BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on August 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

In today’s dynamic economic landscape, the concept of a “side hustle” has evolved from a mere trend to an essential component of personal financial strategy for many individuals; even doctors.

A side hustle is a way to earn extra income outside of your primary job or main source of employment. It typically involves part-time work, freelancing, small businesses, or gig-based activities that can be pursued flexibly in your free time. Unlike traditional employment, side hustles often offer more autonomy, creative freedom, and the potential to monetize skills, hobbies, or passions.

***

***

Doctor Gigs?

So, if you’re a doctor, dentist or podiatrist considering a side hustle, focus on something sustainable and long-term. Ask yourself: What am I already good at? What do people already ask me to help with? The best side hustles don’t require reinventing the wheel — just monetizing the one you’ve already been pushing uphill.

But, avoid gigs that require a huge upfront investment or promise overnight success. Instead, look for something that offers flexibility, ideally something that works with your schedule, not against your sanity.

Track your earnings and how much time you’re putting in. Side income should support your goals, whether that’s paying off debt, saving for a trip or just breathing easier when office rent comes due.

But, if it’s draining your energy from your medical practice with little to show for it, it might be time to rethink the hustle.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

A Supply Chain Management Strategy

By Staff Reporters

***

***

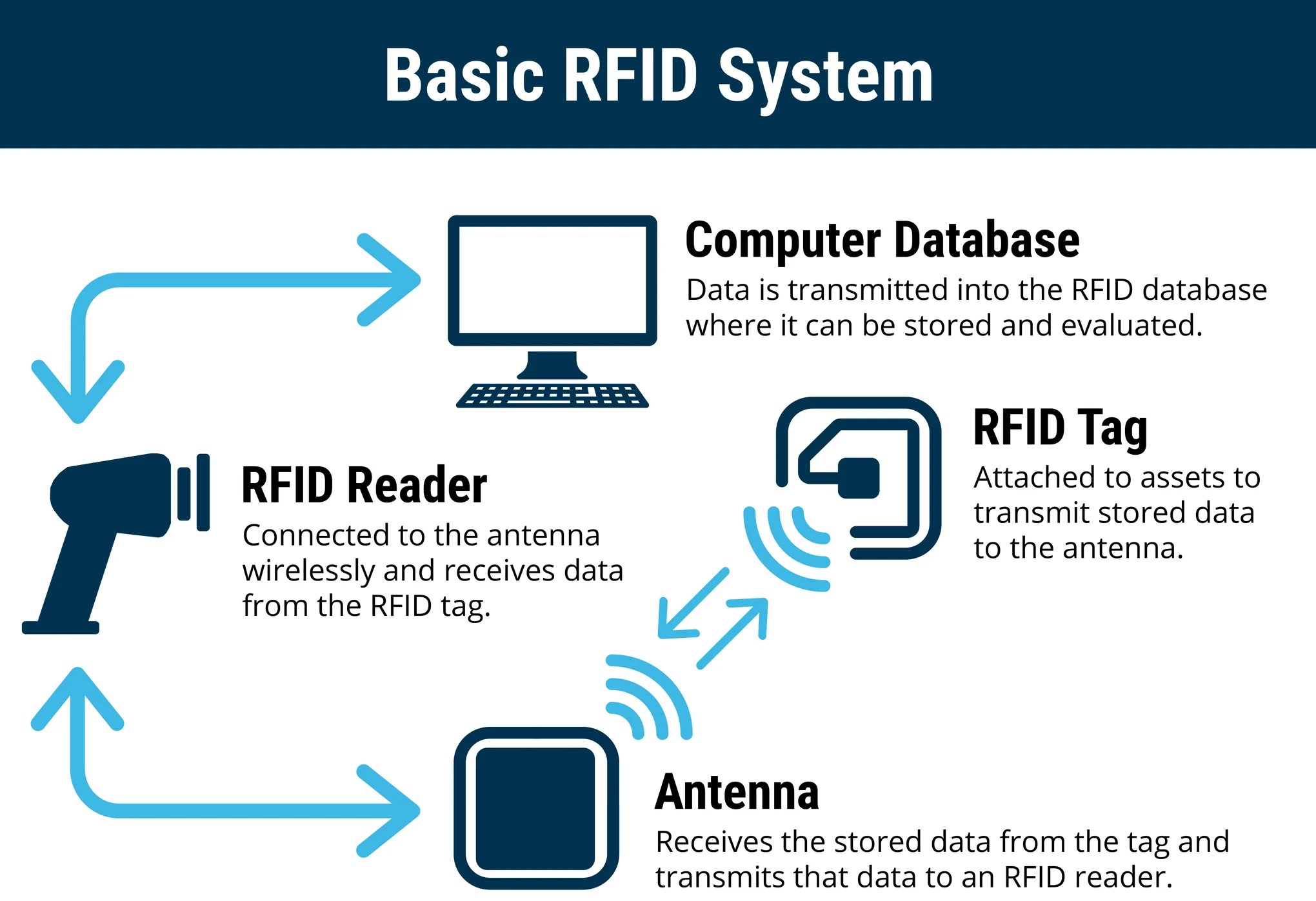

RADIO FREQUENCY IDENTIFICATION

RFID refers to a device attached to an object that transmits data to an RFID receiver. A device can be a large piece of hospital hardware the size of a small book like those attached to ocean containers, or a very small device inserted into a label on a package. RFID has advantages over bar codes such as the ability to hold more data, and to change the stored data as processing occurs. Moreover, it does not require line-of-sight to transfer data, and is very effective in harsh environments where bar-code labels will not work. RFID is not without its own problems, however, as RF signals can be compromised by materials such as metals and liquids.

Although RFID technology is receiving much current attention, it still tends to be cost-prohibitive for some hospital inventory tracking applications. As chip prices go down, there will be continued growth in the application of RFID, but, as in the case of 2D bar codes, many hospital warehouse applications simply do not require this added functionality. The low-cost 1D bar code may continue to be the technology of choice for many hospital inventory tracking applications in the short term.

Smart labels are labels with integrated RFID chips. The idea is to produce labels (probably with bar codes) as well as programming the RFID chips embedded in the label. This would provide all current functionality (human- and machine-readable text and bar codes) as well as adding RFID functionality.

Slap-and-ship describes an approach to complying with vendor requirements for physical identification of shipped goods. More recently, slap-and-ship has been used to describe complying With RFID requirements (such as those from large health care systems); however, it is also applicable to any compliance labeling requirement (such as compliance bar-code labels). Slap-and-ship implies meeting the customer’s requirement by applying the bar-code labels or RFID tags, but not utilizing the technology internally.

Finally, anti-skimming bills were first approved by California and Washington State relative to RFID privacy and are focused on making it illegal for criminals or businesses (or criminal businesses) to read and use personal information from RFID-enabled items such as driver’s licenses and credit cards without the owner’s consent.

