BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Financial Modeling Services — Building discounted cash flow models, scenario analyses, or forecasting tools for startups, founders, or small businesses. CFAs excel at structuring assumptions, validating inputs, and producing investor‑ready models.

Equity Research Writing — Many newsletters, fintech platforms, and media outlets need clear, data‑driven market commentary. You’re not giving personalized advice—you’re explaining trends, fundamentals, and sector dynamics.

Corporate Finance Consulting — Small companies often need help understanding capital structure, cost of capital, or project evaluation. CFAs can provide structured analysis without acting as a broker or advisor.

Valuation Projects — From startup valuations to fairness assessments, valuation is a core CFA skill. This work is project‑based, high‑impact, and often well‑paid.

Teaching Finance Courses — Universities, bootcamps, and online platforms value instructors who can explain complex topics like portfolio theory, derivatives, or financial reporting.

Creating Finance Content — YouTube, LinkedIn, Substack, and podcasts reward clear, authoritative voices. CFAs can break down earnings reports, macro trends, or valuation concepts for broad audiences.

Building Financial Tools — Spreadsheet templates, valuation calculators, KPI dashboards, or risk‑analysis tools can be sold as digital products. This scales better than hourly consulting.

Expert Witness Work — CFAs are sometimes hired to interpret financial statements, valuation disputes, or damages calculations. It’s niche but highly compensated.

Board or Advisory Roles — Startups and nonprofits often seek financially literate advisors. You’re offering governance insight, not investment advice.

Freelance Risk Analysis — Companies need help evaluating credit risk, operational risk, or market exposures. CFAs can provide structured frameworks and reports.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors1738@outlook.com -OR-http://www.MarcinkoAssociates.com

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors1738@outlook.com -OR-http://www.MarcinkoAssociates.com

A Special Purpose Acquisition Company, or SPAC, is a unique financial vehicle designed to take a private company public through a merger rather than a traditional initial public offering. SPACs have existed for decades, but they surged into mainstream attention in recent years as investors, entrepreneurs, and financial markets sought faster and more flexible alternatives to the conventional IPO process. Understanding SPACs requires examining their structure, their appeal, the risks they introduce, and the evolving role they play in modern capital markets.

A SPAC begins as a shell corporation with no commercial operations. It is created by a sponsor—often an experienced investor, private equity group, or industry executive—who raises capital from public investors. At this stage, investors are not buying into an operating business but rather into the sponsor’s ability to identify and acquire one. The money raised is placed in a secure trust account until the SPAC finds a suitable target company. This structure gives early investors a degree of protection: if the SPAC fails to complete a merger within a typical two‑year window, investors may redeem their shares and recover their initial investment with interest. This redemption feature is central to the appeal of SPAC investing.

Once the SPAC identifies a target, the two parties negotiate a merger known as the “de‑SPAC” transaction. This process effectively replaces the traditional IPO. Instead of undergoing months of regulatory review, market testing, and roadshows, the private company can go public more quickly and with greater control over valuation. SPAC mergers also allow companies to present forward‑looking projections, something traditional IPO rules restrict. This flexibility made SPACs particularly attractive to firms in emerging industries such as electric vehicles, biotechnology, and space technology—sectors where future potential often matters more than current revenue.

The rapid rise of SPACs was driven by several converging forces. Low interest rates pushed investors to seek higher‑return opportunities, and SPACs offered a seemingly low‑risk way to participate in early‑stage growth companies. Sponsors were motivated by the “promote,” a substantial equity stake they receive if a deal closes, which can be highly lucrative. Meanwhile, private companies saw SPACs as a way to access public markets quickly, avoid volatile IPO pricing, and partner with experienced sponsors who could provide strategic guidance. These incentives created a surge of activity, with hundreds of SPACs launching in a short period and raising tens of billions of dollars.

