By Dr. David Edward Marcinko; MBA MEd

SPONSOR: http://www.CertifiedMedicalPlanner.org

***

Macro Theory & Dynamics

- Adaptive Expectations — Expectations formed by adjusting past errors.

- Rational Expectations — Expectations formed using all available information.

- Hysteresis — Temporary shocks causing permanent economic effects.

- Output Gap — Difference between actual and potential GDP.

- NAIRU — Unemployment rate consistent with stable inflation.

- Okun’s Law — Relationship between unemployment and output.

- Phillips Curve — Inflation–unemployment tradeoff.

- Secular Stagnation — Persistent low growth and low interest rates.

- Liquidity Trap — Monetary policy becomes ineffective at zero rates.

- Paradox of Thrift — Higher saving reduces aggregate demand.

Monetary Economics

- Seigniorage — Revenue from money creation.

- Monetary Base — Currency + bank reserves.

- Velocity of Money — Frequency of money turnover.

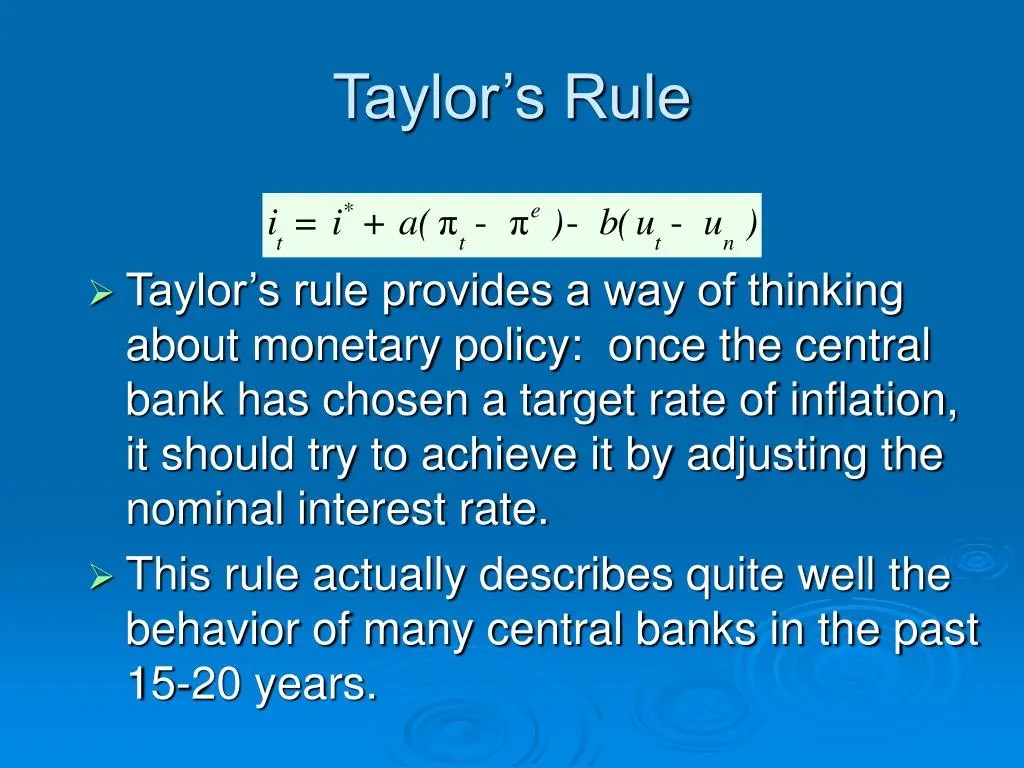

- Taylor Rule — Formula guiding interest‑rate policy.

- Quantitative Easing — Central bank asset purchases.

- Quantitative Tightening — Central bank balance‑sheet reduction.

- Open‑Market Operations — Buying/selling securities to steer rates.

- Interest‑Rate Corridor — Framework bounding short‑term rates.

- Shadow Rate — Implied policy rate when nominal rates hit zero.

- Monetary Neutrality — Money affects prices, not real output, long‑term.

International Economics

- Terms of Trade — Ratio of export to import prices.

- Purchasing Power Parity — Exchange rates adjust to equalize prices.

- J‑Curve Effect — Trade balance worsens before improving after depreciation.

- Marshall–Lerner Condition — When depreciation improves trade balance.

- Currency Substitution — Use of foreign currency domestically.

- Impossible Trinity — Cannot have fixed rates, free capital flow, and independent monetary policy simultaneously.

- Dutch Disease — Resource booms harming other sectors.

- Capital Controls — Restrictions on capital flows.

- Balance of Payments — Record of all international transactions.

- Exchange‑Rate Pass‑Through — How FX changes affect domestic prices.

Microeconomic Theory

- Deadweight Loss — Efficiency loss from distortions.

- Moral Hazard — Risk‑taking increases when consequences are externalized.

