BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Whatever the statistics regarding physician standard of living, the reality is that within most marriages the husband more frequently takes responsibility for understanding and managing the finances. Additionally, women are more likely to remain in the marital home following a separation, thus inheriting a large fixed expense that may prove be an excessive, albeit short-term burden to them. At the time the decision is made to separate or divorce, many women do not have an understanding of how to manage their household budget, or how to manage their assets and liabilities.

An issue many divorcing physicians face is that the other spouse (in the past the wife), may have concentrated their energies on managing the home, while the physician concentrated on earning and managing the finances. The problems of the spouse of a physician are often compounded in divorce; not only do they not understand their personal finances, but that their absence from the work force has made them financially dependent on the other.

At what probably be the most emotionally taxing time in their lives, they are forced to play catch-up.

***

***

Taking a more active role in their own financial planning during the marriage may help the spouse of a physician avoid some of the financial pitfalls of separation and divorce.

NOTE: Barbara Stanny provides an excellent overview and reading bibliography on how people can get smart about money in her book Prince Charming Isn’t Coming. [1]

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

According to Wikipedia, Phantom debt or zombie debt is a debt that is old, defaulted, or not owed and is somehow still being pursued for collection to be paid by the presumed debtor. It generally refers to debt that is more than 3 years old, is long forgotten about or belonged to someone else – like someone with the same name or a deceased parent. The amount owed can grow to hundreds or thousands of dollars more than what was originally owed.

An example of this is from George Miller. George missed an 11 cent Verizon bill and seven years later it had grown to $4,000.00.

Sometimes it was never owed, was owed by a deceased parent, or that was previously owed by the presumed debtor, but was previously paid in full, settled, discharged via bankruptcy or a dismissed court case, is beyond the statute of limitations, or is otherwise not legally collectible, but that a collection agency or other similar service is aggressively attempting to collect, often fraudulently.

While the concept of phantom debt is quite old, it has gotten a lot of attention since the 1990s.

Very often, collectors of phantom debt use intimidating, abusive, or otherwise illegal tactics in an attempt to collect phantom debt that include frequent phone calls, calls to the victim’s place of employment, or threats of scary consequences against the victim that sometimes include arrest and/or criminal prosecution. In the USA, such tactics violate the Fair Debt Collection Practices Act [FDCPA]

The source of phantom debt may be from collectors who buy the debt from other collectors for pennies on the dollar, some of which take action that is not legal in order to collect that debt. Unlawful techniques used include suing or threatening to sue, re-aging the debt on the victim’s credit report to circumvent limits on reporting, or falsely promising to remove a negative credit report entry in exchange for a partial payment.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Doctors and dentists earn money by treating patients. CPAs and Attorneys have clients, and retail stores buy items low and sell them at higher prices. This is called a business model.

More formally, a business model identifies the products or services the business plans to sell, the target market, and any anticipated expenses, in order to outline how to generate a profit. Business models are important for both new and established businesses. They help companies attract investment, recruit talent, and motivate management and staff.

Businesses should regularly update their business model, or they’ll fail to anticipate trends and challenges ahead. Business models also help investors to evaluate companies that interest them and employees to understand the future of a company they may aspire to join.

***

The Business Model of Pharmacy Benefits Managers

In the United States, health insurance providers often hire a third party to handle price negotiations, insurance claims, and distribution of prescription drugs. Providers that use such pharmacy benefit managers include commercial health plans, self-insured employer plans, Medicare Part D [drug] plans, the Federal Employees Health Benefits Program, and state government employee plans. PBMs are designed to aggregate the collective buying power of en-rollees through their client health plans, enabling plan sponsors and individuals to obtain lower prices for their prescription drugs. PBMs negotiate price discounts from retail pharmacies, rebates from pharmaceutical manufacturers, and mail-service pharmacies which home-deliver prescriptions without consulting face-to-face with a pharmacist.

Pharmacy benefit management companies can make revenue in several ways.

First, they collect administrative and service fees from the original insurance plan.

Then, they can also collect rebates from the manufacturer.

Traditional PBMs do not disclose the negotiated net price of the prescription drugs, allowing them to resell drugs at a public list price (also known as a sticker price), which is higher than the net price they negotiate with the manufacturer. This practice is known as “spread pricing”. The industry argues that savings are trade secrets. Pharmacies and insurance companies are often prohibited by PBMs from discussing costs and reimbursements. This leads to lack of transparency.

***

***

Therefore, states are often unaware of how much money they lose due to spread pricing, and the extent to which drug rebates are passed on to en-rollees of Medicare plans. In response, states like Ohio, West Virginia, and Louisiana have taken action to regulate PBMs within their Medicaid programs.

For instance, they have created new contracts that require all discounts and rebates to be reported to the states. In return, Medicaid pays PBMs a flat administrative fee.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

On July 14, 2025, the Centers for Medicare & Medicaid Services (CMS) released its proposed Medicare Physician Fee Schedule (MPFS) for calendar year (CY) 2026.

In addition to the agency’s suggested increase to physician payments, the proposed rule also announces a new payment model and more tele-health flexibilities.

According to CMS, the “proposed rule is one of several proposed rules that reflect a broader Administration-wide strategy to create a health care system that results in better quality, efficiency, empowerment, and innovation for all Medicare beneficiaries.” (Read more…)

Classic Definition: Research from Ernst-Young [Nikhil Lele and Yang Shim] uncovered a chasm between how consumer patients think they’re doing financially, and the actual state of their finances. Even more striking, their study suggested that improving consumers’ financial health will become one of the top imperatives in reframing consumer financial services.

Modern Circumstance: For example, the study asked consumers to rate their own financial health, and 83 percent rated themselves “good,” “very good” or “excellent.” Now, contrast this figure with what is known about their actual situation:

60 percent of Americans say they are financially stressed.

56 percent of Americans have less than $10,000 saved for retirement.

40 million American families have no retirement savings at all.

40 percent of Americans are not prepared to meet a $400 short-term emergency.

Paradox Example: Fortunately, even though the vast majority of consumers rate themselves as financially healthy, the study found that most still want to improve. Importantly for health economists, the attractive 25-34 and 35-49 year-old age groups were most likely to be extremely or very interested in improving their financial and economic health.

Paradox Example: Massively affluent consumer patients are even more interested in improving this paradox than their mass market counterparts.

Posted on July 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On July 15, 2025, the Centers for Medicare & Medicaid Services (CMS) released the proposed rule for the Outpatient Prospective Payment System (OPPS) and Ambulatory Surgical Center (ASC) Payment System for calendar year (CY) 2026.

Among other items, the agency proposes increasing payments to all outpatient providers, eliminating the Inpatient Only (IPO) List, and changing quality reporting programs.

This Health Capital Topics article reviews the proposed updates and changes to outpatient reimbursement. (Read more…)

Posted on July 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP™

***

***

When Maria needed $400,000 for a down payment on a new home, her broker at a large Wall Street firm offered a solution: “Don’t sell investments and trigger capital gains. Just take out a margin loan.”

A margin loan is a line of credit from a brokerage firm, secured by the client’s investment portfolio. It offers quick access to cash with no immediate tax consequences and minimal paperwork. But the convenience comes at a cost. As of mid-2025, margin loan interest rates range from 6.25% to over 11%.

Margin loan recommendations are often presented by brokers as tax-savvy strategies that allow clients to access “tax-free” cash while keeping their portfolios intact. In many cases, however, the math benefits the advisor more than the investor. The cost of borrowing often exceeds what an investor is likely to earn by holding on.

For example, let’s assume an interest rate of 7.5% on Maria’s $400,000 margin loan. While borrowing delayed the payment of $20,000 in capital gains tax, she will eventually have to pay that tax anyway unless she holds the investments until her death. Two years later, with portfolio returns of 4% annually, she had earned around $32,000 from the $400,000 in investments she might have sold. Meanwhile, she had paid $60,000 in interest—leaving her some $28,000 worse off. That’s without factoring in ongoing interest payments, or the risks of a margin call if the investments securing the loan drop in value.

