BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

An annuity is a contract between you and an insurance company. When you purchase an annuity, you make a lump-sum contribution or a series of contributions, generally each month. In return, the insurance company makes periodic payments to you beginning immediately or at a pre-determined date in the future. These periodic payments may last for a finite period, such as 20 years, or an indefinite period, such as until both you and your spouse are deceased. Annuities may also include a death benefit that will pay your beneficiary a specified minimum amount, such as the total amount of your contributions.

The growth of earnings in your annuity is typically tax-deferred; this could be beneficial as you may be in a lower tax bracket when you begin taking distributions from the annuity.

Warning: A word of caution: Annuities are intended as long-term investments. If you withdraw your money early from an annuity, you may pay substantial surrender charges to the insurance company as well as tax penalties to the IRS and state.

***

***

There are three basic types of annuities — fixed, indexed, and variable

1. With a fixed annuity, the insurance company agrees to pay you no less than a specified (fixed) rate of interest during the time that your account is growing. The insurance company also agrees that the periodic payments will be a specified (fixed) amount per dollar in your account.

2. With an indexed annuity, your return is based on changes in an index, such as the S&P. Indexed annuity contracts also state that the contract value will be no less than a specified minimum, regardless of index performance.

3. A variable annuity allows you to choose from among a range of different investment options, typically mutual funds. The rate of return and the amount of the periodic payments you eventually receive will vary depending on the performance of the investment options you select.

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

A Certified Public Accountant (CPA) is a licensed professional who has passed an examination administered by a state’s Board of Accountancy. State CPA exams are created under guidelines issued by The American Institute of Certified Public Accountants (AICPA). The Uniform CPA Exam can only be taken by accountants who already have professional experience in the field and a bachelor’s degree.CPAs are not fiduciaries.

Not all accountants are CPAs. Accountants who are CPAs are licensed by their state’s Board of Accountancy after passing the Uniform CPA Exam. CPAs prepare reports that accurately reflect the business dealings of the companies and individuals that hire them. Many prepare tax returns for individuals or businesses and advise them on ways to minimize taxes. Obtaining the CPA designation requires a bachelor’s degree, typically with a major in business administration, finance, or accounting. Other majors are acceptable if the applicant meets the minimum requirements for accounting courses.

Enrolled Agent

Although not a CPA, an Enrolled Agent [EA] is a person who has earned the privilege of representing taxpayers before the Internal Revenue Service [IRS]. This is done by either passing a three-part comprehensive IRS test covering individual and business tax returns, or through experience as a former IRS employee. Enrolled agent status is the highest credential the IRS awards. Individuals who obtain this elite status must adhere to ethical standards and complete 72 hours of continuing education courses every three years.

Certified Managerial Accountant

A Certified Management Accountant (CMA), which is issued by the Institute of Management Accountants (IMA), builds on financial accounting proficiency by adding management skills that aid in making strategic business decisions based on financial data.

Oftentimes, the reports and analyses prepared by certified management accountants (CMAs) will go above and beyond those required by generally accepted accounting principles (GAAP).

For example, in addition to a company’s required GAAP financial statements, CMAs may prepare additional management reports that provide specific insights useful to corporate decision-makers, such as performance metrics on specific company departments, products, or even employees.

Certified Financial Analyst

A Certified Financial Analyst [CFA] is a globally-recognized professional designation offered by the CFA Institute, an organization that measures and certifies the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management, and security analysis. From 1963 through November 2023, more than 3.7 million candidates had taken the CFA exam. The overall pass rate was 45%. From 2014 through 2023, the 10-year average pass rate was 43%.1

CFA Institute. The CFA Institute was formerly the Association for Investment Management and Research (AIMR).

The CFA charter is one of the most respected designations in finance and is widely considered to be the gold standard in the field of investment analysis. To become a charter holder, candidates must pass three difficult exams, have a bachelors degree, and have at least 4,000 hours of relevant professional experience over a minimum of three years. Passing the CFA Program exams requires strong discipline and an extensive amount of studying.

There are more than 200,000 CFA charter holders worldwide in 164 countries.The designation is handed out by the CFA Institute, which has 11 offices worldwide and 160 local member societies.

Several years ago a group of highly trusted and deeply experienced financial advisors, insurance service professionals and estate planners noted that far too many of their mature retiring physician clients, using traditional stock brokers, management consultants and financial advisors, seemed to be less successful than those who went it alone. These Do-it-Yourselfers [DIYs] had setbacks and made mistakes, for sure. But, the ME Inc doctors seemed to learn from their mistakes and did not incur the high management and service fees demanded from general or retail one-size-fits-all “advisors.”

In fact, an informal inverse related relationship was noted, and dubbed the “Doctor Effect.” In others words, the more consultants an individual doctor retained; the less well they did in all disciplines of the financial planning and medical practice management, continuum.

Of course, the reason for this discrepancy eluded many of them as Wall Street brokerages and wire-houses flooded the media with messages, infomercials, print, radio, TV, texts, tweets, dinners and internet ads to the contrary. Rather than self-learn the basics, the prevailing sentiment seemed to purse the holy grail of finding the “perfect financial advisor.” This realization confirmed the industry culture which seemed to be:

Bread for the advisor – Crumbs for the client!

And so, Marcinko Associates formed a cadre’ of technology focused and highly educated multi-degreed doctors, nurses, financial advisors, attorneys, accountants, psychologists and educational visionaries who decided there must be a better way for their healthcare colleagues to receive financial planning advice, products and related advisory services within a culture of fiduciary responsibility.

We trust you agree with this specific niche knowledge, and collegial consulting philosophy, as illustrated thru our firm and these two books.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

When you buy a share of stock, you are taking ownership in a company. Collectively, the company is owned by all the shareholders, and each share represents a claim on assets and earnings. If the company distributes profits to its shareholders, you should receive a proportionate share of the earnings.

Stocks are often categorized by the size of the company, or their market capitalization. The market capitalization is determined by multiplying the number of outstanding shares by the current share price. The most common market cap classes are small-cap (valued from $100 million to $1 billion), mid-cap ($1 billion to $10 billion), and large cap ($10 billion to $100 billion).

Stocks are also categorized by their sector, or the type of business the company conducts. Common sectors include utilities, consumer staples, energy, communications, financial, health care, transportation, and technology.

***

***

Stocks are often viewed as being in one of two categories — growth or value.

Growth stocks are ones that are associated with high quality, successful companies that are expected to continue growing at a better-than-average rate as compared to the rest of the market.

Value stocks are ones that have generally solid fundamentals, but are currently out of favor with the market. This may be due to the company being relatively new and unproven in the market, or because the company has recently experienced a decline due to the company’s sector being affected negatively. An example of this would be if the federal government was to levy a new tax on all cell phones, thus negatively affecting all cell phone company stocks.

History has shown that, over time, stocks have provided a better return than bonds, real estate, and other savings vehicles. As a result, stocks may be the ideal investment for investors with long-term goals.

Posted on April 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

U.S. stock and bond markets will be closed on Good Friday. Many global markets will also be closed Friday. Exceptions include Japan and mainland China, which will be open as usual. U.S. markets will reopen Monday. Many international markets will remain shut to mark Easter Monday, including Australia, Hong Kong, and exchanges in France, Germany and the U.K.

***

YESTERDAY 4/17/25

***

🟢 What’s up

TSMC eked out a 0.10% gain after the semiconductor maker reported a 60% increase in profits last quarter and downplayed the effects of tariffs.

Charles Schwab isn’t just the guy who made $2 billion from market chaos last week. It’s also the brokerage that reported record quarterly revenue, but shares only rose 0.65%.

Hertz climbed another 43.87%, tacking on another day of big wins after Bill Ackman’s Pershing Square Capital took a stake in the rental car company.

Trump Media & Technology Group popped 11.65% after the company asked the SEC to investigate a hedge fund with a $105 million short bet against it.

