BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

When you buy a share of stock, you are taking ownership in a company. Collectively, the company is owned by all the shareholders, and each share represents a claim on assets and earnings. If the company distributes profits to its shareholders, you should receive a proportionate share of the earnings.

Stocks are often categorized by the size of the company, or their market capitalization. The market capitalization is determined by multiplying the number of outstanding shares by the current share price. The most common market cap classes are small-cap (valued from $100 million to $1 billion), mid-cap ($1 billion to $10 billion), and large cap ($10 billion to $100 billion).

Stocks are also categorized by their sector, or the type of business the company conducts. Common sectors include utilities, consumer staples, energy, communications, financial, health care, transportation, and technology.

***

***

Stocks are often viewed as being in one of two categories — growth or value.

Growth stocks are ones that are associated with high quality, successful companies that are expected to continue growing at a better-than-average rate as compared to the rest of the market.

Value stocks are ones that have generally solid fundamentals, but are currently out of favor with the market. This may be due to the company being relatively new and unproven in the market, or because the company has recently experienced a decline due to the company’s sector being affected negatively. An example of this would be if the federal government was to levy a new tax on all cell phones, thus negatively affecting all cell phone company stocks.

History has shown that, over time, stocks have provided a better return than bonds, real estate, and other savings vehicles. As a result, stocks may be the ideal investment for investors with long-term goals.

Posted on April 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

U.S. stock and bond markets will be closed on Good Friday. Many global markets will also be closed Friday. Exceptions include Japan and mainland China, which will be open as usual. U.S. markets will reopen Monday. Many international markets will remain shut to mark Easter Monday, including Australia, Hong Kong, and exchanges in France, Germany and the U.K.

***

YESTERDAY 4/17/25

***

🟢 What’s up

TSMC eked out a 0.10% gain after the semiconductor maker reported a 60% increase in profits last quarter and downplayed the effects of tariffs.

Charles Schwab isn’t just the guy who made $2 billion from market chaos last week. It’s also the brokerage that reported record quarterly revenue, but shares only rose 0.65%.

Hertz climbed another 43.87%, tacking on another day of big wins after Bill Ackman’s Pershing Square Capital took a stake in the rental car company.

Trump Media & Technology Group popped 11.65% after the company asked the SEC to investigate a hedge fund with a $105 million short bet against it.

Chinese tea chain Chagee soared 15.86% in its first day of trading on the Nasdaq.

DR Horton missed analyst expectations last quarter and lowered its fiscal year guidance, but investors quickly forgave the country’s largest homebuilder and pushed shares up 3.16%.

What’s down

Alphabet took a 1.38% hit after a federal judge ruled that Google is a monopoly. This marks Alphabet’s second antitrust loss since last August.

Alcoa fell 6.98% after the aluminum mining behemoth announced it ate about $20 million in tariff-related costs last quarter, noting that this figure could rise to $90 million in the current quarter.

Abbott Laboratories gained 2.77% after the pharma company missed sales estimates but still beat earnings forecasts.

Gold miners continue to climb as gold keeps hitting new highs. Newmont rose 2.51%, while Gold Fields gained 3.35%.

What’s down

Tesla sank 4.94% after the company’s share of EV sales in California fell below 50% in the first quarter, while export controls threaten plans to produce Cybercabs in the US.

United Airlines fell 0.01% despite reporting its “best first-quarter financial results in five years,” according to management. The airline took the unique measure of providing two different financial outlooks for the year ahead: one for a stable economy, and one for a recession.

Lyft shed just 0.46% on the news that the ride-hailing company is acquiring European taxi app Free Now for $199 million.

Interactive BrokersGroup reported a 47% increase in trading volume last quarter that helped it beat revenue expectations, but the brokerage still tumbled 8.95% after missing profit forecasts.

Palantir gave up some of its recent gains following its big NATO announcement, sinking 5.78% today as investors collected profits.

JB HuntTransport Services’ management team warned that the logistics company sits squarely in the crosshairs of the trade war, pushing shares down 7.68%.

Omnicom Group tumbled 7.28% after the advertising firm missed revenue estimates thanks to economic uncertainty.

Posted on April 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Investors were apparently tired of all the volatility yesterday, leading to a relatively calm day where indexes ever-so-slightly slipped. But it was a big day for Netflix after the Wall Street Journal reported that the streaming giant has plans to double its revenue and reach a $1 trillion valuation by 2030.

***

🟢 What’s up

Hewlett Packard Enterprise popped 5.11% after Elliott Investment Management took a $1.5 billion stake in the tech company.

Rocket Lab rocketed (sorry) 10.14% higher after the space stock inked deals with both the US Air Force and the UK Ministry of Defense.

Netflix rose 4.83% on a report from the Wall Street Journal that the streaming giant plans to hit a $1 trillion market capitalization and double its revenue by 2030. The company announces earnings on Thursday.

Bank of America and Citigroup both posted strong Q1 earnings that beat analyst forecasts (more on that below). BofA climbed 3.60%, while Citi rose 1.76%.

Albertsons tumbled 7.49% after the grocer’s full-year guidance came in below expectations.

Allegro Microsystems sank 9.68% on the news that ON Semiconductor has withdrawn its offer to acquire the chipmaker.

Applied Digital plummeted 35.94% after the digital infrastructure company missed analyst revenue estimates, despite sales climbing 22% last quarter.

#recessionindicator: Coty sank 8.57% after the beauty retailer was double downgraded by Bank of America analysts, citing a slowdown in makeup spending.

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

WARNING – WARNING

By Staff Reporters

***

***

A “retirement account scam” is a type of online fraud that occurs when a third party administrator (TPA) for retirement investment accounts is tricked into authorizing a money distribution to an imposter posing as the true account holder.

The imposter often starts the scam by calling the TPA, identifying himself or herself as an actual account holder, and requesting a withdrawal distribution form. Once the imposter receives the withdrawal distribution form, the imposter returns the completed form to the TPA. The form is completed with the account holder’s real personal identifying information (PII)—often stolen via schemes, data breaches, and other hacking offenses—and bank account information for an account controlled by the imposter or the imposter’s conspirators.

***

***

After the TPA processes the fraudulent request, the request is forwarded to the investment firm responsible for managing the account holder’s investments, and the funds—often the account holder’s life savings—are then directed to the imposter’s designated bank account.

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Natural Disaster Insurance

Protecting accumulated assets by insuring them against the wrath of Mother Nature

Most homeowners’ insurance policies do not cover damages arising from floods or earthquakes. If a home, or any other real property like a vacation home or beach condo, is in an area subject to floods or earthquakes, consider the value of purchasing insurance that covers such catastrophes.

Take the time to review your homeowners’ policy, making sure that it will repair or replace your roof if damaged by hail, and will apply in the event of high winds, rather than only in tornadoes. The key to the maintenance of any type of insurance is to anticipate all of the possible calamities, and then to decide whether you can afford to lose the assets exposed to those calamities.

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Stocks kept the good vibes going for a second trading day yesterday with tech companies like Apple rising as investors reacted to the weekend’s news that smartphones and computers would be temporarily exempt from “reciprocal” tariffs—at least until new semiconductor tariffs are imposed.

