BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Physicians and All Web Surfers Beware!

By Staff Reporters

***

Dark Patterns are tricks used in websites and apps that make you do things that you didn’t mean to, like buying or signing up for something. The purpose of this site is to spread awareness and to shame companies that use them.

Posted on September 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

By Staff Reporters

***

***

Federal Reserve Chairman Jerome Powell just announced that the central bank [FOMC] would cut interest rates amid President Donald Trump’s attempts to reshape the Fed’s independence.

The chairman announced that the Federal Reserve would cut the interest rate by .25 points, the first time that it cut interest rates since December.

Posted on July 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

BREAKING NEWS!

***

***

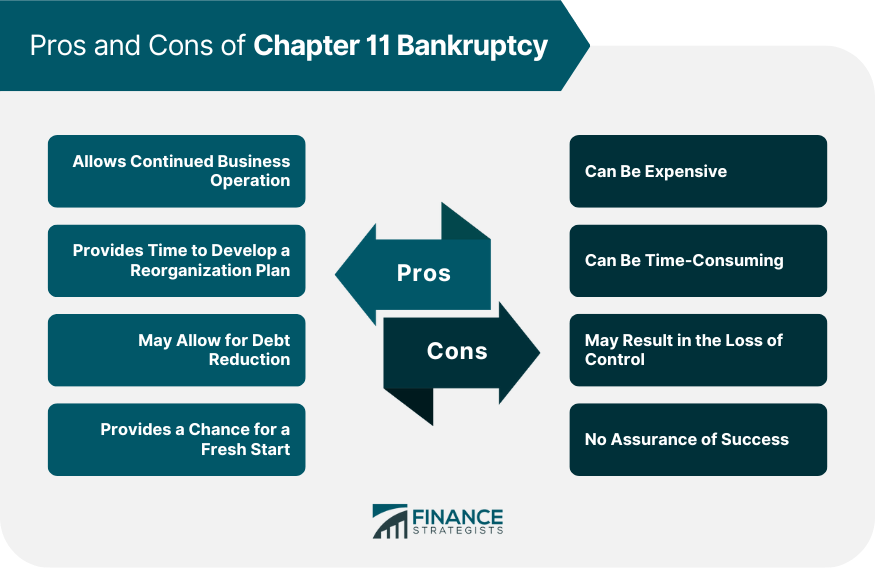

The Villages Health System, LLC, a health care provider operating in The Villages, Florida, filed for Chapter 11 bankruptcy protection on July 3rd, 2025, in the United States Bankruptcy Court for the Middle District of Florida.

“The bankruptcy petition indicates significant financial challenges, with assets estimated between $50 million and $100 million and liabilities between $100 million and $500 million. The United States of America is listed as the largest creditor with a contingent, unliquidated claim of approximately $361 million. The filing indicates that funds will be available for distribution to unsecured creditors,”

Posted on June 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

CBOE Volatility Index

***

***

There’s a lot of confidence in markets these days, and nowhere is that more apparent than in the VIX, aka the CBOE Volatility Index, aka aka the Fear Index.

According to Brew Markets, the VIX literally measures the market’s expectation of volatility based on S&P 500 index options, but it’s become a shorthand way of quantifying investors’ fear or confidence. Any time the VIX rises above 30, it’s taken as a sign of some serious trepidation in the market—but anytime it falls below 20, the market is calm, cool, and collected.

The VIX skyrocketed to over 50 on Liberation Day as investors fretted over what tariffs meant for their portfolios, but it’s been gradually falling ever since. As the chart above shows, the VIX just fell below its key support level of 17—a mark it has failed to break below recently, and a move that underlines investors’ confidence that the good times will keep rolling.

Posted on June 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

NEWS UPDATE!

***

***

On June 10th, Bobby Mukkamala was inaugurated as the 180th president of the American Medical Association (AMA).

An otolaryngologist from Flint, Michigan, Mukkamal chairs the organization’s substance use and pain care task force, won the AMA Foundation’s Excellence in Medicine Leadership Award last June, and served on the AMA board of trustees in 2017 and 2021.

Posted on June 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

***

***

Markets: Brace for +/- volatility as US markets reopen this morning, with the escalating Israel–Iran conflict dominating investors’ Bloomberg Terminals.

Stocks fell the most in nearly a month on Friday, and the prospect of an oil supply shock sent crude prices 7% higher, their biggest one-day gain in years. Through it all, the S&P 500 is less than 3% from its record high.