Chinese tea chain Chagee soared 15.86% in its first day of trading on the Nasdaq.

DR Horton missed analyst expectations last quarter and lowered its fiscal year guidance, but investors quickly forgave the country’s largest homebuilder and pushed shares up 3.16%.

What’s down

Alphabet took a 1.38% hit after a federal judge ruled that Google is a monopoly. This marks Alphabet’s second antitrust loss since last August.

Alcoa fell 6.98% after the aluminum mining behemoth announced it ate about $20 million in tariff-related costs last quarter, noting that this figure could rise to $90 million in the current quarter.

Abbott Laboratories gained 2.77% after the pharma company missed sales estimates but still beat earnings forecasts.

Gold miners continue to climb as gold keeps hitting new highs. Newmont rose 2.51%, while Gold Fields gained 3.35%.

What’s down

Tesla sank 4.94% after the company’s share of EV sales in California fell below 50% in the first quarter, while export controls threaten plans to produce Cybercabs in the US.

United Airlines fell 0.01% despite reporting its “best first-quarter financial results in five years,” according to management. The airline took the unique measure of providing two different financial outlooks for the year ahead: one for a stable economy, and one for a recession.

Lyft shed just 0.46% on the news that the ride-hailing company is acquiring European taxi app Free Now for $199 million.

Interactive BrokersGroup reported a 47% increase in trading volume last quarter that helped it beat revenue expectations, but the brokerage still tumbled 8.95% after missing profit forecasts.

Palantir gave up some of its recent gains following its big NATO announcement, sinking 5.78% today as investors collected profits.

JB HuntTransport Services’ management team warned that the logistics company sits squarely in the crosshairs of the trade war, pushing shares down 7.68%.

Omnicom Group tumbled 7.28% after the advertising firm missed revenue estimates thanks to economic uncertainty.

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Stocks kept the good vibes going for a second trading day yesterday with tech companies like Apple rising as investors reacted to the weekend’s news that smartphones and computers would be temporarily exempt from “reciprocal” tariffs—at least until new semiconductor tariffs are imposed.

Car companies also jumped after President Trump suggested he wanted to “help” as automakers try to transition their production to the US in the face of 25% auto tariffs.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

OVER HEARD IN THE FINANCIAL ADVISOR’S LOUNGE

***

***

By Perry D’Alessio, CPA [D’Alessio Tocci & Pell LLP]

What I see in my accounting practice is that significant accumulation in younger physician portfolio growth is not happening as it once did. This is partially because confidence in the equity markets is still not what it was; but that doctors are also looking for better solutions to support their reduced incomes.

For example, I see older doctors with about 25 percent of their wealth in the market, and even in retirement years, do not rely much on that accumulation to live on. Of this 25 percent, about 80 percent is in their retirement plan, as tax breaks for funding are just too good to ignore.

What I do see is that about 50 percent of senior physician wealth is in rental real estate, both in a private residence that has a rental component, and mixed-use properties. It is this that provides a good portion of income in retirement.

***

***

QUESTION: So, could I add dialog about real estate as a long term solution for retirement?

Yes, as I believe a real estate concentration in the amount of 5 percent is optimal for a diversified portfolio, but in a very passive way through mutual or index funds that are invested in real estate holdings and not directly owning properties.

Today, as an option, we have the ability to take pension plan assets and transfer marketable securities for rental property to be held inside the plan collecting rents instead of dividends.

Real estate holdings never vary very much, tend to go up modestly, and have preferential tax treatment due to depreciation of the property against income.

Posted on April 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

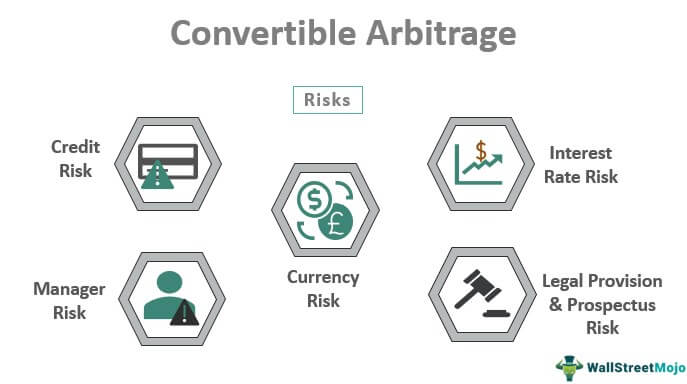

Convertible Arbitrage

Convertible arbitrage is the oldest market-neutral strategy. Designed to capitalize on the relative mispricing between a convertible security (e.g. convertible bond or preferred stock) and the underlying equity, convertible arbitrage was employed as early as the 1950s.

Since then, convertible arbitrage has evolved into a sophisticated, model-intensive strategy, designed to capture the difference between the income earned by a convertible security (which is held long) and the dividend of the underlying stock (which is sold short). The resulting net positive income of the hedged position is independent of any market fluctuations. The trick is to assemble a portfolio wherein the long and short positions, responding to equity fluctuations, interest rate shifts, credit spreads and other market events offset each other.

***

***

Hedge Fund Research (HFR) New York, offers the following description of the strategy

Convertible Arbitrage involves taking long positions in convertible securities and hedging those positions by selling short the underlying common stock. A manager will, in an effort to capitalize on relative pricing inefficiencies, purchase long positions in convertible securities, generally convertible bonds, convertible preferred stock or warrants, and hedge a portion of the equity risk by selling short the underlying common stock. Timing may be linked to a specific event relative to the underlying company, or a belief that a relative mispricing exists between the corresponding securities. Convertible securities and warrants are priced as a function of the price of the underlying stock, expected future volatility of returns, risk free interest rates, call provisions, supply and demand for specific issues and, in the case of convertible bonds, the issue-specific corporate/Treasury yield spread. Thus, there is ample room for relative mis-valuations.

Because a large part of this strategy’s gain is generated by cash flow, it is a relatively low-risk strategy.

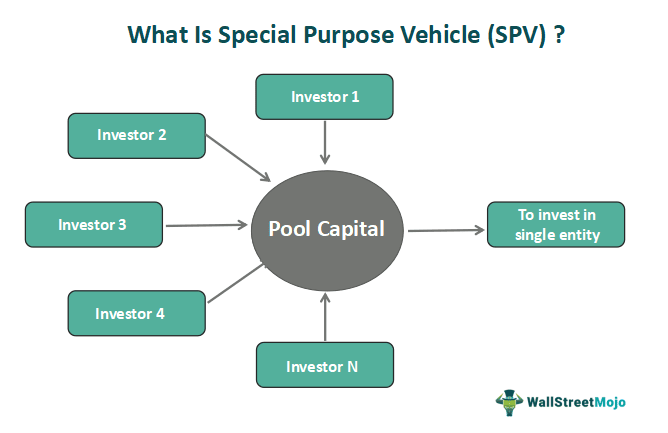

Its purpose is to isolate the parent company from any potential credit or financial risk that may arise from the SPV and is often used to pursue riskier projects, securitize debt, or transfer assets. Since an SPV is separate from the parent company, it isn’t affected by the parent’s performance, and the parent isn’t typically affected by the performance of the SPV. If the parent goes bankrupt and is no longer in existence, the SPV can carry on.

This makes an SPV bankruptcy remote. This also means that the parent company is unaffected by the loss if the SPV fails.

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and Morning Brew

***

***

Microsoft is celebrating its 50th birthday this week looking like a formerly washed up A-lister who’s suddenly rebounded and getting Oscar noms again.

Ever since Bill Gates and Paul Allen huddled in a garage in 1975 to start a company that’d define the experience of sitting in front of a boxy white PC monitor, Microsoft has had an uneven run. But after years of getting roasted for Internet Explorer, it now seems to be back on top—even briefly beating Apple as the world’s most valuable public company last year.

