BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Podiatry, a specialized branch of medicine focused on diagnosing and treating conditions of the foot, ankle, and lower extremities, is often perceived as a stable and rewarding career. However, beneath the surface of clinical success and professional prestige lies a growing concern: the emotional and psychological toll of the profession. Stress, burnout, divorce, and practice turmoil are increasingly common among podiatrists, threatening not only their personal well-being but also the sustainability of their practices and the quality of patient care.

The Nature of Stress in Podiatry

Stress in podiatry arises from multiple sources. Clinical responsibilities, administrative burdens, patient expectations, and financial pressures converge to create a high-stakes environment. Podiatrists often work long hours, manage complex cases, and juggle the demands of running a business. The pressure to maintain high standards of care while navigating insurance reimbursements, staffing issues, and regulatory compliance can be overwhelming.

Moreover, podiatrists frequently deal with chronic conditions that require ongoing management rather than quick resolution. This can lead to emotional fatigue, especially when patients experience limited improvement or express dissatisfaction. The cumulative effect of these stressors can erode a podiatrist’s sense of purpose and satisfaction, leading to burnout.

Burnout: A Silent Epidemic

Burnout is characterized by emotional exhaustion, depersonalization, and a reduced sense of personal accomplishment. In podiatry, it manifests as fatigue, irritability, cynicism, and a decline in empathy toward patients. Burnout not only affects the practitioner’s mental health but also compromises patient safety, increases the risk of medical errors, and contributes to staff turnover.

Studies have shown that healthcare professionals, including podiatrists, are at a higher risk of burnout compared to other professions. The isolation of solo practice, lack of peer support, and limited access to mental health resources exacerbate the problem. Without intervention, burnout can progress to depression, substance abuse, and even suicidal ideation.

The personal lives of podiatrists are not immune to the pressures of the profession. Divorce rates among physicians, including podiatrists, are notably high. The demands of the job often leave little time for family, leading to strained relationships and emotional disconnect. The stress of managing a practice can spill over into home life, creating tension and conflict.

Divorce, in turn, can intensify professional stress. Legal proceedings, financial settlements, and emotional upheaval can distract from clinical duties and disrupt practice operations. The dual burden of personal and professional turmoil can be devastating, leading to a downward spiral that affects every aspect of life.

Practice Turmoil: The Business of Healing

Running a podiatry practice is akin to managing a small business. Beyond clinical expertise, podiatrists must master marketing, human resources, billing, and compliance. Practice turmoil can arise from staff conflicts, financial mismanagement, poor patient retention, or changes in healthcare regulations.

For example, a sudden drop in reimbursements or a lawsuit can destabilize a practice. Staff turnover, especially among key personnel like office managers or billing specialists, can disrupt workflow and erode morale. Inadequate leadership or poor communication can lead to a toxic work environment, further fueling stress and burnout.

Addressing the Crisis

To combat these challenges, podiatrists must prioritize self-care, seek support, and implement systemic changes. Here are several strategies:

Mental Health Support: Regular counseling, peer support groups, and wellness programs can help podiatrists process stress and prevent burnout.

Work-Life Balance: Setting boundaries, delegating tasks, and scheduling personal time are essential for maintaining emotional health.

Practice Management Training: Investing in leadership and business education can improve operational efficiency and reduce turmoil.

Staff Engagement: Creating a positive work culture, recognizing achievements, and fostering open communication can enhance team cohesion.

Technology Integration: Utilizing electronic health records, telemedicine, and automation can streamline administrative tasks and reduce workload.

Professional organizations also play a vital role. The American Podiatric Medical Association (APMA) and similar bodies can offer resources, advocacy, and continuing education to support practitioners. Medical schools and residency programs should incorporate wellness training and stress management into their curricula to prepare future podiatrists for the realities of the profession.

Podiatry is a noble and essential field, but it is not without its challenges. Stress, burnout, divorce, and practice turmoil are real and pressing issues that demand attention. By acknowledging these problems and taking proactive steps, podiatrists can safeguard their well-being, strengthen their practices, and continue to provide compassionate care to their patients. The path to healing begins not just with treating others, but with caring for oneself.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A medical economic white elephant is a healthcare-related investment—such as a hospital, device, or system—that consumes vast resources but fails to deliver proportional value, often becoming a financial burden rather than a benefit to public health.

In economic terms, a white elephant refers to an asset whose cost of upkeep far exceeds its utility. In the medical field, this concept manifests in projects or technologies that are expensive to build, maintain, or operate, yet offer limited practical use, accessibility, or return on investment. These ventures often begin with noble intentions—improving care, advancing technology, or expanding access—but end up draining resources due to poor planning, misaligned incentives, or lack of demand.

One prominent example is the construction of underutilized hospitals or specialty centers in regions with low patient volume. Governments or private entities may invest heavily in state-of-the-art facilities without conducting thorough needs assessments. The result: gleaming buildings with advanced equipment but few patients, high operating costs, and staff shortages. These facilities often struggle to stay open, becoming financial sinkholes that divert funds from more pressing healthcare needs.

Medical devices and technologies can also become white elephants. For instance, robotic surgical systems or high-end imaging machines are sometimes purchased by hospitals to boost prestige or attract patients, despite limited clinical necessity or trained personnel. These devices require costly maintenance, specialized training, and may not significantly improve outcomes compared to traditional methods. When reimbursement rates don’t justify their use, they become liabilities.

***

***

Electronic health record (EHR) systems offer another cautionary tale. While digitizing patient records is essential, some EHR implementations have ballooned into multi-million-dollar projects plagued by inefficiencies, poor interoperability, and user dissatisfaction. Hospitals may invest in proprietary systems that are difficult to integrate with others, leading to fragmented care and wasted resources. In extreme cases, these systems are abandoned or replaced, compounding the financial loss.

The consequences of medical white elephants are far-reaching. They can strain public budgets, increase healthcare costs, and erode trust in institutions. In developing countries, such projects may be funded by international aid or loans, saddling governments with debt while failing to improve population health. Even in wealthier nations, misallocated resources can mean fewer funds for primary care, preventive services, or community health initiatives.

***

***

Avoiding medical white elephants requires rigorous planning, stakeholder engagement, and evidence-based decision-making. Health systems must assess actual needs, forecast demand, and consider long-term sustainability. Cost-benefit analyses should include not only financial metrics but also health outcomes, equity, and accessibility. Transparency and accountability are key to ensuring that investments serve the public good.

In conclusion, the concept of a medical economic white elephant highlights the importance of aligning healthcare investments with real-world needs and outcomes. While innovation and expansion are vital, they must be grounded in practicality and sustainability.

By learning from past missteps, health systems can prioritize value-driven care and avoid the costly pitfalls of overambitious or poorly conceived projects.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Short Interest Theory suggests that high levels of short interest in a stock may actually signal a potential price increase, contrary to traditional bearish interpretations.

