BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on July 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

BREAKING NEWS!

***

***

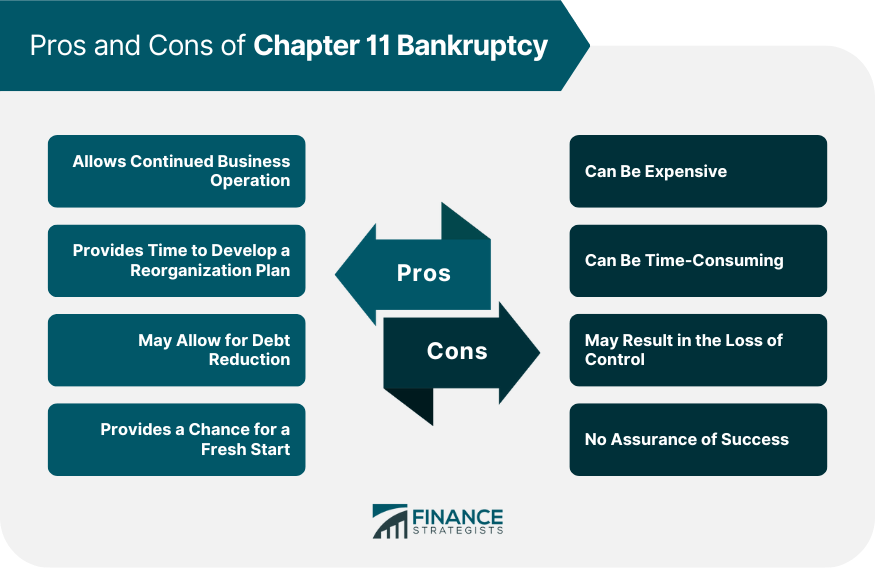

The Villages Health System, LLC, a health care provider operating in The Villages, Florida, filed for Chapter 11 bankruptcy protection on July 3rd, 2025, in the United States Bankruptcy Court for the Middle District of Florida.

“The bankruptcy petition indicates significant financial challenges, with assets estimated between $50 million and $100 million and liabilities between $100 million and $500 million. The United States of America is listed as the largest creditor with a contingent, unliquidated claim of approximately $361 million. The filing indicates that funds will be available for distribution to unsecured creditors,”

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

A recent study published in the Annals of Internal Medicine found that in 2021, UnitedHealth Group received just under $14 billion in extra Medicare Advantage payments after using a code that made its members appear sicker. It’s another tough break for the plan and provider that has faced allegations of illegally taking additional money from patients and taxpayers, especially after its CEO was fatally shot in early December.

US stocks edged higher on Monday as investors focused on tech’s temporary reprieve from President Trump’s tariffs.

The S&P 500 (^GSPC) trimmed bigger gains to rise a healthy 0.8%. The tech-heavy NASDAQ (^IXIC) also closed off its session high, up 0.6%. The Dow Jones Industrial Average (^DJI) was up around 0.7%, or more than 300 points.

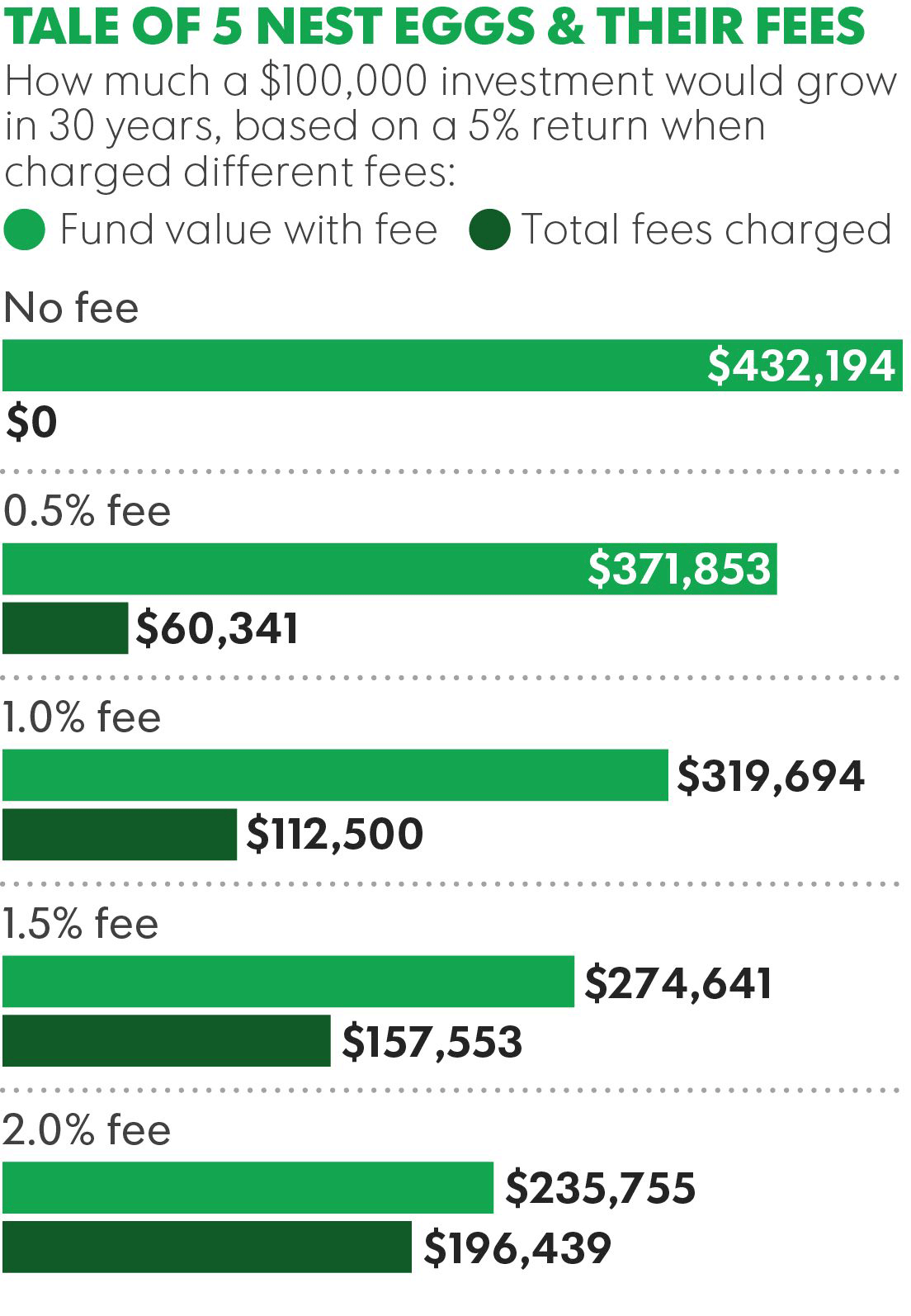

SO – HOW MUCH IS A “FINANCIAL ADVISOR” REALLY WORTH?

This blog holds a rather uncomplimentary opinion of financial advisors, and the financial services and brokerage industry as a whole; deserved, or not? The entire site hints at this attitude as well, in favor of a going it alone or ME, Inc investing when possible. Nevertheless, it is reasonable to wonder how much boost in net-returns might an educated and informed, fee transparent and honest, fiduciary focused “financial advisor” add to a clients’ investment portfolio; all things being equal [ceteris paribus].

And, can it be quantified?

