BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

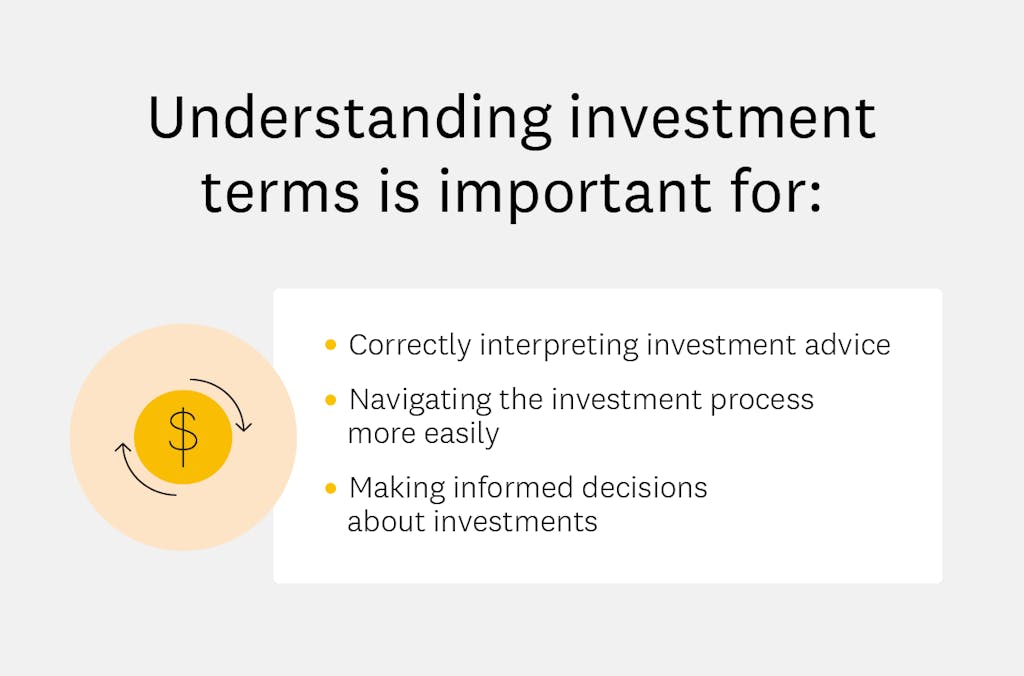

Here is a list of the most common and helpful investment terms you’ll come across and should know.

Ask. The price that someone looking to sell stock wants to receive.

Bid. The price that someone is willing to pay for stock.

Buy. To acquire shares and thereby take a position in a company.

Sell. To get rid of shares whether because you’ve reached your goal or to prevent losses.

Bull market. Market conditions in which investors expect prices to rise.

Bear market. Market conditions in which investors expect prices to fall.

Dividend. A portion of a company’s earnings paid to shareholders.

Blue chip stocks. Shares of large and well-recognized companies that have a long history of solid financial performance.

Earning per share. A company’s net profit divided by the number of outstanding common shares.

Mutual fund. A collection of investments — stocks, bonds, commodities, and more — bundled together and held in common by a group of investors.

Asset. Something you own that could generate a return in the form of more assets.

Asset allocation. Your investment strategy, essentially — the mix of assets you choose to put your money into, whether that be cash, bonds, stocks, commodities, real estate or something else.

Broker. A person or firm — or robot — that arranges transactions between buyers and sellers in exchange for a commission (that is, a fee).

Capital gain (or capital loss). The money you make (or lose) on the sale of an asset.

Diversification. Investing in a variety of sectors, such as health care, energy and IT as well as across different geographic locations.

Dow Jones Industrial Average. A price-weighted list of 30 blue-chip stocks. It’s often used to help get a sense of the overall health of the stock market, even though it only reflects a small portion of the players.

Index fund. A type of mutual fund or exchange-traded fund that allows you to invest in a portfolio that mimics a market index, which is basically a list that tracks the performance of a group of investments either for a specific sector or the overall market.

Hedge fund. A type of investment partnership. Partners pool money from investors and try out a few different investing strategies. Generally, hedge funds will make riskier investments than your typical investor. They’ll also often use leverage (that is, borrowed money) or place bets against the market to get bigger returns. They make their money by charging their investors management fees based on a percentage of their profits.

Expense ratio. The percentage-based fee that mutual fund managers charge you to manage your investments.

Market price. How much it would cost right now to buy or sell an asset or service.

Securities and Exchange Commission (SEC). An independent government body that was created to protect investors and the national banking system. The SEC enforces laws that maintain orderly, fair and efficient markets.

Short selling. A tactic available to investors who predict a stock’s price is about to drop. An investor borrows a quantity of shares through a broker and then sells them, intending to repurchase them later, at a lower price, and return them to the lender.

Stock exchange. A place buyers and sellers come together to buy, sell and trade stock during set business hours. The New York Stock Exchange (NYSE) is the most important stock exchange in the world, but there are a total of 16 exchanges around the world.

Stock market. Refers in general to the collection of markets and exchanges where the buying, selling and trading of investment vehicles takes place.

Price per share. A simple way of calculating a company’s market value at a given moment. To find the price per share, you take a company’s most recent share price and multiply it by its total number of outstanding shares.

Prospectus. A legal document that contains in-depth information about anything you might be planning to invest in: stocks, bonds or mutual funds.

Although many academics argue that value stocks outperform growth stocks, the returns for individuals investing through mutual funds demonstrate a near match.

Introduction

A 2005 study Do Investors Capture the Value Premium? written by Todd Houge at The University of Iowa and Tim Loughran at The University of Notre Dame found that large company mutual funds in both the value and growth styles returned just over 11 percent for the period of 1975 to 2002. This paper contradicted many studies that demonstrated owning value stocks offers better long-term performance than growth stocks.

The studies, led by Eugene Fama PhD and Kenneth French PhD, established the current consensus that the value style of investing does indeed offer a return premium. There are several theories as to why this has been the case, among the most persuasive being a series of behavioral arguments put forth by leading researchers. The studies suggest that the out performance of value stocks may result from investors’ tendency toward common behavioral traits, including the belief that the future will be similar to the past, overreaction to unexpected events, “herding” behavior which leads at times to overemphasis of a particular style or sector, overconfidence, and aversion to regret. All of these behaviors can cause price anomalies which create buying opportunities for value investors.

Another key ingredient argued for value out performance is lower business appraisals. Value stocks are plainly confined to a P/E range, whereas growth stocks have an upper limit that is infinite. When growth stocks reach a high plateau in regard to P/E ratios, the ensuing returns are generally much lower than the category average over time.

Moreover, growth stocks tend to lose more in bear markets. In the last two major bear markets, growth stocks fared far worse than value. From January 1973 until late 1974, large growth stocks lost 45 percent of their value, while large value stocks lost 26 percent. Similarly, from April 2000 to September 2002, large growth stocks lost 46 percent versus only 27 percent for large value stocks. These losses, academics insist, dramatically reduce the long-term investment returns of growth stocks.

***

***

However, the study by Houge and Loughran reasoned that although a premium may exist, investors have not been able to capture the excess return through mutual funds. The study also maintained that any potential value premium is generated outside the securities held by most mutual funds. Simply put, being growth or value had no material impact on a mutual fund’s performance.

Listed below in the table are the annualized returns and standard deviations for return data from January 1975 through December 2002.

