BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

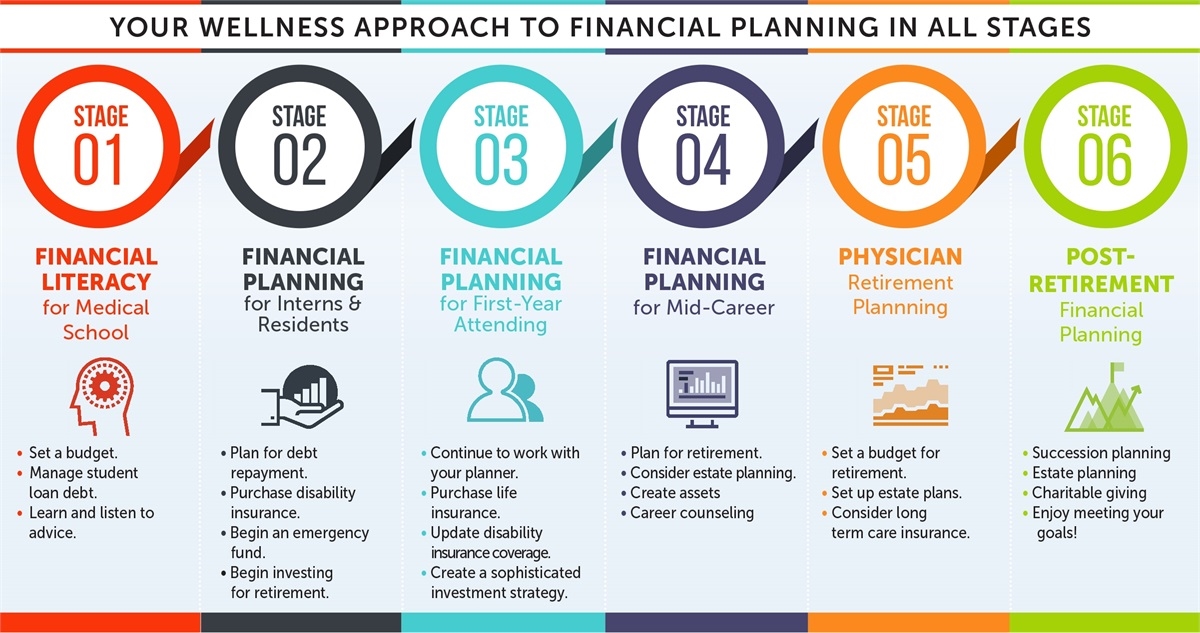

Investing may seem complicated, but today there are many ways for the newly minted physician [MD, DO, DPM, DMD or DDS] to begin, even with minimal knowledge and only a small amount to invest. Starting as soon as possible will help you get closer to the retirement you deserve.

***

Why is investing important?

Investing often feels like a luxury reserved for the already wealthy physician. Many of us find it difficult to think about investing for the future when there are so many things we need that money for right now; medical school loans, auto, home and children; etc. But, at some point, we’re going to want to stop working and enjoy retirement. And simply put, retirement is expensive.

Most calculations advise that you aim for enough savings to give you 70% to 80% of your pre-retirement income for 20 years or more. Depending on your goals for retirement, that means you could need between $500,000 and $1 million in savings by the time you retire. That may not sound attainable, but with the power of compounding growth, it’s not as hard to achieve as you think. The key is starting as soon as possible and making smart choices.

The short answer is “now,” no matter what your age. Due to the way the gains in investments can compound, the earlier you start the better. Money invested in your 20s could very easily grow over 20 times before you retire, without you having to do much.That is powerful. Even if you’re in your 50s or older, you can still make significant progress toward meeting your goals in retirement.

How much should you invest per month?

Most financial experts say you should invest 10% to 15% of your annual income for retirement. That’s the goal, but you don’t have to get there immediately. Whatever you can start investing today is going to help you down the road.

So, if 10% to 15% is too much right now, start small and build toward that goal over time. You can actually start investing with $5 if you want. And you should. Some investment products require a minimum investment, but there are plenty that don’t, and a lot of online brokerage accounts can be started for free.

