BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

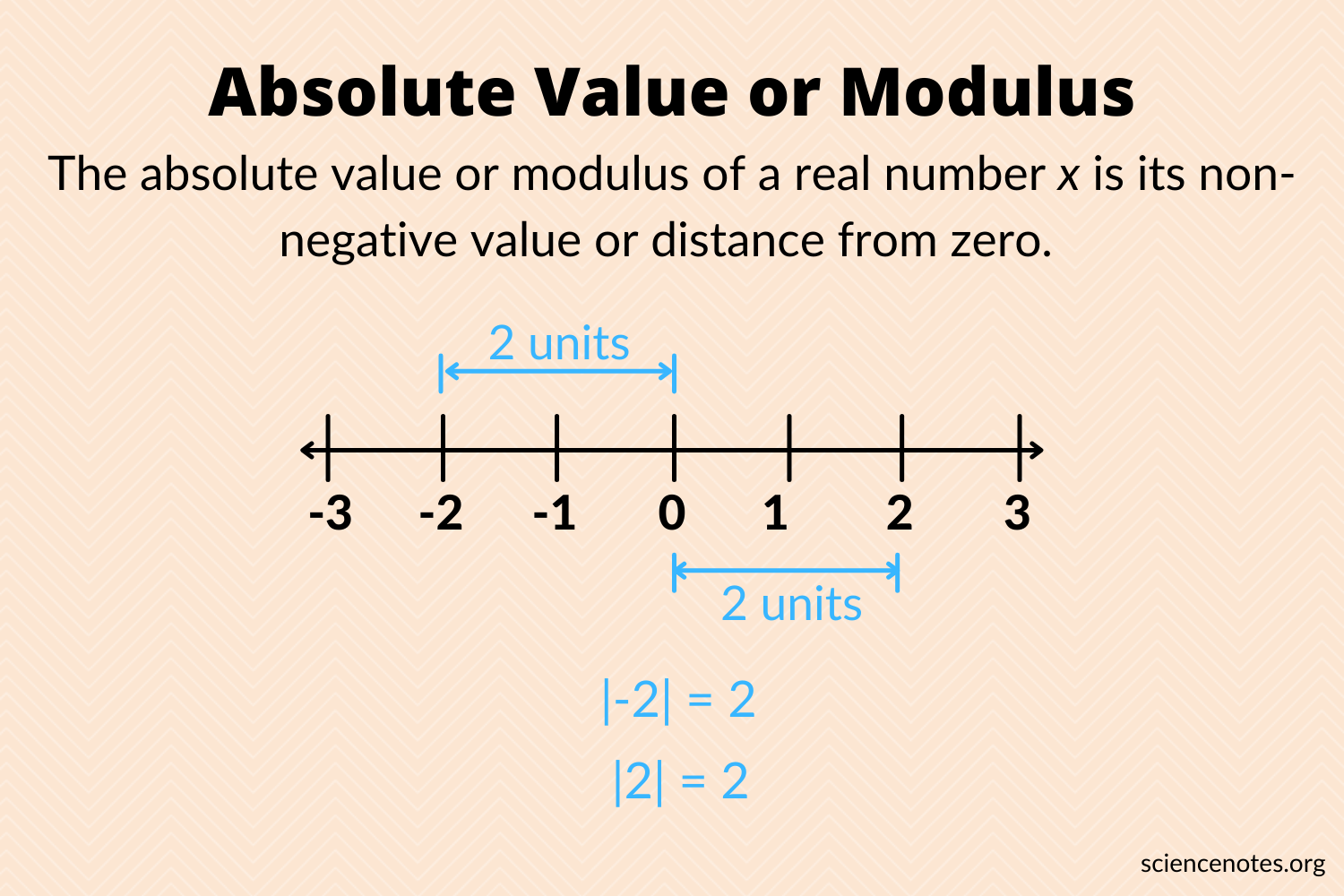

In mathematics, the absolute value or modulus of a real number x, denoted |x|, is the non-negative value of x without regard to its sign. Namely, |x| = x if x is positive, and |x| = −x if x is negative (in which case −x is positive), and |0| = 0. For example, the absolute value of 3 is 3, and the absolute value of −3 is also 3. The absolute value of a number may be thought of as its distance from zero.

***

In finance, absolute value, also known as an intrinsic value, refers to a business valuation method that uses discounted cash flow (DCF) analysis to determine a company’s financial worth. The absolute value method differs from the relative value models that examine what a company is worth compared to its competitors. Absolute value models try to determine a company’s intrinsic worth based on its projected cash flows.

Absolute value refers to a business valuation method that uses discounted cash flow analysis to determine a company’s financial worth.

Investors can determine if a stock is currently under or overvalued by comparing what a company’s share price should be given its absolute value to the stock’s current price.

There are some challenges with using the absolute value analysis including forecasting cash flows, predicting accurate growth rates, and evaluating appropriate discount rates.

