BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

An Internet Protocol (IP) address is a numerical identifier assigned to network interfaces participating in an IP‑based network. It functions as the cornerstone of packet‑switched communication, enabling devices to locate, identify, and exchange data across interconnected networks. At a technical level, an IP address encodes both host identity and network topology, allowing routers to forward packets efficiently through hierarchical addressing structures.

IP Address Structure and Protocol Versions

The two dominant versions of the Internet Protocol—IPv4 and IPv6—define the format and semantics of IP addressing.

IPv4, defined in RFC 791, uses a 32‑bit address space. These 32 bits are typically represented in dotted‑decimal notation, divided into four octets. The address space provides possible addresses, roughly 4.3 billion. IPv4 addresses are logically divided into network and host portions, historically using classful addressing (Classes A, B, C), though modern networks rely on Classless Inter‑Domain Routing (CIDR). CIDR allows arbitrary prefix lengths, expressed as a suffix such as /24, enabling more efficient allocation and route aggregation.

IPv6, defined in RFC 8200, expands the address space to 128 bits, represented in eight groups of hexadecimal values separated by colons. The enormous address space— possible addresses—supports hierarchical routing, stateless address autoconfiguration (SLAAC), and built‑in support for multicast and anycast addressing. IPv6 eliminates broadcast traffic entirely, replacing it with more efficient multicast mechanisms.

Address Types and Scopes

IP addresses can be categorized by scope and function:

Unicast: Identifies a single network interface. Most traffic on the internet is unicast.

Multicast: Identifies a group of interfaces; packets are delivered to all group members.

Broadcast (IPv4 only): Targets all hosts on a local network segment.

Anycast (primarily IPv6): Assigned to multiple interfaces; packets are routed to the nearest instance based on routing metrics.

Additionally, addresses can be public (globally routable) or private (RFC 1918 for IPv4, Unique Local Addresses for IPv6). Private addresses require Network Address Translation (NAT) to communicate with the public internet, a workaround that became essential due to IPv4 exhaustion.

Static vs. Dynamic Assignment

IP addresses may be assigned statically or dynamically:

Static addressing involves manual configuration and is common for servers, routers, and infrastructure requiring predictable reachability.

Dynamic addressing uses the Dynamic Host Configuration Protocol (DHCP). DHCP automates address assignment, lease renewal, and configuration of parameters such as default gateways and DNS servers.

In IPv6 networks, dynamic assignment may use DHCPv6 or SLAAC. SLAAC allows hosts to generate their own addresses using router advertisements and interface identifiers, reducing administrative overhead.

Routing and Packet Delivery

IP addresses are integral to routing—the process by which packets traverse networks. When a host sends a packet, it encapsulates data in an IP header containing source and destination addresses. Routers examine the destination address and consult their routing tables to determine the next hop. Routing protocols such as OSPF, BGP, and IS‑IS maintain these tables by exchanging topology information.

The hierarchical nature of IP addressing enables route aggregation, reducing the size of global routing tables. For example, a provider may advertise a single /16 prefix representing thousands of customer networks.

DNS and Address Resolution

Human‑readable domain names must be translated into IP addresses before communication can occur. The Domain Name System (DNS) performs this translation. When a user enters a URL, the system queries DNS resolvers, which return the corresponding A (IPv4) or AAAA (IPv6) records.

On local networks, the Address Resolution Protocol (ARP) maps IPv4 addresses to MAC addresses. IPv6 uses Neighbor Discovery Protocol (NDP) for similar functionality, leveraging ICMPv6 messages.

Security and Privacy Considerations

IP addresses reveal network topology and can expose approximate geographic location. Attackers may use them for reconnaissance, scanning, or targeted attacks. Techniques such as NAT, VPNs, and IPv6 privacy extensions help mitigate exposure by masking or rotating interface identifiers.

Conclusion

An IP address is far more than a simple identifier; it is a fundamental component of the Internet Protocol suite, enabling routing, addressing, and communication across global networks. Its structure, allocation mechanisms, and interaction with routing and resolution protocols form the backbone of modern digital infrastructure. As the internet continues to scale and diversify, the role of IP addressing—particularly IPv6—remains central to the performance, security, and scalability of global communication systems.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

A Comparative Essay

Retirement planning is a cornerstone of financial security, and employers often provide structured plans to help employees prepare for the future. Two prominent options are Defined Benefit (DB) Plans and Cash Balance Plans. While both fall under the umbrella of employer-sponsored retirement programs, they differ significantly in design, funding, and how benefits are communicated to participants. Understanding these distinctions is essential for employers deciding which plan to offer and for employees evaluating their retirement prospects.

Defined Benefit Plans

A Defined Benefit Plan is the traditional pension model. It promises employees a specific retirement benefit, usually calculated based on a formula that considers salary history, years of service, and age at retirement. For example, a plan might provide 2% of the employee’s final average salary multiplied by years of service.

Key Features:

Employer Responsibility: The employer bears the investment risk and is obligated to deliver the promised benefit regardless of market performance.

Predictable Income: Employees receive a guaranteed monthly payment for life, often with survivor benefits.

Funding Requirements: Employers must contribute enough to meet actuarial obligations, which can be costly and complex.

Decline in Popularity: Due to high costs and liabilities, DB plans have become less common in the private sector, though they remain prevalent in government and unionized workplaces.

Advantages for Employees:

Security of lifetime income.

No need to manage investments directly.

Often includes inflation adjustments or survivor benefits.

Challenges for Employers:

Heavy funding obligations.

Sensitivity to interest rates and market fluctuations.

Long-term liabilities that can strain balance sheets.

Cash Balance Plans

***

***

A Cash Balance Plan is technically a type of Defined Benefit Plan but operates more like a hybrid between DB and Defined Contribution (DC) plans. Instead of promising a monthly pension, the plan defines benefits in terms of a hypothetical account balance. Each year, the employer credits the account with a “pay credit” (a percentage of salary or a flat dollar amount) and an “interest credit” (either a fixed rate or tied to an index).

Key Features:

Account-Based Presentation: Employees see a notional account balance that grows annually, making benefits easier to understand.

Employer Responsibility: The employer still manages investments and guarantees the interest credit, meaning the investment risk remains with the employer.

Portability: Benefits can often be rolled into an IRA or another retirement plan if the employee leaves the company.

Popularity Among Professionals: Cash Balance Plans are increasingly used by small businesses and professional practices (like medical or law firms) to allow higher contributions and tax deferrals.

Advantages for Employees:

Transparent account balance that feels similar to a 401(k).

Portability of benefits upon job change.

Potential for larger accumulations, especially for high earners.

Challenges for Employers:

Still responsible for funding and guaranteeing returns.

Requires actuarial oversight and compliance with pension regulations.

Can be complex to administer compared to pure DC plans.