The best investments for you are going to depend on your age, goals, and strategy. The important thing is to get started. You’ll learn as you go. If you have questions, a dedicated DIYer or investment advisor can help give you the guidance and options you need.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Fundamentals of Physician Investing

By Daniel B. Moisand CFP®, and ME-P staff

It used to be that the only way to get investments and investment information was through paying commissions to a traditional broker. Then in the 70’s (specifically, May, 1975) the brokerage industry went through significant deregulation allowing for the discounting of commissions. Charles Schwab and Company, among others, was able to eliminate the advice component and offer trades at dramatically reduced rates. The full service brokerage business responded by emphasizing the scope of their services namely research and advice in order to compete. The demand for both has continued to grow, even though research information is now readily available through many sources. These brokerage firms continue to thrive despite their poor performance in analyzing tech stocks and the Enron and Global Grossing debacles. More recent debacles in 2008-09, the flash crash a decade ago and more recent developments are legion, as well.

Fundamental Flaws

The fundamental flaw with these firms is the array of conflicts of interest between the firm and its customers. While the incentive to trade has been well chronicled as a conflict, these firms have not let consumer’s demand for a better-aligned compensation arrangement go unnoticed. Fee-based account relationships have proliferated accordingly. In theory, this type of arrangement, usually a percentage of assets, gives an incentive for performance and service rather than trade activity. This certainly has merit. However, conflicts remain that should be considered.

Pay to Play

The practice of paying brokers, higher levels of compensation for in-house products was commonplace. Today, explicitly higher payouts still exist but are less common. Instead, many firms use the sale of proprietary mutual funds and other products as part of management’s compensation. Other forms of non-monetary compensation such as a better office can be used as incentive for the brokers. The greater profitability of these in-house offerings will keep this conflict around for some time.

Subtle Conflicts of Interest

Less obvious is the conflict between the investment banking arm, the research department, and the retail brokerage operations of a firm. Even firms with no proprietary funds to sell may grapple with this issue. Here, research is pressured to say favorable things about a particular company’s stock by the investment bankers in hopes of obtaining more of that company’s business. When a firm brings a company public odds are great that a “strong buy” rating will come with the IPO. Of course, the lesson remains – consider the source.

Assessment

Traditional brokers have a somewhat higher standard of accountability than the on-line firms as to their accountability. If you buy the stock of a company that goes bankrupt through an on-line broker you have little recourse. After all, that was your choice. If a full-service broker recommended the stock to you, that broker will have to defend the recommendation.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Written by doctors and healthcare professionals, this textbook should be mandatory reading for all medical school students—highly recommended for both young and veteran physicians—and an eliminating factor for any financial advisor who has not read it. The book uses jargon like ‘innovative,’ ‘transformational,’ and ‘disruptive’—all rightly so! It is the type of definitive financial lifestyle planning book we often seek, but seldom find. —LeRoy Howard MA CMPTM,Candidate and Financial Advisor, Fayetteville, North Carolina I taught diagnostic radiology for over a decade. The physician-focused niche information, balanced perspectives, and insider industry transparency in this book may help save your financial life. —Dr. William P. Scherer MS, Barry University, Ft. Lauderdale, Florida This book was crafted in response to the frustration felt by doctors who dealt with top financial, brokerage, and accounting firms. These non-fiduciary behemoths often prescribed costly wholesale solutions that were applicable to all, but customized for few, despite ever-changing needs. It is a must-read to learn why brokerage sales pitches or Internet resources will never replace the knowledge and deep advice of a physician-focused financial advisor, medical consultant, or collegial Certified Medical Planner™ financial professional. —Parin Khotari MBA,Whitman School of Management, Syracuse University, New York In today’s healthcare environment, in order for providers to survive, they need to understand their current and future market trends, finances, operations, and impact of federal and state regulations. As a healthcare consulting professional for over 30 years supporting both the private and public sector, I recommend that providers understand and utilize the wealth of knowledge that is being conveyed in these chapters. Without this guidance providers will have a hard time navigating the supporting system which may impact their future revenue stream. I strongly endorse the contents of this book.—Carol S. Miller BSN MBA PMP,President, Miller Consulting Group, ACT IAC Executive Committee Vice-Chair at-Large, HIMSS NCA Board Member This is an excellent book on financial planning for physicians and health professionals. It is all inclusive yet very easy to read with much valuable information. And, I have been expanding my business knowledge with all of Dr. Marcinko’s prior books. I highly recommend this one, too. It is a fine educational tool for all doctors.—Dr. David B. Lumsden MD MS MA,Orthopedic Surgeon, Baltimore, Maryland There is no other comprehensive book like it to help doctors, nurses, and other medical providers accumulate and preserve the wealth that their years of education and hard work have earned them. —Dr. Jason Dyken MD MBA,Dyken Wealth Strategies, Gulf Shores, Alabama I plan to give a copy of this book written ‘by doctors and for doctors’ to all my prospects, physician, and nurse clients. It may be the definitive text on this important topic. —Alexander Naruska CPA,Orlando, Florida

