BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

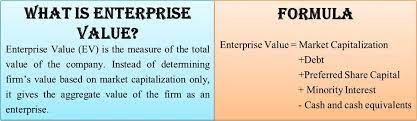

The enterprise value [EV] tends to be thought of as a theoretical takeover price if a company were to be bought. It is calculated as market capitalization plus debt, minority interest and preferred shares, minus total cash and cash equivalents.

Enterprise value = common equity at market value (this line item is also known as “market cap”) + debt at market value (here debt refers to interest-bearing liabilities, both long-term and short-term) + minority interest at market value, if any + preferred equity at market value + unfunded pension liabilities and other debt-deemed provisions – value of associate companies – cash and cash equivalents.

The stock markets have been near all time highs, lately. Physician colleagues and clients are so excited that they are even checking the overnight status of favorite stocks and/or the domestic/overseas markets.

Some colleagues are even becoming a bit OCD by checking the implied open of various markets the night before. But, what exactly is the Implied Open? How is it calculated?

DEFINITION: The Implied Open attempts to predict the prices at which various stock indexes will open, at 9:30am New York time. It is frequently shown on various cable television channels prior to the start of the next business day.

EXAMPLE: Considering the DJIA as an example, the basis of calculating implied open is the price of a “DJX index option futures contract”. This is not the price of the DJIA itself but rather the current ticker price of an option issued by the Chicago Board Options Exchange.

CBOE: The Chicago Board Options Exchange, located at 400 South LaSalle Street in Chicago, is the largest U.S. options exchange with annual trading volume that hovered around 1.27 billion contracts at the end of 2014. CBOE offers options on over 2,200 companies, 22 stock indices, and 140 exchange-traded funds.

NOTE: We would like to remind you that new amendments adopted by the U.S. Securities Exchange Commission (SEC) have gone into effect as of September 28, 2021. These amendments restrict the ability of market makers to publish OTC quotations for those companies that have not made required current financial and company information available to regulators and investors.

Posted on February 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Get ’em … While They are Hot!

By Ann Miller RN MHA

[ME-P Executive Director]

Just click on the book icon to order; get any one or all three! You’ll be glad you did.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Running a business involves a constant learning curve. And that applies whether you’re a rookie entrepreneur just starting out with a great idea for a new business or a more established small business owner with a quickly growing business that needs to expand. You should always be learning as a business owner, no matter where you are in your career—there’s always a new tool to master, new problems to solve, and new vocabulary to understand.

In order to not get totally overwhelmed, it’s helpful to take things one segment at a time. For instance, feeling confident when discussing the business’s financial needs should be a priority for every small business owner. After all, you represent the heart and soul of your business in the marketplace. So knowing the “language” of business finance is an integral part of your job as the owner.

The good news is that you don’t have to be an accountant or a financial planner to negotiate in the world of business finance. Here are some business terms and finance terms that will help you find your way to successful small business funding. https://www.youtube.com/embed/0kD4X2fgxGs

Business and Finance Terms to Know

From accounting, to business loans, to general business financial operations, here’s the ultimate list to all the business finance terms and definitions you need to know:

1. Accounts Payable

Accounts payable is a business finance 101 term. This represents your small business’s obligations to pay debts owed to lenders, suppliers, and creditors. Sometimes referred to as A/P or AP for short, accounts payable can be short or long term depending upon the type of credit provided to the business by the lender.

2. Accounts Receivable

Also known as A/R (or AR, good guess), accounts receivables is another business finance 101 term that means the money owed to your small business by others for goods or services rendered. These accounts are labeled as assets because they represent a legal obligation for the customer to pay you cash for their short-term debt.

3. Accrual Basis

The accrual basis of accounting is an accounting method of recording income when it’s actually earned and expenses when they actually occur. Accrual basis accounting is the most common approach used by larger businesses to record and maintain financial transactions.

4. Accruals

A business finance term and definition referring to expenses that have been incurred but haven’t yet been recorded in the business books. Wages and payroll taxes are common examples.

5. Asset

This business finance key term is anything that has value—whether tangible or intangible—and is owned by the business is considered an asset. Typical items listed as business assets are cash on hand, accounts receivable, buildings, equipment, inventory, and anything else that can be turned into cash.

6. Balance Sheet

Along with three other reports relating to the financial health of your small business, the balance sheet is essential information that gives a “snapshot” of the company’s net worth at any given time. The report is a summary of the business assets and liabilities.

