BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and Morning Brew

***

***

Microsoft is celebrating its 50th birthday this week looking like a formerly washed up A-lister who’s suddenly rebounded and getting Oscar noms again.

Ever since Bill Gates and Paul Allen huddled in a garage in 1975 to start a company that’d define the experience of sitting in front of a boxy white PC monitor, Microsoft has had an uneven run. But after years of getting roasted for Internet Explorer, it now seems to be back on top—even briefly beating Apple as the world’s most valuable public company last year.

The tech giant can not only boast bonanza earnings, it also feels like a purveyor of the next big thing again, leading in the AI race through its partnership with OpenAI.

Windows washed

In the 1990s, it felt like Microsoft’s computer geeks were the overlords of tech. Windows powered most PCs, Internet Explorer became the go-to browser, and proficiency in Office tools became standard resume skills. But in the following decade, the company slept on internet tech and smartphones, ceding ground to Apple, Alphabet, and Meta.

It responded by going into midlife crisis mode, aka blowing cash on a series of questionable acquisitions to stay hip. That…didn’t help. By the 2010s, only grandparents could be reached @hotmail.com, Windows phones were a rarity, and no one used Bing as a verb.

When Gates stepped away from running the company in 2000, its new CEO Steve Ballmer grew its revenue threefold by the end of his tenure in 2013. He spearheaded Microsoft’s foray into gaming with the Xbox console and started its blockbuster cloud computing product Azure. But Microsoft’s profit growth slowed dramatically thanks to a massive cash bleed from its shopping spree.

It dropped $6.3 billion on the owner of ad tech platforms aQuantive to compete with Google’s ad business in 2007, only to write it off as a dud five years later.

The company burned at least $8 billion trying to make Windows phones a bigger force by buying Nokia’s cellphone division in 2014.

Microsoft paid $8.5 billion for Skype in 2011, which must’ve made it extra painful to announce that it was sunsetting the video calling service this winter.

***

***

Cash-slinging comeback kid

When it blew out forty candles in 2015, the tech giant was looking past its prime. The stock was trading at around $35 a share, well below its $58 peak in 1999. Its net profit for the year was $12 billion. But investors who held on until now were rewarded with shares going for $374 on its birthday this week after the company reported a net profit of $88 billion in the last financial year.

Much of the revenue now comes from its Azure cloud computing business, which has been boosted by the booming AI industry ravenous for server power.

When Microsoft’s current CEO Satya Nadella stepped into the role in 2014, he doubled down on Azure to make Microsoft into a B2B behemoth selling computing power to tech companies.

It is now the world’s second largest cloud provider after Amazon Web Services, with a 21% market share, according to Synergy Research Group.

Microsoft also bought some businesses that didn’t fail, including LinkedIn—the thought leadership hub with a user base that has soared to 1 billion since the 2016 acquisition. It also owns GitHub, the leading code-sharing platform for software developers. And in its biggest purchase yet, it snagged gaming IP giant Activision Blizzard that owns Call of Duty and World of Warcraft for a whopping $68 billion in 2022, hoping to make itself a dominant caterer to the Xbox joystick-wielding crowd.

It’s an AI company now

The not-quite-acquisition that really got Microsoft its groundbreaker’s glitz back was pouring $13 billion into OpenAI.

Having gotten in on the ground floor of the AI boom, Microsoft is harnessing OpenAI’s models to power its CoPilot AI agent, which it embedded into its Office tools and Teams app. This pits it against other tech giants betting that AI agents automating tasks will be the biggest in-cubicle revolution since Excel.

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

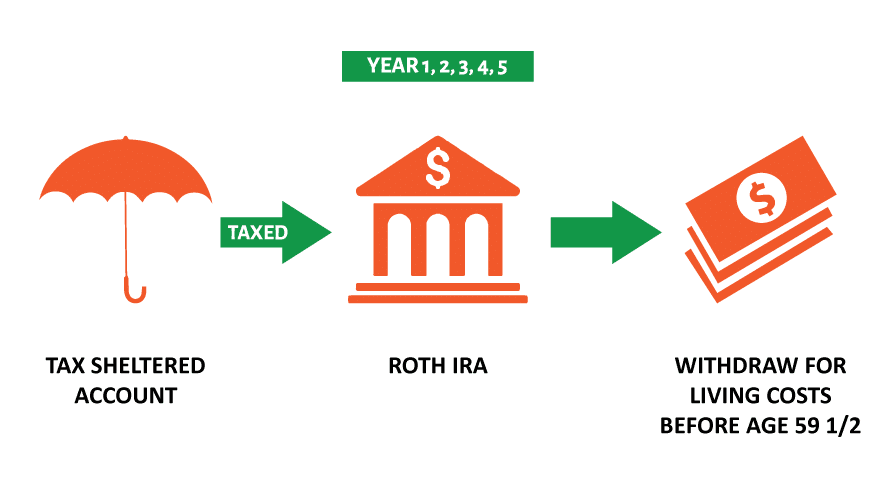

Why would a doctor consider a Roth IRA conversion?

By Staff Reporters

***

***

A Roth conversion involves transferring funds from a traditional retirement account—such as a 401(k), 403(b), or individual retirement account (IRA) funded with pre-tax dollars—into a Roth IRA.

The biggest benefit lies in the tax treatment of the converted funds. Once the funds are in the Roth IRA, future growth of those assets is tax-free. Withdrawals in retirement are also tax-free, assuming they meet certain criteria. As with any strategy, there are important considerations to keep in mind.

When you convert funds to a Roth IRA, the amount converted is taxable income in that tax year. For example, if you convert $100,000 from a traditional IRA to a Roth IRA, that $100,000 will be added to your taxable income in the conversion year.

Converting large amounts can result in a significant tax bill and may push you into a higher tax bracket. Even so, using retirement funds to pay taxes may make sense for those looking to convert large IRAs to reduce their future required minimum distributions (RMDs).

The timing of your Roth conversion matters too. Generally, it’s a good idea to convert when your income is lower—for example, after you’ve retired and before you begin drawing Social Security. You may also choose to convert over the course of several years to spread out the tax impacts. But if you can get comfortable with these considerations, a Roth conversion can provide you with benefits beyond tax-free growth and withdrawals.

Some of these benefits are:

Tax diversification. Having both traditional and Roth accounts allows you to manage your tax liability in retirement. For example, if your income in a given year is higher than expected, you can withdraw from the Roth IRA without increasing your taxable income.

No RMDs. Traditional IRAs and 401(k)s require you to begin taking RMDs at age 73. Roth IRAs have no RMD requirement during your lifetime. With a Roth account, you have more control over your retirement withdrawals and can leave the funds to grow for your heirs.

Benefits for heirs. Roth IRAs can be passed on to beneficiaries, who can inherit the account income tax-free. This means your heirs can enjoy the tax-free growth and withdrawals if the Roth IRA has been held for five years or more—a significant advantage, especially if your beneficiaries are in a higher tax bracket.

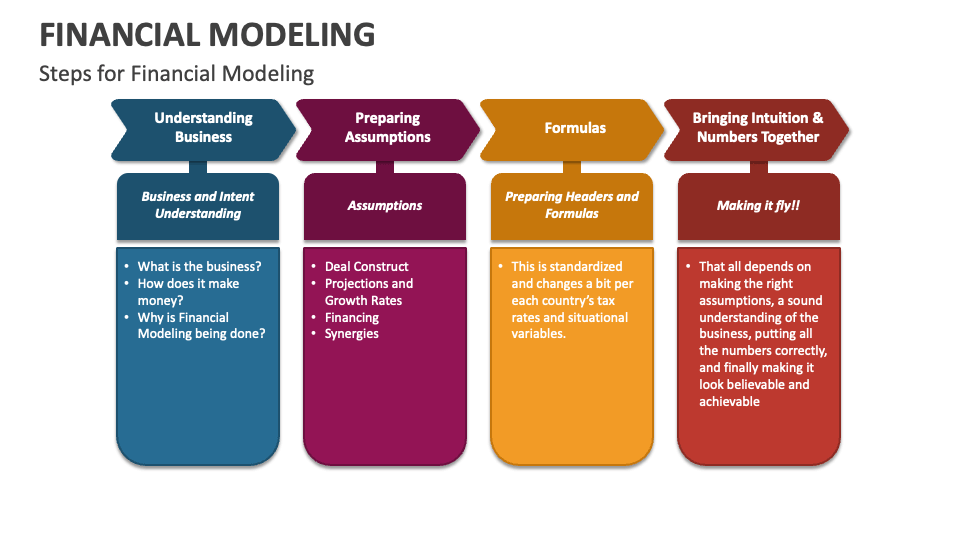

Financial Modeling is one of the most highly valued, but thinly understood, skills in financial analysis. The objective of financial modeling is to combine accounting, finance, and business metrics to create a forecast of a company’s future results.