Absolute value, unlike relative value, does not call for the comparison of companies in the same industry or sector.

Capitated reimbursement is predominantly, but not exclusively, within the realm of physician providers. But, a decade ago Community Nursing Organization project examined an innovative approach to community nursing and ambulatory care services for Medicare beneficiaries. The hypothesis was that provision of such services would promote the timely and appropriate use of health care and to reduce the use of costly acute care services.

Organizations participating in the CNO demonstration were paid a fixed per-member-per-month capitated rate for covered services. But, the participating CNOs were only at risk under capitation for a subset of Medicare benefits [partial-capitation or carve-out]. The financial incentive was to minimize utilization covered under the capitated payment, but not necessarily to minimize utilization of services not covered because traditional Medicare, not the CNO, would be at risk.

Assessment

Final results indicated that the CNO model under partial capitation led to increased Medicare costs based on findings consistent across several analytic approaches. The cost differences between treatment and control or reference groups persisted after the application of increasingly complex risk-adjustment methods.

Moreover, the differences increased over time and were robust to changes in the way CNO participation was defined.

Lastly, there was no statistically significant evidence of increase in physical or social functioning of the treatment group, as compared with the control group. CNOs cost more without providing any health benefits along dimensions measured

[Source: Voluntary Partial Capitation: The CNO Medicare Demonstration Project, Austin Frakt, Steve Pizer, Robert Schmitz, and Soeren Mattke – Health Care Financing Review 2005).

Now – Trading individual bonds is not like trading stocks. Stocks can be bought at uniform prices and are traded through exchanges. Most bonds trade over the counter, and individual brokers price them. But, price transparency has gotten better in the last decade.

For example, in 1999, the bond markets gained clearness from the House of Representatives’ Bond Price Competition Improvement Act of 1999. Responding to this pioneering law, the site http://www.investinginbonds.com was established. This site provides current prices on bonds that have traded more than four times the previous day. With the advent of Investinginbonds.com and real-time reporting of many trades, investors are much better off today. Many well regarded brokers including Schwab, Ameritrade, and Fidelity Investments now have dedicated websites devoted to bond trading and pricing.

Fidelity Investments chose to disclose its fee structure for all bonds, making it clear what it will cost you per trade. Fidelity charges $1 per bond trade. Some on-line brokers charge a flat fee as well, ranging from $10.95 at Zions Direct to $45 at TD Ameritrade. Depending on the number of bonds trading, one may be more complimentary than another. The trading fee disclosures, however, do not divulge the spreads between the buy and sell price embedded in the transaction that some dealer is making in the channel. Keep in mind that only by comparison shopping can assist you in finding the best transaction price, after all fees are taken into account. Other sites may not charge any fee, but rather embed the profit in the spread.

Despite the difficulty in pricing and transparency, investing in individual bonds offers several rewards over purchasing bond mutual funds.

First, bond mutual funds never mature.

Second, you know exactly what you will be receiving in interest each year. You will also know the exact maturity date.

Furthermore, your individual investment is protected against interest rate risk, at least over the full term to maturity. Both individual bonds and bond funds share interest-rate risk (the risk of locking up an investment at a given rate, only to see rates rise). This pushes bond prices down. At least with an individual bond, you can re-invest it at the higher, market rate once the bond matures.

But, the lack of a fixed maturity date on a bond mutual fund causes an open ended problem; there is no promise of the original investment back. Short of default, an individual bond will return all principal and pay all interest assuming you hold it to maturity. Bond funds are not likely to default as most funds maintain positions in hundreds of individual bonds. The force of interest rate risk to individual bond or bond mutual fund prices depends on the maturity of a bond investment: the longer the maturity of a bond or bond fund (average), the more the price will drop due to rising rates. This is known as duration.

Duration is a statistical term that measures the price sensitivity to yield, is the primary measurement of a bond or bond fund’s sensitivity to interest rate changes. Duration indicates approximately how much the price of a bond or bond fund will adjust in the reverse direction given a rise in interest rates. For instance, an individual bond with an average duration of five years will fall in value approximately 5% if rates rise by 1% and the opposite is accurate as well.

Although stated in years, duration is not simply a gauge of time. Instead, duration signals how much the price of your bond investment is likely to oscillate when there is an up or down movement in interest rates. The higher the duration number, the more susceptible your bond investment will be to changes in interest rates. If you have money in a bond or bond fund that holds primarily long-term bonds, expect the value of that fund to decline, perhaps significantly, when interest rates rise. The higher a bond’s duration, the greater its sensitivity to interest rates alterations. This means fluctuations in price, whether positive or negative, will be more prominent.

For example, a bond fund with 10-year duration will diminish in value by 10 percent if interest rates increase by one percent. On the other hand, the bond fund will rise in value by 10 percent if interest rates descend by one percent. The important concept to remember is once you recognize a bond’s or bond fund’s duration, you can forecast how it will react to a change in interest rates.