Comparison

While both plans are employer-funded and fall under defined benefit rules, their differences are notable:

Aspect

Defined Benefit Plan

Cash Balance Plan

Benefit Format

Lifetime monthly pension

Hypothetical account balance

Risk

Employer bears investment risk

Employer bears investment risk

Employee Perception

Complex, formula-based

Simple, account-based

Portability

Limited

High (can roll over)

Popularity

Declining in private sector

Growing among small businesses/professionals

Conclusion

Defined Benefit Plans and Cash Balance Plans represent two approaches to retirement security. The former emphasizes guaranteed lifetime income, offering stability but imposing heavy obligations on employers. The latter modernizes the pension concept by presenting benefits as account balances, improving transparency and portability while still requiring employer guarantees. For employees, Cash Balance Plans often feel more tangible and flexible, while Defined Benefit Plans provide unmatched security. For employers, the choice depends on balancing cost, risk, and workforce needs. Ultimately, both plans underscore the importance of structured retirement savings and highlight the evolving landscape of employer-sponsored benefits.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Retirement planning has evolved significantly over the past several decades, with employers and employees seeking solutions that balance security, flexibility, and predictability. Among the various retirement plan options available today, cash balance plans stand out as a hybrid design that combines features of both traditional defined benefit pensions and defined contribution plans. Their unique structure makes them an attractive choice for employers aiming to provide meaningful retirement benefits while maintaining financial predictability.

At their core, cash balance plans are a type of defined benefit plan. Unlike traditional pensions, which promise retirees a monthly income based on years of service and final salary, cash balance plans define the benefit in terms of a hypothetical account balance. Each participant’s account grows annually through two components: a “pay credit” and an “interest credit.” The pay credit is typically a percentage of the employee’s salary or a flat dollar amount, while the interest credit is either a fixed rate or tied to an index such as U.S. Treasury yields. Although the account is hypothetical—meaning the funds are not actually segregated for each employee—the structure provides participants with a clear, understandable statement of their retirement benefit.

One of the primary advantages of cash balance plans is their transparency. Employees can easily track the growth of their account balance, much like they would with a 401(k). This clarity helps workers better understand the value of their retirement benefits and fosters a sense of ownership. Additionally, cash balance plans are portable: when employees leave a company, they can roll over the vested balance into an IRA or another qualified plan, ensuring continuity in retirement savings.

***

***

From the employer’s perspective, cash balance plans offer several benefits as well. Traditional pensions often create unpredictable liabilities, as they depend on factors such as longevity and investment performance. Cash balance plans, by contrast, provide more predictable costs because the employer commits to specific pay and interest credits. This predictability makes them easier to manage and budget for, particularly in industries where workforce mobility is high. Moreover, cash balance plans can be designed to reward long-term employees while still appealing to younger workers who value portability.

Despite these advantages, cash balance plans are not without challenges. Because they are defined benefit plans, employers bear the investment risk and must ensure the plan is adequately funded. Regulatory requirements, including nondiscrimination testing and funding rules, add complexity and administrative costs. Additionally, while cash balance plans are generally more equitable across generations of workers, transitions from traditional pensions to cash balance designs have sometimes sparked controversy, particularly among older employees who may perceive a reduction in benefits.

In recent years, cash balance plans have gained popularity among professional firms, such as law practices and medical groups, as well as small businesses seeking tax-efficient retirement solutions. These plans allow owners and highly compensated employees to accumulate larger retirement savings than would be possible under defined contribution limits, while still providing benefits to rank-and-file workers. As such, they serve as a valuable tool for both talent retention and financial planning.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

For generations, the prevailing belief in healthcare has been that physicians [MD, DO and DPM], with their high salaries and prestige, inevitably retire wealthier than nurses. Yet this assumption overlooks the financial realities of different nursing specialties and the long‑term impact of debt, lifestyle, and retirement planning. In fact, some Registered Nurses (RNs)—particularly Certified Registered Nurse Anesthetists (CRNAs), visiting nurses, and those who participate in structured pay programs like the Baylor plan—can retire richer than physicians. The reasons lie in the interplay of education costs, career flexibility, income potential, and disciplined financial planning.

Education Costs and Debt Burden

One of the most decisive factors shaping retirement wealth is the cost of education. Physicians often spend over a decade in training, including undergraduate studies, medical school, and residency. This path not only delays their earning years but also saddles them with substantial student debt. The median medical school debt in the United States exceeds $200,000, and many physicians spend years paying it down.

By contrast, RNs typically complete their training in two to four years, with advanced practice nurses such as CRNAs requiring graduate‑level education. Even so, their debt burden is far lighter, often less than half of what physicians carry. This difference means nurses can begin earning earlier, save for retirement sooner, and avoid the crushing interest payments that erode physicians’ wealth. A CRNA who starts practicing in their late twenties may already be investing in retirement accounts while a physician is still in residency earning a modest stipend.

Income Potential of Specialized Nurses

While physicians generally earn more annually than nurses, the gap is narrower in certain specialties. CRNAs, for example, are among the highest‑paid nursing professionals, with average salaries often exceeding $200,000 per year. This places them in direct competition with some physician specialties, especially primary care doctors, who may earn similar or even lower salaries.

Visiting nurses also benefit from unique financial advantages. Many work on flexible schedules, contract arrangements, or per‑visit compensation models. This allows them to maximize income while minimizing burnout. By avoiding the overhead costs of private practice and the administrative burdens physicians face, visiting nurses can channel more of their earnings directly into savings and investments.

When combined with lower debt and earlier career starts, these income streams can compound into significant retirement wealth.

The Baylor plan, a structured pay program used by some hospitals, allows nurses to work full‑time hours compressed into fewer days—often weekends—while still receiving full‑time pay and benefits. This arrangement provides several financial advantages. First, it enables nurses to earn competitive wages while freeing up weekdays for additional work, education, or entrepreneurial ventures. Second, it reduces commuting and childcare costs, allowing more income to be saved. Third, the plan often includes robust retirement benefits, such as employer‑matched contributions to 401(k) or pension programs.

Nurses who consistently participate in such structured pay plans can accumulate substantial nest eggs, often surpassing physicians who delay retirement savings due to debt repayment or lifestyle inflation. The Baylor plan highlights the importance of systematic investing: by automating contributions and focusing on long‑term growth, nurses can harness the power of compound interest. A nurse who invests steadily for 35 years may accumulate more wealth than a physician who begins saving late and inconsistently, despite earning a higher salary.

Lifestyle and Work‑Life Balance

Another overlooked factor is lifestyle. Physicians often face grueling schedules, high stress, and the temptation to maintain expensive lifestyles commensurate with their social status. Luxury homes, cars, and vacations can erode their financial base. Nurses, while not immune to lifestyle inflation, often maintain more modest spending habits.

Visiting nurses, in particular, enjoy flexibility that allows them to balance work with personal life. This reduces burnout and healthcare costs while enabling consistent employment into later years. By living within their means and prioritizing savings, nurses can accumulate wealth steadily without the financial pitfalls that sometimes accompany physician lifestyles.

Retirement Wealth Beyond Salary

Retirement wealth is not solely determined by annual income. It is shaped by debt management, savings discipline, investment strategies, and lifestyle choices. Nurses who leverage high‑paying specialties like anesthesia, flexible arrangements like visiting nursing, and structured programs like the Baylor plan can outperform physicians in these areas.

Consider two professionals: a physician earning $250,000 annually but burdened by $200,000 in debt and high living expenses, and a CRNA earning $200,000 with minimal debt and disciplined savings. Over decades, the CRNA may accumulate more net wealth, retire earlier, and enjoy greater financial security.