Car companies also jumped after President Trump suggested he wanted to “help” as automakers try to transition their production to the US in the face of 25% auto tariffs.

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

A recent study published in the Annals of Internal Medicine found that in 2021, UnitedHealth Group received just under $14 billion in extra Medicare Advantage payments after using a code that made its members appear sicker. It’s another tough break for the plan and provider that has faced allegations of illegally taking additional money from patients and taxpayers, especially after its CEO was fatally shot in early December.

US stocks edged higher on Monday as investors focused on tech’s temporary reprieve from President Trump’s tariffs.

The S&P 500 (^GSPC) trimmed bigger gains to rise a healthy 0.8%. The tech-heavy NASDAQ (^IXIC) also closed off its session high, up 0.6%. The Dow Jones Industrial Average (^DJI) was up around 0.7%, or more than 300 points.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

🟢 What’s up

Auto stocks soared on comments from President Trump that car companies “need a little bit of time.” GM rose 3.48%, Ford climbed 4.13%, and Stellantis gained 5.64%.

Investors are bullish: WeBull exploded 374.72% after the online investment platform went public via SPAC merger last Friday.

Goldman Sachs rose 1.87% after the Wall Street titan announced record revenue in its equities-trading business thanks to stock market volatility in the first quarter.

Palantir gained 4.60% after it sealed a deal with NATO to provide the organization with its advanced AI-powered warfighting system.

Intel climbed 2.89% on news that it will sell a 51% stake in its programmable chips unit Altera to Silver Lake Management.

Pfizer somehow rose 0.96% despite announcing that it is discontinuing the development of a once-daily weight-loss pill after a patient experienced a liver injury. That’s great news for Viking Therapeutics, which has its own oral weight-loss pill in the pipeline. Shares of Viking rose 10.58%.

Speaking of biotech stocks, Verve Therapeutics soared 26.38% after the company reported no issues with patients trialing its new gene-editing technology.

What’s down

Meta Platforms fell 2.22% as its antitrust trial began today. If it loses its case against the FTC, it may be forced to sell off Instagram.

DaVita sank 3.03% after the kidney disease treatment company announced it was the victim of a ransomware attack.

Hilton Worldwide Holdings fell 1.10% on a downgrade from Goldman Sachs analysts, who believe the vacation club company will struggle as fewer people splurge on travel. Marriott International received the same treatment, and also dropped 0.77%.

LVMH Moet Hennessy Louis Vuitton (really rolls off the tongue) tumbled 6.39% after the luxury goods retailer missed analyst expectations, reporting a 3% decline in sales compared to forecasts of 2% growth.

It’s a bit broad, but Citi analysts downgraded all US stocks to “neutral” this morning. The analysts argued that US stocks are too exposed to President Trump’s policies and are expensive compared to international peers, and endorsed investing in Japanese, European, and UK equities instead.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

US Markets

After one of the most volatile weeks in Wall Street history, the S&P 500 closed 5.7% higher for its best week since 2023. But investors are taking little comfort with the rebound in stocks.

A declining dollar fell to a three-year low against the euro on Friday and spiking bond yields have some observers warning of a monumental, structural shift away from the US as a safe haven due to the recent tariff turmoil.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Beneficiary designations can provide a relatively easy way to transfer an account or insurance policy upon your death. However, if you’re not careful, missing or outdated beneficiary designations can easily cause your estate plan to go awry.

Where you can find them

Here’s a sampling of where you’ll find beneficiary designations:

In several states, so-called “lady bird” deeds for real estate

***

***

10 tips about beneficiary designations

Because beneficiary designations are so important, keep these things in mind in your estate planning:

Remember to name beneficiaries. If you don’t name a beneficiary, one of the following could occur:

The account or policy may have to go through probate. This process often results in unnecessary delays, additional costs, and unfavorable income tax treatment.

The agreement that controls the account or policy may provide for “default” beneficiaries. This could be helpful, but it’s possible the default beneficiaries may not be whom you intended.

Name both primary and contingent beneficiaries. It’s a good practice to name a “back up” or contingent beneficiary in case the primary beneficiary dies before you. Depending on your situation, you may have only a primary beneficiary. In that case, consider whether it may make sense to name a charity (or charities) as the contingent beneficiary.

Update for life events. Review your beneficiary designations regularly and update them as needed based on major life events, such as births, deaths, marriages, and divorces.

Read the instructions. Beneficiary designation forms are not all alike. Don’t just fill in names — be sure to read the form carefully. If necessary, you can draft your own customized beneficiary designation, but you should do this only with the guidance of an experienced attorney or tax advisor.

Coordinate with your will and trust. Whenever you change your will or trust, be sure to talk with your attorney about your beneficiary designations. Because these designations operate independently of your other estate planning documents, it’s important to understand how the different parts of your plan work as a whole.

Think twice before naming individual beneficiaries for particular assets. For example, you may establish three accounts of equal value initially and name a different child as beneficiary of each account. Over the years, the accounts may grow or be depleted unevenly, so the three children end up receiving different amounts — which is not what you originally intended.

Avoid naming your estate as beneficiary. If you designate a beneficiary on your 401(k), for example, it won’t have to go through probate court to be distributed to the beneficiary. If you name your estate as beneficiary, the account will have to go through probate. For IRAs and qualified retirement plans, there may also be unfavorable income tax consequences.

Use caution when naming a trust as beneficiary. Consult your attorney or CPA before naming a trust as beneficiary for IRAs, qualified retirement plans, or annuities. There are situations where it makes sense to name a trust — for example if:

Your beneficiaries are minor children

You’re in a second marriage

You want to control access to funds

Be aware of tax consequences. Many assets that transfer by beneficiary designation come with special tax consequences. It’s helpful to work with an experienced tax advisor to help provide planning ideas for your particular situation.

Use disclaimers when necessary — but be careful. Sometimes a beneficiary may actually want to decline (disclaim) assets on which they’re designated as beneficiary. Keep in mind that disclaimers involve complex legal and tax issues and require careful consultation with your attorney and CPA.

Posted on April 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

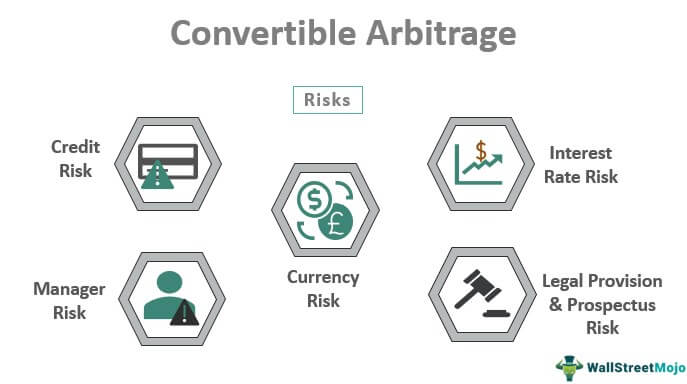

Convertible Arbitrage

Convertible arbitrage is the oldest market-neutral strategy. Designed to capitalize on the relative mispricing between a convertible security (e.g. convertible bond or preferred stock) and the underlying equity, convertible arbitrage was employed as early as the 1950s.