Combined, both the DOW and NASDAQ are up over 750 points, today!

Posted on June 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

BREAKING NEWS

***

***

Job growth is slowing, but still bigger than expected

US employers added 139,000 jobs last month, government data released yesterday shows—that’s less than the down-wardly revised 147,000 new jobs that were added in April, but more than economists had predicted. Meanwhile, the unemployment rate held steady.

Overall, the highly anticipated jobs report reflects employers growing more cautious in the face of the economic uncertainty brought on by the trade war, but so far, there doesn’t seem to be a steep drop off in the labor market. That could give the Fed reason to stay in wait-and-see mode on interest rates, though President Trump still used the occasion to urge Jerome Powell to cut rates “a full point” on Truth Social.

50% tariffs on steel and aluminum went into effect today. To celebrate, President Trump hopped on Truth Social to put China’s President Xi on blast ahead of an expected call between the two heads of state. And, Temu lost 58% of its daily users thanks to tariffs.

The president also pushed Jerome Powell to “LOWER THE RATE” following terrible private sector job numbers. Stocks are seemingly immune to tough trade talk and interest rate rants at this point, but bond yields sank on fears of slower economic growth.

The US dollar slipped, propelling gold higher as investors sought safety.

Posted on June 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

Stanley Fischer, one of the most influential economists of recent decades, has died. He was 81. His death was confirmed by the WSJ and Bank of Israel, where he served as governor from 2005 to 2013.

Fischer served as vice chairman of the Federal Reserve from 2014 to 2017. He left his biggest mark in prior decades, as professor of economics at the Massachusetts Institute of Technology, second in command at the International Monetary Fund, and at the Bank of Israel. In those roles, Fischer helped shape how an entire generation of central bankers and economic policymakers do their jobs.

Fischer was born in 1943 in Northern Rhodesia (now the independent country of Zambia) and first came to the U.S. in 1966 to get a Ph.D. at MIT.

After several years at the University of Chicago, he joined the faculty of MIT.

Robert Jarvik, who developed the first artificial heart to be permanently implanted in a human — a breakthrough that captured the world’s imagination even as it triggered debates about medical ethics — died May 26th at his home in Manhattan, NY. He was 79.

Markets started the day down yesterday but regained lost ground throughout the afternoon as investors decided that any day with no new tariff announcements is a good day.

Be advised: Fed Chair Jerome Powell warned that “supply shocks” pose a challenge for the economy, and that interest rates may need to remain higher for longer. Meanwhile, JPMorgan Chase CEO Jamie Dimon said a recession is still on the table.

Oil took a tumble on comments by President Trump that the US is nearing a deal with Iran over its nuclear program that could lift sanctions against the country.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on May 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

BREAKING NEWS

***

***

UnitedHealth Group just announced the exit of CEO Andrew Witty and suspended its 2025 forecast due to surging medical costs, sending its shares down more than 10%. Chairman Stephen Hemsley will become CEO, effective immediately.

The fourth-largest U.S company big revenue in 2024, Minnetonka-based UnitedHealth has experienced a turbulent year that saw the shock killing of United Healthcare CEO Brian Thompson in New York City, and a cyberattack that affecting an estimated 190 million people and cost the company an estimated $3.1 billion dollars.

Posted on May 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The DOJ wants Google to break up its advertising empire

Following a federal court’s ruling that Google operates an illegal ad-tech monopoly, the Justice Department requested that the company be forced to sell two major products—its Ad Exchange and a management platform—as an appropriate remedy.

Google, unsurprisingly, asked the judge for a less drastic remedy that would see the company make certain changes to its practices without having to break up its ad business. The judge won’t rule until the remedies trial starts in September.

Until then, Google has another thing to dread:

The government also wants the tech giant to sell Chrome to remedy its other monopoly (in search).

Former Supreme Court Justice of the United States, David Souter, the intellectual from New England who disappointed Republicans and delighted liberals by slowing a conservative transformation of the high court, died May 8th at his home in New Hampshire. He was 85 years old.

The high court announced his death but did not cite a cause.

President Trump tapped best-selling author and wellness influencer Dr. Casey Means, whom he described as having “impeccable ‘MAHA’ credentials,” to be Surgeon General

His first nominee, Fox News contributor Dr. Janette Nesheiwat withdrew over questions about her medical training.