The tech giant can not only boast bonanza earnings, it also feels like a purveyor of the next big thing again, leading in the AI race through its partnership with OpenAI.

Windows washed

In the 1990s, it felt like Microsoft’s computer geeks were the overlords of tech. Windows powered most PCs, Internet Explorer became the go-to browser, and proficiency in Office tools became standard resume skills. But in the following decade, the company slept on internet tech and smartphones, ceding ground to Apple, Alphabet, and Meta.

It responded by going into midlife crisis mode, aka blowing cash on a series of questionable acquisitions to stay hip. That…didn’t help. By the 2010s, only grandparents could be reached @hotmail.com, Windows phones were a rarity, and no one used Bing as a verb.

When Gates stepped away from running the company in 2000, its new CEO Steve Ballmer grew its revenue threefold by the end of his tenure in 2013. He spearheaded Microsoft’s foray into gaming with the Xbox console and started its blockbuster cloud computing product Azure. But Microsoft’s profit growth slowed dramatically thanks to a massive cash bleed from its shopping spree.

It dropped $6.3 billion on the owner of ad tech platforms aQuantive to compete with Google’s ad business in 2007, only to write it off as a dud five years later.

The company burned at least $8 billion trying to make Windows phones a bigger force by buying Nokia’s cellphone division in 2014.

Microsoft paid $8.5 billion for Skype in 2011, which must’ve made it extra painful to announce that it was sunsetting the video calling service this winter.

***

***

Cash-slinging comeback kid

When it blew out forty candles in 2015, the tech giant was looking past its prime. The stock was trading at around $35 a share, well below its $58 peak in 1999. Its net profit for the year was $12 billion. But investors who held on until now were rewarded with shares going for $374 on its birthday this week after the company reported a net profit of $88 billion in the last financial year.

Much of the revenue now comes from its Azure cloud computing business, which has been boosted by the booming AI industry ravenous for server power.

When Microsoft’s current CEO Satya Nadella stepped into the role in 2014, he doubled down on Azure to make Microsoft into a B2B behemoth selling computing power to tech companies.

It is now the world’s second largest cloud provider after Amazon Web Services, with a 21% market share, according to Synergy Research Group.

Microsoft also bought some businesses that didn’t fail, including LinkedIn—the thought leadership hub with a user base that has soared to 1 billion since the 2016 acquisition. It also owns GitHub, the leading code-sharing platform for software developers. And in its biggest purchase yet, it snagged gaming IP giant Activision Blizzard that owns Call of Duty and World of Warcraft for a whopping $68 billion in 2022, hoping to make itself a dominant caterer to the Xbox joystick-wielding crowd.

It’s an AI company now

The not-quite-acquisition that really got Microsoft its groundbreaker’s glitz back was pouring $13 billion into OpenAI.

Having gotten in on the ground floor of the AI boom, Microsoft is harnessing OpenAI’s models to power its CoPilot AI agent, which it embedded into its Office tools and Teams app. This pits it against other tech giants betting that AI agents automating tasks will be the biggest in-cubicle revolution since Excel.

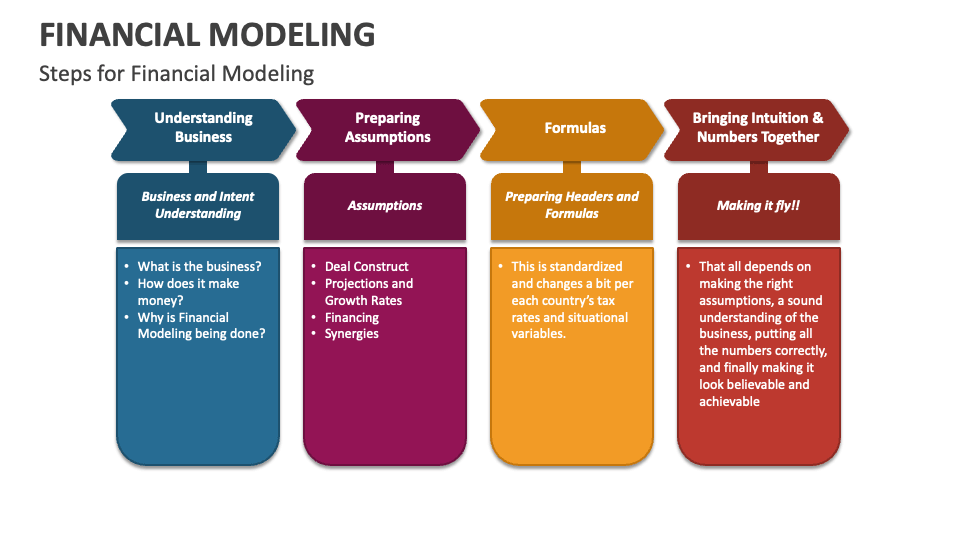

Financial Modeling is one of the most highly valued, but thinly understood, skills in financial analysis. The objective of financial modeling is to combine accounting, finance, and business metrics to create a forecast of a company’s future results.

According to Jeff Schmidt, a financial model is simply a spreadsheet, usually built in Microsoft Excel, that forecasts a business’s financial performance into the future. The forecast is typically based on the company’s historical performance and assumptions about the future and requires preparing an income statement, balance sheet, cash flow statement, and supporting schedules (known as a three-statement model, one of many types of approaches to financial statement modeling). From there, more advanced types of models can be built such as discounted cash flow analysis (DCF model), leveraged buyout (LBO), mergers and acquisitions (M&A), and sensitivity analysis

***

DEFINED TERMS

Discounted Cash Flow (DCF): A valuation method used to estimate the value of an investment based on its expected future cash flows, adjusted for the time value of money. It’s like deciding whether a treasure chest is worth diving for now, based on the gold coins you’ll be able to cash in later.

Sensitivity Analysis: This involves changing one variable at a time to see how it affects an outcome. Imagine tweaking your coffee-to-water ratio each morning to achieve the perfect brew strength.

Budget – A budget is the amount of money a department, function, or business can spend in a given period of time. Usually, but not always, finance does this annually for the upcoming year.

Rolling Forecast – A rolling forecast maintains a consistent view over a period of time (often 12 months). When one period closes, finance adds one more period to the forecast.

Topside – A topside adjustment is an overlay to a forecast. This is typically completed by the corporate or headquarter team. As individual teams submit a forecast, the consolidated result might not make sense or align with expectations. When this occurs, the high-level teams use a topside adjustment to streamline or adjust the consolidated view.

Monte Carlo Simulation: Picture yourself at the casino, but instead of gambling your savings away, you’re using this technique to predict different outcomes of your business decisions based on random variables. It’s like playing financial roulette with the odds in your favor.

What-If Analysis: Ever daydream about what would happen if you took that leap of faith with your business? This tool allows you to explore various scenarios without risking a dime. It’s like trying on outfits in a virtual dressing room before making a purchase.

Leveraged Buyout (LBO) Model: This is a bit like orchestrating a heist, but legally. It’s about acquiring a company using borrowed money, with plans to pay off the debts with the company’s own cash flows. High stakes, high rewards.

Mergers and Acquisitions (M&A) Model: Picture two puzzle pieces coming together. This model evaluates how combining companies can create a new, more valuable entity. It’s the corporate version of a matchmaker.

Three Statement Model: The holy trinity of financial modeling, linking the income statement, balance sheet, and cash flow statement. It’s like weaving a tapestry where each thread is crucial to the overall picture.

Capital Asset Pricing Model (CAPM): A formula that calculates the expected return on an investment, considering its risk compared to the market. It’s like choosing the best roller coaster in the park, balancing thrill and safety.

Cash Flow Forecasting: This is your financial weather forecast, predicting the cash flow climate of your business. It helps you plan for sunny days and save for the rainy ones.