Conclusion

The assumption that physicians always retire richer than nurses is outdated. While physicians command higher salaries, their delayed earnings, heavy debt, and lifestyle pressures often undermine long‑term wealth. Nurses, particularly CRNAs, visiting nurses, and those who participate in structured pay programs like the Baylor plan, can retire wealthier by combining lower debt, earlier savings, competitive incomes, and disciplined financial planning.

Ultimately, retirement wealth is not about prestige but about strategy. Nurses who recognize this truth and act accordingly may find themselves enjoying more financial freedom than the very physicians they once assisted.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd and Copilot A.I.

***

***

The Baylor method of nurse payments is a scheduling and compensation model that allows nurses to work weekend shifts while receiving full-time pay and benefits, offering flexibility and helping healthcare facilities address staffing shortages.

The Baylor method, also known as the Baylor Plan or Baylor Shift, originated at Baylor University Medical Center in Dallas, Texas, as a strategic response to nurse shortages and burnout. It was designed to retain experienced nurses by offering a more flexible work schedule that still met the demands of patient care. Under this model, nurses typically work two 12-hour shifts on the weekend—Saturday and Sunday—and receive compensation equivalent to a full 40-hour workweek.

This approach has become increasingly popular in hospitals, long-term care facilities, and other healthcare settings. The core idea is simple: by concentrating work hours into the weekend, nurses gain more time off during the week while employers maintain adequate staffing during traditionally hard-to-fill shifts. For many nurses, this arrangement provides a better work-life balance, allowing them to pursue education, spend time with family, or take on additional employment during the week.

***

***

Financially, the Baylor method is attractive to both nurses and employers. Nurses benefit from full-time pay and benefits—including health insurance, retirement contributions, and paid time off—while only working two days per week. Employers, on the other hand, can reduce turnover and improve weekend staffing without increasing overall labor costs. Some facilities even offer Baylor shifts with added incentives, such as shift differentials or bonuses, to further encourage weekend coverage.

However, the Baylor method is not without its challenges. Working two consecutive 12-hour shifts can be physically and emotionally demanding, especially in high-acuity units. Nurses may experience fatigue or burnout if they are not adequately supported. Additionally, because Baylor nurses are paid for 40 hours while only working 24, scheduling extra shifts during the week can complicate overtime calculations. Typically, overtime pay only kicks in after 40 actual hours worked, not hours paid, which can lead to confusion or dissatisfaction if not clearly communicated.

From an operational standpoint, the Baylor method helps facilities maintain consistent staffing levels during weekends, which are often underserved due to lower availability of part-time or weekday-only staff. It also allows for more predictable scheduling and can improve patient outcomes by ensuring continuity of care. Facilities that adopt the Baylor model often report higher nurse satisfaction and retention rates.

In conclusion, the Baylor method of nurse payments is a creative and effective solution to some of the most persistent challenges in healthcare staffing. By offering full-time compensation for weekend work, it provides nurses with flexibility and financial stability while helping facilities maintain high-quality care. As healthcare continues to evolve, models like the Baylor shift demonstrate the importance of innovative scheduling strategies that support both caregivers and patients.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

What Medical School Didn’t Teach Doctors About Money

Medical school is designed to mold students into competent, compassionate physicians. It teaches anatomy, pathology, pharmacology, and clinical skills with precision and rigor. Yet, despite the depth of medical knowledge imparted, one critical area is often overlooked: financial literacy. For many doctors, the transition from student to professional comes with a steep learning curve—not in medicine, but in money. From managing debt to understanding taxes, investing, and retirement planning, medical school leaves a financial education gap that can have long-term consequences.

The Debt Dilemma

One of the most glaring omissions in medical education is how to manage student loan debt. The average medical student graduates with over $200,000 in debt, yet few are taught how to navigate repayment options, interest accrual, or loan forgiveness programs. Many doctors enter residency with little understanding of income-driven repayment plans or Public Service Loan Forgiveness (PSLF), missing opportunities to reduce their financial burden. Without guidance, some make costly mistakes—such as refinancing federal loans prematurely or choosing repayment plans that don’t align with their career trajectory.

Income ≠ Wealth

Medical students often assume that a high salary will automatically lead to financial security. While physicians do earn more than most professionals, income alone doesn’t guarantee wealth. Medical school rarely addresses the importance of budgeting, saving, and investing. As a result, many doctors fall into the “HENRY” trap—High Earner, Not Rich Yet. They spend lavishly, assuming their income will always cover expenses, only to find themselves living paycheck to paycheck. Without a solid financial foundation, even high earners can struggle to build net worth.

***

***

Taxes and Business Skills

Doctors are also unprepared for the complexities of taxes. Whether employed by a hospital or running a private practice, physicians face unique tax challenges. Medical school doesn’t teach how to track deductible expenses, optimize retirement contributions, or navigate self-employment taxes. For those who open their own clinics, the lack of business education is even more pronounced. Understanding profit margins, payroll, insurance billing, and compliance regulations is essential—but rarely covered in medical training.

Investing and Retirement Planning

Another blind spot is investing. Medical students are rarely taught the basics of compound interest, asset allocation, or retirement accounts. Many don’t know the difference between a Roth IRA and a traditional 401(k), or how to evaluate mutual funds and index funds. This lack of knowledge delays retirement planning and can lead to missed opportunities for long-term growth. Some doctors rely on financial advisors without understanding the fees or conflicts of interest involved, putting their wealth at risk.

Insurance and Risk Management

Medical school also fails to educate students on insurance—life, disability, malpractice, and health. Doctors need robust coverage to protect their income and assets, but many don’t know how to evaluate policies or understand terms like “own occupation” or “elimination period.” Inadequate coverage can leave physicians vulnerable to financial disaster in the event of illness, injury, or litigation.

Emotional and Behavioral Finance

Beyond technical knowledge, medical school overlooks the emotional side of money. Physicians often face pressure to maintain a certain lifestyle, especially after years of sacrifice. The desire to “catch up” can lead to impulsive spending, luxury purchases, and financial stress. Without tools to manage money mindset and behavioral habits, doctors may struggle with guilt, anxiety, or burnout related to finances.

The Case for Financial Education

Fortunately, awareness of this gap is growing. Organizations like Medics’ Money and podcasts such as “Docs Outside the Box” are working to fill the void by offering financial education tailored to physicians.

These resources cover everything from budgeting and debt management to investing and entrepreneurship. Some medical schools are beginning to incorporate financial literacy into their curricula, but progress is slow and inconsistent.

Conclusion

Medical school equips doctors to save lives, but it doesn’t prepare them to secure their own financial future. The lack of financial education leaves many physicians vulnerable to debt, poor investment decisions, and lifestyle inflation. To thrive both professionally and personally, doctors must seek out financial knowledge beyond the classroom. Whether through self-study, mentorship, or professional guidance, understanding money is as essential as understanding medicine. After all, financial health is a cornerstone of overall well-being—and every doctor deserves to master both.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A paradox is a statement that appears at first to be contradictory, but upon reflection then makes sense. This literary device is commonly used to engage a reader to discover an underlying logic in a seemingly self-contradictory statement or phrase. As a result, paradox allows readers to understand concepts in a different and even non-traditional

***

***

GOVERNMENT HEALTH INFORMATION IS TRUSTED?

