Once these losses start becoming actual losses, the hospital may look to the insurer to pay a part of the claim. This causes disputes between the payor, provider, and/or healthcare organization.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on June 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

“Correlation” has been used over the past twenty years by institutions, [physician] investors and financial advisors to assemble portfolios of moderate INVESTMENT risk

Modern Portfolio Theory approaches investing by examining the complete market and the full economy. MPT places a great emphasis on the correlation between investments.

DEFINITION: Correlation is a measure of how frequently one event tends to happen when another event happens. High positive correlation means two events usually happen together – high SAT scores and getting through college for instance. High negative correlation means two events tend not to happen together – high SATs and a poor grade record. No correlation means the two events are independent of one another.

In statistical terms two events that are perfectly correlated have a “correlation coefficient” of 1; two events that are perfectly negatively correlated have a correlation coefficient of -1; and two events that have zero correlation have a coefficient of 0.

In calculating correlation, a statistician would examine the possibility of two events happening together, namely:

If the probability of A happening is 1/X;

And the probability of B happening is 1/Y; then

The probability of A and B happening together is (1/X) times (1/Y), or 1/(X times Y).

There are several laws of correlation including;

Combining assets with a perfect positive correlation offers no reduction in portfolio risk. These two assets will simply move in tandem with each other.

Combining assets with zero correlation (statistically independent) reduces the risk of the portfolio. If more assets with uncorrelated returns are added to the portfolio, significant risk reduction can be achieved.

Combing assets with a perfect negative correlation could eliminate risk entirely. This is the principle with “hedging strategies”. These strategies are discussed later in the book.

In the real world, negative correlations are very rare. Most assets maintain a positive correlation with each other. The goal of a prudent investor is to assemble a portfolio that contains uncorrelated assets. When a portfolio contains assets that possess low correlations, the upward movement of one asset class will help offset the downward movement of another. This is especially important when economic and market conditions change.

As a result, including assets in your portfolio that are not highly correlated will reduce the overall volatility (as measured by standard deviation) and may also increase long-term investment returns. This is the primary argument for including dissimilar asset classes in your portfolio. Keep in mind that this type of diversification does not guarantee you will avoid a loss. It simply minimizes the chance of loss.

In this table provided by Ibbotson, the average correlation between the five major asset classes is displayed. The lowest correlation is between the U.S. Treasury Bonds and the EAFE (international stocks). The highest correlation is between the S&P 500 and the EAFE; 0.77 or 77 percent. This signifies a prominent level of correlation that has grown even larger during this decade. Low correlations within the table appear most with U.S. Treasury Bills.

It has been argued that physicians have abdicated the “moral high ground” in health care by their interest in seeking protection for their high incomes, their highly publicized self-referral arrangements, and their historical opposition toward reform efforts that jeopardized their clinical autonomy.

Experts Speak

In his book Medicine at the Crossroads, colleague and Emory University professor Melvin Konnor, MD noted that “throughout its history, organized medicine has represented, first and foremost, the pecuniary interests of doctors.” He lays significant blame for the present problems in health care at the doorstep of both insurers and doctors, stating that “the system’s ills are pervasive and all its participants are responsible.”

In order to reclaim their once esteemed moral position, physicians must actively reaffirm their commitment to the highest standards of the medical profession and call on other participants in the health care delivery system also to elevate their values and standards to the highest level.

Evolution

In the evolutionary shifts in models for care, physicians have been asked to embrace business values of efficiency and cost effectiveness, sometimes at the expense of their professional judgment and personal values. While some of these changes have been inevitable as our society sought to rein in out-of-control costs, it is not unreasonable for physicians to call on payers, regulators and other parties to the health care delivery system to raise their ethical bar.

Harvard University physician-ethicist Linda Emmanuel noted that “health professionals are now accountable to business values (such as efficiency and cost effectiveness), so business persons should be accountable to professional values including kindness and compassion.”

Within the framework of ethical principles, John La Puma, M.D., wrote in Managed Care Ethics, that “business’s ethical obligations are integrity and honesty. Medicine’s are those plus altruism, beneficence, non-maleficence, respect, and fairness.”

Incumbent in these activities is the expectation that the forces that control our health care delivery system, the payers, the regulators, and the providers will reach out to the larger community, working to eliminate the inequities that have left so many Americans with limited access to even basic health care.

Charles Dougherty clarified this obligation in Back to Reform, when he noted that “behind the daunting social reality stands a simple moral value that motivates the entire enterprise”.

ASSESSMENT

Health care is indeed grounded in caring. And, managing risk is a component of caring. It arises from a sympathetic response to the suffering of others.

