BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

A FICO score is one of the most influential tools in modern consumer finance, shaping how individuals access credit, the cost of borrowing, and even broader life opportunities. Developed by the Fair Isaac Corporation, the score condenses a person’s credit history into a three‑digit number ranging from 300 to 850. While deceptively simple on the surface, this number reflects a complex evaluation of financial behavior and risk. Over time, the FICO score has become a central mechanism through which lenders make decisions, and its influence extends into housing, employment, insurance, and beyond.

At its core, a FICO score attempts to answer a single question: How likely is a borrower to repay a loan on time? To estimate this, the scoring model analyzes several categories of credit information. The most significant factor is payment history, which accounts for a substantial portion of the score. Late payments, defaults, and collections signal higher risk, while consistent on‑time payments demonstrate reliability. The second major factor is credit utilization, or the percentage of available revolving credit that a person is currently using. High utilization suggests financial strain, while low utilization indicates stability. Other components include the length of credit history, the mix of credit types, and recent credit inquiries. Together, these elements form a predictive model that lenders rely on to assess risk quickly and consistently.

The importance of the FICO score lies in its widespread adoption. Banks, credit unions, mortgage lenders, auto lenders, and credit card issuers all use it as a primary decision‑making tool. A higher score typically leads to lower interest rates, better loan terms, and greater access to credit products. Conversely, a lower score can result in higher borrowing costs or outright denial of credit. This dynamic creates a powerful incentive for consumers to understand and manage their credit behavior carefully. In many ways, the FICO score functions as a financial reputation — a shorthand that follows individuals throughout their economic lives.

Beyond lending, the FICO score has expanded into other domains. Landlords often use credit scores to evaluate rental applicants, viewing them as indicators of reliability. Some employers, particularly in financial sectors, review credit reports (though not always the score itself) as part of background checks. Insurance companies may use credit‑based insurance scores to set premiums. These broader applications mean that a person’s credit behavior can influence not only their financial opportunities but also their housing stability, employment prospects, and cost of living. The score’s reach underscores its role as a structural component of economic mobility.

Despite its usefulness, the FICO score is not without criticism. One major concern is that it can reinforce existing inequalities. Individuals with limited credit histories — often young adults, immigrants, or those from low‑income backgrounds — may struggle to achieve high scores, not because they are irresponsible, but because they lack access to traditional credit products. Negative financial events, such as medical debt or job loss, can disproportionately affect vulnerable populations and depress scores for years. Critics argue that the model does not fully account for context, such as systemic barriers or unexpected hardships. As a result, the score can sometimes reflect circumstances rather than character or capability.

Another critique centers on transparency. While the general factors influencing a FICO score are publicly known, the exact algorithms are proprietary. This opacity can make it difficult for consumers to understand precisely how their actions will affect their score. Although educational tools and credit monitoring services have become more common, many people still find the system confusing or intimidating. The complexity of the scoring model can lead to misconceptions, such as the belief that carrying a balance improves a score or that checking one’s own credit is harmful. These misunderstandings can hinder effective credit management.

Despite these challenges, the FICO score remains deeply embedded in the financial system. Efforts to improve credit scoring have emerged, including models that incorporate alternative data such as rent payments, utility bills, or banking activity. These innovations aim to create a more inclusive and accurate picture of financial behavior. However, the traditional FICO score continues to dominate lending decisions, and its influence is unlikely to diminish in the near future.

Ultimately, the FICO score is both a practical tool and a symbol of the broader credit system. It rewards consistent, responsible financial behavior, but it also reflects structural realities that can advantage some individuals over others. Understanding how the score works empowers consumers to navigate the financial landscape more effectively. By managing payment history, keeping credit utilization low, maintaining long‑standing accounts, and avoiding unnecessary credit inquiries, individuals can strengthen their financial profile and expand their opportunities.

In a society where credit access plays a central role in economic life, the FICO score functions as a key determinant of financial possibility. It is a number that can open doors or close them, shape futures, and influence the trajectory of a person’s financial journey. While not perfect, it remains a powerful indicator of creditworthiness and a critical component of modern financial identity.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on February 4, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Long-Term Liabilities

A secured debt is pledged by a specific property. This is a collateralized loan.

Generally, the purchased item is pledged with the proceeds of the loan. This would include long-term liabilities (more than 12 months) such as a mortgage, home equity loan, or a car loan. Although the creditor has the ability to take possession of your property in order to recover a bad debt, it is done very rarely. A creditor is more interested in recovering money. Sometimes, when borrowing money, there may be a requirement to pledge assets that are owned prior to the loan.

For example, a personal loan from a finance company requires that you pledge all personal property such as your car, furniture, and equipment. The same property may become subject to a judicial lien if you are sued and a judgment is made against you. In this case, you would not be able to sell or pledge these assets until the judgment is satisfied. A common example of a lien would be from unpaid federal, state or local taxes. Doctors can be found personally liable for unpaid payroll taxes of employees in their professional corporations.

***

Distinguishing from Short-Term Liabilities

The primary distinction between long-term and short-term liabilities lies in their repayment timing. Long-term liabilities are obligations due beyond one year, while short-term, or current, liabilities are financial obligations settled within one year of the balance sheet date or the company’s operating cycle, whichever is longer. This timing difference impacts how these obligations are viewed in financial analysis.

Examples of short-term liabilities include accounts payable, which are amounts owed to suppliers for goods or services purchased on credit, typically due within 30 to 60 days. Other common short-term obligations are short-term notes payable, accrued expenses like salaries or utilities, and the portion of long-term debt that becomes due within the next 12 months. These obligations are usually paid using current assets.

This distinction is important for financial analysis, as it helps assess a company’s financial health. Short-term liabilities are relevant for evaluating a company’s liquidity, its ability to meet immediate financial obligations. Conversely, long-term liabilities provide insights into a company’s solvency, indicating its ability to meet financial obligations over an extended period and its overall financial stability.

***

Finally, be aware that some assets and liabilities defy short or long-term definition. When this happens, simply be consistent in your comparison of financial statements, over time.

Rental income can be an attractive source of passive income for physicians seeking financial diversification beyond clinical practice. However, while real estate investing offers potential tax advantages and long-term wealth accumulation, it also carries a unique set of risks that doctors must carefully consider before entering the market.

One of the primary risks is time and management burden. Physicians often work long hours and have demanding schedules, leaving little time to manage rental properties. Even with property managers, landlords must make decisions about maintenance, tenant issues, and legal compliance. Unexpected repairs, vacancies, or tenant disputes can quickly consume time and energy, detracting from a physician’s core professional responsibilities.

***

***

Another significant concern is financial exposure. Real estate investments typically require substantial upfront capital, and financing through loans adds debt to a physician’s balance sheet. If the property fails to generate consistent rental income—due to market downturns, high vacancy rates, or unreliable tenants—the investor may struggle to cover mortgage payments, property taxes, and maintenance costs. This can lead to cash flow problems and even jeopardize personal financial stability.

Market volatility also poses a risk. Real estate values and rental demand fluctuate based on economic conditions, interest rates, and local market trends. Physicians who invest in properties without thoroughly researching the area or understanding market cycles may find themselves holding depreciating assets or facing difficulty finding tenants. Unlike stocks or bonds, real estate is illiquid, meaning it cannot be easily sold in a downturn without potentially incurring losses.