Posted on May 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

As of 1998, May 8th was designated as National Student Nurses Day, to be celebrated annually. And as of 2003, National School Nurse Day is celebrated on the Wednesday within National Nurses Week (May 6-12) each year.

***

***

The nursing profession has been supported and promoted by the American Nurses Association (ANA) since 1896. Each of ANA’s state and territorial nurses associations promotes the nursing profession at the state and regional levels. Each conducts celebrations on these dates to recognize the contributions that nurses and nursing make to the community.

The ANA supports and encourages National Nurses Week recognition programs through the state and district nurses associations, other specialty nursing organizations, educational facilities, and independent health care companies and institutions.

Posted on May 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

According to the Washington Post, legendary investor Warren Buffett said Saturday that he plans to step down from his role leading Berkshire Hathaway. Warren, 94, serves as the conglomerate’s chairman and chief executive. He said Saturday that he will recommend to the Berkshire Hathaway board that Greg Abel become CEO at the end of 2025.

“I think the time has arrived where Greg should become the chief executive officer of the company at year end,” Buffett said at Berkshire Hathaway’s annual meeting in Omaha.

Abel is chairman and CEO of Berkshire Hathaway Energy. Buffett has previously signaled that Abel would be in line to succeed him as CEO.

***

UPDATE: Berkshire Hathaway (NYSE:BRK.A)(NYSE:BRK.B) on Saturday reported its worst drop in quarterly operating earnings since 2020, and noted “considerable uncertainty” around international trade policies and tariffs.

The sprawling conglomerate’s Q1 operating earnings slipped 14.1% Y/Y to $9.64B. This was the steepest fall in operating earnings since a 32.1% decrease logged in the third quarter of 2020

Posted on April 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

Artificial Intelligence Enhanced

***

***

Markets drop as tariff concerns shake the market

Key takeaways (1:30 EST)

The Dow Jones Industrial Average experienced a significant drop of more than 1,100 points, reflecting investor anxiety over tariff policies finance. The S&P was down 150 and the NASDAQ was down 550.

This decline is part of a broader trend affecting the S&P 500 and NASDAQ, as geopolitical tensions and economic uncertainties weigh heavily on market sentiment finance.yahoo.com .

Investors are closely monitoring developments regarding trade policies and their potential impact on the economy, leading to heightened volatility in the stock market

Posted on April 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING US STOCK MARKET NEWS

By ME-P Staff Reporters

***

***

Stocks in the U.S. opened sharply lower on Friday, extending a slide from the previous trading session triggered by President Trump’s announcement of sweeping new tariffs on U.S. imports earlier this week.

The S&P 500 fell 144 points, or 2.5%, to 5,252 as of 9:34 a.m. EST. The Dow Jones Industrial Average tumbled 1,006 points, or 2.5%, and the NASDAQ Composite slid 3.1%.

The indexes’ free-fall Thursday was their biggest one-day drop since 2020, with more than $2 trillion in investor wealth erased from the S&P 500. The S&P 500 and Dow each sank more than 4% yesterday, while the tech-heavy NASDAQ plunged nearly 6%.

NOTE: Drops of this magnitude aren’t unheard of on Wall Street, but they’re rare. Over the last 25 years, the S&P 500 has fallen 4% in a single day 38 times, according to Adam Turnquist, chief technical strategist for brokerage firm LPL Financial.

The genetic testing company 23andMe went from biotech superstar to the brink of collapse. And, its most valuable asset might be its controversial customer DNA data trove.

Now, 23andMe filed for bankruptcy late Sunday night and announced the resignation of its chief executive officer Anne Wojcicki who is stepping down from her position but remains on the board of directors.

Wojcicki has so far tried unsuccessfully to rescue the business by buying it back and capping a precipitous fall for the DNA-testing company.

Posted on March 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

***

***

The Federal Reserve just opted to hold interest rates steady as officials reckon with fearful markets and concerns of an economic slowdown sparked by the trade wars launched by President Donald Trump and his efforts to overhaul and dismantle government agencies.

After a two-day meeting of its monetary policy committee in Washington, D.C., the Fed announced it would hold its rate target at a range of 4.25% to 4.50%. Investors anticipated the move. The Fed’s target rate remains a full percentage point lower than it was when the Fed pivoted to cutting rates last September.

Posted on March 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

US stocks plunged on Monday as investors processed growing concerns about the health of the US economy after President Trump and his top economic officials acknowledged the possibility of a potential rough patch.