UPDATE:

The yield on the 10-year Treasury note serves as a benchmark for interest rates across the US economy. Since bond prices and yields move in opposite directions, falling yields signal higher demand for Treasuries.

Why it matters: At the most basic level, the 10-year yield is a key indicator of investors’ confidence in future US economic growth. As the Delta variant spreads and threatens to slow the economic recovery, the fall in yields means investors are souring on a mega growth spurt and snapping up safer assets rather than riskier stocks.

What does this mean for inflation? Because investors sell bonds when they think inflation is coming, the runup in bond prices means the worst of Wall Street’s inflation concerns may be over. “It feels like we have moved from thinking inflation will be transitory, to fearing growth will be transitory,” Art Hogan, chief marketing strategist at National Securities, said.

Colleagues know that I enjoy personal coaching and public speaking and give as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These include lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, keynote lectures at city and statewide financial coalitions, and annual keynote lectures for a variety of internal yearly meetings.

Colleagues know that I enjoy personal coaching and public speaking and give as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These include lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, keynote lectures at city and statewide financial coalitions, and annual keynote lectures for a variety of internal yearly meetings.

Colleagues know that I enjoy personal coaching and public speaking and give as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These include lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, keynote lectures at city and statewide financial coalitions, and annual keynote lectures for a variety of internal yearly meetings.

Colleagues know that I enjoy personal coaching and public speaking and give as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These include lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, keynote lectures at city and statewide financial coalitions, and annual keynote lectures for a variety of internal yearly meetings.

Colleagues know that I enjoy personal coaching and public speaking and give as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These include lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, keynote lectures at city and statewide financial coalitions, and annual keynote lectures for a variety of internal yearly meetings.

NOTE: The US debt-ceiling bill just passed, June 1, 2023. So, here are some budgeting rules for doctors and medical professionals.

***

Budgeting is probably one of the greatest tools in building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle. This includes living in an exclusive neighborhood, driving an expensive car, wearing imported suits and a fine watch, all of which do not lend themselves to expense budgeting. Only one in ten medical professionals has a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination.

The following guidelines will assist in this microeconomic endeavor:

Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home, or in the office. Deposit it in a money market account for safety and interest.

Do not pay bills early, do not have more taxes withheld from your salary than you owe, and develop spending estimates and budget fixed expenses first. Fixed expenses are usually contractual, and may include housing, utilities, food, telephone, social security, medical, debt repayment, homeowner’ or renter’s insurance, auto, life and disability insurance, and maintenance, etc.

Make variable expenses a priority. Variable expenses are not usually contractual, and may include clothing, education, recreational, travel, vacation, gas, entertainment, gifts, furnishings, savings, investments, etc.

Trim variable expenses by 10-15 percent, and fixed expenses, when possible. Ultimately, all fixed expenses get paid and become variable in the long run.

Use carve-out or set-asides for big ticket items and differentiate “wants from needs.”

Know the difference between saving and investing. Savers tend to be risk adverse and investors understand risk and takes steps to mitigate it.

Determine shortfalls or excesses with the budget period.

Track actual expenses.

Calculate both income and expenses as a percentage of the total, and determine if there is a better way to allocate resources. Then, review the budget on a monthly basis to determine if there is a variance. Determine if the variance was avoidable, unavoidable, or a result of inaccurate assumptions, and take needed corrective action.

***

Verify Your Budget and Follow a Financial Plan

The process of establishing a budget relies heavily on guesswork, and the use of software or “apps”, that seamlessly track expenditures and help your budget and your financial plan become more of reality. Most doctors underestimate their true expenses, so lumping and best guesses on expense usually prove very inaccurate. Personal financial software and mobile phone applications make the verification of budgets easier. Once your personal accounts are setup, free apps like MINT.com will let give you a detailed report on where your money is going and the adjustments you must make. Few professions make larger contributions to the Internal Revenue Service than physicians and the medical profession. It is very important to categorize different budget categories not only to be proactive about your expenses, but also to accurately reflect the effect your different expenditures have on your real savings capability. All expense dollars are not equal.

For example, a mortgage payment, which is mostly interest expense in the early years, is likewise mostly tax deductible. Spending money on your family vacation is typically not tax deductible. Itemized deductions, which are deductions that a US taxpayer can claim on their tax return in order to reduce their Adjustable Gross Income (AGI), may include such costs as property taxes, vehicle registration fees, income taxes, mortgage expense, investment interest, charitable contributions, medical expenses (to the extent the expenses exceed 10% of the taxpayers AGI) and more.

Employing a qualifiedcertified medical planneR® that utilizes a cash-flow based financial planning software program may help the physician identify their actual after-tax projected cash flow and more accurately plan their future.

Posted on April 2, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

All about the Medical Executive-PostBusiness Model

***

One of the questions we receive most often from readers of the Medical Executive-Post is how can we “afford” to give away so much content for free. Or stated another way, “how do we get paid for all of this?”