Legal and regulatory risks are another consideration. Landlords must comply with local housing laws, fair housing regulations, and safety codes. Failure to do so can result in fines, lawsuits, or reputational damage. Physicians unfamiliar with these legal frameworks may inadvertently violate rules, especially if they rely on informal advice or neglect to consult legal professionals.

Additionally, tax complexity can be a challenge. While rental income may offer deductions for depreciation, mortgage interest, and operating expenses, navigating these benefits requires careful record-keeping and often professional tax guidance. Misreporting income or deductions can trigger audits or penalties, adding stress and financial risk to the investment.

***

***

Finally, there’s the opportunity cost. Time and money spent on rental properties could be invested in other ventures, such as medical practice expansion, retirement accounts, or diversified portfolios. Physicians must weigh whether real estate aligns with their long-term financial goals and risk tolerance.

In conclusion, while rental income can be a valuable tool for wealth building, it is not without its pitfalls. Doctors considering this path should conduct thorough due diligence, seek professional advice, and assess whether the demands and risks of property ownership fit their lifestyle and financial strategy. A well-informed approach can help mitigate these risks and turn rental income into a sustainable asset rather than a liability.

Posted on November 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

An Overview

Introduction In the world of finance, the distinction between recourse and non-recourse loans is critical. Non-recourse financing refers to loans in which the lender’s rights are limited strictly to the collateral pledged for the loan. If the borrower defaults, the lender cannot pursue the borrower’s personal assets or income beyond the collateral. This structure makes non-recourse loans particularly attractive to borrowers who want to protect their broader financial portfolio, though it comes with trade-offs such as higher interest rates and stricter eligibility requirements.

Definition and Core Features

A non-recourse loan is secured by collateral, typically real estate or high-value assets. Unlike recourse loans, where lenders can seize collateral and pursue additional assets if the collateral does not cover the debt, non-recourse loans restrict recovery to the collateral alone.

Key features include:

Collateral-based repayment: Only the pledged asset can be seized.

Borrower protection: Other personal or business assets remain untouched.

Higher lender risk: Because recovery is limited, lenders face greater exposure.

Higher interest rates: To offset risk, lenders often charge more.

Applications in Real Estate and Project Financing

Non-recourse financing is most common in commercial real estate and large-scale projects. For example, developers building shopping centers or office towers often rely on non-recourse loans because repayment depends on future rental income once the project is complete. Similarly, infrastructure projects with long lead times—such as energy plants or toll roads—use non-recourse financing to align repayment with project revenues.

This structure allows borrowers to undertake ambitious projects without risking personal bankruptcy if the venture fails. It also encourages investment in sectors where upfront costs are high and returns are delayed.

Comparison with Recourse Loans

The difference between recourse and non-recourse loans lies in risk allocation:

Recourse loans: Lenders can seize collateral and pursue other assets. These loans are lower risk for lenders and typically carry lower interest rates.

Non-recourse loans: Lenders are limited to collateral. Borrowers gain protection, but lenders demand higher rates and stricter terms.

This trade-off means non-recourse loans are less common and usually reserved for borrowers with strong creditworthiness or projects with predictable revenue streams.

Advantages of Non-Recourse Financing

Risk limitation for borrowers: Protects personal wealth and other business assets.

Encourages investment: Makes large-scale, high-risk projects feasible.

Predictable liability: Borrowers know their maximum exposure is limited to collateral.

Disadvantages and Risks

Higher costs: Interest rates and fees are higher due to lender risk.

Strict eligibility: Only borrowers with strong financial standing or valuable collateral qualify.

Collateral dependency: If the collateral loses value, lenders face significant losses.

Bad boy carve-outs: Certain clauses allow lenders to pursue borrowers if fraud, misrepresentation, or intentional misconduct occurs.

Legal and Financial Implications

Non-recourse financing is shaped by legal frameworks that define lender rights. In many jurisdictions, lenders cannot pursue deficiency judgments beyond collateral. However, exceptions exist through “bad boy carve-outs,” which hold borrowers personally liable for misconduct such as misappropriation of funds or environmental violations.

Conclusion

Non-recourse financing is a powerful tool in modern finance, particularly for commercial real estate and infrastructure projects. By limiting borrower liability to collateral, it enables ambitious ventures while protecting personal assets. However, this protection comes at the cost of higher interest rates, stricter eligibility, and potential carve-outs that reintroduce personal liability. Ultimately, non-recourse loans represent a balance between borrower protection and lender risk, shaping the way large-scale projects are funded and developed.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The following are 4 common financial psychological biases. Some are learned while others are genetically determined (and often socially reinforced). While this essay focuses on the financial and investing implications of these biases, they are prevalent in most areas in life.

Loss aversion affected many investors during the stock market crash of 2007-08 or the flash crash of May 6, 2010 also known as the crash of 2:45. During the crash, many people decided they couldn’t afford to lose more and sold their investments.

Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading.

Data convincingly shows that people who trade most often under-perform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we got it.

For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does.

For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

The so-called money factor (abbreviated as MF on invoices) is a number in a decimal form that dealers use to calculate the APR of a car lease. It’s a major part of your monthly payment and dealers are known to jack up the money factor to pad their profits.

Most doctors don’t ask to see it because they’re not aware of it or don’t know how to calculate it. Ask to see the money factor, then multiply it by 2,400.

For example, if the money factor is .00150, you multiply it by 2,400 to get 3.6%. If that’s higher than the prevailing rate, you have room to talk them down.

How to reduce it

So how do you get a good interest rate when you lease a vehicle? The same way you do when borrowing for any other reason, whether it’s buying a home or applying for a personal loan: by having good credit. This may reduce your interest rate because you’ll represent a lower risk to a lender.

A high residual value on the car could also help you get a better interest rate. A higher residual value means you’d have lower monthly payments because there would be less depreciation on the vehicle. Since interest is applied to your monthly payment, a lower monthly payment would equate to reduced interest charges.

The money factor is one of the many numbers you may want to learn about when leasing a car. It’s one of the transactional costs that come with leasing, and allows dealers and finance companies to make a profit on every lease they execute. As a consumer, it’s a smart idea to learn the financial implications of this number and how it’ll affect your overall costs over the course of a multi-year lease.

***

***

If the interest rate is too high, you may need to shop around for a better rate, negotiate with the dealer or lender to lower the money factor, or consider leasing another vehicle that’s more in line with your budget. Either way, make sure you explore all your financial options before taking a car off the lot.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP™

***

***

When Maria needed $400,000 for a down payment on a new home, her broker at a large Wall Street firm offered a solution: “Don’t sell investments and trigger capital gains. Just take out a margin loan.”

A margin loan is a line of credit from a brokerage firm, secured by the client’s investment portfolio. It offers quick access to cash with no immediate tax consequences and minimal paperwork. But the convenience comes at a cost. As of mid-2025, margin loan interest rates range from 6.25% to over 11%.

Margin loan recommendations are often presented by brokers as tax-savvy strategies that allow clients to access “tax-free” cash while keeping their portfolios intact. In many cases, however, the math benefits the advisor more than the investor. The cost of borrowing often exceeds what an investor is likely to earn by holding on.