Health professionals are small business owners who need to apply their self-discipline tactics in establishing and operating successful practices. Talented trainees are leaving the medical profession because they fail to balance the cost of attendance against a realistic business and financial plan. Principles like budgeting, saving, and living below one’s means, in order to make future investments for future growth, asset protection, and retirement possible are often lacking. This textbook guides the medical professional in his/her financial planning life journey from start to finish. It ranks a place in all medical school libraries and on each of our bookshelves. —Dr. Thomas M. DeLauro DPM,Professor and Chairman – Division of Medical Sciences, New York College of Podiatric Medicine

Physicians are notoriously excellent at diagnosing and treating medical conditions. However, they are also notoriously deficient in managing the business aspects of their medical practices. Most will earn $20-30 million in their medical lifetime, but few know how to create wealth for themselves and their families. This book will help fill the void in physicians’ financial education. I have two recommendations: 1) every physician, young and old, should read this book; and 2) read it a second time! —Dr. Neil Baum MD,Clinical Associate Professor of Urology, Tulane Medical School, New Orleans, Louisiana

I worked with a Certified Medical Planner™ on several occasions in the past, and will do so again in the future. This book codified the vast body of knowledge that helped in all facets of my financial life and professional medical practice. —Dr. James E. Williams DABPS, Foot and Ankle Surgeon, Conyers, Georgia

This is a constantly changing field for rules, regulations, taxes, insurance, compliance, and investments. This book assists readers, and their financial advisors, in keeping up with what’s going on in the healthcare field that all doctors need to know. —Patricia Raskob CFP® EA ATA, Raskob Kambourian Financial Advisors, Tucson, Arizona I particularly enjoyed reading the specific examples in this book which pointed out the perils of risk … something with which I am too familiar and have learned (the hard way) to avoid like the Black Death. It is a pleasure to come across this kind of wisdom, in print, that other colleagues may learn before it’s too late— many, many years down the road. —Dr. Robert S. Park MD, Robert Park and Associates Insurance, Seattle, Washington

Although this book targets physicians, I was pleased to see that it also addressed the financial planning and employment benefit needs of nurses; physical, respiratory, and occupational therapists; CRNAs, hospitalists, and other members of the health care team….highly readable, practical, and understandable. —Nurse Cecelia T. Perez RN, Hospital Operating Room Manager, Ellicott City, Maryland