Index Return SD

S&P 500 11.53% 14.88%

Large Growth Funds 11.30% 16.65%

Large Value Funds 11.41% 15.39%

Source: Hough/Loughran Study

The Hough/Loughran study also found that the returns by style also varied over time. From 1965-1983, a period widely known to favor the value style, large value funds averaged a 9.92 percent annual return, compared to 8.73 percent for large growth funds. This performance differential reverses over 1984-2001, as large growth funds generated a 14.1 percent average return compared to 12.9 percent for large value funds. Thus, one style can outperform in any time period.

However, although the long-term returns are nearly identical, large differences between value and growth returns happen over time. This is especially the case over the last ten years as growth and value have had extraordinary return differences – sometimes over 30 percentage points of under performance.

This table indicates the return differential between the value and growth styles since 1992.

YEARLY RETURNS OF GROWTH/VALUE STOCKS

Year

Growth

Value

1992

5.1%

10.5%

1993

1.7%

18.6%

1994

3.1%

-0.6%

1995

38.1%

37.1%

1996

24.0%

22.0%

1997

36.5%

30.6%

1998

42.2%

14.7%

1999

28.2%

3.2%

2000

-22.1%

6.1%

2001

-26.7%

7.1%

2002

-25.2%

-20.5%

2003

28.2%

27.7%

2004

6.3%

16.5%

2005

3.6%

6.1%

2006

10.8%

20.6%

2007

8.8%

1.5%

2008

-38.43%

-36.84%

2009

37.2%

19.69%

2010

16.71%

15.5%

2011

2.64%

0.39%

2012

15.25%

17.50%

Source: Ibbottson.

Between the third quarter of 1994 and the second quarter of 2000, the S&P Growth Index produced annualized total returns of 30 percent, versus only about 18 percent for the S&P Value Index. Since 2000, value has turned the tables and dramatically outperformed growth. Growth has only outperformed value in two of the past eight years. Since the two styles are successful at different times, combining them in one portfolio can create a buffer against dramatic swings, reducing volatility and the subsequent drag on returns.

Assessment

In our analysis, the surest way to maximize the benefits of style investing is to combine growth and value in a single portfolio, and maintain the proportions evenly in a 50/50 split through regular rebalancing. Research from Standard & Poor’s showed that since 1980, a 50/50 portfolio of value and growth stocks beats the market 75 percent of the time.

Conclusion

Due to the fact that both styles have near equal performance and either style can outperform for a significant time period, a medical professional might consider a blending of styles. Rather than attempt to second-guess the market by switching in and out of styles as they roll with the cycle, it might be prudent to maintain an equal balance your investment between the two.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

A psychological paradox is a figure of speech that can seem silly or contradictory in form, yet it can still be true, or at least make sense in the context given.

This is sometimes used to illustrate thoughts or statements that differ from traditional ideas. So, instead of taking a given statement literally, an individual must comprehend it from a different perspective. Using paradoxes in speeches and writings can also add wit and humor to one’s work, which serves as the perfect device to grab a reader or a listener’s attention and/or persuade them to action, sales and closing statements. But paradoxes for the financial sector can be quite difficult to explain by definition alone, which is why it is best to refer to a few examples to further your understanding.

One good psychological paradox example is The Paradox of Thrift which suggests that while saving money is generally considered a prudent financial behavior, excessive saving during times of economic downturn can actually hinder economic recovery. When consumers collectively reduce their spending and increase their savings, it creates a decrease in aggregate demand. This reduction in demand can lead to lower production levels, job losses, and ultimately a decline in economic output. In other words, what may be individually rational behavior (financial saving) can have negative consequences for the overall economy.

The following paradoxical contradictions will help financial advisors guide clients to close more sales to the benefit of both.

____

In the intricate world of finance sales, advisors are often at the crossroads of various paradoxes that challenge client decision-making. While the journey towards financial security involves calculated strategies, it’s the nuanced understanding of paradoxes that can help the advisor close more sales.

____

But, what seems trueabout money often turns out to be false, according to colleague Finance Professor John Goodell, PhD from the University Akron:

The more we try to trade our way to profits, the less likely we are to profit.

The more boring an investment—think index funds—the more exciting the long-run performance will probably be.

The more exciting an investment—name your latest Wall Street concoction, Special Purpose Acquisition Company [SPAC] or anything crypto—the less exciting the long-term results typically are.

The only certainty is uncertainty and the only constant is change. Today’s market decline will eventually become a bull market, and today’s market leaders will eventually yield to other stocks.

Big market trends play a huge role in investment results, and yet trying to time macroeconomic cycles or guess which market sectors will outperform is a fool’s errand. Many big market rotations are set in motion by something wholly unanticipated, like a virus pandemic or a war.

To be happy when wealthy, we also need to be happy with far less money. The fact is, above a relatively modest income level, no amount of extra money will change our level of happiness. More money might even make us miserable, as many lottery winners have discovered.

The more we hate an investing trait—or any trait for that matter—the more likely it is that we’re resisting seeing that trait in ourselves. It’s what Carl Jung MD called the Shadowof Undesirable Personality Aspects that we hide from ourselves. Do prospects get irritated listening to your unsolicited financial advice? There’s a good chance that you often give unsolicited financial advice but don’t like to admit it.

The more we learn about investing, the more we realize we don’t know anything. We should just buy index funds and instead spend our time worrying about stuff we can actually control.

The more an investor is convinced he’s right, the more likely he is to be wrong. Short sellers, in particular, are likely to succumb to this paradoxical trap.

The more options we have, the less satisfied we’ll be with each one. This is the Paradox of Choice; revised. Anyone who has spent hours “optimizing” his or her portfolio knows this all too well. Its close cousin is information overload, another frustration paradox when investing.

The more afraid we are of losing money, the more likely we are to take unwitting risks that lose us money. Sitting in cash seems wise during market selloffs. But the truth is, none of us can reliably time the market. Pull up any chart of the stock market over any period longer than a decade and you’ll see that the riskiest decision is sitting in cash, which gets destroyed by inflation.

The more we think about our investments and look at our financial accounts, the more likely we are to damage our results by buying high because of greed and selling low because of fear. It can pay to look away.

ASSESSMENT

How should you respond to these financial paradoxes? As you plan for your own financial future, as well as your own client prospecting endeavors, embrace the concept of “loosely held views.”

In other words, make financial and client acquisitions plans, but continuously update your views, question your assumptions and paradoxes and rethink your priorities. Years of experience with clients certainly support the futility of trying to help them change their financial behavior by telling them what they “should” know or do.

CONCLUSION

Remember, it is far more useful to listen to client beliefs, fears and goals, and to suggest options and offer encouragement to help them discover their own path toward financial well-being. Then, incentivize them with knowledge of the above psychological paradoxes to your mutual success!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Marcinko, DE and Hetico, HR: Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2016.

Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York. 2006

Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2015.

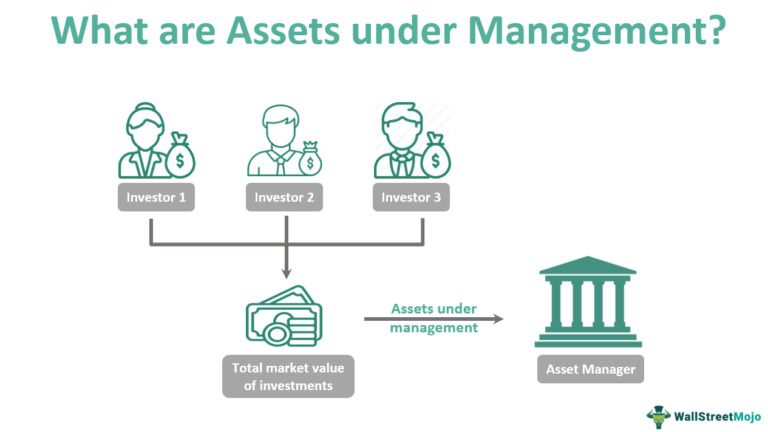

Assets under management (AUM) is a significant parameter in the financial world. It answers financial questions like – how many investments does a company manage? What is the net value of the investments that the company manages? Finally, how many investors have trusted their assets with the company? The higher the answer to these three questions, the more glory to the company.