Short Interest Theory is a contrarian investment concept that challenges conventional wisdom in financial markets. Traditionally, a high short interest—meaning a large percentage of a company’s shares are being sold short—is seen as a bearish signal, indicating that many investors expect the stock’s price to decline. However, Short Interest Theory flips this assumption, proposing that a high short interest can actually be a bullish indicator, suggesting a potential upward price movement due to a phenomenon known as a “short squeeze.”

To understand this theory, it’s important to grasp the mechanics of short selling. When investors short a stock, they borrow shares and sell them on the open market, hoping to repurchase them later at a lower price and pocket the difference. However, if the stock price rises instead of falling, short sellers face mounting losses. To limit these losses, they may be forced to buy back the stock at higher prices, which increases demand and drives the price up even further. This chain reaction is what’s known as a short squeeze.

Short Interest Theory posits that when short interest reaches unusually high levels, the stock becomes a prime candidate for a short squeeze. Investors who follow this theory look for stocks with high short interest ratios—often measured as the number of shares sold short divided by the stock’s average daily trading volume. A high ratio suggests that it would take many days for all short sellers to cover their positions, increasing the likelihood of a rapid price surge if positive news or buying pressure emerges.

This theory gained widespread attention during the GameStop (GME) saga in early 2021. Retail investors noticed that GME had an extremely high short interest—more than 100% of its float—and began buying shares en masse. This triggered a historic short squeeze, sending the stock price soaring and forcing institutional short sellers to cover their positions at massive losses. The event served as a real-world validation of Short Interest Theory and highlighted the power of collective investor behavior in modern markets.

Despite its appeal, Short Interest Theory is not without risks. Betting on a short squeeze can be speculative and volatile. Not all heavily shorted stocks experience upward momentum; some may continue to decline if the negative sentiment is justified by poor fundamentals or weak earnings. Moreover, timing a short squeeze is notoriously difficult, and investors can suffer significant losses if the anticipated rebound fails to materialize.

In conclusion, Short Interest Theory offers a compelling contrarian perspective on market sentiment. By interpreting high short interest as a potential bullish signal, it encourages investors to look beyond surface-level indicators and consider the dynamics of market psychology and trading behavior. While it can lead to lucrative opportunities, especially in the context of short squeezes, it also demands careful analysis and risk management. As with any investment strategy, understanding the underlying fundamentals and market context is essential for making informed decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Valuing a medical practice involves assessing its financial performance, assets, and intangible factors like goodwill and patient loyalty to determine its fair market worth.

Determining the value of a medical practice is a nuanced process that blends financial analysis with strategic insight. Whether you’re preparing to sell, merge, or bring in a partner, understanding how to value your practice ensures informed decision-making and fair negotiations.

There are several recognized methods for valuing a medical practice, each suited to different scenarios. The most common include the income approach, market approach, asset-based approach, and the rule-of-thumb method.

The income approach focuses on the practice’s ability to generate future earnings. This method involves analyzing historical financial statements, projecting future cash flows, and discounting them to present value using a risk-adjusted rate. It’s particularly useful when the practice has stable revenue and predictable expenses. Key metrics include net income, physician productivity, and reimbursement rates.

The market approach compares the practice to similar ones that have recently sold. It relies on data from comparable transactions, adjusted for differences in size, specialty, location, and profitability. This method is ideal when reliable market data is available, though such data can be scarce for niche specialties or rural practices.

The asset-based approach calculates the value of tangible and intangible assets. Tangible assets include medical equipment, office furniture, and real estate. Intangible assets—like patient records, brand reputation, and goodwill—are harder to quantify but can significantly impact value. Goodwill, for instance, reflects the practice’s reputation, patient loyalty, and referral networks.

The rule-of-thumb method uses industry benchmarks, such as a multiple of annual revenue or earnings. For example, a general practice might be valued at 60–80% of annual gross revenue. While quick and easy, this method oversimplifies and may not reflect the unique strengths or weaknesses of a specific practice.https:/https://medicalexecutivepost.com/2025/03/17/medial-practice-valuation-adjustments//medicalexecutivepost.com/2025/03/17/medial-practice-valuation-adjustments/

Beyond these methods, several qualitative factors influence valuation. These include the size and diversity of the patient base, the practice’s specialty, use of technology (like EHR systems or telemedicine), and whether key physicians will remain post-sale. A practice heavily reliant on one provider may be less valuable than one with a strong team and succession plan.

Timing also matters. Economic conditions, regulatory changes, and shifts in healthcare reimbursement can affect practice value. Tax implications and deal structure—such as asset sale vs. stock sale—should also be considered during negotiations.

Ultimately, valuing a medical practice is both art and science. Engaging a professional appraiser or valuation expert can help ensure accuracy and objectivity. They bring experience, access to market data, and the ability to tailor valuation methods to your specific situation.

In summary, a comprehensive valuation considers financial performance, assets, market trends, and intangible factors. By understanding these elements, practice owners can make strategic decisions that reflect the true worth of their medical enterprise.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on October 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

DEFINED

***

***

A physician practice management corporation (PPMC) is a business entity that provides non-clinical administrative and operational support to medical practices, allowing physicians to focus on patient care while the corporation handles the business side of healthcare.

Physician practice management corporations emerged in response to the increasing complexity of running a medical practice. As healthcare regulations, insurance requirements, and operational costs grew, many physicians found it challenging to manage both clinical responsibilities and business operations. PPMCs offer a solution by taking over the administrative burdens, enabling physicians to concentrate on delivering quality care.

At their core, PPMCs are responsible for a wide range of non-medical services. These include billing and coding, human resources, payroll, marketing, compliance, information technology, and financial management. By centralizing these functions, PPMCs can achieve economies of scale, reduce overhead costs, and improve operational efficiency for the practices they manage. This model is particularly attractive to small and mid-sized practices that may lack the resources to manage these functions independently.

PPMCs typically enter into long-term management agreements with physician groups. In some cases, they may purchase the non-clinical assets of a practice—such as equipment, office space, and administrative staff—while the physicians retain control over clinical decisions and patient care. This arrangement allows for a clear division between medical and business responsibilities, which is essential for maintaining compliance with healthcare regulations like the Stark Law and the Anti-Kickback Statute.

A physician practice management corporation (PPMC) is a business entity that provides non-clinical administrative and operational support to medical practices, allowing physicians to focus on patient care while the corporation handles the business side of healthcare.

Physician practice management corporations emerged in response to the increasing complexity of running a medical practice. As healthcare regulations, insurance requirements, and operational costs grew, many physicians found it challenging to manage both clinical responsibilities and business operations. PPMCs offer a solution by taking over the administrative burdens, enabling physicians to concentrate on delivering quality care.

At their core, PPMCs are responsible for a wide range of non-medical services. These include billing and coding, human resources, payroll, marketing, compliance, information technology, and financial management. By centralizing these functions, PPMCs can achieve economies of scale, reduce overhead costs, and improve operational efficiency for the practices they manage. This model is particularly attractive to small and mid-sized practices that may lack the resources to manage these functions independently.