7. Bookkeeping

A method of accounting that involves the timely recording of all financial transactions for the business.

8. Capital

Refers to the overall wealth of a business as demonstrated by its cash accounts, assets, and investments. Often called “fixed capital,” it refers to the long-term worth of the business. Capital can be tangible, like durable goods, buildings, and equipment, or intangible such as intellectual property.

9. Working Capital

Not to be confused with fixed capital, working capital is another business finance 101 term. It consists of the financial resources necessary for maintaining the day-to-day operation of the business. Working capital, by definition, is the business’s cash on hand or instruments that you can convert to cash quickly.

10. Cash Flow

Every business needs cash to operate. The business finance term and definition cash flow refers to the amount of operating cash that “flows” through the business and affects the business’s liquidity. Cash flow reports reflect activity for a specified period of time, usually one accounting period or one month. Maintaining tight control of cash flow is especially important if your small business is new, since ready cash can be limited until the business begins to grow and produce more working capital.

11. Cash Flow Projections

Future business decisions will depend on your educated cash flow projections. To plan ahead for upcoming expenditures and working capital, you need to depend on previous cash flow patterns. These patterns will give you a comprehensive look at how and when you receive and spend your cash. This info is the key to unlock informed, accurate cash flow projections.

12. Depreciation

The value of any asset can be said to depreciate when it loses some of that value in increments over time. Depreciation occurs due to wear and tear. Various methods of depreciation are used by businesses to decrease the recorded value of assets.

13. Fixed Asset

A tangible, long-term asset used for the business and not expected to be sold or otherwise converted into cash during the current or upcoming fiscal year is called a fixed asset. Fixed assets are items like furniture, computer equipment, equipment, and real estate.

14. Gross Profit

This business finance term and definition can be calculated as total sales (income) less the costs (expenses) directly related to those sales. Raw materials, manufacturing expenses, labor costs, marketing, and transportation of goods are all included in expenses.

15. Income Statement

Here is one of the four most important reports lenders and investors want to see when evaluating the viability of your small business. It is also called a profit and loss statement, and it addresses the business’s bottom line, reporting how much the business has earned and spent over a given period of time. The result will be either a net gain or a net loss.

16. Intangible Asset

A business asset that is non-physical is considered intangible. These assets can be items like patents, goodwill, and intellectual property.

17. Liability

This business finance key term is a legal obligation to repay or otherwise settle a debt. Liabilities are considered either current (payable within one year or less) or long-term (payable after one year) and are listed on a business’s balance sheet. A business’s accounts payable, wages, taxes, and accrued expenses are all considered liabilities.

18. Liquidity

Liquidity is an indicator of how quickly an asset can be turned into cash for full market value. The more liquid your assets, the more financial flexibility you have.

19. Profit & Loss Statement

See “Income Statement” above.

20. Statement of Cash Flow

One of the important documents required by lenders and investors that shows a summary of the actual collection of revenue and payment of expenses for your business. The statement of cash flow should reflect activity in the areas of operating, investing, and financing and should be an integral part of your financial statement package.

21. Statement of Shareholders’ Equity

If you have chosen to fund your small business with equity financing and you have established shares and shareholders as part of the controlling interests, you are obligated to provide a financial report that shows changes in the equity section of your balance sheet.

22. Annual Percentage Rate

The business finance term and definition APR represents the yearly real cost of a loan including all interest and fees. The total amount of interest to be paid is based on the original amount loaned, or the principal, and is represented in percentage form. When shopping for the right loan for your small business, you should know the APR for the loan in question. This figure can be very helpful in comparing one financial tool with another since it represents the actual cost of borrowing.

23. Appraisal

Just like your real estate appraisal when buying a house, an appraisal is a professional opinion of market value. When closing a loan for your small business, you will probably need one or more of the three types of appraisals: real estate, equipment, and business value.

24. Balloon Loan

A loan that is structured so that the small business owner makes regular repayments on a predetermined schedule and one much larger payment, or balloon payment, at the end. These can be attractive to new businesses because the payments are smaller at the outset when the business is more likely to be facing strict financial constraints. However, be sure that your business will be capable of making that last balloon payment since it will be a large one.

25. Bankruptcy

This federal law is used as a tool for businesses or individuals who are having severe financial challenges. It provides a plan for reduction and repayment of debts over time or an opportunity to completely eliminate the majority of the outstanding debts. Turning to bankruptcy should be given careful thought because it will have a negative effect on the business credit score.