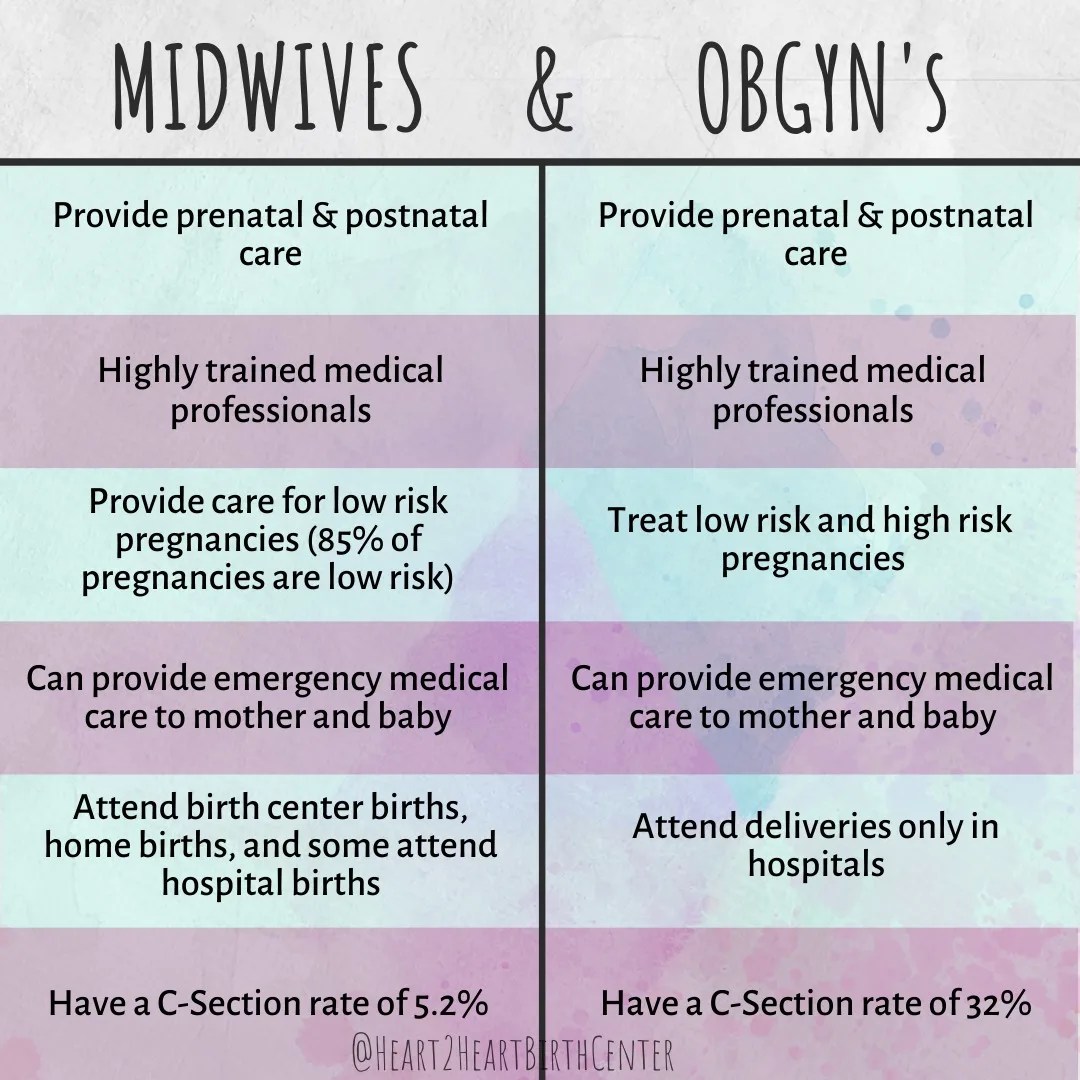

An obstetrician-gynecologist, or OB-GYN, has expertise in female reproductive health, pregnancy, and childbirth. Some OB-GYNs offer a wide range of general health services similar to a primary care doctor. Others focus on the medical care of the female reproductive system. OB-GYNs also provide routine medical services and preventive screenings. This type of doctor has studied obstetrics and gynecology. The term “OB-GYN” can refer to the doctor, an obstetrician-gynecologist, or to the sciences that the doctor specializes in, which are obstetrics and gynecology.

Obstetrician

Obstetrics is the branch of medicine related to medical and surgical care before, during, and after a woman gives birth. Obstetrics focuses on caring for and maintaining a woman’s overall health during maternity. This includes:

pregnancy

labor

childbirth

the postpartum period

OB-GYNs can conduct office visits, perform surgery, and assist with labor and delivery. Some OB-GYNs provide services through a solo or private practice. Others do so as part of a larger medical group or hospital.

***

***

Gynecologist

Gynecology is the branch of medicine that focuses on women’s bodies and their reproductive health. It includes the diagnosis, treatment, and care of women’s reproductive system. This includes the:

vagina

uterus

ovaries

fallopian tubes

This branch of medicine also includes screening for and treating issues associated with women’s breasts. Gynecology is the overarching field of women’s health from puberty through adulthood. It represents most of the reproductive care received during a lifetime. If pregnant, one goes to an obstetrician.

Mid-Wife

Midwives are registered nurses who specialize in midwifery. As such, they’re trained healthcare providers who can oversee low-risk pregnancies, labor, and birth. They can provide other obstetric and gynecological services too. They can do exams and help with basic gynecological concerns like sexually transmitted infections, urinary tract infections, or yeast infections. They help support during labor and in the postpartum period with breastfeeding and birth control.

Doula

Doulas aren’t clinical professionals and can’t give medical advice. They can’t prescribe medicines, and they can’t deliver a baby. But they can offer physical and emotional support during labor—and sometimes during and after pregnancy. Doulas can help with breathing techniques, positional changes, and relaxation strategies during labor. Studies show doulas are associated with fewer C-sections and more vaginal births.

Posted on August 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets struggled to pick a direction as investors took a wait-and-see approach ahead of today’s CPI reading—even as Wall Street worries about the data’s reliability.

Trade: President Trump asked China, the world’s largest soybean buyer, to quadruple its soybean purchases from the US. He also extended the trade war truce with China by 90 days

Commodities: Gold had its worst day in three months as traders waited for the White House to clarify its new tariffs on the key commodity—only for Trump to announce that it won’t be tariffed at all. Meanwhile, Chinese battery giant CATL halted operations at a mine that produces 4% of the world’s lithium, sending prices of the precious metal soaring.

An ophthalmologist is a physician [MD, DO] who undergoes sub-specialty training in medical and surgical eye care. Following a medical degree, a doctor specializing in ophthalmology must pursue additional postgraduate residency training specific to that field. In the United States, following graduation from medical school, one must complete a four-year residency in ophthalmology to become an ophthalmologist. Following residency, additional specialty training (or fellowship) may be sought in a particular aspect of eye pathology.

Ophthalmologists prescribe medications to treat ailments, such as eye diseases, implement laser therapy, and perform surgery when needed. Ophthalmologists provide both primary and specialty eye care—medical and surgical. Most ophthalmologists participate in academic research on eye diseases at some point in their training and many include research as part of their career. Ophthalmology has always been at the forefront of medical research with a long history of advancement and innovation in eye care.

Optometrist

Optometrists focus on regular vision care and primary health care for the eye. After college, they spend 4 years in a professional program and get a doctor of optometry degree. But they don’t go to medical school. Some optometrists get additional clinical training or complete a specialty fellowship after optometry school. They:

Monitor eye conditions related to diseases like diabetes

Manage and treat conditions like dry eye and glaucoma

Provide low-vision aids and vision therapy

There are specialties among optometrists. They include:

Pediatric optometry. These providers work with babies, toddlers, and children, using special techniques to test their vision.

Neuro-optometry. If you have vision problems that result from a brain injury, this is the type of optometrist you might visit.

Low-vision optometry. If you have low vision—that means you can’t see well enough to perform your daily activities and your sight can’t be corrected by glasses or contact lenses, medicine, or surgery—low-vision optometrists offer devices and strategies that can improve your quality of life.

***

***

Optician

An optician is an eye care specialist who helps you choose the right eyeglasses, contact lenses or other vision correction devices. They can’t diagnose or treat conditions that affect your eyes or vision. They’ll work with you to get the right corrective lenses after your optometrist or ophthalmologist gives you a prescription.

Ocularist

An ocularist is an eye care specialist who provides care for people needing prosthetic eyes due to injury, infection or congenital disease (present at birth). Losing or damaging an eye can be a traumatic experience, and the need for a prosthetic can be overwhelming. Ocularists offer long-term care. They collaborate with your healthcare team to create or restore a more natural facial appearance with the goal of enhancing your health-related quality of life.

In the early 1980s, Daniel Kahneman and Amos Tverskey proved in numerous experiments that the reality of decision making differed greatly from the assumptions held by economists. They published their findings in Prospect Theory: An analysis of decision making under risk, which quickly became one of the most cited papers in all of economics.

To understand the importance of their breakthrough, we first need to take a step back and explain a few things. Up until that point, economists were working under a normative model of decision making. A normative model is a prescriptive approach that concerns itself with how people should make optimal decisions. Basically, if everyone was rational, this is how they should act.

Amanda, an RN client, was just informed by her financial advisor that she needed to re-launch her 403-b retirement plan. Since she was leery about investing, she quietly wondered why she couldn’t DIY. Little does her Financial Advisor know that she doesn’t intend to follow his advice, anyway! So, what went wrong?

The answer may be that her advisor didn’t deploy a behavioral economics framework to support her decision-making. One such framework is the “prospect theory” model that boils client decision-making into a “three step heuristic.”