Posted on June 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

VERY IMPORTANT PERSONS

By Dr. David Edward Marcinko MBAMEd CMP

***

VERY IMPORTANT PATIENTS

***

DEFINITION: “VIP syndrome” is a term coined in 1964 by the psychiatrist Walter Weintraub to describe an intriguing paradox: Throughout history, the rich and famous, with all their resources and fancy doctors, have often received worse medical treatment, and suffered from worse health outcomes, than the average person. When physicians afford “special privileges” to their powerful patients, from “Mad King” George III to Michael Jackson, they seem to get sicker and even die. While Weintraub, a psychoanalyst, attributed the problem in part to doctors unconsciously resenting their influential patients, it seems doctors simply get starstruck around famous people and high-ranking figures. Despite their medical expertise, these physicians find themselves opting out of basic tests for “privacy” or prescribing dangerous medications for “comfort.”

Unethical and illegal trading by specialists or market makers. A specialist may buy a stock for themselves from Dr. John Q. Public even though a better price is available from another seller. The specialist can view bid and ask prices and then manually mis-match them, or see ahead to a less favorable price. It happens in this editor’s experience, by observing how long it takes for a stop order to execute after the stop price was reached. This practice is a form of shimming. ***

Trading Imbalance

A situation where a large block of stock is put up for sale, but not enough buyers are available for purchase, and a market maker is unable to buy the imbalance. Lightly traded and tightly held stocks are considered temporarily illiquid during such imbalances. On occasion, a trading halt is put into place until enough buyers are available to purchase the deficit. On rare occasion, a handful of buyers can buy the stock at a huge discount if the stock was not halted during the imbalance. On the New York Stock Exchange, large stocks usually have a “delayed open” for such imbalances, as a trading specialist will fill the order by lining up buyers for the block, and then open trading for the stock for the day. ***

Triple Witching Hour

The final hour of trading on a Friday when stock index futures, stock index options, and stock options all expire. This happens on the third Friday in March, June, September, and December. See Quadruple Witching Hour. ***

A cognitive bias refers to a systematic pattern of deviation from norm or rationality in judgment, whereby inferences about other people and situations may be drawn in an illogical fashion. Individuals create their own “subjective social reality” from their perception of the input.

***

It is a re-emerging topic in investing and financial planning, today! Here are some examples.

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Colleagues know that I enjoy personal coaching and public speaking and give as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world. All in a Corona safe environment.

MARCINKO in the METAVERSE

These include lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, end-note lectures at city and statewide financial coalitions, and annual lectures for a variety of internal yearly meetings.

As human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist.

***

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often underperform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Posted on May 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

THE ENTREPRENEURIAL M.D.

In this episode we are joined by Dr. Brent Jackson, Chief Medical Officer for Mercy General in Sacramento, CA to discuss the physician life-cycle, burnout, and transitioning into leadership within healthcare.

On behalf of [Name of medical practice or clinic] (hereinafter called the “practice”), this letter sets out a proposed agreement for your initial employment in Dr. [Name of physician]’s medical practice. After both you and Dr. [Name of physician] have agreed upon all issues related to your employment, a formal physician employment agreement will be prepared for your review and signature.

1. Term: You will be an employee of the practice for an initial [Duration]-month period starting [Month, Date, Year]. Should you and the practice want to proceed past this initial employment period, an offer of co-ownership may be made to you as described in item nine below.

Your employment with the practice will essentially be “at will,” since you or the practice may voluntarily terminate it at any time upon 30 days’ written notice to the other. However, the following are conditions under which the practice may terminate your employment immediately: (a) upon your death or disability for three (3) consecutive months; (b) upon the suspension, revocation, or cancellation of your right to practice medicine in the State of [State]; (c) if you should lose privileges at any hospital at which the practice regularly maintains admission privileges; (d) should you fail or refuse to follow reasonable policies and directives established by the practice; (e) should you commit an act amounting to gross negligence or willful misconduct to the detriment of the practice or its patients; (f) if you are convicted of a crime involving moral turpitude, including fraud, theft, or embezzlement; and (g) if you breach any of the terms of your employment contract.

2. Compensation: Your salary for the initial 12-month period will be $[dollar value] and $[dollar value] in the second 12-month period, each year payable in monthly installments. You will also be entitled to an incentive bonus calculated as follows: [Percentage] % of your collected production when such collections exceeds $[dollar value] in the first year and $[dollar value] in the second year. The bonus each year will be calculated and paid on a semiannual basis. You will also be entitled to receive a one-time signing bonus of $[dollar value] if you sign your employment contract before [Month, Date, Year].

A portion of your compensation may be paid for by proceeds received from [Name of hospital] under the terms and conditions of a hospital recruitment agreement. The parties to this agreement will be the hospital and the practice only. However, forgiveness of any advances made by the hospital will be directly contingent upon the length of time you remain with the practice. Therefore, should your employment terminate for any reason, the practice will require you to repay to it any amounts the practice repays the hospital, in no matter what form, per the terms and conditions in the hospital recruitment agreement. [Note: Use this if the practice signs a hospital recruitment agreement with the hospital.]