Classic Definition: Despite the PP-ACA, there is ambivalence about the role of the US Government as a source of quality healthcare information.

Modern Circumstance: Of brands presented to respondents in a Consumer Reports (50 percent), and AARP (37 percent) survey, they outpolled the “US Government Healthcare Quality Reporting Website” (36 percent) and Medicare Website (32 percent).

Paradox Example: The focus groups expressed “mixed reactions and raised doubts about government involvement in quality ratings information. At least one participant in each group expressed skepticism about trusting ‘the government’ to compile information.”

Younger consumers especially questioned the relevance of Medicare measures to the non-elderly population. Yet participants gravitated to “.gov” websites over “.org” websites as a more authoritative source.

CITE: Williams, Jason: Health Affairs, December 28, 2016

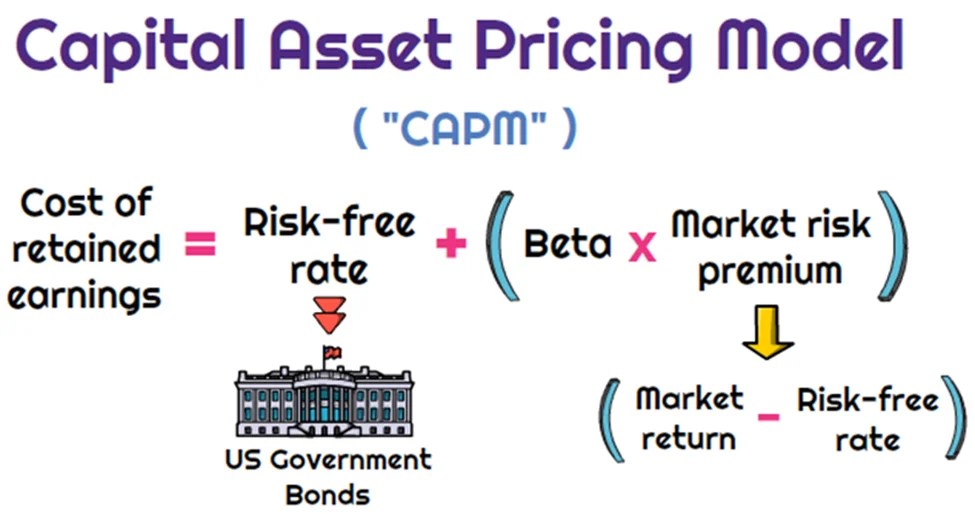

Dr. Harry Markowitz is credited with developing the framework for constructing investment portfolios based on the risk-return tradeoff. William Sharpe, John Lintner, and Jan Mossin are credited with developing the Capital Asset Pricing Model (CAPM).

CAPM is an economic model based upon the idea that there is a single portfolio representing all investments (i.e., the market portfolio) at the point of the optimal portfolio on the Capital Market Line (CML) and a single source of systematic risk, beta, to that market portfolio. The resulting conclusion is that there should be a “fair” return investors should expect to receive given the level of risk (beta) they are willing to assume.

The excess return, or return above the risk-free rate, that may be expected from an asset is equal to the risk-free return plus the excess return of the market portfolio times the sensitivity of the asset’s excess return to the market portfolio excess return. Beta, then, is a measure of the sensitivity of an asset’s returns to the market as a whole. A particular security’s beta depends on the volatility of the individual security’s returns relative to the volatility of the market’s returns, as well as the correlation between the security’s returns and the markets returns.

While a stock may have significantly greater volatility than the market, if that stock’s returns are not highly correlated with the returns of the overall market (i.e., the stock’s returns are independent of the overall market’s returns), then the stock’s beta would be relatively low. A beta in excess of 1.0 implies that the security is more exposed to systematic risk than the overall market portfolio, and likewise, a beta of less 1.0 means that the security has less exposure to systematic risk than the overall market.

MPT has helped focus investors on two extremely critical elements of investing that are central to successful investment strategies.

First, MPT offers the first framework for investors to build a diversified portfolio. Furthermore, an important conclusion that can be drawn from MPT is that diversification does in fact help reduce portfolio risk.

Thus, MPT approaches are generally consistent with the first investment rule of thumb, “understand and diversify risk to the extent possible.”

Additionally, the risk/return tradeoff (i.e., higher returns are generally consistent with higher risk) central to MPT based strategies has helped investors recognize that if it looks too good to be true, it probably is.

Passive Investing

Passive investing is a monetary plan in which an investor invests in accordance with a pre-determined strategy that doesn’t necessitate any forecasting of the economy or an individual company’s prospects. The primary premise is to minimize investing fees and to avoid the unpleasant consequences of failing to correctly predict the future. The most accepted method to invest passively is to mimic the performance of a particular index. Investors typically do this today by purchasing one or more ‘index funds’. By tracking an index, an investor will achieve solid diversification with low expenses.

An ivestor could potentially earn a higher rate of return than an investor paying higher management fees. Passive management is most widespread in the stock markets. But with the explosion of exchange traded funds on the major exchanges, index investing has become more popular in other categories of investing. There are now literally hundreds of different index funds.

Passive management is based upon the Efficient Market Hypothesis theory. The Efficient Market Hypothesis (EMH) states that securities are fairly priced based on information regarding their underlying cash flows and that investors should not anticipate to consistently out-perform the market over the long-term.

The Efficient Market Hypothesis evolved in the 1960s from the Ph.D. dissertation of Eugene Fama. Fama persuasively made the case that in an active market that includes many well-informed and intelligent investors, securities will be appropriately priced and reflect all available information. If a market is efficient, no information or analysis can be expected to result in out-performance of an appropriate benchmark. There are three distinct forms of EMH that vary by the type of information that is reflected in a security’s price:

Weak Form

This form holds that investors will not be able to use historical data to earn superior returns on a consistent basis. In other words, the financial markets price securities in a manner that fully reflects all information contained in past prices.

Semi-Strong Form

This form asserts that security prices fully reflect all publicly available information. Therefore, investors cannot consistently earn above normal returns based solely on publicly available information, such as earnings, dividend, and sales data.

Strong Form

This form states that the financial markets price securities such that, all information (public and non-public) is fully reflected in the securities price; investors should not expect to earn superior returns on a consistent basis, no matter what insight or research they may bring to the table.

While a rich literature has been established regarding whether EMH actually applies in any of its three forms in real world markets, probably the most difficult evidence to overcome for backers of EMH is the existence of a vibrant money management and mutual fund industry charging value-added fees for their services.

The notion of passive management is counterintuitive to many investors. Passive investing proponents follow the strong market theory of EMH. These proponents argue several points including;

In the long term, the average investor will have a typical before-costs performance equal to the market average. Therefore the standard investor will gain more from reducing investment costs than from attempting to beat the market over time.

The efficient-market hypothesis argues that equilibrium market prices fully reflect all existing market information. Even in the case where some of the market information is not currently reflected in the price level, EMH indicates that an individual investor still cannot make use of that information. It is widely interpreted by many academics that to try and systematically “beat the market” through active management is a fools game.