According to Jeff Schmidt, a financial model is simply a spreadsheet, usually built in Microsoft Excel, that forecasts a business’s financial performance into the future. The forecast is typically based on the company’s historical performance and assumptions about the future and requires preparing an income statement, balance sheet, cash flow statement, and supporting schedules (known as a three-statement model, one of many types of approaches to financial statement modeling). From there, more advanced types of models can be built such as discounted cash flow analysis (DCF model), leveraged buyout (LBO), mergers and acquisitions (M&A), and sensitivity analysis

***

DEFINED TERMS

Discounted Cash Flow (DCF): A valuation method used to estimate the value of an investment based on its expected future cash flows, adjusted for the time value of money. It’s like deciding whether a treasure chest is worth diving for now, based on the gold coins you’ll be able to cash in later.

Sensitivity Analysis: This involves changing one variable at a time to see how it affects an outcome. Imagine tweaking your coffee-to-water ratio each morning to achieve the perfect brew strength.

Budget – A budget is the amount of money a department, function, or business can spend in a given period of time. Usually, but not always, finance does this annually for the upcoming year.

Rolling Forecast – A rolling forecast maintains a consistent view over a period of time (often 12 months). When one period closes, finance adds one more period to the forecast.

Topside – A topside adjustment is an overlay to a forecast. This is typically completed by the corporate or headquarter team. As individual teams submit a forecast, the consolidated result might not make sense or align with expectations. When this occurs, the high-level teams use a topside adjustment to streamline or adjust the consolidated view.

Monte Carlo Simulation: Picture yourself at the casino, but instead of gambling your savings away, you’re using this technique to predict different outcomes of your business decisions based on random variables. It’s like playing financial roulette with the odds in your favor.

What-If Analysis: Ever daydream about what would happen if you took that leap of faith with your business? This tool allows you to explore various scenarios without risking a dime. It’s like trying on outfits in a virtual dressing room before making a purchase.

Leveraged Buyout (LBO) Model: This is a bit like orchestrating a heist, but legally. It’s about acquiring a company using borrowed money, with plans to pay off the debts with the company’s own cash flows. High stakes, high rewards.

Mergers and Acquisitions (M&A) Model: Picture two puzzle pieces coming together. This model evaluates how combining companies can create a new, more valuable entity. It’s the corporate version of a matchmaker.

Three Statement Model: The holy trinity of financial modeling, linking the income statement, balance sheet, and cash flow statement. It’s like weaving a tapestry where each thread is crucial to the overall picture.

Capital Asset Pricing Model (CAPM): A formula that calculates the expected return on an investment, considering its risk compared to the market. It’s like choosing the best roller coaster in the park, balancing thrill and safety.

Cash Flow Forecasting: This is your financial weather forecast, predicting the cash flow climate of your business. It helps you plan for sunny days and save for the rainy ones.

Cost of Capital: The price of financing your business, whether through debt or equity. It’s like the interest rate on your growth engine, pushing you to maximize every dollar invested.

Debt Schedule: A timeline of your business’s debts, showing when and how much you owe. It’s your roadmap to becoming debt-free, one milestone at a time.

Equity Valuation: Determining the value of a company’s shares. It’s like assessing the worth of a rare gemstone, ensuring investors pay a fair price for a piece of the treasure.

Financial Leverage: Using debt to amplify returns on investment. It’s like using a lever to lift a heavy object, increasing force but also risk.

Forecast Model: A crystal ball for your finances, projecting future performance based on past and present data. It’s your guide through the financial wilderness, helping you navigate with confidence.

Operating Model: A detailed blueprint of how a business generates value, mapping out operational activities and their financial impact. It’s like laying out the inner workings of a clock, ensuring every gear turns smoothly.

Revenue Growth Model: This tracks potential increases in sales over time, charting a course for expansion. It’s like plotting your ascent up a mountain, anticipating the effort required to reach the summit.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

***

The Hedge Fund manager I am considering is a Registered Investment Adviser [RIA]

QUESTION: What is a Registered Investment Advisor?

If the fund manager is an entity, then any individual you deal with will be a registered investment adviser representative. If the fund manager is an individual, then that individual is a registered investment adviser. In either case, the designation implies several steps have been taken.

In order to become a registered investment adviser, an individual must register for and pass the Series 65 Uniform Investment Adviser Law Exam, a three-hour, 130-question computer-based exam administered by the North American Securities Administrators Association. Topics covered include economics and analysis, investment vehicles, investment recommendations and strategies, and ethics and legal guidelines. A passing score is 70 percent or higher.

Once an individual has passed the Series 65, he or she must then apply via Form ADV to become a registered investment adviser. This application is made to either a state authority or to the SEC, depending on the adviser’s assets under management. If assets under management exceed $30 million, then the adviser must register with the SEC.

Form ADV consists of two parts. Part I provides general information to the regulatory authority. Part II is designed to be distributed to potential clients, and includes disclosure of a decent amount of information about the adviser. If the manager is a registered investment adviser, then you should expect to receive as part of the offering documentation either a current copy of Part II of the adviser’s Form ADV or a brochure that contains all the current information in Part II of Form ADV.

In addition to filing Form ADV and paying a small fee, the registered investment adviser becomes subject to extra administrative/regulatory burden as well as capital adequacy requirements that state the Adviser must maintain certain net worth levels.

By and large, because of the extra administrative burden as well as restrictions on certain activities, hedge fund managers attempt to avoid registering as investment advisers. Whether such managers can or cannot avoid such registration is largely dependent upon the state in which the manager operates. In California, for instance, hedge fund managers must register as investment advisers. In New York, such registration is not necessary. Not surprisingly, hedge fund managers located in California are rare, while they are quite plentiful in New York.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

***

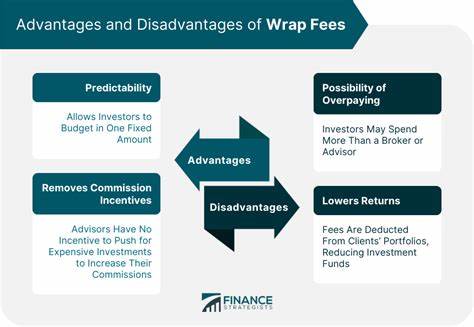

My stock broker is telling me about a “wrap-fee” program involving a hedge fund manager.

QUESTION: What is a Wrap Fee?

A wrap fee program is a service that provides investment advice and portfolio management to clients for one all-inclusive fee. The fee pays for the services provided to the client, including but not limited to securities transactions, portfolio management, research, brokerage, and administrative services. Wrap fee programs also provide an understanding of a client’s financial goals and objectives; research and selection of assets; implementation of investment decisions; account statements, and access to real-time financial data.

The Investment Advisers Act of 1940 regulates investment advisors when they offer these wrap fee programs and requires them to provide comprehensive disclosure documents before investing. This act helps ensure clients have access to all important information that affects their investment decisions.

QUESTION: Why do I need my stock broker? Can I just go directly to the hedge fund manager?

