By Staff Reporters

***

***

On Monday, Newsweek published a list of banks that had trading of shares halted. According to the NASDAQ Trader website, these banks were placed under a Volatility Trading Pause. Some of the banks that were placed under a Volatility Trading Pause included PacWest Bancorp, Western Alliance Bancorporation Common Stock, First Republic Bank Common Stock and Comerica Incorporated Common Stock. Some of these banks were placed under the halt several times, but the pauses only lasted a few minutes. For example, the NASDAQ Trader website shows that PacWest Bancorp was halted at 9:49 a.m. EST and resumed at 9:54 a.m. EST.

CITE: https://www.r2library.com/Resource/Title/0826102549

***

- Billionaire Charles Schwab’s net worth has plunged about $3 billion since March 8th, 2023.

- Shares of Charles Schwab Corp fell sharply amid the collapse of Silicon Valley Bank.

- Investors are worried as Charles Schwab Corp is sitting on a significant amount of unrealized losses on its bond assets.

Billionaire Charles Schwab’s fortune has taken a massive beating after shares of the eponymous company he founded plunged amid the banking crisis. Shares of Charles Schwab Corp, a savings and loan holding company, closed 11.6% lower at $51.91 apiece on Monday, bringing its market value lower by nearly 38% so far this year. But, by 11am Tuesday, shares of the corporation were back up 9.5 percent.

***

Meanshile, mega-manager Vanguard Funds bought sizable stakes in both Silicon Valley Bank (US:SIVB) and Signature Bank (US:SBNY) in recent months, according to data compiled by Fintel.

***

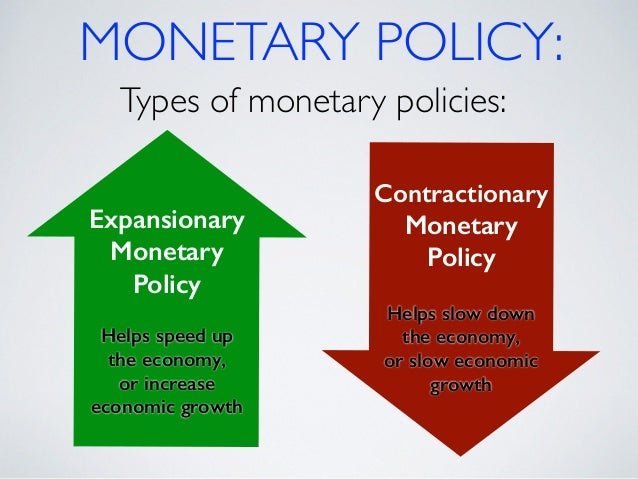

Finally, U.S. equities finished with gains and near the highs of the day, as investors sifted through the first look at February’s inflation picture. The Consumer Price Index (CPI) rose in line with estimates month-over-month, while the core rate—excluding food and energy—increased a little more than expected. On a year-over-year basis, both the headline and core rate declined, but remained elevated. In other economic news, small business optimism increased last month.

The banking sector remained in the headlines, with many banks climbing higher following sharp losses over the past few trading sessions. In other equity news, United Airlines fore-casted an adjusted Q1 loss, and Meta Platforms announced another round of layoffs that will begin tomorrow.

Treasury yields rebounded, especially at the shorter end of the curve, and the U.S. dollar was nearly unchanged, while crude oil prices tumbled, and gold traded lower.

Asian stocks fell as turmoil in the U.S. banking sector spilled over into the region, while European stocks climbed as investors digested the inflation data out of the U.S.

***

ORDER: https://www.routledge.com/Comprehensive-Financial-Planning-Strategies-for-Doctors-and-Advisors-Best/Marcinko-Hetico/p/book/9781482240283

***

COMMENTS APPRECIATED

Thank You

***

Filed under: "Ask-an-Advisor", Alerts Sign-Up, Ethics, Glossary Terms, Investing, Risk Management | Tagged: Asian stocks, banks, banks paused, Charles Schwab, Consumer Price Index, CPI, DJIA, DOW, European stocks, Fintel, gold, Meta, NASDAQ, oil, S&P 500, Schwab, Vanguard | Leave a comment »