For example, let’s assume an interest rate of 7.5% on Maria’s $400,000 margin loan. While borrowing delayed the payment of $20,000 in capital gains tax, she will eventually have to pay that tax anyway unless she holds the investments until her death. Two years later, with portfolio returns of 4% annually, she had earned around $32,000 from the $400,000 in investments she might have sold. Meanwhile, she had paid $60,000 in interest—leaving her some $28,000 worse off. That’s without factoring in ongoing interest payments, or the risks of a margin call if the investments securing the loan drop in value.

Why do advisors keep recommending margin loans? Because selling investments reduces the portfolio size and the advisor’s fee. Borrowing keeps the portfolio intact and the compensation unchanged—while the firm receives additional income from interest on the loan. In some cases, advisors suggest using margin loans to buy more investments, increasing both the portfolio and the fee they collect.

None of this is illegal. But when the borrowing cost is higher than expected returns and the advisor benefits financially, the ethics are questionable. The client takes the risk, while the advisor keeps the revenue.

This kind of conflict appears more often in portfolios where compensation is tied to asset volume and the company’s primary culture rewards gathering assets over delivering unbiased advice. By contrast, fee-only financial planning and investment advisors typically operate on simpler hourly, flat, or tiered fee structures. Their compensation doesn’t depend on whether a client borrows, sells, or holds. The culture of the firm focuses on conflict-free advice aligned with the client’s best interest.

Wall Street brokers are often held to a fiduciary standard, but structure still matters. In 2024 the SEC reported their examinations of brokers would continue to focus on advisor recommendations unduly influenced by the company’s compensation and incentives.

There are rare situations where a margin loan may be appropriate. A client with large unrealized gains might use a short-term margin loan to minimize taxes. An elderly investor might borrow tax-free rather than sell assets that will receive a step-up in basis at their death. Even in those cases, the math must be exact and the client must clearly understand the risks, including the possibility of a margin call.

If your advisor recommends a margin loan, especially to buy more investments, ask strong questions. What’s the interest rate? What return is realistic? What are the tax consequences of selling? How does this affect the advisor’s income?

In a high-rate, low-return environment, margin loans rarely favor the client. The exceptions are narrow. The risks are significant. And the conflict of interest is measurable.

Sometimes the smartest move is the simplest: sell what you need, pay the tax, and leave leverage out of your plan.

Posted on May 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

Today, we’re diving into two thought-provoking questions:

What’s a famous investment rule I don’t agree with? Which key characteristics should a good investor have? Again:

What’s a famous investment rule I don’t agree with?

Which key characteristics should a good investor have?

A Famous Investment Rule I Don’t Agree With: “Buy and Hold”

Buy and hold becomes a religion during bull markets. Then, holding a stock because you bought it is often rewarded through higher and higher valuations. There’s a Pavlovian bull market reinforcement – every time you don’t sell (hold) a stock, it goes higher.

Buying is a decision. So is holding, but it should not be a religion but a decision. The value of any company is the present value of its cash flows. When the present value of cash flows (per share) is less than the price of the stock, the stock should not be “held” but sold.

WarrenBuffett is looked upon as the deity of buy and hold.

Look at Coca Cola when it hit $40 in 1999. Its earnings power at the time was about $0.80. It was trading at 50 times earnings. It was significantly overvalued, considering that most of the growth for this company was in the past.

Fast-forward almost a quarter of a century – literally a generation. Today the stock is at $60. It took more than a decade to reclaim its 1999 high. Today, Coke’s earnings power is around $1.50–1.90. Earnings have stagnated for over a decade. If you did not sell the stock in 1999, you collected some dividends, not a lot but some. The stock is still trading at 30–40x earnings. Unless they discover that Coke cures diabetes (not causes it), its earnings will not move much. It’s a mature business with significant health headwinds against it.

“Long-term” and “buy-and-hold” investing are often confused.

People should not own stocks unless they have a long-term time horizon. Long-term investing is an attitude, an analytical approach. When you build a discounted cash flow model, you are looking decades ahead. However, this doesn’t mean that you should stop analyzing the company’s valuation and fundamentals after you buy the stock, as they may change and affect your expected return. After you put in a lot of analytical work and buy the stock, you should not simply switch off your brain and become a mindless buy-and-hold investor.

This doesn’t mean you shouldn’t be patient, but holding, not selling, a stock is a decision.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

OVER HEARD IN THE FINANCIAL ADVISOR’S LOUNGE

***

***

By Perry D’Alessio, CPA [D’Alessio Tocci & Pell LLP]

What I see in my accounting practice is that significant accumulation in younger physician portfolio growth is not happening as it once did. This is partially because confidence in the equity markets is still not what it was; but that doctors are also looking for better solutions to support their reduced incomes.

For example, I see older doctors with about 25 percent of their wealth in the market, and even in retirement years, do not rely much on that accumulation to live on. Of this 25 percent, about 80 percent is in their retirement plan, as tax breaks for funding are just too good to ignore.

What I do see is that about 50 percent of senior physician wealth is in rental real estate, both in a private residence that has a rental component, and mixed-use properties. It is this that provides a good portion of income in retirement.

***

***

QUESTION: So, could I add dialog about real estate as a long term solution for retirement?

Yes, as I believe a real estate concentration in the amount of 5 percent is optimal for a diversified portfolio, but in a very passive way through mutual or index funds that are invested in real estate holdings and not directly owning properties.

Today, as an option, we have the ability to take pension plan assets and transfer marketable securities for rental property to be held inside the plan collecting rents instead of dividends.

Real estate holdings never vary very much, tend to go up modestly, and have preferential tax treatment due to depreciation of the property against income.

Posted on April 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

THE “FIVE-FIVE” FINANCIAL RULE

By Staff Reporters

***

***

Many of the pros of home ownership will appeal to medical retirees for whom their home is their castle and who appreciate being settled both financially and geographically:

1. Building equity in your home: Each mortgage payment you make brings you closer to owning your house free and clear with no payments. If you can buy a new home or condo outright by selling your current home, you can still build equity in your new home over time.

2. Predictability: If you have a fixed-rate mortgage, your mortgage payments will remain consistent for years and you don’t have to worry about a landlord ever making you move.

3. Tax benefits: You can deduct mortgage interest and property taxes up to certain limits.

4. Customization: You don’t need a landlord’s permission to alter and improve your home.

5. Home appreciation: Homes generally increase in value, so you can increase your net worth by owning a property.

***

***

Renting also has five significant upsides, particularly for physician retirees who want greater freedom to travel and to make bigger moves — potentially across the country or even abroad:

1. Extreme flexibility: You can leave your property after giving notice and go wherever you want much more easily than with an illiquid home you’d have to sell first.

2. Lower upfront costs: You only have to pay first and last month’s rent and a security deposit to move into a rental, not make a large home down payment.

3. No maintenance concerns: If something breaks, your landlord is responsible for the cost of fixing it and the actual repairs. You don’t have to build up an emergency fund for maintenance.

4. Predictable expenses: For the duration of your lease, your monthly housing costs including utilities will remain consistent, even if the cost of energy goes up, for example.

5. Lack of worry: If you’re in a rental apartment, you won’t have to concern yourself with shoveling snow, mowing grass or other matters of upkeep.

Posted on March 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

[Reviewing Terms, Conditions and Selling Agreements]

By Dr. Charles F. Fenton III JD

***

***

Dealing with many issues concerning the actual contract that affect the purchase or sale of a medical practice can be daunting. For example, this chapter will not deal with issue of determining whether or not a physician should retire. Nor will it determine the proper Fair Market Value [FMV] of the practice. However, physicians may be assisted in both instances by a medically focused financial advisor, or valuation specialist. [AVA, CPA-CVA, Certified Medical Planner™; etc] working in conjunction with an experience health care contract attorney to act as an advocate and determine certain contingencies that might occur, and protect him/her from them.