The simple answer is that we know many (or even most) of you will simply take the ideas that we share and implement them yourself. Do-It-YourSelfers can always simply purchase our texts, books and peer reviewed handbooks redacted in more than a thousand, medical, law, business and graduate schools, as well as the Library of Congress,Institute of Health and Library of Congress.

On the other hand, some of you will realize you need some additional help.

For example:

Maybe as a financial advisor you’re “stuck” in your financial planning business and recognize that some outside assistance is necessary to help you get to the next level of niche specificity thru our Certified Medical Planner™ chartered certification program designation. Helping physicians of all specialty types in a fiduciary focused manner is the proverbial Win-Win for all concerned.

OR, perhaps you are seeking a glossary of terms and definitions in heath economics, finance, accounting, insurance, managed care, health information technology and security; found in our Health Dictionary Series Wiki Project? Free and print versions are available.

OR, as a doctor maybe your medical practice is growing so much you just hit a wall where you don’t have time to do it all for your patients. After all, with only “so much” time available every day and week, it’s vital to delegate or outsource anything that isn’t really core to your practice and management skill set.

OR, maybe you are even starting, buying or selling your medical practice and need our financial and valuation services. Part (1) – Part (2) – Part (3) Financial, estate, investing and retirement planning services are also available.

OR, you may just need a second informed opinion about a topic not listed; there are a myriad of issues to consider in the competitive ecosystem today.

So, in the meantime, I hope that the ME-P content continues to be helpful food for thought, and perhaps we’ll have an opportunity to cross paths soon at a future conferences or podcasts. Feel free to invite us to speak at your own seminar/podcast online V-log, as well.

It is not uncommon for practicing physicians to have more than a dozen separate insurance policies to protect their medical practice and personal assets. Yet, most doctors understand very little about their policies.BOOK REVIR

Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors: Best Practices from Leading Consultants and Certified Medical Planners™explains to physicians and insurance professionals the background, theory, and practicalities of medical risk management, asset protection methods, and insurance planning.

The book presents information in a manner that is convenient and highly useful for busy medical practitioners. It discusses the medical records revolution and addresses concerns regarding cloud computing, data security, and technological threats.

The book covers modern health law and policy, including fraud and abuse, workplace-violence, Medicare compliance, HIPAA regulations, AR protection strategies with internal controls, P4P and value based care, insurance and reputation management, and how the ARA legislation is impacting physician practices. It also includes case models and examples that provide you with a real-world understanding of how to recognize and reduce personal and medical practice risks.

With time at a premium for all, and so much information packed into one well-organized resource, this book is a must-read for every physician and financial advisor that serves the health care sector. The book will help physicians make better decisions about the risks they face and will help financial advisors improve the value they provide to their clients who are doctors.

Did you know that most experts recommend against naming a practice with your own name because it limits future growth and you may lose the benefits that a more descriptive name would bring?

Your business name will likely be incorporated using your practice’s name, although larger (multi-specialty group) practices may use a more general name for the entire enterprise; and then having multiple “dba’s” (”Doing Business As”) for the individual practices under the umbrella. It is important to discuss these options with an attorney if you believe this arrangement has advantage; others find it confusing.

Usually, your medical specialty can be used as a base-name, and then some descriptor to differentiate it from local competing practices. Selecting a name like “The Allegiance Partners” does not indicate that medicine is your service. On the other hand, naming your practice “Podiatry Associates of Your Town” won’t be helpful to patients looking for you in the yellow pages, health insurance provider network list, or internet search engines, and finding your practice listed just before “Your Town Podiatry Partners”. It is therefore good to be cognizant of your competitors’ names when choosing your own. And, you should select a name that will hopefully grow with you into a larger enterprise.

For example, are you a solo doctor, but are pretty sure you’ll take on one or more partners in the future? Then besides not naming your practice after yourself, you may choose to add “Group” or “Partners” to your name initially even if you’re the only doctor. Is there any possibility you’ll open a second office in another town? Naming your medical practice something like the ”Apple Street Internal Medicine Group” may not make sense when your second office is opened on Main Street in a nearby city, in a few years.

Order Forms and Practice Stationary

Orders forms, invoices, purchase and estimate forms, business cards, envelopes, stationary and specialty labels can all be personalized for your medical practice name, script, colors and logo. Often, local or regional printers are the most cost effective and you support another entrepreneur, as well.

Posted on December 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Colleges and Universities

TO H.R. RECRUITERS, UNIVERSITY HIRING MANAGERS & SEARCH COMMITTEES

Sooth My Academic Teaching and Classroom Withdrawal Pangs!

I’m screening for my next university Dean, Chair or teaching Professorship opportunity.

Currently, an endowed Resident-Scholar completing a text book production assignment complete with aligned case models, tests, quizzes, rubrics, curriculum teaching portfolio, and accreditation review.