According to colleague Eugene Schmuckler PhD MBA MEd CTS, Prospect theory makes the unspoken biases that we all have more explicit. By identifying all the background assumptions and preferences that clients [patients] bring to the office, decision-making can be crafted so that everyone [family, doctor and patient] or [FA, client and spouse] is on the same page.

1. Simplify choices by focusing on the key differences between investment [treatment] options such as stock, bonds, cash, and index funds.

2. Understanding that clients [patients] prefer greater certainty when it comes to pursuing financial [health] gains and are willing to accept uncertainty when trying to avoid a loss [illness].

3. Cognitive processes lead clients and patients to overestimate the value of their choices thanks to survivor bias, cognitive dissonance, appeals to authority and hindsight biases.

CITE: Jaan E. Sidorov MD [Harrisburg, PA]

Assessment

Much like in healthcare today, the current mass-customized approaches to the financial services industry fall short of recognizing more personalized advisory approaches like prospect theory and assisted client-centered investment decision-making.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

THE ADDICTIVE INVESTING / TRADING PERSONALITY OF DOCTORS

Dr. Donald J. Mandell, a pediatrician, always needs to leave the office fifteen minutes ahead of schedule. The reason is because it takes that long to make the necessary number of trips to ensure the front door is truly locked.

Dr. Kamela A. Shaw, a general surgeon, is constantly rushing to the bath room so that she can wash her hands. As far as she is concerned, it is not possible to get one’s hands clean enough considering the COVID pandemic or recent influenza outbreak.

Although the behaviors displayed by these two doctors are different, they are consistent in that each, to some degree, display behavior that might be called an obsessive-compulsive disorder [OCD].

An obsession is a persistent, recurring preoccupation with an idea or thought. A compulsion is an impulse that is experienced as irresistible.

Obsessive-compulsive individuals feel compelled to think thoughts that they say they do not want to think or to carry out actions that they say are against their will. These individuals usually realize that their behavior is irrational, but it is beyond their control. In general, these individuals are preoccupied with orderliness, perfectionism, and mental and interpersonal control, at the expense of flexibility, openness, and efficiency. Specifically, behaviors such as the following may be seen:

Preoccupation with details.

Perfectionism that interferes with task completion.

Excessive devotion to work and office productivity.

Scrupulous and inflexible about morality (not accounted for by cultural or religious identification);

Inability to discard worn-out or worthless objects without sentimental value;

Reluctance to delegate tasks or to work with others.

Adopts a miserly spending style toward both self and others.

Demonstrates a rigid, inflexible and stubborn nature.

Most people resort to some minor obsessive-compulsive patterns under severe pressure or when trying to achieve goals that they consider critically important. In fact, many individuals refer to this as superstitious behavior. The study habits required for medical students entail a good deal of compulsive behavior.

As the above examples suggest, there are a variety of addictions possible. Recent news accounts have pointed out that even high-level governmental officials can experience sex addiction. The advent of social-media has led to what is referred to as Internet addiction where an individual is transfixed to a computer, tablet PC or smart-phone, “working” for hours on end without a specific project in mind. The simple act of “surfing”, “tweeting-X”, “texting” or merely posting opinions offers the person afflicted with the addiction some degree of satisfaction.

Still another form of addictive behavior is that of the individual with gambling disorder (GD).

GD is recognized as a mental disorder in the American Psychiatric Association’s Diagnostic and Statistical Manual of Mental Disorders-V. This is the behavior of an individual who is unable to resist the impulse to gamble. Many reasons have been posited for this type of behavior including the death instinct; a need to lose; a history of trauma; a wish to repeat a big win; identification with adults the “gambler” knew as an adolescent; and a desire for action and excitement. There are other explanations offered for this form of compulsive behavior. The act of betting allows the individual to express an immature bravery, courage, manliness, and persistence against unfavorable odds. By actually using money and challenging reality, he puts himself into “action” and intense emotion. By means of gambling, the addicted individual is able to pretend that he is favored by “lady luck,” specially chosen, successful, able to beat the system and escape from feelings of discontent.

Greed can also have addictive qualities. In fact, a poll conducted by the Chicago Tribune revealed that folks who earned less than $30,000 a year, said that $50,000 would fulfill their dreams, whereas those with yearly incomes of over $100,000 said they would need $250,000 to be satisfied. More recent studies confirm that goals keep getting pushed upward as soon as a lower level is reached.

Edward Looney, executive director of the Trenton, New Jersey based Council on Compulsive Gambling (CCG) reports that the number of individuals calling with trading-associated problems is doubling annually. In the mid 1980s, when the council was formed, the number of people calling the council’s hotline (1 – 800 Gambler) with stock-market gambling problems was approximately 1.5 percent of all calls received. In 1998 that number grew to 3 percent, and rose to 8 percent by 2012. Today, that number is largely unknown because of its pervasiveness, but Dr. Robert Custer, an expert on compulsive gambling reported, that stock market gamblers represent over 20 percent of the gamblers that he has diagnosed. It is evident that on-line trading presents a tremendous risk to the speculator.

The CCG describes some of the consequences:

Dr. Fred B. is a 43-year-old Asian male physician with a salary above $150,000 and in debt for more than $150,000. He is married with two children. He was a day trader.

Michael Q. is a 28-year-old Hispanic male registered nurse. He is married and the father of one (7 month old) child. He earns $65,000 and lost $50,000 savings in day trading and is in debt for $30,000. He has suicidal ideation.

[B] A Question of Suitability

Since online traders are in it for many reasons, investment suitability rarely enters the picture, according to Stuart Kaswell, general counsel of the Securities Industry Association, in Washington, DC. The kind of question that has yet to be confronted, by day or online trading firms, is a statement, such as: “Equities look good this year. We favor technology stocks. We have a research report on our Web page that looks at the social media industry.” Those kinds of things are seldom considered because they do not involve a specific recommendation of a specific stock, like Apple, Google, Groupon, Facebook or Twitter.

However, if a firm makes a specific recommendation to an investor, whether over the cell-phone, iPad®, fax machine, face-to-face, instagram or over the Internet, or Twitter-X, suitability rules should apply. Opining similarly on the “know your customer” requirements is Steven Caruso, of Maddox, Koeller, Harget & Caruso of New York City. “The on-line firms obviously claim that they do not have a suitability responsibility because they do not want the liability for making a mistake as far as determining whether the investor was suitable or buying any security. I think that ultimately more firms are going to be required to make a suitability, [or eventually fiduciary] determination on every trade”.

[C] On-line Traders and Stock Market Gamblers

Some of the preferred areas of stock market gambling that attract the interest of compulsive gamblers include options, commodities, penny stocks and bit-coins, index investing, new stock offerings, certain types of CAT bonds, crowd-sourcing initiatives, and some contracts for government securities. These online traders and investment gamblers think of themselves as cautious long-term investors who prefer blue chip or dividend paying varieties. What they fail to take into consideration is that even seemingly blue chips can both rise and precipitously drop in value again, as seen in the summer of 2003, the “crash” of 2008, or the “flash crash” of May 6, 2010. On this day, the DJIA plunged 1000 points (about 9%) only to recover those losses within minutes. It was the second largest point swing 1,010.14 points, and the biggest one-day point decline, 998.5 points, on an intraday basis in Dow Jones Industrial Average history.

Regardless of investment choice, the compulsive investment gambler enjoys the anticipation of following the daily activity surrounding these investments. Newspaper, hourly radio and television reports, streaming computer, tablet and smart phone banners and hundreds of periodicals and magazines add excitement in seeking the investment edge. The name of the game is action. Investment goals are unclear, with many participating simply for the feeling it affords them as they experience the highs and lows and struggles surrounding the play. And, as documented by the North American Securities Administrators Association’s president, and Indiana Securities Commissioner, Bradley Skolnik, most day or online traders lose money. “On-line brokerage was new and cutting edge and we enjoyed the best stock market in generations, until the crashes. The message of most advertisements was “just do it”, and you’ll do well. The fact is that research and common sense suggest the more you trade, the less well you’ll do”.

Most day or online traders are young males, some who quit their day jobs before the just mentioned debacles; or more recently with the dismal economy. Many ceased these risky activities but there is some anecdotal evidence that is re-surging again with 2013-14 technology boom and market rise. Most of them start every day not owning any stock, then buy and sell all day long and end the trading day again without any stock – – just a lot of cash. Dr. Patricia Farrell, a licensed clinical psychologist states that day traders are especially susceptible to compulsive behaviors and addictive personalities. Mark Brando, registered principal for Milestone Financial, a day trading firm in Glendale, California states, “People that get addicted to trading employ the same destructive habits as a gambler. Often, it’s impossible to tell if a particular trade comes from a problem gambler or a legitimate trader.”