Since then, convertible arbitrage has evolved into a sophisticated, model-intensive strategy, designed to capture the difference between the income earned by a convertible security (which is held long) and the dividend of the underlying stock (which is sold short). The resulting net positive income of the hedged position is independent of any market fluctuations. The trick is to assemble a portfolio wherein the long and short positions, responding to equity fluctuations, interest rate shifts, credit spreads and other market events offset each other.

***

***

Hedge Fund Research (HFR) New York, offers the following description of the strategy

Convertible Arbitrage involves taking long positions in convertible securities and hedging those positions by selling short the underlying common stock. A manager will, in an effort to capitalize on relative pricing inefficiencies, purchase long positions in convertible securities, generally convertible bonds, convertible preferred stock or warrants, and hedge a portion of the equity risk by selling short the underlying common stock. Timing may be linked to a specific event relative to the underlying company, or a belief that a relative mispricing exists between the corresponding securities. Convertible securities and warrants are priced as a function of the price of the underlying stock, expected future volatility of returns, risk free interest rates, call provisions, supply and demand for specific issues and, in the case of convertible bonds, the issue-specific corporate/Treasury yield spread. Thus, there is ample room for relative mis-valuations.

Because a large part of this strategy’s gain is generated by cash flow, it is a relatively low-risk strategy.

Posted on April 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Credit Card Mistakes to Avoid

No number has as far-reaching an impact on your money as your credit scores. Here are some credit card obstacles all physicians, nurses and medical professionals should dodge on the road to financial security

The vast majority of physicians and medical professionals major in one of the hard science while in college; biology, engineering, chemistry, mathematics, computer science or physics; etc. Few take undergraduate courses in finance, business management, securities analysis, accounting or economics; although this paradigm is changing with modernity. These course are not particularly difficult for the pre-medical baccalaureate major, they are just not on the radar screen for time compressed and highly competitive students; nor are they needed for medical or nursing school admission, or the many related allied health professional schools.

In fact, William C. Roberts MD, originally from Emory University in Atlanta, and former editor for the Baylor University Medical Center Proceedings and The American Journal of Cardiology, opined just a decade ago:

“Of the 125 medical schools in the USA, only one of them to my knowledge offers a class related to saving or investing money.”

And so, it is important to review some basic principles of economics, finance and accounting as they relate to financial planning in thees two textbooks; and this ME-P.

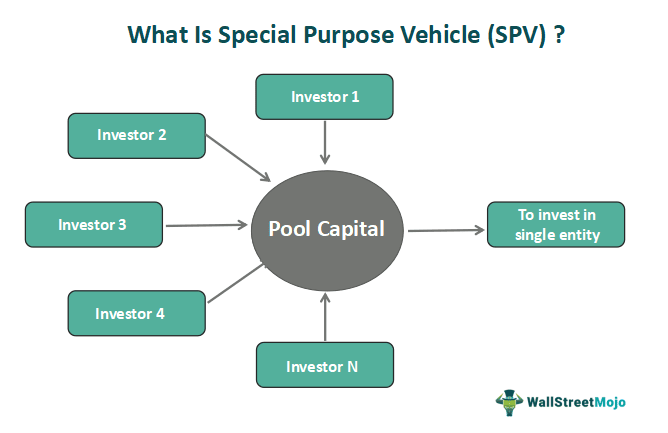

Its purpose is to isolate the parent company from any potential credit or financial risk that may arise from the SPV and is often used to pursue riskier projects, securitize debt, or transfer assets. Since an SPV is separate from the parent company, it isn’t affected by the parent’s performance, and the parent isn’t typically affected by the performance of the SPV. If the parent goes bankrupt and is no longer in existence, the SPV can carry on.

This makes an SPV bankruptcy remote. This also means that the parent company is unaffected by the loss if the SPV fails.

Posted on April 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

THE “FIVE-FIVE” FINANCIAL RULE

By Staff Reporters

***

***

Many of the pros of home ownership will appeal to medical retirees for whom their home is their castle and who appreciate being settled both financially and geographically:

1. Building equity in your home: Each mortgage payment you make brings you closer to owning your house free and clear with no payments. If you can buy a new home or condo outright by selling your current home, you can still build equity in your new home over time.

2. Predictability: If you have a fixed-rate mortgage, your mortgage payments will remain consistent for years and you don’t have to worry about a landlord ever making you move.

3. Tax benefits: You can deduct mortgage interest and property taxes up to certain limits.

4. Customization: You don’t need a landlord’s permission to alter and improve your home.

5. Home appreciation: Homes generally increase in value, so you can increase your net worth by owning a property.

***

***

Renting also has five significant upsides, particularly for physician retirees who want greater freedom to travel and to make bigger moves — potentially across the country or even abroad:

1. Extreme flexibility: You can leave your property after giving notice and go wherever you want much more easily than with an illiquid home you’d have to sell first.

2. Lower upfront costs: You only have to pay first and last month’s rent and a security deposit to move into a rental, not make a large home down payment.

3. No maintenance concerns: If something breaks, your landlord is responsible for the cost of fixing it and the actual repairs. You don’t have to build up an emergency fund for maintenance.

4. Predictable expenses: For the duration of your lease, your monthly housing costs including utilities will remain consistent, even if the cost of energy goes up, for example.

5. Lack of worry: If you’re in a rental apartment, you won’t have to concern yourself with shoveling snow, mowing grass or other matters of upkeep.

Posted on April 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

US stocks turned higher on Friday to cap a chaotic week on Wall Street, as investors weighed the latest tariff-related developments in the trade war between the US and China.

The S&P 500 (^GSPC) rose 1.8% after seesawing earlier in the session. The tech-heavy NASDAQ Composite (^IXIC) climbed 2.1%. The Dow Jones Industrial Average (^DJI) advanced 1.5%, about 600 points.

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

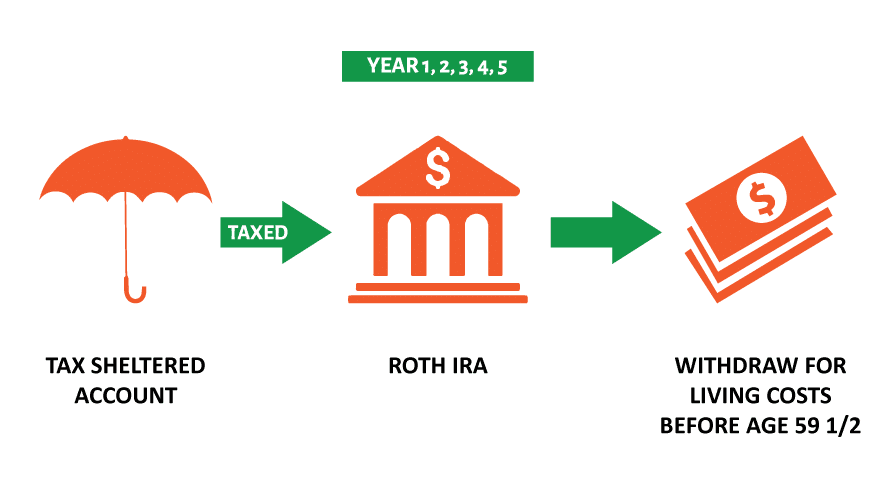

Why would a doctor consider a Roth IRA conversion?