26. Bootstrapping

Using your own money to finance the start-up and growth of your small business. Think of it as being your own investor. Once the business is up and running successfully, the business finance term and definition bootstrapping refers to the use of profits earned to reinvest in the business.

27. Business Credit Report

Just like you have a personal credit report that lenders look at to determine risk factors for making personal loans, businesses also generate credit reports. These are maintained by credit bureaus that record information about a business’s financial history.

Items like how large the company is, how long has it been in business, amount and type of credit issued to the business, how credit has been managed, and any legal filings (i.e., bankruptcy) are all questions addressed by the business credit report. Lenders, investors, and insurance companies use these reports to evaluate risk exposure and financial health of a business.

28. Business Credit Score

A business credit score is calculated based on the information found in the business credit report. Using a specialized algorithm, business credit scoring companies take into account all the information found on your credit report and give your small business a credit score. Also called a commercial credit score, this number is used by various lenders and suppliers to evaluate your creditworthiness.

29. Collateral

Any asset that you pledge as security for a loan instrument is called collateral. Lenders often require collateral as a way to make sure they won’t lose money if your business defaults on the loan. When you pledge an asset for collateral, it becomes subject to seizure by the lender if you fail to meet the requirements of the loan documents.

30. Credit Limit

When a lender offers a business line of credit it usually comes with a credit limit, or a maximum amount that you can use at any given time. It is said that you reach your credit limit or “max out” your credit when you borrow up to or exceed that number. A business line of credit can be especially useful if your business is seasonal or if the income is extremely unpredictable. It is one of the fastest ways to access cash for emergencies.

31. Debt Consolidation

If your small business has several loans with various payments, you might want to consider a business debt consolidation loan. It is a process that lets you combine multiple loans into a single loan. The advantages are possibly reducing the interest rates on the borrowed funds as well as lowering the total amount you repay each month. Businesses use this tool to help improve cash flow.

32. Debt Service Coverage Ratio

The business finance term and definition debt service coverage ratio (DSCR) is the ratio of cash your small business has available for paying or servicing its debt. Debt payments include making principal and interest payments on the loan you are requesting. Generally speaking, if your DSCR is above 1, your business has enough income to meet its debt requirements.

33. Debt Financing

When you borrow money from a lender and agree to repay the principal with interest in regular payments for a specified period of time, you’re using debt financing. Traditionally, it has been the most common form of funding for small businesses.

Debt financing can include borrowing from banks, business credit cards, lines of credit, personal loans, merchant cash advances, and invoice financing. This method creates a debt that must be repaid but lets you maintain sole control of your business.

34. Equity Financing

The act of using investor funds in exchange for a piece or ”share” of your business is another way to raise capital. These funds can come from friends, family, angel investors, or venture capitalists.

Before deciding to use equity financing to raise the cash necessary for your business, decide how much control you are willing to share when it comes to decision-making and philosophy. Some investors will also want voting rights.

35. FICO Score

A FICO score is another type of credit score used by potential lenders for evaluating the wisdom of entering a contract with you and your business. FICO scores comprise a substantial part of the credit report that lenders use to assess credit risk. It was created by the Fair Isaac Corporation, hence the name FICO.

36. Financial Statements

An integral part of the loan application process is furnishing information that shows your business is a good credit risk. The standard financial statement packet includes four main reports: the income statement, the balance sheet, the statement of cash flow, and the statement of shareholders’ equity, if you have shareholders.

Lenders and investors want to see that your business is well-balanced with assets and liabilities, has positive cash flow, and will have capital to make expected repayments.

37. Fixed Interest Rate

The interest rate on a loan that is established in the beginning and does not change for the lifetime of the loan is said to be fixed. Loans with fixed interest rates are appealing to small business owners because the repayment amounts are consistent and easier to budget for in the future.

38. Floating Interest Rate

In contrast to the business finance term and definition fixed rate, the floating interest rate will change with market fluctuations. Also referred to as variable rates or adjustable rates, these amounts may often start out lower than the fixed rate percentages. This makes them more appealing in the short term if the market is trending down.

39. Guarantor

When starting a new small business, lenders might want you to provide a guarantor. This is an individual who guarantees to cover the balance owed on a debt if you or your business cannot meet the repayment obligation.

40. Interest Rate

All loans and other lending instruments are assigned the business finance key term interest rates. This is a percentage of the principal amount charged by the lender for the use of its money. Interest rates represent the current cost of borrowing.