PPMCs typically enter into long-term management agreements with physician groups. In some cases, they may purchase the non-clinical assets of a practice—such as equipment, office space, and administrative staff—while the physicians retain control over clinical decisions and patient care. This arrangement allows for a clear division between medical and business responsibilities, which is essential for maintaining compliance with healthcare regulations like the Stark Law and the Anti-Kickback Statute.

***

***

One of the key advantages of working with a PPMC is access to capital and advanced infrastructure. PPMCs often invest in state-of-the-art electronic health record (EHR) systems, data analytics tools, and revenue cycle management platforms. These technologies can enhance patient care, streamline operations, and improve financial performance. Additionally, PPMCs may offer strategic guidance on practice expansion, mergers and acquisitions, and payer contract negotiations.

However, the relationship between physicians and PPMCs must be carefully managed. While PPMCs bring valuable expertise and resources, there is a risk that business priorities could overshadow clinical autonomy. To mitigate this, successful PPMCs prioritize physician engagement, transparent governance, and aligned incentives. They work collaboratively with physicians to ensure that business strategies support, rather than hinder, the delivery of high-quality care.

The physician practice management industry has evolved significantly over the past few decades. After a wave of failures in the 1990s due to overexpansion and misaligned incentives, modern PPMCs have adopted more sustainable and physician-centric models. Today, they play a crucial role in helping practices adapt to value-based care, population health management, and other emerging trends in healthcare delivery.

In conclusion, a physician practice management corporation serves as a strategic partner to medical practices, offering the business acumen and operational support needed to thrive in a complex healthcare environment. By offloading administrative tasks and providing access to advanced resources, PPMCs empower physicians to focus on what they do best—caring for patients—while ensuring the long-term success and sustainability of their practices.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Historically, the term “risk management” has brought to mind one subject for the practicing physician – medical malpractice. Unfortunately, physicians today face a multitude of other risks which may be more insidious and daunting than malpractice. It is important to recognize these risks, and to have the appropriate procedures and policies in place to mitigate the risks. These risks come from the federal government, state government, insurance companies, patients, employees, and even prospective employees. Some risks, many unique to small businesses and medical practices, include the following:

Medicare recoupment risk – challenges to coding and subsequent billing by the physician.

Medicare fraud. Numerous laws can be used by the federal government to go after the physician, including the Medicare and Medicaid Anti-Fraud and Abuse Statute, the RICO statute, and the Federal False Claims Act. The recently enacted Patient Protection & Affordable Care Act aims to save money by increasing funding for anti-fraud efforts.

Insurance fraud. An inquiry from Medicare to look for fraud in a physician’s practice is often followed by similar efforts by insurance companies.

The HIPPA Act of 1996 creates new definitions and penalties to use against the physician.

Self referral risks. Federal regulations in this area include the Medicare Anti-Fraud and Abuse Statute, the Medicare Safe Harbor Regulations, and the Stark Amendment.

Federal agency risks. These include regulations from the Occupational Health and Safety Agency (OSHA), Health and Human Services (HHS), the Drug Enforcement agency (DEA), and even the Environmental Protection Agency (EPA).

Anti-trust risks. The Department of Justice (DOJ) and Federal Trade Commission (FTC) formulate regulations in this arena.

Managed care contractual risks. Most managed care contracts require the individual physician rather than the professional corporation to sign the contract, thus placing the physician’s personal assets at risk.

Medical malpractice risks. Although the vast majority of claims are paid by the insurance carrier, there can be other adverse consequences for the physician. These include the risk of increased premiums, non-renewal of policies, and difficulty in getting replacement insurance.

Loss of income due to death or disability. Most physicians recognize the importance of life insurance, but the medical professional is actually much more likely to lose income due to disability at some point in his or her career.

The practicing physician should seek the advice of professionals with expertise in these areas. Every practice should have an experienced attorney on retainer. It is very important to seek advice from fiduciaries – experts who have no conflicts of interest and who can therefore act in the best interest of the client. A Certified Medical Planner is such a fiduciary with training and expertise in these areas.

It can be particularly challenging to find an insurance advisor with no conflicts of interest, as this industry is built upon product sales and commissions. One such insurance advisor is Scott Witt, a fee-only insurance advisor with Witt Actuarial Services (www.wittactuarialservices.com).

Others can be found with an internet search for “fee only insurance advisor”.

Conclusion

Your comments on this ME-P are appreciated. How do you select an advisor? Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, be sure to subscribe. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Subscribe Now:Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed:And, credible sponsors and like-minded advertisers are always welcomed.

Posted on October 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and A.I.

***

***

Dentistry is often perceived as a stable and rewarding profession, yet beneath the surface lies a troubling reality: dentists face disproportionately high levels of stress, burnout, divorce, practice turmoil, and even suicide. These issues stem from a complex interplay of emotional, financial, and professional pressures that uniquely affect dental practitioners.

Emotional and Psychological Strain

Dentists frequently operate in high-stakes environments where precision is paramount. The pressure to deliver flawless results while managing patient anxiety and discomfort can be overwhelming. Many patients fear dental procedures, and this fear often manifests as hostility or distrust, placing emotional strain on the dentist. Over time, the cumulative effect of these interactions can lead to compassion fatigue and emotional exhaustion.

Unlike other medical professionals who often work in collaborative hospital settings, dentists typically operate in solo or small group practices. This isolation can limit opportunities for peer support and professional camaraderie. Without a strong support network, dentists may struggle to process the emotional toll of their work, increasing their vulnerability to depression and burnout.

Financial and Business Pressures

Running a dental practice involves more than clinical expertise—it requires business acumen. Dentists must manage overhead costs, staff salaries, insurance reimbursements, and patient billing. The financial burden of student loans, often exceeding six figures, adds to the stress. Economic downturns or shifts in healthcare policy can destabilize practices, leading to turmoil and uncertainty.

***

***

Work-Life Imbalance and Marital Strain

The demanding nature of dentistry often spills into personal life. Long hours, administrative responsibilities, and the emotional weight of patient care can leave little time or energy for family. This imbalance contributes to high divorce rates among dentists. The stress of maintaining a successful practice while nurturing personal relationships can become untenable, especially without adequate coping mechanisms.

Burnout and Suicide Risk

Burnout in dentistry is alarmingly common. A study by the American Dental Association found that 84% of dentists report experiencing burnout at some point in their careers.

Addressing these challenges requires systemic change. Mental health support, peer mentorship, and business education should be integrated into dental training. Encouraging open conversations about stress and providing resources for emotional well-being can help reduce stigma and promote resilience.

By acknowledging the hidden struggles of dentistry, the profession can move toward a healthier, more sustainable future.

Why It Is Difficult to Practice Medicine Part-Time Today?