Cost of Capital: The price of financing your business, whether through debt or equity. It’s like the interest rate on your growth engine, pushing you to maximize every dollar invested.

Debt Schedule: A timeline of your business’s debts, showing when and how much you owe. It’s your roadmap to becoming debt-free, one milestone at a time.

Equity Valuation: Determining the value of a company’s shares. It’s like assessing the worth of a rare gemstone, ensuring investors pay a fair price for a piece of the treasure.

Financial Leverage: Using debt to amplify returns on investment. It’s like using a lever to lift a heavy object, increasing force but also risk.

Forecast Model: A crystal ball for your finances, projecting future performance based on past and present data. It’s your guide through the financial wilderness, helping you navigate with confidence.

Operating Model: A detailed blueprint of how a business generates value, mapping out operational activities and their financial impact. It’s like laying out the inner workings of a clock, ensuring every gear turns smoothly.

Revenue Growth Model: This tracks potential increases in sales over time, charting a course for expansion. It’s like plotting your ascent up a mountain, anticipating the effort required to reach the summit.

I am in an unenviable position. The policy coming out of the White House has a significant impact on economics, more than ever before in my career. If I say anything positive about that policy, I’ll be put in the MAGA camp. If I criticize it, I’ll be accused of suffering from Trump derangement syndrome. I am hired by you to make the best investment decisions possible. Rather than see me as engaged in political commentary, I’d ask that you view my remarks as purely analytical.

Let me give you this analogy. I live in Denver. Let’s imagine I am a huge Broncos fan, and the Broncos are playing the Chicago Bears. If I am betting a significant amount of money on this game, I should put my affinity for the Broncos and hatred of the Chicago Bears aside and analyze data and facts. The Broncos are either going to win or lose; my wanting them to win has zero impact on the outcome. The same applies to my analysis here. My motto in life is Seneca’s saying, “Time discovers truth.” I just try to discover it before time does.

When it comes to politics, I also have a significant advantage. I was not born in this country. From a young age, I was brainwashed about communism, not about team Republican versus team Democrat. The failure of the Soviet Union de-brainwashed me fast concerning the virtues of communism and converted me into a believer in free markets.

As a result, I never bought into either party’s ideology, and thus in the last four presidential elections I voted for a Republican, an independent, a Democrat, and wrote in my youngest daughter, Mia Sarah (not in that order). In my articles I have criticized the policies of both Biden (student loan forgiveness, unions) and Trump (Bitcoin reserve).

I remind myself that in times like these you have to be a nuanced thinker. Some of Trump’s policies are terrific, others … not so much (I am being diplomatic here).

Scott Fitzgerald once said “The test of a first-rate intelligence is the ability to hold two opposed ideas in mind at the same time, and still retain the ability to function.” In 2025 we are taking this “first-rate intelligence” test daily.

What will happen to the US dollar? The US dollar will likely continue to get weaker, which is inflationary for the US. Let me start with some easily identifiable reasons:

We have too much debt. We ran 6-7% budget deficits while our economy was growing and unemployment was at record lows. Now we have $36 trillion in debt. Our interest expenses exceed our defense spending, and these costs will continue to climb. If/when we go into recession, we may see something we have not seen in a long time – higher interest rates. Our budget deficits will balloon to between 9–12%, and the debt market, realizing that inflation (i.e., money printing) is inevitable, will say, “Pay up!”

New competition from Bitcoin. President Trump’s approval of Bitcoin as a potential reserve currency is one of the most self-serving and anti-American things I’ve seen any president do. The US dollar is the world’s reserve currency. We still have little competition for that title. China could be a contender, but it is not a democracy and has capital controls. This policy has no upside for America, only downside.

A stronger Europe. Ironically, we may inadvertently create a stronger Europe by threatening to abandon NATO. I don’t want to insult European clients (or my European friends), but the following analogy describes the US-Europe relationship on some level: Europe gradually evolved into a trust fund kid (when it came to security) and the US turned into its sugar daddy. The trust fund kid was incredibly dependent on the sugar daddy. It criticized its parent for being a barbarian and money-driven, but it relied heavily on that parent to protect it from bullies.

President Trump cut off Europe’s allowance by threatening that the US might not protect Europe from Russia. This has forced Europe to spend more money on defense. Outside of Germany (which has little debt), few European economies can afford that. This may force Europe (or at least some European countries) to become more pragmatic – to cut social programs and bureaucracy. If this leads to a stronger Europe both economically and militarily, the euro will be competing with the US dollar. This is a big if.

Our new foreign policy.

When people describe President Trump’s foreign policy as “transactional,” they’re highlighting a fundamental shift in how America engages with the world – one with profound implications for our global standing, national interests, and the US dollar. The shift affects both types of capital – financial and reputational.

Reputational capital isn’t at risk in ‘one-shot’ transactions like house selling. Imagine you’re selling your primary residence and moving elsewhere. Do you disclose every flaw, or let the buyer figure things out? Your incentive is to maximize short-term profits. You’ll likely never meet this buyer again, and therefore there are incentives not to care what they’ll think of you afterward. You’ll be transactional, seeking the highest price possible for your biggest asset. This exemplifies a ‘one-shot’ system where future interactions aren’t expected.

Contrast this with a relationship- and trust-based system. Now imagine you are a homebuilder in a small town. Your suppliers only extend credit if you have a reputation for paying on time. Your employees do quality work only if you treat them fairly. Your buyers tell friends about their experience with you. The incentives naturally create a relational approach. In this trust-based system, incentives skew toward maximizing long-term profits, where reputational capital becomes the glue creating continuity.

Reputational capital radiates predictability – you know how someone will behave based on their history – but operating with low or negative reputational capital is difficult and expensive. People won’t enter long-term contracts with you or will demand external guarantees. Many potential partners will simply refuse to deal with you.

Building reputational capital works like adding pennies to a jar – each good deed incrementally adds to your standing. Yet reputational capital can collapse instantly by removing the jar’s bottom. A single breach of trust doesn’t just remove one penny; it can wipe out your entire balance and plunge you into reputational bankruptcy. The math is brutally asymmetric: good deeds might add a point or two, while bad deeds subtract by factors of 50 or 100.

This doesn’t mean transactions shouldn’t be profitable. If you’re accumulating reputational capital while consistently losing money, you’re probably in the wrong business. Each deal should be evaluated considering both long-term financial and reputational capital.

Individual transactions can sacrifice some profit but cannot afford to lose reputational capital. A “one-shot” transactional approach used in a trust-system environment may provide greater short-term profitability, but if this success comes at the expense of reputational capital, the long-term consequences for America’s global position could be devastating.

This brings us to our current foreign policy.

Relationships between nations are a trust-based system. I’d argue it’s a super-relational system because it’s multigenerational, lasting beyond the life of any one human. Reputational capital is paramount here.

Part of the US’s strength has been the soft power – the reputational capital – it exerted. We had a lot of friends, which helped us to be more effective in dealing with our foes. We keep telling ourselves that America is an “exceptional” nation. This exceptionalism didn’t just come from our financial and military might – it accumulated based on our reputational capital.

Though we don’t always succeed, we are a people who try to do the right thing. Our exceptionalism has been earned through our actions. We are the country that helped rebuild Europe and gave it six decades to repay lend-lease. We toppled communism.

I don’t know the nuances of the Ukraine mineral deal, but initially it had the optics of extortion. Though I think the renegotiated and signed version appears to be fair to both sides, forcing repayment while Ukraine is dodging Russian missiles made the US look transactional.

Actions by President Trump over the last month have undermined our reputation. We are quickly becoming a “one-shot” transactional player in a trust-based environment. Imposing tariffs on Canada on a whim to try to get it to become the 51st state erodes American reputational capital. So does not ruling out America invading Greenland. This puts us on the same moral plane as Russia invading Ukraine.