41. Invoice Factoring or Financing

If your business has a significant amount of open invoices outstanding, you may contact a factoring company and have them purchase the invoices at a discount. By raising capital this way, there is no debt, and the factoring company assumes the financial responsibility for collecting the invoice debts.

42. Lien

This business finance term and definition is a creditor’s legal claim to the collateral pledged as security for a loan is called a lien.

43. Line of Credit

A lender may offer you an unsecured amount of funds available for your business to draw on when capital is needed. This line of credit is considered a short-term funding option, with a maximum amount available. This pre-approved pool of money is appealing because it gives you quick access to the cash.

44. Loan-to-Value

The LTV comparison is a ratio of the fair-market value of an asset compared to the amount of the loan that will fund it. This is another important number for lenders who need to know if the value of the asset will cover the loan repayment if your business defaults and fails to pay.

45. Long-Term Debt

Any loan product with a total repayment schedule lasting longer than one year is considered a long-term debt.

46. Merchant Cash Advance

A merchant may offer a funding method through a loan based on the business’s monthly sales volume. Repayment is made with a percentage of the daily or weekly sales. These tend to be short-term loans and are one of the costliest ways to fund your small business.

47. Microloan

Microloans are loans made through nonprofit, community-based organizations and they are most often for amounts under $50,000.

48. Personal Guarantee

If you’re seeking financing for a very new business and don’t have a high value asset to offer as collateral, you may be asked by the lender to sign a statement of personal guarantee. In effect, this statement affirms that you as an individual will act as guarantor for the business’s debt, making you personally liable for the balance of the loan even in the event that your business fails.

49. Principal

Any loan instrument is made of three parts—the principal, the interest, and the fees. The principal is a business finance key term and is the original amount that is borrowed or the outstanding balance to be repaid less interest. It is used to calculate the total interest and fees charged.

50. Revolving Line of Credit

This business finance term and definition is a funding option is similar to a standard line of credit. However, the agreement is to lend a specific amount of money, and once that sum is repaid, it can be borrowed again.

51. Secured Loan

Many lenders will require some form of security when loaning money. When this happens, this business finance term and definition is a secured loan. The asset being used as collateral for the loan is said to be “securing” the loan. In the event that your small business defaults on the loan, the lender can then claim the collateral and use its fair-market value to offset the unpaid balance.

52. Term Loan

These are debt financing tools used to raise needed funds for your small business. Term loans provide the business with a lump sum of cash up front in exchange for a promise to repay the principal and interest at specified intervals over a set period of time. These are typically longer term, one-time loans for start-up expenses or costs for established business expansion.

53. Unsecured Loans

Loans that are not backed by collateral are called unsecured loans. These types of loans represent a higher risk for the lender, so you can expect to pay higher interest rates and have shorter repayment time frames. Credit cards are an excellent example of unsecured loans that are a good option for small business funding when combined with other financing options.

54. Articles of Incorporation

This is legal documentation of the business’s creation, including name, type of business, and type of business structure or incorporation. This paperwork is one of the first tasks you will complete when you officially start your business. Once submitted, your articles of incorporation are kept on file with the appropriate governmental agencies.

55. Business Plan

Here is your tool for demonstrating how you want to establish your small business and how you plan to grow it into good financial health. When writing a business plan, it should include financial, operational, and marketing goals as well as how you plan to get there. The more specific you are with your business plan, the better prepared you will be in the long run.

56. Employer Identification Number (EIN) Certificate

In order to be more easily identified by the Internal Revenue Service, every business entity is assigned a unique number called an EIN. When you start your small business, an EIN will be assigned and mailed to the business address. This number never changes, and you will be asked to furnish it for many reasons.

57. Franchise Agreement

For a small business entrepreneur, entering into a franchise agreement with a larger company can be a way to enter the marketplace. The agreement made between you and the larger company gives you the right to operate as a satellite of the larger company in a certain territory for a given period of time. This lets you, the business owner, take advantage of a brand name that’s already familiar in the marketplace and a process or operation that has already been tested.

58. Net Worth

This business finance term and definition is an expression of your business’s total value, as determined by your total current assets less the total liabilities currently owed by the business. With your business’s most recent balance sheet in hand, you can calculate the net worth using a simple formula: Assets – Liabilities = Net Worth.

59. Retained Earnings

Just like it sounds, this term represents any profits earned that are retained in the business. This can also be referred to as bootstrapping.