The Dow Jones Industrial Average (^DJI) fell nearly 900 points, or over 2%, while the benchmark S&P 500 (^GSPC) dropped around 2.7% after the index posted its worst week since September.

The tech-heavy NASDAQ Composite (^IXIC) fell 4% in its worst day since 2022, as the “Magnificent Seven” stocks led the sell-off. Tesla’s (TSLA) rout continued, plunging 15% and officially wiping out the gains it had made in the wake of Trump’s election win. Nvidia (NVDA), Apple (AAPL), Google parent Alphabet (GOOG), and Meta (META) all each lost more than 4%.

Posted on March 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

AGREE or DISAGREE?

By Staff Reporters

***

***

US Treasury Secretary Scott Bessent made waves yesterday with his comment that the American economy is facing a “detox period.”

Should we be seeing that this economy that we inherited [is] starting to roll a bit? Sure. And look, there’s going to be a natural adjustment as we move away from public spending to private spending. The market and the economy have just become hooked, and we’ve become addicted to this government spending, and there’s going to be a detox period. There’s going to be a detox” .

Bessent, a former hedge-fund manager, said during a CNBC interview.

“Employment should be from private companies, not from government. And I’m confident, if we have the right policies, it will be a very smooth transition.”

Bessent said, in an apparent reference to the layoffs of federal workers executed in large part by the entity known as the Department of Government Efficiency, which is run by Trump adviser Elon Musk.

Posted on February 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

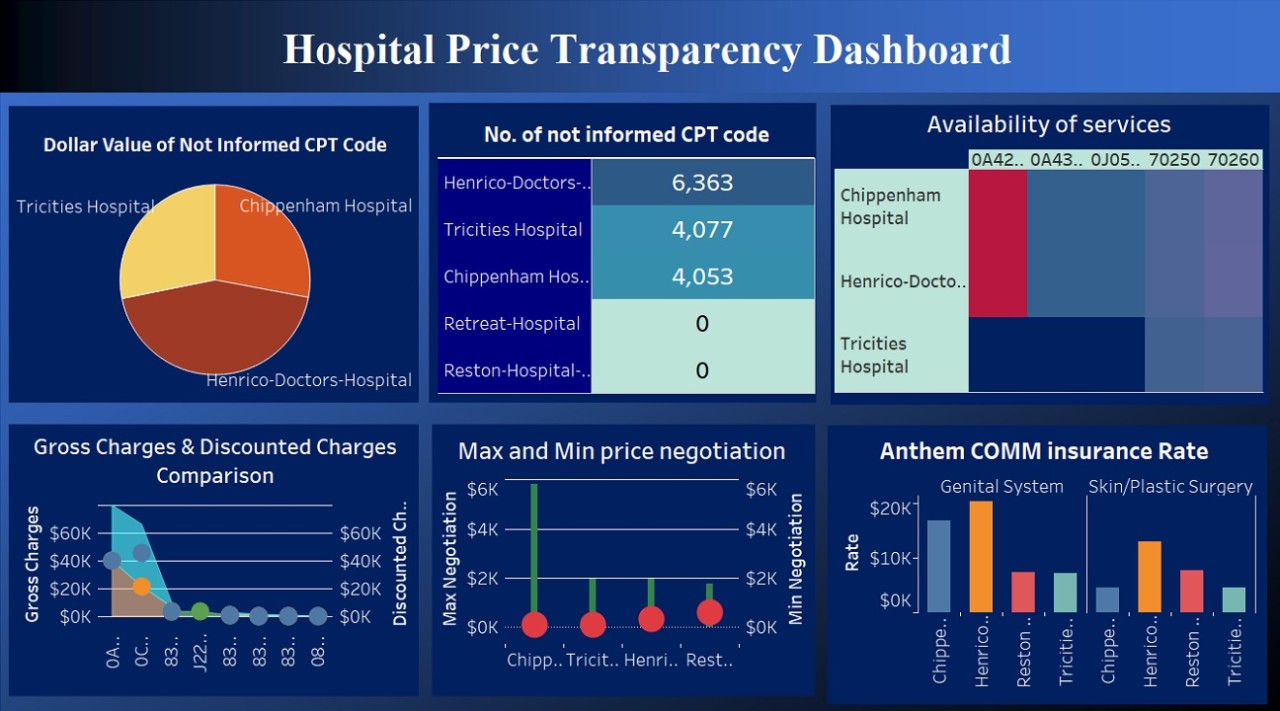

WASHINGTON, Feb 25 (Reuters) – U.S. President Donald Trump signed an executive order on Tuesday aiming to improve price transparency on healthcare costs by directing federal agencies to strictly enforce a 2019 order he signed during his first term.