However, the SPAC model also presents significant challenges. One of the most widely discussed issues is dilution. Because sponsors receive a large equity stake and SPACs often raise additional financing through PIPE deals, the ownership of ordinary shareholders can be heavily diluted by the time the merger closes. This dilution can reduce the value of shares and make it more difficult for the post‑merger company to meet investor expectations. Understanding SPAC dilution is essential for evaluating the true economics of these transactions.

Another challenge is the incentive structure. Sponsors only profit if a merger occurs, which can create pressure to complete a deal even if the target company is not ideal. During the SPAC boom, several companies that went public through SPAC mergers struggled to meet their optimistic projections, leading to sharp stock declines and increased scrutiny. This raised questions about whether SPACs were enabling companies to bypass the rigorous vetting that traditional IPOs impose.

Regulators responded by tightening rules around disclosures, projections, and accounting practices. These changes aim to bring SPACs closer in line with traditional IPO standards and ensure that investors receive clear, accurate information. As a result, the SPAC market has cooled from its peak, but it has not disappeared. Instead, it is evolving into a more disciplined and selective environment where sponsor quality, deal structure, and target fundamentals matter more than hype.

Despite their challenges, SPACs remain an important financial innovation. They offer a distinctive blend of speed, flexibility, and investor protections that can be valuable under the right circumstances. For private companies with complex business models or long‑term growth trajectories, SPACs can provide a more narrative‑driven path to the public markets. For investors, SPACs offer optionality: the ability to participate in a deal or redeem shares if the proposed merger seems unattractive. This optionality makes SPAC structures fundamentally different from traditional IPO investments.

Looking ahead, SPACs are likely to settle into a more specialized role rather than serving as a broad‑based alternative to IPOs. They may become particularly useful for companies in emerging or capital‑intensive industries where traditional IPO metrics do not fully capture long‑term potential. At the same time, investors are now more cautious, focusing on sponsor reputation, alignment of incentives, and the underlying fundamentals of target companies. This shift suggests that SPACs will continue to exist but with greater discipline and more realistic expectations.

In summary, SPACs represent both the creativity and complexity of modern financial markets. They challenge traditional pathways to going public and offer an alternative that can be powerful when used responsibly. Yet they also highlight the importance of transparency, investor protection, and thoughtful regulation. As markets continue to evolve, SPACs will remain a subject of debate, innovation, and strategic interest—an example of how financial engineering can reshape the landscape of public capital formation.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The word entrepreneur has become one of the most recognizable terms in modern economic and cultural vocabulary, often used to describe innovators, risk‑takers, and business founders who shape industries and drive economic progress. Yet the history of the word itself reveals a long, complex evolution that mirrors broader changes in society, economics, and the understanding of human initiative. Far from being a recent invention of the business world, the term has roots that stretch back centuries, undergoing multiple transformations before arriving at its contemporary meaning.

The linguistic origins of entrepreneur lie in the Old French verb entreprendre, meaning “to undertake” or “to take in hand.” This verb, in turn, traces back to the Latin phrase inter prehendere, meaning “to seize” or “to grasp.” The earliest uses of entreprendre in medieval France were not tied to business in the modern sense but instead referred broadly to undertaking any kind of task or mission. By the sixteenth century, the noun entrepreneur had emerged in French, originally describing individuals who undertook significant projects. These early entrepreneurs were not business founders but often military leaders or organizers of large expeditions. In this context, the term carried connotations of leadership, responsibility, and the willingness to take on complex, uncertain ventures.

As European societies evolved, so did the meaning of the word. During the seventeenth century, entrepreneur expanded to include individuals involved in engineering and construction projects. These were people who accepted contracts to build fortifications, roads, or public works—tasks that required coordination, planning, and the management of labor and materials. The shift from military to engineering contexts reflected broader changes in European economies, where large‑scale infrastructure projects became increasingly important. The entrepreneur, in this sense, was someone who accepted responsibility for delivering a defined outcome, often under conditions of uncertainty.