In the past, part-time medical practice offered physicians a flexible way to balance professional responsibilities with personal or family commitments. Today, however, the healthcare environment has evolved in ways that make part-time medicine increasingly challenging. From administrative burdens to economic pressures and patient expectations, the obstacles are both systemic and personal.

One of the most significant barriers is the rise in administrative complexity. Physicians are now required to navigate electronic health records (EHRs), comply with insurance documentation, and meet regulatory standards such as HIPAA and MACRA. These tasks consume hours of non-clinical time, which is difficult to compress into a part-time schedule. Even seeing fewer patients doesn’t exempt part-time doctors from the same documentation and compliance requirements as their full-time counterparts.

***

***

Another challenge is financial viability. Many physicians are paid based on productivity metrics, such as Relative Value Units (RVUs), which reward volume over quality. Part-time practitioners often struggle to meet these benchmarks, resulting in lower compensation and reduced benefits. Additionally, malpractice insurance premiums and licensing fees remain fixed regardless of hours worked, further eroding the financial appeal of part-time practice.

Continuity of care is also a concern. Patients increasingly expect immediate access to their providers, especially in primary care and specialties like psychiatry or pediatrics. Part-time physicians may not be available for urgent issues, leading to fragmented care and dissatisfaction. This can strain relationships with patients and colleagues who must cover gaps in availability.

From a professional standpoint, part-time physicians may face limited career advancement. Leadership roles, academic appointments, and research opportunities often favor full-time commitment. There’s also a perception—sometimes unfair—that part-time doctors are less dedicated or less competent, which can affect peer respect and influence within medical institutions.

Technology, while beneficial, adds another layer of complexity. Telemedicine, remote monitoring, and digital communication tools have expanded access but also increased the expectation for constant availability. Part-time physicians may find it difficult to manage asynchronous messages, follow-ups, and virtual visits without extending their work hours beyond what they intended.

***

***

Lastly, burnout and work-life balance—ironically one of the reasons doctors seek part-time roles—can still be elusive. The pressure to maintain clinical excellence, stay updated with medical advancements, and meet patient needs doesn’t diminish with reduced hours. In fact, squeezing these responsibilities into fewer days can intensify stress rather than alleviate it.

In conclusion, while part-time medical practice may seem like a solution to modern work-life challenges, the reality is far more complex. The structure of today’s healthcare system, combined with economic, technological, and cultural pressures, makes it difficult for physicians to thrive in part-time roles. Addressing these challenges will require systemic reform, flexible compensation models, and a cultural shift in how we value and support diverse medical careers.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on October 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Efficient New Patient-Scheduling Models

[By Staff Writers]

Most doctors follow a linear (series-singular) time allocation strategy for scheduling patients (i.e., every 15 or 20 minutes). This can create bottlenecks because of emergencies, late patients, traffic jams, absent office personal, paperwork delays, etc.

Therefore, as first proposed by Dr. Neal Baum, a practicing urologist in New Orleans, one of these three newer scheduling approaches might prove more useful.

Customized Scheduling

The bottleneck problem may be reduced by trying to customize, estimate or project the time needed for the patient’s next office visit.

For example: CPT #99211 (15 minutes), #99212 (25 minutes), #99213 (35 minutes), or #99214 (45 minutes). Occasionally, extra time is need, and can be accommodated, if the allocated times are not too tightly scheduled.

Wave Scheduling

Most patients do not mind a brief 20-30 minute wait prior to seeing the doctor. Wave scheduling assumes that no patient will wait longer than this time period, and that for every three patients; two will be on time and one will be late.

This model begins by scheduling the three patients on the hour; and works like this.The first patient is seen on schedule, while the second and third wait for a few minutes. The later two patients are booked at 20 minutes past the hour and one or both may wait a brief time. One patient is scheduled for 40 minutes past the hour. The doctor then has 20 minutes to finish with the last three patients and may then get back on schedule before the end of the hour.

Bundle Scheduling

Bundling involves scheduling like-patient activities in blocks of time to increase efficiency.

For example, schedule minor surgical checkups on Monday morning, immunizations on Tuesday afternoon, and routine physical examinations on Wednesday evening, or make Thursday kid’s day and Friday senior citizens day. Do not be too rigid, but by scheduling similar activities together, assembly-line efficiency is achieved without assembly line mentality, and allows you to develop the most economically profitable operational flow process possible for the office.

Patient Self Scheduling (Internet Based Access Management)

New software programs allow patients to schedule their own appointments over the internet. The software allows solo or individual group physicians with a practice to set their own parameters of time, availability and even insurance plans. Through a series of interrogatories, the program confirms each appointment. When the patient arrives, a software tracker communicates with office staff and follows the patients from check-in, to procedures, to checkout.

Today, many hospitals have even abandoned the check-in or admissions, department. It has been replaced by Access Management.

Assessment

The traditional inear patient scheduling system is slowly being abandoned by modern medical practitioners; an all venues (medical practices, clinics, hospitals and various other healthcare entireties).

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Yourmedical practice. Your personal goals. Your financial plan. Our experienced confirmation guide.

***

***

When you know exactly where you are today, have a vision of where you want to be tomorrow, and have trusted counsel at your side, you have already achieved so much success. Marcinko Associates works to keep you at that level of confidence every day. We use a comprehensive economic process to uncover what’s most important to you and then develop a financial strategy that gives you the highest probability of achieving your monetary goals.

We assess, plan, and opine for your success

To accurately see where you are today, chart a strategic path to your goals and help you make the most informed decisions to keep you on financial track, our key services for physicians and high net worth medical clients include:

Investment Portfolio Review

Fee, Charge and Cost Review

Comprehensive Financial Planning

Insurance Reviews

Estate Planning

Investment and Asset Management Second Opinions

We take a deep dive into your financial retirement plans

Physicians and dental employers now have options for how to design and deliver retirement benefits and we can help you make the best choice for your healthcare business. Our services for retirement plans include:

Fee, Charges & Fiduciary Review

Portfolio Analysis

Single Employer Retirement Plan Advisory

Retirement Plans Risk Analysis

Capital Funding and Financing

Business Planning and Practice Valuations

Career Development

and more!

We take a broad and balanced look at your financial life life

We coordinate our recommendations with your other advisors, including attorneys, accountants, insurance professionals and others, to ensure each decision is consistent with your goals and overall strategy. For example, through our partnerships we offer physician colleagues deeper expanded advisory services, like:

Posted on September 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

BREAKING NEWS

Law enforcement officials in Utah released a video of the suspected shooter in the assassination of Turning Point USA co-founder and CEO Charlie Kirk, saying that the person wore Converse tennis shoes and left a hand print and a shoe print at the scene.

The suspect in Charlie Kirk’s assassination has been identified as Tyler Robinson, a 22-year-old Utah resident. Law enforcement sources told the Daily Mail that Robinson was taken into custody as the alleged assassin who killed Kirk at a rally at Utah Valley University on Wednesday.