The order directs the Departments of the Treasury, Labor, and Health and Human Services to within 90 days come up with a framework to enforce Trump’s 2019 executive order forcing health insurers and hospitals to disclose healthcare cost details.

***

***

This includes requiring the disclosure of actual prices not estimates, update existing guidance or proposing new regulations that ensure price information is standardized, and updating or issuing enforcement policies that guarantee compliance.

“You’re not allowed to even talk about it when you’re going to a hospital or see a doctor. And this allows you to go out and talk about it,” Trump told reporters as he signed the order. “It’s been unpopular in some circles because people make less money, but it’s great for the patient.”

Posted on February 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

UPDATE

By PayPal and Staff Reporters

***

***

NOTE: Information provided by PayPal is not intended to be and should not be construed as tax advice. For questions about your specific tax situation, please consult a tax professional.

Payment processors, including PayPal, are required to provide information to the US Internal Revenue Service (IRS) about customers who receive payments for the sale of goods and services above the reporting threshold in a calendar year.

Will I have to pay taxes when sending and receiving money on PayPal – what exactly is changing?

The Internal Revenue Service (IRS) announced transitional reporting requirements for payments received for goods and services. These requirements will lower the Form 1099-K reporting threshold over a 3-year period from the previous threshold of more than $20,000 in goods and services transactions and more than 200 goods and services transactions in a calendar year. We’ve summarized the IRS thresholds for Form 1099-K below.

Posted on February 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. Stock Markets will be closed for Presidents Day. But crypto trading takes no days off.

The Presidents Day holiday was originally intended to celebrate the birthday of the first President George Washington on February 22nd, according to the Library of Congress. The holiday is still formally designated as Washington’s Birthday by the Office of Personnel Management. Washington’s birthday was an informal holiday during the country’s early existence and President Rutherford B. Hayes formalized the holiday in 1879, according to History.com. The holiday’s proximity to the birthday of President Abraham Lincoln on February 12th caused the general public to link the two and later expand the celebration to all presidents.

***

Berkshire Hathaway, the investment conglomerate led by Warren Buffett, reduced its holdings in two US banks. Bank of America (BoA) and Citigroup shares were sold in the final quarter of 2024. The move, disclosed in a regulatory filing last Friday, comes as Buffett continues to trim Berkshire’s stock portfolio, favoring safer investments such as US Treasury bills.

***

Wall Street just dumped nearly every dollar of the $12.5 billion in loans that helped Elon Musk buy Twitter—now called X—in 2022. A group of seven major banks, led by Morgan Stanley, offloaded $4.74 billion of the debt last Friday, selling more than their planned $3 billion as investors flooded in with $12 billion in orders, according to a report from the Financial Times.

Posted on February 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Confirmed as US Health Secretary

BREAKING NEWS

***

The Senate just confirmed Robert F. Kennedy Jr. as President Trump’s US health secretary, putting the prominent vaccine skeptic in control of $1.7 trillion in federal spending, vaccine recommendations and food safety as well as health insurance programs for roughly half the country.