Not everyone believes in the efficient market. Numerous researchers over the previous decades have found stock market anomalies that indicate a contradiction with the hypothesis. The search for anomalies is effectively the hunt for market patterns that can be utilized to outperform passive strategies. Such stock market anomalies that have been proven to go against the findings of the EMH theory include;

Low Price to Book Effect

January Effect

The Size Effect

Insider Transaction Effect

The Value Line Effect

All the above anomalies have been proven over time to outperform the market. For example, the first anomaly listed above is the Low Price to Book Effect. The first and most discussed study on the performance of low price to book value stocks was by Dr. Eugene Fama and Dr. Kenneth R. French. The study covered the time period from 1963-1990 and included nearly all the stocks on the NYSE, AMEX and NASDAQ. The stocks were divided into ten subgroups by book/market and were re-ranked annually. In the study, Fama and French found that the lowest book/market stocks outperformed the highest book/market stocks by a substantial margin (21.4 percent vs. 8 percent). Remarkably, as they examined each upward decile, performance for that decile was below that of the higher book value decile. Fama and French also ordered the deciles by beta (measure of systematic risk) and found that the stocks with the lowest book value also had the lowest risk.

Today, most researchers now deem that “value” represents a hazard feature that investors are compensated for over time. The theory being that value stocks trading at very low price book ratios are inherently risky, thus investors are simply compensated with higher returns in exchange for taking the risk of investing in these value stocks. The Fama and French research has been confirmed through several additional studies. In a Forbes Magazine 5/6/96 column titled “Ben Graham was right–again,” author David Dreman published his data from the largest 1500 stocks on Compustat for the 25 years ending 1994. He found that the lowest 20 percent of price/book stocks appreciably outperformed the market.

One item a medical professional should be aware of is the strong paradox of the efficient market theory. If each investor believes the stock market were efficient, then all investors would give up analyzing and forecasting. All investors would then accept passive management and invest in index funds. But if this were to happen, the market would no longer be efficient because no one would be scrutinizing the markets. In actuality, the efficient market hypothesis actually depends on active investors attempting to outperform the market through diligent research.

The case for passive investing and in favor of the EMH is that a preponderance of active managers do actually underperform the markets over time. The latest study by Standard and Poor’s (S&P) confirms this fact. S&P recently compared the performance of actively-managed mutual funds to passive market indexes twice per year. The 2012 S&P study indicated that indexes were once again outperforming actively-managed funds in nearly every asset class, style and fund category. The lone exception in the 2012 report was international equity, where active outperformed the index that S&P chose. The study examined one-year, three-year and five-year time periods. Within the U.S. equity space, active equity managers in all the categories failed to outperform the corresponding benchmarks in the past five year period. More than 65 percent of the large-cap active managers lagged behind the S&P 500 stock index. More than 81 percent of mid-cap mutual funds were outperformed by the S&P MidCap 400 index.

Lastly, 77 percent of the small-cap mutual funds were outperformed by the S&P SmallCap 600 index. U.S. bond active managers fared no better that equity managers over a five year period. More than 83 percent of general municipal mutual funds under-performed the S&P National AMT-Free Municipal Bond index, 93 percent of government long-term funds under-performed the Barclays Long Government index, nearly 95 percent of high yield corporate bond funds under-performed the Barclays High Yield index. Although the performance measurements for index investing are very strong, many analysts find three negative elements of passive investing;

Downside Protection: When the stock market collapses like in 2008, an index investor will assume the same loss as the market. In the case of 2008, the S&P 500 stock index fell by more than 50 percent, offering index investors no downside protection.

Portfolio Control: An index investor has no control over the holdings in the fund. In the event that a certain sector becomes over-owned (i.e. technology stocks in 2000), an index investor maintains the same weight as the index.

Average Returns: An index investor will never have the opportunity to outperform the market, but will always follow. Although the markets are very efficient, an investor can perhaps take advantage of market anomalies and invest with those managers who have maintained a long-term performance edge over the respective index.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

If you’re looking at this tab, chances are you are fed up with your financial brokerage accounts, thinking of finances, investing, retirement or all of the above.

And so, we can help

An investment portfolio second opinion, also called a “ portfolio review,” is an analysis of your financial holdings and associated strategies, allocations, fees and performance to determine whether the most effective instruments and methodologies are being utilized to reach your goals.

No Worries! You may have come to the right place.

E-Mail Ann Miller RN MHA CPHQ for an Initial Appointment: MarcinkoAdvisors@outlook.com

The purpose of this initial appointment is for you to ask a lot of questions to make sure you are comfortable with potentially working with us. It also helps if you are prepared to provide a verbal summary of your current situation.

Here are some questions to consider asking us during your first meeting:

1) Can you tell us about your financial qualifications, experience, education and training; if any?

2) Can you provide some information about your current financial advisory team?

3) On what type of investments do you typically purchase and own?

5) How much do pay your financial management firm?

6) How long have you been working with your current financial management firm?

8) What other services does your financial team provide?

An investment advisor (sometimes spelled “investment adviser”) is defined as a company or person who has a government registration allowing them to choose, manage and recommend investments for clients. Investment advisors are also sometimes referred to as stock brokers. They are not fiduciaries.

Unlike other financial advisors who may not be regulated, investment advisors are regulated by their state or the Securities Exchange Commission depending on how much money they manage. Investment advisors may also offer services like retirement planning.

COMMENTS APPRECIATED

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

My medical practice has a small self-directed pension plan with profit sharing features.

QUESTION: Can my medical practice’s retirement plan invest in a hedge fund?

Such a pension fund falls under a category called self-directed “plan” assets.

Among the rules are that each participant in the plan counts toward the 100 investor maximum under which most hedge funds operate, that each plan participant be a fully accredited investor, and that the hedge fund keep investments such as pension plans and other funds covered under ERISA to less than 25 percent of total assets under management.

Some retired people live on a fixed income and many of them live right on the edge of their financial capability. At some time in their life, they may have to make a choice regarding many purchases.

In this case, we will illustrate “choice” using a couple’s purchase of Long-Term-Care Insurance [LTCI]. Of course, economics is the study of choice; wants, needs and scarcity, etc. In our case, if they decide to make the purchase they commit to a lifetime of premium payments. The financial tradeoff is this; if they make the commitment to purchase LTCI, they must give up something else.

EXAMPLE: In order to maintain a monthly premium of $100 ($1,200per year), an elderly patient, retired layman or couple must essentially relegate about $30,000 of financial assets to generate the $100 necessary to make an average premium payment (assumes a 7% rate of return with 4% withdrawal rate) or [4% X $30,000 = $1,200 year]. Thus, if the monthly premium cost is $500 per month, the elder must give up the use of $150,000 of retirement asset just to generate enough cash flow to pay for the LTC insurance.

***

***

The married elder couple has to make the Hobson’s Choice decision among lifestyle (dinners, vacations, gifts to children, prescription drugs, medical care or food and shelter) versus paying an insurance premium to provide for nursing home coverage for a need, which may be very real, but will not occur until sometime in the ambiguous future.