- Adverse Selection — Hidden information harms market outcomes.

- Signaling — Actions conveying private information.

- Screening — Mechanisms to reveal private information.

- Principal–Agent Problem — Misaligned incentives between delegator and agent.

- Coase Theorem — Bargaining solves externalities under zero transaction costs.

- Giffen Goods — Goods with upward‑sloping demand curves.

- Veblen Goods — Goods whose demand rises with price due to status.

- Elasticity of Substitution — Ease of replacing one input with another.

Industrial Organization

- Contestable Markets — Markets disciplined by potential entry.

- Natural Monopoly — Single firm most efficient due to scale.

- Price Discrimination — Charging different prices to different buyers.

- Two‑Sided Markets — Platforms serving interdependent user groups.

- Network Externalities — Value increases with number of users.

- Bertrand Competition — Price‑based competition.

- Cournot Competition — Quantity‑based competition.

- Monopsony Power — Buyer with market power.

- Limit Pricing — Incumbent sets low price to deter entry.

- Predatory Pricing — Pricing below cost to eliminate rivals.

Development Economics

- Big Push Theory — Coordinated investment needed for development.

- Poverty Trap — Self‑reinforcing low‑income equilibrium.

- Dual Economy — Coexistence of modern and traditional sectors.

- Informal Sector — Unregulated economic activity.

- Human Capital Externalities — Social benefits of education beyond private returns.

- Import Substitution Industrialization — Developing by replacing imports with domestic production.

- Export‑Led Growth — Growth driven by external demand.

- Dependency Theory — Underdevelopment caused by global power structures.

- Structural Adjustment — Policy reforms tied to international lending.

- Microfinance — Small loans to underserved populations.

Behavioral Economics

- Anchoring — Relying too heavily on initial information.

- Loss Aversion — Losses weigh more than gains.

- Hyperbolic Discounting — Preference for immediate rewards.

- Mental Accounting — Categorizing money irrationally.

- Prospect Theory — Decisions under risk deviate from expected utility.

- Endowment Effect — Ownership increases perceived value.

- Status Quo Bias — Preference for existing conditions.

- Framing Effects — Choices influenced by presentation.

- Bounded Rationality — Limited cognitive capacity shapes decisions.

- Time Inconsistency — Preferences change over time.

Public Finance

- Pigouvian Tax — Tax correcting externalities.

- Laffer Curve — Relationship between tax rates and revenue.

- Fiscal Multipliers — Impact of government spending on output.

- Automatic Stabilizers — Built‑in fiscal responses to cycles.

- Ricardian Equivalence — Debt‑financed spending may not affect demand.

- Tax Incidence — Who ultimately bears a tax burden.

- Public Goods — Non‑rival, non‑excludable goods.

- Common‑Pool Resources — Rival but hard‑to‑exclude resources.

- Fiscal Federalism — Allocation of fiscal powers across government levels.

- Crowding Out — Government borrowing reducing private investment.

Labor Economics

- Efficiency Wages — Paying above market wage to boost productivity.

- Search Frictions — Costs and delays in matching workers to jobs.

- Matching Function — Relationship between vacancies and hires.

- Labor Hoarding — Firms retain workers during downturns.

- Reservation Wage — Minimum wage a worker accepts.

- Insider–Outsider Theory — Incumbent workers influence wage setting.

- Wage Stickiness — Wages slow to adjust downward.

- Human Capital Accumulation — Skills gained through education/experience.

- Labor Share — Portion of income going to workers.

- Gig Economy — Flexible, platform‑based labor markets.

Advanced & Miscellaneous

- General Equilibrium — All markets clearing simultaneously.

- Arrow–Debreu Model — Formal model of complete markets.

- Dynamic Stochastic General Equilibrium — Micro‑founded macro modeling.

- Overlapping Generations Model — Multi‑cohort economic modeling.

- Endogenous Growth Theory — Growth driven by internal factors.

- Creative Destruction — Innovation displacing old industries.

- Path Dependence — History shapes current outcomes.

- Transaction Costs — Costs of making economic exchanges.

- Information Asymmetry — Unequal access to information.

- Externalities — Spillover costs or benefits.

COMMENTS APPRECIATED

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR- http://www.MarcinkoAssociates.com

Like, Refer and Subscribe

HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

CLINICS: http://www.crcpress.com/product/isbn/9781439879900

ADVISORS: www.CertifiedMedicalPlanner.org

FINANCE:Financial Planning for Physicians and Advisors

INSURANCE:Risk Management and Insurance Strategies for Physicians and Advisors

Dictionary of Health Economics and Finance

Dictionary of Health Information Technology and Security

Dictionary of Health Insurance and Managed Care

***

Share this:

Filed under: iMBA, Inc. | Tagged: arcane, economics, economy, econonic, finance, inflation, Marcinko, politics, terms | Leave a comment »