It was not until the early eighteenth century that the word began to take on a more explicitly economic meaning. A key figure in this transition was the economist Richard Cantillon, who offered one of the earliest formal definitions of the entrepreneur. Writing in the early 1700s, Cantillon described entrepreneurs as individuals who bore the risk of buying goods at certain prices and selling them at uncertain ones. In his view, the defining characteristic of the entrepreneur was not simply undertaking a project but assuming financial risk in the face of unpredictable market conditions. This was a significant conceptual shift: the entrepreneur was no longer just a contractor or organizer but a central figure in the functioning of markets.

***

***

Cantillon’s ideas laid the groundwork for later economic thinkers, most notably Jean‑Baptiste Say, who further expanded the meaning of the term in the early nineteenth century. Say argued that entrepreneurs were not merely risk‑bearers but also innovators who played a crucial role in economic development. According to Say, entrepreneurs shifted resources from areas of lower productivity to areas of higher productivity, thereby driving economic progress. This interpretation introduced the idea of the entrepreneur as a creative force—someone who identifies opportunities, reorganizes resources, and generates new value. Say’s work helped cement the entrepreneur as a key figure in classical economic theory.

Throughout the nineteenth century, the word entrepreneur gradually entered English usage, though it initially retained a narrower meaning. Early English references often described individuals who managed theatrical productions or other organized ventures. Only later did the term broaden to encompass business founders and managers more generally. By the mid‑nineteenth century, the modern sense of the entrepreneur as a business leader began to take hold, reflecting the rise of industrial capitalism and the increasing importance of private enterprise.

The twentieth century brought further refinement to the concept. Economists such as Joseph Schumpeter emphasized the entrepreneur’s role as an agent of “creative destruction,” someone who disrupts existing markets through innovation. Others, like Frank Knight, highlighted the distinction between measurable risk and true uncertainty, arguing that entrepreneurs are defined by their willingness to operate in environments where outcomes cannot be predicted. These theoretical developments enriched the meaning of the word, aligning it with broader discussions about innovation, uncertainty, and economic change.

By the late twentieth and early twenty‑first centuries, entrepreneur had become a global term, widely used across cultures and disciplines. Its meaning expanded beyond traditional business contexts to include social entrepreneurs, cultural entrepreneurs, and even political entrepreneurs—individuals who apply entrepreneurial thinking to create change in various domains. The rise of the technology sector further popularized the term, associating it with startup founders, venture capital, and rapid innovation. Today, the entrepreneur is often celebrated as a symbol of creativity, independence, and economic dynamism.

Despite its modern associations, the history of the word entrepreneur reveals that its core meaning has remained surprisingly consistent: it has always referred to individuals who undertake significant, uncertain, and often transformative projects. What has changed over time is the context in which these undertakings occur—from military expeditions to construction projects, from market speculation to technological innovation. The evolution of the word reflects the evolution of society itself, as new forms of economic and social organization have emerged.

In tracing the history of entrepreneur, we see not only the development of a word but also the development of an idea: that progress depends on individuals willing to take risks, challenge conventions, and seize opportunities. The term’s journey from medieval France to the global business lexicon of today underscores the enduring importance of human initiative in shaping the world.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Kirzner’s theory places the entrepreneur at the center of market coordination, arguing that markets function not because individuals possess perfect information, but because some individuals are alert to opportunities that others overlook. His work reframes the market as a dynamic, discovery‑driven process rather than a static system tending automatically toward equilibrium. In doing so, Kirzner offers a distinctive account of how coordination emerges in real-world economies marked by uncertainty, dispersed knowledge, and continual change.

At the heart of Kirzner’s framework is the concept of entrepreneurial alertness. Unlike definitions that portray entrepreneurs as innovators, risk‑bearers, or managers, Kirzner emphasizes the entrepreneur’s unique ability to notice previously unseen possibilities. This alertness is not a matter of deliberate search or specialized expertise; it is a readiness to perceive discrepancies in the market—unmet consumer demands, mispriced goods, or underutilized resources. When an entrepreneur recognizes such a discrepancy, they act to exploit it, and in doing so, they help correct the underlying error. This corrective action is what moves markets toward greater coordination.