Before today, forensic podiatry has even made it into the public zeitgeist with the hit TV show “Bones” which premiered on September 13, 2005, and concluded on March 28, 2017, airing for 246 episodes over 12 seasons. The show was based on forensic anthropology and forensic archaeology, with each episode focusing on the mystery behind human body remains brought in for examination and identification.

In one show, eight pairs of dismembered feet washed ashore after a flood on the U.S.-Canada border, but things didn’t add up when only seven pairs of feet were identified as research corpses from a nearby university body farm.

When the fictional Canadian forensic podiatrist Dr. Douglas Filmore took the remains back to Canada, he had to form a jurisdictional alliance with the United States to match the pairs of feet and identify the victims. A rare and expensive pair of sneakers led the team to the victim’s murderer.

In 2016, an actual forensic podiatry club was started at the Barry University School of Podiatric Medicine. And, a formal class covering aspects of forensic podiatry is held at the New York College of Podiatric Medicine. Students exit the class with an in depth knowledge of forensic podiatry and other legal knowledge applicable to current cases.

More expertly, real-life colleague Michael Steven Nirenberg DPMactually testified in the murder trial of defendants Kailie Brackett and Donnell Dana with the state calling three witnesses to testify, including the podiatrist who claimed Brackett’s footprints match the ones found in blood at the apartment of the victim, Kimberly Neptune. The forensic podiatrist focused on the footprints discovered at Neptune’s apartment, using prints and images of the defendant’s feet taken by law enforcement. After study, he claimed the prints at the scene bore a resemblance to Kailie Brackett’s in the width of the foot. The defense questioned the field of forensic podiatry and pressed Dr. Nirenberg on whether the measurements would be altered depending on how thick the sock covering the foot was woven.

Dr. Nirenberg was also interviewed on National Public Radio’s Morning Edition on April 14th 2023 about the gait of the bombing suspect associated with the capital riot on Wednesday January 6th, 2021. Dr. Nirenberg is president of the American Society of Forensic Podiatry and co-editor of the textbook: “Forensic Gait Analysis: Principles and Practice”. The bombing suspect had placed bombs at the DNC and RNC headquarters in Washington, DC on the night before. NPR asked Dr. Nirenberg to comment on the features of the person’s gait.

Additionally, Nirenberg was interviewed by Nancy Grace on her TV show Crime Stories. Grace interviewed Nirenberg about his forensic podiatry work in helping to solve the murder of a mother of 3 who was killed in a church. The case remains unsolved. The episode, “Fitness-Mom Missy Bevers Bludgeoned Dead in Creekside Church” aired June 6th, 2024 and is available online at Merit+ TV.

And, Netflix’s 2023 docu-series, “Till Murder Do Us Part”, recounts the killings of Derek and Nancy Haysom by including a series of interviews with a cast of real people. The four-part docu-series revolves around the unpacking of how a wealthy couple was murdered in Virginia in 1985. It also focuses on how the suspects, Elizabeth Haysom, and her boyfriend, Jens Soehring, betrayed each other during the trial. Dr. Sarah Reel DPM was the forensic podiatrist who was involved with Jens’ and Elizabeth’s footprint examination. Dr. Reel pointed out that, statistically, there was no difference “between a bare footprint and a socked footprint.” The doctor suggested that Jens’ reference footprint matched closely with the crime scene footprint.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Medicine today is vastly different than a generation ago, and all health care professionals need new skills to be successful and reduce the emerging risks outlined in this textbook, as well as the “unknown-unknowns” elsewhere. Traditionally, the physician was viewed as the “captain of the ship”. Today, their role may be more akin to a ship’s navigator, using clinical, teaching skills and knowledge to chart the patient’s course through a confusing morass of insurance requirements, fees, choices, rules and regulations to achieve the best attainable clinical outcomes.

This new leadership paradigm includes many classic business school principles, now modified to fit the decade long PP-ACA, the era of health reform, and modern technical connectivity and EMRs.

Thus, the physician must be a subtle guide on the side; not bombastic sage on the stage. These, newer health 3.0 leadership philosophies might include:

•Negotiation – working to optimize appropriate treatment plans; ie., quality of life versus quantity of life, •Team play – working in concert with other allied healthcare professionals to coordinate care delivery ,ithin a clinically appropriate and cost-effective framework; •Working within the limits of competence – avoiding the pitfalls of the medical generalist versus the specialist that may restrict access to treatment, medications, physicians and facilities by clearly acknowledging when a higher degree of service is needed on behalf of the patient – all while embracing holistic primary care; •Respecting different cultures and values – inherent in the support of the medical Principle of Autonomy is the acceptance of values that may differ from one’s own. As the US becomes more culturally hetero geneous, medical providers are called upon to work within, and respect, the socio-cultural and/or spiritual framework of patients, students and their families; •Seeking clarity on what constitutes marginal care – within a system of finite resources; providers are called upon to openly communicate with patients regarding access to marginal medical information and/or treatments. •Supporting evidence-based practice – healthcare providers, should utilize outcomes data to reduce variation in treatments to achieve higher efficiencies and improved care delivery thru evidence based medicine [EBM]; •Fostering transparency and openness in communications – healthcare professionals should be willing, and prepared, to discuss all aspects of care, especially when discussing end-of-life issues or when problems arise; •Exercising decision-making flexibility – treatment algorithms, templates and clinical pathways are useful tools when used within their scope; but providers must have the authority to adjust the plan if circumstances warrant.

Becoming skilled in the art of listening and interpreting — In her ground-breaking book, Narrative Ethics: Honoring the Stories of Illness, Rita Charon, MD PhD, a professor at Columbia University, writes of the extraordinary value of using the patient’s personal story in the treatment plan. She notes that, “medicine practiced with narrative competence will more ably recognize patients and diseases; convey knowledge and regard, join humbly with colleagues, and accompany patients and their families through ordeals of illness.” In many ways, attention to narrative returns medicine full circle to the compassionate and caring foundations of the patient-physician relationship.

These thoughts represent only a handful of examples to illustrate the myriad of new skills that tomorrows’ healthcare professionals must master in order to meet their timeless professional obligations of compassionate care and contemporary treatment effectiveness; all within the context modern risk management principles.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP™

***

***

When Maria needed $400,000 for a down payment on a new home, her broker at a large Wall Street firm offered a solution: “Don’t sell investments and trigger capital gains. Just take out a margin loan.”

A margin loan is a line of credit from a brokerage firm, secured by the client’s investment portfolio. It offers quick access to cash with no immediate tax consequences and minimal paperwork. But the convenience comes at a cost. As of mid-2025, margin loan interest rates range from 6.25% to over 11%.

Margin loan recommendations are often presented by brokers as tax-savvy strategies that allow clients to access “tax-free” cash while keeping their portfolios intact. In many cases, however, the math benefits the advisor more than the investor. The cost of borrowing often exceeds what an investor is likely to earn by holding on.