Personal financial success in the PP-ACA era will be more difficult to achieve than ever before. It requires the next generation of doctors to rethink frugality, delay gratification, and redefine the very definition of success and work–life balance. And, they will surely need the subject matter medical specificity and new-wave professional guidance offered in this book. This book is a ‘must-read’ for all health care professionals, and their financial advisors, who wish to take an active role in creating a new subset of informed and pioneering professionals known as Certified Medical Planners™. —Dr. Mark D. Dollard FACFAS, Private Practice, Tyson Corner, Virginia As healthcare professionals, it is our Hippocratic duty to avoid preventable harm by paying attention. On the other hand, some of us are guilty of being reckless with our own financial health—delaying serious consideration of investments, taxation, retirement income, estate planning, and inheritances until the worry keeps one awake at night. So, if you have avoided planning for the future for far too long, perhaps it is time to take that first step toward preparedness. This in-depth textbook is an excellent starting point—not only because of its readability, but because of his team’s expertise and thoroughness in addressing the intricacies of modern investments—and from the point of view of not only gifted financial experts, but as healthcare providers, as well … a rare combination. —Dr. Darrell K. Pruitt DDS, Private Practice Dentist, Fort Worth, Texas This text should be on the bookshelf of all contemporary physicians. The book is physician-focused with unique topics applicable to all medical professionals. But, it also offers helpful insights into the new tax and estate laws, fiduciary accountability for advisors and insurance agents, with investing, asset protection and risk management, and retirement planning strategies with updates for the brave new world of global payments of the Patient Protection and Affordable Care Act. Starting out by encouraging readers to examine their personal ‘money blueprint’ beliefs and habits, the book is divided into four sections offering holistic life cycle financial information and economic education directed to new, mid-career, and mature physicians.

This structure permits one to dip into the book based on personal need to find relief, rather than to overwhelm. Given the complexity of modern domestic healthcare, and the daunting challenges faced by physicians who try to stay abreast of clinical medicine and the ever-evolving laws of personal finance, this textbook could not have come at a better time. —Dr. Philippa Kennealy MD MPH, The Entrepreneurial MD, Los Angeles, California Physicians have economic concerns unmatched by any other profession, arriving ten years late to the start of their earning years. This textbook goes to the core of how to level the playing field quickly, and efficaciously, by a new breed of dedicated Certified Medical Planners™. With physician-focused financial advice, each chapter is a building block to your financial fortress. —Thomas McKeon, MBA, Pharmaceutical Representative, Philadelphia, Pennsylvania An excellent resource … this textbook is written in a manner that provides physician practice owners with a comprehensive guide to financial planning and related topics for their professional practice in a way that is easily comprehended. The style in which it breaks down the intricacies of the current physician practice landscape makes it a ‘must-read’ for those physicians (and their advisors) practicing in the volatile era of healthcare reform. —Robert James Cimasi, MHA ASA FRICS MCBA CVA CM&AA CMP™, CEO-Health Capital Consultants, LLC, St. Louis, Missouri Rarely can one find a full compendium of information within a single source or text, but this book communicates the new financial realities we are forced to confront; it is full of opportunities for minimizing tax liability and maximizing income potential. We’re recommending it to all our medical practice management clients across the entire healthcare spectrum. —Alan Guinn, The Guinn Consultancy Group, Inc., Cookeville, Tennessee Dr. David Edward Marcinko MBA CMP™ and his team take a seemingly endless stream of disparate concepts and integrate them into a simple, straightforward, and understandable path to success. And, he codifies them all into a step-by-step algorithm to more efficient investing, risk management, taxation, and enhanced retirement planning for doctors and nurses. His text is a vital read—and must execute—book for all healthcare professionals and physician-focused financial advisors. —Dr. O. Kent Mercado, JD, Private Practitioner and Attorney, Naperville, Illinois