Why do advisors keep recommending margin loans? Because selling investments reduces the portfolio size and the advisor’s fee. Borrowing keeps the portfolio intact and the compensation unchanged—while the firm receives additional income from interest on the loan. In some cases, advisors suggest using margin loans to buy more investments, increasing both the portfolio and the fee they collect.

None of this is illegal. But when the borrowing cost is higher than expected returns and the advisor benefits financially, the ethics are questionable. The client takes the risk, while the advisor keeps the revenue.

This kind of conflict appears more often in portfolios where compensation is tied to asset volume and the company’s primary culture rewards gathering assets over delivering unbiased advice. By contrast, fee-only financial planning and investment advisors typically operate on simpler hourly, flat, or tiered fee structures. Their compensation doesn’t depend on whether a client borrows, sells, or holds. The culture of the firm focuses on conflict-free advice aligned with the client’s best interest.

Wall Street brokers are often held to a fiduciary standard, but structure still matters. In 2024 the SEC reported their examinations of brokers would continue to focus on advisor recommendations unduly influenced by the company’s compensation and incentives.

There are rare situations where a margin loan may be appropriate. A client with large unrealized gains might use a short-term margin loan to minimize taxes. An elderly investor might borrow tax-free rather than sell assets that will receive a step-up in basis at their death. Even in those cases, the math must be exact and the client must clearly understand the risks, including the possibility of a margin call.

If your advisor recommends a margin loan, especially to buy more investments, ask strong questions. What’s the interest rate? What return is realistic? What are the tax consequences of selling? How does this affect the advisor’s income?

In a high-rate, low-return environment, margin loans rarely favor the client. The exceptions are narrow. The risks are significant. And the conflict of interest is measurable.

Sometimes the smartest move is the simplest: sell what you need, pay the tax, and leave leverage out of your plan.

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial planning and investment decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just a few weeks ago.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

Assessment

QUESTION: How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.” In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.

Yes, you can contribute to both a Roth IRA and a 401(k), provided you don’t exceed annual contribution limits for each account.

Determining whether to contribute to a Roth IRA, 401(k), or both can be an important step in planning for your retirement. Here are the key differences, including tax advantages, employer contributions, and investment options.

Eligibility requirements are the first consideration when contributing to a Roth IRA and a 401(k). For Roth IRA contributions, your eligibility is determined by your income. Specifically, if your modified adjusted gross income (MAGI) exceeds certain thresholds, your ability to contribute to a Roth IRA may be reduced or eliminated. However, there are no income limits for contributing to a 401(k), making it accessible to anyone with earned income.

IRS rules do allow for contributions to both a Roth IRA and a 401(k), provided you adhere to the annual contribution limits for each account.

This means you can take advantage of the higher contribution limits of a 401(k) while also benefiting from the tax-free growth of a Roth IRA. This dual approach can be a strategy for maximizing your retirement savings. The advantages to contributing to both accounts present some key benefits, such as:

Tax diversification in retirement, allowing for better management of taxable income.

Potential reduction of overall tax burden.

Maximization of savings potential by taking full advantage of the benefits each account offers.3

Balancing contributions between a Roth IRA and a 401(k) requires careful planning. You might start by contributing enough to your 401(k) to receive the full employer match, which is essentially free money, if your employer offers this. Once you’ve secured the match, consider maxing out your Roth IRA contributions, if you’re eligible.

Posted on July 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Lucid exploded 36.24% higher on the news that the EV maker is partnering with Uber to roll out the ridesharing company’s new robotaxis.

PepsiCo popped 7.45% thanks to a strong quarter for the snack and soda giant, while shareholders cheered the details of its turnaround plan.

UnitedAirlines may have missed Wall Street’s revenue forecast, but its profits were enough to impress investors. Shares rose 3.11%.

Reports that Union Pacific is thinking about acquiring a rival sent shares of fellow train operators CSX and NorfolkSouthern up 3.73% and 3.65%, respectively.

Sarepta Therapeutics soared 19.53% after the biotech announced it will lay off 500 employees and restructure its entire business.

Quantumscape continued its hot streak, rising yet another 19.82% thanks to its recent battery breakthrough.

Speaking of hot streaks, OpenDoorTechnologies rose another 10.74% as retail traders pour into what is quickly becoming the next big meme stock.

Stocks down

GE Aerospace crushed earnings expectations and raised its fiscal guidance, but it still wasn’t enough to impress investors, who pushed shares of the engine maker down 2.10%.

USBancorp sank 1.03% after revenue and net interest income missed forecasts last quarter.

AbbottLaboratories beat on both top and bottom line guidance, but still fell 8.53% after the pharma company narrowed its fiscal forecasts.

President Trump is expected to sign an executive order in the coming days designed to help make private-market investments more available to U.S. retirement plans, according to people familiar with the matter. The order would instruct the Labor Department and the Securities and Exchange Commission to provide guidance to employers and plan administrators on including investments like private assets in 401(k) plans.

Bettors are currently able to deduct 100% of their gambling losses, so they only pay taxes on their winnings. But starting next year, only 90% of gambling losses will be deductible.

So, if a professional gambler wins $100,000, then loses $100,000 that same year, according to the New York Times:

In 2025, that gambler would owe taxes on $0.

In 2026, that gambler would owe taxes on $10,000.

Bettors could even end up paying taxes if they finished the year with a net loss.

Posted on July 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants LLC

***

***

On June 25th, 2025, the Centers for Medicare & Medicaid Services (CMS) released its forecast on U.S. healthcare spending through 2033. The analysis, published in Health Affairs, estimated healthcare spending growth in 2024 and projected the growth into 2033. CMS found that overall healthcare spending growth has decreased slightly but is still elevated compared to pre-pandemic levels, and is expected to continue to moderately grow.

This Health Capital Topics article examines the factors underlying the forecasts. (Read more…)

One Big Beautiful Bill Act (OBBBA; OBBB; BBB), or the Big Beautiful Bill, is a budget reconciliation bill in the 119th US Congress.

Hospitals are not happy with the health care provisions of the bill, which would reduce the support they receive from states to care for Medicaid enrollees and leave them with more uncompensated care costs for treating uninsured patients.

“The real-life consequences of these nearly $1 trillion in Medicaid cuts – the largest ever proposed by Congress – will result in irreparable harm to our health care system, reducing access to care for all Americans and severely undermining the ability of hospitals and health systems to care for our most vulnerable patients,” said Rick Pollack, CEO of the American Hospital Association.

The association said it is “deeply disappointed” with the bill, even though it contains a $50 billion fund to help rural hospitals contend with the Medicaid cuts, which hospitals say is not nearly enough to make up for the shortfall.

The S&P 500 closed within a hair of a new record yesterday marking an enormous comeback that followed the April announcement of “Liberation Day” tariffs.

Despite a persistent vibe of uncertainty related to US economic policy and geopolitics:

The S&P 500 closed less than 0.1% away from a record high which it notched in February before cratering nearly 20% in April. The index has regained ground in fits and starts since then and briefly surpassed its record in intra-day trading yesterday.

On Monday, the tech-heavy NASDAQ 100 one-upped the broader market and logged its highest-ever close. It came after President Trump said Israel and Iran agreed to a ceasefire, which eased investors’ concerns about a potential oil crisis.

According to Morning Brew, between unresolved geopolitical conflicts and President Trump’s still-unfolding tariff policies, a portfolio manager with Capital Wealth Planning, Kevin Simpson, told CNBC that he was “surprised by the magnitude of the rebound.”

Posted on June 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants; LLC

***

***

On May 22, 2025, the U.S. House of Representatives moved President Trump’s budget proposal forward, sending to the Senate a budget reconciliation bill (with a one-vote margin) – the One Big Beautiful Bill Act of 2025 – that renews expiring tax cuts and enacts new ones at a cost of almost $4 trillion. These costs would largely be paid for by cuts to other programs, including to federal healthcare programs, which cuts will have significant ramifications for the healthcare industry.

