By Dr. David Edward Marcinko; MBA MEd

SPONSOR: http://www.CertifiedMedicalPlanner.org

***

***

Bankruptcy in the healthcare sector unfolds under conditions unlike those in any other industry. Hospitals, physician groups, long‑term care facilities, and other providers operate within a system where financial distress does not simply threaten shareholders or creditors—it threatens patient access, community health, and sometimes regional stability. Because of this, the duration and resolution of healthcare bankruptcies tend to be longer, more intricate, and more heavily supervised than those in non‑healthcare fields. Understanding why requires examining the operational, regulatory, and ethical pressures that shape the process from start to finish.

The duration of healthcare bankruptcies is often extended because healthcare organizations cannot simply halt operations while restructuring. A manufacturing company may shut down a plant or pause production during bankruptcy, but a hospital cannot close its emergency department without risking patient harm and violating federal obligations such as the Emergency Medical Treatment and Labor Act. This requirement to maintain continuous operations forces debtors to secure emergency financing, retain staff, and preserve supply chains even while insolvent. Each of these steps adds layers of negotiation and oversight that lengthen the timeline.

Another factor extending the duration is the complexity of healthcare revenue streams. Providers rely on a mix of commercial insurance, Medicare, Medicaid, and supplemental programs, each with its own billing rules, reimbursement delays, and audit risks. When a healthcare organization files for bankruptcy, these payers may temporarily suspend payments or increase scrutiny, creating cash‑flow instability at the very moment the debtor needs liquidity. Resolving disputes with government payers—especially when overpayments or penalties are involved—can take months or years, slowing the overall process.

The presence of regulatory oversight also contributes to longer bankruptcy durations. Healthcare organizations must comply with licensing requirements, quality‑of‑care standards, and patient‑safety regulations even while restructuring. State health departments, federal agencies, and accreditation bodies may all intervene to ensure that patient care is not compromised. These agencies may require detailed operational plans, staffing assurances, or quality monitoring before approving major restructuring steps such as service reductions or facility sales. Each approval adds time and complexity.

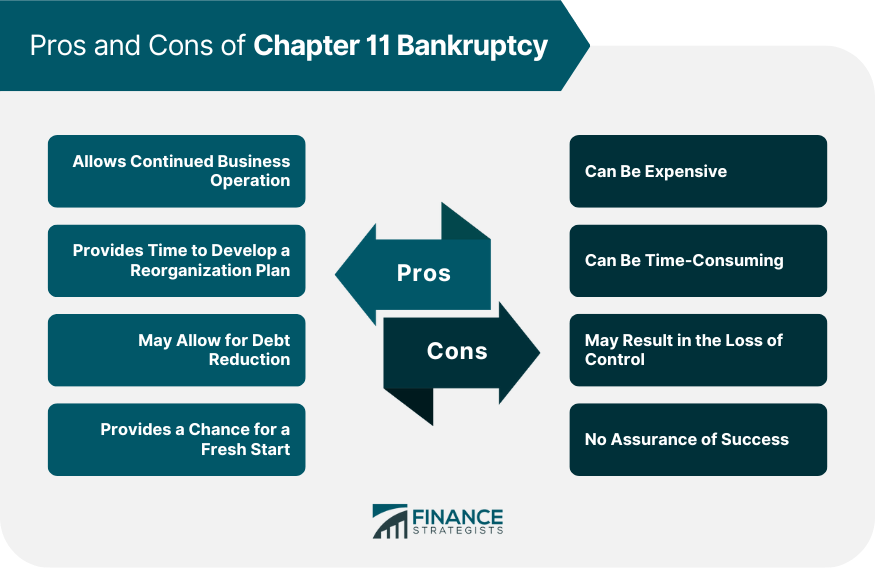

Resolution in healthcare bankruptcies is similarly shaped by the need to protect patients and communities. In many cases, the preferred resolution is a sale of the organization to a financially stronger operator. Asset sales allow continuity of care, preserve jobs, and satisfy creditors more effectively than liquidation. However, selling a healthcare facility is far more complicated than selling a typical business. Buyers must obtain licenses, secure payer contracts, and demonstrate compliance with regulatory standards. Certificate‑of‑need laws in many states require additional approvals before ownership changes or service expansions can occur. These steps can significantly delay closing timelines.

***

***

When a sale is not feasible, reorganization becomes the primary path to resolution. Reorganization plans in healthcare often involve renegotiating labor contracts, restructuring debt, consolidating services, or forming partnerships with larger health systems. Because these changes affect patient access and community health, they frequently draw scrutiny from local governments, unions, advocacy groups, and residents. Public hearings, community negotiations, and political involvement can all extend the resolution timeline.

Liquidation, while rare, presents the most challenging form of resolution. Closing a healthcare facility requires transferring patients, securing medical records, disposing of controlled substances, and ensuring continuity of care for vulnerable populations. Regulators may require detailed closure plans, and courts often appoint patient‑care ombudsmen to monitor conditions during the wind‑down. These safeguards, while essential, make liquidation slower and more expensive than in other industries.

A unique feature of healthcare bankruptcy resolution is the role of the patient‑care ombudsman. Appointed in many cases, the ombudsman monitors the quality of patient care and reports to the court. Their findings can influence decisions about financing, staffing, or operational changes. This additional layer of oversight ensures patient safety but also adds procedural steps that lengthen the process.

Another challenge is the interdependence of healthcare providers within regional networks. The bankruptcy of one hospital can strain nearby facilities, disrupt referral patterns, and destabilize physician groups. Courts and regulators may therefore consider broader system impacts when evaluating restructuring proposals. This systemic perspective, while necessary, can slow resolution as stakeholders negotiate solutions that preserve regional healthcare capacity.

***

***

Despite these complexities, healthcare bankruptcies can ultimately lead to stronger and more sustainable organizations. Successful resolutions often involve aligning financial structures with modern healthcare realities—shifting toward outpatient care, integrating technology, or partnering with larger systems. The process may be lengthy, but it can produce long‑term stability for both providers and the communities they serve.

In sum, the duration and resolution of healthcare bankruptcies are shaped by the sector’s unique obligations to patients, regulators, and communities. Continuous operations, complex revenue streams, regulatory oversight, and the ethical imperative to protect patient welfare all contribute to longer timelines and more intricate resolutions. Yet these same factors ensure that the process prioritizes continuity of care and community health, making healthcare bankruptcy not just a financial event but a public‑interest undertaking.

COMMENTS APPRECIATED

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR- http://www.MarcinkoAssociates.com

Like, Refer and Subscribe

***

Share this:

Filed under: iMBA, Inc. | Tagged: AI, artificial intelligence, bankruptcy, health, healthcare, Marcinko, Technology | Leave a comment »