By Staff Reporters

***

***

A Roth conversion involves transferring funds from a traditional retirement account—such as a 401(k), 403(b), or individual retirement account (IRA) funded with pre-tax dollars—into a Roth IRA.

The biggest benefit lies in the tax treatment of the converted funds. Once the funds are in the Roth IRA, future growth of those assets is tax-free. Withdrawals in retirement are also tax-free, assuming they meet certain criteria. As with any strategy, there are important considerations to keep in mind.

When you convert funds to a Roth IRA, the amount converted is taxable income in that tax year. For example, if you convert $100,000 from a traditional IRA to a Roth IRA, that $100,000 will be added to your taxable income in the conversion year.

Converting large amounts can result in a significant tax bill and may push you into a higher tax bracket. Even so, using retirement funds to pay taxes may make sense for those looking to convert large IRAs to reduce their future required minimum distributions (RMDs).

The timing of your Roth conversion matters too. Generally, it’s a good idea to convert when your income is lower—for example, after you’ve retired and before you begin drawing Social Security. You may also choose to convert over the course of several years to spread out the tax impacts. But if you can get comfortable with these considerations, a Roth conversion can provide you with benefits beyond tax-free growth and withdrawals.

Some of these benefits are:

Tax diversification. Having both traditional and Roth accounts allows you to manage your tax liability in retirement. For example, if your income in a given year is higher than expected, you can withdraw from the Roth IRA without increasing your taxable income.

No RMDs. Traditional IRAs and 401(k)s require you to begin taking RMDs at age 73. Roth IRAs have no RMD requirement during your lifetime. With a Roth account, you have more control over your retirement withdrawals and can leave the funds to grow for your heirs.

Benefits for heirs. Roth IRAs can be passed on to beneficiaries, who can inherit the account income tax-free. This means your heirs can enjoy the tax-free growth and withdrawals if the Roth IRA has been held for five years or more—a significant advantage, especially if your beneficiaries are in a higher tax bracket.

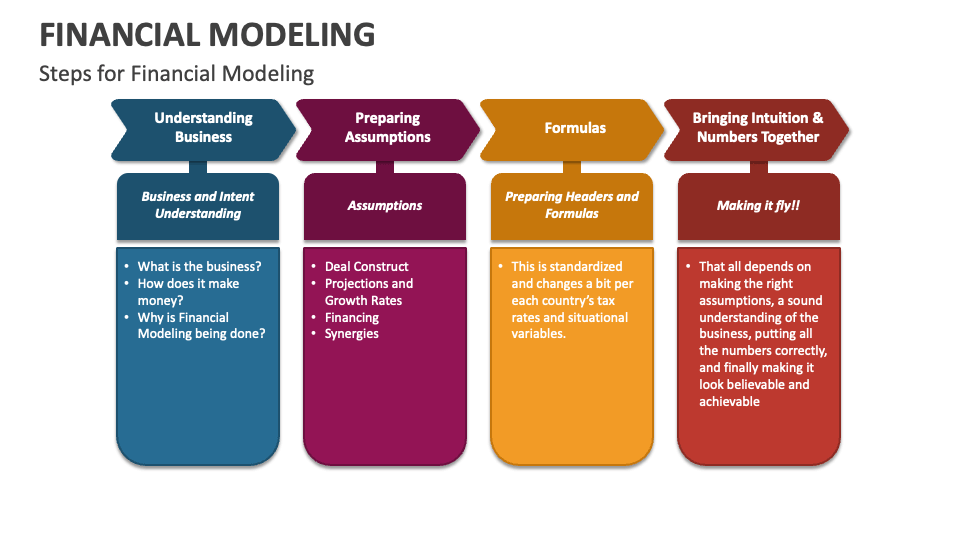

Financial Modeling is one of the most highly valued, but thinly understood, skills in financial analysis. The objective of financial modeling is to combine accounting, finance, and business metrics to create a forecast of a company’s future results.

According to Jeff Schmidt, a financial model is simply a spreadsheet, usually built in Microsoft Excel, that forecasts a business’s financial performance into the future. The forecast is typically based on the company’s historical performance and assumptions about the future and requires preparing an income statement, balance sheet, cash flow statement, and supporting schedules (known as a three-statement model, one of many types of approaches to financial statement modeling). From there, more advanced types of models can be built such as discounted cash flow analysis (DCF model), leveraged buyout (LBO), mergers and acquisitions (M&A), and sensitivity analysis

***

DEFINED TERMS

Discounted Cash Flow (DCF): A valuation method used to estimate the value of an investment based on its expected future cash flows, adjusted for the time value of money. It’s like deciding whether a treasure chest is worth diving for now, based on the gold coins you’ll be able to cash in later.

Sensitivity Analysis: This involves changing one variable at a time to see how it affects an outcome. Imagine tweaking your coffee-to-water ratio each morning to achieve the perfect brew strength.

Budget – A budget is the amount of money a department, function, or business can spend in a given period of time. Usually, but not always, finance does this annually for the upcoming year.

Rolling Forecast – A rolling forecast maintains a consistent view over a period of time (often 12 months). When one period closes, finance adds one more period to the forecast.

Topside – A topside adjustment is an overlay to a forecast. This is typically completed by the corporate or headquarter team. As individual teams submit a forecast, the consolidated result might not make sense or align with expectations. When this occurs, the high-level teams use a topside adjustment to streamline or adjust the consolidated view.

Monte Carlo Simulation: Picture yourself at the casino, but instead of gambling your savings away, you’re using this technique to predict different outcomes of your business decisions based on random variables. It’s like playing financial roulette with the odds in your favor.

What-If Analysis: Ever daydream about what would happen if you took that leap of faith with your business? This tool allows you to explore various scenarios without risking a dime. It’s like trying on outfits in a virtual dressing room before making a purchase.

Leveraged Buyout (LBO) Model: This is a bit like orchestrating a heist, but legally. It’s about acquiring a company using borrowed money, with plans to pay off the debts with the company’s own cash flows. High stakes, high rewards.

Mergers and Acquisitions (M&A) Model: Picture two puzzle pieces coming together. This model evaluates how combining companies can create a new, more valuable entity. It’s the corporate version of a matchmaker.

Three Statement Model: The holy trinity of financial modeling, linking the income statement, balance sheet, and cash flow statement. It’s like weaving a tapestry where each thread is crucial to the overall picture.

Capital Asset Pricing Model (CAPM): A formula that calculates the expected return on an investment, considering its risk compared to the market. It’s like choosing the best roller coaster in the park, balancing thrill and safety.

Cash Flow Forecasting: This is your financial weather forecast, predicting the cash flow climate of your business. It helps you plan for sunny days and save for the rainy ones.