60. Tax Lien

If your business fails to pay taxes owed to the designated government entity, namely the IRS, you may find your assets seized by the claim of a tax lien. The government can not only seize your assets for liquidation to resolve the tax debt, but they can also charge you penalties on the amount you owe.

Don’t Be Overwhelmed by Health Economics, Business and Finance Terms

As a small business owner, physicians are required to wear many different hats—often including that of chief financial officer or bookkeeper. Before you let yourself get intimidated by all the business terms and definitions, just remember that knowledge is power.

You can serve your small practice business, clinic, out-patient center or hospital most effectively by becoming familiar with terms used in business and finance and how they will affect your financial health. Armed with a basic understanding of business finance key terms, you will be prepared to face the financial challenges that go along with being a modern doctor, today!

“”Medical economics and finance is an integral component of the health care industrial complex. Its language is a diverse and broad-based concept covering many other industries: accounting, insurance, mathematics and statistics, public health, provider recruitment and retention, Medicare, health policy, forecasting, aging and long-term care, are all commingled arenas.

The Dictionary of Health Economics and Finance will be an essential tool for doctors, nurses and clinicians, benefits managers, executives and health care administrators, as well as graduate students and patients? With more than 5,000 definitions, 3,000 abbreviations and acronyms, and a 2,000 item oeuvre of resources, readings, and nomenclature derivatives? it covers the financial and economics language of every health care industry sector.”” – From the Preface byDavid Edward Marcinko “

Posted on April 14, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

Of Characteristics and Commonalities

[By Dr. David Edward Marcinko MBA CMP™]

[By Eugene Schmuckler PhD MBA EMd CTS]

It does not matter if you are in the healthcare or financial services sector; or both.

Many psychologists and behavioral experts believe there are commonalities and characteristics applicable to all industries and sectors; including education which is a big part of what we do here at the Medical Executive Post.

Key Leadership Competencies – Definitions

And so, here is a list of key leadership competencies and definitions for your review.

Living by personal conviction – Means you know and are in touch with your values and beliefs, are not afraid to take a lonely or unpopular stance if necessary, are comfortable in tough situations, can be relied on in intense circumstances, are clear about where you stand, and will face difficult challenges with poise and self-assurance.

Possessing emotional intelligence – Means you recognize personal strengths and weaknesses; see the linkages between feelings and behaviors; manage impulsive feelings and distressing emotions; are attentive to emotional cues; show sensitivity and respect for others; challenge bias and intolerance; collaborate and share; are an open communicator; and can handle conflict, difficult people, and tense situations effectively. Emotional intelligence may often be labeled EQ, or emotional intelligence quotient.

Being visionary – Means that you see the future clearly, anticipate large-scale and local changes that will affect the organization and its environment, are able to project the organization into the future and envision multiple potential scenarios/outcomes, have a broad way of looking at trends, and are able to design competitive strategies and plans based on future possibilities.

Communicating vision – Means that you distill complex strategies into a compelling call to march, inspire and help others see a core reason for the organization to make change, talk beyond the day-to-day tactical matters that face the organization, show confidence and optimism about the future state of the organization, and engage others to join in.

Earning loyalty and trust – Means you are a direct and truthful person; are willing to admit mistakes; are sincerely interested in the concerns and dreams of others; show empathy and a generally helpful orientation toward others; follow promises with actions; maintain confidences and disclose information ethically and appropriately; and conduct work in open, transparent ways.

Listening like you mean it – Means you maintain a calm, easy-to-approach demeanor, are patient, open minded, and willing to hear people out; understand others and pick up the meaning of their messages; are warm, gracious and inviting; build strong rapport; see through the words that others express to the real meaning (i.e., cut to the heart of the issue); and maintain formal and informal channels of communication.

Giving feedback – Means you set clear expectations, bring important issues to the table in a way that helps others “hear” them, show an openness to facing difficult topics and sources of conflict, deal with problems and difficult people directly and frankly, provide timely criticism when needed, and provide feedback messages that are clear and unambiguous.

Mentoring others – Means you invest the time to understand the career aspirations of your direct reports, work with direct reports to create engaging mentoring plans, support staff in developing their skills, support career development in a non-possessive way (will support staff moving up and out as necessary for their advancement), find stretch assignments and other delegation opportunities that support skill development, and role model professional development by advancing your own skills.

Developing teams – Means you select executives who will be strong team players, actively support the concept of teaming, develop open discourse and encourage healthy debate on important issues, create compelling reasons and incentives for team members to work together, effectively set limits on the political activity that takes place outside the team framework, celebrate successes together as a unit, and commiserate as a group over disappointments.