Kudos. The editors and contributing authors have compiled the most comprehensive reference book for the medical community that has ever been attempted. As you review the chapters of interest and hone in on the most important concerns you may have, realize that the best minds have been harvested for you to plan well… Live well. —Martha J. Schilling; AAMS® CRPC® ETSC CSA, Shilling Group Advisors, LLC, Philadelphia, Pennsylvania I recommend this book to any physician or medical professional that desires an honest no-sales approach to understanding the financial planning and investing world. It is worthwhile to any financial advisor interested in this space, as well. —David K. Luke, MIM MS-PFP CMP™, Net Worth Advisory Group, Sandy, Utah Although not a substitute for a formal business education, this book will help physicians navigate effectively through the hurdles of day-to-day financial decisions with the help of an accountant, financial and legal advisor. I highly recommend it and commend Dr. Marcinko and the Institute of Medical Business Advisors, Inc. on a job well done. —Ken Yeung MBA CMP™, Tseung Kwan O Hospital, Hong Kong I’ve seen many ghost-written handbooks, paperbacks, and vanity-published manuals on this topic throughout my career in mental healthcare. Most were poorly written, opinionated, and cheaply produced self-aggrandizing marketing drivel for those agents selling commission-based financial products and expensive advisory services. So, I was pleasantly surprised with this comprehensive peer-reviewed academic textbook, complete with citations, case examples, and real-life integrated strategies by and for medical professionals. Although a bit late for my career, I recommend it highly to all my younger colleagues … It’s credibility and specificity stand alone. —Dr. Clarice Montgomery PhD MA,Retired Clinical Psychologist In an industry known for one-size-fits-all templates and massively customized books, products, advice, and services, the extreme healthcare specificity of this text is both refreshing and comprehensive. —Dr. James Joseph Bartley, Columbus, Georgia

My brother was my office administrator and accountant. We both feel this is the most comprehensive textbook available on financial planning for healthcare providers. —Dr. Anthony Robert Naruska DC,Winter Park, Florida

The physician, nurse, or other medical professional should easily recognize that there are a vast array of opportunities, obstacles, and pitfalls when it comes to managing one’s finances. Still, with some modicum of effort, the basic aspects of insurance, investments, taxes, accounting, portfolio management, retirement and estate planning, debt reduction, asset protection and practice management can be largely self-taught. Yet, it is realized that nuances and subtleties can make a well-intentioned financial plan fall short. The devil truly is in the details. Moreover, none of these areas can be addressed in isolation. It is common for a solution in one area to cause a new set of problems in another.

Accordingly, most health care practitioners would be well served to hire [independent, hourly compensated and prn] financial help. Unlike some medical problems, financial issues may not cause any “pain” or other obvious symptoms. Medical professionals tend to have far more complex financial situations than most lay people. Despite the complexities of the new world of health reform, far too many either do nothing; or give up all control totally, to an external advisor. This either/or mistake can be costly in many ways, and should be avoided.

In reality, and at various time in their careers, the medical professional needs a team comprised of at least a financial analyst, lawyer, management consultant, risk manager [actuary, mathematician or insurance counselor] and accountant. At various points in time, each member of the team, or significant others, will properly assume a role of more or less importance, but the doctor must usually remain the “quarterback” or leader; in the absence of a truly informed other, or Certified Medical Planner™.

This is necessary because only the doctor has the personal self-mandate with skin in the game, to take a big picture view. And, rightly or wrongly, investments dominate the information available regarding personal finance and the attention of most physicians. One is much more likely to need or want to discuss the financial markets with their financial advisor than private letter rulings by the IRS, or with their estate planning attorney or tax accountant. While hiring for expertise is a good idea, there is sinister way advisors goad doctors into using all their retail services; all of the time. That artifice is – the value of time.

True integrated physician focused and financial planning is at its core a service business, not a product or sales endeavor. And, increasingly money is more likely to be at the top of the list for providers as the healthcare environment is contracting.

So, eschewing the quarterback model of advice, and choosing to self-educate thru this book and elsewhere, may be one of the best efforts a smart physician can make.

Dr. David Edward Marcinko, editor-in-chief, is a next-generation apostle of Nobel Laureate Kenneth Joseph Arrow, PhD, as a health-care economist, insurance advisor, financial advisor, risk manager, and board-certified surgeon from Temple University in Philadelphia. In the past, he edited eight practice-management books, three medical textbooks and manuals in four languages, five financial planning yearbooks, dozens of interactive CD-ROMs, and three comprehensive health-care administration dictionaries. Internationally recognized for his clinical work, he is a distinguished visiting professor of surgery and a recipient of an honorary Bachelor of Medicine–Bachelor of Surgery (MBBS) degree from Marien Hospital in Aachen, Germany. He provides litigation support and expert witness testimony in state and federal court, with medical publications archived in the Library of Congress and the Library of Medicine at the National Institutes of Health.