THE PARTIES

The first determination is whether the party at interest is an individual, group of individuals, or an entity (such as a partnership, limited liability partnership, limited partnership, limited liability company, or corporation – whether an S corporation, C corporation or a professional corporation). In many instances, even if the party at interest is an individual is an entity, the individual or individuals behind the entity should be made parties to the agreement.

From the buyer’s perspective, the purchase of a medical practice is a highly person-oriented business. The practice value depends much upon the personality of the current treating physicians. If the current treating physicians are also the owners of the entity, then binding those individuals (especially as applies to the restrictive covenant) is of primary importance.

If the current treating physicians are not owners of the entity, but rather employees, then a determination of whether they will continue in their same positions or whether the buyer will be taking over the treatment of patients becomes the prime focus. If the current treating physicians will be continuing in their same positions, then their current employment contract must be reviewed to determine whether the rights of the seller will accrue to the buyer.

If the rights of the seller will not accrue to the buyer, then the Purchase and Sale Agreement must have a provision that makes the continued employment of those current-treating physicians a condition to consummation of the sale. In such instances, the new employment agreement might be an exhibit to the main agreement and executed contemporaneously with the main agreement.

If the current treating physicians will not be continuing in their same position and if the purchaser will be assuming treatment of the patients, then the main agreement must provide for the dissolution of the employment agreement and provision must be made for restricting the ability of those physicians from competing with the buyer. If the employment contract with the seller contains a restrictive covenant, then the buyer must ensure that such covenants will accrue to the buyers benefit. Otherwise, the buyer should insist that those physicians sign restrictive covenants. In such an instance, a portion of the purchase price may need to be allocated towards the consideration for those restrictive covenants and paid directly to those physicians.

DATE OF AGREEMENT AND CLOSING DATE

In general, it usually does not matter when the agreement is dated. It should usually be dated once all the terms are agreed to and the parties desire to bind each other and to be bound. In certain instance, the parties may have reached an agreement, but certain issues (such as the obtaining of a state license to practice medicine) may be outstanding. In such a case, then an option can be given by either the seller or the buyer to bind the other to sell or buy the practice upon exercise of the option. Giving an option can also push the agreement date into the future. The option will usually be given with token consideration (e.g., one hundred dollars) and will have a fixed expiration date (e.g., thirty to ninety days).

The determination of the closing date is more important than the date that the agreement is dated. Just like in the purchase of a house where certain issues (such as obtaining a mortgage and home inspection) must occur before closing, in the purchase of a practice, there may be certain issues which require time to undertake before the actual transfer can be consummated. For example, the buyer may still need to obtain financing or the landlord may need to approve the assignment of the lease.

RECITALS

The recitals – or “whereas” clauses – traditionally enunciate the reasons the parties are entering into the agreement. In the sale of the practice the recitals may simply state that the buyer wishes to buy the practice and the seller wishes to sell the practice. Yet, there is a modern growing tendency among contract attorneys to eliminate the “whereas” clauses as some attorneys feel that such language is antiquated. In such instances, the agreement will simply have a paragraph or two delineation of the “Purpose” of the agreement.

ARTICLES, SECTIONS, AND PARAGRAPHS

The agreement will often be divided and numbered in some logical fashion, either into articles, sections, paragraphs, or a combination of these. The reason for doing so is twofold. First, it allows ready reference to the numbered paragraph, and secondly it allows the agreement to be divided and grouped in logical associations.

BINDING THE PARTIES

The first paragraph of the first article will often bind the seller to sell and the buyer to buy the practice under the terms of the agreement. The rest of the agreement simply spells out those terms.

WHAT IS PURCHASED?

The agreement must disclose the items which are being transferred and the items which are not considered part of the agreement. This section should be crystal clear, so that anybody reading the contract (and hence a court which may be called upon to enforce the contract) and not privy to the preliminary negotiations will know what is part of the agreement and what is not part of the agreement.

[1] Sale of Stock vs. Sale of Assets

In most cases, well-informed financial advisors [FAs] will recommend that the buyer solely purchase the assets of the practice and not the stock of the practice. By purchasing selected assets, the buyer is ensured that he will not become responsible for the known or unknown liabilities of the corporation. In prior days, avoiding purchasing the stock of the corporation was a wise recommendation.

However, with the advent of managed care, the purchase of the stock of the corporation can provide the new practitioner with certain competitive advantages. It may take a new practitioner three to nine months to get onto enough managed care panels to make the practice profitable. Purchase of the stock of the corporation ensures the new practitioner of acquiring the Federal Tax Identification Number [TIN], Personal Identification Number [PIN], Drug Enforcement Agency [DEA], Centers for Medicare and Medicaid [CMS], Global Location Number [GLN] , National Provider Identifier [NPI], HIE-Form 834 transmission number, Durable Medical Equipment Number [DME] etc, of the corporate entity. Since most managed care corporations identify providers by the Federal TIN, purchase of the stock of the corporation should allow the new practitioner to be enrolled on managed care panels in a shorter period of time.

[2] Items Purchased

Items purchased often lists the tangible and intangible property of the seller which will be transferred to the buyer. Such items often include:

A detailed inventory of the tangible assets to be purchased;

A detailed listing of the inventory of the practice;

The names and addresses of all of the patients of record treated by the seller;

The patient medical records maintained by seller;

The computer records maintained by seller;

All licenses, permits, accreditation and franchises issued by any federal, state, municipal, or quasi-government authority relating to the use, maintenance or operation of the practice, running to or in favor of seller, but only to the extent that they are accepted by buyer;

All of sellers’ right, title, and interest in and to all real estate and equipment leases, if any, services agreements, employment and professional service contracts relating to the practice but only to the extent that the foregoing are accepted by buyer;

Assignment of lease should be attached and be incorporated to the agreement;

All existing telephone numbers used in connection with the operation of the practice and all yellow page advertising of the practice; and

The goodwill of the practice, which includes seller’s assistance and cooperation in transfer of all sellers’ rights and interests in the practice to buyer and any other intangible assets of the practice not listed in any other category.

Certain items purchased, such as [paper or electronic] medical records, governmental licenses, fax, email, website and telephone numbers have special considerations as discussed below.

[3] Medical Records

The seller should protect its future need to use the transferred patient medical records. In the current managed care environment, providers are subject to strict scrutiny. Even after leaving practice the provider may find himself subject to a government or third party audit or subject to a medical malpractice lawsuit. Therefore, the provider should ensure that the contract allows for him to take future possession of the specific medical record(s) of the practice in order to mount an appropriate defense.

[4] Governmental Licenses

Certain government licenses and permits may be nontransferable. These would include items such as the federal and state employer identification numbers, as these are unique to seller as a corporate entity. Likewise, other items unique to seller include Medicare identification numbers, Medicaid identification numbers, NPIs and UPINs. The buyer would have to purchase the stock of the corporation order to acquire such items, which is another advantage of a stock transaction versus an asset transaction. Likewise, some local business licenses may or may not be transferable.