A wealthy investor who is not concerned by higher fees but wants maximum returns of their asset will probably choose an asset manager based on its AUM. Thus, the AUM indicates the financial performance of the firm. Also, based on the funds under management, the firm collects fees from other clients.

So, what are the investments which qualify as AUM? Any liquid asset of the investor they have entrusted the asset manager with monitoring and control. For example, bank deposits, cash balances, equity shares, bonds, mutual funds, and other investments.

What are the services an asset manager provides to their clients? The most important function is decision-making. With the constant fluctuations and rapid movements in the market, an asset manager has to make decisions about holding or selling an investment. The firm communicates with the investors and advises them about the necessary action.

Once the decision is taken, the firm acts on the decision, i.e., the investor does not have to enter the field. In addition, the asset management company will buy, sell, and make any other transactions on behalf of the investor. Finally, the firm also renders services like accounting, tax reporting, proxy voting (equity shares), client reporting, and other financial services.

What are Assets Under Advisement?

Assets under advisement refer to assets on which your firm provides advice or consultation but for which your firm does either does not have discretionary authority or does not arrange or effectuate the transaction. Such services would include financial planning or other consulting services where the assets are used for the informational purpose of gaining a full perspective of the client’s financial situation, but you are not actually placing the trade.

Assets under advisement could also be those which you monitor for a client on a non-discretionary basis, where you may make recommendations but where the client is the party responsible for arranging or effecting the purchase or sale. A common example of this scenario is when an adviser reviews a participant’s 401(k) allocations. If the adviser does not have the authority or ability to effect changes in the portfolio, these assets are likely considered assets under advisement rather than regulatory assets under management.

Assets under advisement are permitted to be disclosed on Form ADV Part 2A as a separate asset figure from the assets under management. There is no requirement to disclose the assets under advisement figure, but some advisers opt to include the figure to give prospective clients a more complete picture of the firm’s responsibilities. If you choose to report your assets under advisement, be sure to make a clear distinction between this figure and your regulatory assets under management.

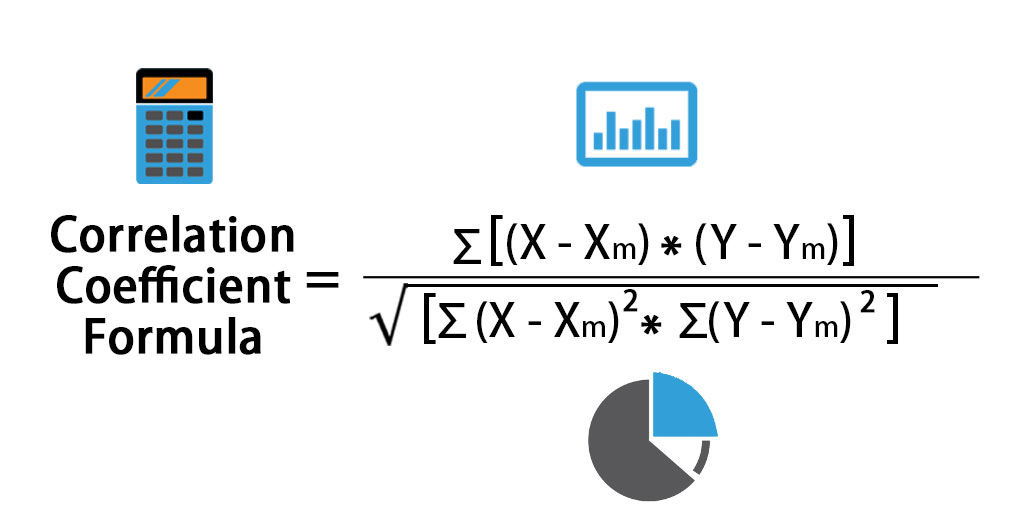

Correlation measures the relationship between two investments–the higher the correlation, the more likely they are to move in the same direction for a given set of economic or market events. Correlation, in the finance and investment industries, is a statistic that measures the degree to which two securities move in relation to each other. Correlations are used in advanced portfolio management, computed as the correlation coefficient which has a value that must fall between -1.0 and +1.0.

So if two securities are highly positively correlated, they will move in the same direction the vast majority of the time. Negatively correlated investments do the opposite–as one security rises, the other falls, and vice versa. No correlation means there is no relationship between the movement of two securities–the performance of one security has no bearing on the performance of the other.

Correlation is an important concept for portfolio diversification--combining assets with low or negative correlations can improve risk-adjusted performance over time by providing a diversity of payouts under the same financial conditions.

Posted on June 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stat: 2%. That’s the portion of Medicaid expansion enrollees who were either not working or in school due to “lack of interest” in finding a job. (Robert Wood Johnson Foundation)

Quote: “It’s just devastating. So much human toil has gone into this. Just when it looked like we could beat this virus, we’re going to give up.”—Dennis Burton, a Scripps Research Institute immunologist, on how a new HIV vaccine was about to start clinical trials before federal funding cuts (NPR)

Read: A look at HHS Secretary RFK Jr.’s new appointees to the CDC vaccine advisory panel. (Stat)

The wait is finally over: USSteel climbed 5.10% after President Trump signed an executive order approving its takeover by Nippon Steel.

Roku jumped 10.43% after announcing a partnership with Amazon that gives advertisers the ability to reach roughly 80% of American households with connected TVs.

AdvancedMicroDevices rose 8.81% on an upgrade from Piper Sandler analysts, who think the semi stock’s AI business will boom.

EchoStar exploded 49.11% after Trump pushed the FCC to resolve its ongoing spectrum dispute with the satellite company.

Victoria’s Secret rose 2.36% on reports that the struggling retailer has attracted the attention of an activist investor.

SageTherapeutics soared 35.37% on the news that it will be acquired by Supernus Pharmaceuticals in a $795 million deal.

MGMResorts climbed 8.10% after the casino company revealed that its Bet MGM online gambling platform is expected to pull in more revenue than previously thought.

Kering, the parent company of Gucci, Yves Saint Laurent, and other luxury brands, popped 12.37% on the news that it has convinced Renault’s CEO to run the company.

What’s down

Sarepta Therapeutics plunged 42.12% after the pharma company reported a second death of a patient taking its Duchenne muscular dystrophy treatment Elevidys.

Reports that Iran wants to end hostilities pushed oil prices lower this afternoon, hurting shares of energy stocks like APACorp (down 2.43%), DevonEnergy (down 1.45%) and ConocoPhillips (down 2.02%).

Alternatively Weighted Exchange Traded Funds are designed to track an index that is constructed based on criteria other than market capitalization (the methodology used for most traditional indexes).