Energizing staff – Means you set a personal example of good work ethic and motivation; talk and act enthusiastically and optimistically about the future; enjoy rising to new challenges; take on your work with energy, passion and drive to finish successfully; help others recognize the importance of their work; are enjoyable to work for; and have a goal oriented, ambitious and determined working style.

Generating informal power – Means you understand the roles of power and influence in organizations; develop compelling arguments or points of view based on knowledge of others’ priorities; develop and sustain useful networks up, down and sideways in the organization; develop a reputation as a go-to person; and effectively affect the thoughts and opinions of others, both directly and indirectly, through others.

Building consensus – Means you frame issues in ways that facilitate clarity from multiple perspectives, keep issues separated from personalities, skillfully use group decision techniques (e.g., Nominal Group Technique), ensure that quieter group members are drawn into discussions, find shared values and common adversaries, and facilitate discussions rather than guide them.

Making decisions effectively – Means you make decisions based on an optimal mix of ethics, values, goals, facts, alternatives and judgments; use decision tools (such as force-field analysis, cost-benefit analysis, decision trees, paired comparisons analysis) effectively and at appropriate times; and show a good sense of timing related to decision making.

Driving results – Means you mobilize people toward greater commitment to a vision, challenge people to set higher standards and goals, keep people focused on achieving goals, give direct and complete feedback that keeps teams and individuals on track, quickly take corrective action as necessary to keep everyone moving forward, show a bias toward action, and proactively work through performance barriers.

Stimulating creativity – Means you see broadly outside of the typical, are constantly open to new ideas, are effective with creative group processes (e.g., brainstorming, Nominal Group Technique, scenario building), see future trends and craft responses to them, are knowledgeable in business and societal trends, are aware of how strategies play out in the field, are well read, and make connections between industries and unrelated trends.

Cultivating adaptability – Means you quickly see the essence of issues and problems, effectively bring clarity to situations of ambiguity, approach work using a variety of leadership styles and techniques, track changing priorities and readily interpret their implications, balance consistency of focus against the ability to adjust course as needed, balance multiple tasks and priorities such that each gets appropriate attention, and work effectively with a broad range of people.

Is if often said that leaders rise to the occasion. What do you think?

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Insider transactions shouldn’t be used primarily to make an investing decision, however an insider transaction can be an important factor in the investing decision.

In legal terms, an “insider” refers to any shareholder who owns at least 10% of a company. This can include executives in the c-suite and large hedge funds. These insiders are required to let the public know of their transactions via a Form 4 filing, which must be filed within two business days of the transaction.

Mark Zuckerberg, CEO at Facebook (NASDAQ:FB), just made a large buy and sell of company shares on November 3, according to a new SEC filing. A Form 4 filing from the U.S. Securities and Exchange Commission states that Mark Zuckerberg exercised options to purchase 62,300 Facebook shares for $0 on November 3. They then sold their shares on the same day in the open market. They sold at prices ranging from $324.04 to $332.02 to raise a total of $25,463,482 from the stock sale.

Zuckerberg still owns a total of 232,400 shares of Facebook worth, $78,226,142.

According to Wikipedia, selling away in the U.S. securities brokerage industry is the inappropriate practice of an investment professional who sells, or solicits the sale of, securities not held or offered by the brokerage firm with which he is associated.

An example of the term expressed in a sentence is, “The broker was selling investments away from the firm.” Brokers marketing securities must have obtained the appropriate securities licenses for various types of investments. Brokers in the U.S. may be “associated” with one or more Brokerage firms and must obtain licenses by passing standardized Financial Industry Regulatory Authority exams such as the Series 6 or Series 7 exam.

***

In the past I’ve held these as well as a Series 63 and 65 license [SEC].

The foreign exchange market is a global decentralized or over-the-counter market for the trading of currencies. This market determines foreign exchange rates for every currency. It includes all aspects of buying, selling and exchanging currencies at current or determined prices.

In terms of trading volume, it is by far the largest market in the world, followed by the credit market.

The forex market is not dominated by a single market exchange, but a global network of computers and brokers from around the world. Forex brokers act as market makers as well and may post bid and ask prices for a currency pair that differs from the most competitive bid in the market.

The forex market is made up of two levels—the interbank market and the over-the-counter (OTC) market. The interbank market is where large banks trade currencies for purposes such as hedging, balance sheet adjustments, and on behalf of clients. The OTC market, on the other hand, is where individuals trade through online platforms and brokers.