Arthur Levitt, former Chairman of the Securities and Exchange Commission (SEC) in discussing the risks and misconceptions of investing are only amplified by on-line trading. In a speech before the National Press Club a few years ago, he attempted to impress individuals as to the risks and difficulties involved with day trading. Levitt cited four common misconceptions that knowledgeable medical professionals, and all investors, should know:

Personal computers, tablets, mobile devices and smart-phones are not directly linked to the markets – Thanks to Level II computer software, day traders can have access to the same up-to-the-second information available to market makers on Wall Street. “Although the Internet makes it seem as if you have a direct connection to the securities market, you don’t. Lines may clog; systems may break; orders may back-up.”

The virtue of limit orders – “Price quotes are only for a limited number of shares; so only the first few investors will receive the currently quoted price. By the time you get to the front of the line, the price of the stock could be very different.”

Canceling an order – “Another misconception is that an order is canceled when you hit ‘cancel’ on your computer. But, the fact is it’s canceled only when the market gets the cancellation. You may receive an electronic confirmation, but that only mean your request to cancel was received – not that your order was actually canceled”.

Buying on margin – “if you plan to borrow money to buy a stock, you also need to know the terms of the loan your broker gave you. This is margin. In volatile markets, investors who put up an initial margin payment for a stock may find themselves required to provide additional cash if the price of the stock falls.

How then, can the medical professional or financial advisor tell if he or she is a compulsive gambler? A diagnostic may be obtained from Gamblers Anonymous. It is designed to screen for the identification of problem and compulsive gambling.

But, it is also necessary to provide a tool to be used by on-line traders. This questionnaire is as follows:

1. Are you trading in the stock market with money you may need during the next year?

2. Are you risking more money than you intended to?

3. Have you ever lied to someone regarding your on-line trading?

4. Are you risking retirement savings to try to get back your losses?

5. Has anyone ever told you that spend too much time on-line?

6. Is investing affecting other life areas (relationships, vocational pursuits, etc.)?

7. If you lost money trading in the market would it materially change your life?

8. Are you investing frequently for the excitement, and the way it makes you feel?

9. Have you become secretive about your on-line trading?

10. Do you feel sad or depressed when you are not trading in the market?

NOTE: If you answer to any of these questions you may be moving from investing to gambling.

***

***

The cost of compulsive gambling and day trading is high for the individual medical or lay professional, the family and society at large. Compulsive gamblers, in the desperation phase of their gambling, exhibit high suicide ideation, as in the case of Mark O Barton’s the murderous day-trader in Atlanta who killed 12 people and injured 13 more in July 29th 1999. His idea actually became a final act of desperation.

Less dramatically, for doctors, is a marked increase in subtle illegal activity. These acts include fraud, embezzlement, CPT® up-coding, medical over utilization, excessive full risk HMO contracting, Stark Law aberrations and other “white collar crimes.” Higher healthcare and social costs in police, judiciary (civil and criminal) and corrections result because of compulsive gambling. The impact on family members is devastating. Compulsive gamblers cause havoc and pain to all family members. The spouses and other family members also go through progressive deterioration in their lives.

In this desperation phase, dysfunctional families are left with a legacy of anger, resentment, isolation, and in many instances, outright hate.

[D] Day Trading Assessment

Internet day trading, like the Internet and telecommunications sectors, become something of a investment bubble a few years ago, suggesting that something lighter than air can pop and disappear in an instant. History is filled with examples: from the tulip mania of 1630 Holland and the British South Sea Bubble of the 1700’s; to the Florida land boom of the roaring twenties and the Great Crash of 1929; to the collapse of Japans stock and real estate market in early 1990’s; and to an all-time high of $1,926 for an ounce of commodity gold a few years ago.

Today it is Ask: $3,388.30 USD Bid: $3,367.30 USD

CONCLUSION

To this list, one might again include smart-phone or mobile day trading.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

An acute care inpatient hospital is a health care organization or “anchor hospital” in which a patient is treated for an acute (immediate and severe) episode of illness or the subsequent treatment of injuries related to an accident or trauma, or during recovery from surgery. Specialized personnel using complex and sophisticated technical equipment and materials usually render acute professional care in a hospital setting. Unlike chronic care, acute care is often necessary for only a short time. Measures of acute health care utilization are represented by three separate rates:

Rate of admissions per 1000 patients.

Average length of stay per admission.

Total days of care per 1000 patients.

***

***

Psychiatric Hospital

A psychiatric hospital (behavioral health, mental hospital, or asylum) specializes in the treatment of patients with mental illness or drug-related illness or dependencies. Psychiatric wards differ only in that they are a unit of a larger hospital.

Specialty Hospital

A specialty hospital is a type of health care organization that has a limited focus to provide treatment for only certain illnesses such as cardiac care, orthopedic or plastic surgery, elder care, radiology / oncology services, neurological care, or pain management cases. These organizations are often owned by doctors who refer patients to them. In recent years, single-specialty hospitals have emerged in various locations in the United States. Instead of offering a full range of inpatient services, these hospitals focus on providing services relating to a single medical specialty or cluster of specialties.

Long-Term Care Hospital

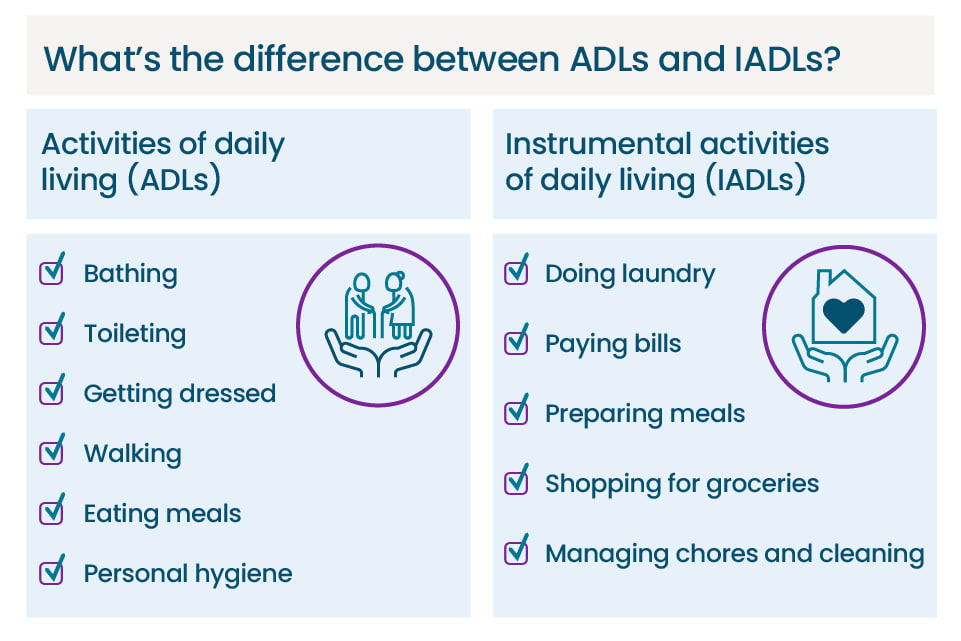

A long-term care hospital is an entity that provides assistance and patient care for the activities of daily living (ADLs), including reminders and standby help for those with physical, mental, or emotional problems. This includes physical disability or other medical problems for 3 months or more (90 days). The criteria of five ADLs may also be used to determine the need for help with the following: meal preparation, shopping, light housework, money management, and telephoning. Other important considerations include taking medications, doing laundry, and getting around outside.

Rural Hospital

The parameters of a rural hospital are determined based on distance. A rural hospital is defined as a hospital serving a geographic area 10 or more miles from the nexus of a population center of 30,000 or more.