[5] Telephone and Fax Numbers, Website URLs and Twitter [X] Accounts, etc

Transference of the telephone numbers often requires that a special local telephone company form authorizing transfer of the telephone numbers to the buyer. Often the new owner of the telephone number will also become liable for any current yellow page advertisement monthly fees. It is the same with an URL or website or e-mail address or office Twitter X account, etc.

[6] Items Not Purchased

Items not purchased or “excluded items” often list the personal items of the parties or of the employees of the parties. Such items would often include:

All cash on hand or on deposit;

All accounts receivable generated prior to the closing date;

All prepaid expenses, utility deposits, tax rebates, insurance claims, credits due from suppliers and other allowances after Closing Date;

The personal effects, including but not limited to photographs, diplomas, uniforms, books, mementos, memorabilia, personally owned art and any personal property owned by them;

Life insurance, disability insurance, and disability buy-out insurance on seller;

Motor vehicles used in connection with the practice;

Any or all tangible-intangible assets used in conjunction with another practice of seller; and

All other assets owned by seller other than those specifically described as items purchased.

The exact items transferred will often depend upon the prior negotiations of the parties. For example, the parties may have agreed that the accounts receivable will be transferred with the practice. In such an instance, the accounts receivable will be listed as an item to be purchased.

PURCHASE PRICE AND TERMS

The price of the transaction (or the value of the practice) is often the one item that is aggressively negotiated between the parties. That is because both the buyer and the seller are overly concerned with “how much?” As this chapter demonstrates, there are a lot more details that go into the negotiation and final contract than just the price. The buyer or seller would be doing themselves a disservice to consider the other factors simply “lawyer details.” Many additional terms of the agreement should be considered by one side or the other as “walk-way” conditions. The party that fully adheres to their additional terms is likely to find the other party capitulating to them. This is because the other party will most likely be fixated on the price.

The purchase price should be delineated in the agreement. Furthermore, the method of payment of the purchase price should be delineated. Although the usual method of payment would be cash, there are other methods available as well.

Cash payment can be made by an official bank cashier’s check, by a certified check, by deposit of funds into an escrow account, or by other method agreed upon by the parties.

Non-cash type transactions include loan agreements and exchanges. Exchanges can provide certain tax benefits if the exchange is a “like kind” exchange. A like kind exchange would occur when parties swap practices. For example, a group practice might have several offices. As part of the breakup of the group, the parties might exchange their stock of one office for all of the stock of another office. Like kind exchanges have strict guidelines that must be adhered to or the tax advantages will disappear. The reader is cautioned to get current legal and financial advice prior to the time of exchange.

It is in the seller’s best interest to get all cash at the time of closing. Then the seller can walk away and not worry about the success or failure of his predecessor. The seller will not have to worry about collecting periodic payments. The seller will not have to worry about placing the buyer in default or about eventually having to repossess the practice and begin to practice medicine at that office again. If a seller repossesses a practice, the buyer may have driven the patients away or lost the managed care contracts (why else would the buyer not be able to honor the loan agreement?). So the repossessed practice will have a significantly lower market value – if it is even marketable at that time.

On the opposite end of the spectrum, it is in the buyer’s best interest to get long and lean loan terms. First, by getting loan terms, the buyer will often have to come up with much less initial capital. Second, because of the discussion in the preceding paragraph, the seller has a vested interest in ensuring that the buyer succeeds once the practice changes hands.

If the transaction involves a seller-financed loan, then the agreement should specify the terms. Additionally, a separate loan agreement and security agreement should be attached as exhibits to the agreement. Finally, in order to perfect the security agreement, the lien should be recorded at the local courthouse in accordance to local rules and customs.

***

***

ALLOCATION OF PURCHASE PRICE

The final purchase price will actually be the amalgamation of various assets of the practice. Those assets include the tangible and intangible assets. The tangible assets include the hard assets (such as computers, treatment tables, chairs and furniture, DME and x-ray machines, etc) and the soft assets (such as Q-tips, paper and cotton balls). The intangible assets will include going concern value, goodwill, and the value of any restrictive covenant.

The parties should delineate the allocation of the purchase price amongst those various categories to reach a mutual best fit with the potential tax obligations. The buyer is the one who should strive to make the allocation fit his needs as best as possible.

Generally, the sale of the assets will be ordinary income to the seller and taxed at the seller’s usual rate. The buyer will be able to depreciate the purchased items. However, the characterization of those assets and the allocated portion of the purchase price will determine how much can be depreciated and over what time period the items can be depreciated.

As a general rule, soft assets can be depreciated fully in the year of purchase. Generally, hard assets can be depreciated over a three to seven year time period, depending upon the class of the asset. Also, under Section §179, a certain dollar amount can be “expensed” or deducted in the year of purchase. The sooner and the faster that the assets can be deducted the less current taxes that the buyer will be required to pay. However, intangible assets generally must be deducted over a 15-year period. This prolongs the tax benefits of any payments characterized as such.

Nonetheless, purchase of the assets results in better tax consequences that purchase of the stock of the practice. When stock is purchased, there is no depreciation allowance allocated in the current or subsequent years. Instead, the cost of the stock becomes the “basis” of the buyer in the practice. Any gain or loss from that basis will only have tax benefits or tax consequences in the year that the stock is sold or becomes worthless.

Because of the tax consequences of the characterization of the allocations of the purchase price, it is important that the agreement delineate the portion of the practice price which is allocated to each category. Each party should further agree never to claim a different allocation in any future tax filings. Generally, the soft and hard assets will be valued at their current actual cash value. In no event should the purchase price allocated to the soft and hard assets exceed the actual initial cost that the seller paid for the item. The only exception to the foregoing would be if the sale involved the transfer of an appreciable asset.

LEASE ASSIGNMENT

The agreement should provide that upon closing that the seller will assign the lease to the buyer. The buyer then acquires possession of the premises and assumes responsibility for the lease payments.

Sellers often do not understand that even though they do not practice at the leased premises and even though the buyer is making the lease payments, that the seller still remains liable to the landlord under the original lease. Usually this does not present a problem for the seller. But if the buyer abandons the premises or stops making the lease payments, then the landlord will look to the seller for the lease payments through the expiration of the lease.

If the seller has signed a restrictive covenant, then the seller may find himself in the unenviable position of making lease payments for the premises and prohibited from practicing at the premises. The seller should protect himself from this possibility. Therefore, the seller should ensure that the original agreement contains a provision that if the seller becomes liable under the lease that the seller can enter onto the premises, take possession of the practice and the practice assets and can practice medicine at the location until the seller’s liabilities are extinguished.

INDEMNIFICATION AND EXCLUSION/INCLUSION OF LIABILITIES

During the sale of a medical practice, each party will have certain liabilities that the other party should not assume and should not be required to assume. A mutual indemnification clause will act to ensure that each party remains liable for its own liabilities.

In a medical practice, the most common liability is a claim of medical malpractice against the provider. The seller has an interest in insuring that he is not liable for any claim brought by a patient that resulted after he leaves the practice and the buyer has an interest in insuring that she is not liable for any claim brought by a patient that resulted before she acquired the practice.

There are other areas of liability in the sale of a medical practice that may not be readily apparent. These include premise liability (e.g., slip and fall claims), employment claims (e.g., unemployment liability, sexual harassment, discrimination, and wrongful termination claims), tax claims (e.g., unpaid employment taxes and income or sales tax liabilities), and third party payer claims (e.g., Medicare recoupment claims). Consult your insurance agent to determine whether you can obtain insurance coverage to limit your liability under these clauses.

