By Dr. David Edward Marcinko; MBA MEd

By Dr. Gary L. Bode; CPA MSA

SPONSOR: http://www.MarcinkoAssociates.com

***

***

For CPA Exam Success

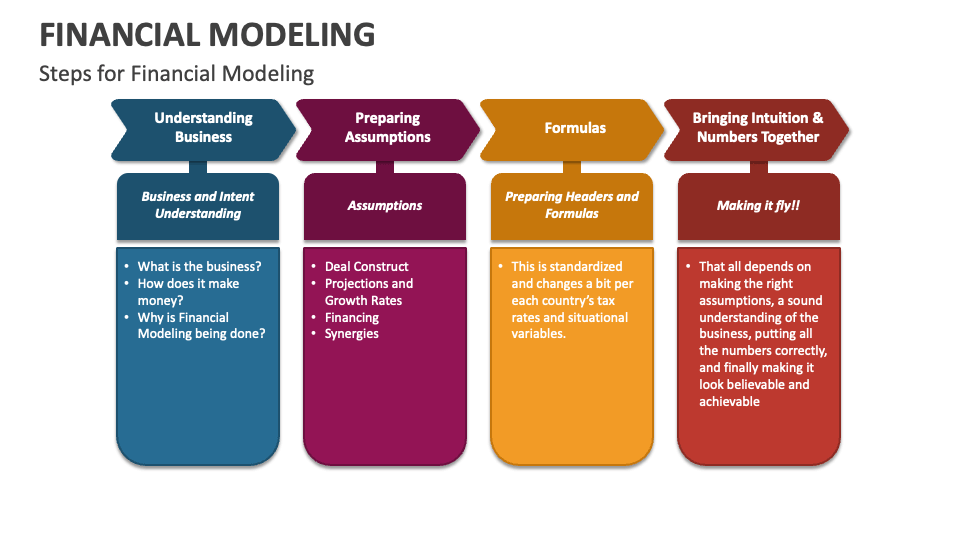

Project management plays a central role in modern accounting, and for CPA candidates, understanding this discipline is more than practical knowledge — it is essential exam content. Across the CPA Exam’s core and discipline sections, candidates are expected to demonstrate the ability to plan engagements, manage risk, coordinate stakeholders, and ensure high‑quality outputs. Mastery of project management principles strengthens not only real‑world accounting performance but also a candidate’s ability to analyze scenarios, apply judgment, and recognize best practices under exam conditions.

A strong accounting project begins with clear scoping and planning, a concept that appears frequently in AUD and BAR task‑based simulations. Planning defines the engagement’s objectives, deliverables, and constraints, ensuring that the accountant or auditor understands what must be accomplished and by when. On the CPA Exam, candidates are often asked to identify missing planning elements, evaluate the adequacy of a project plan, or determine how changes in scope affect timelines and resource allocation. Effective planning includes establishing milestones, assigning responsibilities, and identifying dependencies — all of which help prevent the bottlenecks and last‑minute errors that exam scenarios often highlight. For CPA candidates, recognizing the link between planning and engagement efficiency is critical, as many exam questions test the ability to anticipate issues before they arise.

Once planning is established, coordination and communication become essential. The CPA Exam frequently tests communication expectations in audit engagements, internal control evaluations, and tax advisory scenarios. Accounting projects involve multiple stakeholders — clients, internal departments, auditors, regulators — each requiring timely and accurate information. Project management emphasizes structured communication through status updates, documentation, and escalation procedures. On the exam, candidates may be asked to determine the appropriate communication method, identify breakdowns in communication, or evaluate whether documentation meets professional standards. Understanding these principles helps candidates navigate simulations where miscommunication leads to errors, delays, or compliance failures.

Another major theme across CPA Exam sections is risk management, a core project management function. Accounting work carries inherent risks, including data inaccuracies, fraud, system failures, and regulatory noncompliance. Project management frameworks require early identification of risks, assessment of their likelihood and impact, and development of mitigation strategies. In AUD, this aligns directly with risk assessment procedures; in BAR, it connects to operational and financial risk analysis; and in REG, it relates to compliance and penalty avoidance. CPA candidates must be able to evaluate risk scenarios, propose controls, and recognize when contingency planning is necessary. Exam questions often present situations where a failure to anticipate risk leads to material misstatements or missed deadlines, making risk management knowledge indispensable.

Quality control is another project management area deeply embedded in CPA Exam content. Accounting projects demand accuracy, consistency, and adherence to professional standards. Project management supports quality through review cycles, standardized templates, checklists, and documentation protocols. In AUD, this aligns with engagement quality reviews and documentation requirements. In FAR, it relates to ensuring that financial statements reflect accurate application of GAAP. In REG, it connects to due diligence and ethical responsibilities. Candidates must understand how quality control procedures prevent errors and support reliable reporting. Exam scenarios often test the ability to identify weaknesses in review processes or determine whether documentation is sufficient.

Technology has become increasingly important in both accounting practice and CPA Exam content. Modern project management relies on software tools that track tasks, centralize documentation, and automate routine processes. The CPA Exam emphasizes digital acumen, including data analytics, workflow automation, and system controls. Understanding how technology enhances project management — by improving transparency, reducing manual errors, and enabling real‑time monitoring — helps candidates navigate exam questions involving system implementations, data governance, and internal control design.

Ultimately, project management elevates accounting from a transactional function to a strategic discipline — a theme that resonates across the CPA Exam’s focus on critical thinking and professional judgment. By applying structured methodologies, accountants deliver more reliable results, adapt to changing conditions, and provide insights that support decision‑making. For CPA candidates, mastering project management concepts strengthens exam performance by improving the ability to analyze scenarios, identify best practices, and apply judgment under pressure.

COMMENTS APPRECIATED

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR- http://www.MarcinkoAssociates.com

Like, Refer and Subscribe

HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

CLINICS: http://www.crcpress.com/product/isbn/9781439879900

ADVISORS: www.CertifiedMedicalPlanner.org

FINANCE:Financial Planning for Physicians and Advisors

INSURANCE:Risk Management and Insurance Strategies for Physicians and Advisors

Dictionary of Health Economics and Finance

Dictionary of Health Information Technology and Security

Dictionary of Health Insurance and Managed Care

***

Share this:

Filed under: iMBA, Inc. | Tagged: Accounting, AI, artificial intelligence, business, by-dr-gary-l-bode-cpa-msa, ChatGPT, CPA, Marcinko, project-management, Technology | Leave a comment »

***

***