Cost of Capital: The price of financing your business, whether through debt or equity. It’s like the interest rate on your growth engine, pushing you to maximize every dollar invested.

Debt Schedule: A timeline of your business’s debts, showing when and how much you owe. It’s your roadmap to becoming debt-free, one milestone at a time.

Equity Valuation: Determining the value of a company’s shares. It’s like assessing the worth of a rare gemstone, ensuring investors pay a fair price for a piece of the treasure.

Financial Leverage: Using debt to amplify returns on investment. It’s like using a lever to lift a heavy object, increasing force but also risk.

Forecast Model: A crystal ball for your finances, projecting future performance based on past and present data. It’s your guide through the financial wilderness, helping you navigate with confidence.

Operating Model: A detailed blueprint of how a business generates value, mapping out operational activities and their financial impact. It’s like laying out the inner workings of a clock, ensuring every gear turns smoothly.

Revenue Growth Model: This tracks potential increases in sales over time, charting a course for expansion. It’s like plotting your ascent up a mountain, anticipating the effort required to reach the summit.

Posted on April 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Treasury notes are typically considered one of the world’s safest safe-haven assets—the US has always repaid bondholders on their investment, plus yield (interest). That’s why you can usually count on the bond market to rally when the stock market craters. And, vice-versa. But not this time:

The benchmark 10-year bond yield, which moves inversely to bond prices, had its steepest spike this week since the 2008 financial crisis. The 10-year yield is more closely watched than the 30-year yield (which also spiked) in part because it influences home and auto loan rates.

A Treasury auction of 3-year bonds on Tuesday was met with the softest demand since December 2023. That helped drive the bond sell-off on fears of a pullback among international investors, who hold $8.5 trillion in US Treasuries (Japan and China lead the pack).

I am in an unenviable position. The policy coming out of the White House has a significant impact on economics, more than ever before in my career. If I say anything positive about that policy, I’ll be put in the MAGA camp. If I criticize it, I’ll be accused of suffering from Trump derangement syndrome. I am hired by you to make the best investment decisions possible. Rather than see me as engaged in political commentary, I’d ask that you view my remarks as purely analytical.

Let me give you this analogy. I live in Denver. Let’s imagine I am a huge Broncos fan, and the Broncos are playing the Chicago Bears. If I am betting a significant amount of money on this game, I should put my affinity for the Broncos and hatred of the Chicago Bears aside and analyze data and facts. The Broncos are either going to win or lose; my wanting them to win has zero impact on the outcome. The same applies to my analysis here. My motto in life is Seneca’s saying, “Time discovers truth.” I just try to discover it before time does.

When it comes to politics, I also have a significant advantage. I was not born in this country. From a young age, I was brainwashed about communism, not about team Republican versus team Democrat. The failure of the Soviet Union de-brainwashed me fast concerning the virtues of communism and converted me into a believer in free markets.

As a result, I never bought into either party’s ideology, and thus in the last four presidential elections I voted for a Republican, an independent, a Democrat, and wrote in my youngest daughter, Mia Sarah (not in that order). In my articles I have criticized the policies of both Biden (student loan forgiveness, unions) and Trump (Bitcoin reserve).

I remind myself that in times like these you have to be a nuanced thinker. Some of Trump’s policies are terrific, others … not so much (I am being diplomatic here).

Scott Fitzgerald once said “The test of a first-rate intelligence is the ability to hold two opposed ideas in mind at the same time, and still retain the ability to function.” In 2025 we are taking this “first-rate intelligence” test daily.

What will happen to the US dollar? The US dollar will likely continue to get weaker, which is inflationary for the US. Let me start with some easily identifiable reasons:

We have too much debt. We ran 6-7% budget deficits while our economy was growing and unemployment was at record lows. Now we have $36 trillion in debt. Our interest expenses exceed our defense spending, and these costs will continue to climb. If/when we go into recession, we may see something we have not seen in a long time – higher interest rates. Our budget deficits will balloon to between 9–12%, and the debt market, realizing that inflation (i.e., money printing) is inevitable, will say, “Pay up!”

New competition from Bitcoin. President Trump’s approval of Bitcoin as a potential reserve currency is one of the most self-serving and anti-American things I’ve seen any president do. The US dollar is the world’s reserve currency. We still have little competition for that title. China could be a contender, but it is not a democracy and has capital controls. This policy has no upside for America, only downside.

A stronger Europe. Ironically, we may inadvertently create a stronger Europe by threatening to abandon NATO. I don’t want to insult European clients (or my European friends), but the following analogy describes the US-Europe relationship on some level: Europe gradually evolved into a trust fund kid (when it came to security) and the US turned into its sugar daddy. The trust fund kid was incredibly dependent on the sugar daddy. It criticized its parent for being a barbarian and money-driven, but it relied heavily on that parent to protect it from bullies.

President Trump cut off Europe’s allowance by threatening that the US might not protect Europe from Russia. This has forced Europe to spend more money on defense. Outside of Germany (which has little debt), few European economies can afford that. This may force Europe (or at least some European countries) to become more pragmatic – to cut social programs and bureaucracy. If this leads to a stronger Europe both economically and militarily, the euro will be competing with the US dollar. This is a big if.

Our new foreign policy.

When people describe President Trump’s foreign policy as “transactional,” they’re highlighting a fundamental shift in how America engages with the world – one with profound implications for our global standing, national interests, and the US dollar. The shift affects both types of capital – financial and reputational.

Reputational capital isn’t at risk in ‘one-shot’ transactions like house selling. Imagine you’re selling your primary residence and moving elsewhere. Do you disclose every flaw, or let the buyer figure things out? Your incentive is to maximize short-term profits. You’ll likely never meet this buyer again, and therefore there are incentives not to care what they’ll think of you afterward. You’ll be transactional, seeking the highest price possible for your biggest asset. This exemplifies a ‘one-shot’ system where future interactions aren’t expected.

Contrast this with a relationship- and trust-based system. Now imagine you are a homebuilder in a small town. Your suppliers only extend credit if you have a reputation for paying on time. Your employees do quality work only if you treat them fairly. Your buyers tell friends about their experience with you. The incentives naturally create a relational approach. In this trust-based system, incentives skew toward maximizing long-term profits, where reputational capital becomes the glue creating continuity.

Reputational capital radiates predictability – you know how someone will behave based on their history – but operating with low or negative reputational capital is difficult and expensive. People won’t enter long-term contracts with you or will demand external guarantees. Many potential partners will simply refuse to deal with you.

Building reputational capital works like adding pennies to a jar – each good deed incrementally adds to your standing. Yet reputational capital can collapse instantly by removing the jar’s bottom. A single breach of trust doesn’t just remove one penny; it can wipe out your entire balance and plunge you into reputational bankruptcy. The math is brutally asymmetric: good deeds might add a point or two, while bad deeds subtract by factors of 50 or 100.

This doesn’t mean transactions shouldn’t be profitable. If you’re accumulating reputational capital while consistently losing money, you’re probably in the wrong business. Each deal should be evaluated considering both long-term financial and reputational capital.