NOTE: FOREX.com is a registered FCM and RFED with the CFTC and member of the National Futures Association (NFA # 0339826). Forex trading involves significant risk of loss and is not suitable for all physicians or investors.

Posted on October 7, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

BY DR. DAVID E. MARCINKO MBA

Designated a Doody’s Core Title!

“”Medical economics and finance is an integral component of the health care industrial complex. Its language is a diverse and broad-based concept covering many other industries: accounting, insurance, mathematics and statistics, public health, provider recruitment and retention, Medicare, health policy, forecasting, aging and long-term care, are all commingled arenas.

The Dictionary of Health Economics and Finance will be an essential tool for doctors, nurses and clinicians, benefits managers, executives and health care administrators, as well as graduate students and patients? With more than 5,000 definitions, 3,000 abbreviations and acronyms, and a 2,000 item oeuvre of resources, readings, and nomenclature derivatives? it covers the financial and economics language of every health care industry sector.”” – From the Preface byDavid Edward Marcinko “

People really love money since it is needed to buy just about everything. In fact, we actually published a formal print dictionary on health economics and finance terms that is very popular with physician investors and medical colleagues; it is a favorite of economic students as well!

And, money is by far one of those words that has more slang or terms for it than any others. This proves that cash or money, does not have be boring when speaking about it. Just keep in mind that these slang synonyms are in plural form. They are also words mostly used for US currency.

Perhaps the fact that money is so important may help to explain why there are so many different ways to say it. These 95 slang words for money and their meanings are really worth taking a look at. This list not only contains the countless ways to speak, write or say the word money, but also what are the meanings behind each phrase or term.

Health care in the US is technologically advanced but expensive, costing about $3.6 trillion in 2018, which was 16.9% of gross domestic product (GDP) (1). This percentage is significantly higher than in any other nation.

According to the Organization for Economic Cooperation and Development (OECD), in 2018 the next highest spending countries were Switzerland (12.2% of GDP) and France, Germany, Sweden, and Japan (each about 11%), while the average of the 35 OECD countries (OECD35) was 8.8% (2).

ASSESSMENT: Of course, the absolute amount and the rate of increase of health care spending in the US are widely regarded as unsustainable. Consequences of increased US spending on health care include the following:

Posted on October 19, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

YOU DECIDE AND OPINE

By Dr. David E. Marcinko MBA

The Plot Thickens

Autumn is here, and leaves aren’t the only thing falling.

After seven months of higher monthly closes, plus one record-setting high early in the month, the benchmark S&P 500® Index wobbled its way to a 5% pullback in September. The causes were many—uncertainty emanating from Washington, inflation, supply chain problems, and softer earnings growth forecasts—and now the horizon is looking foggy as we gaze ahead toward the final months of 2021.

Shipping bottlenecks and a near-record number of job openings are raising costs and putting upward pressure on wages, which may start to hurt profit margins, and the twin specters of inflation and higher interest rates are making investors wonder when the Federal Reserve might step in to raise interest rates.

But, if there’s a potential bright spot, we have to look across the sea to the Eurozone, where the signs point toward an era of increased government spending that could be positive for global economic growth.

To keep up with the ever-changing healthcare industrial complex, we must learn new definitions and re-learn old terminology in order to correctly apply it to practice. By aggregating the most up-to-date abbreviations, acronyms, definitions and terms, the Health DictionarySeries offers a wealth of information to help understand the ever-changing terms-of-art in healthcare today.

Each 10,000 item handbook is essential for doctors, nurses, benefits managers, financial advisors/planners, and insurance agents, CPAs, and administrators; as well as graduate and under graduate students and professors. Our goal to for each dictionary to be designated as a Doody’s Core Title.

Dictionary of Health Insurance and Managed Care

With more than 10,000 definitions, 4,000 abbreviations and acronyms, and a 3,000 item oeuvre of resources, readings, and nomenclature derivatives, this dictionary covers the Medicare, managed care and Medicaid, private insurance, Veteran’s Administration and PP-ACA language of the entire health and long-term care insurance sector.

Dictionary of Health Economics and Finance

Health economics and finance is an integral component of the health care industrial complex. Its language is a diverse and broad-based concept covering many other industries: accounting, mathematics, the actuarial sciences, stochastics and statistics, salary reimbursements, physician payments, compensation and forecasting are all commingled arenas.