Kirzner’s understanding of markets is inseparable from his view of knowledge. He argues that economic actors operate with incomplete and unevenly distributed information. No one possesses a full picture of the market, and errors are therefore inevitable. Yet these errors are not signs of market failure. Instead, they create the very conditions that make entrepreneurial discovery possible. The entrepreneur’s alertness allows them to detect what others have missed, and their actions reveal new information to the rest of the market. In this way, discovery is a social process: one person’s insight becomes a signal that guides the decisions of others.

This process is most clearly expressed through profit and loss, which Kirzner interprets as feedback mechanisms. Profit is the reward for having perceived an opportunity that others overlooked. It indicates that the entrepreneur has moved the market closer to a more coordinated state. Loss, by contrast, signals that the entrepreneur’s judgment was mistaken or that conditions have shifted. These signals are essential because they guide behavior without requiring any central authority. They allow countless individuals to adjust their plans in response to new information, creating a spontaneous order that no planner could design.

Kirzner’s theory also offers a distinctive view of competition. Rather than treating competition as a static state characterized by many firms producing identical goods, he describes it as a dynamic process of discovery. Entrepreneurs compete by being more alert than others—by noticing opportunities sooner or interpreting signals more effectively. This competitive process continually reshapes the market, pushing it toward greater coordination even as new opportunities and errors emerge. Competition, in Kirzner’s sense, is not a condition but an activity.

***

***

A key implication of this view is that markets are inherently open-ended. Because knowledge is never complete and conditions are always changing, the discovery process has no final equilibrium. Even if markets move toward coordination, new opportunities constantly arise. This makes the entrepreneur indispensable: without entrepreneurial alertness, markets would stagnate, and errors would persist uncorrected. The entrepreneur is the agent through whom markets learn.

Kirzner’s theory stands in contrast to other influential accounts of entrepreneurship. For example, while Schumpeter emphasizes innovation and “creative destruction,” Kirzner focuses on discovery and error correction. Schumpeter’s entrepreneur disrupts the market by introducing something fundamentally new; Kirzner’s entrepreneur restores coordination by recognizing what already exists but has not been noticed. These two views highlight different aspects of economic change, but Kirzner’s approach is more closely tied to the everyday functioning of markets and the continual adjustments that keep them coherent.

Kirzner’s insights also have implications for policy. Because entrepreneurial discovery depends on freedom of entry, flexible prices, and open competition, regulations that restrict these conditions can unintentionally suppress the discovery process. Barriers to entry reduce the number of individuals scanning the environment for overlooked opportunities. Price controls distort the signals that guide entrepreneurial judgment. Excessive regulation can therefore freeze the market in a state of uncorrected error. Kirzner does not argue that all regulation is harmful, but he warns that policymakers often underestimate the subtle, decentralized nature of discovery.

Ultimately, Kirzner’s theory presents a vision of markets as learning systems. Entrepreneurs are not heroic figures but ordinary individuals who happen to notice what others have missed. Their discoveries, guided by profit and loss, help coordinate the plans of millions of people who will never meet. Markets, in this view, are not perfect, but they are adaptive. They evolve through the continual interplay of error and discovery, ignorance and alertness. Kirzner’s contribution lies in showing that the true strength of markets is not their tendency toward equilibrium, but their capacity for self‑correction through entrepreneurial action.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A capital call is a notice sent to investors requesting that they contribute additional capital to a private equity fund. Capital calls are made when the fund manager has identified a new investment opportunity that requires additional funds.

Investors must be prepared to respond to capital calls with the required funds in a timely manner, as failure to do so could result in penalties or even the loss of their investment.

Carried Interest: Understanding the Concept

Carried interest is a form of incentive fee paid to private equity fund managers. This fee is calculated as a percentage of the profits generated by the fund’s investments.

Carried interest is often criticized as a tax loophole, as it is treated as capital gains, which are taxed at a lower rate than ordinary income.

Deal Flow: What it Means for Investors

Deal flow refers to the number of potential investment opportunities that a private equity firm evaluates. A robust deal flow is important for private equity firms, as it provides a pipeline of potential investments to consider.