For example, let’s assume an interest rate of 7.5% on Maria’s $400,000 margin loan. While borrowing delayed the payment of $20,000 in capital gains tax, she will eventually have to pay that tax anyway unless she holds the investments until her death. Two years later, with portfolio returns of 4% annually, she had earned around $32,000 from the $400,000 in investments she might have sold. Meanwhile, she had paid $60,000 in interest—leaving her some $28,000 worse off. That’s without factoring in ongoing interest payments, or the risks of a margin call if the investments securing the loan drop in value.

Why do advisors keep recommending margin loans? Because selling investments reduces the portfolio size and the advisor’s fee. Borrowing keeps the portfolio intact and the compensation unchanged—while the firm receives additional income from interest on the loan. In some cases, advisors suggest using margin loans to buy more investments, increasing both the portfolio and the fee they collect.

None of this is illegal. But when the borrowing cost is higher than expected returns and the advisor benefits financially, the ethics are questionable. The client takes the risk, while the advisor keeps the revenue.

This kind of conflict appears more often in portfolios where compensation is tied to asset volume and the company’s primary culture rewards gathering assets over delivering unbiased advice. By contrast, fee-only financial planning and investment advisors typically operate on simpler hourly, flat, or tiered fee structures. Their compensation doesn’t depend on whether a client borrows, sells, or holds. The culture of the firm focuses on conflict-free advice aligned with the client’s best interest.

Wall Street brokers are often held to a fiduciary standard, but structure still matters. In 2024 the SEC reported their examinations of brokers would continue to focus on advisor recommendations unduly influenced by the company’s compensation and incentives.

There are rare situations where a margin loan may be appropriate. A client with large unrealized gains might use a short-term margin loan to minimize taxes. An elderly investor might borrow tax-free rather than sell assets that will receive a step-up in basis at their death. Even in those cases, the math must be exact and the client must clearly understand the risks, including the possibility of a margin call.

If your advisor recommends a margin loan, especially to buy more investments, ask strong questions. What’s the interest rate? What return is realistic? What are the tax consequences of selling? How does this affect the advisor’s income?

In a high-rate, low-return environment, margin loans rarely favor the client. The exceptions are narrow. The risks are significant. And the conflict of interest is measurable.

Sometimes the smartest move is the simplest: sell what you need, pay the tax, and leave leverage out of your plan.

Posted on July 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets shrugged off President Trump’s weekend threat of 30% levies against the EU and Mexico, as well as his proposed 100% secondary tariffs against Russia today. Stocks eked out a win across the board, with the NASDAQ climbing to a new record close.

Commodities: Oil prices fell while gold took a breather, but the big winner was orange juice futures, which hit a four-month high thanks to Trump’s promise of 50% tariffs on all imports from Brazil. Coffee prices also climbed.

Posted on July 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Medical doctors, dentists, and podiatrists have to undergo extensive training before they can practice medicine independently. Once they receive training, there are opportunities to increase pay and prestige in the medical field through a series of promotions. As a doctor, how much training, experience and skills you have can determine your ability to move upward in these levels. But, personal branding strategies may even be more vital in today’s social media age?

***

Physician, medical and healthcare branding is more than just the creation of logos, taglines, or specific brand messaging. It’s about creating a meaningful connection between your mission, vision and values and the people served – from patients and their families to local and global communities.

While there are many different types of branding strategies in marketing science, they all share key elements that serve as the foundation for the strategy. These 9 elements for all physicians and medical professionals include the following:

Brand purpose: The reason the physician is in practice and what he/she is trying to achieve.

Brand vision: The ideas and goals behind the dentist which serve as inspiration for practice growth.

Brand values: The osteopaths beliefs and what they stand for.

Target audience: The demographic(s) and patient targets that the podiatrist is aiming to reach.

Market analysis: An analysis of the marketplace that identifies gaps where the chiropractor has an opportunity to position him/her self based on a unique value proposition.

Awareness goals: The initiatives the doctor will take in order to reach a target market patient demographic.

Brand personality: The human-like attributes of the physician that will help build relationships with patients, consumers and other physicians and practitioners.

Brand voice: The language and tone the doctor uses to communicate with patients, physicians and consumers.

Brand tagline: A memorable slogan that sums up the physician and their medical offering in a few choice words.

And so, physician branding is the development of a easily recognizable identity for a medical practice, clinic or healthcare organization that helps to shape perception by current and prospective patients and the wider world.

Posted on June 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Markets: That feeling when you have a $10 trillion rally. To wit:

The S&P 500 closed at a record high this week despite a brief dip as trade tensions with Canada ratcheted up. That puts the index about 20% up from its April low, when the broad tariff announcement sent it spiraling, and up ~5% for the year.

NVIDIA also hit an all-time high, and it keeps edging closer to becoming the first company to hit a $4 trillion valuation.

Life planning and behavioral finance as proposed for physicians and integrated by the Institute of Medical Business Advisors Inc., is unique in that it emanates from a holistic union of personal financial planning, human physiology and medical practice management, solely for the healthcare space. Unlike pure life planning, pure financial planning, or pure management theory, it is both a quantitative and qualitative “hard and soft” science, with an ambitious economic, psychological and managerial niche value proposition never before proposed and codified, while still representing an evolving philosophy. Its’ first-mover practitioners are called Certified Medical Planners™.

Financial Life Planning is an approach to financial planning that places the history, transitions, goals, and principles of the client at the center of the planning process. For the financial advisor or planner, the life of the client becomes the axis around which financial planning develops and evolves.

Financial Life Planning is about coming to the right answers by asking the right questions. This involves broadening the conversation beyond investment selection and asset management to exploring life issues as they relate to money.

Financial Life Planning is a process that helps advisors move their practice from financial transaction thinking, to life transition thinking. The first step is aimed to help clients “see” the connection between their financial lives and the challenges and opportunities inherent in each life transition.

But, for informed physicians, life planning’s quasi-professional and informal approach to the largely isolate disciplines of financial planning and medical practice management is inadequate. Today’s practice environment is incredibly complex, as compressed economic stress from HMOs managed care, financial insecurity from insurance companies, ACOs and VBC, Washington DC and Wall Street; liability fears from attorneys, criminal scrutiny from government agencies, and IT mischief from malicious electronic medical record [eMR] hackers. And economic bench marking from hospital employers; lost confidence from patients; and the Patient Protection and Affordable Care Act [PP-ACA] more than a decade ago. All promote “burnout” and converge to inspire a robust new financial planning approach for physicians and most all medical professionals.

The iMBA Inc., approach to financial planning, as championed by the Certified Medical Planner™ professional certification designation program, integrates the traditional concepts of financial life planning, with the increasing complex business concepts of medical practice management. The former topics are presented in this textbook, the later in our recent companion text: The Business of Medical Practice [Transformational Health 2.0 Skills for Doctors].