Well, according to Vanguard Brokerage Services®, perhaps as much as 3%? In a decade long paper from the Valley Forge, PA based mutual fund and ETF giant, Vanguard said financial advisors can generate returns through a framework focused on five wealth management principles:

• Being an effective behavioral coach: Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value added: up to 1.50%).

• Applying an asset location strategy: The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value added: from 0% to 0.75%).

• Employing cost-effective investments: This component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value added: up to 0.45%).

• Maintaining the proper allocation through rebalancing: Over time, as investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value added: up to 0.35%).

• Implementing a spending strategy: As the retiree population grows, an advisor can help clients make important decisions about how to spend from their portfolios. (Potential value added: up to 0.70%).

Source: Financial Advisor Magazine, page 20, April 2014.

Assessment

However, Vanguard notes that while it’s possible all of these principles could add up to 3% in net returns for clients, it’s more likely to be an intermittent number than an annual one because some of the best opportunities to add value happen during extreme market lows and highs when angst or giddiness [fear and greed] can cause investors to bail on their well-thought-out investment plans.

And, is the study applicable to doctors and allied healthcare providers? Doe Vanguard have a vested interest in the topic. What about fee based versus fee-only financial advice?

Conclusion

Finally, recognize the plethora of other financial planning life-cycle topics addressed in this ME-P were not included in the Vanguard investment portfolio-only study a decade ago.

And what about today with contemporaneous internet advising, chat-rooms, linkedin, robo-advisors, reddit and the like?

Posted on January 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Credit report with score on a desk

***

Credit analysis is a form of financial analysis used primarily to determine the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s debt securities. Credit analysis is typically an important component of security analysis and selection in credit-sensitive bond sectors such as the corporate bond market and the municipal bond market.

Credit default swap index (CDX) is a credit derivative, based on a basket of CDS, which can be used to hedge credit risk or speculate on changes in credit quality.

Credit default swaps (CDS) are credit derivative contracts between two counterparties that can be used to hedge credit risk or speculate on changes in the credit quality of a corporation or government entity.

Credit quality reflects the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s securities. Common measurements of credit quality include the credit ratings provided by credit rating agencies such as Standard & Poor’s and Moody’s. Credit quality and credit quality perceptions are a key component of the daily market pricing of fixed-income securities, along with maturity, inflation expectations and interest rate levels.

Credit Rating Agency (CRA) is a company that assigns credit ratings for issuers of certain types of debt obligations as well as the debt instruments themselves. In the United States, the Securities and Exchange Commission (SEC) permits investment banks and broker-dealers to use credit ratings from “Nationally Recognized Statistical Rating Organizations” (NRSRO) for similar purposes. As of January 2012, nine organizations were designated as NRSROs, including the “Big Three” which are Standard and Poor’s, Moody’s Investor Services and Fitch Ratings.

Credit rating downgrade, by a credit rating agency (Standard & Poor’s, Moody’s or Fitch) means reducing its credit rating for a debt issuer and/or security. This is based on the agency’s evaluation, indicating, to the agency, a decline in the issuer’s financial stability, increasing the possibility of default. A downgrade should not to be confused with a default; a debt security can be downgraded without defaulting. And, conversely, a debt issuer can suddenly default without being downgraded first–credit ratings and credit rating agencies are not infallible.

Credit ratings are measurements of credit quality provided by credit rating agencies. Those provided by Standard & Poor’s typically are the most widely quoted and distributed, and range from AAA (highest quality; perceived as least likely to default) down to D (in default). Securities and issuers rated AAA to BBB are considered/perceived to be “investment-grade”; those below BBB are considered/perceived to be non-investment-grade or more speculative.

Credit risk is the inability or perceived inability of the issuers of debt securities to make interest and principal payments will cause the value of those securities to decrease. Changes in the credit ratings of debt securities could have a similar effect.

Credit Risk Transfer Securities (CRTS) are unsecured obligations of the GSEs (Government Sponsored Enterprises). Although cash flows are linked to prepays and defaults of the reference mortgage loans, the securities are unsecured loans, backed by general credit rather than by specified assets.

Today marks the anniversary of the 1941 attack on Pearl Harbor, which led to the US entering World War II

***

***

Strategically situated between the US West Coast and the Asia-Pacific region, Pearl Harbor remains an important site to the US military 83 years after the attack. Pearl Harbor is home to one of the Navy’s four public shipyards, and it’s the largest industrial employer in Hawaii (they do maintenance on nuclear submarines there).

The Navy’s other three public shipyards are located in Portsmouth, NH; Norfolk, VA; and Bremerton, WA.

Posted on November 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

In breaking news, the Biden administration is attempting to cover anti-obesity drugs for weight loss under Medicare and Medicaid. A recent study finds 137 million people are eligible for semaglutide drugs nationwide.

Another insurer can claim victory against CMS after UnitedHealthcare prevailed in its star ratings lawsuit on Friday. The feds will now have to recalculate the scores.

And ... Emory Healthcare is looking to expand value-based care for more than 350,000 patients through a population health partnership with tech company Guidehealth.

Amgen’s new drug did help patients lose up to 20% of their weight in a given year, but that wasn’t enough to impress shareholders, who kicked shares down 4.76%.

Kohl’s plummeted 17.01% after the retailer met revenue expectations but missed on earnings last quarter. It definitely doesn’t help that the CEO announced his retirement last night.

Abercrombie & Fitch’s turnaround is well underway, and the company beat earnings forecasts last quarter and projected strong holiday sales. But it still fell short of shareholder expectations, and the stock sank 5.10% today.

Best Buy rounded out retailer earnings today, dropping 4.89% after missing revenue expectations last quarter and cutting its full-year guidance.

Zoom Communications changed its name, but that wasn’t enough to save the company from a 6.31% decline today thanks to its tepid fiscal outlook.

The S&P 500® index (SPX)rose 34.26 points (0.57%) to 6,021.63; the Dow Jones Industrial Average®($DJI) added 123.74 points (0.28%) to 44,860.31; and the NASDAQ Composite®($COMP) gained 119.46 points (0.63%) to 19,174.30.

The 10-year Treasury note yield climbed four basis points to 4.3% after Trump’s tariff comments, but shorter-term yields fell after the Fed minutes, keeping the yield curve slightly out of inversion.

The CBOE Volatility Index®(VIX)dropped to 14.19, near a two-week low.

Posted on November 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Doctors, Facing Another Pay Cut, Call for Permanent Medicare Payment Reform

The Centers for Medicare and Medicaid Services (CMS) is moving forward with a 2.9% cut to physician payments in 2025 despite protest from major industry groups. CMS has finalized the calendar year 2025 Medicare Physician Fee Schedule rule that sets payment rates for next year and also outlines new policies focused on primary care, preserved telehealth flexibilities, and a strengthened Medicare Shared Savings Program (MSSP).

But, provider groups were quick to condemn CMS’ decision to go ahead with the pay cut, which was proposed in the draft rule released in July. In a statement, Bruce Scott, MD, president of the American Medical Association (AMA), pointed out that that while physicians are receiving a 2.8% payment cut next year, medical practice costs for physicians will increase by 3.5% in 2025. After adjusted for inflation, Medicare reimbursement to physicians has decreased 29% since 2001, the AMA says.

The Physicians Foundation conducted a survey on physician practice patterns and perspectives a few years ago. Here are some key findings from the report:

• 31% of physicians identify as independent practice owners or partners. • Almost half (47%) of physicians plan to change career paths. • 78% of physicians sometimes, often or always experience feelings of burnout. • Nearly a quarter of physician time is spent on non-clinical paperwork.