Instead, alternatively weighted indexes select and weight securities based on other factors, such as growth, valuation, and price momentum, among others. Examples include:

Invesco S&P 500 Equal Weight ETF (NYSEARCA: RSP)

SPDR Technology ETF (NYSEARCA: XNTK)

First Trust NYSE Arca Biotechnology Index Fund (NYSEARCA: FBT)

Amplify Online Retail ETF (NASDAQ: IBUY)

iShares MSCI USA Equal Weighted ETF (NYSEARCA: EUSA)

here are many ways for a doctor, osteopath, podiatrist or dentist to financially invest. Traditionally, this meant picking individual stocks and bonds. Today, there are many other ways to purchase securities en mass. For example:

MUTUAL FUND: A regulated investment company that manages a portfolio of securities for its shareholders.

Open End Mutual Funds: An investment company that invests money in accordance with specific objectives on behalf of investors. Fund assets expand or contract based on investment performance, new investments and redemptions. Trade at Net Asset Value or the price the fund shares scheduled with the US Securities and Exchange Commission (SEC) trade. NAV can change on a daily basis. Therefore, per-share NAV can, as well.

Closed End Mutual Funds: Older than open end mutual funds and more complex. A CEMF is an investment company that registers shares SEC regulations and is traded in securities markets at prices determined by investments. Shares of closed-end funds can be purchased and sold anytime during stock market hours. CEMF managers don’t need to maintain a cash reserve to redeem or / repurchase shares from investors. This can reduce performance drag that may otherwise be attributable to holding cash. CEMFs may be able to offer higher returns due to the heavier use of leverage [debt]. They are subject to volatility, less liquid than open-end funds, available only through brokers and may sells at a heavily discount or premium to [NAV] determined by subtracting its liabilities from its assets. The fund’s per-share NAV is then obtained by dividing NAV by the number of shares outstanding. .

Sector Mutual Funds: Sector funds are a type of mutual fund or Exchange-Traded Fund (ETF) that invests in a specific sector or industry such as technology, healthcare, energy, finance, consumer goods, or real estate. Sector funds focus on a particular industry, allowing investors to gain targeted exposure to specific market areas. The goal is to outperform the overall market by investing in companies within a specific sector that is expected to perform well. However, they are also more susceptible to market fluctuations and specific sector risks, making them a more specialized and potentially higher-risk investment option.

EXCHANGE TRADED FUNDS: ETFs are a type of fund that owns various kinds of securities, often of one type. For example, a stock ETF holds stocks, while a bond ETF holds bonds. One share of the ETF gives buyers ownership of all the stocks or bonds in the fund. If an ETF held 100 stocks, then those who owned the fund would own a stake – albeit a very tiny one – in each of those 100 stocks.

ETFs are typically passively managed, meaning that the fund usually holds a fixed number of securities based on a specific preset index of investments. These are tax efficient. In contrast, many mutual funds are actively managed, with professional investors trying to select the investments that will rise and fall.

The Standard & Poor’s 500 Index is perhaps the world’s best-known index, and it forms the basis of many ETFs. Other popular indexes include the Dow Jones Industrial Average and the National Association of Securities Dealers Automated Quotations [NASDAQ] Composite Index.

ETFs based on these funds are called Index Funds and just buy and hold whatever is in the index and make no active trading decisions. ETFs trade on a stock exchange during the day, unlike mutual funds that trade only after the market closes. With an ETF you can place a trade whenever the market is open and know exactly the price you’re paying for the fund.

INDEX FUNDS: Index funds mirror the performance of benchmarks like the DJIA. These passive investments are an unimaginative way to invest. Passive index funds tracking market benchmarks accounted for just 21% of the U.S. equity fund market in 2012. By 2024, passive index funds had grown to about half of all U.S. fund assets. This rise of passive funds has come as they often outperform their actively managed peers. According to the widely followed S&P Indices Versus Active (SPIVA) scorecards, about 9 out of 10 actively managed funds didn’t match the returns of the S&P 500 benchmark in the past 15 years.

ASSESSMENT

Investing in individual stocks is psychologically and academically different than investing in the above funds, according to psychiatrist and colleague Ken Shubin-Stein MD, MPH, MS, CFA who is a professor of finance at the Columbia University Graduate School of Business When you buy shares of a company, you are putting all your eggs in one basket. If the company does well, your investment will go up in value. If the company does poorly, your investment will go down. Fund diversification helps reduce this risk.

CONCLUSION

Investing in the above fund types will help mitigate single company security risk.

References:

1. Fenton, Charles, F: Non-Disclosure Agreements and Physician Restrictive Covenants. In, Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. Productivity Press, New York, 2015.

Readings:

1. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017

2. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

4. Shubin-Stein, Kenneth: Unifying the Psychological and Financial Planning Divide [Holistic Life Planning, Behavioral Economics, Trading Addiction and the Art of Money]. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

We make second investment portfolio opinions affordable

Approximately 1 million allopathic physicians, 150,000 dentists, 200,000 osteopaths, 15,000 podiatrists and 6 million nurses often find it difficult to get an unbiased and fiduciary second opinion on their retirement or brokerage accounts. By offering second opinions for a flat fee, the monetary barriers that prevented colleagues from receiving a second opinion in the past have been removed.

We make second investment portfolio opinions convenient

Here’s how we work: you book an initial appointment with us, answer a few preliminary questions and email us your portfolio information. We then provide a second opinion. It is then up to you to incorporate or not.

We make second investment portfolio opinions timely

Financial markets, jobs and colleague age change like the weather. It is not always okay to wait a week, year or more, to seek a professional second financial portfolio opinion. You need to receive an opinion now. That’s where we come in. We are standing by, ready to take your email [MarcinkoAdvisors@outlook.com] and schedule a free initial consultation within two or three days, or less.

We make second investment portfolio opinions accurate

Fiduciary and non-sales orientated second opinions have the power to change financial lives in the long term. We’ve seen it happen many times. What characterizes a good second opinion? Three things: the opinion must be individualized to your investment portfolio[s], informed and results-oriented. That’s the informed fiduciary approach we take. We are colleagues and look forward to working with you.

Posted on June 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

A Basic Overview for Emerging Physician and Medical Professional Investors

By Somnath Basu; PhD, MBA

There are three basic considerations in any investment decision.

1] The first is the understanding of the investment objective or why the investment is being made. While this may seem somewhat irrelevant at first – why would you be investing if you do not know what you are doing – combining investment objectives can pose problems down-stream.

For example, if you are saving for your retirement so that you can afford the retirement lifestyle you desire (the investment objective), your saving plan should not include any savings you are making for your children’s education (a separate investment objective). Compounding the two savings streams in one plan can very easily lead to one or both of the plans failing.

2] The second consideration is the time horizon of the investment. As a rough guide, investments that need to mature in the next 5-7 years can be considered as short term, 8-15 years as medium term and the rest as long term.

3] Finally, and probably the most important consideration of all is the importance you attach (priority) to achieving your investment objective; in other words, how safe and secure should your investments be. For example, if you are 70 years old and considering how you should invest your retirement funds so that your expenses are covered say for the next 25 years, you do not want a large margin of error in how your investments turn out; you can ill afford to be broke when you are older and hence you want your investments to be as secure as possible.

On the other hand, if the investment is for a second home or a boat, for example, you may wish to engage in some risk taking which may help in lowering your upfront investment needs. It is very important for any investor to clearly understand how much loss they can bear from any investment decision.

Decision Matrix

It is useful to express the investment framework described above as a simple decision matrix. Using the matrix (shown below) as a decision support system should clarify and simplify most investment decisions.

Understanding where in the matrix your decision falls is a very good first step of your decision. Both these elements (safety and time) will ultimately decide the kinds of financial instruments that will reside in your portfolio. We will examine the structure of each of the 9 possible combinations shown in the matrix. Before doing so, let us start by examining the various investment alternatives (e.g. stocks, bonds, etc.) since they have an implicit connection with the two dimensions portrayed in our matrix.