Yes, you can, but you may find a different fee arrangement when you reach the hedge fund manager, and you may be participating in an unethical transaction. When hedge fund managers set up separate accounts for wrap-fee clients, they agree to take a set fee in exchange for managing this money. They also enter into agreements with one or more brokers to help market this aspect of their money management business. A portion of the wrap fee you pay goes to the broker, and a portion goes to the manager. Incentive compensation is not generally used.

When approached directly, hedge fund managers will typically offer only the hedge fund, complete with incentive compensation and pooled investment features. However, if the hedge fund manager is willing to set up a separate account, it is possible that the investor will find the set fee much less than what he or she would have paid in a wrap fee account through a broker.

Finally, the very large caveat to all this is that the ethics of a hedge fund manager who steals clients from brokers with whom he has a marketing relationship ought to be called into question. And when it comes to hedge funds, the ethics of the manager are of paramount importance.

Posted on April 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS – MARKET VOLATILITY

By Staff Reporters

***

***

US stocks nosedived on Thursday, with the Dow tumbling more than 1,200 points as President Trump’s surprisingly steep “Liberation Day” tariffs sent shock waves through markets worldwide. The tech-heavy NASDAQ Composite (IXIC) led the sell-off, plummeting over 4%. The S&P 500 (GSPC) dove 3.7%, while the Dow Jones Industrial Average (^DJI) tumbled roughly 3%. [ongoing story].

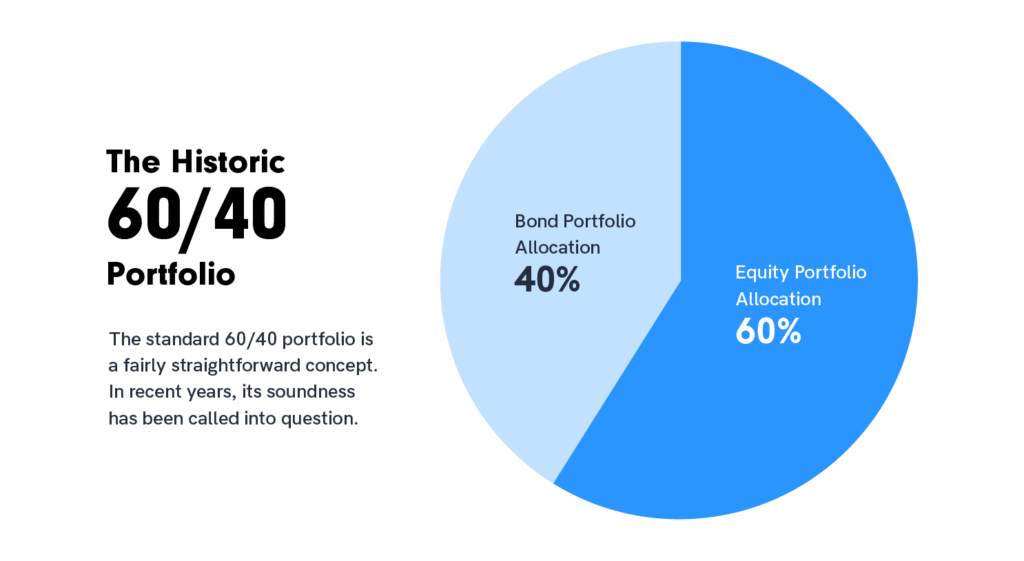

So, does the traditional 60 stock / 40 bond strategy still work or do we need another portfolio model?

***

The 60/40 strategy evolved out of American economist Harry Markowitz’s groundbreaking 1950s work on modern portfolio theory, which holds that investors should diversify their holdings with a mix of high-risk, high-return assets and low-risk, low-return assets based on their individual circumstances.

While a portfolio with a mix of 40% bonds and 60% equities may bring lower returns than all-stock holdings, the diversification generally brings lower variance in the returns—meaning more reliability—as long as there isn’t a strong correlation between stock and bond returns (ideally the correlation is negative, with bond returns rising while stock returns fall).

For 60/40 to work, bonds must be less volatile than stocks and economic growth and inflation have to move up and down in tandem. Typically, the same economic growth that powers rallies in equities also pushes up inflation—and bond returns down. Conversely, in a recession stocks drop and inflation is low, pushing up bond prices.

***

But, the traditional 60/40 portfolio may “no longer fully represent true diversification,” BlackRock CEO Larry Fink writes in a new letter to investors.

Instead, the “future standard portfolio” may move toward 50/30/20 with stocks, bonds and private assets like real estate, infrastructure and private credit, Fink writes.

Here’s what experts say individual investors may want to consider before dabbling in private investments.

It may be time to rethink the traditional 60/40 investment portfolio, according to BlackRock CEO Larry Fink. In a new letter to investors, Fink writes the traditional allocation comprised of 60% stocks and 40% bonds that dates back to the 1950s “may no longer fully represent true diversification.“

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on April 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHA CPHQ CMP™

***

***

Finally … Fiduciary second investing and financial planning opinions right here!

Telephonic or electronic advice for medical professionals that is:

Objective, affordable, medically focused and financially personalized

Rendered by a pre-screened financial consultant for doctors and medical professionals

Offered on a pay-as-you-go basis, by phone or secure e-mail transmission

The iMBA Discussion Forum™ is a physician-to-financial advisor telephone or e-mail portal that connects independent financial professionals to doctors, nurses or healthcare executives desiring affordable and unbiased financial planning advice.

Medical professionals and healthcare executives can now receive direct access to pre-screened iMBA professionals in the areas of Investing, Financial Planning, Asset Allocation, Portfolio Management, Insurance, Mortgage and Lending, Human Resources, Retirement Planning and Employee Benefits. To assist our medical professional and healthcare executive members, we can be contracted with per-minute or per-project fees, and contacted by client phone, email or secure instant messaging.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

QUESTION:Can I invest my Individual Retirement Account [IRA] in a Hedge Fund?

This is up to the manager, but there is no legal restriction on a hedge fund accepting individual retirement account (IRA) assets. IRA accounts are not well suited for funds that make extensive use of leverage, however. In such cases, the fund is likely to generate significant amounts of unrelated business taxable income (UBTI) – profits of the fund attributable to the use of leverage. The holder of an IRA account must pay taxes on UBTI, even if the UBTI was generated in an IRA account.

But, today’s hedge funds may or may not use leverage. Many hedge funds are not hedged at all, but rather are just specialized versions of regular long stock portfolios. If such funds do not use much leverage, IRA investors will not encounter much difficulty with UBTI and should not hesitate in considering these funds.

In considering whether to accept IRA money, hedge fund managers must consider several factors. If the only type of retirement money accepted by the hedge funds is IRA money, then the manager has no limit on how much retirement money the fund can accept. If, however, there are other types of retirement money invested in the fund, such as pension funds, IRA money will be counted towards a total of 25 percent of fund assets that can be invested in retirement accounts before the fund becomes subject to the Employment Retirement Income Security Act of 1974 (ERISA). Funds subject to ERISA regulations face a heavy administrative burden and more restrictions than most fund managers like.

Finally, IRA distributions from a hedge fund are subject to the standard 20 percent withholding unless the funds are directly rolled over to other qualified plans.

*** Several years ago we noted that far too many mid-career, mature and physician clients using traditional stock brokers, management consultants and “financial advisors”, seemed to be less successful than those who went it alone. These Do-it-Yourselfers [DIYs] had setbacks and made mistakes, for sure. But, the ME Inc,. doctors seemed to learn from their mistakes and did not incur the high management and service fees demanded from general or retail one-size-fits-all “advisors.”

In fact, an informal inverse related relationship was noted, and dubbed the “Doctor Effect.” In other words, the more consultants an individual doctor retained; the less well they did in all disciplines of the financial planning, professional portfolio and investing continuum.