The conversation about tariffs has many nuances. For instance, I don’t know anyone who opposes reciprocal tariffs – they seem fair and don’t consume any reputational capital. But tariffs that are used as weapons in a trade war in order to annex another country erode reputational capital. Threatening to leave NATO and not protect countries that don’t spend enough on their defense diminishes reputational capital. Maybe the only way to get European countries to spend on defense was to threaten not to defend them – you can agree or disagree with the rationale behind each of Trump’s decisions, but what can’t be argued is that they undermined our reputational capital.

As we lose soft power, our influence will diminish, and thus so will perceptions of our power. The world will start looking at us not from the perspective of the continuity of generations but of presidential cycles. The word of the American president will have an expiration date of the next presidential or mid-term election.

There are two negotiation styles – Warren Buffett’s and Donald Trump’s. Both have their advantages and disadvantages. Buffett will give you one offer and one offer only. Once the deal is agreed to, even just verbally, that is the deal. Critics would say that there is downside to that predictability, as foes know how you are going to respond. Donald Trump’s style is to be unpredictable, which has its own advantages when you deal with foes – it keeps opponents guessing. But it destroys trust with your allies.

In a world of fiat currencies, all currency is a financial and reputational promise. President Trump, with the help of DOGE (and maybe even tariffs) may increase our financial strength. I hope he does, but it will likely come at a very high cost to our reputational capital, and therefore US global influence and the US dollar will continue its decline.

How are we positioned for this?

About half of our portfolio is foreign companies whose sales are not in dollars. They will benefit from a weaker dollar. We also have exposure to oil, which is priced in the US dollar and usually appreciates when the dollar weakens.

A weaker dollar means our imports will become more expensive, which is inflationary. We own many companies with pricing power and also companies that have claims on someone else’s revenues. Take Uber for example: they get about 20% of each ride. If the cost of the ride goes up, so does their dollar take.

Why does President Trump keep pushing crypto?

In July 2019, Trump said the following: “I am not a fan of Bitcoin and other cryptocurrencies, which are not money, and whose value is highly volatile and based on thin air.” Five years later he promised to establish the US Crypto Reserve, and in 2025 he did.

What changed? There is no logical reason for an American president to endorse crypto. None. Here is the honest answer: Crypto bros made mega-contributions to his campaign.

To top it off, three days before he took office he issued $TRUMP – a shitcoin. Believe it or not, “shitcoin” is a technical term in the crypto community (any coin other than Bitcoin is called a shitcoin by Bitcoin “maximalists”, folks who believe Bitcoin is the one and only digital currency). The future sitting president literally issued – I don’t want to call it a currency, so I guess shitcoin is the right name – that will at some point decline to zero in value. In other words, he’ll fleece his loyal followers who purchase $TRUMP of billions of dollars.

I previously referenced both reputational capital and soft power. These types of acts by a sitting president subtract from both.

Markets: Last week’s market bloodbath will go down in the history books. The S&P 500’s 10% plunge on Thursday and Friday, after President Trump announced massive tariffs, ranks among the steepest two-day decline in the last 70 years, on par with Black Monday in 1987, the post-Lehman Brothers rout in 2008, and the Covid plunge in March 2020. More than $6 trillion was wiped out from stocks over two days, and the NASDAQ entered a bear market, down 20% from a previous high.

Trading restarted at 9:30 am ET for what Bill Ackmanpredicts will be “one of the more interesting days in our country’s economic history.”

***

Monday Crash?

On the other hand, CNBC host and market commentator Jim Cramer just warned that America is in store for another “Black Monday” market crash similar to the record 1987 collapse if President Trump doesn’t curtail his tariff plan.

Cramer — who noted that the 1987 crash saw the Dow Jones Industrial Average fall by 22.6% in a single day — said the bloodbath could be repeated after the brutal two-day sell-off following the announcement of Trump’s sweeping tariffs against nearly 90 countries.

If the president doesn’t try to reach out and reward these countries and companies that play by the rules, then the 1987 scenario … the one where we went down three days and then down 22% on Monday, has the most cogency,” Cramer said on his show Saturday, referencing the worst single-day fall in the history of the Dow.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

***

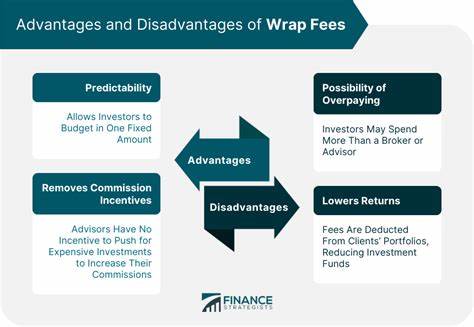

My stock broker is telling me about a “wrap-fee” program involving a hedge fund manager.

QUESTION: What is a Wrap Fee?

A wrap fee program is a service that provides investment advice and portfolio management to clients for one all-inclusive fee. The fee pays for the services provided to the client, including but not limited to securities transactions, portfolio management, research, brokerage, and administrative services. Wrap fee programs also provide an understanding of a client’s financial goals and objectives; research and selection of assets; implementation of investment decisions; account statements, and access to real-time financial data.

The Investment Advisers Act of 1940 regulates investment advisors when they offer these wrap fee programs and requires them to provide comprehensive disclosure documents before investing. This act helps ensure clients have access to all important information that affects their investment decisions.

QUESTION: Why do I need my stock broker? Can I just go directly to the hedge fund manager?

Yes, you can, but you may find a different fee arrangement when you reach the hedge fund manager, and you may be participating in an unethical transaction. When hedge fund managers set up separate accounts for wrap-fee clients, they agree to take a set fee in exchange for managing this money. They also enter into agreements with one or more brokers to help market this aspect of their money management business. A portion of the wrap fee you pay goes to the broker, and a portion goes to the manager. Incentive compensation is not generally used.

When approached directly, hedge fund managers will typically offer only the hedge fund, complete with incentive compensation and pooled investment features. However, if the hedge fund manager is willing to set up a separate account, it is possible that the investor will find the set fee much less than what he or she would have paid in a wrap fee account through a broker.

Finally, the very large caveat to all this is that the ethics of a hedge fund manager who steals clients from brokers with whom he has a marketing relationship ought to be called into question. And when it comes to hedge funds, the ethics of the manager are of paramount importance.

Posted on April 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS – MARKET VOLATILITY

By Staff Reporters

***

***

US stocks nosedived on Thursday, with the Dow tumbling more than 1,200 points as President Trump’s surprisingly steep “Liberation Day” tariffs sent shock waves through markets worldwide. The tech-heavy NASDAQ Composite (IXIC) led the sell-off, plummeting over 4%. The S&P 500 (GSPC) dove 3.7%, while the Dow Jones Industrial Average (^DJI) tumbled roughly 3%. [ongoing story].

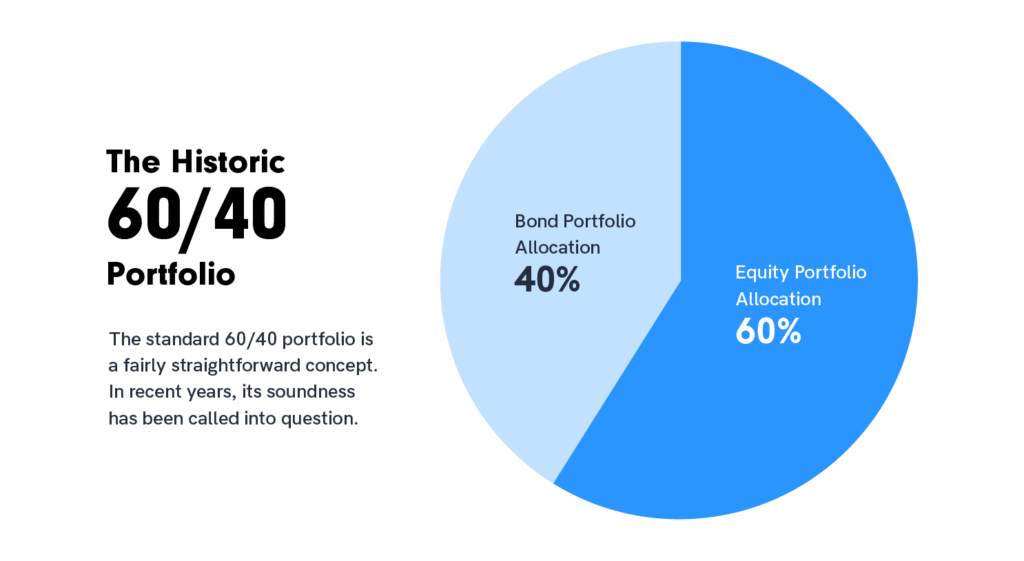

So, does the traditional 60 stock / 40 bond strategy still work or do we need another portfolio model?