More specifically, a rural hospital means an entity characterized by one of the following:

Type A rural hospital—small and remote, has fewer than 50 beds, and is more than 30 miles from the nearest hospital

Type B rural hospital—small and rural, has fewer than 50 beds, and is 30 miles or less from the nearest hospital

Type C rural hospital—considered rural and has 50 or more beds

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

One of the major concepts that most investors should be aware of is the relationship between the risk and the return of a financial asset. It is common knowledge that there is a positive relationship between the risk and the expected return of a financial asset. In other words, when the risk of an asset increases, so does its expected return. What this means is that if an investor is taking on more risk, he/she is expected to be compensated for doing so with a higher return. Similarly, if the investor wants to boost the expected return of the investment, he/she needs to be prepared to take on more risk.

Harry Max Markowitz (August 24, 1927 – June 22, 2023) was an American economist who was a professor of finance at the Rady School of Management at UCSD. He is best known for his pioneering work in modern portfolio theory, studying the effects of asset risk, return, correlation and diversification on probable investment portfolio returns.

One important thing to understand about Modern Portfolio Theory (MPT) is Markowitz’s calculations treat volatility and risk as the same thing. In layman’s terms, Dr. Markowitz uses risk as a measurement of the likelihood that an investment will go up and down in value – and how often and by how much. The theory assumes that investors prefer to minimize risk. The theory assumes that given the choice of two portfolios with equal returns, investors will choose the one with the least risk. If investors take on additional risk, they will expect to be compensated with additional return.

According to MPT, risk comes in two major categories:

Systematic risk – the possibility that the entire market and economy will show losses negatively affecting nearly every investment; also called market risk

Unsystematic risk – the possibility that an investment or a category of investments will decline in value without having a major impact upon the entire market.

***

***

Diversification generally does not protect against systematic risk because a drop in the entire market and economy typically affects all investments. However, diversification is designed to decrease unsystematic risk. Since unsystematic risk is the possibility that one single thing will decline in value, having a portfolio invested in a variety of stocks, a variety of asset classes and a variety of sectors will lower the risk of losing much money when one investment type declines in value. Thus putting together assets with low correlations can reduce unsystematic risks.

Although broad risks can be quickly summarized as “the failure to achieve spending and inflation-adjusted growth goals,” individual assets may face any number of other subsidiary risks:

Call risk – The risk, faced by a holder of a callable bond that a bond issuer will take advantage of the callable bond feature and redeem the issue prior to maturity. This means the bondholder will receive payment on the value of the bond and, in most cases, will be reinvesting in a less favorable environment (one with a lower interest rate)

Capital risk – The risk an investor faces that he or she may lose all or part of the principal amount invested.

Commodity risk – The threat that a change in the price of a production input will adversely impact a producer who uses that input.

Company risk – The risk that certain factors affecting a specific company may cause its stock to change in price in a different way from stocks as a whole.

Concentration risk – Probability of loss arising from heavily lopsided exposure to a particular group of counterparties

Counterparty risk – The risk that the other party to an agreement will default.

Credit risk – The risk of loss of principal or loss of a financial reward stemming from a borrower’s failure to repay a loan or otherwise meet a contractual obligation.

Currency risk – A form of risk that arises from the change in price of one currency against another.

Deflation risk – A general decline in prices, often caused by a reduction in the supply of money or credit.

Economic risk – the likelihood that an investment will be affected by macroeconomic conditions such as government regulation, exchange rates, or political stability.

Hedging risk – Making an investment to reduce the risk of adverse price movements in an asset.

Inflation risk – The uncertainty over the future real value (after inflation) of your investment.

Interest rate risk – Risk to the earnings or market value of a portfolio due to uncertain future interest rates.

Legal risk – risk from uncertainty due to legal actions or uncertainty in the applicability or interpretation of contracts, laws or regulations.

Liquidity risk – The risks stemming from the lack of marketability of an investment that cannot be bought or sold quickly enough to prevent or minimize a loss.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

In order to create and monitor an investment portfolio for personal or institutional use, the physician executive, financial advisor, wealth manager, or healthcare institutional endowment fund manager, should ask three questions:

How much do we have invested?

How much did we make on our investments?

How much risk did we take to get that rate of return?

Introduction to the IPS

Most doctors, and hospital endowment fund executives, know how much money they have invested. If they don’t, they can add a few statements together to obtain a total. But, few can answers the questions above or actually know the rate of return achieved last year; or so far this year. Everyone can get this number by simply subtracting the ending balance from the beginning balance and dividing the difference. But, few take the time to do it. Why? A typical response to the question is, “We’re doing fine.”

Now, ask how much risk is in the portfolio and help is needed [risk adjusted rate of return]. In fact, Nobel laureate Harry Markowitz, Ph.D. said, “If you take more risk, you deserve more return.” Using standard deviation, he referred to the “variability of returns;” in other words, how much the portfolio goes up and down, its volatility [Markowitz, H: Portfolio Selection. Journal of Finance, March, 1952].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

THE FOOT & ANKLE DOCTORS

By A.I.

***

***

Podiatry offers a promising career with a balanced mix of specialization and income. By understanding the factors that influence salaries—such as location, experience, and practice type—a doctor can strategically enhance his/er earning potential. Staying informed about healthcare policies and market trends is crucial for maximizing income.

With an aging population and advancements in technology, the demand for podiatrists is expected to grow, making it a rewarding field both professionally and financially. Investing in specialized training and adapting to policy changes will help doctors remain competitive and successful in the evolving healthcare landscape.

A podiatrist is a healthcare professional specialized in diagnosing and treating conditions related to the feet and ankles. Their responsibilities include performing surgeries, prescribing orthotics, and providing preventive care.

What education is required to become a podiatrist?

To become a podiatrist, one must complete a Doctor of Podiatric Medicine (DPM) degree, which typically takes four years after earning a bachelor’s degree. Following this, a residency program lasting 2-3 years is required for practical training.

What factors influence the salary of a podiatrist?

Geographic location, level of experience, specialization, and type of practice significantly affect a podiatrist’s salary. Areas with a higher cost of living or demand for services usually offer higher salaries.

How does the salary of a podiatrist compare to other medical professions?

Podiatrists generally earn more than general practitioners but less than specialty surgeons. This disparity is due to differences in training length, specialization, and practice complexity among these professions.

Can the salary of a podiatrist increase over time?

Yes, a podiatrist’s salary can increase with additional experience, further specialization, and strategic practice location choices. Continuing education and staying updated on healthcare policies can also enhance earning potential.

What impact do healthcare policies have on podiatrist salaries?

Healthcare policies, including changes in insurance reimbursement rates and government health initiatives, can affect podiatrist salaries. Adapting to these policy shifts is crucial for maximizing earning potential in the field.

What are the future trends in podiatry salaries?

Future trends suggest potential salary growth due to increasing demand from an aging population, technological advancements, and geographic disparities in healthcare access. Keeping informed about these trends can help podiatrists plan their careers strategically.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, hospitals, financial advisory firms, RIAs, or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Classic Definition: Research from Ernst-Young [Nikhil Lele and Yang Shim] uncovered a chasm between how consumer patients think they’re doing financially, and the actual state of their finances. Even more striking, their study suggested that improving consumers’ financial health will become one of the top imperatives in reframing consumer financial services.

Modern Circumstance: For example, the study asked consumers to rate their own financial health, and 83 percent rated themselves “good,” “very good” or “excellent.” Now, contrast this figure with what is known about their actual situation:

60 percent of Americans say they are financially stressed.

56 percent of Americans have less than $10,000 saved for retirement.

40 million American families have no retirement savings at all.

40 percent of Americans are not prepared to meet a $400 short-term emergency.

Paradox Example: Fortunately, even though the vast majority of consumers rate themselves as financially healthy, the study found that most still want to improve. Importantly for health economists, the attractive 25-34 and 35-49 year-old age groups were most likely to be extremely or very interested in improving their financial and economic health.

Paradox Example: Massively affluent consumer patients are even more interested in improving this paradox than their mass market counterparts.

Posted on July 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

A decaying body at the University of Tennessee’s Anthropological Research Facility known as the The Body Farm in Knoxville, where up to 80 bodies at a time are studied as they decay in a variety of different scenarios. (Photo by David Howells/Corbis via Getty Images)

***

The term “body farm” refers to a type of outdoor research facility in which human remains are left to decompose in a variety of environmental conditions naturally. While some individuals may find the concept of a body farm unsettling, these facilities are very useful for forensic science research.

Body farms facilitate the hard (or sometimes outright impossible) research on the various stages of human decomposition, aiming to gain a deeper understanding of how the process can differ under various conditions. This new-found knowledge can then be utilized to assist forensic investigators in determining the time and cause of death and potentially even more information.

