BEWARE THE STOCK MARKETS TODAY

By Dr. David E. Marcinko MBA CMP®

SPONSOR: http://www.CertifiedMedicalPlanner.org

Markets: While yesterday was somewhat of a snoozefest on Wall Street, today should be more interesting. In a quarterly event known as “quadruple witching,” stock options, index options, stock futures, and index futures all expire on the same day, which can produce fireworks.

CITE: https://www.r2library.com/Resource/Title/0826102549

HISTORY

The phrase quadruple witching brings to mind stories that begin, “It was a dark and stormy night…” or folkloric visions of witches flying chaotically on broomsticks across the brightness of a moon.

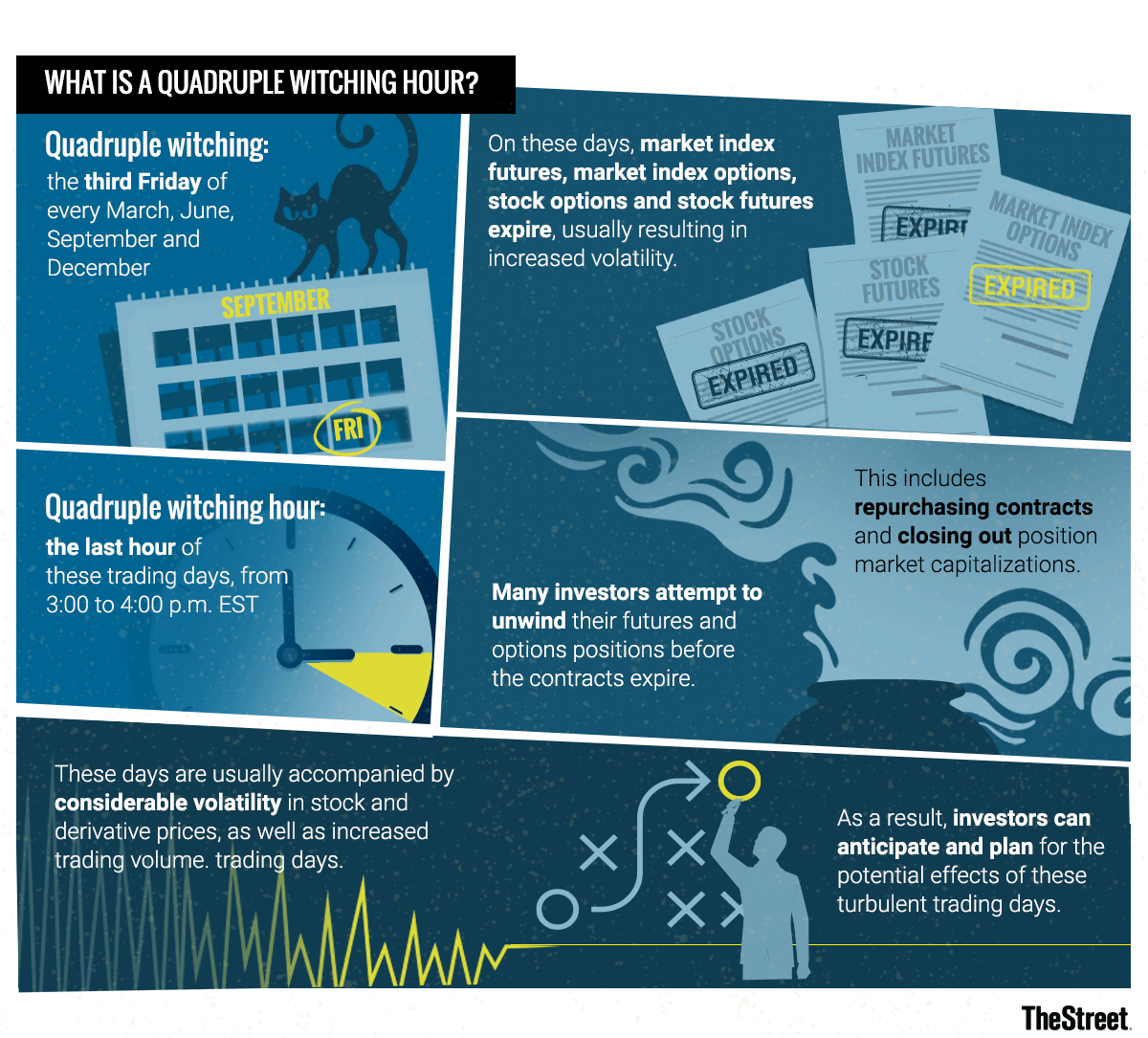

In the context of investing, quadruple witching also refers to possible chaos but chaos in the financial markets. Such chaos can erupt due to four different types of contracts on financial assets expiring on the same day. The quadruple witching hour is the last hour of the trading session on that day. The question is whether investors can make abnormally robust profits on quadruple witching days due to market fluctuations.

What Is Quadruple Witching?

Quadruple witching refers to four days during the calendar year when the contracts on four different kinds of financial assets expire. The days are the third Friday of March, June, September and December. The assets on which the contracts expire on that day are stock options, single stock futures, stock index futures and stock index options. Options contracts also expire monthly. Futures contracts expire quarterly.

Because all four types of contracts expire on the same day, the quadruple witching day usually sees a heavier volume of trading. This is why the reference to chaos is made about this witching day. Market volume is increased partly due to offsetting trades that are made automatically. Volume on quadruple witching days has increased roughly two-thirds of the time since 2005.

Recent Quadruple Witching Expiration Day

On June 18, 2021, a quadruple witching day, a near-record volume of single-stock equity options was set to expire at the end of the day in the amount of $818 billion. As a result, a near-record of single stock open interest of about $3 trillion stood on June 18, 2021. Open interest refers to how many contracts are open during any given point during the day. It is an important metric for traders to watch since a large amount of open interest can move the value of the underlying stock.

YOUR COMMENTS ARE APPRECIATED.

Thank You

***

INVITE DR. MARCINKO: https://medicalexecutivepost.com/dr-david-marcinkos-

***

Share this:

Filed under: Breaking News, Glossary Terms, Investing, Touring with Marcinko | Tagged: quadruple expiration day, quadruple witching expiration day, triple expiration day, triple witching day, triple witching expiration day | 5 Comments »