Posted on March 2, 2014 by Dr. David Edward Marcinko MBA MEd CMP™

Purchase today and Profit in 2014

By Ann Miller RN MHA

[Executive-Director]

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to write a book review or check out our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

The demands on medical practitioners today can seem overwhelming. It’s no secret that health-care delivery is changing, and those changes are reflected in the financial issues that health-care professionals face every day. You must continually educate yourself about new research in your chosen specialty, stay current on the latest technology that is transforming health care, and pay attention to business considerations, including ever-changing state and federal insurance regulations.

Like many, you may have transitioned from medical school and residency to being on your own with little formal preparation for the substantial financial issues you now face. Even the day-to-day concerns that affect most people–paying college tuition bills or student loans, planning for retirement, buying a home, insuring yourself and your business–may be complicated by the challenges and rewards of a medical practice. It’s no wonder that many medical practitioners look forward to the day when they can relax and enjoy the fruits of their labors.

Unfortunately, substantial demands on your time can make it difficult for you to accurately evaluate your financial plan, or monitor changes that can affect it. That’s especially true given ongoing health care reform efforts that will affect the future of the industry as a whole. Just as patients need periodic checkups, you may need to work with a financial professional to make sure your finances receive the proper care.

Maximizing your personal assets

Much like medicine, the field of finance has been the subject of much scientific research and data, and should be approached with the same level of discipline and thoughtfulness. Making the most of your earning years requires a plan for addressing the following issues.

Retirement

Your years of advanced training and perhaps the additional costs of launching and building a practice may have put you behind your peers outside the health-care field by a decade or more in starting to save and invest for retirement. You may have found yourself struggling with debt from years of college, internship, and residency; later, there’s the ongoing juggling act between making mortgage payments, caring for your parents, paying for weddings and tuition for your children, and maybe trying to squeeze in a vacation here and there. Because starting to save early is such a powerful ally when it comes to building a nest egg, you may face a real challenge in assuring your own retirement. A solid financial plan can help.

Investments

Getting a late start on saving for retirement can create other problems.

For example, you might be tempted to try to make up for lost time by making investment choices that carry an inappropriate level or type of risk for you. Speculating with money you will need in the next year or two could leave you short when you need that money. And once your earnings improve, you may be tempted to overspend on luxuries you were denied during the lean years. One of the benefits of a long-range financial plan is that it can help you protect your assets–and your future–from inappropriate choices.

Tuition

Many medical professionals not only must pay off student loans, but also have a strong desire to help their children with college costs, precisely because they began their own careers saddled with large debts.

Tax considerations

Once the lean years are behind you, your success means you probably need to pay more attention to tax-aware investing strategies that help you keep more of what you earn.

Using preventive care

The nature of your profession requires that you pay special attention to making sure you are protected both personally and professionally from the financial consequences of legal action, a medical emergency of your own, and business difficulties. Having a well-defined protection plan can give you confidence that you can practice your chosen profession without putting your family or future in jeopardy.

Liability insurance

Medical professionals are caught financially between rising premiums for malpractice insurance and fixed reimbursements from managed-care programs and you may find yourself evaluating a variety of approaches to providing that protection. Some physicians also carry insurance that protects them against unintentional billing errors or omissions.

Remember that in addition to potential malpractice claims, you also face the same potential liabilities as other business owners. You might consider an umbrella policy as well as coverage that protects against business-related exposures such as fire, theft, employee dishonesty, or business interruption.

Disability insurance

Your income depends on your ability to function, especially if you’re a solo practitioner, and you may have fixed overhead costs that would need to be covered if your ability to work were impaired. One choice you’ll face is how early in your career to purchase disability insurance. Age plays a role in determining premiums, and you may qualify for lower premiums if you are relatively young. When evaluating disability income policies, medical professionals should pay special attention to how the policy defines disability. Look for a liberal definition such as “own occupation,” which can help ensure that you’re covered in case you can’t practice in your chosen specialty.