Posted on October 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

AND … BURNOUT

By Staff Reporters

***

***

Compassion fatigue is emotional exhaustion caused by the repeated exposure to others’ suffering. It’s like burning out your empathy circuits. Caregivers, doctors, nurses, healthcare workers and anyone in the helping professions are especially susceptible.

When you’re constantly giving support, it’s easy to feel drained and detached. To combat compassion fatigue, practice self-care and set healthy boundaries.

So, remember, you can’t pour from an empty cup – take care of yourself so you can take care of others.

Posted on September 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stat: 150. That’s how many health systems use AI to help draft replies on MyChart, sometimes without disclosing this to patients. (the New York Times)

Contained in a roughly 200-page quarterly filing from JPMorgan Chase last month were eight words that underscore how contentious the bank’s relationship with the government has become. The lender disclosed that the Consumer Financial Protection Bureau could punish JPMorgan for its role in Zelle, the giant peer-to-peer digital payments network. The bank is accused of failing to kick criminal accounts off its platform and failing to compensate some scam victims.

Bristol-Myers Squibb rose 1.56% after the FDA approved its new drug for schizophrenia, the first new treatment of its kind in decades. Some analysts expect the drug, Cobenfy, to bring in $6 billion in peak annual revenue.

Trump Media gained 5.58% despite a co-founder of its Truth Social platform cashing out nearly all of his shares—worth about $100 million at current prices.

Chinese EV maker Nio added another 12.80% to bring its weekly gains to nearly 25%. It’s benefiting from the overall euphoria around Chinese stocks and anticipation over its quarterly delivery numbers due next week.

Speaking of the Chinese government’s stimulus measures, investors are wagering that the Macau locations of Las Vegas Sands Corp. (up 5.59%) and Wynn Resorts (up 7.24%) will see more visitors.

IonQ, a quantum computing company based in College Park, MD (go Terps), shot up 20.47% after inking a contract with the US Air Force Research Lab.

Stocks down

Nvidia dropped 2.17%. Bloomberg reported that the Chinese government is ramping up the pressure on local tech companies to move away from using Nvidia AI chips and lean more on domestic suppliers.

WeightWatchers, whose shares are down more than 90% this year, booted its CEO Sima Sistani, who pivoted the company to weight-loss drugs. Investors aren’t betting a change at the top will lead to a turnaround, sending shares 2.11% lower on the day.

Globe Life sank 4.74% after the US Equal Employment Opportunity Commission found that the life insurance company tolerated a “pervasive pattern of harassing conduct” at one of its top sales agencies, per Business Insider.

The S&P 500® index (SPX) lost 7.20 points (–0.13%) to 5,738.17 to end the week up 0.62%; the Dow Jones Industrial Average® ($DJI) added 137.89 points (0.33%) to 42,313.00 to end the week up 0.59%; the NASDAQ Composite® ($COMP) fell 70.70 points (–0.39%) to 18,119.59 to end the week up 0.95%.

The 10-year Treasury note yield (TNX) fell four basis points to 3.75%, up two basis points for the week.

Meta is facing a fine of $102 million for storing some users’ passwords in “plaintext”. The social media giant has admitted to poor password management.

Acadia and the Department of Justice just reached a ~$20M agreement to settle accusations that the company billed Medicare, Medicaid, and TRICARE for medically unnecessary inpatient mental health services. Acadia found itself under pressure after a New York Times investigation published earlier in September allegedly found that the company kept patients in facilities against their will to maximize insurance payments.

Posted on August 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

FTX was ordered to pay $12.7 billion to customers. All customers will recoup their deposits that were locked when the crypto exchange went under in 2022, the Commodity Futures Trading Commission just said last Thursday.

Take-Two Interactive Software surged 4.35% after it beat earnings estimates last quarter, but no word yet on how its Gearbox acquisition is helping its bottom line, nor when GTA 6 is going to be released.

Expedia traveled 10.21% higher due to an earnings beat, with the company sidestepping a consumer spending slowdown quite nicely.

What’s down

e.l.f. Beauty tanked 14.46% despite beating earnings estimates and guiding for a better fiscal year than expected, as investors worry about tough competition.

Capri Holdings slid 4.86% as the company founded by Michael Kors faces slowing sales from cash-strapped consumers.

The S&P 500® index (SPX) rose 25 points (0.5%) to 5,344.16, ending the week little changed; the Dow Jones Industrial Average® ($DJI) rose 51 points (0.1%) to 39,497.54 to end the week down about 0.6%; the NASDAQ Composite® ($COMP) ended 85 points higher (0.5%) at 16,745.30, leaving it about 0.2% lower for the week.

The 10-year Treasury note yield (TNX) dropped five basis points to 3.944%.

The Cboe Volatility Index (VIX) declined three points (13%) to 20.7.

Google and Meta teamed up to target teens with ads for Instagram on YouTube, going against Google’s own rules, the Financial Times reported.

Posted on August 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A carry trade is a tactic in which an investor borrows a currency with lower interest rates and invests the proceeds in a higher-yielding asset, often in a different market with higher interest rates.

Over the past few years, many funds were using this strategy by buying US equities or selling US bonds with money borrowed from the yen because of the huge disparity in interest rates between the US and Japan. Japan kept the yen cheap on purpose because its economy is primarily export-driven, and the low price of Japanese products kept exports thriving. And the dollar, as the dominant global currency, has remained impressively strong through thick and thin.

This was all fun and profits, until Japan raised interest rates for the first time in 17 years last week. Suddenly, the yen wasn’t as cheap as it once was. And at the exact same time, the US is expected to cut interest rates in September, which means the dollar would become less valuable, completely throwing this international carry trade out of balance

Posted on July 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

A.I. and Computers

By Staff Reporters

***

***

***

***

Google revealed its answer to ChatGPT: an “experimental conversational AI service” called Bard that’s currently in testing mode.

Microsoft (which invested in ChatGPT) announced its own surprise event scheduled for later today in order to “share some progress on a few exciting projects.”

Chinese tech giant Baidu confirmed it’s on track to introduce its AI chatbot, known as “Ernie Bot” in English, in March.

Posted on July 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters [1 hours ago]

***

***

People woke up to technological chaos this Friday morning as Microsoft suffered a massive, ongoing global IT outage, which is hitting airports, airlines, banks and broadcasters around the world. The problem appears to be with Microsoft 365 services and apps, which many companies and organizations rely on as part of their critical internet infrastructure. Perhaps most concerning of all, many states across the US have reported that their emergency 911 lines are down.

Microsoft said on X that it was aware of an issue impacting people’s ability to access 365 services late on Thursday. The latest update was issued around 4 a.m. ET/1 a.m. PT, when it said, “multiple services are continuing to see improvements in availability as our mitigation actions progress.” The company didn’t immediately respond to request for further comment.

According to CNET, the outage, which also took down the London Stock Exchange, has been linked to a faulty update from cybersecurity company CrowdStrike. The company handles the security of many Windows PCs and services around the world. The last time there was an internet outage this widespread was when a service called Fastly went down in 2021. It’s a reminder of how much of the internet is underpinned by shared infrastructure, which leaves it vulnerable to widespread issues such as this.

Nevertheless, this Medical Executive-Post remains strong; so far.

Posted on July 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Employers expect health benefit costs to rise by more than 5% on average in 2024 as factors like high inflation, health labor shortages, and expensive new therapies put pressure on plan spending after years of 3%–4% annual growth, early data suggests.