Medical practitioners should understand the full risk of signing an indemnification or hold harmless clause. If a claim is brought against the other party, then the party giving indemnification can be forced to pay any judgment or settlement incurred by that other party. The party giving indemnification can even be required to pay the other party’s attorney bills. This is an important point that the reader should consider carefully: Even if the other party successfully defends a claim, the indemnifying party can be held liable for the other party’s attorney’s fees. Since attorney fees can mount up rapidly, the indemnifying party can find itself responsible for thousands or even tens or thousands of dollars of attorneys’ fees.

If at all possible, one should never sign an indemnification agreement, whether in the sale of a medical practice, a managed care contract, or even a home security monitoring contract. Sometimes, one has no choice but to assume the risk and sign the contract. If at all possible, one should strive to sign such clauses in a corporate capacity and not in an individual capacity. If that is not possible, then seek insurance to minimize the risk. Indemnification clauses and the potential unlimited risk that they pose is one reason why the professional should undertake a carefully planned asset protection program.

***

***

OTHER FACTORS AND CLAUSES

[A] Integration

As a general rule, once parties have seen fit to put their agreement in writing, then no prior oral agreement regarding the same subject is binding. A paragraph stating that the written agreement contains the entire understanding of the parties simply reflects this rule of contract construction. Such a paragraph also places the parties on notice that any oral representation of the other party that has not been placed in the contract will be worthless.

[B] Construction

At times a court may hold any ambiguities in a contract against the party that prepared the agreement or that had the agreement prepared for them. If the party on the other side of the contract is an individual that was not represented by counsel and especially if that party has had very little business experience (such as a physician or medical provider recently in practice), courts are much more likely to hold ambiguities against the drafter of the agreement.

A paragraph regarding the construction of the agreement and stating that the agreement was formed from negotiation (as opposed to a “take-it-or-leave-it” proposition) can identify for any court constructing the contract that the court should not hold any ambiguities against the drafter. After all, even with negotiated contracts, one party or the other draws up the agreement.

[C] Choice of Law

In the United States today, it is common for parties in different states to have business dealings with each other. Likewise, in the sale of a medical practice, the buyer may begin negotiations in one state and then move to the practice state after consummation of the sale. In a similar vein, following the sale the buyer may move to another state.

In most cases, the various state laws should be similar on the contractual issues involved in the sale of a medical practice. However, a statement in the contract identifying the state whose laws will govern the contract will eliminate one possible source of dispute involving a side issue to the contract. In the vast majority of contracts, the laws of the state where the practice is physically located should be chosen by the parties to govern the contract

[D] Choice of Venue

Just like providing for choice of law, a side issue to the contract can be eliminated by choosing ahead of time the venue to resolve any conflicts that may arise. The venue is simply the place where the conflict will be decided. In most cases, the parties should choose the trial court of the county in which the practice is located.

[E] Survival of Obligations

An agreement to purchase a medical practice contains two aspects. First is the transference of the practice assets in exchange for the purchase price. Second are the various other terms, such as preservation of the medical records. By providing that these obligations survive the closing, each party is assured that the other party will not claim that the actual closing of the agreement extinguished the rights of the parties under the agreement.

[F] No Waiver Clause

A provision providing that a party does not waive its rights unless such a waiver is committed to writing allows a party to be a “nice guy” without risking its future rights. In some instances, if a party does not insist upon full compliance by the other party, then the first party may be considered to have waived its rights and may have no recourse against the other party.

There may be instances when the forbearance to exercise a right under the contract will benefit both parties. For example, if the buyer cannot pay the seller an installment on time, the seller may agree to extend the time for payment of that installment. The no waiver clause allows the seller to refuse to extend the time for payment of a future installment. Without the clause the buyer might be able to argue that the seller had waived its future rights to timely payments.

[G] Notices

There may be various reasons under the contract why one party may need to give a notice to the other party. Most often such notice will be that a party is claiming that the other is in breach of some provision of the agreement.

By specifying the address and method of delivery of any notice, the sending party can be assured that a court will rule that the receiver had actual or constructive notice.

Such a provision should also provide that one type of notice would be a change of address. Such a change of address notification would then supersede the address delineated in the agreement.

In most cases, the agreement should provide that the counsel to the party would receive a copy of any notice. This accomplishes two goals. First, there is a greater likelihood that the receiving party would receive actual notice. If the receiving party had moved and had failed to provide notice of the change of address, then the party’s counsel would have received the notice. Secondly, the party’s counsel would have received the notice in a timely manner and could take any immediate action that may be necessary.

[H] Severability Clause

A severability clause helps to ensure that if one provision is held by a court to be illegal or unenforceable, then the offending clause will be stricken from the agreement and the parties will be held to the agreement without the clause.

Without a severability clause, if a court finds that one provision of the agreement illegal or unenforceable, then the court has the power to strike down the entire agreement. Although even with a severability clause a court could strike down the entire agreement, the severability clause tells the court that the intent of the parties was that only the offending clause be stricken and essentially asks the court to honor the parties’ intent.

[I] Further Assurances Clause

After execution of the agreement, the parties may discover that certain other documents are necessary to complete the transaction. Unless such documents materially change the meaning and purpose of the agreement, a further assurance clause requires the party of parties to execute and deliver the document.

***

***

CLOSING – SETTLEMENT

The closing or settlement date should be chosen for a mutually time and place. Generally the date will be between 30 and 90 days from the execution of the agreement. This will allow the buyer and the seller adequate time to complete any conditions precedent to closing. At closing, the buyer will tender to the seller the agreed upon funds and will execute any loan and security agreements required under the purchase and sale agreement. If the restrictive covenant also contains a buyer’s covenant, then the buyer will execute that document. The seller will deliver to the buyer a bill of sale for the assets of the practice, will execute the restrictive covenant, will deliver the keys to the practice, and will surrender the assets and the premises to the buyer. Both the buyer and the seller will execute the lease assignment.

Many of the provisions of the agreement will survive the closing. This includes any agreement to prorate expenses not allocated in at the closing, the restrictive covenant agreement, the indemnifications, and any seller’s right maintained in the medical records.

TRANSITION

Both the seller and the buyer have certain interests to protect after the closing which would require the seller to stay with the practice for a period of time following the closing. The seller may have ongoing treatment plans with certain patients (such as post-operative follow-up treatment). The agreement should specify that the seller be allowed to continue at the practice location for the purpose of finishing such treatment plans. Although the buyer may be fully capable of completing such treatment plans, both the buyer and seller should be cognizant that the patient may claim abandonment. Allowing the seller to complete treatment plans in progress will mitigate against any perceived or actual claims of abandonment.

The buyer will want to require the seller to stay with the practice for a certain period of time, usually between three to six months. During that time, the seller will act to introduce the buyer to the current patients and the buyer will begin treatment of any new patients to the practice. In this way, the transition will appear smooth and natural to the current patients.

Of course, during the transition period, the seller will have the right to be paid by the buyer. To avoid misunderstanding, the method of payment should be reduced to writing. Usually the rate of compensation will be the profit margin percentage of the practice allocated to all income collected from the seller’s efforts during the time period in question. An astute negotiator might be able to require the seller to function during the transition period as an implicit condition for the payment of the practice price.