To protect your business if you become disabled, consider business overhead expense insurance that will cover routine expenses such as payroll, utilities, and equipment rental. An insurance professional can help evaluate your needs.

Practice management and business planning

Is a group practice more advantageous than operating solo, taking in a junior colleague, or working for a managed-care network? If you have an independent practice, should you own or rent your office space? What are the pros and cons of taking over an existing practice compared to starting one from scratch? If you’re part of a group practice, is the practice structured financially to accommodate the needs of all partners? Does running a “concierge” or retainer practice appeal to you? If you’re considering expansion, how should you finance it?

Questions like these are rarely simple and should be done in the context of an overall financial plan that takes into account both your personal and professional goals.

Many physicians have created processes and products for their own practices, and have then licensed their creations to a corporation. If you are among them, you may need help with legal and financial concerns related to patents, royalties, and the like. And if you have your own practice, you may find that cash flow management, maximizing return on working capital, hiring and managing employees, and financing equipment purchases and maintenance become increasingly complex issues as your practice develops.

Practice valuation

You may have to make tradeoffs between maximizing current income from your practice and maximizing its value as an asset for eventual sale. Also, timing the sale of a practice and minimizing taxes on its proceeds can be complex. If you’re planning a business succession, or considering changing practices or even careers, you might benefit from help with evaluating the financial consequences of those decisions.

Estate planning

Estate planning, which can both minimize taxes and further your personal and philanthropic goals, probably will become important to you at some point. Options you might consider include:

Life insurance

Buy-sell agreements for your practice

Charitable trusts

You’ve spent a long time acquiring and maintaining expertise in your field, and your patients rely on your specialized knowledge. Doesn’t it make sense to treat your finances with the same level of care?

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 11, 2011 by Dr. David Edward Marcinko MBA MEd CMP™

Physician Retirement Planning –in the news– too!

[Reprinted from Medical News, Inc.]

By Ann Miller RN MHA

[Executive-Director]

Our ME-P Founder and Publisher-in-Chief, Dr. David Edward Marcinko FACFAS, MBA, CMP™, was recently interviewed by investigative reporter Sharon H. Fitzgerald of the Medical News magazine and newspaper for physicians. Here is a synopsis and copy of that article, along with the words of financial advisor Mr. Paul Larson, CFP™.

Physicians Have Unique Challenges and Opportunities

Physicians today “are getting squeezed from both ends” when it comes to their finances, according Mr. Larson, president of Larson Financial Group. On one end, collections and reimbursements are down; on the other end, taxes are up.

That’s why financial planning, including a far-sighted strategy for retirement, is a necessity.

CEO – Institute of Medical Business Advisors, Inc

Dr. Marcinko’s retirement investment advice – and it’s the same iMBA Inc advice he gives to anyone – is to invest first [fifteen] 15, and then [twenty] 20 percent [%], of your income in a world-wide indexed mutual fund for the next 50 [fifty] years, or so!

“We all want to make it more complicated than it is, don’t we?” he said.

With a professional readership composed of physicians and key industry decision makers, the Medical News magazine and paper is the only local professional publication devoted entirely to healthcare issues that impact both clinical and administrative best practices. Monthly focus features on a variety of clinical and business topics allow the Medical News to zero in on medical advances, regulatory issues and innovative ways to enhance reader’s bottom line.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on March 4, 2010 by Dr. David Edward Marcinko MBA MEd CMP™

Moneywise?

By Somnath Basu; PhD, MBA

For those of us between the ages of 45 to 54, the thought of retirement should be popping up a few times these days. And, for doctors between ages 55 and 64, the thought may be taking on urgent tones. Many of us are reconciling to the idea that it may be a fact that we have to either postpone our retirements or live a much simpler life during retirement. Whatever the thoughts may be, what’s driving them is our preparedness to retire.