Preliminary results from Mercer’s 2023 National Survey of Employer-Sponsored Health Plans found that total health benefit costs could increase by as much as 6.6% per employee if companies do nothing to control spending, or an average of 5.4% if employers take steps to hold down costs.

That slight gap suggests most employers don’t plan to make cost-cutting changes to their plans—likely due to concerns about healthcare affordability, the analysis noted. Many large companies (with 500+ employees) have avoided shifting costs to employees over the last five years, resulting in little growth in deductibles and other cost-sharing requirements.

Several years ago a group of highly trusted and deeply experienced financial services professionals and estate planners noted that far too many of their physician clients, using traditional stock brokers, management consultants and financial advisors, seemed to be less successful than those who went it alone. These Do-it-Yourselfers [DIYs] had setbacks and made mistakes, for sure. But, the ME Inc. doctors seemed to learn from their mistakes and did not incur the high management and service fees demanded from general or retail one-size-fits-all “advisors.“

”In fact, an informal inverse relationship was noted, and dubbed the “Doctor Effect.” In others words, the more consultants an individual doctor retained; the less well they did in all disciplines of the financial planning and medical practice management, continuum.

Of course, the reason for this discrepancy eluded many of them as Wall Street brokerages and wire-houses flooded the media with messages, infomercials, print, radio, TV, texts, tweets, and internet ads to the contrary. Rather than self-learn the basics, the prevailing sentiment seemed to purse the holy grail of finding the “perfect financial advisor.” This realization was a confirmation of the industry culture which seemed to be: Bread for the advisor – Crumbs for the client!

And so, at D.E. Marcinko & Associates, our informed cadre’ of technology focused and highly educated doctors, nurses, financial advisors, attorneys, accountants, psychologists and educational visionaries decided there must be a better way for their healthcare colleagues to receive financial planning advice and related management services within a culture of fiduciary responsibility.

Many financial planning websites mention fees, as required, but still remain opaque to potential clients because the advisor wants to control the discussion and understandably wishes to avoid the website shopper phenomenon.

But, physicians and all investors can still control the discussion, and still provide transparency, because posting up front pricing information doesn’t mean presenting information in a vacuum!

For example, a 1%/year fee doesn’t have to just be 1%; it can be 1%, compared to an industry average cost of X%, where the average cost of an actively managed mutual fund is Y%.

***

***

Similarly, it doesn’t have to be a retainer fee of $1,000/year; it can be a retainer fee for less than the cost of a monthly cable bill! And, a financial plan doesn’t cost $1,500; it costs 8-12 hours of staff time to craft extensive, customized solutions; but saves the doctor-client so much more!

And, if services have a range of potential prices, they might be provided with some insight into the factors that impact the price. Modern young and internet savvy doctors expect this sort of information.

Posted on March 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

TO FIX THE FDA APPROVAL’S FLAW

By Staff Reporters

***

***

DEFINITION: Right-to-try laws are United States state laws and a federal law that were created with the intent of allowing terminally ill patients access to experimental therapies (drugs, biologics, devices) that have completed Phase I testing but have not been approved by the Food and Drug Administration (FDA).

This law would allow patients suffering from rare and genetic diseases to try personalized treatments not yet approved by the FDA, as long as they have the support of their physician and have exhausted other treatment options. This policy would have an outsized impact on patients with rare diseases. Although rare diseases have small patient pools by definition, collectively, about 30 million Americans are estimated to have a rare disease.

Posted on January 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

JPMorgan Chase’s profit fell in the fourth quarter as the lender set aside nearly $3 billion to help refill a government deposit insurance fund. JPMorgan and several major banks are required to pay a bulk of the $16 billion to replenish the Federal Deposit Insurance Corporation’s deposit insurance fund (DIF), which was drained after Silicon Valley Bank and Signature Bank failed last year.

***

Bank of America’s fourth-quarter profit shrank as the lender took $3.7 billion in combined charges to refill a government deposit insurance fund and phase out a loan index. Its net interest income (NII) – the difference between what banks earn from loans and pay to depositors – fell 5% to $13.9 billion as the company spent more to keep customer deposits and demand for loans stayed subdued amid high interest rates.

***

Wells Fargo press release (NYSE:WFC): Q4 Non-GAAP EPS of $1.29 beats by $0.20. Revenue of $20.48B (+2.2% Y/Y) beats by $100M. Shares -1% PM. Fourth quarter 2023 results included: ◦ $(1.9) billion, or ($0.40) per share, of expense from an FDIC special assessment ◦ $(969) million, or ($0.20) per share, of severance expense for planned actions ◦ $621 million or $0.17 per share, of discrete tax benefits related to the resolution of prior period tax matters ◦ Provision for credit losses in fourth quarter 2023 included an increase in the allowance for credit losses driven by credit card and commercial real estate loans, partially offset by a lower allowance for auto loans. The change in allowance for credit losses also included higher net loan charge-offs for commercial real estate office and credit card loans

***

Citigroup (C) is in the middle of a complicated restructuring. It made it clear Wednesday that its fourth quarter earnings report Friday will be complicated, too.

The giant New York-based bank said in a regulatory document it will take more than $3 billion in one-time reserves and expenses as part of those fourth quarter results. They include everything from a $1.3 billion reserve build for currency exposure in Argentina and Russia to $780 million in charges related to severance costs and other aspects of a wide-ranging restructuring of the bank led by CEO Jane Fraser.

First – a little “insider expert” background on the confusion. It exists largely because of the influence that large financial institutions (who earn revenue through the sale of financial products) have on legislators.

The Investment Advisors Act of 1940 requires that anyone giving investment advice must be acting in a fiduciary capacity. The intent was to separate the financial salespeople, who had significant conflicts of interest, from the investment advisors, who had few to none. If you know very little about financial products, would you rather be educated as the customer of a commissioned salesperson or the client of a fee-for-service advisor? Hands down, you’d want the fee-for-service advisor.

Of course, the financial institutions selling products understood this. They were able to influence the drafting of the 1940 Investment Advisors Act, to exclude “any broker or dealer whose performance of such [advisory] services is solely incidental to the conduct of his business as a broker or dealer.” So if salespeople just happen to give some financial advice that is “incidental” to the sale of a product, they and their companies are not held to the fiduciary standard. Our U.S. Congress allows financial companies to advertise as if they are fiduciaries while their sales forces are not held to a fiduciary standard.

Now, according to Rick Kahler CFP®, the same conflict arises in some professional designations, like the Certified Financial Planner® designation conferred by the CFP® Board. The designation initially certified the completion of training in financial planning. In 2008 the Board added a fiduciary requirement to the designation.

However, CFP®’s are only held to a fiduciary requirement when they are doing what the CFP® Board defines as financial planning. If a CFP® professional is giving advice to a client, the fiduciary standard applies. Yet the same professional can sell the same client an annuity with high fees and high commissions, even if the product may not be in the client’s best interest, as long as no “financial planning” is part of the transaction. The result is significant confusion for consumers.

The bottom line is this: when you look for financial advice or financial products, don’t assume the advisor is looking out for you. It’s your responsibility to find out whether any financial professional owes you a fiduciary duty.

So, I suggest you ask directly, “Am I a customer or a client?” The answer is almost always “a client,” as most financial services salespeople honestly don’t know the difference. After you explain that difference, ask them to verify their fiduciary duty in writing. That five-minute solution may have a lasting impact on your financial well-being.