Two-decades of domestic and international teaching experience and credentials in health economics, finance, investing, business, policy, risk management, IT and administration. Hundreds of peer-reviewed and trade publications [TNTC] with 30 major textbooks redacted in more than a thousand university libraries [NIH, Library of Congress and National Institute Health, etc]. Public and population health global speaker and thought leader. Wall Street experience as start-up founder, entrepreneur and CXO.

Ideal mentor for under graduate thru post-doctoral and fellowship students [PhD, DBA, MD/DO, MHA and MBA, etc].

Compensation important, but fit is paramount as servant-leader. [+] RANKED: Google Scholar and “H” Index CV available upon request.

The IHS provides health care in 36 states to approximately 2.2 million out of 3.7 million American Indians and Alaska Natives (AI/AN). As of April 2017, the IHS consisted of 26 hospitals, 59 health centers, and 32 health stations. Thirty-three urban Indian health projects supplement these facilities with a variety of health and referral services. Several tribes are actively involved in IHS program implementation. Many tribes also operate their own health systems independent of IHS. It also provides support to students pursuing medical education in order staff Indian health programs.

***

EDITOR’S NOTE: I did a rotation at a Federally Qualified Health Center through the I.H.S. when I was a surgical fellow back in the day. I enjoyed it immensely. Consulting services since then.

Posted on June 19, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

REALLY?

By Dr. David Edward Marcinko MBA

***

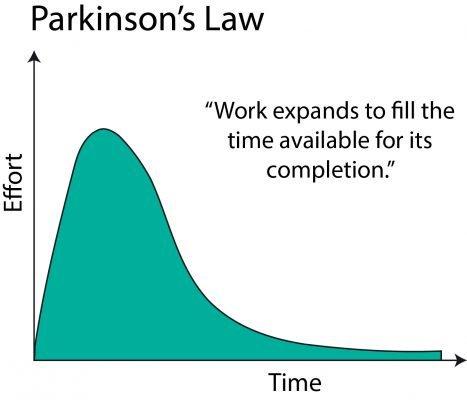

The business cycle is also known as the economic cycle and reflects the expansion or contraction in economic activity. Understanding the business cycle and the indicators used to determine its phases may influence investment or economic business decisions and financial or medical planning expectations.

Although often depicted as the regular rising and falling of an episodic curve, the business cycle is very irregular in terms of amplitude and duration. Moreover, many elements move together during the cycle and individual elements seldom carry enough momentum to cause the cycle to move.

However, elements may have a domino effect on one another, and this is ultimately drives the cycle, too. We can also have a large positive cycle, coincident with a smaller but still negative cycle, as may be seen in the current healthcare climate of today.

First Phase: Trough to Recovery (service and production driven)

Scenario: A depressed GNP leads to declining industrial production and capacity utilization. Decreased workloads result in improved labor productivity and reduced labor (unit) costs until actual producer (wholesale) prices decline.

Second Phase: Recovery to Expansion (patient and consumer driven)

Scenario: CPI declines (due to reduced wholesale prices) and consumer real income rises, improving consumer sentiment and actual demand for consumer goods.

Third Phase: Expansion to Peak (service and production driven)

Scenario: GNP raises leading to increased industrial production and capacity utilization. But, labor productivity declines and unit labor costs and producer (wholesale) prices rise.

Fourth Phase: Peak to Contraction (patient and consumer driven)

Scenario: CPI rises making consumer real income and sentiment erode until consumer demand, and ultimately purchases, shrink dramatically. Recessions may occur and economists have an alphabet used to describe them.

For example, with a “V” graph shape, the drop and recovery is quick. For a “U” shaped graph, the economy moves up more sluggishly from the bottom. A “W” is what you would expect: repeated recoveries and declines. An “L” shaped recession describes a prolonged dry economic spell or even depression.

The Physician Executive Summary is always included at the beginning of a formal business plan and represents a brief synopsis of the medical prarctice entire plan. Its appearance, grammar and style should be sharp and crisp as it represents an enticement for the reader to maintain interest and contribute intelligent or economic input into the new venture.

It should contain information about the practice, advertising and marketing opportunities, physician management, proposed financing with four Pro Forma financial statements, business operations and exit strategy. This last point, while unpleasant is often overlooked by naive practitioners. Business experts however, look favorably upon an escape plan and view it as the mark of mature professional that realizes the possibility of success as well as failure.

****

***

Ultimately, the plan must explain to potential investors how you will make the practice profitable and produce the required Return on Investment (ROI) for them. It must describe medical services, patient acceptance and benefits, provider qualifications and accomplishments, the amount of capital required, market size, potential practice growth rate, and market niche.

Additional information may include office location, proximity to labor, transportation, license requirements, business entity status, proprietary technology and potential working agreements with various insurance, managed care, ACA and HMO plans. If all of the above seems bewildering to the uninitiated, you are correct.