Of course, the reason for this discrepancy eluded many of them as Wall Street brokerages and wire-houses flooded the media with messages, infomercials, print, radio, TV, texts, tweets, and internet ads to the contrary. Rather than self-learn the basics, the prevailing sentiment seemed to purse the holy grail of finding the “perfect financial advisor.” This realization was a confirmation of the industry culture which seemed to be: Bread for the advisor – Crumbs for the client!

And so, we at the the Institute of Medical Business Advisors Inc. (iMBA), and this Medical Executive-Post, formed a cadre’ of technology focused and highly educated doctors, financial advisors, attorneys, accountants, psychologists and educational visionaries who decided there must be a better way for their healthcare colleagues to receive financial planning advice, products and related management services within a culture of fiduciary responsibility.

We trust you agree with this ME Inc philosophy as illustrated in this free white paper available upon request.

PROFESSIONAL PORTFOLIO CONSTRUCTION [Investing Assets and their Management] Subscribe, Read, Like and Refer

Email whiote paper request here:MarcinkoAdvisors@outlook.com

Posted on March 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Donald Trump has officially dropped a stablecoin. It’s called USD1, and it’s pegged 1:1 with the US dollar, according to a statement from his family company World Liberty Financial Inc, (WLFI) today. The company says the token is fully backed by short-term US government treasuries, USD deposits, and other cash equivalents. Every token equals one dollar, no exceptions. WLFI says it built the whole thing to give people a stablecoin they don’t have to second guess.

US stocks rose for a third day in a row despite souring consumer confidence — and as investors weighed whether President Trump would temper his plans for upcoming tariffs.

The benchmark S&P 500 (^GSPC) rose more than 0.1%, while the Dow Jones Industrial Average (^DJI) ticked just above the flatline. The tech-heavy NASDAQ Composite (^IXIC) rose nearly 0.5%, bolstered by a more than 3% jump from Tesla (TSLA).

Absolute Return – the goal is to have a positive return, regardless of market direction. An absolute return strategy is not managed relative to a market index.

Accredited Investor – wealthy individual or well-capitalized institutions covered under Regulation D of the Securities Act of 1933.

Alpha – the return to a portfolio over and above that of an appropriate benchmark portfolio (the manager’s “value added”).

Arbitrage – any strategy that invests long in an asset, and short in a related asset, hoping the prices will converge.

Attribution – the process of “attributing” returns to their sources. For example, did the returns to a portfolio (over and above some benchmark) come from stock selection, industry/sector over- or under-weighting or factor weighting. Software programs are helpful in reporting an attribution.

Beta – a measure of systematic (i.e., non-diversifiable) risk. The goal is to quantify how much systematic risk is being taken by the fund manager vis-à-vis different risk factors, so that one can estimate the alpha or value-added on a risk-adjusted basis.

Correlation – a measure of how strategy returns move with one another, in a range of –1 to +1. A correlation of –1 implies that the strategies move in opposite directions. In constructing a portfolio of hedge funds, one usually wants to combine a number of non-correlated strategies (with decent expected returns) to be well diversified.

Drawdown – the percentage loss from a fund’s highest value to its lowest, over a particular time frame. A fund’s “maximum drawdown” is often looked at as a measure of potential risk.

Hurdle Rate – the return where the manager begins to earn incentive fees. If the hurdle rate is 5% and the fund earns 15% for the year, then incentive fees are applied to the 10% difference.

Leverage – one uses leverage if he borrows money to increase his position in a security. If one uses leverage and makes good investment decisions, leverage can magnify the gain. However, it can also magnify a loss.

Opportunistic – a general term that describes an aggressive strategy with a goal of making money (as opposed to holding on to the money one already has).

***

***

Pairs Trading – usually refers to a long/short strategy where one stock is bought long, and a similar stock is sold short, often within the same industry. Buying the stock of Home Depot and shorting Lowe’s in an equal amount would be an example.

Portfolio Simulation – involves testing an investment strategy by “simulating” it with a database and analytic software. Often referred to as “backtesting” a strategy. The simulated returns of the strategy are compared to those of a benchmark over a specific time frame to see if it can beat that benchmark.

Sharpe Ratio – a measure of risk-adjusted return, computed by dividing a fund’s return over the risk-free rate by the standard deviation of returns. The idea is to understand how much risk was undertaken to generate the alpha.

Short Rebate – if you borrow stock and then sell it short, you have cash in your account. The short rebate is the interest earned on that cash.

R-Squared – a measure of how closely a portfolio’s performance varies with the performance of a benchmark, and thus a measure of what portion of its performance can be explained by the performance of the overall market or index. Hedge fund investors want to know how much performance can be explained by market exposure versus manager skill.

Transportable Alpha – the alpha of one active strategy can be combined with another asset class. For example, an equity market-neutral strategy’s value-added can be “transported” to a fixed income asset class by simply buying a fixed income futures contract. The total return comes from both sources.

Value at Risk – a technique which uses the statistical analysis of historical market trends and volatilities to estimate the likelihood that a specific portfolio’s losses will exceed a certain amount.

SO – HOW MUCH IS A “FINANCIAL ADVISOR” REALLY WORTH?

This blog holds a rather uncomplimentary opinion of financial advisors, and the financial services and brokerage industry as a whole; deserved, or not? The entire site hints at this attitude as well, in favor of a going it alone or ME, Inc investing when possible. Nevertheless, it is reasonable to wonder how much boost in net-returns might an educated and informed, fee transparent and honest, fiduciary focused “financial advisor” add to a clients’ investment portfolio; all things being equal [ceteris paribus].

And, can it be quantified?

Well, according to Vanguard Brokerage Services®, perhaps as much as 3%? In a decade long paper from the Valley Forge, PA based mutual fund and ETF giant, Vanguard said financial advisors can generate returns through a framework focused on five wealth management principles:

• Being an effective behavioral coach: Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value added: up to 1.50%).

• Applying an asset location strategy: The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value added: from 0% to 0.75%).

• Employing cost-effective investments: This component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value added: up to 0.45%).

• Maintaining the proper allocation through rebalancing: Over time, as investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value added: up to 0.35%).

• Implementing a spending strategy: As the retiree population grows, an advisor can help clients make important decisions about how to spend from their portfolios. (Potential value added: up to 0.70%).

Source: Financial Advisor Magazine, page 20, April 2014.

Assessment

However, Vanguard notes that while it’s possible all of these principles could add up to 3% in net returns for clients, it’s more likely to be an intermittent number than an annual one because some of the best opportunities to add value happen during extreme market lows and highs when angst or giddiness [fear and greed] can cause investors to bail on their well-thought-out investment plans.

And, is the study applicable to doctors and allied healthcare providers? Doe Vanguard have a vested interest in the topic. What about fee based versus fee-only financial advice?

Conclusion

Finally, recognize the plethora of other financial planning life-cycle topics addressed in this ME-P were not included in the Vanguard investment portfolio-only study a decade ago.

And what about today with contemporaneous internet advising, chat-rooms, linkedin, robo-advisors, reddit and the like?

Posted on March 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BANK IDENTIFICATION NUMBER – DEFINED

By Staff Reporters

***

***

What Is a BIN Attack?

The BIN, or the Bank Identification Number, is the first six digits on a credit card. These are always tied to its issuing institution – usually a bank. In a BIN attack, fraudsters use these six numbers to algorithmically try to generate all the other legitimate numbers, in the hopes of generating a usable card number.

How Does a BIN Attack Work?

Fraudsters conduct BIN attacks by generating hundreds of thousands of possible credit card numbers and testing them out.

A fraudster looks up the BIN of the bank they will target. Ranging from four to six digits, this information is in the public domain and is thus easy to source.

Using dedicated software such as an auto-dialer, they generate thousands, often tens of thousands, combinations of possible existing card numbers by this issuer.

At this point, these credentials need to be tested. The fraudster identifies a suitable online shop or donation page.

They start card testing by attempting a small payment with each generated card number.

They keep track of the small percentage of card details that worked, which they are ready to use in earnest for their fraudulent pursuits.