Investors may want to investigate a private equity firm’s deal flow as part of their due diligence process, as a strong deal flow can indicate the firm has a good track record of finding attractive investment opportunities.

Due Diligence: A Key Step in Private Equity Investing

Due diligence is the process of evaluating a potential investment opportunity to assess its viability. This process involves a thorough investigation of the company’s financials, operations, and management team.

Due diligence is a critical step in the private equity investment process, as it helps to identify potential risks associated with an investment opportunity. Investors who skip due diligence do so at their own risk.

Exit Strategy: How Private Equity Firms Make Money

Exit strategy refers to the plan that private equity firms have in place to cash out of their investments. Private equity firms typically exit investments through an initial public offering (IPO), a sale to another company, or a management buyout.

Exit strategy is critical to the private equity investment process, as it is how investors ultimately make returns on their investments.

Fund of Funds: An Overview

A fund of funds is a type of investment fund that invests in other investment funds. In the private equity space, fund of funds typically invest in a portfolio of private equity funds.

Fund of funds can be a good way for investors to gain exposure to a wider range of private equity investments with less risk than investing in individual funds.

General Partner vs Limited Partner: What’s the Difference?

The general partner is the party responsible for managing the private equity fund and making investment decisions. Limited partners, on the other hand, are typically passive investors who provide capital but have little involvement in the investment process.

The distinction between general partners and limited partners is important for investors to understand, as it can impact their level of involvement in the investment process.

Investment Horizon: A Crucial Factor in Private Equity Investments

Investment horizon refers to the length of time an investor plans to hold an investment. In the private equity space, investment horizons can be several years or even a decade.

Investment horizon is a critical factor for investors to consider, as it impacts the level of liquidity they will have and the returns they can expect to make on their investment.

Leveraged Buyout (LBO): Definition and Examples

A leveraged buyout is a type of acquisition where the acquiring company uses a significant amount of debt to finance the purchase. The idea is that the acquired company’s assets will be used as collateral to secure the debt.

Leveraged buyouts can be an effective way for private equity firms to acquire companies with minimal capital investment. However, the use of leverage also increases the risk associated with these types of acquisitions.

Management Fee vs Performance Fee: Understanding the Two

The management fee is the fee paid to the general partner for managing the private equity fund. The performance fee, or carried interest, is paid based on the fund’s performance and returns generated for investors.

The distinction between management fees and performance fees is important for investors to understand, as it affects the level of fees they will be responsible for paying.

Pitchbook: A Guide to Creating an Effective Pitchbook

A pitchbook is a presentation used by private equity firms to pitch their investment strategy to potential investors. An effective pitchbook should be clear, well-organized, and provide a compelling rationale for why investors should consider investing in the fund.

Investors reviewing a fund’s pitchbook should look for evidence of a well-thought-out investment strategy and a track record of successful investments.

Private Placement Memorandum (PPM): What it is and Why It Matters

A private placement memorandum is a legal document provided to potential investors that details the terms of the private equity fund. It includes information on the fund’s investment strategy, expected returns, fees, and risks associated with the investment.

Reviewing a fund’s private placement memorandum is a critical step in the due diligence process, as it provides investors with a comprehensive understanding of the investment opportunity.

Recapitalization: A Strategy for Restructuring a Company

Recapitalization is a strategy used by private equity firms to restructure a company’s capital structure. This can involve issuing debt to pay off equity holders or issuing equity to pay off debt holders.

Recapitalization is often used to improve a company’s financial position and increase its value, making it a key tool in the private equity arsenal.

Valuation Techniques Used in Private Equity Investing

Valuation techniques are used to determine the value of a private company. These techniques can include discounted cash flow analysis, market multiples analysis, and asset-based valuation.

Understanding valuation techniques is important for investors, as it allows them to evaluate the relative value of investment opportunities and make informed investment decisions.

Posted on February 1, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

In Healthcare

Monopsony and Oligopsony occur when discounts are extracted from healthcare providers because of supply and demand size inequalities, and may run afoul of anti-trust laws.