Better yet, consider speaking to your fiduciary focused and fee-only Certified Medical Planner® professional colleagues at D.E. Marcinko & Associates.

Posted on December 5, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

DEFINITION: Income is the money you receive in exchange for your labor or products. Income may have different definitions depending on the context—for example, taxation, financial accounting, or economic analysis. For most people, income is their total earnings in the form of wages and salaries, the return on their investments, pension distributions, and other receipts. For businesses, income is the revenue from selling services, products, and any interest and dividends received with respect to their cash accounts and reserves related to the business. Economists have different definitions of income and different ways of measuring it, from focusing on earnings, savings, consumption, production, public finance, capital investment or other topics … Maybe?

WASHINGTON (Reuters) – The U.S. Supreme Court is set on Tuesday to consider a challenge to the legality of a tax targeting owners of foreign corporations that could undermine efforts at imposing a wealth tax on the very rich in a case that has already sparked controversy over a call for Justice Samuel Alito to recuse.

The justices are due to hear arguments in an appeal by Charles and Kathleen Moore – a retired couple from Redmond, Washington couple – of a lower court’s decision rejecting their challenge to the tax on foreign company earnings, even though those profits had not been distributed.

The one-time “mandatory repatriation tax” (MRT), which applied to taxpayers owning at least 10% of certain foreign corporations, was part of a 2017 Republican-backed tax bill signed into law by former President Donald Trump.

At issue in the case is whether this levy on unrealized gains is allowed under the U.S. Constitution’s 16th Amendment, which enabled Congress to “collect taxes on incomes.” The Moores, backed by the Competitive Enterprise Institute and other conservative and business groups, contend that “income” means only those gains that are realized through payment to the taxpayer, not a mere increase in the value of property.

Why Your Medical Internet Marketing Campaign Isn’t Effective

A strong online presence is crucial for healthcare businesses, but many are struggling to figure out where to invest their marketing dollars. It is important to diversify marketing efforts and not rely solely on one channel, as changes in the industry are inevitable.

Search marketing, direct marketing, and social media are three key components that healthcare organizations should incorporate in their marketing campaigns. Search marketing has evolved over the years with changes in Google’s algorithms and the saturation of the market, requiring a focus on quality content and the expertise of a PPC expert.

Direct marketing is becoming more popular, with lead generation companies and email marketing being effective and budget-friendly tactics. Social media is constantly evolving and increasing in price, with networks like Facebook and Twitter pushing paid advertisements. While social media should not be the focal point of a healthcare organization’s marketing campaign, it is an integral component that can contribute to search engine rankings.

Overall, a well-rounded marketing strategy that incorporates these three elements is crucial for success. A strong online presence is crucial for healthcare businesses, and diversifying marketing efforts across search marketing, direct marketing, and social media is important for success. Search marketing has changed with Google’s algorithms and increased ad costs, while direct marketing and social media have become more popular. Social media also affects search engine rankings.

Posted on November 18, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Healthcare Fraud and Abuse Control Program Annual Report Released

In Fiscal Year (FY) 2022, the Department of Justice (DOJ) opened more than 809 new criminal healthcare fraud investigations. Federal prosecutors filed criminal charges in over 419 cases involving at least 680 defendants. More than 477 defendants were convicted of healthcare fraud related crimes during the year. Also, in FY 2022, DOJ opened more than 774 new civil healthcare fraud investigations and had over 1,288 civil healthcare fraud matters pending at the end of the fiscal year.

Federal Bureau of Investigation (FBI) investigative efforts resulted in over 499 operational disruptions of criminal fraud organizations and the dismantlement of the criminal hierarchy of more than 132 healthcare fraud criminal enterprises. In FY 2022, investigations conducted by HHS’s Office of Inspector General (HHS-OIG) resulted in 661 criminal actions against individuals or entities that engaged in crimes related to Medicare and Medicaid, and 726 civil actions, which include false claims, unjust-enrichment lawsuits filed in Federal district court, and civil monetary penalty (CMP) settlements. HHS-OIG excluded 2,332 individuals and entities from participation in Medicare, Medicaid, and other Federal healthcare programs.

Source: U.S. Department of Health and Human Services and U.S. Department of Justice

Posted on October 24, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

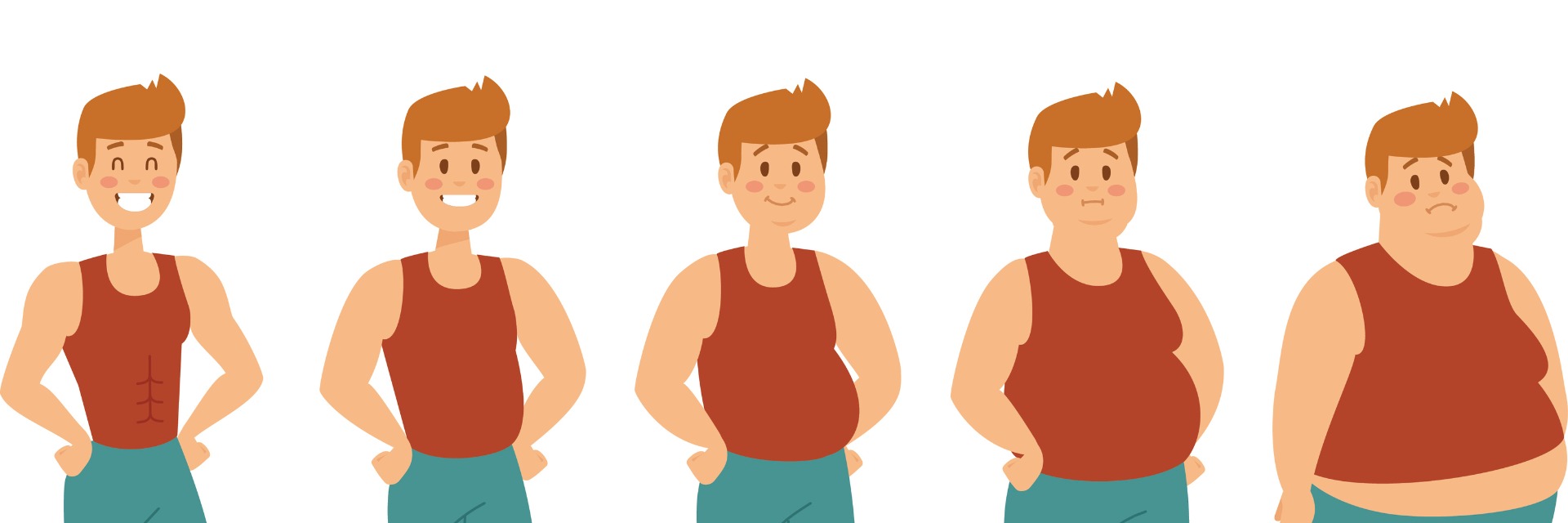

The already booming market for weight loss treatments like Ozempic might get even bigger as drug companies seek to make them available for children. The CDC estimates that ~20% of kids 6+ in the US have obesity, and manufacturers are working to make their weight loss drugs available for that age group.

According to Bloomberg, Novo Nordiskis testing its Saxenda in kids as young as six, and Eli Lilly is getting ready for similar trials of Mounjaro. That could give the companies lifelong customers since the drugs only keep weight off as long as people take them—and Goldman Sachs’s recent estimate that the drug category would make $100 billion by 2030 didn’t even take sales to children into account.