***

***

Remember that the fraudster will start off with only six digits, yet there are many more card details required for a successful transaction. If those are entered erroneously, the transaction will decline. This includes the CVV number, the expiration date, as well as likely address verification service (AVS) failures. Card testing transactions are executed remotely in a fast fashion, so distance checks should also be a hint as well as velocity alerts.

Fraudsters may use bad merchant accounts directly for this purpose, or more frequently involve multiple online stores and services during a BIN attack, as their attempts keep getting blocked at most outlets.

Posted on March 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

The Power of Attorney Mistake That Could Cost You Everything

By Rick Kahler CFP®

***

***

Recently, reading a training manual on elder abuse, I was reminded of a financial risk that is often overlooked. One of the fastest and easiest ways to unravel your financial security is to have the wrong person gain control of your money.

The example in the manual mirrored a heartbreaking situation I once experienced with a long-term client. As her mental and physical health declined, this single woman moved into assisted living. Her newly designated power of attorney, a relative from out of town, took control of her financial affairs.

Almost immediately, without consulting us, the relative began making large withdrawals, closed her accounts, and transferred funds elsewhere. They challenged the financial plan, investments, and strategies we had established to safeguard the client’s financial security and provide for her long-term care. Even though their actions threatened the client’s wellbeing, we were powerless to stop them. Our only recourse was to report the behavior to the authorities.

This heartbreaking and frustrating experience underscored just how critical it is to be mindful when executing a Power of Attorney. Besides designating someone you trust, it is wise to build in safeguards to prevent even a well-meaning relative from inadvertently derailing a carefully constructed financial plan.

***

***

One such safeguard is to include a financial advisor in your POA—as long as that person is a fee-only, fiduciary advisor with an obligation to act in your best interests. In many cases, advisors are hesitant to suggest this option because they are sensitive to the potential conflict of interest and do not want to appear self-serving. An unfortunate reality is that you should be cautious if an advisor, particularly one who sells products on commission, seems eager to be added to your POA.

Including your financial advisor in your POA does not mean you designate them as your agent to manage your affairs. Instead, you include a clause naming them as the professional of record you want your designated agent to continue working with. This creates continuity and accountability. It prevents your agent from replacing your advisor with someone who may be unfamiliar with your needs and goals, unqualified, or untrustworthy.

Your advisor might also recommend adding a secondary safeguard, such as naming an attorney or accountant to oversee the selection of a successor advisor in case your current advisor is unable to continue. This additional layer of protection ensures that the financial professionals guiding your portfolio remain aligned with your best interests. Taking these extra steps can save you—and your loved ones—from significant financial stress down the road.

Including safeguards in your POA is not about mistrusting your loved ones, but about equipping them with the right resources and support to act in your best interest. Financial management is complex, and it requires expertise that most people, even those with the best intentions, may not possess.

One of the hardest parts about planning for diminished financial capacity is the emotional aspect. No one likes to imagine a time when they might not be able to manage their own money. But in reality, taking steps now to protect your financial future is the ultimate act of control. It can help ensure that your wishes are respected and the financial foundation you’ve worked so hard to build remains intact.

Remember, too, that avoiding conversations often increases financial vulnerability. If you don’t have a POA or aren’t comfortable with what you do have, now is the time to bring it up with your advisor, attorney, or a trusted family member. These safeguards are about protecting yourself. They also support those you will rely on to care for you and your financial legacy,

Posted on March 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

Today, I’m going to share stories about my best and worst investment decisions. But don’t worry, this isn’t just a brag-and-cringe session about making or losing money. These stories are about the valuable lessons learned, and how these adventures in investing helped shape my current approach.

The Best Investment Decision

In investing, you don’t get extra points for creativity or difficulty. A million dollars earned while you are smiling buys as many potatoes as a million dollars that cost you your marriage and hair.

However, from a personal, creative satisfaction perspective, our investment in Uber was one of our best. That’s not to say that it has been the most successful decision from a financial perspective, at least not yet.

Uber doesn’t fit into the traditional value stock category. Until 2023, the third year of our ownership, it never made money. It was a stock everyone hated. After we bought it, I had clients reach out to me asking if I had been kidnapped and someone else was making these purchases of Uber.

We bought more shares very opportunistically during and after the pandemic. I wrote a long research report on it, which you can read here.

On one hand, Uber’s switchboard is a digital business, but the company also has a physical presence in thousands of cities, which incurs costs (the analog side of the business). Additionally, the availability of cheap money caused the ride-share market to go crazy and act rationally irrational, as competitors jostled in a land grab.

My thesis consisted of several insights:

Unlike traditional-tech, digital-only companies, Uber is a hybrid, both digital and analog. Thus, its cost structure is much higher than that of other companies. This, in part, explains the higher losses.

It has a strong brand; its name has become a verb.

The rideshare market is inevitable and will only continue to grow. Uber is not just in competition with taxis, second cars, or seldomly used cars; it is also in competition with the favors we ask of friends and relatives, such as dropping us off at the mechanic or picking us up from the doctor’s office.

Uber has global scale, which its competitors lack, allowing it to spread R&D across more markets.

As its revenue grows, each incremental dollar comes with a very high margin, which directly drops to the bottom line. Therefore, at some point, its earnings will explode to the upside as fixed costs stop growing, allowing it to scale.

The Uber story is not over; we still own the stock. I don’t want to do a celebratory dance. But this idea came with a lot of creative satisfaction. There is another point of pride here. Despite our very tumultuous ownership of this stock, we remained rational (I have written about that here). We bought more when it became extremely undervalued, and I would be lying if I said that was psychologically easy – it was not, but we followed our research and process.

The Worst Investment Decision

My worst investments that resulted in losses had several things in common: They were low-quality companies; their financials were complex and not transparent (for instance, one-time items were labeled as “one-time” every quarter); and they had questionable management.

However, they were all considered “cheap”… until they were not. Now, I hope you see why I am dogmatic about quality.

However.

When you are wrong on an investment and you lose money, the most you can lose is 100%. I have learned a lot from those. But they were not my worst investments. Those were the ones where I left 300–400% on the table when I sold too soon. Let me detail two examples.

EA – Electronic Arts

We bought EA in the early 2010s. I wrote about it – you can read my investment case for it here. To sum up, games were moving from being sold in stores to being digital downloads, which would lead to higher margins (don’t have to pay for packaging and Best Buy to sell them). The market for games was exploding, as every adult and teenager had a gaming device in their hands – a smartphone. The market for video games was going to be much larger. EA was the largest player in that space, with great franchises.

The following two years of ownership were very painful. EA had a few big game flops, and the market did not care about improving fundamentals. The stock kept declining. We continued to buy more. Every time we bought more shares, the stock fell further. Fast-forward a year or two. The stock doubled from our original purchase, but I was mentally exhausted. I did a celebratory dance and sold the stock. The stock then went up another 4x within a few years after we sold it. It went up for the right reasons – its earnings exploded to the upside, in line with my original thesis.

The sale was a mistake, not because the price went up but because I let frustration over the stock-price decline (volatility) get to me. Investing is a mental game. I learned from this adventure that it is important to zoom out and not obsess over individual stocks in the portfolio. This is why we have a portfolio. It was a very costly but educational mistake. Our ownership of Uber was not a walk in the park, either – just look at the stock price over the last few years. But I had learned my lesson from EA and was able to do the analysis, update our model, and zoom out.

In investing, there is a big difference between intellectual and tactile knowledge. I am going to go PG-13 on you for a second and quote the irascible Charlie Munger: “Learning about investing through a model portfolio is like learning about sex through romantic novels.” A big part of investing is observing yourself as an investor – your thoughts and emotions as you ride the actual rollercoaster of owning a stock.

I also made an important modification to our process.