***

The 60/40 strategy evolved out of American economist Harry Markowitz’s groundbreaking 1950s work on modern portfolio theory, which holds that investors should diversify their holdings with a mix of high-risk, high-return assets and low-risk, low-return assets based on their individual circumstances.

While a portfolio with a mix of 40% bonds and 60% equities may bring lower returns than all-stock holdings, the diversification generally brings lower variance in the returns—meaning more reliability—as long as there isn’t a strong correlation between stock and bond returns (ideally the correlation is negative, with bond returns rising while stock returns fall).

For 60/40 to work, bonds must be less volatile than stocks and economic growth and inflation have to move up and down in tandem. Typically, the same economic growth that powers rallies in equities also pushes up inflation—and bond returns down. Conversely, in a recession stocks drop and inflation is low, pushing up bond prices.

***

But, the traditional 60/40 portfolio may “no longer fully represent true diversification,” BlackRock CEO Larry Fink writes in a new letter to investors.

Instead, the “future standard portfolio” may move toward 50/30/20 with stocks, bonds and private assets like real estate, infrastructure and private credit, Fink writes.

Here’s what experts say individual investors may want to consider before dabbling in private investments.

It may be time to rethink the traditional 60/40 investment portfolio, according to BlackRock CEO Larry Fink. In a new letter to investors, Fink writes the traditional allocation comprised of 60% stocks and 40% bonds that dates back to the 1950s “may no longer fully represent true diversification.“

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

For years, I thought of cryptocurrency as a digital replacement for traditional money. After all, Bitcoin has “coin” right in the name. But let’s be honest: if Bitcoin is a currency, then my mother’s old Beanie Baby collection is a retirement fund.

A real currency needs to be stable. It should allow you to buy a coffee today without wondering whether, by tomorrow, that same amount could buy a car—or be worth nothing at all. Bitcoin and its kin like Ethereum and Dogecoin fail this test spectacularly.

Recently I have realized that cryptocurrency might be something even bigger and stranger than currency. It is not just digital money; it’s a bet on the huge global demand for financial autonomy.

In an age where every dollar is tracked, crypto offers an escape from traditional financial oversight. That makes it attractive not just to cybercriminals and tax evaders, but also to privacy advocates, speculators, and people living under restrictive financial policies. It doesn’t replace traditional money, it sidesteps it. It allows people to move, store, create, and destroy wealth outside of conventional banking systems. Some use it for transactions. Others see it as a hedge against inflation or a bet on the future of decentralized finance. Governments and banks don’t quite know what to do with it.

Crypto exists in a financial gray zone. It’s not widely accepted for everyday purchases, yet it can hold immense value. Unlike cash, which is limited by geography, or gold, which requires secure storage, crypto can be transferred globally in seconds. That’s part of its appeal, especially in countries with strict capital controls or volatile economies.

At the heart of cryptocurrency’s identity is the way it is produced. Crypto isn’t just a speculative asset—it’s an industrialized wealth-creation system. Imagine a massive warehouse filled with powerful computers “manufacturing” cryptocurrency. These mining operations exist solely to create new “coins” and process transactions, consuming enormous amounts of electricity in the process. The larger the operation, the more crypto it produces.

This is not how traditional currencies work. Fiat currencies are managed by central banks aiming for economic stability. Crypto, by contrast, is controlled by a decentralized network of miners and participants [block-chain]. Its supply is fixed, immune to government intervention. Some see this as a weakness. Others argue it is crypto’s greatest strength.

As Bitcoin and other major cryptocurrencies become more integrated into mainstream finance, the risks evolve. Even as regulators warn about crypto’s role in illicit activity, major corporations and investment firms are offering crypto-backed products. Some politicians, including President Trump, are discussing national Bitcoin reserves. This growing legitimacy makes crypto harder to ignore. But if crypto-backed funds become widespread, a crash could ripple far beyond crypto traders. That said, crypto remains a small fraction of global finance. Unless institutional adoption grows significantly, even a major downturn likely wouldn’t trigger systemic collapse.

Crypto’s increasing presence in finance does not make it a sound retirement investment. It is still a speculation. And speculations—whether in Bitcoin, meme stocks, or dot-com startups—are high-risk and not suitable for long-term financial security. Retirement portfolios should be built on diversification, stability, and predictable returns. Crypto offers none of these.

For years, I saw crypto as a failed currency. What I now think it to be is a decentralized speculative asset, driven by a growing demand to bypass traditional financial systems. Its future remains uncertain. As regulation increases and mainstream adoption expands, its role will continue to shift. But crypto is no longer just a niche experiment. It has become a financial force that governments, institutions, and individuals must reckon with—whether they embrace it or try to control it.

*** Several years ago we noted that far too many mid-career, mature and physician clients using traditional stock brokers, management consultants and “financial advisors”, seemed to be less successful than those who went it alone. These Do-it-Yourselfers [DIYs] had setbacks and made mistakes, for sure. But, the ME Inc,. doctors seemed to learn from their mistakes and did not incur the high management and service fees demanded from general or retail one-size-fits-all “advisors.”

In fact, an informal inverse related relationship was noted, and dubbed the “Doctor Effect.” In other words, the more consultants an individual doctor retained; the less well they did in all disciplines of the financial planning, professional portfolio and investing continuum.

Of course, the reason for this discrepancy eluded many of them as Wall Street brokerages and wire-houses flooded the media with messages, infomercials, print, radio, TV, texts, tweets, and internet ads to the contrary. Rather than self-learn the basics, the prevailing sentiment seemed to purse the holy grail of finding the “perfect financial advisor.” This realization was a confirmation of the industry culture which seemed to be: Bread for the advisor – Crumbs for the client!

And so, we at the the Institute of Medical Business Advisors Inc. (iMBA), and this Medical Executive-Post, formed a cadre’ of technology focused and highly educated doctors, financial advisors, attorneys, accountants, psychologists and educational visionaries who decided there must be a better way for their healthcare colleagues to receive financial planning advice, products and related management services within a culture of fiduciary responsibility.

We trust you agree with this ME Inc philosophy as illustrated in this free white paper available upon request.

PROFESSIONAL PORTFOLIO CONSTRUCTION [Investing Assets and their Management] Subscribe, Read, Like and Refer

Email whiote paper request here:MarcinkoAdvisors@outlook.com

Posted on March 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

While some medical practitioners and facilities can operate without Professional Liability Insurance coverage, one business related insurance that cannot / should not be avoided is Worker’s Compensation. Employers in all but seven states – so-called “monopolistic” states because they have their own state funds, are under statutory obligation to provide coverage for their employees. Historically, Worker’s Compensation pre-dates Social Security entitlements and well before the emergence of employer sponsored group benefits.

The coverage under worker’s compensation provides for lost income due to on-the-job accidents or work-related disability or death and the amount of benefits vary by state. In some instances, the coverage will reimburse the employee for medical expenses incurred with the accident.