Many medical providers have monopoly or near-monopoly power, yet antitrust laws prevent some potentially beneficial integration.

***

Introduction

Monopsony and oligopsony are two terms that are often used interchangeably, but they are not the same thing.

Monopsony refers to a market structure where there is only one buyer of a certain product or service, while oligopsony refers to a market structure where there are only a few buyers of a certain product or service.

In this ME-P, we will explore the differences between these two market structures and their implications.

The main difference between monopsony and oligopsony is the number of buyers in the market. In a monopsony, there is only one buyer, which gives them significant bargaining power over the suppliers. In contrast, an oligopsony has a few buyers, which means that the suppliers have some bargaining power, but not as much as they would in a perfectly competitive market.

For example, the government is often the only buyer of certain goods and services, such as military equipment, healthcare [ACA] or public transportation. This gives them significant bargaining power over the suppliers, who have no other buyers to turn to. On the other hand, the automobile industry is an example of an oligopsony, with a few large manufacturers controlling the majority of the market. Suppliers have some bargaining power, but they still have to compete for contracts with the few buyers in the market.

2. Price Setting

In a monopsony, the buyer has the power to set the price of the product or service. Since there is only one buyer, the suppliers have no choice but to accept the price offered. This can lead to lower prices for the buyer, but it can also lead to lower quality products or services, as suppliers may cut corners to meet the buyer’s demands.

In an oligopsony, the buyers have some bargaining power, but they still have to compete with each other for the best deals. This can lead to higher prices for the suppliers, but it can also lead to higher quality products or services, as suppliers have more resources to invest in their products.

3. Competition

One of the main advantages of a perfectly competitive market is the competition between buyers and sellers. This competition leads to better prices and higher quality products or services. In a monopsony, there is no competition between buyers, which can lead to lower quality products or services and higher prices for the suppliers.

In an oligopsony, there is some competition between buyers, which can lead to better prices and higher quality products or services. However, the competition is limited to a few buyers, which means that suppliers have less choice and bargaining power than they would in a perfectly competitive market.

The implications of monopsony and oligopsony depend on the specific market and the parties involved. In general, monopsony can lead to lower prices for the buyer, but it can also lead to lower quality products or services and reduced innovation. Oligopsony can lead to higher prices for the suppliers, but it can also lead to higher quality products or services and increased innovation.

Conclusion

Monopsony and oligopsony are two different market structures with different implications for buyers and suppliers. While monopsony can lead to lower prices for the buyer, it can also lead to reduced quality and innovation. Oligopsony can lead to higher prices for the suppliers, but it can also lead to higher quality and increased innovation.

The best option depends on the specific market and the parties involved.

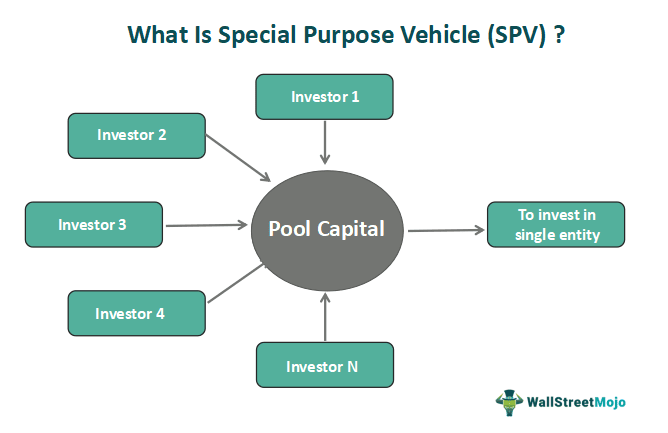

Its purpose is to isolate the parent company from any potential credit or financial risk that may arise from the SPV and is often used to pursue riskier projects, securitize debt, or transfer assets. Since an SPV is separate from the parent company, it isn’t affected by the parent’s performance, and the parent isn’t typically affected by the performance of the SPV. If the parent goes bankrupt and is no longer in existence, the SPV can carry on.