Dictionary of Health Information Technology Security

There is a myth that all healthcare stakeholders understand the meaning of information technology jargon. In truth, the vernacular of contemporary systems is unique, and often misused or misunderstood. Moreover, emerging Heath Information Technology (HIT) thru the HITECG initiatives; in the guise of terms, definitions, acronyms, abbreviations and standards; often puts the non-expert in a position of maximum uncertainty and minimum productivity.

Posted on October 16, 2014 by Dr. David Edward Marcinko MBA MEd CMP™

Promoting the … Health Dictionary Series™

By Dr. David Edward Marcinko FACFAS MBA CMP™

[Editor-in-Chief]

A day for lexicographers everywhere, Dictionary Day was founded to celebrate the achievements and contributions of Noah Webster – the father of the modern dictionary.

The objective of this day is to emphasize the importance of dictionary skills, and seeks to improve vocabulary.

History

Webster began to write his dictionary at the age of 43. It took him 27 years to finish it! In addition to traditional English vocabulary, it contained uniquely American words.

Our Health Dictionary Series™

The HDS Consists of three handbooks:

Dictionary of Health Insurance and Managed Care

Dictionary of Health Information Technology and Security

Dictionary of Health Economics and Finance

Each has 10,000 terms, definitions and initialisms!

Why not take the opportunity to learn some new health administration terms, words and definitons? Designated as Doody’s Core Titles.

“Health care economist Dr. David Edward Marcinko, MBA, and his colleagues at the Institute of Medical Business Advisors, Inc., should be complimented for conceiving and completing this laudable project. The Dictionary of Health Insurance and Managed Care lifts the fog of confusion surrounding the most contentious topic in the health care industrial complex today. My suggestion, therefore, is to “read it, refer to it, recommend it, and reap.”

-Dictionary of Health Insurance and Managed Care

Michael J. Stahl, PhD

[Director, Physician Executive MBA Program]

William B. Stokely Distinguished Professor of Business

College of Business Administration

The University of Tennessee

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on September 26, 2011 by Dr. David Edward Marcinko MBA MEd CMP™

Dictionary of Health Economics and Finance

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Posted on August 17, 2010 by Dr. David Edward Marcinko MBA MEd CMP™

The “Father” of Health Economics

By Dr. David Edward Marcinko MBA, CMP™

[Editor-in-Chief]

Professor Kenneth Arrow is a Nobel laureate who explored the characteristics of a perfectly competitive marketplace for an ordinary commodity – and how the healthcare industry deviated from those characteristics – and what aspects of health care might explain these deviations.

But, in as much as he did all this in the 1960’s, he is known today as the “father” of health [not health care] economics.

In fact, his 1963 paper launched health economics as a unique discipline and is as close to required reading as can exist for followers of the ME-P and our related websites and educational consulting firms [sidebar].

Assessment

Arrow Title: “Uncertainty and the Welfare Economics of Medical Care”

Glossary:Dictionary of Health Economics and Finance

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on July 26, 2010 by Dr. David Edward Marcinko MBA MEd CMP™

Explaining Healthcare Administration Terms, Too!

By Ann MiIler RN, MHA

[Executive-Director]

According to the Wall Street Journal, when it comes to understanding medical information, even the most sophisticated patient may not fully understand. Nearly nine out of 10 adults have difficulty following routine medical advice, largely because it’s often incomprehensible to average people, the CDC says. And that’s bad for health care.

Enter the Medical Jargon

Confused by scientific jargon, doctors’ instructions and complex medical phrases, patients are more likely to skip necessary medical tests or fail to properly take their medications, the agency says. Studies show that poor health literacy drives up costs to the health-care system and worsens patient outcomes.

And so, we too have attempted to explain some of the healthcare administration and practice management jargon in use today

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

A CMO is a debt security backed by mortgages. These mortgage pools are usually separated into different maturity classes called tranches (from the French word for “slice”). The securities were issued by private issuers, as well as the Federal Home Loan Mortgage Corporation (Freddie Mac). As the mortgages were usually government-guaranteed, CMOs usually carried AAA ratings until their current financial meltdown. The early versions of CMOs were known as “plain vanilla,” but recent developments gave us PACs (planned amortization certificates) and TACs (targeted amortization certificates); among too many others. They were all variations on how principal repayments in advance of maturity date were treated.

Speaker:If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com or Bio: www.stpub.com/pubs/authors/MARCINKO.htm

Our Other Print Books and Related Information Sources:

Subscribe Now:Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.