Posted on October 5, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Darrell Pruitt DDS

***

***

Less than a week after the American Dental Association pushed dentists to adopt electronic dental records, Infosecurity Magazine announced “Record Numbers of Ransomware Victims Named on Leak Sites.”

So whom does the ADA protect? It’s not dentists and their patients.

Posted on September 19, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Medicare enrollees could save $500+ per year in out-of-pocket spending if federal lawmakers expand parts of the program to include dental services, according to a report released last week.

The Urban Institute analysis—aided by funding from the Robert Wood Johnson Foundation—examined the implications of expanding Medicare Part B, which covers medically necessary and preventive services, to include dental care. The proposed coverage would be subject to Part B deductibles and 20% cost-sharing, and it could lower out-of-pocket expenses by 80%, or $530 per person annually, the report found.

Katherine Hempstead, a Robert Wood Johnson Foundation senior policy advisor, said the proposed expansion is “an opportunity to increase equity and close long-standing gaps in access to dental services.” Low-income older adults currently “bear the brunt” of Medicare’s lack of dental coverage, she added.

Posted on September 16, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

One week into the 10-week trial in the U.S.A’s government’s high-stakes antitrust case against Google as the two sides have already staked out their positions.

The DOJ claims that Google spends billions per year to maintain its monopoly over search, paying to be the default on web browsers and mobile devices. Google, meanwhile, asserts that its dominant position comes from being better than all its competitors.

“If Google is prevented from competing, that won’t make Yahoo or DuckDuckGo run faster,” the company’s lawyer reportedly said in court.

Posted on September 5, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

A JOE BIDEN PROPOSAL

By Staff Reporters

***

***

WASHINGTON (Reuters) – President Joe Biden’s administration just proposed setting federal minimum staffing levels for nursing homes, a move aimed at addressing longtime complaints about abuse and neglect in the industry that were highlighted during the COVID-19 pandemic.

Biden pledged last year to protect American seniors’ lives and life savings by cracking down on nursing homes that commit fraud or endanger patients’ safety and address the chronic under staffing at long-term care facilities that was exposed during the pandemic.

The nursing home industry takes in nearly $100 billion a year from U.S. taxpayers, yet many under staff their facilities, the White House said. The new rule proposes that facilities have a registered nurse (RN) on site around the clock. It says each resident should receive 2.45 hours (two hours and 27 minutes) of care from a nurse aide every day, plus at least 33 minutes of care from an registered nurse every day.

EDITOR’SNOTE: Dr. Zubin Damania, MD is a UCSF/Stanford-trained hospital doctor and host of The ZDoggMD Show, dedicated to Alt-Middle sense-making in healthcare and beyond. Videos are informational and are not medical advice, more info: https://zdoggmd.com/terms

Posted on July 26, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA CMP

***

***

(AP) — A federal lawsuit alleges that health insurance giant CIGNA used a computer algorithm to automatically reject hundreds of thousands of patient claims without examining them individually as required by California law.

The class-action lawsuit, just filed in federal court in Sacramento, says CIGNA Corp. and CIGNA Health and Life Insurance Co. rejected more than 300,000 payment claims in just two months last year.

The company used an algorithm called PXDX, shorthand for ”procedure-to-diagnosis,” to identify whether claims met certain requirements, spending an average of just 1.2 seconds on each review, according to the lawsuit.

Posted on June 24, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Health care sharing is not insurance, but the plans count as insurance under the Affordable Care Act (ACA). That means more affordable healthcare benefits while avoiding the tax penalty for going uninsured. Other pros of health care sharing over insurance include: Lower cost. Monthly costs of health sharing are usually much lower than insurance premiums, although the rules are different for what’s covered. Also, the annual “unshared amount” is much, much lower than deductibles on lower-premium or catastrophic insurance plans. Your choice of provider. There are no network requirements, and you provide your health sharing card as coverage. If a doctor won’t accept your plan and you have to pay out-of-pocket, health sharing plans reimburse your expense.s

Now, the caveats: Health care sharing plans aren’t required to cover pre-existing conditions, such as cancer, diabetes, or lifestyle-related conditions like smoking. Those who have them may be declined membership or won’t have the conditions fully covered for a year or more. Health care sharing also doesn’t typically cover the essential health benefits like wellness exams or mental health counseling.

Yet, at least 1.7 million Americans are involved in a health sharing agreements despite a lack of protections (KFF Health News).

Posted on June 11, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

CRANIA: A delivery driver for the Anatomical Gift Association (AGA) of Illinois claims that after he complained about corpse storage protocol, he arrived at work to find three [3] severed heads in plastic containers in his office. The AGA denied it was retaliation, saying a desk full of skulls is just part of the job.

***

Doctors on TikTok? Hospital re-brandings? Healthcare marketers are trying new strategies to reach patients—but they’re not always a slam dunk success.

Posted on April 2, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

WORKPLACE MEDICAL VIOLENCE

By Staff Reporters

***

***

Workplace safety is no joke. Slips and trips can lead to a hospital visit—though at least it’s a quick commute for healthcare workers in states with high rates of workplace injuries. In fact, Maine, Oregon, and Vermont had the highest rates of nonfatal workplace accidents and injuries, according to an analysis shared with Healthcare Brew via email of 2021 US Bureau of Labor Statistics data compiled by High Rise Financial, a pre-settlement legal funding company.

What do these states also have in common? According to HealthcareBrew, nursing, ranked within the top 10 most popular professions in each state.

Maine had the highest rate of workplace accidents: 4.7 out of every 100 full-time workers in the state were involved in a nonfatal workplace accident in 2021, High Rise Financial found. That is 67.9% higher than the country’s yearly average. In 2021, 30,270 of the 592,000 registered employees in Maine were home healthcare workers or registered nurses. MaineHealth was the state’s largest private employer in 2021 with approximately 20,500 employees, per the Maine Center for Workforce Research and Information. But the state’s high accident rate isn’t a failure—it suggests that Maine workers are reporting accidents and injuries before they become more serious and require workers’ compensation, Maine Public Radio reported. The most recent data from 2011 shows that workers’ compensation losses cost hospitals nationwide $2 billion, the Occupational Safety and Health Administration found.

If tedious workplace safety rules sound like a pain, try having an accident. “Slips, trips, and falls,” especially without a wet floor warning sign, are the top causes of workplace accidents that are eligible for pre-settlement funding, according to the High Rise Financial analysis. Even a small slip could lead to a back injury, a broken bone, or a concussion—no banana peel needed.

It’s not all doom and gloom: The CDC has generously curated a list of songs with workplace safety and health themes to liven up your nine-to-five. Just be sure to wear nonslip shoes if you feel like dancing.

One nonprofit, United Network for Organ Sharing, has had a monopoly on running the system for nearly four decades, but the government’s proposal includes potentially bringing more organizations in, as well as upping funding and modernizing the computer systems involved.

Posted on March 23, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

AT1 BONDS =OH NO!

By Staff Reporters

***

***

DEFINITION: Junk bonds are bonds that carry a higher risk of default than most bonds issued by corporations and governments. A bond is a debt or promise to pay investors interest payments along with the return of invested principal in exchange for buying the bond. Junk bonds represent bonds issued by companies that are financially struggling and have a high risk of defaulting or not paying their interest payments or repaying the principal to investors. Junk bonds are also called high-yield bonds since the higher yield is needed to help offset any risk of default.