We always value every company in the portfolio on earnings (free cash flows) at least four years out. Why four years? Three seems too short. There is no magic in this number, other than it being longer than most analyst estimates. We do this for all stocks in the portfolio, and then the total return for each is calculated and annualized. If a company has strong growth potential, it may appear to be expensive based on current earnings; but in reality, it may actually be cheap based on earnings projected four years from now.

On the other side of the spectrum, a company that has no growth or dividends may seem “cheap” based on its current earnings multiple, but this cheapness may quickly dissipate once a total return is calculated using future earnings. Time is on the side of growing businesses and the enemy of the ones that stand still. Therefore, a non-growing or slow-growing business needs a much greater discount (margin of safety) to secure a spot in our portfolio.

I want to stress another point. We sometimes sell a stock and then it goes higher. If we sold it for the right fundamental reasons, this doesn’t bother me. There is very little to learn.

Twilio

I’ll give you another crazy example. We bought Twilio at $25 in 2017 or so. Our thesis was that they had built the largest digital telecommunications network, which gave them a brief competitive advantage. They were also spending 5x more on R&D than competitors to build applications around this network, which would give them long-term advantages.

The stock price went up to $60 in a few months without anything significantly changing, so we sold a third of our position. Then it went up to $90, and we sold some more. To our disbelief, we sold the rest at around $120, a bit before the pandemic.

During the pandemic, Twilio’s price hit $400. I had zero regret about not holding on to the shares. Absolutely none. Twilio’s profitability did not match the stock market’s opinion of its price. Twilio’s stock price was as crazy to me at $250 as it was at $300 or $400. After reviewing our models, we concluded that even $120 was at the extreme end of our optimistic assumptions. Fast-forward to today, where the stock is at $60 or so. We are currently sharpening our pencils, but we have not bought the stock – yet.

Selling EA was a mistake; selling Twilio was not.

***

Key takeaways

My “best investment decision” with Uber wasn’t just about financial gains, but the creative satisfaction it brought. It taught me the value of sticking to our research and process, even when it’s psychologically challenging.

The worst investments often share common traits: low-quality companies, complex financials, questionable management, and the illusion of being “cheap.” This reinforces my dogmatic stance on prioritizing quality.

Sometimes, the costliest mistakes aren’t the ones where you lose money, but those where you leave significant gains on the table by selling too soon. My experience with EA taught me this lesson the hard way.

There’s a crucial difference between intellectual and tactile knowledge in investing. Actually owning stocks and experiencing the emotional roller coaster is invaluable for developing as an investor.

Selling a stock that later increases in value isn’t always a mistake if the decision was based on sound fundamental reasons. My experience with Twilio illustrates this point – sometimes it’s right to sell even if the price continues to climb.

NOTE:Please read the following important disclosure here.

According to Patricia Salber MD [personal communication], there are a number of reasons why direct patient access to laboratory medical results is a good idea:

Between 8 and 26% of abnormal test results, including those suspicious for cancer, are not followed up in a timely manner. Direct access could help reduce the number of times this occurs

Self-management, particularly of chronic illness has known benefits. Just like the QS people, many folks with chronic illness obtain and manage to self-acquired lab results every day via gluco-meters, home pulmonary function tests, blood pressure measurements, and so forth. Direct access to laboratory-acquired data, one could argue is a continuation of that personal responsibility

Patients want to be notified about their results in what they perceive as a timely fashion. In one study, patients who received direct notification of their bone density tests results were more likely to perceive they had timely notification compared to usual care even though there was no measurable effect on actual treatment received after three months

Being more responsible for test results could encourage consumers to try to learn more about the meaning of the test results, conceivably increasing their health literacy.

But, the arguments against direct access discussed include the following:

Patients prefer their physicians contact them directly when they have abnormal test results, although the major studies published in 2005 and 2009, preceded the extraordinary use of the internet to access health information that exists today.

There is concern over whether patients will know what to do when they receive the results – will they make erroneous interpretations or fail to contact their docs? This could be, but the intent of the proposed rule is shared access to the results. We suspect if the rule become law, docs will develop better notification mechanisms so that they reach the patient before the patient directly accesses the results or lab companies will design better lab test notifications with easy-to-understand interpretations or a whole new industry will appear that can provide instantly available individualized lab interpretation…or maybe all three of these would happen and that would be a very good thing.

Unknown impact of dual notification (doctors and patients) of lab test results on physician behavior…would docs simply shift responsibility for initiating follow-up care from themselves to their patients?

Would direct access of life-changing lab tests, such as HIV or malignancy, lead to unnecessary patient anxiety – or worse? (Conversely, is there less anxiety, desperation, or suicidal ideation if the bad news is delivered face to face?

Individuals likely may contact their physicians immediately after getting the lab results asking for a telephonic or face-to-face interpretation … it is not known how this would impact physician workload and/or potential for reimbursement [personal communication, Richard Hudson DO, Atlanta, GA].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and IRS

***

***

Straddles: A straddle is any set of offsetting positions on personal property. For example, a straddle may consist of a purchased option to buy and a purchased option to sell on the same number of shares of the security, with the same exercise price and period.

Personal property.

This is any actively traded property. It includes stock options and contracts to buy stock but generally does not include stock.

Straddle rules for stock.

Although stock is generally excluded from the definition of personal property when applying the straddle rules, it is included in the following two situations.

The stock is of a type that is actively traded, and at least one of the offsetting positions is a position on that stock or substantially similar or related property.

The stock is in a corporation formed or availed of to take positions in personal property that offset positions taken by any shareholder.

Note

For positions established before October 22, 2004, condition 1 above does not apply. Instead, personal property includes stock if condition 2 above applies or the stock was part of a straddle in which at least one of the offsetting positions was:

An option to buy or sell the stock or substantially identical stock or securities,

A securities futures contract on the stock or substantially identical stock or securities, or

A position on substantially similar or related property (other than stock).

Position

A position is an interest in personal property. A position can be a forward or futures contract or an option.

An interest in a loan denominated in a foreign currency is treated as a position in that currency. For the straddle rules, foreign currency for which there is an active inter bank market is considered to be actively traded personal property.

Offsetting position

This is a position that substantially reduces any risk of loss you may have from holding another position. However, if a position is part of a straddle that is not an identified straddle, do not treat it as offsetting to a position that is part of an identified straddle.

Presumed offsetting positions

Two or more positions will be presumed to be offsetting if:

The positions are established in the same personal property (or in a contract for this property), and the value of one or more positions varies inversely with the value of one or more of the other positions;

The positions are in the same personal property, even if this property is in a substantially changed form, and the positions’ values vary inversely as described in the first condition;

The positions are in debt instruments with a similar maturity, and the positions’ values vary inversely as described in the first condition;

The positions are sold or marketed as offsetting positions, whether or not the positions are called a straddle, spread, butterfly, or any similar name; or

The aggregate margin requirement for the positions is lower than the sum of the margin requirements for each position if held separately.

Related persons

To determine if two or more positions are offsetting, you will be treated as holding any position your spouse holds during the same period. If you take into account part or all of the gain or loss for a position held by a flow-through entity, such as a partnership or trust, you are also considered to hold that position.

Some Stupid Things Financial Advisors Say to Physician Clients

A few years ago and just for giggles, colleague Lon Jefferies MBA CFP® and I collected a list of dumb-stupid things said by some Financial Advisors to their doctor, dentist, nurse and and other medical professional clients, along with some recommended under-breath rejoinders:

“They don’t have any debt except for a mortgage and student loans.” OK. And I’m vegan except for bacon-wrapped steak.

“Earnings were positive before one-time charges.” This is Wall Street’s equivalent of, “Other than that Mrs. Lincoln; how was the play?”

“Earnings missed estimates.” No. Earnings don’t miss estimates; estimates miss earnings. No one ever says “the weather missed estimates.” They blame the weatherman for getting it wrong. Finance is the only industry where people blame their poor forecasting skills on reality.

“Earnings met expectations, but analysts were looking for a beat.” If you’re expecting earnings to beat expectations, you don’t know what the word “expectations” means.