This makes an SPV bankruptcy remote. This also means that the parent company is unaffected by the loss if the SPV fails.

Posted on February 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITIONS

By SBA and Staff Reporters

***

***

Acquisition

The acquiring of supplies or services by the federal government with appropriated funds through purchase or lease.

Affiliates

Business concerns, organizations, or individuals that control each other or that are controlled by a third party. Control may include shared management or ownership; common use of facilities, equipment, and employees; or family interest.

Best and Final Offer

For negotiated procurements, a contractor’s final offer following the conclusion of discussions.

Certificate of Competency

A certificate issued by the Small Business Administration (SBA) stating that the holder is “responsible” (in terms of capability, competency, capacity, credit, integrity, perseverance, and tenacity) for the purpose of receiving and performing a specific government contract.

Certified 8(a) Firm

A firm owned and operated by socially and economically disadvantaged individuals and eligible to receive federal contracts under the Small Business Administration’s 8(a) Business Development Program.

Contract

A mutually binding legal relationship obligating the seller to furnish supplies or services (including construction) and the buyer to pay for them.

Contracting

Purchasing, renting, leasing, or otherwise obtaining supplies or services from nonfederal sources. Contracting includes the description of supplies and services required, the selection and solicitation of sources, the preparation and award of contracts, and all phases of contract administration. It does not include grants or cooperative agreements.

Contracting Officer

A person with the authority to enter into, administer, and/or terminate contracts and make related determinations and findings.

Contractor Team Arrangement

An arrangement in which (a) two or more companies form a partnership or joint venture to act as potential prime contractor; or (b) an agreement by a potential prime contractor with one or more other companies to have them act as its subcontractors under a specified government contract or acquisition program.

Defense Acquisition Regulatory Council (DARC)

A group composed of representatives from each Military department, the Defense Logistics Agency, and the National Aeronautics and Space Administration and that is in charge of the Federal Acquisition Regulation (FAR) on a joint basis with the Civilian Agency Acquisition Council (CAAC).

Defense Contractor

Any person who enters into a contract with the United States for the production of material or for the performance of services for the national defense.

Electronic Data Interchange

Transmission of information between computers using highly standardized electronic versions of common business documents.

Emerging Small Business

A small business concern whose size is no greater than 50 percent of the numerical size standard applicable to the Standard Industrial Classification code assigned to a contracting opportunity.

Equity

An accounting term used to describe the net investment of owners or stockholders in a business. Under the accounting equation, equity also represents the result of assets less liabilities.

Fair and Reasonable Price

A price that is fair to both parties, considering the agreed-upon conditions, promised quality, and timeliness of contract performance. “Fair and reasonable” price is subject to statutory and regulatory limitations.

Federal Acquisition Regulation (FAR)

The body of regulations which is the primary source of authority governing the government procurement process. The FAR, which is published as Chapter 1 of Title 48 of the Code of Federal Regulations, is prepared, issued, and maintained under the joint auspices of the Secretary of Defense, the Administrator of General Services Administration, and the Administrator of the National Aeronautics and Space Administration. Actual responsibility for maintenance and revision of the FAR is vested jointly in the Defense Acquisition Regulatory Council (DARC) and the Civilian Agency Acquisition Council (CAAC).

Full and Open Competition

With respect to a contract action, “full and open” competition means that all responsible sources are permitted to compete.

Intermediary Organization

Organizations that play a fundamental role in encouraging, promoting, and facilitating business-to-business linkages and mentor-protégé partnerships. These can include both nonprofit and for-profit organizations: chambers of commerce; trade associations; local, civic, and community groups; state and local governments; academic institutions; and private corporations.

Joint Venture

In the SBA Mentor-Protégé Program, an agreement between a certified 8(a) firm and a mentor firm to perform a specific federal contract.

Mentor

A business, usually large, or other organization that has created a specialized program to advance strategic relationships with small businesses.

Negotiation

Contracting through the use of either competitive or other-than-competitive proposals and discussions. Any contract awarded without using sealed bidding procedures is a negotiated contract.