The four general benefits covered under Worker’s Compensation are:

Medical Care – for expenses incurred usually without limitations on amount or period of care.

Disability Income – payable for both total and partial disability and is usually based on 66 2/3 percent of their wage base.

Death Benefits – generally fall into two categories; one a flat amount for “burial” insurance; and two, survivor benefits. Though varying by state, these benefits are similar to the disability payment (a percentage of weekly base wages) but may be capped as to total benefit, such as $50,000 or a period, such as 10 years

Rehabilitation Benefits – includes not only medical rehabilitation, but vocational rehabilitation, vocational counseling, retraining or educational benefits, and job placement

Traditionally, the secondary purpose of Worker’s Compensation was to reduce potential litigation because employees accepting the benefits from a Worker’s Compensation claim generally waived their right to sue their employer.

***

***

However, in our litigious society, this “protective shelter” has been severely tested and is crumbling.

Employers may provide their Worker’s Compensation three ways:

Private commercial insurance

State government funds

Self-insurance

Very few factors drive the premium structure – the occupation of the workers is the single most important determinant of premiums. An office worker may have premiums as low as $.10 per hundred of wages and a coal miner may exceed $50.00 per hundred of wages. Generally speaking, however, Worker’s Compensation premiums for the medical profession or healthcare worker are among the lowest available.

Therefore, for the medical practice, some physicians may consider self-insurance because the weekly benefits are typically below $500, thus making this decision attractive.

Alternatively, because officers and owners can elect not to be covered by Worker’s Compensation, the decision to purchase coverage from a private insurance company may afford inexpensive assurance that the benefits will be conveniently provided, and administered, by a private insurance company for their employees.

Absolute Return – the goal is to have a positive return, regardless of market direction. An absolute return strategy is not managed relative to a market index.

Accredited Investor – wealthy individual or well-capitalized institutions covered under Regulation D of the Securities Act of 1933.

Alpha – the return to a portfolio over and above that of an appropriate benchmark portfolio (the manager’s “value added”).

Arbitrage – any strategy that invests long in an asset, and short in a related asset, hoping the prices will converge.

Attribution – the process of “attributing” returns to their sources. For example, did the returns to a portfolio (over and above some benchmark) come from stock selection, industry/sector over- or under-weighting or factor weighting. Software programs are helpful in reporting an attribution.

Beta – a measure of systematic (i.e., non-diversifiable) risk. The goal is to quantify how much systematic risk is being taken by the fund manager vis-à-vis different risk factors, so that one can estimate the alpha or value-added on a risk-adjusted basis.

Correlation – a measure of how strategy returns move with one another, in a range of –1 to +1. A correlation of –1 implies that the strategies move in opposite directions. In constructing a portfolio of hedge funds, one usually wants to combine a number of non-correlated strategies (with decent expected returns) to be well diversified.

Drawdown – the percentage loss from a fund’s highest value to its lowest, over a particular time frame. A fund’s “maximum drawdown” is often looked at as a measure of potential risk.

Hurdle Rate – the return where the manager begins to earn incentive fees. If the hurdle rate is 5% and the fund earns 15% for the year, then incentive fees are applied to the 10% difference.

Leverage – one uses leverage if he borrows money to increase his position in a security. If one uses leverage and makes good investment decisions, leverage can magnify the gain. However, it can also magnify a loss.

Opportunistic – a general term that describes an aggressive strategy with a goal of making money (as opposed to holding on to the money one already has).

***

***

Pairs Trading – usually refers to a long/short strategy where one stock is bought long, and a similar stock is sold short, often within the same industry. Buying the stock of Home Depot and shorting Lowe’s in an equal amount would be an example.

Portfolio Simulation – involves testing an investment strategy by “simulating” it with a database and analytic software. Often referred to as “backtesting” a strategy. The simulated returns of the strategy are compared to those of a benchmark over a specific time frame to see if it can beat that benchmark.

Sharpe Ratio – a measure of risk-adjusted return, computed by dividing a fund’s return over the risk-free rate by the standard deviation of returns. The idea is to understand how much risk was undertaken to generate the alpha.

Short Rebate – if you borrow stock and then sell it short, you have cash in your account. The short rebate is the interest earned on that cash.

R-Squared – a measure of how closely a portfolio’s performance varies with the performance of a benchmark, and thus a measure of what portion of its performance can be explained by the performance of the overall market or index. Hedge fund investors want to know how much performance can be explained by market exposure versus manager skill.

Transportable Alpha – the alpha of one active strategy can be combined with another asset class. For example, an equity market-neutral strategy’s value-added can be “transported” to a fixed income asset class by simply buying a fixed income futures contract. The total return comes from both sources.

Value at Risk – a technique which uses the statistical analysis of historical market trends and volatilities to estimate the likelihood that a specific portfolio’s losses will exceed a certain amount.

Posted on March 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Split-Dollar Life Insurance: An arrangement under which a life insurance policy’s premium, cash values, and death benefit are split between two parties—usually a corporation and a key employee or executive. Under such an arrangement an employer may own the policy and pay the premiums and give a key employee or executive the right to name the recipient of the death benefit.

***

***

Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policy holder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance.

Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

SO – HOW MUCH IS A “FINANCIAL ADVISOR” REALLY WORTH?

This blog holds a rather uncomplimentary opinion of financial advisors, and the financial services and brokerage industry as a whole; deserved, or not? The entire site hints at this attitude as well, in favor of a going it alone or ME, Inc investing when possible. Nevertheless, it is reasonable to wonder how much boost in net-returns might an educated and informed, fee transparent and honest, fiduciary focused “financial advisor” add to a clients’ investment portfolio; all things being equal [ceteris paribus].

And, can it be quantified?

Well, according to Vanguard Brokerage Services®, perhaps as much as 3%? In a decade long paper from the Valley Forge, PA based mutual fund and ETF giant, Vanguard said financial advisors can generate returns through a framework focused on five wealth management principles:

• Being an effective behavioral coach: Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value added: up to 1.50%).

• Applying an asset location strategy: The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value added: from 0% to 0.75%).

• Employing cost-effective investments: This component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value added: up to 0.45%).

• Maintaining the proper allocation through rebalancing: Over time, as investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value added: up to 0.35%).

• Implementing a spending strategy: As the retiree population grows, an advisor can help clients make important decisions about how to spend from their portfolios. (Potential value added: up to 0.70%).

Source: Financial Advisor Magazine, page 20, April 2014.

Assessment

However, Vanguard notes that while it’s possible all of these principles could add up to 3% in net returns for clients, it’s more likely to be an intermittent number than an annual one because some of the best opportunities to add value happen during extreme market lows and highs when angst or giddiness [fear and greed] can cause investors to bail on their well-thought-out investment plans.

And, is the study applicable to doctors and allied healthcare providers? Doe Vanguard have a vested interest in the topic. What about fee based versus fee-only financial advice?

Conclusion

Finally, recognize the plethora of other financial planning life-cycle topics addressed in this ME-P were not included in the Vanguard investment portfolio-only study a decade ago.

And what about today with contemporaneous internet advising, chat-rooms, linkedin, robo-advisors, reddit and the like?

Posted on March 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BANK IDENTIFICATION NUMBER – DEFINED

By Staff Reporters

***

***

What Is a BIN Attack?

The BIN, or the Bank Identification Number, is the first six digits on a credit card. These are always tied to its issuing institution – usually a bank. In a BIN attack, fraudsters use these six numbers to algorithmically try to generate all the other legitimate numbers, in the hopes of generating a usable card number.

How Does a BIN Attack Work?

Fraudsters conduct BIN attacks by generating hundreds of thousands of possible credit card numbers and testing them out.

A fraudster looks up the BIN of the bank they will target. Ranging from four to six digits, this information is in the public domain and is thus easy to source.

Using dedicated software such as an auto-dialer, they generate thousands, often tens of thousands, combinations of possible existing card numbers by this issuer.

