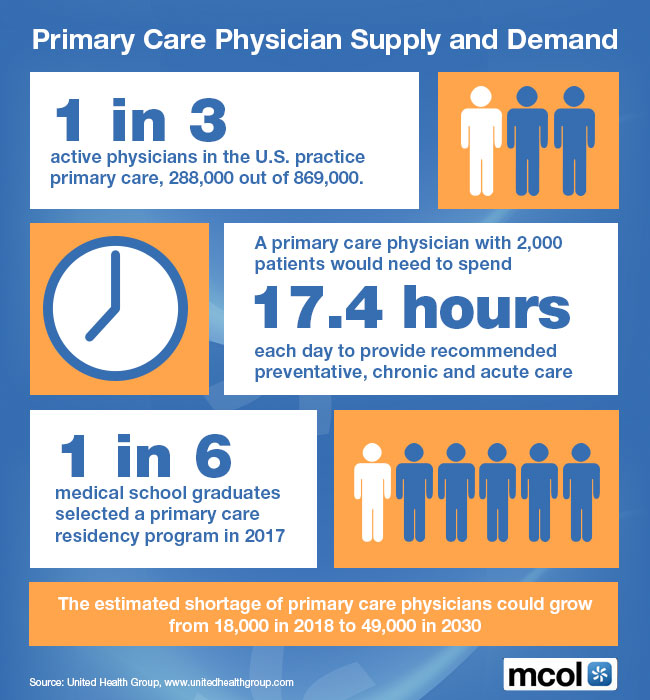

What it is – How it works?

[By Dr. Marcinko and staff reporters]

Sell in May and go away is an investment strategy for stocks based on a theory (sometimes known as the Halloween indicator) that the period from November to April inclusive has significantly stronger growth on average than the other months.

***

“DANCE OF DEATH”

[Copyright 2018 iMBA Inc., All rights reserved. USA]

***

The Strategy

In such strategies, stocks are sold at the start of May and the proceeds held in cash (e.g. a money market fund); stocks are bought again in the autumn, typically around Halloween. “Sell in May” can be characterised as the belief that it is better to avoid holding stock during the summer period.

Though this seasonality is often mentioned informally, it has largely been ignored in academic circles (perhaps being assumed to be a mere superstition). Nonetheless analysis by Bouman and Jacobsen (2002) shows that the effect has indeed occurred in 36 out of 37 countries examined, and since the 17th century (1694) in the United Kingdom; it is strongest in Europe. While the effect may reflect a failure of the efficient-market hypothesis, alternatives exist such as small sample size or time variation in expected stock market returns.

***

***

Causes the Effect

Although it’s not clear what causes the effect, what’s most interesting is that it shows that stock market returns in many countries during the period May–October are systematically negative or lower than the short-term interest rate, which also goes against the efficient-market hypothesis. Stock market returns should not be predictably lower than the short-term interest rate (risk free rate).

Popular media often refer to this market wisdom in the month of May, claiming that in the six months to come things will be different and the pattern will not show.

However, as the effect has been strongly present in most developed markets (including the United States, Canada, Japan, the United Kingdom and most European countries) in the last decade – especially May–October 2009 – these claims are often proved wrong.

That said, between April 30 and October 30, 2009, the FTSE 100 gained 20% (from 4,189.59 to 5,044.55)

Academics

The effect has largely been ignored in academic circles. The idea contradicts much established theory, especially the efficient-market hypothesis.

Maberly and Pierce extended the data to April 2003. They also tested the strategy for April 1982 through April 2003 except for two months, October 1987 and August 1998. They found that it doesn’t work well in the time period April 1982–September 1987 plus November 1987–July 1998 plus September 1998–April 2003.[7] Other regression models using the same data but controlling for extreme outliers have found the Halloween effect to still be significant.[8]

“Sell in May and go away” has persisted as a profitable market-timing strategy for stock investors, according to a follow-up study by Andrade, Chhaochharia and Fuerst (2012). They find that the Sell-in-May seasonal pattern persists after the end of Bouman and Jacobsen’s (2002) sample. This is important in showing that the Halloween effect is not a statistical fluke detected by data mining. Strikingly, in the 1998–2012 sample on average November–April returns are larger than May–October returns in all 37 markets they study. On average, the difference is equal to about 10% percentage points. Also strikingly, the magnitude of the difference is the same in Bouman and Jacobsen’s (2002) and in the out-of-sample analysis of Andrade, Chhaochharia and Fuerst (2012). Further backtesting by Mebane Faber has shown this effect has been in place since 1950.

Source: Sell in May – Wikipedia, the free encyclopedia

***

***

More:

- Is Another [Double-Dip] Stock Market Crash Looming? The Hindenburg Omen!

Even More:

- Popular ME-P Halloween Content for 2014

- Black Licorice May Be A Bad Halloween Treat

- Halloween Trends for 2011

Much More:

- 16 spooky Halloween-themed ICD-10 codes

- Healthcare Triage: Strangers Probably Aren’t Going to Poison Your Kids’ Halloween Candy

Assessment

Was this indicator appropriate for 2018?

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

- PRACTICES: www.BusinessofMedicalPractice.com

- HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

- CLINICS: http://www.crcpress.com/product/isbn/9781439879900

- ADVISORS: www.CertifiedMedicalPlanner.org

- FINANCE: Financial Planning for Physicians and Advisors

- INSURANCE: Risk Management and Insurance Strategies for Physicians and Advisors

- Dictionary of Health Economics and Finance

- Dictionary of Health Information Technology and Security

- Dictionary of Health Insurance and Managed Care

***

***

Share this:

Filed under: Investing, LifeStyle | Tagged: Halloween Index, Halloween indicator, Hindenburg Omen | 9 Comments »