Partnering

A mutually beneficial business-to-business relationship based on trust and commitment and that enhances the capabilities of both parties.

Prime Contract

A contract awarded directly by the Federal government.

Protégé

A firm in a developmental stage that aspires to increasing its capabilities through a mutually beneficial business-to-business relationship.

Request for Proposal (RFP)

A document outlining a government agency’s requirements and the criteria for the evaluation of offers.

SCORE

Counselors to America’s Small Business is a 12,400-member volunteer association sponsored by the SBA. SCORE matches volunteer business-management counselors with present prospective small business owners in need of expert advice.

Small Business

A business smaller than a given size as measured by its employment, business receipts, or business assets.

Small Business Development Centers (SBDC)

SBDCs offer a broad spectrum of business information and guidance as well as assistance in preparing loan applications.

Small Business Innovative Research (SBIR) Contract

A type of contract designed to foster technological innovation by small businesses with 500 or fewer employees. The SBIR contract program provides for a three-phased approach to research and development projects: technological feasibility and concept development; the primary research effort; and the conversion of the technology to a commercial application.

Small Disadvantaged Business Concern

A small business concern that is at least 51 percent owned by one or more individuals who are both socially and economically disadvantaged. This can include a publicly owned business that has at least 51 percent of its stock unconditionally owned by one or more socially and economically disadvantaged individuals and whose management and daily business is controlled by one or more such individuals.

Standard Industrial Classification (SIC) Code

A code representing a category within the Standard Industrial Classification System administered by the Statistical Policy Division of the U.S. Office of Management and Budget. The system was established to classify all industries in the US economy. A two-digit code designates each major industry group, which is coupled with a second two-digit code representing subcategories.

Subcontract

A contract between a prime contractor and a subcontractor to furnish supplies or services for the performance of a prime contract or subcontract.

Posted on September 22, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

WHAT IS IT?

On an earnings call last year Microsoft CEO Satya Nadella said the term “enterprise metaverse.”

By [Avatar] Dr. David Edward Marcinko MBA

DEFINITION: The Metaverse is a collective virtual shared space, created by the convergence of virtually enhanced physical reality and physically persistent virtual space, including the sum of all virtual worlds, augmented reality, and the Internet.

The word “metaverse” is made up of the prefix “meta” (meaning beyond) and the stem “verse” (a back formation from “universe“); the term is typically used to describe the concept of a future iteration of the internet, made up of persistent, shared, 3D virtual spaces linked into a perceived virtual universe.

Posted on August 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Free Market Medical Association

*** DEFINITION: Direct Primary Care (DPC) is an innovative alternative payment model improving access to high functioning healthcare with a simple, flat, affordable membership fee. No fee-for-service payments. No third party billing. The defining element of DPC is an enduring and trusting relationship between a patient and his or her primary care provider. Patients have extraordinary access to a physician of their choice, often for as little as $70 per month, and physicians are accountable first and foremost their patients. DPC is embraced by health policymakers on the left and right and creates happy patients and happy doctors all over the country!

Posted on October 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Try (or learn about) Entrepreneurship

BY DR. DAVID EDWARD MARCINKO MBAMEdCMP®

One of the greatest things about the virtual economy is the expanded opportunity for people to branch out on their own and create something using their own expertise. Related to this is the growing societal desire to have more free time and a more balanced, efficient life overall.

In fact, years ago when I was in business school, I learned that during a recession when jobs were sparse – folks would either go back to school to re-engineer and re-educate OR start their own business.

Today – If the pandemic taught us anything, it’s that we need to be able to pivot when circumstances call for it. In the years ahead, there will be a premium on flexibility, portability, and improvisation; knowing how to earn income outside the traditional employer-employee relationship will continue to be an especially valuable skill.

ASSESSMENT: So, if you are a physician, nurse, medical professional or financial advisor in the healthcare space, think about what you’re naturally good at (or at least interested in), and determine if there’s an opportunity to monetize it in some way on your own. Your career might thank you for it!