Stocks

Stocks are the most well known and popular form of financial investments. Stocks may be further segregated between large cap and small cap stocks, where the term “cap” is surrogate for the size of the underlying corporation or firm.

Stocks may represent investments in both domestic and international companies. Within the international category, stocks may represent corporations registered in developed (safer) or emerging (riskier) markets. In terms of our matrix dimensions, stocks are best suited when the decision is of medium or long term. In terms of safety, large cap (both domestic and international) stocks are the safest, while small cap and emerging market stocks are the most risky. The riskier the stock, the greater are the profit possibilities as are the chances of large losses.

Bonds

The second common type of investment are bonds Generally, bonds are much safer than stocks with the exception of a class of bonds known as high yield (or junk) bonds. Bonds are issued by companies, governments (domestic and international) and other agencies such as local governments (municipal bonds or “munis” which are especially desirable for those in high income tax rate categories) and quasi-government agencies such as Federal Home Loan Bank, Student Loan Administration, Agricultural Cooperative Banks, etc (collectively known as “Agency” bonds such as Ginnie/Fannie/Sallie Mae, Freddie Mac, etc.).

Government bonds are the safest, followed by agency and municipal bonds and then by bonds issues by corporations.

Corporate bonds may be safe (which are assigned credit safety ratings such as AAA, AA, BBB, etc.) or risky (junk bonds with ratings such as BB, CCC, CC etc.).

Bonds can be used for all time horizons, their maturities ranging from 3 months to 30 years. Very short term bond and bond like instruments (with maturities of one year or less) are known as money market securities which are generally safer than most other investments.

Alternate Investments

Other types of investments include real estate (long term, risky), commodities (such as energy, basic building materials, precious metals, etc.) which are also risky and which may be used for both short term and long term purposes and provide a good hedge (counter balance) in an inflationary environment, derivatives (options and futures) which are very risky and typically short term in nature. Derivatives are generally suggested for very sophisticated investors and are best left alone otherwise.

Risk Reduction

A very important feature about investments is that when various types of investments are bundled together in a portfolio, they help to reduce the risk of the investment decision without affecting the profits in a comparable way. This basic aspect of mixing various kinds of investments (stocks, bonds, etc) to reduce risk is known as diversification and it is a “must” for any investment portfolio. It is a “must” because this technique of risk reduction is generally costless (unless you are paying a financial advisor to do this for you) and it is very worthwhile. All other methods of risk reduction have cost implications.

Scenario Matrix

Armed with this nomenclature regarding various investment types we can now go about examining what the 9 combination (Scenario) portfolios may look like for investment purposes.

Starting with Scenario 1, if you wish to make a short term decision that is very important to you and needs to be very safe, investments should be made in very short term bonds (government or treasury bills)and other similar money market (short term, safe) securities. International short term bonds of developed countries may also be included. Such investment products are generally available through mutual funds or Exchange Traded Funds (or ETFs). ETFs are just like mutual funds except that they are usually cheaper, much easier to buy and sell and may provide tax deferral benefits.

If your investment falls in the Scenario 2 category, include agency/municipal bonds as well as some domestic and international (developed country) large cap stocks while for Scenario 3, smaller portions of small cap and emerging market stocks may be added proportionately while reducing some of the safer investments.

If your investment was a Scenario 4 type of investment, corporate large cap stocks (both domestic and international) could be added to agency or corporate (domestic and international) bonds. Before investing in stocks (in any Scenario) for this Scenario 4, a good question to ask is the following: how profitable were stock investments in the last 3-5 years? If the answer is “very profitable” then reduce the proportion of stocks as compared to bonds in the portfolio. If the last few years were not good, then it would be good to increase their comparable shares. The main reason for this “fine tuning” is that the fortunes of stocks (and many other types of investments) follow a cyclical pattern and the cycle is related to the general cycle of economic (GDP) growth and contraction.

It can be seen now how Scenarios 5 and 6 (as also 8 and 9) will follow a similar pattern as before, increasing proportionally in stocks (of all sizes, domestic/international), real estate, commodities, etc. Portfolios falling in these groups may also include some small cap and emerging market stocks as well as high yield or junk bonds. The proportion of these riskier investments would of course be higher for Scenario 6 over Scenario 5 (and Scenario 9 over 8).

For Scenario 7, the investment portfolio would typically resemble one that would be like an opposite of the portfolio in Scenario 1 and would include a greater proportion of large cap (domestic/international) stocks and a much smaller proportion of bonds. As we move towards Scenarios 8 and 9, the portfolios would be dominated by small cap and emerging market stocks as well as junk bonds.

Assessment

In the discussion above, I have tried to generalize the investment decision in a simplifying way. While the discussion may have centered more on stocks and bonds, it is important to note that all portfolios must “diversify” the investment risks by expanding upon the various types of investment products contained in the portfolios. The very fact that a portfolio contains various types of investments will ensure that the portfolio will perform better than those which are not as well diversified. This will be so in spite of any one of the investment types underperforming at any point in time and the diversification benefit will be received consistently over long periods of time. A popular analogy to this diversification benefit is the common phrase of not putting all eggs in one basket.

Editor’s Note: Somnath Basu PhD is program director of the California Institute of Finance in the School of Business at California Lutheran University where he’s also a professor of finance. He can be reached at (805) 493 3980 or basu@callutheran.edu

Conclusion

The above approach to investment decision-making can be considered as a basic template that can be used universally. For those seeking greater sophistication and who have a foundation built on the above model, expert advice is strongly recommended.

And so, your thoughts and comments on this ME-P are appreciated. Financial advisors please chime in on the debate? Is Basu correct; why or why not? Review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, be sure to subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@outlook.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed

And, credible sponsors and like-minded advertisers are always welcomed.

FIVE INVESTING MISTAKES OF DOCTORS; PLUS 1 VITAL TIP

As a former US Securities and Exchange Commission [SEC] Registered Investment Advisor [RIA] and business school professor of economics and finance, I’ve seen many mistakes that doctors must be aware of, and most importantly, avoid. So, here are the top 5 investing mistakes along with suggested guideline solutions.

Mistake 1: Failing to Diversify Investment but Beware Di-Worsification

A single investment may become a large portion of your portfolio as a result of solid returns lulling you into a false sense of security. The Magnificent Seven stocks are a current example:

Apple, up +5,064%% since 1/18/2008

Amazon, up +30,328% since 9/6/2002

Alphabet, up +1,200% since 7/20/2012

Tesla, up +21,713% since 11/16/2012

Meta, up +684% since 2/20/2015

Microsoft, up +22% since 12/21/2023

Nvidia, up +80,797% since 4/15/2005

Guideline: The Magnificent Seven [7] has grown from 9% of the S&P 500 at the end of 2013 to 31% at the end of 2024! That means even if you don’t own them, you’re still very exposed if you have an Index Fund [IF] or Exchange Traded Fund [ETF] that tracks the market. Accordingly, diversification is the only free lunch in investing which can reduce portfolio risk. But, remember the Wall Street insider aphorism that states: “Di-Versification Means Always Having to Say Your Sorry.”

The term “Di-Worsification” was coined by legendary investor Peter Lynch in his book, One Up On Wall Street to refer to over-diversifying an investment portfolio in such a way that it reduces your overall risk-return characteristics. In other words, the potential return rises with an increase in risk and invested money can render higher profits only if willing to accept a higher possibility of losses [1].