This Health Capital Topics article reviews the current status of the budget bill and healthcare industry implications. (Read more…)

Posted on June 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

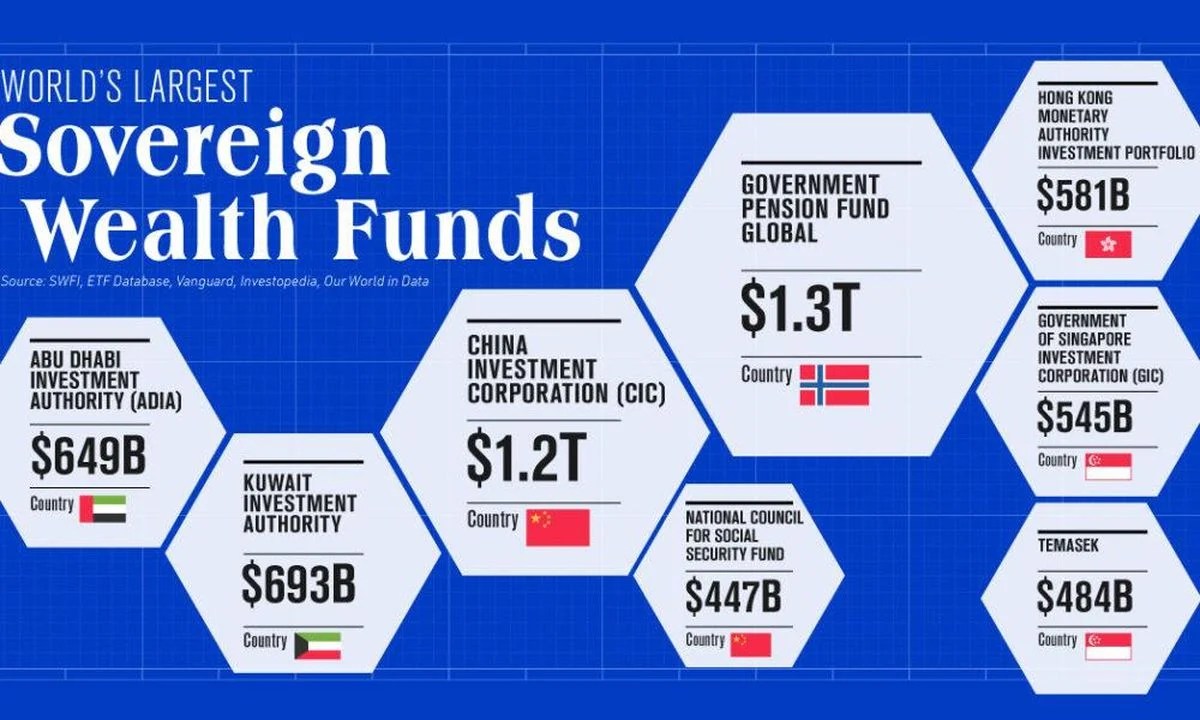

A SWF is essentially an investment fund run by the government. Similar to how a hedge fund or a private equity firm operates, the government would set aside a pot of money and invest it in assets such as stocks, bonds, startups, or real estate.

The idea of the US establishing a sovereign wealth fund akin to Norway’s or Abu Dhabi’s gained momentum recently across the political spectrum. Former President Trump endorsed the concept during a speech on his economic policy agenda for a second term, and the Biden administration has been quietly cheffing up a proposal for a wealth fund over the past several months, Bloomberg reported.

Trump and Biden officials described the fund as a key tool the country could deploy to win the global technological arms race and better compete against geopolitical rivals like China.

For example, the wealth fund could finance capital-intensive sectors such as shipbuilding, nuclear fission, and quantum cryptography that don’t offer near-term ROI for private investors.

However, disadvantages of a SWF include:

Non-Guaranteed Returns, with the Risk of Total Loss

Influence on Foreign Exchange Rates, Introducing Uncertainty

Potential Mismanagement of Funds Due to a Lack of Transparency

Dependency on Global Economic Conditions, Impacting Fund Performance

Challenges in Maintaining Accountability and Addressing Ethical Concerns

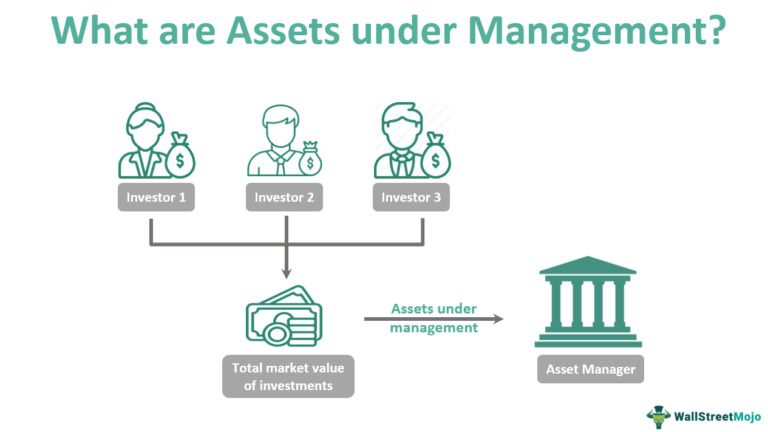

Assets under management (AUM) is a significant parameter in the financial world. It answers financial questions like – how many investments does a company manage? What is the net value of the investments that the company manages? Finally, how many investors have trusted their assets with the company? The higher the answer to these three questions, the more glory to the company.

A wealthy investor who is not concerned by higher fees but wants maximum returns of their asset will probably choose an asset manager based on its AUM. Thus, the AUM indicates the financial performance of the firm. Also, based on the funds under management, the firm collects fees from other clients.

So, what are the investments which qualify as AUM? Any liquid asset of the investor they have entrusted the asset manager with monitoring and control. For example, bank deposits, cash balances, equity shares, bonds, mutual funds, and other investments.

What are the services an asset manager provides to their clients? The most important function is decision-making. With the constant fluctuations and rapid movements in the market, an asset manager has to make decisions about holding or selling an investment. The firm communicates with the investors and advises them about the necessary action.

Once the decision is taken, the firm acts on the decision, i.e., the investor does not have to enter the field. In addition, the asset management company will buy, sell, and make any other transactions on behalf of the investor. Finally, the firm also renders services like accounting, tax reporting, proxy voting (equity shares), client reporting, and other financial services.

What are Assets Under Advisement?

Assets under advisement refer to assets on which your firm provides advice or consultation but for which your firm does either does not have discretionary authority or does not arrange or effectuate the transaction. Such services would include financial planning or other consulting services where the assets are used for the informational purpose of gaining a full perspective of the client’s financial situation, but you are not actually placing the trade.

Assets under advisement could also be those which you monitor for a client on a non-discretionary basis, where you may make recommendations but where the client is the party responsible for arranging or effecting the purchase or sale. A common example of this scenario is when an adviser reviews a participant’s 401(k) allocations. If the adviser does not have the authority or ability to effect changes in the portfolio, these assets are likely considered assets under advisement rather than regulatory assets under management.

Assets under advisement are permitted to be disclosed on Form ADV Part 2A as a separate asset figure from the assets under management. There is no requirement to disclose the assets under advisement figure, but some advisers opt to include the figure to give prospective clients a more complete picture of the firm’s responsibilities. If you choose to report your assets under advisement, be sure to make a clear distinction between this figure and your regulatory assets under management.

Posted on June 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Call for Manuscripts, Articles, Essays, Comments or Opinions

Dear Medical and Financial Services Colleagues, Health Economists, CPAs, JDs, Insurance Agents and Consultants,

The Medical Executive-Post (ME-P), supported by iMBA Inc., with (ISSN 13: 978-1-4665-5873-1] is currently accepting manuscripts for publication.

The ME-P is an open access, multidisciplinary, international, blind peer-reviewed and non-peer-reviewed electronic forum which publishes high-quality solicited and unsolicited research, commentary, opinions, curated news and review articles in English, in all areas of Physician Focused Financial Planning, health economics, finance, accounting, medical practice management, health law, IT, policy and administration. We have over 50 topic channels.

Rapid Response Peer-Review

ME-P is a rapid response forum that publishes daily. One of our objectives is to inform contributors (authors) of the decision on their manuscript(s) within 48 hours of submission. Following acceptance, a paper would be published in the next available issue. The ME-P provides immediate open access to published articles without any barrier.

***

[ME-P Fast Review, Turn-Around and Publishing Time]

***

Broad Exposure Potential

Publishing your news, opinions or comments, essays or articles with the ME-P means that they will be available to millions of readers and researchers because our large and diverse readership base comprises millions of collaborators. Our forum supports the free downloading of published articles by scholars for use as materials for lecture, by government officials for policy making, professors, colleges, universities and educators, and by corporate researchers and FAs to selected firms and organizations world-wide.

Blog Citations

Assessment

Also, ME-P is a member of several local and international organizations, making it possible for the far and wide distribution of published materials. We ask you to support this initiative by publishing your thoughts, comments, articles and original paper(s) 0n this forum, and in our textbooks and white-papers, etc.

Stocks: The S&P 500 touched 6,000 points for the first time since February and wrapped up its fifth positive week in the past seven following a better-than-expected jobs report. The vibes got even better in the afternoon following a President Trump announcement that the US and China trade teams will meet in London on Monday. STOCKS: https://medicalexecutivepost.com/2025/04/18/stocks-basic-definitions/

Bonds: Treasury yields ticked up in response to the solid May jobs report, a sign that investors were reducing bets on the scale of rate cuts this year. That’s not what Trump wants to hear: He urged Fed Chair Jerome Powell to slash interest rates by a jumbo-sized full point to pour “rocket fuel” on the economy. REVENUE BONDS: https://medicalexecutivepost.com/2024/12/20/bonds-revenue/

Oil: Oil prices have gone sideways for three straight weeks now, trading within a $4 range around $65/barrel since the middle of May. We’ll let you know when something interesting happens. CRUDE OIL:https://medicalexecutivepost.com/2024/08/14/wti-crude-oil/

Posted on June 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

BREAKING NEWS

***

***

Job growth is slowing, but still bigger than expected

US employers added 139,000 jobs last month, government data released yesterday shows—that’s less than the down-wardly revised 147,000 new jobs that were added in April, but more than economists had predicted. Meanwhile, the unemployment rate held steady.

Overall, the highly anticipated jobs report reflects employers growing more cautious in the face of the economic uncertainty brought on by the trade war, but so far, there doesn’t seem to be a steep drop off in the labor market. That could give the Fed reason to stay in wait-and-see mode on interest rates, though President Trump still used the occasion to urge Jerome Powell to cut rates “a full point” on Truth Social.

Posted on June 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

A recent joint report by the National Association of Accountable Care Organizations (NAACOS) and Innovaccer Inc., a healthcare artificial intelligence (AI) company, found tangible evidence that the U.S. healthcare delivery system is indeed moving toward value-based care (VBC).

Fifteen years after the passage of the Patient Protection and Affordable Care Act (ACA), which promoted VBC through the advent of ACOs and other alternative payment models, there is finally evidence that providers are actually moving in that direction.

This Health Capital Topics article reviews the joint report on “The State and Science of Value-based Care 2025.”(Read more…)

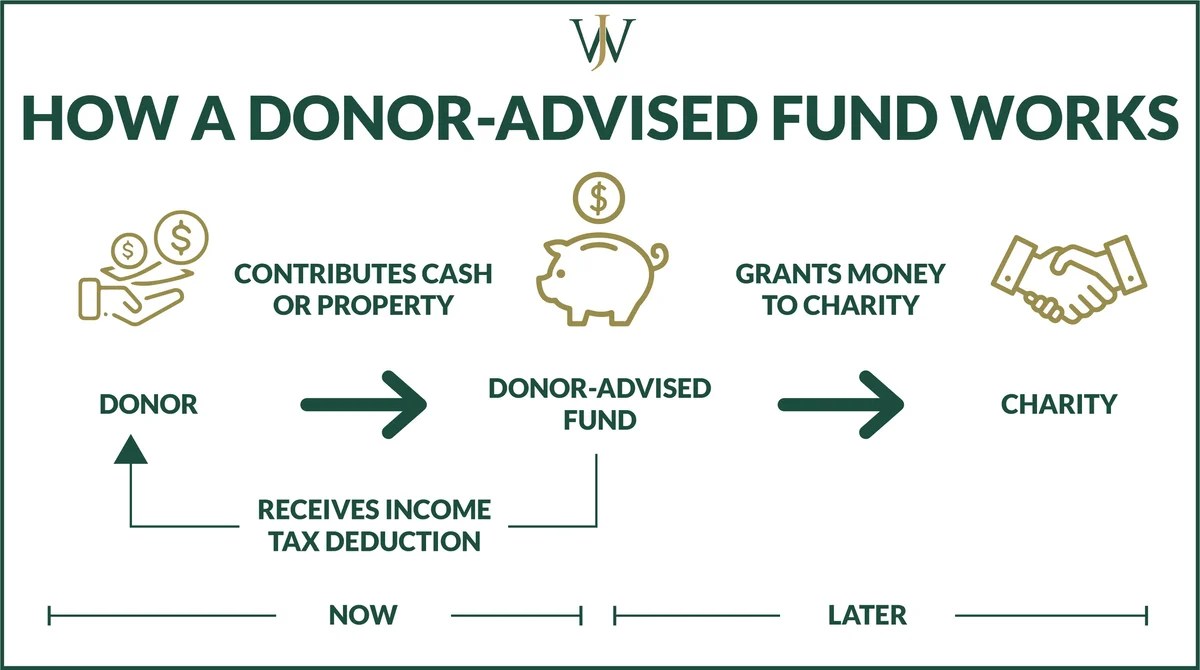

A donor-advised fund is a private account created to manage and distribute charitable donations on behalf of an organization, family, or individual. Donor-advised funds can democratize philanthropy by aggregating the contributions of multiple donors, thus multiplying their impact on worthy causes. Donor-advised funds also have abundant tax advantages.

Donor-advised funds have become increasingly popular, as they offer the donor greater ease of administration while still allowing them to maintain significant control over the placement and distribution of charitable gifts. But, unlike private foundations, donor-advised fund holders enjoy a federal income tax deduction of up to 60% of adjusted gross income (AGI) for cash contributions and up to 30% of AGI for the appreciated securities they donate. Donors to these funds can contribute cash, stock shares, and other assets. When they transfer assets such as limited-partnership interests, they can avoid capital gains taxes and receive immediate fair market value tax deductions.

According to the National Philanthropic Trust’s 2023 Donor-Advised Fund Report, these funds have continued to grow in recent years, despite some headwinds including the Covid-19 pandemic and occasional stock market setbacks. Total grants awarded by donor-advised funds in 2022 increased by 9% to $52.16 billion, while total contributions rose by 9% to $85.5 billion.

Many donor-advised funds accept non-cash assets—such as checks, wire transfers, and cash positions from a brokerage account—in addition to cash and cash equivalents.

Donating non-cash assets may be more beneficial for individuals and businesses, leading to bigger tax bigger write-offs.

Posted on May 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

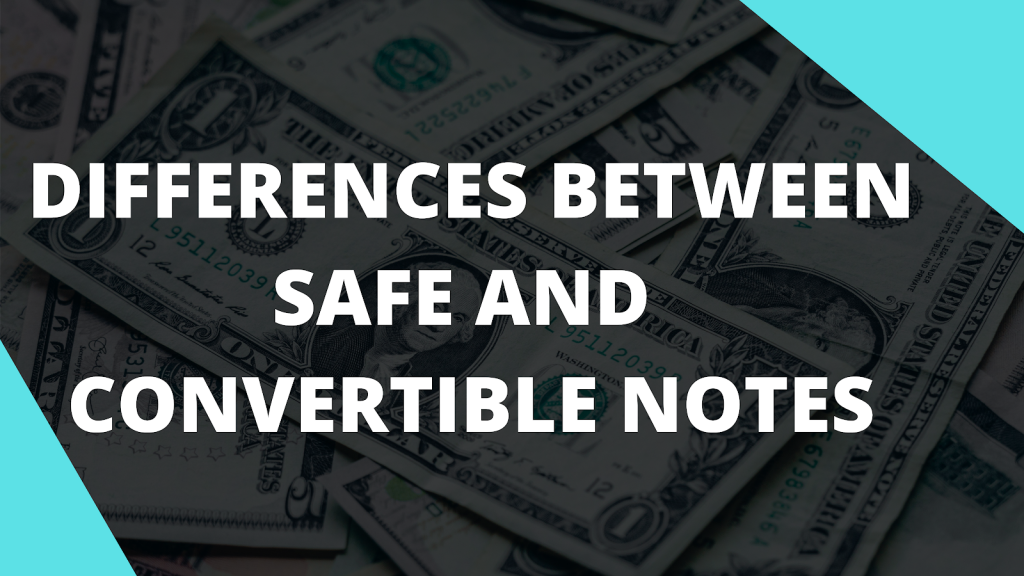

What Is a SAFE Note?

A SAFE note is a type of convertible security that specifies a certain amount of money an investor will pay you as a business owner. In exchange, you agree to give the investor a certain amount of equity in your company at an agreed-upon future date. In other words, a SAFE note confers the right for an investor to purchase shares in your company in a future-priced round.

How SAFE Notes Work

According to ContractsCounsel, a SAFE note works in the following way:

An investor provides funding in exchange for the right to future equity.

You use the funding to grow your business.

After your company grows sufficiently, you secure another investor, and your company receives a “post-money valuation.”

You calculate your company’s price per share.

You convert the SAFE note into the applicable number of shares and distribute them to the SAFE investor. Typically, a SAFE note converts after an equity financing round.

Example of a SAFE Note

An investor purchases a SAFE note with a valuation cap of $20 million. During the next funding round, the value of your company is set at $40 million at $20 a share. Because the SAFE note has a valuation cap of $20 million, its owner can purchase twice as many shares of your company as new investors can. This was the incentive for the SAFE investor to provide funding earlier.

Within venture capital financing, a convertible note is a type of short-term debt financing that’s used in early-stage capital raises. In other words, convertible notes are loans to early-stage startups from investors who are expecting to be paid back when their note comes due. But, instead of being paid back in principal with interest—as would be the case with a typical loan—the investor can be repaid in equity in your company.

You might also think of a convertible note like an IOU. An investor provides you with capital now and the convertible note, acting as a short-term loan, ensures that you give the investor a stake in your startup later. From the investor’s point of view, the benefit in this exchange is that if they give you capital and a vote of confidence early on and you do well, you’ll repay them many times over.

How Do Convertible Notes Work?

Typically, an investor will provide an early-stage startup in need of capital with a loan (with repayment terms in the ballpark of a standard short-term loan, usually a year or two), along with repayment terms. This is the “note.” The note will include a due date at which time it’s mature and the balance will be due, along with interest. Generally, however, the note is not repaid like a normal short-term loan. Instead, you repay the investor for their loan with equity in your company, usually in conjunction with another funding round.

If, however, the maturity date comes along and your startup has not yet converted the note to equity, the investor can either extend the convertible note’s maturity date or call for the actual repayment of the note.

This being said, the whole idea behind convertible notes is that your company is on a strong growth trajectory and that is why the note is being issued—it amasses value for the investor and beelines to a priced round. Ultimately, the point of a convertible note is that the noteholder, or investor, doesn’t want to get their loan paid back— they want their debt to convert into a heavily discounted security in a successful, valuable company that’s growing extremely quickly.

Cons: The major downside of a convertible note is that you will eventually be giving up some control over your business. When the convertible note comes due, the investor will be granted equity in your business. If you’re not ready to split ownership of your business with outside parties, this is not the right financing option for you.

Posted on May 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP®

***

***

OVER HEARD IN THE FINANCIAl ADVISOR’S LOUNGE

A basic strategy for asset protection is to hold various assets in different entities. Putting real estate, small businesses, and other assets into trusts, corporations, or limited liability companies (LLCs) is effective protection that is relatively easy to put into practice. Not only do I recommend this strategy to clients, I use it myself. Recently, however, I discovered a potential downside.

About 25 years ago, I invested in some rare coins in a corporation I owned and put them into a safe deposit box owned by the corporation. When my business relocated 12 years ago, the safe deposit box billing was not forwarded to the new address and was never paid again. Last year I went to retrieve the coins from the safe deposit box, which I had not visited in 25 years. I discovered the box had been drilled open three years earlier and my collection turned over to the unclaimed property division of the State Treasurer’s office.

I was told getting the coins back would be simple enough. I just needed to verify that I owned the company which owned them by providing the corporation’s tax ID number. However, the corporation no longer existed. I didn’t have a record of its tax ID number. The IRS wouldn’t verify the number without my giving them the address the company had used. That address was a post office box number that I no longer used and couldn’t remember. The state’s position was “no tax ID, no coins.” The only verification of my identity as owner of the corporation was my signature on the bank’s safe deposit box application. Eventually, with the support of bank officers who were willing to swear that I was who I claimed to be, I got my coin collection back. The hassle involved in this process was a reminder of an important component of asset protection. Maintain accurate records so you don’t end up hiding assets from yourself.

***

***

A good start is to create a master file of all the entities that hold your assets. This can be any system that’s easy for you to use: a computer spreadsheet, a set of file folders, or a single paper list. Share it as appropriate with your CPA, attorney, or financial planner. The master list should include the name of each company, its date of incorporation, tax ID number, address, and other relevant information like phone or bank account numbers. Also keep an inventory of the assets each company owns.

Once you’ve created a master list, it’s essential to keep it up to date as you buy or sell assets, close companies, or transfer ownership. Set up a system, as well, to remind yourself of tasks like filing tax returns, completing minutes of annual meetings, and paying the annual safe deposit box rent. Make your record-keeping easier by eliminating unnecessary complications.

For example, you probably don’t need a separate address for each trust, corporation, or LLC. Instead of creating a separate company for each asset, you might consider grouping smaller assets within one entity. I’d suggest first discussing the pros and cons with an attorney or financial planner. For larger assets like real estate, I do recommend holding each one separately.

When I talk to clients about asset protection, I mention that part of the price we pay for it is an increase in paperwork. It’s easy to accept that idea with casual good intentions. The case of my reclaimed coin investment is a good reminder of the importance of keeping up with that paperwork. If we don’t, we might protect ourselves right out of access to our own assets.

Most individual physician portfolios are simply a list of stocks. Doctors with such lists usually know the cost of each position and when they acquired it. It is not unusual to find inherited low cost stocks in the account that have been held for many years.

When you inherit securities, a new cost basis is established (the price of the stock on the date of death or six months later—the executor of the estate makes this determination). Even though there would be no capital gain liability if the stock were sold immediately after date of death, most people simply don’t do anything, just hold the stock. Of course taxes should be considered when selling securities but the investment merit should be the overriding factor.

***

***

Doctor and Accountant Opinions

In a personal communication, Mr. L. Eddie Dutton, CPA said, “First make an investment decision and if it fits into the tax plan, so much the better. Doctors often wonder where they will get the money to pay the taxes. I say to get it from the sale of the appreciated stock and cry all the way to the bank with your profit.”

Dr. Ernest Duty MD, a very successful private investor advises “Ask yourself this question: If you had the money instead of the stock, would you buy the stock? If your answer is ‘Yes’ then, hold on to the stock but if you say ‘No, I wouldn’t buy that stock today’ then, sell it” [personal communication].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: E-MAILCONTACT: MarcinkoAdvisors@outlook.com

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

I want to invest with a manager that has the skills to “hedge” a portfolio, but I do not wish to mix my money with other investors as in a hedge fund.

QUESTION:Can I hire hedge fund managers to manage my account separately?

Some hedge fund managers do take the time to recruit and manage separate accounts, with or without the help of referring brokers.

However, before long the administrative burden of managing so many separate accounts can become quite significant. Hence, the minimums for such separate accounts are generally much higher than if one were to invest in the manager’s hedge fund.

The best feature of these separate accounts is that potentially every aspect of the investment account, including fees, is negotiable. Other features include greater transparency and increased liquidity, since separately managed accounts can often be shut down on short notice.

Investors must be aware, however, that for practical purposes the portfolio manager generally will buy and sell the same securities in the separately managed accounts that the portfolio manager buys and sells in the hedge fund, yet the expenses incurred by the investor will likely be higher.

According to Baumol’s Cost Disease, in theory, workers should get higher pay because they get more productive. But an economist named William J. Baumol PhD noticed this isn’t always true; as in a paradox.

For example, musicians take the same time to play a string quartet as they did in Mozart’s day, but are paid more nevertheless. The reason is competition for labor; musicians can take other jobs. So rising wages in productive parts of the economy (eg, manufacturing) lead to higher wages in less productive sectors.

MORE: For more on the paradoxical disease, read this article; and for more on Baumol, read this one.

Financial Advisors and Financial Planners Usually Aren’t Millionaires

According to the most recent data from the Bureau of Labor Statistics (BLS), financial advisors had a median annual salary of $99,580 in 2023, which is significantly higher than the national average of $65,470. Of course, salaries of financial advisors can differ significantly by their location and level of expertise. The client’s profile may also have an impact on their compensation. But, many are not rich.

This is unfortunate. Financial advisors and Financial planners don’t rank among the millionaire professions in Thomas J. Stanley and William D. Danko’s book The Millionaire Next Door. Many work as salaried employees rather than entrepreneurs, lacking the scalable income potential of business owners who reinvest profits.

Stanley and Danko also stressed frugality, a challenge for advisors pressured to flaunt success—think luxury cars or upscale offices—making them “income-statement affluent” rather than “balance-sheet affluent.”

The truth is that a Financial Advisors’ success isn’t measured in client returns. Instead it is measured in their ability to gather assets and retain clients. In other words; Financial Advisors do not need to be good with money.

Financial Advisors need to be good with marketing, advertising, sales and people.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

My medical practice has a small self-directed pension plan with profit sharing features.

QUESTION: Can my medical practice’s retirement plan invest in a hedge fund?

Such a pension fund falls under a category called self-directed “plan” assets.

Among the rules are that each participant in the plan counts toward the 100 investor maximum under which most hedge funds operate, that each plan participant be a fully accredited investor, and that the hedge fund keep investments such as pension plans and other funds covered under ERISA to less than 25 percent of total assets under management.

Posted on May 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

BREAKING NEWS

***

***

UnitedHealth Group just announced the exit of CEO Andrew Witty and suspended its 2025 forecast due to surging medical costs, sending its shares down more than 10%. Chairman Stephen Hemsley will become CEO, effective immediately.

The fourth-largest U.S company big revenue in 2024, Minnetonka-based UnitedHealth has experienced a turbulent year that saw the shock killing of United Healthcare CEO Brian Thompson in New York City, and a cyberattack that affecting an estimated 190 million people and cost the company an estimated $3.1 billion dollars.

Posted on April 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Consumer sentiment is a statistical measurement of the overall health of the economy as determined by consumer opinion. It takes into account how people feel about their current financial health, the health of the economy in the short-term, and the prospects for longer-term economic growth. It is widely considered to be a useful economic indicator.

Consumer sentiment emerged as an economic statistic during the mid-20th century and has since become a barometer that influences public and economic policy. It is considered a lagging indicator because it takes people several months to notice and feel the effects of changes in economic activity.

American consumers are Worried about the Economy

Consumer sentiment dropped 8% from March to April amid worries about inflation, according to the University of Michigan’s closely watched survey. Though sentiment edged up slightly from an even lower reading earlier in the month, inflation expectations climbed to their highest since 1991 as consumers fret about the potential impact of tariffs.

And even beyond possible rising prices, things could be about to get rougher for consumers: Major retailers have warned that unless President Trump’s tariff policy toward China changes, they’re likely to encounter empty store shelves in a few weeks.

Posted on April 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler CFP™

***

***

Lately, I’ve been hearing the same question from clients and readers alike: “Is Social Security even going to be there in five years?” Fueling this concern is a recent viral comment from Elon Musk, who told Joe Rogan that Social Security is “the biggest Ponzi scheme of all time.” That quote has been repeated in every corner of the internet, stirring up uncertainty and fear.

Elon Musk is a genius, but his brilliance in technology and innovation doesn’t automatically translate into expertise in public policy. When it comes to Social Security, he’s outside his lane. Calling it a Ponzi scheme may make for a great soundbite, but it’s a fundamental mischaracterization.

Social Security is not a Ponzi scheme. Not even close.

A Ponzi scheme is a form of financial fraud that lures investors with the promise of high returns. Instead of earning those returns through legitimate investments, the scheme pays earlier investors using money from newer ones. Eventually, the model collapses when there aren’t enough new participants to keep it going, leaving most people with significant losses. This is what happened to those who trusted Bernie Madoff, operator of one of the worst Ponzi schemes in history. Ponzi schemes are illegal, deceptive, and doomed from the start.

Social Security, in contrast, is a government-run, pay-as-you-go tax program. It’s fully transparent; you know exactly where your money is going. The payroll taxes you and your employer pay are used to provide income to today’s retirees, people with disabilities, and surviving family members of deceased workers. This isn’t a con, it’s a social contract.

So why the confusion? Part of the issue is that Social Security does, on the surface, resemble the flow of a Ponzi scheme: money coming in from the young to support the old. But similarity in structure doesn’t make it fraudulent. The program does not promise high returns, it promises a modest, inflation-adjusted benefit to support people as they age.

Social Security does face challenges. The trust fund reserves, built up during years when payroll taxes exceeded payouts, are projected to run dry around 2033. If Congress does nothing, benefits will need to be cut by about 20%. That’s serious, but it’s a solvency issue, not a scam.

And the solvency issue is fixable. There are numerous bipartisan proposals to shore up the system for the long term, from raising the payroll tax cap to gradually adjusting benefits. These aren’t radical ideas, they’re common-sense repairs. A bipartisan mix of 100 CFPs in a room could work out a solution in two days.

When clients ask me if the system will be around in five years, what they’re really asking is: Can I trust it? Can I trust the government? Can I trust that my years of work and tax payments will mean something in retirement? These are not just policy questions. They are emotional questions based on fear of scarcity and a desire for security. When someone with Elon Musk’s influence wrongly calls Social Security a Ponzi scheme, his attention-grabbing soundbite shakes the emotional foundation of that trust.

If we’re serious about preserving Social Security, let’s start by calling it what it is: a commitment to our elders. A tax-supported promise to care for one another across generations.

Social Security is not a fraud, it’s a shared responsibility based on the kind of society we want and woven into the fabric of American life. Yes, it needs some adjustments, but it’s not broken. Rather than eroding public trust with misleading comparisons, we should be focused on debating public policy and how we can strengthen and sustain the program for future generations.

***

ME-P NOTE: An increase in Social Security benefits is on the horizon, providing a potential financial cushion against rising inflation. The Cost of Living Adjustment (COLA) for 2025 is set at 2.5% monthly, translating to an average annual increase of approximately $600 for beneficiaries. This adjustment is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers. While not guaranteed annually, COLA has historically been implemented in most years due to persistent inflationary trends.

An annuity is a contract between you and an insurance company. When you purchase an annuity, you make a lump-sum contribution or a series of contributions, generally each month. In return, the insurance company makes periodic payments to you beginning immediately or at a pre-determined date in the future. These periodic payments may last for a finite period, such as 20 years, or an indefinite period, such as until both you and your spouse are deceased. Annuities may also include a death benefit that will pay your beneficiary a specified minimum amount, such as the total amount of your contributions.

The growth of earnings in your annuity is typically tax-deferred; this could be beneficial as you may be in a lower tax bracket when you begin taking distributions from the annuity.

Warning: A word of caution: Annuities are intended as long-term investments. If you withdraw your money early from an annuity, you may pay substantial surrender charges to the insurance company as well as tax penalties to the IRS and state.

***

***

There are three basic types of annuities — fixed, indexed, and variable

1. With a fixed annuity, the insurance company agrees to pay you no less than a specified (fixed) rate of interest during the time that your account is growing. The insurance company also agrees that the periodic payments will be a specified (fixed) amount per dollar in your account.

2. With an indexed annuity, your return is based on changes in an index, such as the S&P. Indexed annuity contracts also state that the contract value will be no less than a specified minimum, regardless of index performance.