RESTRICTIVE COVENANTS

As part of the purchase price the buyer is paying for intangible assets of the practice. A medical practice is a highly individual based business. The practice depends in large part upon the reputation of the selling physician. For that reason, the buyer must ensure that the seller cannot use that highly individualized asset to compete against the practice for which she has just paid a high sum. The restrictive covenant protects this interest of the buyer.

A restrictive covenant actually contains several covenants to protect the buyer’s interests. These include not only the obvious covenant not to compete, but also a covenant regarding financial interests, a covenant regarding solicitations, and a covenant regarding proprietary information.

The first covenant is the covenant not to compete. In this covenant, the seller agrees not to compete with the practice in the geographic area during the time term of the agreement. This covenant prohibits the seller from actually practicing or from practicing indirectly. For example, the seller could not set up a clinic within the geographic area during the time period and employ a nurse practitioner to treat patients under his medical license.

The next covenant would be the covenant regarding financial interests. In this covenant, the seller is prohibited from investing in a competing business (i.e., medical practice), within the geographic area during the time period. This provision prevents the seller from investing in such a medical practice, even if he does not directly treat patients at that location.

The third covenant would be the covenant regarding solicitation. In this covenant the seller agrees not only to refrain from contacting patients of the practice during the time period, but also to refrain from contacting employees of the practice. If the seller maintains another office location which will not be sold, then the seller should ensure that the agreement provides that the seller is allowed to treat patients which find themselves to that practice location. Otherwise, the seller may be liable for patient abandonment and may also violate managed care contracts.

A final covenant would be a covenant regarding proprietary information. Simply by the fact of operating the practice, the seller has obtained certain proprietary information about the practice. This includes patient lists, accounting information, managed care contracts, and forms and handbooks. The seller should be prohibited from using such knowledge to the detriment of the practice.

[A] Time and Distance

The time and distance covered by the restrictive covenants must be reasonable. If either the time or distance is unreasonable, then a court might strike down the entire restrictive covenant.

A reasonable time is usually between two to five years. A two-year time period should be the minimum that the buyer should insist upon. The purpose of the time period is to allow sufficient time for the practice patients to consider the buyer as their “doctor” and to lose confidence in the selling doctor. For that reason, any time period over five years is likely to be considered an unreasonable restraint.

On the other hand, a reasonable distance depends upon many individual factors. A reasonable distance in an urban area like New York City would most likely be completely unreasonable in rural areas, such as rural Iowa. In most metropolitan areas, a five to ten mile radius from the practice location is likely to be considered reasonable. In rural areas, an entire county or even several contiguous counties may be considered reasonable. The main determination of the reasonableness of the distance factor is the total area from which the practice draws its patients.

Most practice management software programs allow for delineation of the practice patient base determined by zip code. That will provide the parties a starting point from which to negotiate the distance factor of the restrictive covenant.

[B] Buyer’s Covenants

The restrictive covenant should also contain buyer’s covenants, although it may seem counterintuitive that the buyer, having paid the seller tens of thousands of dollars for the practice, should be required to sign buyer’s covenants. However, a buyer’s covenant is an important part of the restrictive covenant. Under the purchase agreement, the seller might retain the right to repossess the practice, the practice assets, and the premises. This is most likely to happen when the seller finances the purchase price and the buyer defaults on the payments. It can also happen when the seller assigns the lease to the buyer and the buyer either abandons the premises or otherwise causes a default under the lease. The seller then remains liable as principle under the lease.

For those reasons, the restrictive covenant should provide that if the seller is required to enter onto the premises and take possession of the practice, then the Seller is relieved of his obligations under the restrictive covenants and the buyer now becomes bound by those same obligations. Such buyer’s covenants will prevent the buyer from abandoning the practice and then setting up a nearby competing practice.

CORPORATE RESOLUTION

Most medical practices being sold are corporate entities. If the transaction is a sale for stock, then the transaction is between private parties – the buyer paying cash and the seller transferring the stock.

However, in those cases where the buyer is purchasing the assets of the corporate practice, then the corporation must take certain prerequisite steps. Generally, a corporation, through its officers and directors, is prohibited from selling significant assets without permission of the shareholders.

For that reason, a shareholder meeting must be held and the shareholders at that meeting must approve a resolution allowing the officers and directors to sell significant assets of the corporation.

ASSESSMENT

The contract regarding the sale of a medical practice is the final agreement of the parties. Such a contract should only be executed after sufficient investigation into the practice and upon consultation with proficient professionals, including attorneys, accountants, FAs and practice management consultants. Understanding the basic terms and conditions of a contract regarding the sale of a medical practice is the first step in successfully negotiating the best agreement possible. Before one can negotiate for a certain provision, one must first be aware of the possibility of such a provision and its possible ramifications.

So, what else can FAs and consultants do to help plan properly for the sale of a medical practice, physician succession planning, and this major life liquidity event? Some experience FAs suggest constructing a “dry run template analysis” so the doctor can envision what life will be like after the sale, and what their corresponding financial needs might be. When the practice is sold, life is very different because many expenses that the practice paid become expenses the doctor now must pay. And so, the use of an astute financial advisor, practice valuation specialist, and healthcare contract attorney is highly advised.

CONCLUSION

As we have seen, the purchase price of a medical practice, although am important part of any sale, should only be considered one element of the negotiations. There are many clauses and provisions of a contract regarding the sale of the medical practice, which if not negotiated favorably should be considered factors to initiate the party to walk away from the sale.

Boundy, Charles: Business Contracts Handbook Gower Pub, NY 2010

Fenton, CF: Contracts Regarding the Sales of a Medical Practice. Financial Planning for Physicians and Healthcare Professionals; Aspen Publishers, New York, NY, 2003.

Hekman, K: Buying, Selling & Merging a Medical Practice. Keneth Hekman, New York 2008.

Walker, Lewis: The Ultimate Transition. Financial Advisor, page 33, 2014.

Schatzki, M: Negotiation Speak: Winning Words and Phrases for Sales, Purchasing, Contract and Other Business Negotiations – All the Dialogue and Skills You Need to Come Out Ahead, Dynamic Negotiations, Chicago, IL 2009.

UCC, Commercial Contracts and Business Law Blog: LexisNexis 2010.

Posted on February 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Permanent Life Insurance: A class of life insurance policies that do not expire—as long as premiums are kept current—and which combine a death benefit with a savings component. This savings portion can accumulate a cash value against which the policy owner may be able to borrow funds.

Several factors will affect the cost and availability of life insurance, including age, health and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. So, you should consider determining whether you are insurable before implementing a strategy involving life insurance.