A podiatrist can easily fall into the trap of chasing securities or mutual funds showing the highest return. It is almost an article of faith that they should only purchase mutual funds sporting the best recent performance. But in fact, it may actually pay to shun mutual funds with strong recent performance. Unfortunately, many struggle to appreciate the benefits of their investment strategy because in jaunty markets, people tend to run after strong performance and purchase last year’s winners.

Similarly, in a market downturn, investors tend to move to lower-risk investment options, which can lead to missed opportunities during subsequent market recoveries. The extent of underperformance by individual investors has often been the most awful during bear markets. Academic studies have consistently shown that the returns achieved by the typical stock or bond fund investors have lagged substantially.

Guideline: Understand chasing performance does not work.Continually monitor your investments and don’t feel the need to invest in the hottest fund or asset category. In fact, it is much better to increase investments in poor performing categories (i.e. buy low). Also keep in remind rebalancing of assets each year is key. If stocks perform poorly and bonds do exceptionally well, then rebalance at the end of the year. In following this strategy, this will force a doctor into buying low and selling high each year.

Often doctors make their investment decisions under the belief that stocks will consistently give them solid double-digit returns. But the stock markets go through extended long-term cycles.

In examining stock market history, there have been 6 secular bull markets (market goes up for an extended period) and 5 secular bear markets (market goes down) since 1900. There have been five distinct secular bull markets in the past 100+ years. Each bull market lasted for an extended period and rewarded investors.

For example, if an investor had started investing in stocks either at the top of the markets in 1966 or 2000, future stock market returns would have been exceptionally below average for the proceeding decade. On the other hand, those investors fortunate enough to start building wealth in 1982 would have enjoyed a near two-decade period of well above average stock market returns. They key element to remember is that future historical returns in stocks are not guaranteed. If stock market returns are poor, one must consider that he or she will have to accept lower projected returns and ultimately save more money to make up for the shortfall. For example,

The May 6th, 2010, flash crash, also known as the crash of 2:45, was a United States trillion-dollar stock market plunge which started at 2:32 pm EST and lasted for approximately 36 minutes.

And, investors who have embraced the “buy the dip” strategy in 2025 have been handsomely rewarded, with the S&P 500 delivering its strongest post-pull back returns in over three decades.

According to research from Bespoke Investment Group, the S&P 500 has gained an average of 0.36% in the trading session following a down day so far in 2025. The only year with a comparable performance was 2020, which saw a 0.32% average post-dip gain [2].

The most recent example came on May 27, 2025 when the S&P 500 surged more than 2% after falling 0.7% in the final session before the holiday weekend. The rally was sparked by President Trump’s decision to scale back huge previously threatened tariffs on EU —a recurring catalyst behind many of 2025’s rebound.

Guideline: Beware of projecting forward historical returns. Doctors should realize that the stock markets are inherently volatile and that, while it is easy to rely on past historical averages, there are long periods of time where returns and risk deviate meaningfully from historical averages.

Some doctors believe they are “smarter than the market” and can time when to jump in and buy stocks or sell everything and go to cash. Wouldn’t it be nice to have the clairvoyance to be out of stocks on the market’s worst days and in on the best days?

Using the S&P 500 Index, our agile imaginary doctor-investor managed to steer clear of the worst market day each year from January 1st, 1992 to March 31st, 2012. The outcome: s/he compiled a 12.42% annualized return (including reinvestment of dividends and capital gains) during the 20+ years, sufficient to compound a $10,000 investment into $107,100.

But what about another unfortunate doctor-investor that had the mistiming to be out of the market on the best day of each year. This ill-fated investor’s portfolio returned only 4.31% annualized from January 1992 – March 2012, increasing the $10,000 portfolio value to just $23,500 during the 20 years. The design of timing markets may sound easy, but for most all investors it is a losing strategy.

More contemporaneously on December 18th 2024, the DJIA plummeted 2.5%, while the S&P 500 declined 3% and the NASDAQ tumbled 3.5%

Guideline: If it looks too good to be true, it probably is. While jumping into the market at its low and selling right at the high is appealing in theory, we should recognize the difficulties and potential opportunity and trading costs associated with trying to time the stock market in practice. In general, colleagues are be best served by matching their investment with their time horizon and looking past the peaks / valleys along the way.

Mistake 5: Failing to Recognize the Impact of Fees and Expenses

A free dinner seminar or a polished stock-broker sales pitch may hide the total underlying costs of an investment. So, fees absolutely matter.

The first costing step is determining what the fees actually are. In a mutual fund, these costs are found in the company’s obligatory “Fund Facts”. This manuscript clearly outlines all the fees paid–including up front fees (commissions and loads), deferred sales charges and any switching fees. Fund management expense ratios are also part of the overall cost. Trading costs within the fund can also impact performance.

Here is a list of the traditional mutual fund fees:

Front End Load: The commission charged to purchase a fund through a stock broker or financial advisor. The commission reduces the amount you have available to invest. Thus, if you start with $100,000 to invest, and the advisor charges up to an 8 percent front end load, you end up actually investing $92,000.

Deferred Sales Charge (DSC) or Back End Load: Imposed if you sell your position in the mutual fund within a pre-specified period of time (normally one – five years). It is initiated at a higher start percentage (i.e. as high as 10 percent) and declines over a specific period of time.

Operating Fees: Costs of the mutual fund including the management fee rewarded to the manager for investment services. It also includes legal, custodial, auditing and marketing fees.

Annual Administration Fee: Many mutual fund companies also charge a fee just for administering the account – usually under $100-150 per year.

Guideline: Know and understand all fees.

For example: A 1 percent disparity in fees may not seem like much but it makes a considerable impact over a long time period.

Consider a $100,000 portfolio that earns 8 percent before fees, grows to $320,714 after 20 years if the investor pays a 2 percent operating fee. In comparison, if s/he opted for a fund that charged a more reasonable 1 percent fee, after 20 years, the portfolio grows to be $386,968 – a divergence of over $66,000!

This is the value of passive or index investing. In the case of an index fund, fees are generally under 0.5 percent, thus offering even more savings over a long period of time.

One Vital Tip: Investing Time is on Your Side

Despite thousands of TV shows, podcasts, textbooks, opinions and university studies on investing, it really only has three simple components. Amount invested, rate of return and time. By far, the most important item is time! For example:

Nvidia: if you invested $1,000 in 2009, you’d have $338,103 today.

Apple: if you invested $1,000 in 2008, you’d have $48,005 today.

Netflix: if you invested $1,000 in 2004, you’d have $495,679 today.

Unfortunately, this list of investing mistakes is still being made by many doctors. Fortunately, by recognizing and acting to mitigate them, your results may be more financially fruitful and mentally quieting.

REFERENCES:

1. Lynch, Peter: One Up on Wall Street [How to Use What You Already Know to Make Money in the Market]: Simon and Shuster (2nd edition) New York, 2000.

1. Marcinko, DE; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

2. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York, 2006.

3. Marcinko, DE; Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] CRC Press, New York, 2015.

BIO: As a former university Professor and Endowed Department Chair in Austrian Economics, Finance and Entrepreneurship, the author was a NYSE Registered Investment Advisor and Certified Financial Planner for a decade. Later, he was a private equity and wealth manager

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on June 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Tesla climbed another 5.67% on signs that Elon Musk and President Trump are mending fences and on hype around the robotaxi reveal this week.

TSMC rose 2.63% after the semiconductor company reported that its revenue in the month of May rose 39.6% year over year.