Body farms in the US include: California University of Pennsylvania, Sam Houston State University, Texas State University, University of Tennessee at Knoxville, and Western Carolina University.

Posted on July 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

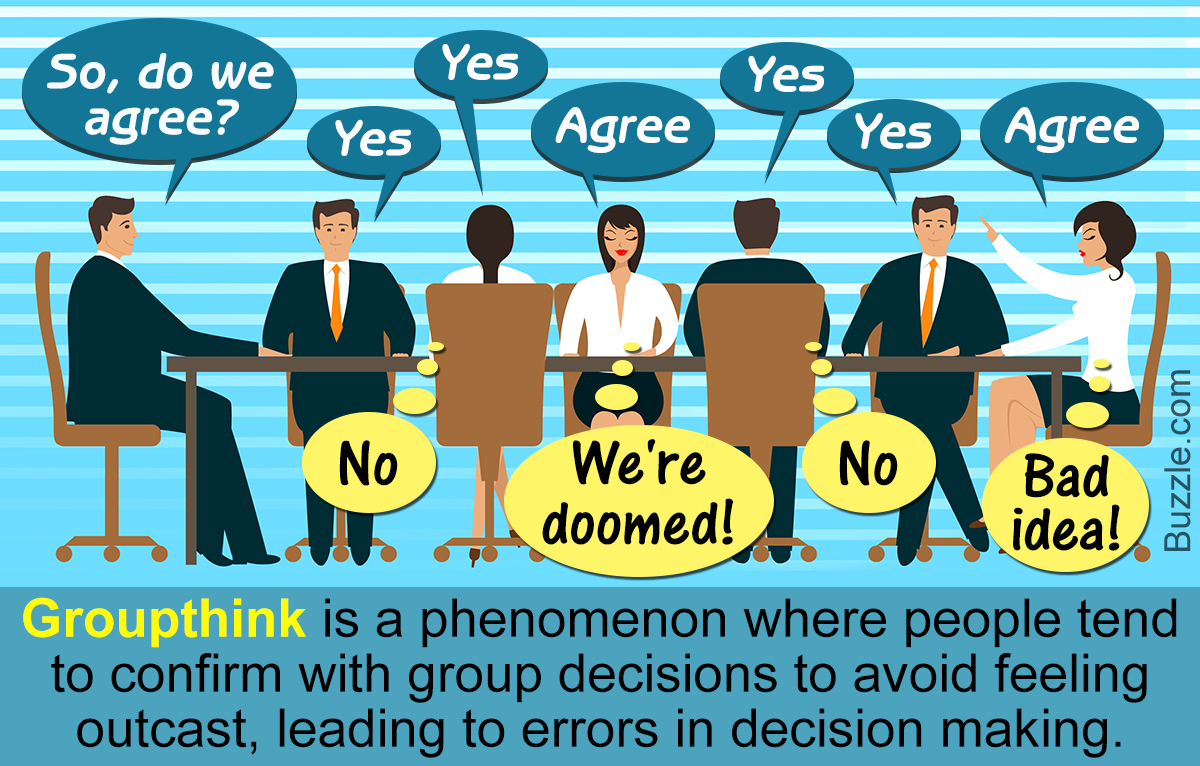

“lemming effect” or “group-think”

By Staff Reporters

***

***

According to psychologist and colleague Dan Ariely PhD, human beings have evolved – probably both genetically and socially – to be consistent. It is easier and safer to deal with others if they honor their commitments and if they behave in a consistent and predictable manner over time. This allows people to work together and build trust that is needed for repeat dealings and to accomplish complex tasks.

In the jungle, this trust was necessary to for humans to successfully work as a team to catch animals for dinner, or fight common threats. In business and life it is preferable to work with others who exhibit these tendencies. Unfortunately, the downside of these traits is that people make errors in judgment because of the strong desire not to change, or be different (“lemming effect” or “group-think”). So the result is that most people will seek out data that supports a prior stated belief or decision and ignore negative data, by not “thinking outside the box”.

Additionally, future decisions will be unduly influenced by the desire to appear consistent with prior decisions, thus decreasing the ability to be rational and objective. The more people state their beliefs or decisions, the less likely they are to change even in the face of strong evidence that they should do so. This bias results in a strong force in most people causing them to avoid or quickly resolve the cognitive dissonance that occurs when a person who thinks of themselves as being consistent and committed to prior statements and actions encounters evidence that indicates that prior actions may have been a mistake. It is particularly important therefore for advisors to be aware that their communications with clients and the press clouds the advisor’s ability to seek out and process information that may prove current beliefs incorrect.

Since this is obviously irrational, one must actively seek out negative information, and be very careful about what is said and written, being aware that the more you shout it out, the more you pound it in.

Posted on July 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP™

***

***

When Maria needed $400,000 for a down payment on a new home, her broker at a large Wall Street firm offered a solution: “Don’t sell investments and trigger capital gains. Just take out a margin loan.”

A margin loan is a line of credit from a brokerage firm, secured by the client’s investment portfolio. It offers quick access to cash with no immediate tax consequences and minimal paperwork. But the convenience comes at a cost. As of mid-2025, margin loan interest rates range from 6.25% to over 11%.

Margin loan recommendations are often presented by brokers as tax-savvy strategies that allow clients to access “tax-free” cash while keeping their portfolios intact. In many cases, however, the math benefits the advisor more than the investor. The cost of borrowing often exceeds what an investor is likely to earn by holding on.

For example, let’s assume an interest rate of 7.5% on Maria’s $400,000 margin loan. While borrowing delayed the payment of $20,000 in capital gains tax, she will eventually have to pay that tax anyway unless she holds the investments until her death. Two years later, with portfolio returns of 4% annually, she had earned around $32,000 from the $400,000 in investments she might have sold. Meanwhile, she had paid $60,000 in interest—leaving her some $28,000 worse off. That’s without factoring in ongoing interest payments, or the risks of a margin call if the investments securing the loan drop in value.

Why do advisors keep recommending margin loans? Because selling investments reduces the portfolio size and the advisor’s fee. Borrowing keeps the portfolio intact and the compensation unchanged—while the firm receives additional income from interest on the loan. In some cases, advisors suggest using margin loans to buy more investments, increasing both the portfolio and the fee they collect.

None of this is illegal. But when the borrowing cost is higher than expected returns and the advisor benefits financially, the ethics are questionable. The client takes the risk, while the advisor keeps the revenue.

This kind of conflict appears more often in portfolios where compensation is tied to asset volume and the company’s primary culture rewards gathering assets over delivering unbiased advice. By contrast, fee-only financial planning and investment advisors typically operate on simpler hourly, flat, or tiered fee structures. Their compensation doesn’t depend on whether a client borrows, sells, or holds. The culture of the firm focuses on conflict-free advice aligned with the client’s best interest.

Wall Street brokers are often held to a fiduciary standard, but structure still matters. In 2024 the SEC reported their examinations of brokers would continue to focus on advisor recommendations unduly influenced by the company’s compensation and incentives.

There are rare situations where a margin loan may be appropriate. A client with large unrealized gains might use a short-term margin loan to minimize taxes. An elderly investor might borrow tax-free rather than sell assets that will receive a step-up in basis at their death. Even in those cases, the math must be exact and the client must clearly understand the risks, including the possibility of a margin call.

If your advisor recommends a margin loan, especially to buy more investments, ask strong questions. What’s the interest rate? What return is realistic? What are the tax consequences of selling? How does this affect the advisor’s income?

In a high-rate, low-return environment, margin loans rarely favor the client. The exceptions are narrow. The risks are significant. And the conflict of interest is measurable.

Sometimes the smartest move is the simplest: sell what you need, pay the tax, and leave leverage out of your plan.

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial planning and investment decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just a few weeks ago.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

Assessment

QUESTION: How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.” In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.

Yes, you can contribute to both a Roth IRA and a 401(k), provided you don’t exceed annual contribution limits for each account.

Determining whether to contribute to a Roth IRA, 401(k), or both can be an important step in planning for your retirement. Here are the key differences, including tax advantages, employer contributions, and investment options.