And so, when faced with such a tough economics Hobson’s Medicine Choice, neither of which delivers peace of mind or a respectable solution; many will simply decide that, in either case, they may already end up impoverished. Thus, many will often opt for the better lifestyle now … while they can enjoy it … together.

Cite: Anonymous Health Insurance Agent, Norcross, Georgia

COMMENTS APPRECIATED

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

OVER HEARD IN THE FINANCIAL ADVISOR’S LOUNGE

***

***

By Perry D’Alessio, CPA [D’Alessio Tocci & Pell LLP]

What I see in my accounting practice is that significant accumulation in younger physician portfolio growth is not happening as it once did. This is partially because confidence in the equity markets is still not what it was; but that doctors are also looking for better solutions to support their reduced incomes.

For example, I see older doctors with about 25 percent of their wealth in the market, and even in retirement years, do not rely much on that accumulation to live on. Of this 25 percent, about 80 percent is in their retirement plan, as tax breaks for funding are just too good to ignore.

What I do see is that about 50 percent of senior physician wealth is in rental real estate, both in a private residence that has a rental component, and mixed-use properties. It is this that provides a good portion of income in retirement.

***

***

QUESTION: So, could I add dialog about real estate as a long term solution for retirement?

Yes, as I believe a real estate concentration in the amount of 5 percent is optimal for a diversified portfolio, but in a very passive way through mutual or index funds that are invested in real estate holdings and not directly owning properties.

Today, as an option, we have the ability to take pension plan assets and transfer marketable securities for rental property to be held inside the plan collecting rents instead of dividends.

Real estate holdings never vary very much, tend to go up modestly, and have preferential tax treatment due to depreciation of the property against income.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Beneficiary designations can provide a relatively easy way to transfer an account or insurance policy upon your death. However, if you’re not careful, missing or outdated beneficiary designations can easily cause your estate plan to go awry.

Where you can find them

Here’s a sampling of where you’ll find beneficiary designations:

In several states, so-called “lady bird” deeds for real estate

***

***

10 tips about beneficiary designations

Because beneficiary designations are so important, keep these things in mind in your estate planning:

Remember to name beneficiaries. If you don’t name a beneficiary, one of the following could occur:

The account or policy may have to go through probate. This process often results in unnecessary delays, additional costs, and unfavorable income tax treatment.

The agreement that controls the account or policy may provide for “default” beneficiaries. This could be helpful, but it’s possible the default beneficiaries may not be whom you intended.

Name both primary and contingent beneficiaries. It’s a good practice to name a “back up” or contingent beneficiary in case the primary beneficiary dies before you. Depending on your situation, you may have only a primary beneficiary. In that case, consider whether it may make sense to name a charity (or charities) as the contingent beneficiary.

Update for life events. Review your beneficiary designations regularly and update them as needed based on major life events, such as births, deaths, marriages, and divorces.

Read the instructions. Beneficiary designation forms are not all alike. Don’t just fill in names — be sure to read the form carefully. If necessary, you can draft your own customized beneficiary designation, but you should do this only with the guidance of an experienced attorney or tax advisor.

Coordinate with your will and trust. Whenever you change your will or trust, be sure to talk with your attorney about your beneficiary designations. Because these designations operate independently of your other estate planning documents, it’s important to understand how the different parts of your plan work as a whole.

Think twice before naming individual beneficiaries for particular assets. For example, you may establish three accounts of equal value initially and name a different child as beneficiary of each account. Over the years, the accounts may grow or be depleted unevenly, so the three children end up receiving different amounts — which is not what you originally intended.

Avoid naming your estate as beneficiary. If you designate a beneficiary on your 401(k), for example, it won’t have to go through probate court to be distributed to the beneficiary. If you name your estate as beneficiary, the account will have to go through probate. For IRAs and qualified retirement plans, there may also be unfavorable income tax consequences.

Use caution when naming a trust as beneficiary. Consult your attorney or CPA before naming a trust as beneficiary for IRAs, qualified retirement plans, or annuities. There are situations where it makes sense to name a trust — for example if:

Your beneficiaries are minor children

You’re in a second marriage

You want to control access to funds

Be aware of tax consequences. Many assets that transfer by beneficiary designation come with special tax consequences. It’s helpful to work with an experienced tax advisor to help provide planning ideas for your particular situation.

Use disclaimers when necessary — but be careful. Sometimes a beneficiary may actually want to decline (disclaim) assets on which they’re designated as beneficiary. Keep in mind that disclaimers involve complex legal and tax issues and require careful consultation with your attorney and CPA.

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Why would a doctor consider a Roth IRA conversion?

By Staff Reporters

***

***

A Roth conversion involves transferring funds from a traditional retirement account—such as a 401(k), 403(b), or individual retirement account (IRA) funded with pre-tax dollars—into a Roth IRA.

The biggest benefit lies in the tax treatment of the converted funds. Once the funds are in the Roth IRA, future growth of those assets is tax-free. Withdrawals in retirement are also tax-free, assuming they meet certain criteria. As with any strategy, there are important considerations to keep in mind.

When you convert funds to a Roth IRA, the amount converted is taxable income in that tax year. For example, if you convert $100,000 from a traditional IRA to a Roth IRA, that $100,000 will be added to your taxable income in the conversion year.

Converting large amounts can result in a significant tax bill and may push you into a higher tax bracket. Even so, using retirement funds to pay taxes may make sense for those looking to convert large IRAs to reduce their future required minimum distributions (RMDs).

The timing of your Roth conversion matters too. Generally, it’s a good idea to convert when your income is lower—for example, after you’ve retired and before you begin drawing Social Security. You may also choose to convert over the course of several years to spread out the tax impacts. But if you can get comfortable with these considerations, a Roth conversion can provide you with benefits beyond tax-free growth and withdrawals.

Some of these benefits are:

Tax diversification. Having both traditional and Roth accounts allows you to manage your tax liability in retirement. For example, if your income in a given year is higher than expected, you can withdraw from the Roth IRA without increasing your taxable income.

No RMDs. Traditional IRAs and 401(k)s require you to begin taking RMDs at age 73. Roth IRAs have no RMD requirement during your lifetime. With a Roth account, you have more control over your retirement withdrawals and can leave the funds to grow for your heirs.

Benefits for heirs. Roth IRAs can be passed on to beneficiaries, who can inherit the account income tax-free. This means your heirs can enjoy the tax-free growth and withdrawals if the Roth IRA has been held for five years or more—a significant advantage, especially if your beneficiaries are in a higher tax bracket.

Posted on April 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHA CPHQ CMP™

***

***

Finally … Fiduciary second investing and financial planning opinions right here!

Telephonic or electronic advice for medical professionals that is:

Objective, affordable, medically focused and financially personalized

Rendered by a pre-screened financial consultant for doctors and medical professionals

Offered on a pay-as-you-go basis, by phone or secure e-mail transmission

The iMBA Discussion Forum™ is a physician-to-financial advisor telephone or e-mail portal that connects independent financial professionals to doctors, nurses or healthcare executives desiring affordable and unbiased financial planning advice.

Medical professionals and healthcare executives can now receive direct access to pre-screened iMBA professionals in the areas of Investing, Financial Planning, Asset Allocation, Portfolio Management, Insurance, Mortgage and Lending, Human Resources, Retirement Planning and Employee Benefits. To assist our medical professional and healthcare executive members, we can be contracted with per-minute or per-project fees, and contacted by client phone, email or secure instant messaging.