Disney rose 2.65% higher a day after agreeing to purchase Comcast’s stake in streaming service Hulu for $438.7 million. Comcast climbed 2.95%.

Solar stocks got a bit of hope after the Wall Street Journal reported that tech companies are lobbying Congress to keep clean energy subsidies in the tax and spending bill. SolarEdge rose 11.81%, and Sunrun gained 7.13%.

Insmed exploded 28.65% thanks to strong results for the biopharma company’s new treatment for pulmonary arterial hypertension.

Casey’s General Store rose 11.59% after the retailer crushed Wall Street’s profit expectations last quarter and raised its dividend.

McDonald’s lost 1.43% thanks to a double downgrade from Redburn Atlantic analysts, who think the fast food titan’s slowing foot traffic and headwinds from obesity drugs will hurt its growth. That’s the company’s third downgrade in three days.

Stocks: Markets meandered higher as investors awaited news from ongoing US & China trade negotiations in London. Commerce Secretary Howard Lutnick said talks were going well and could continue into tomorrow.

Commodities: Oil soared to its highest price since April on hopes that a trade deal between the world’s largest economies could spur demand, but plunged back to earth after the US said oil output will fall next year.

Crypto: After just barely holding on last week, Bitcoin has now stayed above $100,000 for 30 days straight for the first time ever—a signal to traders that there’s a new level of support for the crypto king.

Many doctors are surprised to learn of an alternative investment known as a hedge fund, pooled investment vehicle or private investment fund. Unlike mutual funds, they can be structured in many ways. However, these funds cannot be marketed or advertised, but they are far from illegal or illicit.

In fact, physicians were among the early investors in one the most successful hedge funds. Warren Buffett got his start in 1957 running the Buffett Partnership, a hedge fund not open to the public. His first appearance as a money manager was before a group of physicians in Omaha, Nebraska. Eleven decided to invest some money with him. A few then followed into Berkshire Hathaway Inc, now among the most highly valued companies in the world.

And, more recently, Scion Asset Management® LLC, is a private investment firm founded and led by my eloquent colleague Michael J. Burry, MD and featured in the movie, The Big Short. Other hedge fund mangers of note include: George Soros, Carl Icahn, Ken Griffin, David Tepper, John Paulson and Bill Ackman.

A hedge fund is a limited partnership of private investors whose money is managed by professional fund managers who use a wide range of strategies; including leveraging [debt] or trading of non-traditional assets [real-estate, collectible, commodities, cyrpto-currency, etc] to earn above-average returns. Hedge funds are considered a risky alternative investment and usually require a high minimum investment or net worth. This person is known as an “accredited investor” or “Regulation D” investor by the US Securities Exchange Commission and must have the following attributes:

A net worth, combined with spouse, of over $1 million, not including primary residence

An income of over $200,000 individually, or $300,000 with a spouse, in each of the past two years

The hurdle rate is part of the fund manager’s performance incentive compensation. Also known as a “benchmark,” it is the amount, expressed in percentage points an investor’s capital must appreciate before it becomes subject to a performance incentive fee. Podiatrists should view the hurdle rate as a form of protection or the fee arrangement.

The hurdle rate benchmarks a single year’s performance and may be considered mutually exclusive of any other year, or the hurdle rate may compound each year. The former case is more common. In the latter case, a portfolio manager failing to attain a hurdle rate in the first year will find the effective hurdle rate considerably higher during the second year.

Once a fund manager attains the hurdle rate, the investor’s capital account may be charged a performance incentive fee only on the performance above and beyond the hurdle rate. Alternatively, the account may be charged a performance fee for the entire level of performance, including the performance required to attain the hurdle rate. Other variations on the use of the hurdle rate exist, and are limited only by the contract signed between the fund manager and the investor. The hurdle rate is not generally a negotiating point, however.

Example: A fund charges a performance fee with a 6 percent hurdle rate, calculated in mutually exclusive manner. A podiatrist places $100,000 with the fund. The first year’s performance is 5 percent. The doctor therefore owes no performance fee during the first year because the portfolio manager did not attain the hurdle rate. During year two, the portfolio manager guides the fund to a 7 percent return. Because the hurdle rate is mutually exclusive of any other year, the portfolio manager has attained the 6 percent hurdle rate and is entitled to a performance fee.

High Water Mark

Some hedge funds feature a “high water mark” provision known as a ”loss-carry forward.” As with the hurdle rate, the high water mark is a form of protection. It is an amount equal to the greatest value of an investor’s capital account, adjusted for contributions and withdrawals. The high water mark ensures that the manager charges a performance incentive fee only on the amount of appreciation over and above the high water mark set at the time the performance fee was last charged. The current trend is for newer funds to feature this high water mark, while older, larger funds may not feature it.

Example: A fund charges a 20 percent performance fee with a high water mark but no hurdle rate. A podiatrist contributes $100,000 to the fund. During the first year, the hedge fund manager grows that capital account to $110,000 and charges a 20 percent performance fee, or $2,000. The ending capital account balance and high water mark is therefore $108,000. During year two, the account falls back to $100,000, but the high water mark remains $108,000. During year three, in order for the manager to charge a performance fee, the manager must grow the capital account to a level above $108,000.

Claw Back Provision

Rarely, a hedge fund may provide investors with a “claw back” provision. This term results in a refund to the investor of all or part of a previously charged performance fee if a certain level of performance is not attained in subsequent years. Such refunds in the face of poor or inadequate performance may not be legal in some states or under certain authorities.

ASSESSMENT

Managers of hedge funds, like colleague Dimitri Sogoloff MBA who is the CEO of Horton Point investment-technology firm, often aim to produce returns that are relatively uncorrelated with market indices and are consistent with investors’ desired level of risk.

While hedging may reduce some risks overall, they cannot all be eliminated. According to a report by the Hennessee Group, hedge funds were approximately one-third less volatile between 1993 and 2010.

For a podiatrist who already holds mutual funds and/or individual stocks and bonds, a hedge fund may provide diversification and reduce overall portfolio risk. Consider investing in them with care.

2. Burry, Michael, J: Hedge Funds [Wall Street Personified]. In, Marcinko, DE and Hetico, HR: Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

3. Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. Productivity Press, New York, 2015.

4. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

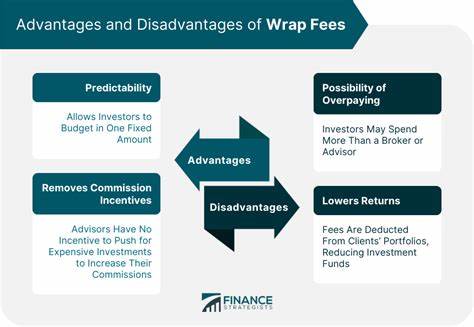

WHAT YOU “MUST KNOW“ ABOUT FINANCIAL ADVISORY FEES

Investment fees still matter despite dropping dramatically over the past several decades due to computer automation, algorithms and artificial intelligence, etc. And, they can make a big difference to your financial health. So, before buying any investment, it’s vital to uncover all real financial advisor and stock broker costs.

1. Up-front salesperson commissions. It is easy to ask; “If I buy this investment today and want to get out tomorrow, how much money do I get back?” If the answer is not “all your money,” the difference is probably upfront fees and commissions. These fees may run as high as 30% of the money invested. If you were to earn 5% a year on the investment, it would take 8 years just to break even.

2. Ongoing advisory fees. These are monthly, quarterly, or annual fees paid to advisors for their investment advice and oversight. This includes working with you to pick the asset classes, set diversification, select a portfolio manager, optimize taxes, re-balance holdings and other periodic tasks.