Finally, any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

Posted on December 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

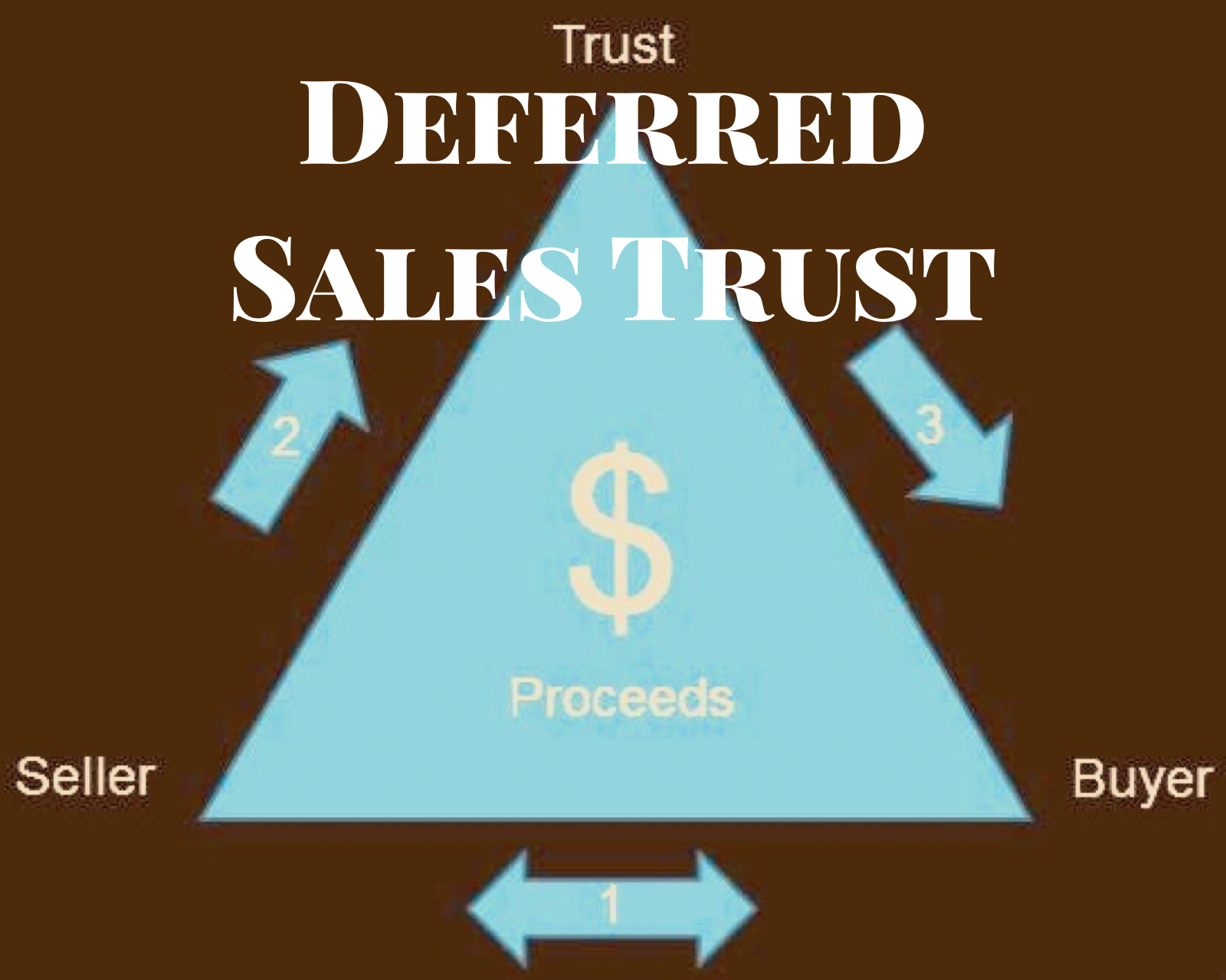

A deferred sales trust (DST) is an advanced tax strategy that allows investors to delay capital gains taxes on the sale of assets that have significantly risen in value, such as real estate or businesses. By selling the asset to a trust, the seller can receive payments over time, spreading out tax liabilities and allowing the profits to grow tax-deferred.

For example, a business owner may sell their company to a DST, avoiding a large tax bill upfront and instead receive income over multiple years. However, DSTs can be complex, and there are often fees involved in setting up and maintaining the trust.

Now, let’s point out some of the pros and cons of Deferred Sales Trusts.

One potential positive feature of using an installment sale to defer your capital gains taxes rather than a 1031 exchange is that installment sales don’t come with the same strict guidelines that govern 1031 exchanges. In particular, in light of the Tax Cuts and Jobs Act of 2017, 1031 exchanges are restricted to real property, whereas Deferred Sales Trusts and other installment sale arrangements can be used to defer capital gains for any kind of asset.

Conversely, the IRS has provided little to no guidance on how to defer taxes using an installment sale.

The basic rationale behind why you don’t receive capital gain is that you are not profiting immediately from the sale made with a Deferred Sales Trust. Given this rationale, there are various constraints on how a Deferred Sales Trust must be organized so that no capital gains taxes are in fact realized.

The third party to whom you transfer your asset generally cannot be a “related person” to you, such as a family member or a corporation in which you hold an interest. Except in special circumstances, if you attempt to set up a Deferred Sales Trust with a related person it will be viewed as a “sham trust” made just for the purposes of avoiding capital gains taxes, and will not be protected by the provisions in Section 453.

As with the 1031 exchange, you, the seller, cannot at any point in the transfer of your asset be in constructive receipt of the proceeds from the third party’s sale of that asset. To successfully defer capital gains taxes, either the third party or the trust of which they are trustee must be the only party which receives cash in the sale of the transferred asset. This includes receipt of a bond which is payable on demand.

This has been a general, informal introduction to Deferred Sales Trusts. As always, before attempting to carry out any important financial decision, investors should consult with a qualified tax or legal advisor regarding the specifics of their situation.

Posted on December 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Freddie Mac (FHLMC-Federal Home Loan Mortgage Corporation)

Freddie Mac is a GSE [government-sponsored enterprise] established by Congress. It’s similar to Fannie Mae with a publicly owned corporate structure. (Freddie Mac’s stock (FRE) trades on the New York Stock Exchange.) These two giant GSEs increase liquidity in the U.S. mortgage market by purchasing mortgages from lenders, then typically repackaging (securitizing) the debt and reselling it to investors, helping to create a “secondary” market for mortgages.

The GSEs’ main purpose is to assure that mortgage money is available for borrowers. But they don’t lend money directly. Instead, they purchase mortgages from “primary” lenders like mortgage companies, banks, and credit unions. That allows the primary lenders to replenish their funds and lend more money to home buyers. The GSEs finance their mortgage purchases by issuing mortgage-backed securities (MBS) and other debt instruments (often referred to as agency debt, even though, technically, the GSEs aren’t government agencies). GSE debt is considered to have relatively high credit quality based on its implicit government backing, reinforced by what happened during the Financial Crisis in 2008.

Since Fannie Mae and Freddie Mac were placed into government conservatorship in September 2008, the government has pledged to support any shortfall in the balance sheets of the two GSEs. The U.S. Treasury has said it will ensure that both GSEs can maintain a positive net worth and fulfill all of their financial obligations. This statement of support lends credence to the very high credit ratings of MBS and other debt issued by Fannie and Freddie.

Collateralized Mortgage Obligations (CMOs) are a form of securitized debt derived from mortgage-backed securities. It’s a form of derivative security. Like most MBS pass-through securities, CMOs are typically backed by pools of residential mortgages and their payments. But not all investors want to receive the monthly payments of principal and interest that “plain vanilla” MBS pass-throughs offer–some prefer just the principal, some prefer just the interest, or some want payments with other particular/special characteristics.

For them, the cash flows from MBS can be pooled and structured into many classes of CMOs with different maturities and payment schedules, creating securities with very specific characteristics and behaviors. These characteristics and behaviors can vary widely. Some CMOs can offer less risk than “plain-vanilla” MBS, or can help offset other forms of risk in a diversified portfolio, but others can be much more volatile.