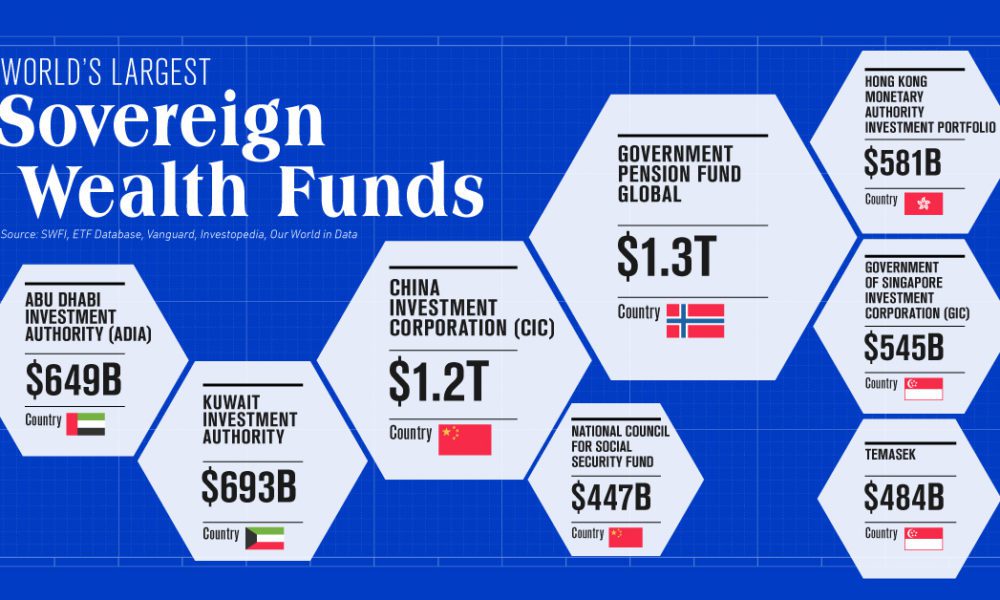

A Sovereign Wealth Fund (SWF) is a large pool of capital managed by a country’s government to achieve specific economic and social goals. These funds are invested in various assets such as stocks, bonds, real estate, commodities, and other financial instruments.

SWFs are typically funded from the savings of state-owned enterprises, foreign currency reserves from central banks, or commodity exports. The size and composition of each SWF can vary significantly between countries based on their respective economic circumstances. Each country has various reasons for setting up an SWF. However, the most common purpose of establishing one is to diversify and protect a country’s economy. For instance, this fund can be used as emergency reserves for potential future global financial shocks.

Purpose of a Sovereign Wealth Fund

Sovereign wealth funds invest a country’s wealth to achieve the government’s economic and social objectives. These funds provide countries with an additional method to diversify their economies and reduce risk exposure. They also give governments a chance to invest in global markets outside their own countries, which can get them better returns on their investments. This increases the earning potential on foreign exchanges and provides additional economic stability.

Furthermore, SWFs are a valuable tool to help countries build up buffers and savings for future generations to be better prepared for future economic shocks. Proper use of SWFs leads to long-term economic growth and stability.

In addition to providing an alternative form of investment for governments and enterprises worldwide, SWFs have also been used to increase financial transparency and accountability in many countries. By making their investment decisions public, these funds help promote corporate governance standards across the globe. This encourages market stability and reduces risks associated with certain types of investments.

Posted on February 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

UnitedHealthcare has agreed to a $2.5 million settlement in response to a class action lawsuit accusing the company of making unauthorized telemarketing calls. More than 12,000 individuals may be entitled to compensation, with payouts ranging from $350 to $1,000 per person, depending on how many claims are filed.

The lawsuit, filed under the Telephone Consumer Protection Act (TCPA), alleges that UnitedHealthcare placed calls to individuals without their consent between January 9, 2015, and January 9th, 2019. If you received these calls, you could be eligible for a cash settlement—but you must act before April 15th, 2025.

PALM BEACH, Fla. (AP) — President Donald Trump has fired the director of the Consumer Financial Protection Bureau, Rohit Chopra, in the latest purge of a Biden administration holdover. Chopra was one of the more important regulators from the previous Democratic administration who was still on the job since Trump took office on Jan. 20th.

A 2020 STAT analysis found more than two-thirds of Congress receiving a check from pharmaceutical companies that year. More recent data from Open Secrets likewise confirms that a large majority of leaders serving in the U.S. Congress and Senate receive significant contributions from pharmaceutical or health products companies, averaging $45,000 and $47,000 for Republicans and Democrats in the House of Representatives, respectively — and $50,000 and $69,000 for Republicans and Democrats in the Senate.

Posted on January 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

WASHINGTON: 8:15 am: The President Joe Biden administration just preemptively pardoned Anthony Fauci, MD.

“Our nation relies on dedicated, selfless public servants every day. They are the lifeblood of our democracy,” Biden said in a statement just hours before President-elect Donald Trump is sworn into office.

“The issuance of these pardons should not be mistaken as an acknowledgment that any individual engaged in any wrongdoing, nor should acceptance be misconstrued as an admission of guilt for any offense,” Biden said in a statement.

Posted on January 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

By Staff Reporters

***

***

Sorry, TikTok isn’t available right now

A law banning TikTok has been enacted in the U.S. Unfortunately, that means you can’t use TikTok for now.

We are fortunate that President Trump has indicated that he will work with us on a solution to reinstate TikTok once he takes office. Please stay tuned!

In the meantime, you can still log in to download your data.