AT1 DEFINITION: Additional Tier 1 bonds are also known as “contingent convertibles,” or “CoCos”. They were created in the wake of the 2008 financial crisis as a way for failing banks to absorb losses, making a taxpayer-funded bailout less likely. They are a risky bet — if a lender gets into trouble, this class of bonds can be quickly converted into equity, or written down completely. Because they are higher-risk, AT1s offer a higher yield than most other bonds issued by borrowers with similar credit ratings, making them very risky. If AT1s are converted into equity, this supports a bank’s balance sheet and helps it to stay afloat. They also pave the way for a “bail-in”, or a way for banks to transfer risks to investors and away from taxpayers if they get into trouble.

UBS’s emergency takeover of Credit Suisse may have been necessary to avert a financial crisis, but at least one group is Yosemite Sam-level angry over how the deal shook out. Investors holding $17 billion worth of Credit Suisse’s additional tier-one bonds were shocked to discover that their $17 billion was now worth a grand total of…$0. The value of those bonds had been completely wiped out in the deal.

Additional tier-one bonds, or AT1 bonds for short, were established after the 2008 financial crisis to reduce the likelihood that taxpayers would have to bail out a failed bank. AT1s are considered riskier assets, but with that risk comes higher potential returns.

So, if these bondholders knew they were taking on risk, why are they so upset?

According to MorningBrew, mainly because, in this unusual deal, they got wiped out while shareholders didn’t. That’s not how the order of operations usually works:

When a write-down happens, shareholders traditionally suffer losses before bondholders get hit.

This deal flipped the food chain, and livid AT1 bondholders are now huddling up with lawyers about potential legal action.

Posted on March 20, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

When Does Spring Start?

By Staff Reporters

***

***

In 2023, the official first day of spring is today Monday, March 20th. This date marks the “spring equinox” in the Northern Hemisphere. So, what is the spring equinox and is it always on the 20th? Read on to learn more—plus, enjoy ideas on how to celebrate the season!

UBS agreed to buy its embattled rivalCredit Suisse for 3 billion Swiss francs ($3.25 billion) yesterday, with Swiss regulators playing a key part in the deal as governments looked to stem a contagion threatening the global banking system.

“With the takeover of Credit Suisse by UBS, a solution has been found to secure financial stability and protect the Swiss economy in this exceptional situation,” read a statement from the Swiss National Bank, which noted the central bank worked with the Swiss government and the Swiss Financial Market Supervisory Authority to bring about the combinationof the country’s two largest banks.

Posted on March 10, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

***

By AnonymousLetter Leaker

***

DAVE – This is what happens when private equity takes over anesthesiologists and other medical services. Private equity has squeezed so much out of physician lives and their practices, that practice has become intolerable. They are all so burnt out that the physician anesthesiologist must now strike out against their own private equity group owners (NAPA). The trickle-down effect becomes with the hospital now caught in the middle, contracted with a private equity group which provides anesthesia, but they have no anesthesiologist employees.

Where does patient care survive?

***

February 2023

Colleagues,

As you may be aware, Inova contracts with North American Partners in Anesthesia (NAPA) to provide anesthesia services at Inova Loudoun Hospital. This week, we received notice that our anesthesiologists at Inova Loudoun Hospital have submitted 90-day notice letters of resignation to NAPA. In the spirit of full transparency, we are sharing this news with our physicians.

Here’s what you need to know:

Although we are monitoring this situation, Inova is not a participant in discussions. They are held solely between the anesthesiologists and NAPA. We are actively working to ensure minimal disruptions to current workflows at our care sites. Our anesthesiologists are among the best in the country, and we fully expect that our team members will continue to provide world-class healthcare to the communities we are privileged to serve.

Per our care mandate, people are at the center of everything we do, and we take any situation that affects the work environment of our team members very seriously. We will continue to communicate with NAPA and keep you apprised of pertinent developments.

If you have questions about this situation, please contact Loren Rufino, Senior Vice President, Perioperative Services.

Thank you,

John J. Moynihan, MD, FACS President, Surgery Service Line

Loren A. Rufino SVP, Perioperative Services Administrator Surgery Service Line

Paula R. Graling, DNP, RN, CNOR, NEA-C,FAAN VP, Nursing, Surgery Service Line

CMS pays Medicare Advantage Plans per member based on a risk score. The more chronic conditions the person has, the larger the payments CMS makes to the Medicare Advantage Plan.

Medicare Advantage Plans may be overexaggerating how sick their members are in order to increase their payments from CMS.

The Department of Justice is currently suing Cigna and Elevance (Anthem) for such over exaggerations.

However there is a deeper problem… CMS itself had performed its own audits, but has not done so in 10 years. CMS identified $650M in overpayments and did nothing about them.

When the Kaiser Family Foundation (KFF) requested information on the audits, CMS refused. KFF had to sue CMS to obtain the audit information and it took 3 years for KFF to win the case.

Perhaps it is incompetence on the part of CMS or perhaps CMS does not want to reveal the audits or do anything about them due to political pressure.

TUCSON, Ariz., Dec. 06, 2022 (GLOBE NEWSWIRE) — Sheila Page, D.O., a family physician in Aledo, Texas, and president of the Association of American Physicians and Surgeons (AAPS), is featured in the winter issue of the of the Journal of American Physicians and Surgeons. She writes: “Today physicians often feel constrained to pick from among options that are not in the best interest of patients but are ‘covered’ by insurance or approved by officials.”

“An apparently free choice when there is no real alternative is a Hobson’s Choice, and physicians must understand the political structure in which this type of ‘choice’ is embedded,” Dr. Page explains.

“During the COVID pandemic, people often faced a Hobson’s Choice of taking a shot that they believed put their life, health, or fertility at risk, or be barred from their education or career,” she noted.

“Voters generally believe that they have two choices, Republican or Democrat, and that they represent extremes of political ideology. However, when they are in office, politicians behave as if they belong to the same club,” she writes.

“Physicians have accepted the Hobson’s Choice of either abiding by ridiculous regulatory burdens or refusing to treat the senior population,” she explains. They “accept the Hobson’s Choice of either standing against the oppression or keeping their ‘place at the table.'”

“The phrase ‘we need to keep our place at the table to avoid being on the menu’ entirely misses the point,” she states. “The profession is on the table already being carved up. How many times have we been told we must choose the lesser of two evils? Either choice is still evil!”

“We must identify the enemy within,” Dr. Page writes. “The medical profession must grasp the extent to which it has been manipulated by pharmaceutical, insurance, and other systems tied to medicine. We have been burdened with regulations and threats to our licenses by the same people who are selling us the solutions.”

“There is tremendous profit in the existing system, but we must nevertheless offer healing and hope, learn how to fight back effectively, and reject the Hobson’s Choice,” she concludes.