***

***

For example, views of medical practice, personal lifestyle, investing and retirement, both what they are and how they may look in the future, are rapidly changing as the retail mentality of medicine is replaced with a wholesale and governmental philosophy. Or, how views on maximizing current practice income might be more profitably sacrificed for the potential of greater wealth upon eventual practice sale and disposition.

Or, how the ultimate fear represented by Yale University economist Robert J. Shiller, in The New Financial Order: Risk in the 21st Century, warns that the risk for choosing the wrong profession or specialty, might render physicians obsolete by technological changes, managed care systems or fiscally unsound demographics. OR, if a medical degree is even needed for future physicians?

Say, what medical license?

Dr. Shirley Svorny, chair of the economics department at California State University, Northridge, holds a PhD in economics from UCLA. She is an expert on the regulation of health care professionals who participated in health policy summits organized by Cato and the Texas Public Policy Foundation. She argues that medical licensure not only fails to protect patients from incompetent physicians, but, by raising barriers to entry, makes health care more expensive and less accessible. Institutional oversight and a sophisticated network of private accrediting and certification organizations, all motivated by the need to protect reputations and avoid legal liability, offer whatever consumer protections exist today.

Yet, the opportunity to revise the future at any age through personal re-engineering, exists for all of us, and allows a joint exploration of the meaning and purpose in life. To allow this deeper and more realistic approach, the informed transformation advisor and the doctor client, must build relationships based on trust, greater self-knowledge and true medical business management and personal financial planning acumen.

[A] The iMBA Philosophy

As you read this ME-P website, we hope you will embrace the opportunity to receive the focused and best thinking of some very smart people. Hopefully, along the way you will self-saturate with concrete information that proves valuable in your own medical practice and personal money journey. Maybe, you will even learn something that is so valuable and so powerful, that future reflection will reveal it to be of critical importance to your life. The contributing authors certainly hope so.

At the Institute of Medical Business Advisors, and thru the Certified Medical Planner™ program, we suggest that such an epiphany can be realized only if you have extraordinary clarity regarding your personal, economic and [financial advisory or medical] practice goals, your money, and your relationship with it. Money is, after only, no more or less than what we make of it.

Ultimately, your relationship with it, and to others, is the most important component of how well it will serve you.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on April 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

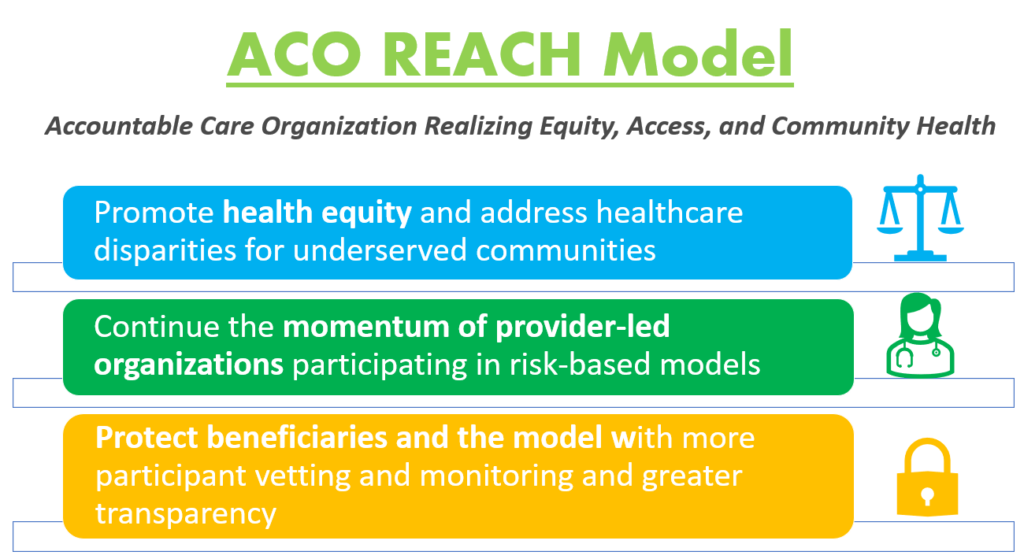

ACCOUNTABLE CARE ORGANIZATIONS

Realizing Equity, Access, and Community Health

By Staff Reporters

***

***

Model Overview

The ACO REACH Model provides novel tools and resources for health care providers to work together in an ACO to improve the quality of care for people with Traditional Medicare. REACH ACOs are comprised of different types of providers, including primary and specialty care physicians.

The ACO REACH Model makes important changes to the previous Global and Professional Direct Contracting (GPDC) Model which include:

***

***

Promote Provider Leadership and Governance. The ACO REACH Model includes policies to ensure doctors and other health care providers continue to play a primary role in accountable care. At least 75% control of each ACO’s governing body generally must be held by participating providers or their designated representatives, compared to 25% during the first two Performance Years of the GPDC Model. In addition, the ACO REACH Model goes beyond prior ACO initiatives by requiring at least two beneficiary advocates on the governing board (at least one Medicare beneficiary and at least one consumer advocate), both of whom must hold voting rights.

Protect Beneficiaries and the Model with More Participant Vetting, Monitoring and Greater Transparency. CMS will ask for additional information on applicants’ ownership, leadership, and governing board to gain better visibility into ownership interests and affiliations to ensure participants’ interests align with CMS’s vision. We will employ increased up-front screening of applicants, robust monitoring of participants, and greater transparency into the model’s progress during implementation, even before final evaluation results, and will share more information on the participants and their work to improve care. Last, CMS will also explore stronger protections against inappropriate coding and risk score growth.

Profitability ratios measure a company’s ability to generate income relative to revenue, balance sheet assets, operating costs, and equity. Common profitability financial ratios include the following:

The gross margin ratio compares the gross profit of a company to its net sales to show how much profit a company makes after paying its cost of goods sold:

Gross margin ratio = Gross profit / Net sales

The operating margin ratio, sometimes known as the return on sales ratio, compares the operating income of a company to its net sales to determine operating efficiency:

Operating margin ratio = Operating income / Net sales

The return on assets ratio measures how efficiently a company is using its assets to generate profit:

Return on assets ratio = Net income / Total assets

The return on equity ratio measures how efficiently a company is using its equity to generate profit:

Return on equity ratio = Net income / Shareholder’s equity

Patient satisfaction occurs when patient perceptions exceed their expectations. They get an intangible “something extra” from their visit, above what they paid for. When patient expectations match their perceptions, mutual obligations are fulfilled, making both practitioner and patient “break-even”.