Individual transactions can sacrifice some profit but cannot afford to lose reputational capital. A “one-shot” transactional approach used in a trust-system environment may provide greater short-term profitability, but if this success comes at the expense of reputational capital, the long-term consequences for America’s global position could be devastating.

This brings us to our current foreign policy.

Relationships between nations are a trust-based system. I’d argue it’s a super-relational system because it’s multigenerational, lasting beyond the life of any one human. Reputational capital is paramount here.

Part of the US’s strength has been the soft power – the reputational capital – it exerted. We had a lot of friends, which helped us to be more effective in dealing with our foes. We keep telling ourselves that America is an “exceptional” nation. This exceptionalism didn’t just come from our financial and military might – it accumulated based on our reputational capital.

Though we don’t always succeed, we are a people who try to do the right thing. Our exceptionalism has been earned through our actions. We are the country that helped rebuild Europe and gave it six decades to repay lend-lease. We toppled communism.

I don’t know the nuances of the Ukraine mineral deal, but initially it had the optics of extortion. Though I think the renegotiated and signed version appears to be fair to both sides, forcing repayment while Ukraine is dodging Russian missiles made the US look transactional.

Actions by President Trump over the last month have undermined our reputation. We are quickly becoming a “one-shot” transactional player in a trust-based environment. Imposing tariffs on Canada on a whim to try to get it to become the 51st state erodes American reputational capital. So does not ruling out America invading Greenland. This puts us on the same moral plane as Russia invading Ukraine.

The conversation about tariffs has many nuances. For instance, I don’t know anyone who opposes reciprocal tariffs – they seem fair and don’t consume any reputational capital. But tariffs that are used as weapons in a trade war in order to annex another country erode reputational capital. Threatening to leave NATO and not protect countries that don’t spend enough on their defense diminishes reputational capital. Maybe the only way to get European countries to spend on defense was to threaten not to defend them – you can agree or disagree with the rationale behind each of Trump’s decisions, but what can’t be argued is that they undermined our reputational capital.

As we lose soft power, our influence will diminish, and thus so will perceptions of our power. The world will start looking at us not from the perspective of the continuity of generations but of presidential cycles. The word of the American president will have an expiration date of the next presidential or mid-term election.

There are two negotiation styles – Warren Buffett’s and Donald Trump’s. Both have their advantages and disadvantages. Buffett will give you one offer and one offer only. Once the deal is agreed to, even just verbally, that is the deal. Critics would say that there is downside to that predictability, as foes know how you are going to respond. Donald Trump’s style is to be unpredictable, which has its own advantages when you deal with foes – it keeps opponents guessing. But it destroys trust with your allies.

In a world of fiat currencies, all currency is a financial and reputational promise. President Trump, with the help of DOGE (and maybe even tariffs) may increase our financial strength. I hope he does, but it will likely come at a very high cost to our reputational capital, and therefore US global influence and the US dollar will continue its decline.

How are we positioned for this?

About half of our portfolio is foreign companies whose sales are not in dollars. They will benefit from a weaker dollar. We also have exposure to oil, which is priced in the US dollar and usually appreciates when the dollar weakens.

A weaker dollar means our imports will become more expensive, which is inflationary. We own many companies with pricing power and also companies that have claims on someone else’s revenues. Take Uber for example: they get about 20% of each ride. If the cost of the ride goes up, so does their dollar take.

Why does President Trump keep pushing crypto?

In July 2019, Trump said the following: “I am not a fan of Bitcoin and other cryptocurrencies, which are not money, and whose value is highly volatile and based on thin air.” Five years later he promised to establish the US Crypto Reserve, and in 2025 he did.

What changed? There is no logical reason for an American president to endorse crypto. None. Here is the honest answer: Crypto bros made mega-contributions to his campaign.

To top it off, three days before he took office he issued $TRUMP – a shitcoin. Believe it or not, “shitcoin” is a technical term in the crypto community (any coin other than Bitcoin is called a shitcoin by Bitcoin “maximalists”, folks who believe Bitcoin is the one and only digital currency). The future sitting president literally issued – I don’t want to call it a currency, so I guess shitcoin is the right name – that will at some point decline to zero in value. In other words, he’ll fleece his loyal followers who purchase $TRUMP of billions of dollars.

I previously referenced both reputational capital and soft power. These types of acts by a sitting president subtract from both.

Posted on April 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Just after midnight, President Trump’s “reciprocal” tariffs went into effect against 86 countries. Analysts have estimated that the new US average effective tariff rate is north of 20%, the highest in more than 100 years. Ahead of the tariff deadline, markets swung violently, mostly way down: According to Bloomberg’s Cameron Crise, yesterday was the fourth straight trading day when the S&P 500’s trading range was 5% or more. That’s only happened in 1987, 2008, and 2020.

***

***

The Apple A18 and Apple A18 Pro are a pair of 64-bit ARM-based system on a chip (SoC) designed by Apple Inc., part of the Apple silicon series. They are used in the iPhone 16 and iPhone 16 Pro lineups and the iPhone 16e, and built on a second generation 3 nm process by TSMC.

***

Yesterday, for several hours on Tuesday, it looked like stocks were going to regain some of the ground lost during the market’s very bad week. But after the Trump administration made it clear that its increased tariffs on China would go into effect, all three indexes plunged. Apple, which makes most of its iPhones in China, was hit harder than many of its Big Tech peers.

So shoppers are thinking it’s better to have an Apple A18 processor and not need it, than to need it and not have it. Apple customers are scrambling to buy new iPhones out of fear that the company could raise prices to offset President Trump’s tariffs.

Employees at locations throughout the US said they’re being bombarded with questions about potential price hikes and have witnessed customers panic-buying phones. Though Apple declined to comment to Bloomberg, its retail stores reportedly saw higher sales over the last weekend than in previous years.

Posted on April 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Initial Public Offering Defined

IPO stands for initial public offering. It is when a company takes a portion of their shares and makes them available for the general public to buy on the open market. It is a way for the company to raise money by selling those shares to the general public. You can usually access shares from an IPO by working directly with an investment bank.

Paused IPOs

Private companies StubHub and Klarna each paused their imminent plans to go public.

Klarna, which was set to IPO on this Monday, was expected to jump-start the frozen IPO market this year with an expected ~$15 billion valuation.

StubHub, meanwhile, reportedly wants to wait for the market to calm down before resuming its plans to go public.

Markets: Last week’s market bloodbath will go down in the history books. The S&P 500’s 10% plunge on Thursday and Friday, after President Trump announced massive tariffs, ranks among the steepest two-day decline in the last 70 years, on par with Black Monday in 1987, the post-Lehman Brothers rout in 2008, and the Covid plunge in March 2020. More than $6 trillion was wiped out from stocks over two days, and the NASDAQ entered a bear market, down 20% from a previous high.

Trading restarted at 9:30 am ET for what Bill Ackmanpredicts will be “one of the more interesting days in our country’s economic history.”

***

Monday Crash?

On the other hand, CNBC host and market commentator Jim Cramer just warned that America is in store for another “Black Monday” market crash similar to the record 1987 collapse if President Trump doesn’t curtail his tariff plan.