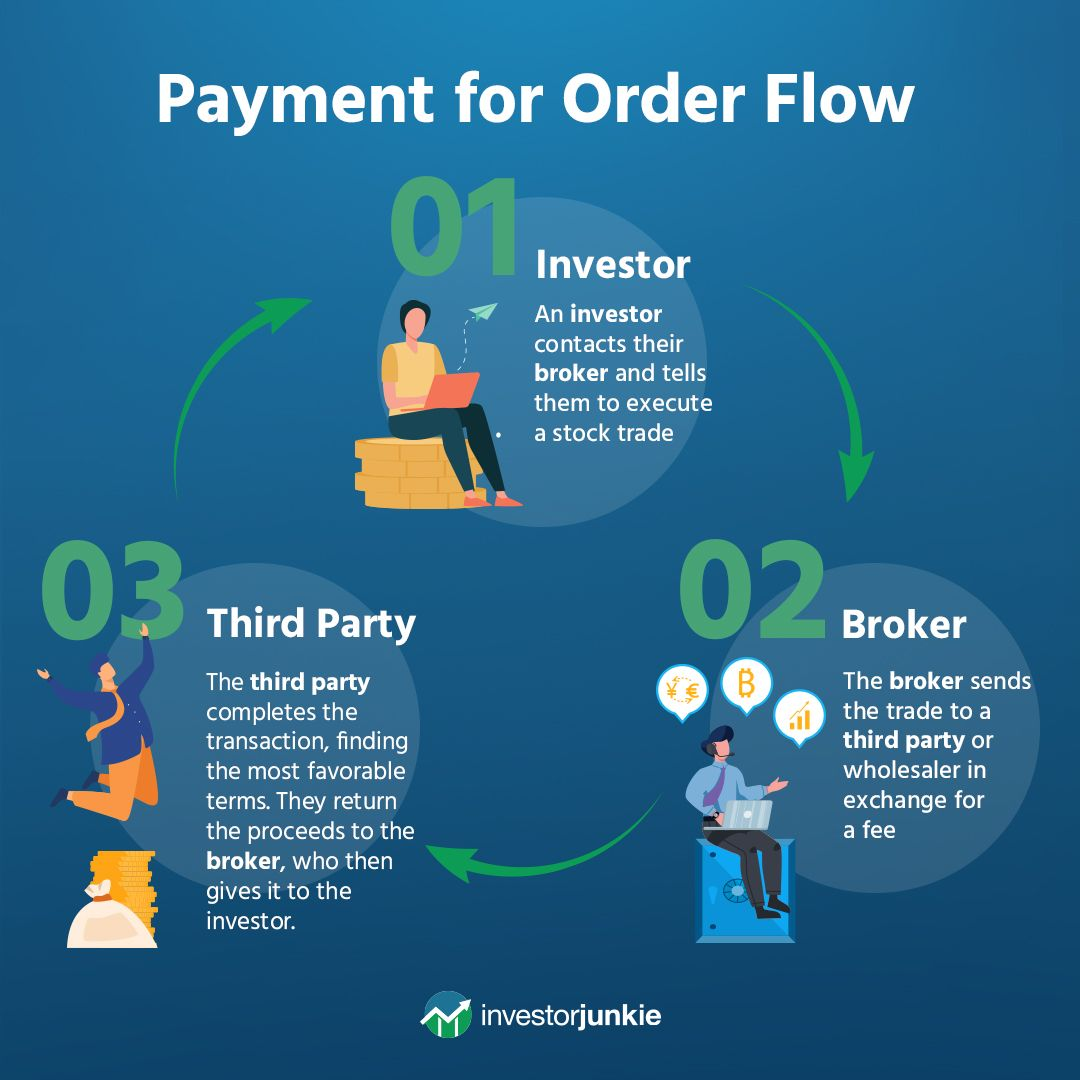

Yesterday the SEC proposed the biggest update to the stock trading rules book since 2005. The four proposed rules may become the magnum opus of Gary Gensler, who took over as SEC chair after the meme stock mayhem of 2021. The rules aim to get retail traders better prices by targeting a method of executing trades called payment for order flow (PFOF). PFOF works like this:

Brokers like Robinhood send trades to wholesalers like Citadel, which profit off the difference between the individual trader’s proposed price and the price they actually make the trade for.

Wholesalers pay brokers a small fee for the privilege of making the trade, and *juicy detail alert* those “small fees” make up a huge chunk of the brokers’ revenue.

Gensler has long argued that PFOF limits competition and encourages brokers to gamify risky trading behavior—like vetting your life savings on GameStop stock. The practice is banned in the UK and Canada.

But the SEC has definitely put it in the “no longer sparks joy” pile

Under the most significant rule proposed yesterday, the “order competition” rule, wholesalers would have to send most retail investors’ trades to an auction where dealers compete to fulfill them for the best price.

The wholesaler only gets to fulfill any leftover trades that no one has bid on. Some on Wall Street argue this will be the most common scenario so the rule won’t have its intended effect, but Gensler thinks auctions could save individual traders up to $1.5 billion per year.

Posted on November 21, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Markets: It’ll be a short but stuffed Turkey Day week for investors. In the lead-up to Thanksgiving, when markets will close, we’ll get another batch of earnings reports and minutes from the previous Fed meeting. Traders will have to clock in on Black Friday for a half day.

Stock spotlight: The e-scooter rental company Bird is probably grateful that FTX’s implosion is stealing the spotlight from its own collapse. Last week, the company said it overstated revenue for more than two years and is warning it could go bankrupt if things don’t turn around. Currently a penny stock, Bird will be de-listed by the NYSE if its share price doesn’t rise above $1 by the end of the year.

Disney just announced that former CEO Bob Iger would return to his role atop the entertainment giant, replacing his successor Bob Chapek, who’s been CEO for less than three years.After leading the company for 15 years, Iger handed over the reins to Chapek in February 2020. It was an unexpected choice, given that streaming boss Kevin Mayer was seen as a more likely heir to the Disney throne than Chapek, who led the parks and entertainment division. But Iger had reportedly handpicked Chapek as his successor, and repeatedly said he was satisfied with being retired. “I can’t think of a better person to succeed me in this role,” Iger said in March 2020.

Posted on November 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

DEFINITION

Upcoding is a type of fraud where healthcare providers submit inaccurate billing codes to insurance companies in order to receive inflated reimbursements. These false “current procedural technology” (CPT) submissions indicate that doctors provided patients with treatments that were more complex, costly, and time-consuming than what they actually received. This unlawful scheme is a violation of the False Claims Act (FCA) because it defrauds federal programs including Medicare, Medicaid, and Tricare.

There are nearly 7,800 CPT codes used by healthcare providers. Collectively, these codes represent all of the procedures, conditions, and drugs that are currently reimbursable by the health insurance industry. Each one of them has an associated cost for individuals and insurance companies, based upon the urgency of the issue and the complexity of the decision-making required of the healthcare provider. Medicaid and Medicare reimburse providers based on this system. For example, a five-minute consultation with a nurse for a minor medical question would receive a different, less expensive CPT than the one for a full examination by a doctor lasting 45-minutes. However, if the physician charges the federal programs for the more expensive 45-minute examination when the five-minute consultation is what actually occurred, this would constitute upcoding.

Unbundling

Unbundling is another common form of upcoding. This fraudulent scheme involves billing for individual procedures that are usually performed and billed together under a single CPT code. In some cases, the billing codes for complicated medical operations have associated components built into their CPTs. For example, a hip replacement surgery may factor in the costs of the surgeon’s as well as the use of the operating room. Unbundling occurs when a healthcare provider submits each component within a CPT to Medicare or Medicaid separately. This creates a cost redundancy where wrongdoers can unlawfully seek reimbursement for the same procedure several times over.

Downcoding is the opposite of upcoding. If you perform a service but record the CPT for a lower-level service, that is downcoding. Downcoding also leaves you vulnerable to an audit, which is never good. But, it can also cost a practice thousands of dollars a year in lost revenue because you’re not getting the higher rate of pay that you would if you had recorded the service properly.

According to the National Correct Coding Initiative (NCCI): “Physicians must avoid downcoding. If an HCPCS/CPT code exists that describes the services performed, the physician must report this code rather than report a less comprehensive code with other codes describing the services not included in the less comprehensive code.”