Posted on January 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

China’s 10-year bond yield plunged to a record low this month, while the Chinese currency [yuan] traded in Hong Kong on Wednesday hit its weakest against the U.S. dollar in more than a year.

The People’s Bank of China is “trying to cool down the market by suspending government bond buying,” said Larry Hu, chief China economist at Macquarie.

And, the U.S. economy added a much larger-than-expected total of new hires last month, adding more upward pressure to wage inflation and likely stoking a further selloff in U.S. Treasury bonds.

The Bureau of Labor Statistics said 256,000 new jobs were created last month, well ahead Wall Street’s 164,000 forecast and the down-wardly revised 212,000 reading from November.

***

Finally, Wall Street’s major averages are tumbling today as investors digested the hotter than expected jobs report. Early on and the S&P 500 (SP500) was -1.7%, the NASDAQ Composite (COMP:IND) was -2.2%, and the Dow (DJI) was -1.3%.

Posted on January 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

By Staff Reporters

***

***

TORONTO—Canadian Prime Minister Justin Trudeau just announced that he will resign after almost a decade in power, bowing to members of his party who have been calling on him to step aside ahead of an election later this year.

“It has become clear to me that if I’m having to fight internal battles, I cannot be the best option in that election,” said Trudeau in an announcement from the country’s capital, Ottawa.

LAS VEGAS (AP) — A vehicle caught fire and exploded Wednesday outside the lobby of President-elect Donald Trump’s hotel in Las Vegas, authorities said.

Las Vegas police said they are investigating the fire and explosion, but neither they nor the Clark County Fire Department immediately provided more details. A county spokeswoman said in a statement that the fire was in the hotel’s valet area and was reported at 8:40 a.m.

At least 10 people are dead and 35 injured after a man drove a pickup truck into a large crowd on New Orleans’ Bourbon and Canal streets early New Year’s Day, officials said. The suspect is dead. President Biden has been notified.

In an early Wednesday press conference, New Orleans Police Department (NOPD) chief Anne Kirkpatrick said a man drove a pickup truck down Bourbon Street with “clear intent.”

“He was hell bent on creating the carnage and the damage he did,” Kirkpatrick said, adding that two NOPD officers are among those injured.

The man drove down Bourbon Street “at a very fast pace,” indicating “very intentional behavior [and] trying to run over as many people as he possibly could,” Kirkpatrick said.

At least one improvised explosive device was found on the scene, said FBI New Orleans special agent-in-charge Alethea Duncan, and officials are “working on confirming if this was a viable device or not.”

The FBI is taking over the investigation, officials said.

More updates are expected from NOPD headquarters at 11 a.m. and 3 p.m. local time.

Posted on December 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

Former President Jimmy Carter has died at the age of 100.

The 39th president of the United States was a Georgia peanut farmer who sought to restore trust in government when he assumed the presidency in 1977 and then built a reputation for tireless work as a humanitarian.

The Federal Reserve cut interest rates by a quarter of a percentage point just now, delivering relief for borrowers at the central bank’s last meeting before President-elect Donald Trump takes office next month. The central bank predicted fewer rate cuts next year than it had previously indicated, however, suggesting concern that inflation may prove more difficult to bring under control than policymakers thought just a few months ago.

The move marked the third consecutive interest rate cut since the Fed opted to start dialing back its fight against inflation in the fall. The FOMC has lowered interest rates by a percentage point in recent months.

However, the Fed’s forecast said it anticipates only a half a percentage point of rate cuts next year and another half-percent cut in 2026.

Posted on December 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

BREAKING NEWS!

***

***

The internet web page listing the corporate leadership team behind Anthem Blue Cross Blue Shield (BCBS), one of America’s biggest health insurers, has disappeared from the company’s website.

The disappearance of the page listing the provider’s 25 highest-ranking employees was highlighted in a post shared to the r/antiwork subreddit on Reddit by the user u/wendysdriv

Posted on December 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

“Rest-in-Peace”

Dr. Kelly Powers, a podiatric surgeon and Fox News medical contributor, died Sunday from a remission of brain cancer. She was 45. A a regular commentator on Fox News and Fox Business Network, Powers survived heart failure—symptoms of which she experienced on air while covering that very topic. “It’s crazy–I went into heart failure while doing a report on Fox Business–live–on heart health and talking about the subtle signs that women often miss.