Cramer — who noted that the 1987 crash saw the Dow Jones Industrial Average fall by 22.6% in a single day — said the bloodbath could be repeated after the brutal two-day sell-off following the announcement of Trump’s sweeping tariffs against nearly 90 countries.

If the president doesn’t try to reach out and reward these countries and companies that play by the rules, then the 1987 scenario … the one where we went down three days and then down 22% on Monday, has the most cogency,” Cramer said on his show Saturday, referencing the worst single-day fall in the history of the Dow.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

***

The Hedge Fund manager I am considering is a Registered Investment Adviser [RIA]

QUESTION: What is a Registered Investment Advisor?

If the fund manager is an entity, then any individual you deal with will be a registered investment adviser representative. If the fund manager is an individual, then that individual is a registered investment adviser. In either case, the designation implies several steps have been taken.

In order to become a registered investment adviser, an individual must register for and pass the Series 65 Uniform Investment Adviser Law Exam, a three-hour, 130-question computer-based exam administered by the North American Securities Administrators Association. Topics covered include economics and analysis, investment vehicles, investment recommendations and strategies, and ethics and legal guidelines. A passing score is 70 percent or higher.

Once an individual has passed the Series 65, he or she must then apply via Form ADV to become a registered investment adviser. This application is made to either a state authority or to the SEC, depending on the adviser’s assets under management. If assets under management exceed $30 million, then the adviser must register with the SEC.

Form ADV consists of two parts. Part I provides general information to the regulatory authority. Part II is designed to be distributed to potential clients, and includes disclosure of a decent amount of information about the adviser. If the manager is a registered investment adviser, then you should expect to receive as part of the offering documentation either a current copy of Part II of the adviser’s Form ADV or a brochure that contains all the current information in Part II of Form ADV.

In addition to filing Form ADV and paying a small fee, the registered investment adviser becomes subject to extra administrative/regulatory burden as well as capital adequacy requirements that state the Adviser must maintain certain net worth levels.

By and large, because of the extra administrative burden as well as restrictions on certain activities, hedge fund managers attempt to avoid registering as investment advisers. Whether such managers can or cannot avoid such registration is largely dependent upon the state in which the manager operates. In California, for instance, hedge fund managers must register as investment advisers. In New York, such registration is not necessary. Not surprisingly, hedge fund managers located in California are rare, while they are quite plentiful in New York.

Your knee hurts, so you pay a visit to your favorite orthopedist. He smiles, maybe even gives you a hug, and then tells you: “I feel your pain. Really, I do. But I don’t treat left knees, only right ones. I find I am so much better with the right ones. Last time I worked on a left knee, I didn’t do so well.”

Though many professionals — doctors as well as lawyers, architects and engineers — get to choose their specializations, they rarely get to choose the problems they solve. Problems choose them. Investors enjoy the unique luxury of choosing problems that let them maximize the use of not just their IQ but also their EQ — emotional intelligence.

Let’s start with IQ. Our intellectual capacity to analyze problems will vary with the problem in front of us. Just as we breezed through some subjects in college and struggled with others, our ability to understand the current and future dynamics of various companies and industries will fluctuate as well. This is why we buy stocks that fall within our sphere of competence. We tend to stick with ones where our IQ is the highest.

Though we usually think about our capacity to analyze problems as being dependable and stable over time, it isn’t. It might be if we were characters from Star Trek, with complete control over our emotions, like Mr. Spock, or who lacked emotions, like Lieutenant Commander Data. This is where our EQ comes in.

I am not a licensed psychologist, but I have huge experience treating a very difficult patient: me. And what I have found is that emotions have two troublesome effects on me. First, they distort probabilities; so even if my intellectual capacity to analyze a problem is not impacted, my brain may be solving a distorted problem. Second, my IQ is not constant, and my ability to process information effectively declines under stress. I either lose the big picture or overlook important details. This dilemma is not unique to me; I’m sure it affects all of us to various degrees.

The higher my EQ with regard to a particular company, the more likely that my IQ will not degrade when things go wrong (or even when they go right). There is a good reason why doctors don’t treat their own children: Their ability to be rational (properly weighing probabilities) may be severely compromised by their emotions.

A friend of mine who is a terrific investor, and who will remain nameless though his name is George, once told me that he never invests in grocery store stocks because he can’t be rational when he holds them. If we spent some Freudian time with him, we’d probably discover that he had a traumatic childhood event at the grocery store (he may have been caught shoplifting a candy bar when he was eight), or he may have had a bad experience with a grocery stock early in his career. The reason for his problem is irrelevant; what is important is that he has realized that his high IQ will be impaired by his low EQ if he owns grocery stocks.

There is no cure for emotions, but we can dramatically minimize the impact they have on us as investors by adjusting our investment process. First and foremost, investors have the incredible advantage of picking domains where they can remain rational.

To be a successful investor, you don’t need Albert Einstein’s IQ (though sometimes I wish I had Spock’s EQ). Warren Buffett undoubtedly has a very high IQ, but even the Oracle of Omaha chooses carefully his battles; for instance, he doesn’t invest in technology stocks.

Investors have the luxury of investing only in stocks for which both their IQ and EQ are maximized, because there are tens of thousands of stocks out there to choose from, and they need just a few dozen.

Meanwhile, I hope when I go see the doctor, he will tell me, “I don’t do left knees,” because the best result will come from a doctor who while treating me will utilize both IQ and EQ.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

***

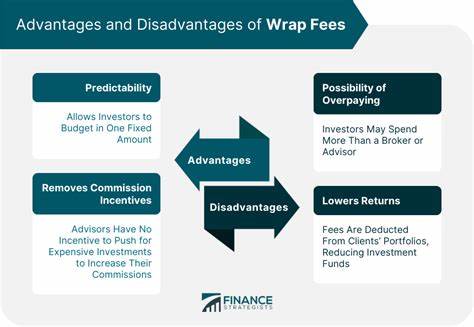

My stock broker is telling me about a “wrap-fee” program involving a hedge fund manager.

QUESTION: What is a Wrap Fee?

A wrap fee program is a service that provides investment advice and portfolio management to clients for one all-inclusive fee. The fee pays for the services provided to the client, including but not limited to securities transactions, portfolio management, research, brokerage, and administrative services. Wrap fee programs also provide an understanding of a client’s financial goals and objectives; research and selection of assets; implementation of investment decisions; account statements, and access to real-time financial data.

The Investment Advisers Act of 1940 regulates investment advisors when they offer these wrap fee programs and requires them to provide comprehensive disclosure documents before investing. This act helps ensure clients have access to all important information that affects their investment decisions.

QUESTION: Why do I need my stock broker? Can I just go directly to the hedge fund manager?

Yes, you can, but you may find a different fee arrangement when you reach the hedge fund manager, and you may be participating in an unethical transaction. When hedge fund managers set up separate accounts for wrap-fee clients, they agree to take a set fee in exchange for managing this money. They also enter into agreements with one or more brokers to help market this aspect of their money management business. A portion of the wrap fee you pay goes to the broker, and a portion goes to the manager. Incentive compensation is not generally used.