3. A variable annuity allows you to choose from among a range of different investment options, typically mutual funds. The rate of return and the amount of the periodic payments you eventually receive will vary depending on the performance of the investment options you select.

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

A Certified Public Accountant (CPA) is a licensed professional who has passed an examination administered by a state’s Board of Accountancy. State CPA exams are created under guidelines issued by The American Institute of Certified Public Accountants (AICPA). The Uniform CPA Exam can only be taken by accountants who already have professional experience in the field and a bachelor’s degree.CPAs are not fiduciaries.

Not all accountants are CPAs. Accountants who are CPAs are licensed by their state’s Board of Accountancy after passing the Uniform CPA Exam. CPAs prepare reports that accurately reflect the business dealings of the companies and individuals that hire them. Many prepare tax returns for individuals or businesses and advise them on ways to minimize taxes. Obtaining the CPA designation requires a bachelor’s degree, typically with a major in business administration, finance, or accounting. Other majors are acceptable if the applicant meets the minimum requirements for accounting courses.

Enrolled Agent

Although not a CPA, an Enrolled Agent [EA] is a person who has earned the privilege of representing taxpayers before the Internal Revenue Service [IRS]. This is done by either passing a three-part comprehensive IRS test covering individual and business tax returns, or through experience as a former IRS employee. Enrolled agent status is the highest credential the IRS awards. Individuals who obtain this elite status must adhere to ethical standards and complete 72 hours of continuing education courses every three years.

Certified Managerial Accountant

A Certified Management Accountant (CMA), which is issued by the Institute of Management Accountants (IMA), builds on financial accounting proficiency by adding management skills that aid in making strategic business decisions based on financial data.

Oftentimes, the reports and analyses prepared by certified management accountants (CMAs) will go above and beyond those required by generally accepted accounting principles (GAAP).

For example, in addition to a company’s required GAAP financial statements, CMAs may prepare additional management reports that provide specific insights useful to corporate decision-makers, such as performance metrics on specific company departments, products, or even employees.

Certified Financial Analyst

A Certified Financial Analyst [CFA] is a globally-recognized professional designation offered by the CFA Institute, an organization that measures and certifies the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management, and security analysis. From 1963 through November 2023, more than 3.7 million candidates had taken the CFA exam. The overall pass rate was 45%. From 2014 through 2023, the 10-year average pass rate was 43%.1

CFA Institute. The CFA Institute was formerly the Association for Investment Management and Research (AIMR).

The CFA charter is one of the most respected designations in finance and is widely considered to be the gold standard in the field of investment analysis. To become a charter holder, candidates must pass three difficult exams, have a bachelors degree, and have at least 4,000 hours of relevant professional experience over a minimum of three years. Passing the CFA Program exams requires strong discipline and an extensive amount of studying.

There are more than 200,000 CFA charter holders worldwide in 164 countries.The designation is handed out by the CFA Institute, which has 11 offices worldwide and 160 local member societies.

Carried interest accounts for the bulk of private equity fund managers’ compensation. It is calculated as a share of fund profits, historically 20% above a threshold rate of return for limited partners.

In contrast with most other forms of employment compensation and business income, carried interest earned from fund investments held for at least three years is taxed as a long-term capital gain at a rate below the top marginal income tax rate.

Critics of the provision contend it taxes highly compensated private equity managers at a lower rate than comparably paid providers of labor or business services.

Defenders of carried interest argue taxing it as income would be unfair because it represents capital gains even if they’re not derived from recipients’ capital.

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

WARNING – WARNING

By Staff Reporters

***

***

A “retirement account scam” is a type of online fraud that occurs when a third party administrator (TPA) for retirement investment accounts is tricked into authorizing a money distribution to an imposter posing as the true account holder.

The imposter often starts the scam by calling the TPA, identifying himself or herself as an actual account holder, and requesting a withdrawal distribution form. Once the imposter receives the withdrawal distribution form, the imposter returns the completed form to the TPA. The form is completed with the account holder’s real personal identifying information (PII)—often stolen via schemes, data breaches, and other hacking offenses—and bank account information for an account controlled by the imposter or the imposter’s conspirators.

***

***

After the TPA processes the fraudulent request, the request is forwarded to the investment firm responsible for managing the account holder’s investments, and the funds—often the account holder’s life savings—are then directed to the imposter’s designated bank account.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

OVER HEARD IN THE FINANCIAL ADVISOR’S LOUNGE

***

***

By Perry D’Alessio, CPA [D’Alessio Tocci & Pell LLP]

What I see in my accounting practice is that significant accumulation in younger physician portfolio growth is not happening as it once did. This is partially because confidence in the equity markets is still not what it was; but that doctors are also looking for better solutions to support their reduced incomes.

For example, I see older doctors with about 25 percent of their wealth in the market, and even in retirement years, do not rely much on that accumulation to live on. Of this 25 percent, about 80 percent is in their retirement plan, as tax breaks for funding are just too good to ignore.

What I do see is that about 50 percent of senior physician wealth is in rental real estate, both in a private residence that has a rental component, and mixed-use properties. It is this that provides a good portion of income in retirement.

***

***

QUESTION: So, could I add dialog about real estate as a long term solution for retirement?

Yes, as I believe a real estate concentration in the amount of 5 percent is optimal for a diversified portfolio, but in a very passive way through mutual or index funds that are invested in real estate holdings and not directly owning properties.

Today, as an option, we have the ability to take pension plan assets and transfer marketable securities for rental property to be held inside the plan collecting rents instead of dividends.

Real estate holdings never vary very much, tend to go up modestly, and have preferential tax treatment due to depreciation of the property against income.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Beneficiary designations can provide a relatively easy way to transfer an account or insurance policy upon your death. However, if you’re not careful, missing or outdated beneficiary designations can easily cause your estate plan to go awry.

Where you can find them

Here’s a sampling of where you’ll find beneficiary designations:

In several states, so-called “lady bird” deeds for real estate

***

***

10 tips about beneficiary designations

Because beneficiary designations are so important, keep these things in mind in your estate planning:

Remember to name beneficiaries. If you don’t name a beneficiary, one of the following could occur:

The account or policy may have to go through probate. This process often results in unnecessary delays, additional costs, and unfavorable income tax treatment.

The agreement that controls the account or policy may provide for “default” beneficiaries. This could be helpful, but it’s possible the default beneficiaries may not be whom you intended.

Name both primary and contingent beneficiaries. It’s a good practice to name a “back up” or contingent beneficiary in case the primary beneficiary dies before you. Depending on your situation, you may have only a primary beneficiary. In that case, consider whether it may make sense to name a charity (or charities) as the contingent beneficiary.

Update for life events. Review your beneficiary designations regularly and update them as needed based on major life events, such as births, deaths, marriages, and divorces.

Read the instructions. Beneficiary designation forms are not all alike. Don’t just fill in names — be sure to read the form carefully. If necessary, you can draft your own customized beneficiary designation, but you should do this only with the guidance of an experienced attorney or tax advisor.

Coordinate with your will and trust. Whenever you change your will or trust, be sure to talk with your attorney about your beneficiary designations. Because these designations operate independently of your other estate planning documents, it’s important to understand how the different parts of your plan work as a whole.

Think twice before naming individual beneficiaries for particular assets. For example, you may establish three accounts of equal value initially and name a different child as beneficiary of each account. Over the years, the accounts may grow or be depleted unevenly, so the three children end up receiving different amounts — which is not what you originally intended.

Avoid naming your estate as beneficiary. If you designate a beneficiary on your 401(k), for example, it won’t have to go through probate court to be distributed to the beneficiary. If you name your estate as beneficiary, the account will have to go through probate. For IRAs and qualified retirement plans, there may also be unfavorable income tax consequences.

Use caution when naming a trust as beneficiary. Consult your attorney or CPA before naming a trust as beneficiary for IRAs, qualified retirement plans, or annuities. There are situations where it makes sense to name a trust — for example if:

Your beneficiaries are minor children

You’re in a second marriage

You want to control access to funds

Be aware of tax consequences. Many assets that transfer by beneficiary designation come with special tax consequences. It’s helpful to work with an experienced tax advisor to help provide planning ideas for your particular situation.