The clinical result, within a relevant range, is only part of the patient’s perceptions. Numerous sub-conscious impressions comprise the remainder. We’ve all had patients love us despite a less than optimal result. We’ve all had patients angrily leave the practice over some non-clinical matter like a trivial billing dispute. A patient’s perception of any health care service is colored by a vast array of prior experiences that set up current expectations. The patient is pleased to the extent that his current perceptions exceed his/her pre existing expectations. This encompasses far more than the clinical result (within a relevant range), and includes such non-treatment issues as the demeanor of the staff, condition of the physical premises, psychological comfort during the visit, etc.

Remember, all patients talk about you anyway. In the past, a happy patient told four others about what a nice doctor you are. Today, patients post website comments or blogs immediately after their visits. They are more likely to complete treatment and follow instructions, thus obtaining a better medical outcome, and, generating additional fees for the practice. They pay quicker, cause less bad-debt and help create a pleasant environment for us to work in.

An unhappy patient vehemently tells nine others, onground or online, what a nasty greedy rip-off artist you are. Sad, but true! They are not as likely to complete treatment, thus incurring a less than optimal result, and generate fewer fees. They pay slower, if at all, create a stressed environment and detrimentally affect the attitude of other patients in the office.

Try to eliminate problems that might cause negative perceptions (i.e., a filthy restroom) and implement controls that help assure positive perceptions. Patient satisfaction is a soft managerial science. It is a numbers game. Most patients don’t pre-define what would be “acceptable” from this encounter, but have vaguely defined ranges of prior expectations anyway, gleaned from a lifetime of health care related experience. Any variance between these this “acceptable” range of expectations and each trivial encounter invokes some degree positive or negative feeling in the patient.

***

***

The total perception of the office experience is an aggregate of multiple trivial, often subliminal, observations. Patient satisfaction is an intangible and amorphous process complicated by:

Inter patient variables: Significant differences between patients in their “expectations”. Intra patient variables: A single patient can perceive the same thing or situation differently at different times, depending on uncontrollable variables like mood, or, context of occurrence which may (sometimes and/or partially) be controllable by the practice. Luck of the draw” in physical variables: Does Sally or Mary escort the patient to the exam room? Was it the blue or green exam room? Did the last patient to use the rest room, five minutes ago, leave a disgusting mess? Heterogeneous staff variables: Even with appropriate training, people are not machines and have their own quirks.

ASSESSMENT

By proactively anticipating the entire visit, from the patient’s perspective, the practitioner can structure and arrange things such that most patients have, mostly positive perceptions, most of the time. This can be done despite all the potential hetero-genicity of the above factors. Patient satisfaction can be improved in any office, and can be done by anyone.

CONCLUSION

Because patient satisfaction is a multi-faceted amorphous subject, there are multiple correct approaches to the subject and no “cook book” recipe on how to proceed. Try and get the big picture. Identify the worst areas and fix them. Identify the best areas and reinforce them. Proceed slowly. It can be done one facet at a time. Adapt things to your own managerial style and personality. Be completely open to suggestion and change.

Finally, be aware that patient relationship and satisfaction implementation strategies frequently overlap.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on March 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

[Reviewing Terms, Conditions and Selling Agreements]

By Dr. Charles F. Fenton III JD

***

***

Dealing with many issues concerning the actual contract that affect the purchase or sale of a medical practice can be daunting. For example, this chapter will not deal with issue of determining whether or not a physician should retire. Nor will it determine the proper Fair Market Value [FMV] of the practice. However, physicians may be assisted in both instances by a medically focused financial advisor, or valuation specialist. [AVA, CPA-CVA, Certified Medical Planner™; etc] working in conjunction with an experience health care contract attorney to act as an advocate and determine certain contingencies that might occur, and protect him/her from them.

THE PARTIES

The first determination is whether the party at interest is an individual, group of individuals, or an entity (such as a partnership, limited liability partnership, limited partnership, limited liability company, or corporation – whether an S corporation, C corporation or a professional corporation). In many instances, even if the party at interest is an individual is an entity, the individual or individuals behind the entity should be made parties to the agreement.

From the buyer’s perspective, the purchase of a medical practice is a highly person-oriented business. The practice value depends much upon the personality of the current treating physicians. If the current treating physicians are also the owners of the entity, then binding those individuals (especially as applies to the restrictive covenant) is of primary importance.

If the current treating physicians are not owners of the entity, but rather employees, then a determination of whether they will continue in their same positions or whether the buyer will be taking over the treatment of patients becomes the prime focus. If the current treating physicians will be continuing in their same positions, then their current employment contract must be reviewed to determine whether the rights of the seller will accrue to the buyer.

If the rights of the seller will not accrue to the buyer, then the Purchase and Sale Agreement must have a provision that makes the continued employment of those current-treating physicians a condition to consummation of the sale. In such instances, the new employment agreement might be an exhibit to the main agreement and executed contemporaneously with the main agreement.

If the current treating physicians will not be continuing in their same position and if the purchaser will be assuming treatment of the patients, then the main agreement must provide for the dissolution of the employment agreement and provision must be made for restricting the ability of those physicians from competing with the buyer. If the employment contract with the seller contains a restrictive covenant, then the buyer must ensure that such covenants will accrue to the buyers benefit. Otherwise, the buyer should insist that those physicians sign restrictive covenants. In such an instance, a portion of the purchase price may need to be allocated towards the consideration for those restrictive covenants and paid directly to those physicians.

DATE OF AGREEMENT AND CLOSING DATE

In general, it usually does not matter when the agreement is dated. It should usually be dated once all the terms are agreed to and the parties desire to bind each other and to be bound. In certain instance, the parties may have reached an agreement, but certain issues (such as the obtaining of a state license to practice medicine) may be outstanding. In such a case, then an option can be given by either the seller or the buyer to bind the other to sell or buy the practice upon exercise of the option. Giving an option can also push the agreement date into the future. The option will usually be given with token consideration (e.g., one hundred dollars) and will have a fixed expiration date (e.g., thirty to ninety days).

The determination of the closing date is more important than the date that the agreement is dated. Just like in the purchase of a house where certain issues (such as obtaining a mortgage and home inspection) must occur before closing, in the purchase of a practice, there may be certain issues which require time to undertake before the actual transfer can be consummated. For example, the buyer may still need to obtain financing or the landlord may need to approve the assignment of the lease.

RECITALS

The recitals – or “whereas” clauses – traditionally enunciate the reasons the parties are entering into the agreement. In the sale of the practice the recitals may simply state that the buyer wishes to buy the practice and the seller wishes to sell the practice. Yet, there is a modern growing tendency among contract attorneys to eliminate the “whereas” clauses as some attorneys feel that such language is antiquated. In such instances, the agreement will simply have a paragraph or two delineation of the “Purpose” of the agreement.

ARTICLES, SECTIONS, AND PARAGRAPHS

The agreement will often be divided and numbered in some logical fashion, either into articles, sections, paragraphs, or a combination of these. The reason for doing so is twofold. First, it allows ready reference to the numbered paragraph, and secondly it allows the agreement to be divided and grouped in logical associations.

BINDING THE PARTIES