3. Benefits: In addition to your base compensation and incentive bonus, the practice will pay for the following: (a) health insurance, (b) malpractice insurance, (c) continuing medical education (CME) costs, (d) medical license fee, (e) board certification exam fee, (f) reasonable cellular phone costs, and (g) a pager. You will also be entitled to a moving cost allowance for relocating to [Location.] You will be entitled to two weeks of paid vacation, 10 working days as paid sick leave, and four days paid time off for CME or the board certification exam.

4. Disability Leave: In case of absence because of your illness or injury, your base salary will continue for a period not exceeding 30 days per calendar year, plus any unused vacation time and sick leave. You will be entitled to any incentive bonus payments that may be due to you as collections are received on your prior production. Absence in excess of 30 days would be without pay. Unused sick leave cannot be carried over to succeeding years, nor will it be paid for at any time.

5. Exclusive Employment: As an employee, you will be involved full-time in the practice and you may not take any outside employment during the term of your employment agreement without the practice’s written approval. However, you will be entitled to keep compensation from honorariums, royalties, and copyrights if approved by the practice in writing. If the practice does not give approval, then the income from such activities shall remain the property of the practice.

6. Termination Compensation: Should your employment terminate for any reason, you will be entitled to accrued but unpaid base compensation, earned but unpaid incentive bonus, and unused vacation leave.

7.Non-Solicitation: During the course of your employment, the practice will introduce and make available to you its contacts and referring physician relationships, ongoing patient flow, general hospital sources, business and professional relationships, and the like. Since you have not been in private practice in the area previously, you acknowledge that you currently have no established patients following you. If there should be a termination, the practice will not restrict your ability to practice medicine in the area; however, it will require you to enter into a nonsolicitation agreement in which you agree not to solicit the employees of the practice nor its patients to follow you into your new medical practice. [Note: Insert Covenant Not to Compete here, if applicable.]

8. Employee-Only Status: During the term of your employment, you will not be required to contribute any money toward the practice’s equipment or operations, but likewise your work will give you no financial interest in the assets of the practice. However, the practice intends to offer you the opportunity to buy into the ownership of the practice as set forth in item 9 below.

9. Ownership Opportunity: At the end of your employment period, the practice will evaluate your relationship and may offer you the opportunity to become a co-owner in the practice (or enter into an office-sharing relationship). This offer is not mandatory and is at the total discretion of the practice. Should an offer not be tendered for some reason, the practice will wait until the end of your next 12-month employment period to decide whether to tender an offer of co-ownership. If an offer of co-ownership is made, Dr. [Name of physician] will discuss with you the following: (a) what percentage of the practice you will be allowed to acquire, (b) how best to value such interest, and (c) how you will pay for the acquisition of such interest. The practice hopes to achieve mutually agreeable solutions to these ownership issues.

We hope this offer meets with your approval. If so, please contact Dr. [Name of physician] as soon as possible. This letter is not intended to be a legally binding agreement; it is, rather, a tool to be used to prepare your formal physician employment agreement. If you should have any questions, please do not hesitate to contact myself or Dr. [Name of physician] at your convenience.

At Marcinko & Associates our clients traditionally includephysicians [MD, MBBS and DO], dentists [DDS and DMD], podiatrists [DPM], Registered Nurses [RNs], Certified Registered Nurse Anesthetists [CRNA], Physician Assistants [PA] and Nurse Practitioners [NP]. A growing cohort of clients include medical technologists, physical, speech and occupational therapists, etc.

The above are naturally segregated into three career tranches: 1. New practitioners, 2] Mid-Career practitioners and 3] Mature practitioners. We serve them all and are fully prepared for any special needs situation that may arise in any tranche [death, divorce, adverse risk event and/or bankruptcy, etc].

Marcinko & Associates understands the complexity of financial and non-financial deal terms because we are also doctors. Our “hard” knowledge of your business comes from being actual healthcare facility owners, operators and medical practitioners [with additional professional licenses and expertise] enabling us to effectively analyze your business, take corrective measures and present your healthcare entity in the best possible and accurate light.

***

But, if you’re looking at this website, chances are you are fed up, burned out, seeking practice management techniques or a better work-life balance. Or, you are looking for a new non-clinical career, thinking of finance, investing, retirement, or all of the above. Perhaps you are just looking to regain the joy and meaning in your medical or professional career? This is known as “soft” psychology, coaching, personal consulting or fraternal advice.

***

Regardless, of your “soft” personal or “hard” corporate needs, our transparent Fees for Service [FFS] model is moderated for all colleagues based on the acuity and urgency of their engagements. Reduced rates and/or limited charity work may also be possible.