Posted on March 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEdCMP®

***

***

Your Executor or personal representative is named in your Will and is responsible for management of assets subject to probate. A basic checklist of the duties of the personal representative looks like this:

Gather all estate assets;

Collect all amounts owed the decedent;

Notify creditors and paying all valid debts;

Selling assets as needed to pay expenses or as directed by the Will;

Distribute assets to beneficiaries;

File decedents final federal income tax return;

File an estate tax return if the estate is large enough; and

File inventories and annual returns with the probate court, if required.

The position requires a lot of responsibility and involves many duties and a considerable commitment of time. The personal representative must petition the probate court for formal appointment.

Selection of your personal representative should not be made lightly, or as a favor to a friend. It requires a lot of work and very often for little or no pay. Friends and family typically will not charge the estate for their time and work. Outside advisers like attorneys and accountants will not hesitate to bill for their work effort. A few items for your selection criteria should be:

Longevity – the person should have a likelihood of being able to serve after your death;

Skill in managing legal and financial affairs;

Familiarity with your estate and wishes;

Integrity and loyalty; and

Impartiality and absence of conflicts of interest.

Alternatives to family or friends might be a corporate executor, such as a bank, an attorney, or other adviser. Similar criteria should be used in the selection of a trustee.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

9. We act with honesty, integrity and are always straightforward. 8. We strive to be innovative, creative, iconoclastic, and flexible. 7. We admit and learn from mistakes and don’t repeat them. 6. We work hard always as competitors are trying to catch up. 5. We treat others with dignity and respect. 4. We are the onus of consulting advice for the well being of others. 3. We fight complacency as former success is in the past. 2. The best management styles are timeless, not timely. 1. Our clients are colleagues and always come first.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

In retirement, according to Josephine Nesbit, your economic class can be broadly categorized into four distinct groups, each defined by their net worth and financial capabilities, ranging from retirees with limited resources to the wealthy. And, according to Moneywise, here are the net worth categories of the poor, middle class (and upper-middle class) and rich:

Poor retirees: Poor retirees are in the lower 20th percentile, and may have a net worth of around $10,000. This is often without property ownership, forcing many to rely mainly on Social Security or minimal pensions.

Middle-class retirees: Making up the 50th percentile, with a median net worth of approximately $281,000, this group usually includes home equity, retirement savings and a 401(k) plan.

Upper-middle-class retirees: These retirees possess a net worth between $201,800 and $608,900. They have diversified assets and enjoy a comfortable retirement cushion.

Rich retirees: In the 90th percentile, with net worth starting at $1.9 million, this group has much more financial freedom and is able to afford luxuries and legacy planning.

Posted on February 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The U.S. added 143,000 jobs in January, fewer than economists expected, but the unemployment rate inched down to 4% from 4.1%, beating forecasts. Forecasters surveyed by Dow Jones had anticipated 169,000 payroll gains in January, after a surprisingly large 256,000 jump in December.

Last month, the Securities and Exchange Commission said Vanguard would pay more than $100 million to settle charges for misleading statements related to capital gains distributions and tax consequences for retail investors who held Vanguard Investor Target Retirement Funds in taxable accounts.

Major U.S. equities indexes moved lower to close out the trading week as the January jobs report showed slower-than-expected hiring but a down tick in the unemployment rate. Despite the slump in job additions, the overall resilience in the labor market could encourage the Federal Reserve to hold off on additional interest-rate cuts. The S&P 500 and the Dow ended Friday’s session with daily losses of roughly 1.0%. The tech-heavy NASDAQ fell 1.4%.

Most notable this month is the appointment of Tim Noel as the new CEO of UnitedHealthcare after former CEO Brian Thompson was fatally shot in New York City in December.

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

(“Informed Voice of a New Generation of Fiduciary Advisors for Healthcare”)

For most lay folks, personal financial planning typically involves creating a personal budget, planning for taxes, setting up a savings account and developing a debt management, retirement and insurance recovery plan. Medicare, Social Security and Required Minimal Distribution [RMD] analysis is typical for lay retirement. Of course, we can assist in all of these activities, but lay individuals can also create and establish their own financial plan to reach short and long-term savings and investment goals.

But, as fellow doctors, we understand better than most the more complex financial challenges doctors can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

Academic Team of Internationally Known Contributors

D. E. Marcinko & Associates is one of the most academically published authorities on the topic of financial planning and private wealth management for physicians, nurses and medical professionals. We have published 33 major peer reviewed textbooks redacted in the Library of Medicine, Institute of Health and the Library of Congress, in four languages, with over 5,025 online white papers, web-posts and related publications. These cover a range of financial planning topics from medical malpractice, risk management and insurance, to investment policy statement analysis and endowment funding management, and to taxation, retirement, estate and legacy planning.

Financial planning, business and strategic management, FMV for practice and clinics and related “hard” topics are included.

***

We also include “soft” subjects from investor psychology, ethics and lost fortunes to luxury spending, from understanding the middle-class millionaire to the political philosophies of physicians and the affluent. Our corpus of work is regularly consulted by doctors, medical, business, graduate and nursing schools, to elite advisors, private and investment bankers, wealth managers, venture capitalists, academics and the press.

Posted on December 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHACMP™

INTRODUCING OUR NEXT GENERATION e-BOOK LIBRARYFROM iMBA, Inc.

An e-book is an electronic or digital book that can be read on a computer or a handheld device.

Our new e-books consists of text, images, and are fixed to a specific spot on the page.

And, our e-books are a data files similar in content and structure to a word-processing document that comes in a PDF format. To use our e-books, you need to purchase and download it to a device that has a .pdf file reader app, such as ADOBE® or similar on a smartphone, tablet or computer. A PDF, also known as a portable document format, is the format most people are familiar with and used in our e-books. PDFs are known for their ease of use and ability to hold custom layouts. They are the most commonly used e-Book formats, especially by professionals and adult-learners.

You can then access the e-book and read it, or highlight pages and even take side notes.

e-Books Save Money

With no manufacturing, printing, binding or shipping costs, e-Books are cheaper than traditional hard or paper back books.The price of each specialized and highly niche focused e-Book [50-100 pages] is only $25, whereas similar paperback printed books of this type generally cost $145, or more!

With the PP-ACA, increased compliance regulations and higher tax rates impending from the Biden administration – not to mention the corona pandemic, venture capital based healthcare corporations and telehealth – physicians are more concerned about their retirement and retirement planning than ever before; and with good reason. After payroll taxes, dividend taxes, limited itemized deductions, the new 3.8% surtax on net investment income and an extra 0.9% Medicare tax, for every dollar earned by a high earning physician, almost 50 cents can go to taxes!

Introduction

Retirement planning is not about cherry picking the best stocks, ETFs or mutual funds or how to beat the short term fluctuations in the market. It’s a disciplined long term strategy based on scientific evidence and a prudent process. You increase the probability of success by following this process and monitoring on a regular basis to make sure you are on track.