At this point, these credentials need to be tested. The fraudster identifies a suitable online shop or donation page.

They start card testing by attempting a small payment with each generated card number.

They keep track of the small percentage of card details that worked, which they are ready to use in earnest for their fraudulent pursuits.

***

***

Remember that the fraudster will start off with only six digits, yet there are many more card details required for a successful transaction. If those are entered erroneously, the transaction will decline. This includes the CVV number, the expiration date, as well as likely address verification service (AVS) failures. Card testing transactions are executed remotely in a fast fashion, so distance checks should also be a hint as well as velocity alerts.

Fraudsters may use bad merchant accounts directly for this purpose, or more frequently involve multiple online stores and services during a BIN attack, as their attempts keep getting blocked at most outlets.

When analyzing a set of financial statements to determine practice value, adjustments (normalizations) generally are needed to produce a clearer picture of likely future income and distributable cash flow. It also allows more of an “apples to apples” line item comparison. This normalization process usually consists of making three main adjustments to a medical practice’s net income (profit and loss) statement.

1. Non-Recurring Items: Estimates of future distributable cash flow should exclude non-recurring items. Proceeds from the settlement of litigation, one-time gains/losses from the selling of assets or equipment, and large write-offs that are not expected to reoccur, each represent potential nonrecurring items. The impact of nonrecurring events should be removed from the practice’s financial statements to produce a clearer picture of likely future income and cash flow.

2. Perquisites: The buyer of a medical practice may plan to spend more or less than the current doctor-owner for physician executive compensation, travel and entertainment expenses, and other perquisites of current management. When determining future distributable cash flow, income adjustments to the current level of expenditures should be made for these items.

3. Non-cash Expenses: Depreciation expense, amortization expense, and bad debt expense are all non-cash items which impact reported profitability. When determining distributable cash flow, you must analyze the link between non-cash expenses and expected cash expenditures.

The annual depreciation expense is a proxy for likely capital expenditures over time. When capital expenditures and depreciation are not similar over time, an adjustment to expected cash flow is necessary. Some practices reduce income through the use of bad debt expense rather than direct write-offs. Bad debt expense is a non-cash expense that represents an estimate of the dollar volume of write-offs that are likely to occur during a year. If bad debt expense is understated, practice profitability will be overstated.

***

***

Balance Sheet Adjustments

Adjustments also can be made to a practice’s balance sheet to remove non-operating assets and liabilities, and to restate asset and liability value at market rates (rather than cost rates). Assets and liabilities that are unrelated to the core practice being valued should be added to or subtracted from the value, depending on whether they are acquired by the buyer.

Examples include the asset value less outstanding debt of a vacant parcel of land, and marketable securities that are not needed to operate the practice. Other non-operating assets, such as the cash surrender value of officer life insurance, generally are liquidated by the seller and are not part of the business transaction.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

The Power of Attorney Mistake That Could Cost You Everything

By Rick Kahler CFP®

***

***

Recently, reading a training manual on elder abuse, I was reminded of a financial risk that is often overlooked. One of the fastest and easiest ways to unravel your financial security is to have the wrong person gain control of your money.

The example in the manual mirrored a heartbreaking situation I once experienced with a long-term client. As her mental and physical health declined, this single woman moved into assisted living. Her newly designated power of attorney, a relative from out of town, took control of her financial affairs.

Almost immediately, without consulting us, the relative began making large withdrawals, closed her accounts, and transferred funds elsewhere. They challenged the financial plan, investments, and strategies we had established to safeguard the client’s financial security and provide for her long-term care. Even though their actions threatened the client’s wellbeing, we were powerless to stop them. Our only recourse was to report the behavior to the authorities.

This heartbreaking and frustrating experience underscored just how critical it is to be mindful when executing a Power of Attorney. Besides designating someone you trust, it is wise to build in safeguards to prevent even a well-meaning relative from inadvertently derailing a carefully constructed financial plan.

***

***

One such safeguard is to include a financial advisor in your POA—as long as that person is a fee-only, fiduciary advisor with an obligation to act in your best interests. In many cases, advisors are hesitant to suggest this option because they are sensitive to the potential conflict of interest and do not want to appear self-serving. An unfortunate reality is that you should be cautious if an advisor, particularly one who sells products on commission, seems eager to be added to your POA.

Including your financial advisor in your POA does not mean you designate them as your agent to manage your affairs. Instead, you include a clause naming them as the professional of record you want your designated agent to continue working with. This creates continuity and accountability. It prevents your agent from replacing your advisor with someone who may be unfamiliar with your needs and goals, unqualified, or untrustworthy.

Your advisor might also recommend adding a secondary safeguard, such as naming an attorney or accountant to oversee the selection of a successor advisor in case your current advisor is unable to continue. This additional layer of protection ensures that the financial professionals guiding your portfolio remain aligned with your best interests. Taking these extra steps can save you—and your loved ones—from significant financial stress down the road.

Including safeguards in your POA is not about mistrusting your loved ones, but about equipping them with the right resources and support to act in your best interest. Financial management is complex, and it requires expertise that most people, even those with the best intentions, may not possess.

One of the hardest parts about planning for diminished financial capacity is the emotional aspect. No one likes to imagine a time when they might not be able to manage their own money. But in reality, taking steps now to protect your financial future is the ultimate act of control. It can help ensure that your wishes are respected and the financial foundation you’ve worked so hard to build remains intact.

Remember, too, that avoiding conversations often increases financial vulnerability. If you don’t have a POA or aren’t comfortable with what you do have, now is the time to bring it up with your advisor, attorney, or a trusted family member. These safeguards are about protecting yourself. They also support those you will rely on to care for you and your financial legacy,

According to Patricia Salber MD [personal communication], there are a number of reasons why direct patient access to laboratory medical results is a good idea:

Between 8 and 26% of abnormal test results, including those suspicious for cancer, are not followed up in a timely manner. Direct access could help reduce the number of times this occurs

Self-management, particularly of chronic illness has known benefits. Just like the QS people, many folks with chronic illness obtain and manage to self-acquired lab results every day via gluco-meters, home pulmonary function tests, blood pressure measurements, and so forth. Direct access to laboratory-acquired data, one could argue is a continuation of that personal responsibility

Patients want to be notified about their results in what they perceive as a timely fashion. In one study, patients who received direct notification of their bone density tests results were more likely to perceive they had timely notification compared to usual care even though there was no measurable effect on actual treatment received after three months

Being more responsible for test results could encourage consumers to try to learn more about the meaning of the test results, conceivably increasing their health literacy.

But, the arguments against direct access discussed include the following:

Patients prefer their physicians contact them directly when they have abnormal test results, although the major studies published in 2005 and 2009, preceded the extraordinary use of the internet to access health information that exists today.

There is concern over whether patients will know what to do when they receive the results – will they make erroneous interpretations or fail to contact their docs? This could be, but the intent of the proposed rule is shared access to the results. We suspect if the rule become law, docs will develop better notification mechanisms so that they reach the patient before the patient directly accesses the results or lab companies will design better lab test notifications with easy-to-understand interpretations or a whole new industry will appear that can provide instantly available individualized lab interpretation…or maybe all three of these would happen and that would be a very good thing.

Unknown impact of dual notification (doctors and patients) of lab test results on physician behavior…would docs simply shift responsibility for initiating follow-up care from themselves to their patients?

Would direct access of life-changing lab tests, such as HIV or malignancy, lead to unnecessary patient anxiety – or worse? (Conversely, is there less anxiety, desperation, or suicidal ideation if the bad news is delivered face to face?

Individuals likely may contact their physicians immediately after getting the lab results asking for a telephonic or face-to-face interpretation … it is not known how this would impact physician workload and/or potential for reimbursement [personal communication, Richard Hudson DO, Atlanta, GA].