“It’s a Ponzi scheme.” The number of things called Ponzi schemes that are actually Ponzi schemes rounds to zero. It’s become a synonym for “thing I disagree with.”

“The [thing not going perfectly] crisis.” Boy who cried wolf, meet analyst who called crisis.

“He predicted the market crash in 2008.” He also predicted a crash in 2006, 2004, 2003, 2001, 1998, 1997, 1995, 1992, 1989, 1984, 1971…

“More buyers than sellers.” This is the equivalent of saying someone has more mothers than fathers. There’s one buyer and one seller for every trade. Every single one.

“Stocks suffer their biggest drop since September.” You know September was only six weeks ago, right?

“We’re cautiously optimistic.” You’re also an oxymoron.

[Guy on TV]: “It’s time to [buy/sell] stocks.” Who is this advice for? A 20-year-old with 60 years of investing in front of him, or a 82-year-old widow who needs money for a nursing home? Doesn’t that make a difference?

“We’re neutral on this stock.” Stop it. You don’t deserve a paycheck for that.

“There’s minimal downside on this stock.” Some lessons have to be learned the hard way.

“We’re trying to maximize returns and minimize risks.” Unlike everyone else, who are just dying to set their money ablaze!

“Shares fell after the company lowered guidance.” Guys, they just proved their guidance can be wrong. Why are you taking this new one seriously?

“Our bullish case is conservative.” Then it’s not a bullish case. It’s a conservative case. Those words mean opposite things.

“We look where others don’t.” This is said by so many investors that it has to be untrue most of the time.

“Is [X] the next black swan?” Nassim Taleb’s blood pressure rises every time someone says this. You can’t predict black swans. That’s what makes them dangerous.

“We’re waiting for more certainty.” Good call. Like in 1929, 1999 and 2007, when everyone knew exactly what the future looked like. Can’t wait!

“The Dow is down 50 points as investors react to news of [X].” Stop it – you’re just making stuff up. “Stocks are down and no one knows why” is the only honest headline in this category.

“Investment guru [insert name] says stocks are [insert forecast].” Go to Morningstar.com. Look up that guru’s track record against their benchmark. More often than not, their career performance lags an index fund. Stop calling them gurus.

“We’re constructive on the market.” I have no idea what that means. I don’t think you do, either.

“[Noun] [verb] bubble.” (That’s a sarcastic observation from investor Eddy Elfenbein.)

“Investors are fleeing the market.” Every stock is owned by someone all the time.

“We expect more volatility.” There has never been a time when this was not the case. Let me guess, you also expect more winters?

“This is a strong buy.” What do I do with this? Click the mouse harder when placing the order in my brokerage account?

“He was tired of throwing his money away renting, so he bought a house.” He knows a mortgage is renting money from a bank, right?

“This is a cyclical bull market in a secular bear.” Vapid nonsense.

“Will Obamacare ruin the economy?” No. And get a grip.

So, don’t let these aphorisms blind you to the critical thinking skills you learned in college, honed in medical school and apply every day in life.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

US stocks plunged on Monday as investors processed growing concerns about the health of the US economy after President Trump and his top economic officials acknowledged the possibility of a potential rough patch.

The Dow Jones Industrial Average (^DJI) fell nearly 900 points, or over 2%, while the benchmark S&P 500 (^GSPC) dropped around 2.7% after the index posted its worst week since September. The tech-heavy NASDAQ Composite (^IXIC) fell 4% in its worst day since 2022, as the “Magnificent Seven” stocks led the sell-off. Tesla’s (TSLA) rout continued, plunging 15% and officially wiping out the gains it had made in the wake of Trump’s election win. Nvidia (NVDA), Apple (AAPL), Google parent Alphabet (GOOG), and Meta (META) all each lost more than 4%.

Key inflation data includes the Consumer Price Index (CPI) and Producer Price Index (PPI) on Wednesday and Thursday could help set the tone, though economic growth concerns seem to have replaced inflation as the prime concern. The S&P 500 index (SPX) dropped more than 3% last week, the worst performance since September.

However, the U.S. economy “is in a good place” despite recent policy uncertainty, Federal Reserve Chairman Jerome Powell said Friday. He sees no need to hurry rate cuts until there’s more policy clarity, Bloomberg reported. Stocks rallied on Powell’s words late Friday, but Monday’s early action indicates that rallies continue being sold, and the Cboe Volatility Index (VIX) rose above 26 as investors piled into risk-off assets like bonds. The 200-day moving average of 5,734 for the SPX remains a key technical support area, and the SPX was on pace to open below that Monday, now more than 6% off of all-time highs but not yet in –10% correction territory.

I was having lunch with a close friend of mine. He mentioned that he had accumulated a significant sum of money and did not know what to do with it. It was sitting in bonds, and inflation was eating its purchasing power at a very rapid rate.

He is a dentist and had originally thought about expanding his business, but a shortage of labor and surging wages turned expanding into a risky and low-return investment. He complained that the stock market was extremely expensive. I agreed.*

He said that the only thing left was residential real estate. I pushed back. “What do you think will happen to the affordability of houses if – and most likely when – interest rates go up? Inflation is now 6%. I don’t know where it will be in a year or two, but what if it becomes a staple of the economy? Interest rates will not be where they are today. Even at 5% interest rates [I know, a number unimaginable today] houses become unaffordable to a significant portion of the population. Yes, borrowers’ incomes will be higher in nominal terms, but the impact of the doubling of interest rates on the cost of mortgages will be devastating to affordability.”

He rejoined, “But look at what happened to housing over the last twenty years. Housing prices have consistently increased, even despite the financial crisis.”

I agreed, but I qualified his statement: “Over the past twenty, actually thirty, years interest rates declined. I honestly don’t know where interest rates will be in the future. But probabilistically, knowing what we know now, the chances that they are going to be higher, much higher, are more likely than their staying low. Especially if you think that inflation will persist.”

We quickly shifted our conversation toward more meaningful topics, like kids.

It seems that every year I think we have finally reached the peak of crazy, only to be proven wrong the next year. The stock market and thus index funds, just like real estate, have only gone one way – up. Index funds became the blunt instrument of choice in an always-rising market. So far, this choice has paid off nicely.

The market is the most expensive it has ever been, and thus future returns of the market and index funds will be unexciting. (I am being gentle here.)

You don’t have to be a stock market junkie to notice the pervasive feeling of euphoria. But euphoria is a temporary, not a permanent emotion; and at least when it comes to the stock market, it is usually supplanted by despair. Market appreciation that was driven by expanding valuations was not a gift but a loan – the type of loan that must always be paid back with a high rate of interest.

I don’t know what straw will break the feeble back of this market or what will cause the music to stop (there, you got two analogies for the price of none). We are in an environment where there are very few good options. If you do nothing, your savings will be eaten away by inflation. If you do something, you find that most assets, including the stock market as a whole, are incredibly overvalued.

We are doing the only sensible thing that you can do today. We spend very little time thinking about straws or what will cause the music to stop or how overvalued the market is. We are focusing all our energy on patiently building a portfolio of high-quality, cash-generative, significantly undervalued businesses that have pricing power.

This has admittedly been less rewarding than taking risky bets on unimaginably expensive assets. It may lack the excitement of sinking money into the darlings you see in the news every day, but we hope that our stocks will look like rare gems when the euphoria condenses into despair. As we keep repeating in every letter, the market is insanely overvalued. Our portfolio is anything but – we don’t own “the market”.

*A question may arise:Why did I not tell my dentist friend to pick individual stocks? He runs a busy dental practice and wouldn’t have the time or the training to pick stocks.

Why didn’t I offer him our services? IMA manages all my and my family’s liquid assets, but I have a rule that I never (ever!) break – I don’t manage my friends’ money. I’ll help them as much as possible with free advice but will never have a professional relationship with them. I intentionally create a separation between my personal and professional lives. After a difficult day in the market, I want to be able to go for beers with friends and leave the market at the office.