Eligibility requirements are the first consideration when contributing to a Roth IRA and a 401(k). For Roth IRA contributions, your eligibility is determined by your income. Specifically, if your modified adjusted gross income (MAGI) exceeds certain thresholds, your ability to contribute to a Roth IRA may be reduced or eliminated. However, there are no income limits for contributing to a 401(k), making it accessible to anyone with earned income.

IRS rules do allow for contributions to both a Roth IRA and a 401(k), provided you adhere to the annual contribution limits for each account.

This means you can take advantage of the higher contribution limits of a 401(k) while also benefiting from the tax-free growth of a Roth IRA. This dual approach can be a strategy for maximizing your retirement savings. The advantages to contributing to both accounts present some key benefits, such as:

Tax diversification in retirement, allowing for better management of taxable income.

Potential reduction of overall tax burden.

Maximization of savings potential by taking full advantage of the benefits each account offers.3

Balancing contributions between a Roth IRA and a 401(k) requires careful planning. You might start by contributing enough to your 401(k) to receive the full employer match, which is essentially free money, if your employer offers this. Once you’ve secured the match, consider maxing out your Roth IRA contributions, if you’re eligible.

Posted on July 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The consumer price index, a broad-based measure of goods and services costs, increased 0.3% on the month, putting the 12-month inflation rate at 2.7%, the Bureau of Labor Statistics reported Tuesday. The numbers were right in line with the Dow Jones consensus. Excluding volatile food and energy prices, core inflation picked up 0.2% on the month, with the annual rate moving to 2.9%, also matching the respective estimates.

The Trump administration has launched a probe into drone imports. Drones use polysilicon, a key ingredient for solar panels, and tariffs on the material could help boost profitability for domestic manufacturers like FirstSolar, which rose 6.90%.

National Fuel Gas rose 5.65% after the energy company caught a rare double upgrade from Bank of America analysts, who like the energy company’s improved productivity.

Stocks down

BlackRock fell 5.86% after the world’s largest asset manager reported that a single client pulled $52 billion last quarter.

It wasn’t a great day for other big banks: WellsFargo sank 5.43% after cutting its 2025 net interest income guidance, while JPMorgan Chase lost 0.74% despite beating sales and profit estimates.

Albertsons tumbled 5.02% even though the grocer reported a solid quarter thanks to strong pharmacy sales and digital revenue.

Newmont dropped 5.71% on the news that CFO Karyn Ovelmen is leaving the gold miner.

Also called “qualified” or “statutory” stock options, ISOs are considered tax-advantaged stock options based on U.S. tax law. With ISOs, the spread (the difference between the award price and the fair market value) will count as income for the alternative minimum tax (AMT) in the year you exercise your options.

Example: If you exercise and hold the shares for more than one year past the exercise date and more than two years past the original grant date, the sale of the stock becomes a qualifying disposition, and any realized profit is typically taxed at the long-term capital gains rate. If you sell earlier, the spread will be taxed at your ordinary income tax rate.

ISOs vs. NSOs: What’s the difference?

There are two types of employee stock options: statutory and nonstatutory. They can also be referred to as qualified and nonqualified, respectively. ISOs are statutory (qualified) and differ from nonstatutory (nonqualified) stock options (NSOs) in a few key ways:

Eligibility. ISOs are issued only to employees, whereas NSOs can be granted to outside service providers like advisors, board directors or other consultants. Typically, mainly senior executives or key employees are given ISOs, as a company is not required to offer ISOs to all employees.

Tax perks. ISOs have more compelling tax treatment compared with NSOs.

Posted on July 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Drug and medical device companies paid at least $13.2 billion to medical professionals in 2024, according to CMS data released June 30th. There’s been steady growth in these payments over the last few years, which include everything from research payments to free meals to promotional or conference fees. Drug and medical device companies paid out $13.1 billion in 2023, $13.1 in 2022, and $12.6 in 2021. If you’re a medical provider, you’ve probably gotten one of those perks from a drug or medical device company and thought it wouldn’t affect your decision-making.

But research suggests physicians are more likely to prescribe drugs from companies that pay them, with some studies specifically associating this with drugs that are costlier to patients. “Really well-trained people who affirm an oath to do no harm can be influenced, and are,” Neil Jay Sehgal, associate professor of health systems and population health at the University of Washington School of Public Health, told Healthcare Brew.

Bitcoin is booming, and crypto stocks climbed along with it. MicroStrategy rose 3.86%, RobinhoodMarkets added 1.67%. and Coinbase gained 1.80%.

Boeing rose 1.64% on preliminary reports that investigators have found no evidence of malfunction in the plane that crashed in India last month. Engine-maker GEAerospace also gained 2.71%.

Warner Bros Discovery climbed 2.39% thanks to a strong opening weekend for the new Superman movie.

Autodesk popped 5.05% on the news that it is not pursuing an acquisition of rival software maker PTC. PTC fell 1.25%.

Kenvue, the company behind Band Aids and Listerine, gained 2.18% after kicking its CEO to the curb.

PayPal climbed 3.55% despite the news that JPMorgan will start charging the fintech fees for access to customer data.

Stocks Down

Starbucks sank 1.60% on news that employees will have to return to the office four days a week. Shareholders were also unimpressed with the coffee giant’s new secret menu.

Synopsys stumbled 1.74% after getting regulatory approval from Chinese authorities to acquire software designer Ansys for $35 billion. Ansys rose 3.03% on the news.

Waters plunged 13.81% on the news that it will merge with Becton Dickinson’s bioscience and diagnostic solutions business in a $17.5 billion deal.

RivianAutomotive lost 2.15% thanks to a downgrade from Guggenheim analysts, who forecast soft sales for the automaker’s latest models.

Posted on July 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets shrugged off President Trump’s weekend threat of 30% levies against the EU and Mexico, as well as his proposed 100% secondary tariffs against Russia today. Stocks eked out a win across the board, with the NASDAQ climbing to a new record close.

Commodities: Oil prices fell while gold took a breather, but the big winner was orange juice futures, which hit a four-month high thanks to Trump’s promise of 50% tariffs on all imports from Brazil. Coffee prices also climbed.

According to Leslie Kernisan MD MPH, these are the basic self-care tasks that we initially learn as very young children. They are sometimes referred to as “Basic Activities of Daily Living” (BADLs). They include:

Walking, or otherwise getting around the home or outside. The technical term for this is “ambulating.”

Feeding, as in being able to get food from a plate into one’s mouth.

Dressing and grooming, as in selecting clothes, putting them on, and adequately managing one’s personal appearance.

Toileting, which means getting to and from the toilet, using it appropriately, and cleaning oneself.

Bathing, which means washing one’s face and body in the bath or shower.

Transferring, which means being able to move from one body position to another. This includes being able to move from a bed to a chair, or into a wheelchair. This can also include the ability to stand up from a bed or chair in order to grasp a walker or other assistive device.

If a person is not fully independent with ADLs, then we usually include some information about the amount of assistance they require. ADLs were originally defined in the 1950s by a geriatrician named Sidney Katz, who was trying to define what it might look like for a person to recover to independence after a disabling event such as a stroke or hip fracture. So these measures are sometimes called the “Katz Index of Independence in Activities of Daily Living.”

***

***

Instrumental Activities of Daily Living (IADLs)

These are the self-care tasks we usually learn as teenagers. They require more complex thinking skills, including organizational skills. They include:

Managing finances, such as paying bills and managing financial assets.

Managing transportation, either via driving or by organizing other means of transport.

Shopping and meal preparation. This covers everything required to get a meal on the table. It also covers shopping for clothing and other items required for daily life.

Housecleaning and home maintenance. This means cleaning kitchens after eating, keeping one’s living space reasonably clean and tidy, and keeping up with home maintenance.

Managing communication, such as the telephone and mail.

Managing medications, which covers obtaining medications and taking them as directed.

Because managing IADLs requires a fair amount of cognitive skill, it’s common for IADLs to be affected when an older person is having difficulty with memory or thinking. For those older adults who develop Alzheimer’s disease or a related dementia, IADLs will usually be affected before ADLs are.

IADLs were defined about ten years after ADLs, by a psychologist named M.P. Lawton. Dr. Lawton felt there were more skills required to maintain independence than were listed on the original Katz ADL index, and hence created the “Lawton Instrumental Activities of Daily Living Scale.”

Overconfident Investing Bias happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. This causes the results of a study to be unreliable and hard to reproduce in other research settings.