General Surveys

According to a survey from the Employee Benefit Research Institute [EBRI] and Greenwald & Associates; nearly half of workers without a retirement plan were not at all confident in their financial security, compared to 11 percent for those who participated in a plan, according to the 2014 Retirement Confidence Survey (RCS).

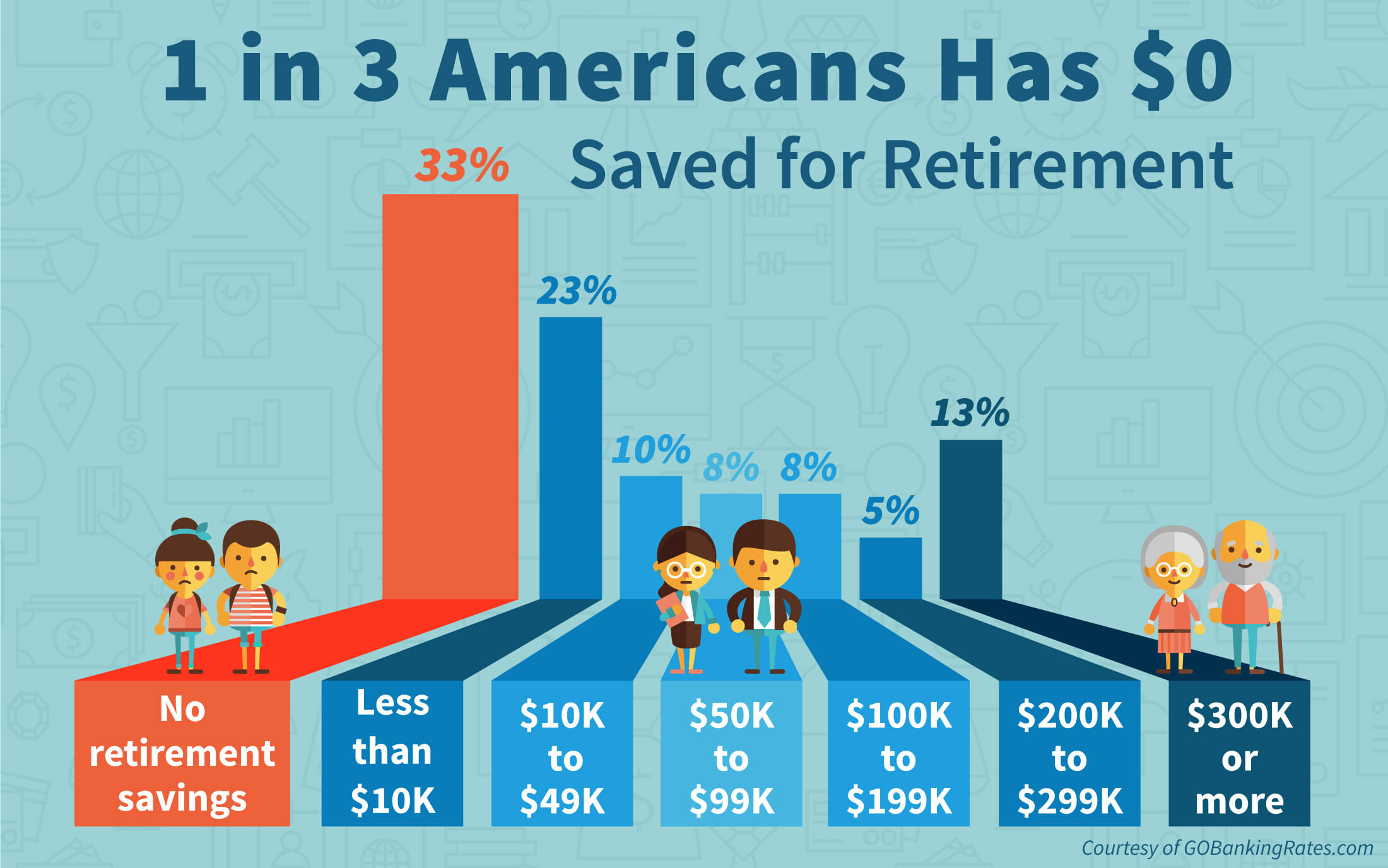

In addition, 35 percent of workers have not saved any money for retirement, while only 57 percent are actively saving for retirement. Thirty-six percent of workers said the total value of their savings and investments—not including the value of their home and defined benefit plan—was less than $1,000, up from 29 percent in the 2013 survey. But, when adjusted for those without a formal retirement plan, 73 percent have saved less than $1,000.

Debt is also a concern, with 20 percent of workers saying they have a major problem with debt. Thirty-eight percent indicate they have a minor problem with debt. And, only 44 percent of workers said they or their spouse have tried to calculate how much money they’ll need to save for retirement. But, those who have done the calculation tend to save more.

The biggest shift in the 24 years has been the number of workers who plan to work later in life. In 1991, 84 percent of workers indicated they plan to retire by age 65, versus only 9 percent who planned to work until at least age 70. In 2014, 50 percent plan on retiring by age 65; with 22 percent planning to work until they reach 70.

Physician Statistics

Now, compare and contrast the above to these statistics according to a 2018 survey of physicians on financial preparedness by American Medical Association [AMA] Insurance. The statistics are still alarming:

The top personal financial concern for all physicians is having enough money to retire.

Only 6% of physicians consider themselves ahead of schedule in retirement preparedness.

Nearly half feel they were behind

41% of physicians average less than $500,000 in retirement savings.

Nearly 70% of physicians don’t have a long term care plan.

Only half of US physicians have a completed estate plan including an updated will and Medical directives.

Thoughts to Ponder

And so, to help make your golden years comfortable and worry free, here are ten important retirement questions for all physicians to consider:

How much money do you need to retire?

What is your retirement cash flow?

What is your retirement vision?

How to stay on retirement track?

How to maximize retirement plan contributions such as 401(k) or 403(b)?

How to maximize retirement income from retirement plans?

What are some other retirement plan savings options?

What is your retirement plan and investing style?

What is the role of social security in retirement planning?

How to integrate retirement with estate planning?

The opinion of a competent Certified Medical Planner® can assist.

ASSESSMENT: Your thoughts, comments and input are appreciated.

Posted on November 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

The number of people living with Alzheimer’s disease is growing. The ripple effect is straining families, communities, and the healthcare system, yet talking about the disease on a personal level can be difficult.

November is Alzheimer’s Awareness Month because it can happen in any family, and because it’s worth talking about the challenges of living with or caring for someone with this disease.

You may notice splashes of teal and purple sprouting up this November, as both colors are associated with Alzheimer’s awareness. Teal is the color of the Alzheimer’s Foundation of America, chosen for its calming effect. Purple is the signature color of the Alzheimer’s Foundation, which stands for strength in the fight against Alzheimer’s disease.

Posted on November 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The Internal Revenue Service (IRS) ruled that employees at an unnamed company can designate a portion of their employer match to student debt repayments or health reimbursement accounts, in addition to their traditional 401(k).

Warren Buffett’s Midas touch gave a boost to Domino’sPizza and PoolCorp. after Berkshire Hathaway announced it has bought shares of both companies. Domino’s popped to start the day but dropped 1.27%, while Pool climbed just 0.54%.