Also, this simplifies my relationships with my friends. There is no ambiguity in our friendship.

You can also listen to a professional narration of this article on iTunes & online.

ENCORE: March 22, 2004

A basic property of religion is that the believer takes a leap of faith: to believe without expecting proof. Often you find this property of religion in other, unexpected places – for example, in the stock market. It takes a while for a company to develop a “religious” following: only a few high-quality, well-respected companies with long track records ever become worshipped by millions of investors. My partner, Michael Conn, calls these “religion stocks.” The stock has to make a lot of shareholders happy for a long period of time to form this psychological link.

The stories (which are often true) of relatives or friends buying few hundred shares of the company and becoming millionaires have to fester a while for a stock to become a religion. Little by little, the past success of the company turns into an absolute – and eternal – truth. Investors’ belief becomes set: the past success paints a clear picture of the future.

Gradually, investors turn from cautious shareholders into loud cheerleaders. Management is praised as visionary. The stock becomes a one-decision stock: buy. This euphoria is not created overnight. It takes a long time to build it, and a lot of healthy pessimists have to become converted into believers before a stock becomes a “religion.”

Once a stock is lifted up to “religion” status, beware: Logic is out the window. Analysts start using T-bills to discount the company’s cash flows in order to justify extraordinary valuations. Why, they ask, would you use any other discount rate if there is no risk? When a T-bill doesn’t do the trick, suddenly new and “more appropriate” valuation metrics are discovered.

Other investors don’t even try to justify the valuation – the stock did well for me in the past, why would it stop working in the future? Faith has taken over the stock. Fundamentals became a casualty of “stock religion.” These stocks are widely held. The common perception is that they are not risky.

The general public loves these companies because they can relate to the companies’ brands. A dying husband would tell his wife, “Never sell _______ (fill in the blank with the company name).” Whenever a problem surfaces at a “religion stock,” it is brushed away with the comment that “it’s not like the company is going to go out of business.” True, a “religion stock” company is a solid leader in almost every market segment where it competes and the company’s products carry a strong brand name. However, one should always remember to distinguish between good companies and good stocks.

Coca-Cola is a classic example of a “religion stock.” There are very few companies that have delivered such consistent performance for so long and have such a strong international brand name as Coca-Cola. It is hard not to admire the company.

But admiration of Coca-Cola achieved an unbelievable level in the late nineties. In the ten years leading up to 1999, Coca-Cola grew earnings at 14.5% a year, very impressive for a 103-year-old company. It had very little debt, great cash flow and a top-tier management. This admiration came at a steep price: Coca-Cola commanded a P/E of 47.5. That P/E was 2.7 times the market P/E. Even after T-bills could no longer justify Coke’s valuation, analysts started to price “hidden” assets – Coke’s worldwide brand. No money manager ever got fired for owning Coca-Cola.

The company may not have had a lot of business risk. But in 1999, the high valuation was pricing in expectations that were impossible for any mature company to meet. “The future ain’t what it used to be” – Yogi Berra never lets us down. Success over a prolonged period of time brings a problem to any company – the law of large numbers.

Enormous domestic and international market share, combined with maturity of the soft drink market, has made it very difficult for Coca-Cola to grow earnings and sales at rates comparable to the pre-1999 years. In the past five years, earnings and sales have grown 2.5% and 1.5% respectively. After Roberto C. Goizueta’s death, Coke struggled to find a good replacement – which it acutely needed.

Old age and arthritis eventually catch up with “religion stocks.” No company can grow at a fast pace forever. Growth in earnings and sales eventually decelerates. That leads to a gradual deflation of the “religion” premium. For Coke, the descent from its “religious” status resulted in a drop of nearly 20% in the share price – versus an increase of 65% in the broad market over the same time. And at current prices, the stock still is not cheap by any means. It trades at 25 times December 2004 earnings, despite expectations for sales growth in the mid single digits and EPS growth in the low double digits.

It takes a while for the religion premium to be totally deflated because faith is a very strong emotion. A lot of frustration with sub-par performance has to come to the surface.

Disappointment chips away at faith one day at a time. “Religion” stocks are not safe stocks. The leap of faith and perception of safety come at a large cost: the hidden risk of reduction in the “religion premium.” The risk is hidden because it never showed itself in the past. “Religion” stocks by definition have had an incredibly consistent track record. Risk was rarely observed.

However, this hidden risk is unique because it is not a question of if it will show up but a question of when. It is very hard to predict how far the premium will inflate before it deflates – but it will deflate eventually. When it does, the damage to the portfolio can be huge.

Religion stocks generally have a disproportionate weight in portfolios because they are never sold – exposing the trying-to-be-cautious investor to even greater risks. Coca-Cola is not alone in this exclusive club. General Electric, Gillette, Berkshire Hathaway are all proud members of the “religion stock” club as well. Past members would include: Polaroid – bankrupt; Eastman Kodak – in a major restructuring; AT&T – struggling to keep its head above water. That stock is down from over $80 in 1999 to $18 today.

Emotions have no place in investing. Faith, love, hate, and disgust should be left for other aspects of our life. More often than not, emotions guide us to do the opposite of what we need to do to be successful. Investors need to be agnostic towards “religion stocks.” The comfort and false sense of certainty that those stocks bring to the portfolio come at a huge cost: prolonged under performance.

My thoughts today (20+ years later)

This is one of the first investment articles I ever wrote. I had just started writing for TheStreet.com. It’s interesting to read this article more than 20 years later. I am surprised my writing was not as bad as I had feared (though in many cases it was worse than I feared when I read my other early articles).

So much has happened since then – I am a different person today than I was back then. I have two more kids; I have written three more books and a thousand articles. The last two decades were my formative years as an investor and adult.

The goal of the article was not to make predictions but to warn readers that the long-term success of certain companies creates a cult-like following and deforms thinking. In fact, my original article – the one I submitted to TheStreet.com – did not mention any companies other than Coke. The editors wanted me to include more names so that the article would show up on more pages of Yahoo! Finance.

With the exception of Berkshire Hathaway, all of these companies have produced mediocre or horrible returns. In the best case, their fundamental returns in their old age were only a fraction of what they were when these companies were younger and the world was their oyster.

To my surprise, Coke’s stock is still trading at a high valuation. Its business has performed like the old-timer it is, with revenue and earnings growing by only 3–4% a year. The days of double-digit revenue and earnings growth were left in the 80s and 90s, though the high valuation remained.

Posted on March 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

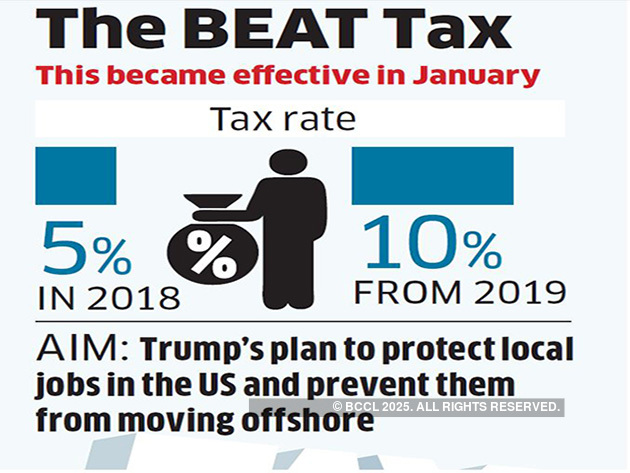

Base-Erosion Anti-Abuse Tax (BEAT): The 2017 tax reforms moved the U.S. from a worldwide taxation system to a quasi-territorial system, so foreign earnings are no longer included in a company’s domestic tax base.

To discourage companies operating in the U.S. from avoiding tax liability by shifting profits out of the country, Congress imposed a 10% minimum tax called Base-Erosion Anti-Abuse Tax (BEAT). The BEAT rate will increase from 10% to 12.5% in 2026.