Remember however, that if you do not have, or can’t borrow the funds to begin a private practice, you will just have to become an employed practitioner until you can. It is therefore imperative to start off on the right foot, with a sound business plan, as you begin your medical career.

Whether you do contract work or have your own small business, tax deductions for the self-employed physician consultant and/or medical executive or nurse consultant, etc., can add up to substantial tax savings.

With self-employment comes freedom, responsibility, and a lot of expense. While most self-employed people celebrate the first two, they cringe at the latter, especially at tax time. They might not be aware of some of the tax write-offs to which they are entitled.

When it comes time to file your returns, don’t hesitate to claim the benefits you get for being the boss. As a self-employed success story, you’ve earned them.

FORM 1099NEC: Form 1099 NEC is one of several IRS tax forms used in the United States to prepare and file an information return to report various types of income other than wages, salaries, and tips. The term information return is used in contrast to the term tax return although the latter term is sometimes used colloquially to describe both kinds of returns.

“Many times an overlooked deduction is educational expenses. If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Individual Retirement Plans (IRAs)

One of the best tax write-offs for the self-employed physician consultant is a retirement plan. A person with no employees can set up an individual 401 (k). “You can contribute $19,500 in 2021 as a 401(k) deferral, plus 25 percent of net income.”

If you have employees, consider a SIMPLE (Savings Incentive Match Plan for Employees) IRA—an IRA-based plan that gives small employers a simplified method to make contributions to their employees’ retirement. As of 2021, an employee may defer up to $13,500 and employees over 50 may contribute an additional $3,000.

“A third retirement plan is Simplified Employee Pension IRA (SEP IRA).” The employer may contribute the lesser of 25 percent of income or $58,000 in 2021. If the employer has eligible employees, an equal percentage of their income must be contributed.

Recall that retirement plans are “absolutely the No. 1 tax deduction. The government is helping fund retirement.”

Business use of home or dwelling

Now, most self-employed taxpayers’ businesses start as home-based businesses. These people need to know portions of business costs are deductible and so “It is very important that you keep track of expenses relating to your housing costs.”

If your gross income from your business exceeds your total expenses, then you can deduct all of your expenses related to the business use of your home. If your gross income is less than your total expenses, your deduction will be limited to the difference between your gross income and the sum of all business expenses you would pay if the business was not in your home. Those expenses could include telephone lines, the Internet, and other costs to do business.

You must also have a home office that is truly used for work and the Internal Revenue Service may require you to document this.

***

Deducting automobile expenses

If you travel for business, even short distances within your own city, you may deduct the dollar value of business miles traveled on your tax return. The taxpayer may file the actual expense s/he incurred, or use the standard mileage rate prescribed by the IRS, which is 56 cents as of 2021. The IRS allowable mileage rates should be checked every year as they can change.

“If you decide to use actual car expenses, be sure to include payments, depreciation, registration, insurance, garage rent, licenses, repairs and maintenance, and parking and toll fees.” AND, “If you decide to use the standard mileage rate, it would be in your best interest to keep a log—daily, weekly or monthly—of miles driven to distinguish personal use from business use.”

Depreciation of property and equipment

Some self-employed people may purchase property and equipment for a business. If they expect that property to last longer than one year, it should be depreciated on the tax return.

Claims regarding property, according to the IRS, must meet the following criteria: You must own the property and it must be used or held to generate income. The property should have an estimated useful life, meaning you should be able to guess how long you can generate income with it. It may not have a useful life of one year or less, and may not be purchased and disposed of in the same year.

Certain repairs on property used for business may also be deducted.

Educational expenses

Any educational expense is potentially tax-deductible.

“Many times an overlooked deduction is educational expenses. “If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Think about any books, web courses, local college courses, or other classes or materials that you have purchased to improve your job or business. It’s easy to forget a work-related webinar or business e-book that was purchased online, so remember to save e-receipts.

Also recall that subscriptions to trade or professional publications and donations to business organizations, both of which are frequently necessary for the continuation and growth of your business.

Other areas to explore

Other deductions that can be easily missed are advertising and promotional expenses, banking fees, and air, bus, or train fare. Restaurant meals and other entertainment costs may be written off as long as they are necessary business expenses.

And, consider health insurance premiums, which in most cases represent a credit rather than a tax deduction. “A credit goes directly against one’s taxes, rather than a reduction of income.”

Regardless of which expenses you discover that you may write off, the most important thing is to keep accurate records throughout the year. Save receipts, including e-mail receipts, and file or log them so you have easy access to them at tax time. Not only does keeping receipts, mileage logs, and other expense records make filing taxes easier, but it also facilitates a system that allows you to track changes from year to year.

***

Long-term tax-saving strategies

Don’t just look at last-minute write-offs when considering self-employment tax deductions. Think about laying down some long-term strategies for money savings from year to year—particularly if you are a high earner.