Example: Data convincingly shows that people and financial planners/advisors and wealth managers who trade most often under-perform the market by a significant margin over time. Active traders lose money.

Example: Overconfidence Investing Bias moreover leads to: (1) excessive trading (which in turn results in lower returns due to costs incurred), (2) underestimation of risk (portfolios of decreasing risk were found for single men, married men, married women, and single women), (3) illusion of knowledge (you can get a lot more data nowadays on the internet) and (4) illusion of control (on-line trading).

The terms “psychologist” and “psychiatrist” are often used interchangeably to describe anyone who provides therapy services, but the two professions and the services they provide differ in terms of content and scope. A major difference between the two types of experts is that psychiatrists can prescribe medication [Rx].

As physicians [MD/DO] psychiatrists are trained to recognize the ways biological processes affect mental functioning.

Psychologists are oriented to how thoughts, feelings, and social factors influence mental functioning.

PSYCHIATRIST

Psychiatrists are medical or osteopathic doctors who are able to prescribe psychotropic medications, which they do in conjunction with providing psychotherapy though medical and pharmacological interventions are often their focus.

PSYCHOLOGIST

Though many psychologists hold doctorate degrees, they are not medical doctors, and most cannot prescribe medications. Rather, they solely provide psycho-therapy, which may involve cognitive and behavioral interventions, psycho-dynamic or psycho-analytic approaches.

NOTEPROTECTED TITLE: The title of “psychologist” can only be used by an individual who has completed the required education, training, and state license requirements. Informal titles, such as “counselor” or “therapist,” are often used as well. Other mental health care professionals, such as licensed social workers, can claim those titles, but not the title of “psychologist.”

Stocks: Jobless claims came in lower than expected, the 30-year US bond auction met with strong demand, and Delta Airlines unofficially kicking off earnings season with a solid report. The S&P 500 and the NASDAQhit record highs.

Crypto: Bitcoin reached a record high for the second day in a row, hitting $113,863.31 today. The crypto’s price has stayed above $100k for 60 consecutive days.

Commodities: Coffee futures in New York climbed as much as 3.5% in response to President Trump’s threat to slap 50% tariffs on Brazil, which is the top producer of higher-end arabica coffee.

According to Leslie Kernisan MD MPH, these are the basic self-care tasks that we initially learn as very young children. These are the self-care tasks we then learn as teenagers. They require more complex thinking skills, including organizational skills. They include:

Managing finances, such as paying bills and managing financial assets.

Managing transportation, either via driving or by organizing other means of transport.

Shopping and meal preparation. This covers everything required to get a meal on the table. It also covers shopping for clothing and other items required for daily life.

Housecleaning and home maintenance. This means cleaning kitchens after eating, keeping one’s living space reasonably clean and tidy, and keeping up with home maintenance.

Managing communication, such as the telephone and mail.

Managing medications, which covers obtaining medications and taking them as directed.

Because managing IADLs requires a fair amount of cognitive skill, it’s common for IADLs to be affected when an older person is having difficulty with memory or thinking. For those older adults who develop Alzheimer’s disease or a related dementia, IADLs will usually be affected before ADLs are.

***

***

IADLs were defined about ten years after ADLs, by a psychologist named M.P. Lawton. Dr. Lawton felt there were more skills required to maintain independence than were listed on the original Katz ADL index, and hence created the “Lawton Instrumental Activities of Daily Living Scale.”

According to Leslie Kernisan MD MPH, these are the basic self-care tasks that we initially learn as very young children. They are sometimes referred to as “Basic Activities of Daily Living” (BADLs). They include:

Walking, or otherwise getting around the home or outside. The technical term for this is “ambulating.”

Feeding, as in being able to get food from a plate into one’s mouth.

Dressing and grooming, as in selecting clothes, putting them on, and adequately managing one’s personal appearance.

Toileting, which means getting to and from the toilet, using it appropriately, and cleaning oneself.

Bathing, which means washing one’s face and body in the bath or shower.

Transferring, which means being able to move from one body position to another. This includes being able to move from a bed to a chair, or into a wheelchair. This can also include the ability to stand up from a bed or chair in order to grasp a walker or other assistive device.

***

***

If a person is not fully independent with ADLs, then we usually include some information about the amount of assistance they require. ADLs were originally defined in the 1950s by a geriatrician named Sidney Katz, who was trying to define what it might look like for a person to recover to independence after a disabling event such as a stroke or hip fracture. So these measures are sometimes called the “Katz Index of Independence in Activities of Daily Living.”

Posted on July 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler CFP™

***

***

One serious risk to financial wellbeing in retirement that is difficult to talk about is financial exploitation. Someone whose cognitive abilities are declining is vulnerable to harm from both financial predators and their own financial misjudgments. Protecting such clients is a crucial part of a financial advisor’s role.

A little-known but important law, the Senior Safe Act, was enacted in 2018. It encourages financial advisors and institutions to report suspected elder abuse by offering immunity from legal liability when reports are made in good faith and with reasonable care. To qualify for these protections, financial professionals must undergo annual training to recognize the signs of exploitation and know how to act on their suspicions.

In many ways, the Senior Safe Act mirrors the duty of therapists to report when clients are threats to themselves, such as when a client becomes suicidal. Just as a therapist must balance confidentiality with the moral and legal responsibility to protect their client from harm, a financial advisor must weigh privacy against the need to prevent financial exploitation. Both roles rely on professional judgment, training, and the courage to act when the stakes are high.

Financial advisors, accountants, and attorneys are often the first to notice troubling signs that someone is being taken advantage of financially. These might include sudden large withdrawals, changes to account ownership or beneficiaries, or a newly and overly involved friend or family member. Behavioral shifts like confusion, anxiousness, secretiveness, or uncharacteristic deference are also red flags. These patterns are unsettling and demand attention, even when stepping in is uncomfortable.

Reporting possible elder abuse isn’t always straightforward, especially if the suspected abuser is a family member. As an advisor, I worry about misunderstandings, potential conflicts with the family, and even the possibility of damaging a relationship with the client. None of this is easy, But when the signs of exploitation become clear, staying silent could mean allowing harm to continue. That’s a risk I can’t take.

One of the tools I started using decades ago is the trusted contact disclosure form. This simple but powerful document allows clients to name someone my firm can contact if they notice unusual activity, such as a suspicious withdrawal or transfer. The trusted contact does not have control over the client’s account but serves as a resource to verify their well-being and ensure that their financial decisions align with their long-term goals. If you as a client have not signed such a form, it’s worth discussing with your advisor as a preventative step.

If you are concerned about the financial well-being of an elderly loved one, it’s crucial to alert not only their financial advisor but also other professionals like accountants, attorneys, or bankers. These professionals may have insights or access to information you don’t have, and by sharing your concerns, you provide a broader picture that can help them detect and address issues more effectively. Even if they are already monitoring for red flags, your input can provide valuable context to guide their next steps.

Difficult though it may be, stepping into uncomfortable territory is often essential to protecting vulnerable individuals. Whether it’s a financial advisor detecting exploitation or a therapist intervening in a mental health crisis, the goal is the same—to prevent harm while respecting the person’s autonomy.

The Senior Safe Act is a reminder that sometimes the most impactful safeguards work quietly behind the scenes. Taking simple steps like completing a trusted contact form or encouraging your loved one to work with a reputable, fiduciary advisor can make all the difference. Vigilance is an act of care that helps protect someone’s financial assets as well as their dignity and well-being.

Posted on July 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants LLC

***

***

On June 9th, 2025, Oregon’s governor signed into law the country’s strictest corporate practice of medicine (CPOM) prohibition. Senate Bill (SB) 951 will severely curtail the involvement of private equity firms and other corporations in the state’s medical practices.

This Health Capital Topics reviews the bill and discusses the implications on the healthcare industry. (Read more…)

Posted on July 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Medical doctors, dentists, and podiatrists have to undergo extensive training before they can practice medicine independently. Once they receive training, there are opportunities to increase pay and prestige in the medical field through a series of promotions. As a doctor, how much training, experience and skills you have can determine your ability to move upward in these levels. But, personal branding strategies may even be more vital in today’s social media age?

***

Physician, medical and healthcare branding is more than just the creation of logos, taglines, or specific brand messaging. It’s about creating a meaningful connection between your mission, vision and values and the people served – from patients and their families to local and global communities.