You can’t make this up,” she toldPreferred Health Magazine after she had also faced a bout with glioblastoma, which was detected in 2020. After several surgeries, Powers underwent chemotherapy and radiation, and eventually recovered. During that time, she became pregnant and had her now three-year-old son. That cancer returned this year, however. “She was a brave and beautiful soul who could make friends anywhere she went,” an obituary reads. “Kelly had a love for people and she was dedicated to helping others.”

Powers leaves behind her husband, Steven Doll, and son Bennett.

Posted on December 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

How to Do it Like a Pro

Need help getting the best online deals on You may with these shopping tips for our ME-P readers and subscribers, and you’ll be ready for the biggest traditional online shopping day of the year.

Best of all, you can learn a few fun facts along the way!

Assessment

When you’ve learned everything you need to know, be sure to bookmark this Cyber Monday page and come back next year to again save on the best holiday gifts in 2025.

PLEASE SUBSCRIBE, LIKE AND REFER

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on December 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

By Staff Reporters

***

President Joe Biden has just pardoned his son, Hunter Biden, who was convicted on federal gun charges and was due for sentencing in December, 2023.

Despite the White House’s assurances last month that the president had no intentions of pardoning his son, the announcement came through on Sunday evening that he had pardoned him.

Posted on November 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

CLOSINGS TODAY ON THANKSGIVING2024

By Staff Reporters

***

***

United States stock markets will be closed on Thursday, November 28th and will close early on Friday, November 29th in observance of the Thanksgiving Holiday.

The NASDAQ and NYSE will both be closed on Thanksgiving and will open on November 29th, but close early at 1 p.m. ET. The U.S. bond market will also be closed on Thursday and are scheduled to close at 2 p.m. ET on Friday, according to the The Securities Industry and Financial Markets Association (SIFMA)..

After closing for the Thanksgiving holiday, and closing early on Black Friday, it will be business as usual on Wall Street until late December. The next scheduled stock market closure is on Wednesday, December 25th in observance of Christmas. Markets are also scheduled to close early on Christmas Eve

Posted on November 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The S&P 500 and NASDAQ stayed in the green all day, with the S&P 500 hitting yet another new all-time high, while the Dow clawed its way out of negative territory to reach a new high as well.

The minutes from the last Federal Reserve meeting revealed that central bankers feel rate cuts are still warranted, though they’ll need to be gradual. Treasuryyields rose on the news.

Bitcoin continues to fall further away from the promised land of $100,000 as traders begin logging off ahead of the holiday—though bulls believe this is just a pullback to gather momentum ahead of the final push.

Posted on November 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. Bertalan Meskó, MD PhD

***

***

Regarding AI, the emphasis will shift away from the regulatory environment towards technology companies making their own decisions. Trump also promised to repeal Biden’s executive order on AI because it “hinders AI Innovation”.

Regarding health care, Trump said he would let Robert F. Kennedy “go wild” on health. Being a vaccine doubter and having made many unscientific claims about health, this could be a huge risk to digital health and the FDA’s job on regulating technologies. READ MORE

Posted on November 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Spirit Airlines said Monday it has filed for Chapter 11 bankruptcy protection after struggling with losses, growing debt and a failed merger during the post-pandemic travel lull. The company said in a stock market statement that it had secured a prearranged deal with bondholders that includes £300 million in financing to keep it afloat, with the business planning to end its bankruptcy in the first quarter of 2025.

Analysts are expectingNvidia, the world’s largest publicly traded company, to show quarterly sales of ~$33 billion, up 10% from the previous quarter and 83% year over year, but they also warn the mind-blowing growth of the chip maker could begin to slow.

Posted on November 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

November 13th, 2024

***

***

World Kindness Day is an international holiday first introduced in 1998 by the World Kindness Movement.

The holiday is devoted to promoting kindness throughout the world, understanding the positive potential of large and small acts of kindness, and unifying together as human beings.

Stocks just roared out of the gate this Wednesday morning following news that former President Donald Trump has secured a second term in the White House and Republicans won a majority in the Senate.

The Dow Jones Industrial Average rose 1,341 points, or about 3.1 percent, as the market opened, reaching a record high. It was the first time it has jumped more than 1,000 points in a single day since November 2022.

The S&P 500 also gained 1.9 percent, and the NASDAQ climbed 1.8 percent.

Despite concern from big business about Trump’s plan to impose blanket tariffs on imports to the U.S., Wall Street is anticipating tax cuts and deregulation during a second Trump presidency.