Use disclaimers when necessary — but be careful. Sometimes a beneficiary may actually want to decline (disclaim) assets on which they’re designated as beneficiary. Keep in mind that disclaimers involve complex legal and tax issues and require careful consultation with your attorney and CPA.

The vast majority of physicians and medical professionals major in one of the hard science while in college; biology, engineering, chemistry, mathematics, computer science or physics; etc. Few take undergraduate courses in finance, business management, securities analysis, accounting or economics; although this paradigm is changing with modernity. These course are not particularly difficult for the pre-medical baccalaureate major, they are just not on the radar screen for time compressed and highly competitive students; nor are they needed for medical or nursing school admission, or the many related allied health professional schools.

In fact, William C. Roberts MD, originally from Emory University in Atlanta, and former editor for the Baylor University Medical Center Proceedings and The American Journal of Cardiology, opined just a decade ago:

“Of the 125 medical schools in the USA, only one of them to my knowledge offers a class related to saving or investing money.”

And so, it is important to review some basic principles of economics, finance and accounting as they relate to financial planning in thees two textbooks; and this ME-P.

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

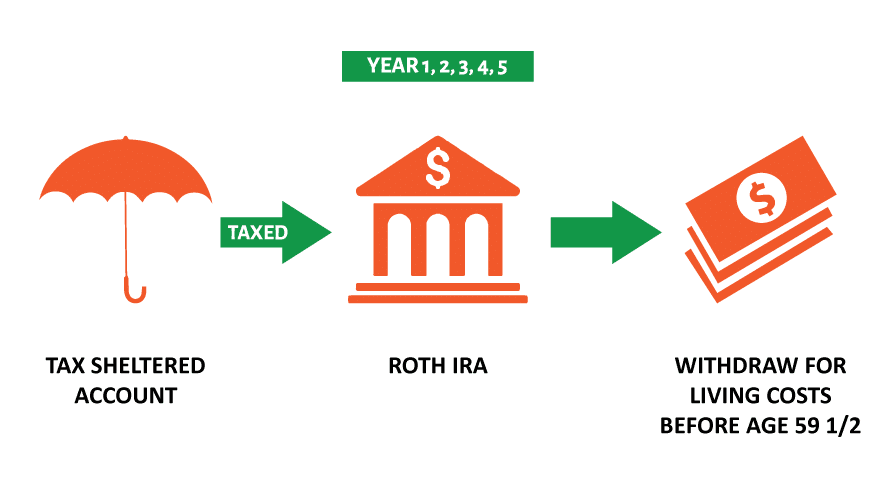

Why would a doctor consider a Roth IRA conversion?

By Staff Reporters

***

***

A Roth conversion involves transferring funds from a traditional retirement account—such as a 401(k), 403(b), or individual retirement account (IRA) funded with pre-tax dollars—into a Roth IRA.

The biggest benefit lies in the tax treatment of the converted funds. Once the funds are in the Roth IRA, future growth of those assets is tax-free. Withdrawals in retirement are also tax-free, assuming they meet certain criteria. As with any strategy, there are important considerations to keep in mind.

When you convert funds to a Roth IRA, the amount converted is taxable income in that tax year. For example, if you convert $100,000 from a traditional IRA to a Roth IRA, that $100,000 will be added to your taxable income in the conversion year.

Converting large amounts can result in a significant tax bill and may push you into a higher tax bracket. Even so, using retirement funds to pay taxes may make sense for those looking to convert large IRAs to reduce their future required minimum distributions (RMDs).

The timing of your Roth conversion matters too. Generally, it’s a good idea to convert when your income is lower—for example, after you’ve retired and before you begin drawing Social Security. You may also choose to convert over the course of several years to spread out the tax impacts. But if you can get comfortable with these considerations, a Roth conversion can provide you with benefits beyond tax-free growth and withdrawals.

Some of these benefits are:

Tax diversification. Having both traditional and Roth accounts allows you to manage your tax liability in retirement. For example, if your income in a given year is higher than expected, you can withdraw from the Roth IRA without increasing your taxable income.

No RMDs. Traditional IRAs and 401(k)s require you to begin taking RMDs at age 73. Roth IRAs have no RMD requirement during your lifetime. With a Roth account, you have more control over your retirement withdrawals and can leave the funds to grow for your heirs.

Benefits for heirs. Roth IRAs can be passed on to beneficiaries, who can inherit the account income tax-free. This means your heirs can enjoy the tax-free growth and withdrawals if the Roth IRA has been held for five years or more—a significant advantage, especially if your beneficiaries are in a higher tax bracket.

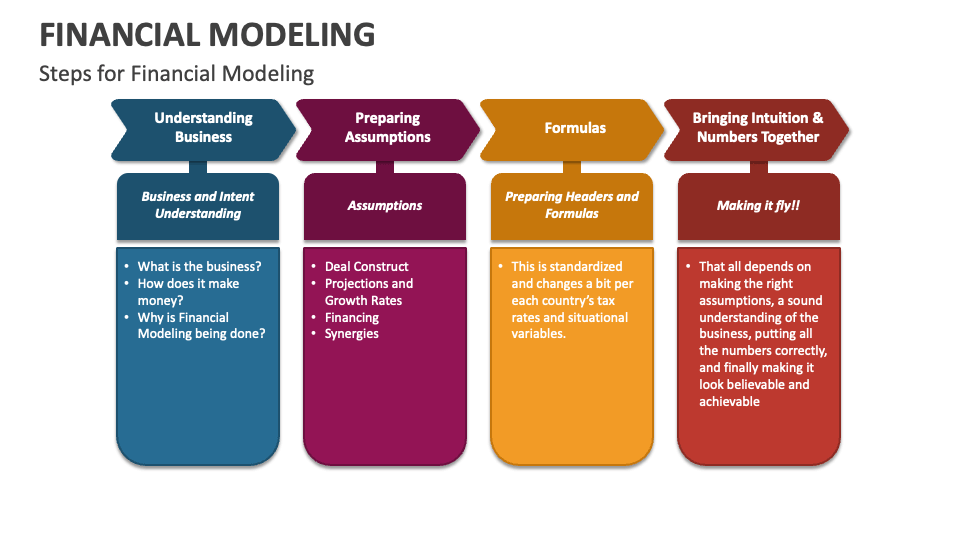

Financial Modeling is one of the most highly valued, but thinly understood, skills in financial analysis. The objective of financial modeling is to combine accounting, finance, and business metrics to create a forecast of a company’s future results.

According to Jeff Schmidt, a financial model is simply a spreadsheet, usually built in Microsoft Excel, that forecasts a business’s financial performance into the future. The forecast is typically based on the company’s historical performance and assumptions about the future and requires preparing an income statement, balance sheet, cash flow statement, and supporting schedules (known as a three-statement model, one of many types of approaches to financial statement modeling). From there, more advanced types of models can be built such as discounted cash flow analysis (DCF model), leveraged buyout (LBO), mergers and acquisitions (M&A), and sensitivity analysis

***

DEFINED TERMS

Discounted Cash Flow (DCF): A valuation method used to estimate the value of an investment based on its expected future cash flows, adjusted for the time value of money. It’s like deciding whether a treasure chest is worth diving for now, based on the gold coins you’ll be able to cash in later.

Sensitivity Analysis: This involves changing one variable at a time to see how it affects an outcome. Imagine tweaking your coffee-to-water ratio each morning to achieve the perfect brew strength.

Budget – A budget is the amount of money a department, function, or business can spend in a given period of time. Usually, but not always, finance does this annually for the upcoming year.

Rolling Forecast – A rolling forecast maintains a consistent view over a period of time (often 12 months). When one period closes, finance adds one more period to the forecast.

Topside – A topside adjustment is an overlay to a forecast. This is typically completed by the corporate or headquarter team. As individual teams submit a forecast, the consolidated result might not make sense or align with expectations. When this occurs, the high-level teams use a topside adjustment to streamline or adjust the consolidated view.

Monte Carlo Simulation: Picture yourself at the casino, but instead of gambling your savings away, you’re using this technique to predict different outcomes of your business decisions based on random variables. It’s like playing financial roulette with the odds in your favor.