Preparedness Components

So, we will now examine what the component (dos and don’ts) may be for physicians, and others, to assess whether they are on the right path in their preparations to retire. It is somewhat easier if we consider the preparedness issues of the expectant retirees along the two age groups we tagged earlier. It is possible that we may find that the proper components of our retirement plans may already exist for us and we need to give them a good and disciplined effort to carry us through in the retirement years. It is also important to note, in this vein, that as a nation, our savings rate has gone from -0.6% in 2006 to about 5% today. While most of the increase in savings is the result of people building back an emergency nest egg, we can also take heart in the fact that the savings habit has not become obsolete or even rusty, and given the proper motivation (e.g. a sub-standard retired lifestyle), we can alter our destinies by riding on the same savings wave.

The Possibilities

Let us begin by describing the possibilities for the younger group (ages 45-54) doctors and employees pondering their retirement moves. There are two aspects of retirement that needs consideration. First is the contemplation of the needs associated with retirement lifestyles and the corresponding financial requirements required to sustain such lifestyles.

The second is to consider our current lifestyles, living standards (consumption), our income and savings and to assess whether we are set to achieve our retirement lifestyle targets. To understand the many possibilities, we will examine some typical scenarios using data from the Employee Benefits Research Institute (EBRI). Note that all calculations are only approximations for a typical individual.

Example:

If you are about 50 years of age, have worked and saved for about 20 years [401(k), or 403(b)] or other pension plan) and earn about $100,000 a year, you should have about $200,000 in your retirement account today. Assuming that Social Security (if the organization remains viable and makes its required payouts), covers about 27% of your needed retirement expenses. You could expect a Social Security payment of about $30,000 per year at age 65. This would mean that in about 15 years, you would need to generate an additional $80,000 per year from your own savings. While you may think that you are not consuming $110,000 worth of lifestyle today, it is useful to note that this estimate is in future (and inflated) dollar terms.

This brings us back to the second question of how much you may be consuming today. If you are paying about 25% as taxes and saving another 5%, then you are currently spending about $70,000 today. At a 3% inflation rate, in 15 years this amounts to a spending of $110,000 on an income of approximately $160,000.

Thus, if your 403(b) balance does not change from now till retirement and you estimate to plan for a 25 year retirement phase, then your 403(b) account will be equivalent to about an additional $8,000 per year, which itself will grow every year minimally at the inflation rate.

If you assume the 403(b) plan will itself grow at about 7% a year over the next 40 years (from ages 50 to 90) then at retirement (age 65) you’ll have about $550,000 and be able to withdraw about $50,000 per year. This will leave you with a shortfall of $30,000 per year. To be able to afford retirement to its fullest, you’ll need to save an additional $15,000 per year for the next 15 years. Before you begin thinking that is a doable task and start assessing which parts of current lifestyle to pare, note that many of the assumptions above may not hold true.

Average Rates of Return

For example, earning a 7% average rate of return over 40 years is no simple task; Social Security may not be able to deliver on its promise. Physician income and job security is a political issue. Paring current lifestyle is a bigger issue. Healthcare and leisure types of costs during retirement may increase by more than 3%, even as you consume more of these retirement lifestyle services.

Therefore, you may want to continue enjoying your current medical practice lifestyle and consider worrying about retirement about 10 years (or more) later or you may take stock of your current situation. If your situation is worse than the average portrayed above, a big issue for you is to keep your physical and mental health well balanced and not depressed and medicated; plan to postpone retirement and practice or work longer, albeit in good health.

Assessment

If you are about 60 years of age, have worked for about 25-30 years, earn $100,00 per year and have about $350,000 in your retirement accounts, your problems are more exacerbated and your fears (of postponing retirement, paring current or future lifestyle or not being able to make up shortfalls) are much more real. The strategies remain the same from earlier in that you have to make some urgent and difficult decisions. These are decisions that cannot be postponed any longer.

Note: First released “All Things Financial Planning Blog” on December 18, 2009.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES: