A conversion can get you into a Roth IRA—even if your income is too high

By Dr. David E. Marcinko MBA CMP®

SPONSOR: http://www.CertifiedMedicalPlanner.org

If you’re a physician looking to get ahead on planning for retirement, you’re likely familiar with individual retirement accounts, or IRAs. An IRA is a tax-advantaged vehicle that helps you grow your retirement savings. Roth IRAs are particularly attractive, because you don’t pay taxes on withdrawals in retirement.

CITE: https://www.r2library.com/Resource/Title/0826102549

There’s one problem: you can’t contribute to a Roth IRA directly if you make above a certain income. A backdoor IRA, though, can solve your problem by allowing you to convert a traditional IRA into a Roth.

Here’s how it works:

First, place your contribution in a traditional IRA—which has no income limits.

Then, move the money into a Roth IRA using a Roth conversion.

But make sure you understand the tax consequences before using this strategy.

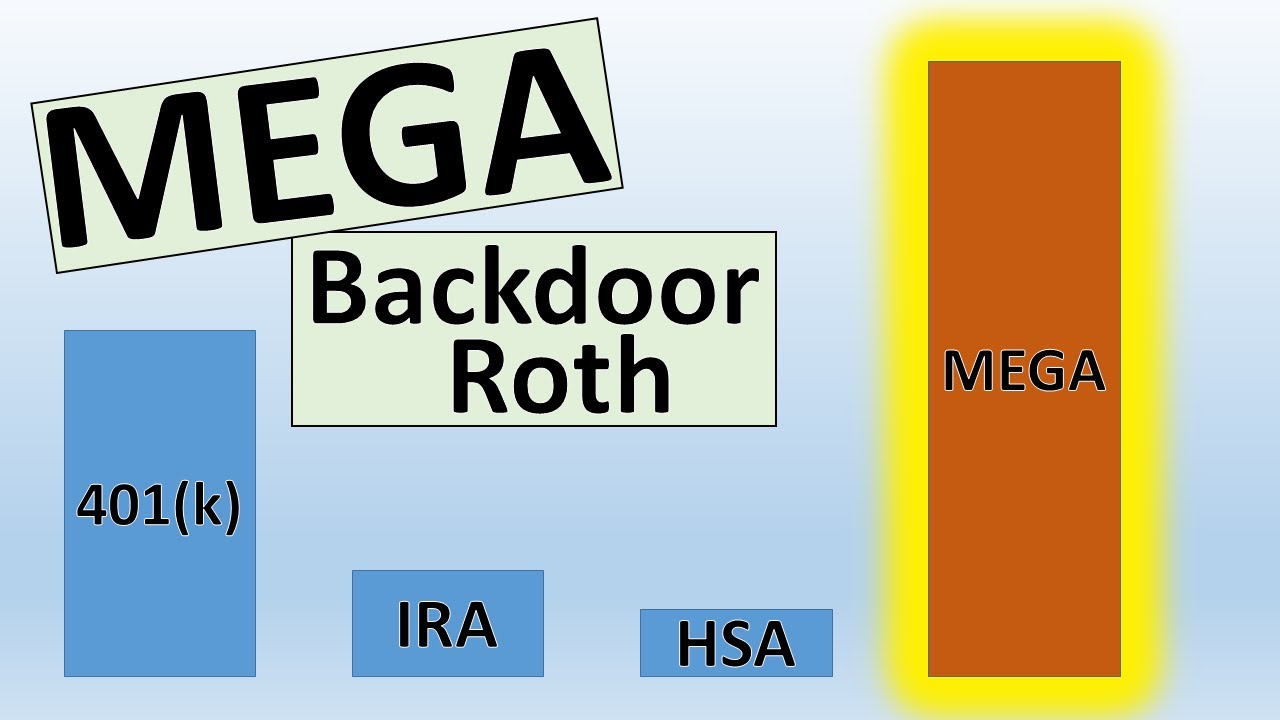

How a MEGA Backdoor Roth Works

The mega backdoor Roth allows you to put up to $38,500 in a Roth IRA or Roth 401(k) in 2021, on top of the regular contribution limits for those accounts. If you have a Roth 401(k) at work (and the plan allows for the mega option as described below), generally you can choose whether the final destination of your mega contributions is the Roth 401(k) or a Roth IRA. If your employer offers only a traditional 401(k), then your mega contributions would end up in a Roth IRA.

Here’s a quick summary of what you need to have in place for the ideal mega backdoor Roth strategy:

- A 401(k) plan that allows “after-tax contributions.” After-tax contributions are a separate bucket of money from your traditional and Roth 401(k) contributions. About 43% of 401(k) plans allow after-tax contributions, according to a 2017 survey of large and midsize employers by consulting firm Willis Towers Watson.

- Your employer offers either in-service distributions to a Roth IRA — that is, you can take money out of the 401(k) plan while you’re still working at the company — or lets you move money from the after-tax portion of your plan into the Roth 401(k) part of the plan. If you’re not sure, ask your human resources department or plan administrator.

- You’ve got money left over to save, even after maxing out your regular 401(k) and Roth IRA contributions.

***

YOUR COMMENTS ARE APPRECIATED.

***

Thank You

INVITE DR. MARCINKO: https://medicalexecutivepost.com/dr-david-marcinkos-

***

Share this:

Filed under: "Ask-an-Advisor", CMP Program, Investing, Retirement and Benefits, Touring with Marcinko | Tagged: Back Door IRA, Certified Medical Planner™, CMP, David E. Marcinko, IRA, Mega IRA, Mega Roth IRA, Roth IRA |

QSBS

Once an obscure provision of the tax code, “qualified small business stock,” or QSBS, benefits venture capital-backed startups in technology and other industries that are aiming to get very big, very quickly. If these young companies go public or get acquired, holders of their QSBS pay no capital gains taxes on windfalls of $10 million or — in some cases — even more.

And despite its name, the vast majority of small businesses can never qualify for the tax break.

Charlie

LikeLike

ROTH Update – Don’t Worry?

https://www.msn.com/en-us/news/other/why-you-dont-need-to-worry-about-losing-your-roth-ira/ar-AARQ7mR?li=BBnb7Kz

DEM

LikeLike