These fees have many names including wrap fee or investment advisory fees. The normal “rule of thumb” is 1% of assets managed, although fees can range from 0 to 7%. Today, it can even be as low as .5%. It can be charged even if the advisor receives an upfront commission. It can be easy to see, or hidden in the fine print.

3. Additional service fees. Find out specifically what services are included financial advisory fees. Additional fees for financial planning or other services are rarely disclosed. They can range from minimal hand-holding focused on your investments to comprehensive financial planning.

4. Ongoing managerial expense ratio fees. These are incredibly well hidden that you may not see them in your statements or invoices. The only way to know is to read the prospectus or other third party analysis, like Morningstar.com. And, they can vary greatly for the same investment, depending on the class of share you buy.

For example, American Fund’s New Perspective Fund’s expense ratio ranges from 0.45% to 1.54%. The average expense ratio of a mutual fund that invests in stocks is 1.35%. Conversely, the average expense ratio of a Vanguard S&P 500 Fund is 0.10%. The difference of 1.25% is staggering over time.

5. Miscellaneous fees. Some advisors charge $50 – $100 a year per account to open or close an account, and even fees to dollar cost average your funds into the market.

6. Transaction fees. Every time you buy or sell a fund, a fee is typically paid to a custodian. These can range from $5 to hundreds of dollars per transaction.

7. Fee Only: Paid directly by clients for their services and can’t receive other sources of compensation, such as payments from fund providers. Act as a fiduciary, meaning they are obligated to put their clients’ interests first

8. Fee Based: Paid by clients but also via other sources, such as commissions from financial products that clients purchase. Brokers and dealers (or registered representatives) are simply required to sell products that are “suitable” for their clients.

A “suitable” investment is defined by FINRA as one that fits the level of risk that an investor is willing and able, as measured by personal financial circumstances, to take on. The Financial Industry Regulatory Authority is a private American corporation that acts as a Self Regulatory Organization (SRO) that regulates member stock brokerage firms and exchange markets. These criteria must be met. It is not enough to state that an investor has a risk-friendly investment profile. In addition, they must be in a financial position to take certain chances with their money. It is also necessary for them to

A hedge fund is a limited partnership of private investors whose money is managed by professional fund managers who use a wide range of strategies; including leveraging [debt] or trading of non-traditional assets [real-estate, collectible, commodities, cyrpto-currency, etc] to earn above-average returns. Hedge funds are considered a risky alternative investment and usually require a high minimum investment or net worth. This person is known as an “accredited investor” or “Regulation D” investor by the US Securities Exchange Commission and must have the following attributes:

A net worth, combined with spouse, of over $1 million, not including primary residence

An income of over $200,000 individually, or $300,000 with a spouse, in each of the past two years

Choose the fee structure. The fee structure should align with your needs. Consider the type of advice you seek, the number of times needed and the complexity of your financial situation. You can always negotiating tactics are free to ask for a better deal.

Compare fees. It is essential to research and compare different fees. Be sure to read the fine print for details or costs that are not a base fee.

Robo-advisors: For simple investment goals, with little specificity, robo-advisors may be a cost-effective option. They charge lower fees than conventional financial advisors and provide an automated, algorithmic approach to managing your investments.

Assessment

The average cost of working with a human financial advisor in 2024 was 0.5% to 2.0% of assets managed, $200 to $400 per hourly consultation, a flat fee of $1,000 to $3,000 for a one-time service, and/or a 3% to 6% commission fee on the product types sold.

When ruminating over financial advisory fees; read and understand the contract with disclosures, do not sign a confidentiality or non-disclosure agreement, and do not waive your right to a lawsuit. According to colleague Dr. Charles F. Fenton IIII JD, forced legal settlements almost always favor the advisor over the client.

2. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

3. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

As many medical, dental and podiatric colleagues are aware, Environmental, Social and Governance (ESG) investing refers to a set of standards for a company’s behavior used by socially conscious investors to screen potential investments. Over the last decade, or so, I have seen many investors pursing this laudable aim.

Yet, more than 80% of private equity fund managers have now stepped away from at least one deal due to ESG concerns, according to the 2023 BDO Private Capital Survey. The reasons are complex, and point towards fund managers’ sentiment towards risk-reward in the current economic environment.

This retreat from ESG is due to backlash from conservatives who are critical of the idea that mutual fund managers should be considering any other factor but a company’s share holders in their investment decisions. Accusations of “Greenwashing” have also plagued many ESG funds, which is when an asset management firm charging higher fees or a specific thematic fund without actually delivering a unique investment strategic competitive advantage.

Greenwashing is the process of conveying a false impression or misleading information about how a company’s products are environmentally sound. Greenwashing involves making an unsubstantiated claim to deceive consumers and / or investors into believing that a company’s products are environmentally friendly or have a greater positive environmental impact than they actually do. Greenwashing may also occur when a company attempts to emphasize sustainable aspects of a product to overshadow the company’s involvement in environmentally damaging practices.

According to internationally known linguistics and cognitive science Professor,Mackenzie Hope Marcinko PhD of the University of Delaware, greenwashing is performed through the use of environmental imagery, misleading labels, cognitive biases and tendencies hiding tradeoffs. Greenwashing is also a play on the term “Whitewashing,” which means using false information to intentionally hide wrongdoing, errors or an unpleasant situation in an attempt to make it seem less bad than it really is.

To be sure, uncertainty around ESG regulations in the USA is leading financial deal makers to tread carefully. For example, Jim ClaytonMBA, aprivate equity advisor also from the University of Delaware recently stated:

“We’re a year past when the SEC said they were going to issue ESG reporting standards for public filers which has created more noise in the system.”

“People are nervous about what I would call ESG-intense exposed industries, in other words, those with “heavy carbon footprints”.

And, a federal judge in Texas said that American Airlines violated federal law by basing investment decisions for its employee retirement plan on environmental, social, and other non-financial factors. The ruling in January 2025 by US District Judge Reed O’Connor appeared to be the first of its kind amid growing backlash by conservatives to an uptick in socially-conscious investing. O’Connor said American had breached its legal duty to make investment decisions based solely on the financial interests of 401(k) plan beneficiaries by allowing BlackRock, its asset manager and a major shareholder, to focus on environmental, social and corporate governance (ESG) factors.

Even the State of Florida pulled $2 billion from the investment management firm BlackRock in the largest divestment ever made. Florida Governor Ron DeSantis claimed that by taking ESG standards into account when making investment decisions, the firm isn’t prioritizing the financial bottom line for Floridians.

Assessment

But, for a few years at least, things were indeed good. In 2020 and 2021, ESG funds outperformed the market by ~4.3%.

Conclusion

So, always remember [caveat emptor]: let the buyer beware!

2. Marcinko, DE; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017

3. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

According to wikipedia, the S&P 500 Dividend Aristocrats is a stock market index composed of the companies in the S&P 500 index that have increased their dividends in each of the past 25 consecutive years. It was launched in May 2005.

There are other indexes of dividend aristocrats that vary with respect to market cap and minimum duration of consecutive yearly dividend increases. Components are added when they reach the 25-year threshold and are removed when they fail to increase their dividend during a calendar year or are removed from the S&P 500. However, a study found that the stock performance of companies improves after they are removed from the index The index has been recommended as an alternative to bonds for investors looking to generate income.

To invest in the index, there are several exchange traded funds (ETFs), which seek to replicate the performance of the index.

Posted on May 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“