“Accountants typically tell you what you have to pay but they don’t always tell you strategies to reduce your payments.”

To reduce your gross taxable income, consider setting up a defined-benefit pension plan. This plan is based on your age and income: The older you are and the higher your earnings, the more you are allowed to contribute. An alternative plan is an age-weighted profit-sharing plan, which is similar and can benefit those who have several employees.

Another strategy for high-earning business owners who own their own building through a limited liability company or similar business structure is to pay themselves rent. This rent is used to pay down the mortgage, but it is also considered a business expense for tax purposes.

Self-employed professionals required to have liability insurance should consider setting up their own insurance company. A captive insurance company is one that insures the risks of the business—or businesses, in the case of a cooperative. Its premiums can be tax-deductible.

But, if money accumulates and claims are minimal, the money taken out is taxable under capital gains. This is not a retirement strategy, but that it can save you money by allowing you to “pay yourself” instead of an insurance company and still deduct the premiums.

Assessment

With any of these more complicated, long-term strategies, consult with a business attorney, CPA/EA or financial planner to ensure you have the best plan possible for your business.

Posted on January 16, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

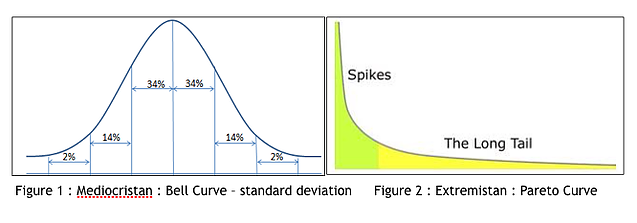

The 2-Ps [80/20] Rule

[By staff reporters]

Pareto’s law is either of the following closely related ideas: Pareto principle or law of the vital few, stating that 80% of the effects come from 20% of the causes Pareto distribution

Pareto distribution

The Pareto distribution, named after the Italian civil engineer, economist, and sociologist Vilfredo Pareto, is a power law probability distribution that is used in description of social, scientific, geophysical, actuarial, and many other types of observable phenomena. en.wikipedia.org

DEFINITION: The meaning of meme stocks is sort of self-explanatory: hyped stocks that perform well. But from a fundamental perspective, they shouldn’t do well at all.

For example, Reddit forums and social media hype drive meme stocks. Speculators on Twitter and Reddit united together to trade their favorite companies in hopes of driving them “to the moon.”

It may not be fair to call them speculators. These hype beasts want to buy and hold stocks of companies that might not have a great long-term outlook.

Brokerages like Robinhood helped level the playing field with apps and ‘easier’ access. That’s giving retail traders more opportunity. Robinhood traders can buy with just a few clicks on their smartphones and use partial positions to buy chunks of stocks.

How much will it cost you to start a dental practice – with Business Plan?

There are many costs to consider to set up a successful dental practice. Note that the following values are not the exact amount but an average of setting up a dental practice:

Purchase price – this includes valuation fees of between $1,000-4,500, solicitor fees of between $4,000 – 17,000, accountancy and bank fees of around $3,000, and bank solicitors, which can be up to $3,500. Many of these can be reduced or obliterated.

Materials – $40,000

Lab fees – $36,000

Staff costs – $82,000

Other costs (associates fees) – [$245,000 – $295,000]

Other Factors

“Big” Tech – Many startup doctors want to include CBCT or CAD/CAM or 3D printing in their startup, any of which can add $25,000-$175,000. In other situations, waiting is the best option.

Cabinetry Preferences – Costs for cabinetry can range from $5,000 to $175,000.

Practice Management Software (PMS) – Pricing will range from a few thousand dollars to $25,000; OR none at all.

Mechanical Delivery – Typically referred to as chairs, lights, and units, this category of dental equipment costs will range between $5,000 and $100,000 based on your startup plans.

Vision – Ignore the so-called “experts” who will try to create a cookie-cutter model for your equipment costs. That is the thinking of corporate dentistry. You want a customized private practice vision that allows you to create a model matching your standards. Prioritize your vision, so your values and philosophy will lead your dental equipment budget and purchasing decisions. Your equipment budget will be—and should be—customized.

Do your children have income-generating assets in a custodial account?

If so, be sure you understand the so-called kiddie tax.

This law was passed to discourage wealthier individuals from transferring assets to their children to take advantage of their lower tax rates. The kiddie tax has seen many iterations but current rules tax a minor child’s unearned income—including capital gains distributions, dividends, and interest income—at the parents’ tax rate if it exceeds the annual limit ($2,200 in 2021).

The tax applies to dependent children under the age of 18 at the end of the tax year (or full-time students younger than 24) and works like this:

The first $1,100 of unearned income is covered by the kiddie tax’s standard deduction, so it isn’t taxed.

The next $1,100 is taxed at the child’s marginal tax rate.

Anything above $2,200 is taxed at the parents’ marginal tax rate.

So – If your child also has earned income, say from a summer job or legitimate work in your medical office or practice, the rules become more complicated.

Posted on July 22, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

BOOK REVIEW

“The Dictionary of Health Insurance and Managed Care lifts the fog of confusion surrounding the most contentious topic in the health care industrial complex today. My suggestion therefore is to ‘read it, refer to it, recommend it, and reap’.”

—Michael J. Stahl, PhD, Physician Executive MBA Program [William B. Stokely Distinguished Professor of Business]

The University of Tennessee, College of Business Administration

BOOK-VALUE: Cost of capital assets minus accumulated depreciation for a healthcare [corporation], or other organization.

The net asset value of a [healthcare] companies common stock. This is calculated by dividing the net tangible assets of the company (minus the par value of any preferred stock the company has) by the number of common shares outstanding.

****

PAR VALUE: For common stock, the value on the books of the corporation. It has little to do with market value or even the original price of shares at first issuance.

The difference between par and the price at first issuance is carried on the books of a corporation as “paid-in capital” or “capital surplus.”

Posted on May 8, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

See You Soon!

Colleagues know that I enjoy personal coaching and public speaking and give as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world. All in a Corona safe environment.

These include lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, end-note lectures at city and statewide financial coalitions, and annual lectures for a variety of internal yearly meetings.

Posted on November 13, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

About iMBA, Inc

By Staff Reporters

iMBA Inc., is a healthcare consulting and financial planning analytics firm specializing in medical practice management and physician alignment.

Our mission is to empower physician colleagues and healthcare organizations to drive clarity, improve performance, and create accountability.

Our team combines a cross-section of skill-sets including public and population health, financial operations, business intelligence, and data science.

And, our diverse background of experience includes advanced academic training, economic and financial research, global marketing, management consulting, and entrepreneurial spirit.

SCHEDULE A MEDICAL PRACTICE & FINANCIAL PLANNING CONSULTATION TODAY!

Courtesy: https://lnkd.in/eBf-4vY

For Doctors – By Doctors – Confidential – Video Conference WEB: https://lnkd.in/eVGcji5

[Authentic Consulting for Physicians & Medical Colleagues]

My fee is $250 per hour prorated, so you only pay for the time used. This fee covers almost any medical practice management, insurance and risk management, personal financial planning or investment related topic, including document review, phone or Skype® consultation, research and/or written investment strategies.

IOW: No high water marks, no claw-back fees, sales or commissions, front or back end loads, 12[b]-1 fees or Assets Under Management [AUM] charges; etc. “Pay-as-you-Go”; period! Client Centricity.

Posted on August 28, 2019 by Dr. David Edward Marcinko MBA MEd CMP™

Academic Titles are Different in Europe

By Dr. David E. Marcinko MBA

***

I’ve taught in medical, graduate and business school academia for a while now, and served as instructor, adjunct, assistant, associate and full professor in the USA and Europe. I even held chair and endowed positions. But, the precise definition of these titles has always eluded me. So, I did a bit of research to arrive at the following conclusions mingled with my personal experiences..

***

A “Professor-of-the-Practice” or P-O-P is a non-tenured person appointed to the academic staff of an American university with exceptional experiences in their “practice” (profession) and holding a terminal doctoral degree.

I’ve seen this position in medical schools and allied health care institutuions.

NOTE: In American universities, a “professor” is practically any lecturer with a doctor’s degree, whereas in most of the world the title is reserved for senior academics; including most Commonwealth Nations (United Kingdom), German-speaking nations and Northern Europe. It may also be a department head or specifically bestowed chair. A professor is a highly accomplished and recognized academic, and the title is awarded only after decades of scholarly work. In the United States and Canada the title of professor is granted to all scholars with doctorate degrees (typically Ph.D.s) who teach in two and four year colleges and universities, and used in the titles Assistant Professor and Associate Professor, which are not considered full professorship level positions elsewhere.

***

***

A Scholar-in-Residence can serve a university in a full-time, visiting, or part-time capacity. A full-time SIR will be provided on-campus housing and is asked to: hold 2-5 office hours/programs per week in the community. A part-time SIR will host at least 2 programs/activities during the appointment and attend appropriate community meetings.

I’ve seen this position mostly in the graduate school universe.

Finally, an “Entrepreneur-in-Residence” is a position typically held by successful entrepreneurs in venture capital firms, private equity firms, startup accelerators, law firms, or business schools. The EIR typically leads a small, early-stage, emerging company deemed to have high growth potential, or has demonstrated high growth. The university endowment fund provides the Entrepreneur-in-Residence with working capital to nurture expansion, new-product development, or restructuring of the company’s operations, management, and/or ownership.

This is likely the newest business school nomenclature iteration IMHO.

Assessment: So, how did I do with these definitions which still may vary among different colleges, universities and institutions? Your thoughts are appreciated.