When approached directly, hedge fund managers will typically offer only the hedge fund, complete with incentive compensation and pooled investment features. However, if the hedge fund manager is willing to set up a separate account, it is possible that the investor will find the set fee much less than what he or she would have paid in a wrap fee account through a broker.

Finally, the very large caveat to all this is that the ethics of a hedge fund manager who steals clients from brokers with whom he has a marketing relationship ought to be called into question. And when it comes to hedge funds, the ethics of the manager are of paramount importance.

Profitability ratios measure a company’s ability to generate income relative to revenue, balance sheet assets, operating costs, and equity. Common profitability financial ratios include the following:

The gross margin ratio compares the gross profit of a company to its net sales to show how much profit a company makes after paying its cost of goods sold:

Gross margin ratio = Gross profit / Net sales

The operating margin ratio, sometimes known as the return on sales ratio, compares the operating income of a company to its net sales to determine operating efficiency:

Operating margin ratio = Operating income / Net sales

The return on assets ratio measures how efficiently a company is using its assets to generate profit:

Return on assets ratio = Net income / Total assets

The return on equity ratio measures how efficiently a company is using its equity to generate profit:

Return on equity ratio = Net income / Shareholder’s equity

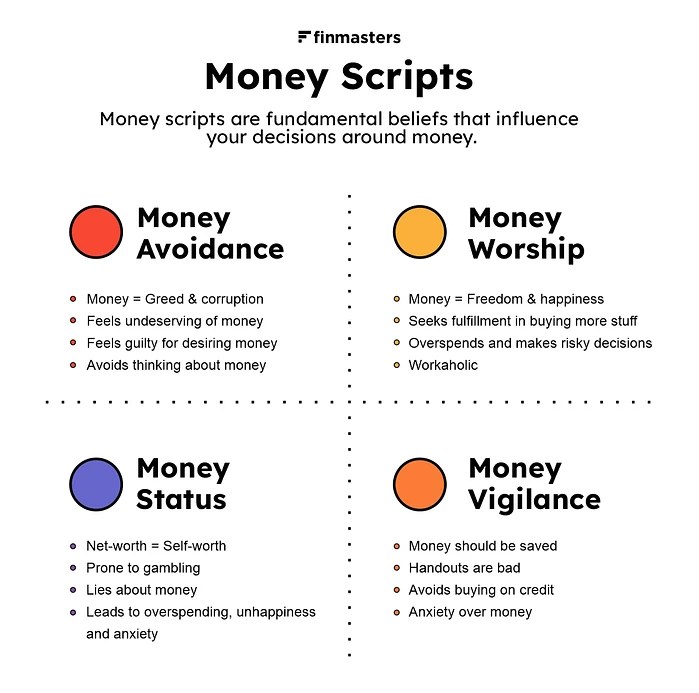

Stocks were decimated yesterday in the first full trading day following President Trump’s tariff announcement. It was the biggest single-day decline since the start of the Covid-19 pandemic in March 2020. Every Magnificent Seven stock was battered—Apple worst of all. And so perhaps it is a good time to discuss the concept of “Money Scripts”.

***

Money Scripts are unconscious beliefs about money that are typically only partially true, are developed in childhood, and drive adult financial behaviors. Money scripts may be the result of “financial flashpoints,” which are salient early experiences around money that have a lasting impact in adulthood. Money scripts are often passed down through the generations and social groups often share similar money scripts. And so, we argue that Money scripts are at the root of all illogical, ill-advised, self-destructive, or self-limiting financial behaviors.

In research at Kansas State University [KSU], researchers identified four distinct Money script patterns, which are associated with financial health and predict financial behaviors. These include: (a) money avoidance, (b) money worship, (c) money status, and (d) money vigilance [personal communication Brad Klontz, PsyD, CFP®, Kenneth Shubin-Stein, MD, MPH, MS, CFA and Sonya Britt, PhD, CFP®].

And so, we all like to think our financial decisions are fully rational, but the truth is that our subconscious beliefs have a dramatic impact on our money and financial decisions. These money scripts are important to know and understand. A summary is below:

Money Avoidance

Money avoidance scripts are illustrated by beliefs such as “Rich people are greedy,”“It is not okay to have more than you need,” and “I do not deserve a lot of money when others have less than me.” Money avoiders believe that money is bad or that they do not deserve money. They believe that wealthy people are corrupt and there is virtue in living with less money. They may sabotage their financial success or give money away even though they cannot afford to do so. Money avoidance scripts may be associated with lower income and lower net worth and predict financial behaviors including ignoring bank statements, overspending, financial dependence on others, financial enabling of others, and having trouble sticking to a budget.

Money Worship

Money worship is typified by beliefs such as “More money will make you happier,” “You can never have enough money,” and “Money would solve all my problems.” Money worshipers are convinced that money is the key to happiness. At the same time, they believe that one can never have enough. Money worships have lower income, lower net worth, and higher credit card debt. They are more likely to be hoarders, spend compulsively, and put work ahead of family.

Money Status

Money status scripts include “I will not buy something unless it is new,” “Your self-worth equals you net worth,” and “If something isn’t considered the ‘best’ it is not worth buying.” Money status seekers see net worth and self-worth as being synonymous. They pretend to have more money than they do and tend to overspend as a result. They often grew up in poorer families and believe that the universe should take care of their financial needs if they live a virtuous life. Money status scripts are associated with compulsive gambling, overspending, being financially dependent on others, and lying to one’s spouse about spending.

Money Vigilance

Money vigilant beliefs include “It is important to save for a rainy day,” “You should always look for the best deal, even if it takes more time,” and “I would be a nervous wreck if I did not have an emergency fund.” The money vigilants are alert, watchful and concerned about their financial welfare. They are more likely to save and less likely to buy on credit. As a result, they tend to have higher income and higher net worth. They also have a tendency to be anxious about money and are secretive about their financial status outside of their household. While money vigilance is associated with frugality and saving, excessive anxiety can keep someone from enjoying the benefits that money can provide.

Identification

When money scripts are identified, it is helpful to examine where they came from. A simple behavioral finance technique involves reflecting on the following questions:

What three lessons did you learn about money from your mother?

What three lessons did you learn about money from your father?

What is your first memory around money?

What is your most painful money memory?

What is your most joyful money memory?

What money scripts emerged for you from this experience?

How have they helped you?

How have they hurt you?

What money scripts do you need to change?

Conclusion

Ideally, from a balanced middle ground, we can see past the limitations of money scripts, our self and others who are polarized. Those who believe “Money is meant to be spent” or “Money is meant to be saved” have a world view that results in extreme positions. Labeling them as “correct” or “wrong” is not a useful way to try to shift anyone’s polarized money script beliefs.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on April 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Roughly $2.5 trillion was erased from the S&P 500 Index on Thursday amid worries that President Donald Trump’s sweeping new round of tariffs could plunge the economy into a recession. The damage was heaviest in companies whose supply chains are most dependent on overseas manufacturing. Apple Inc., which makes the majority of its US-sold devices in China, fell 9.3%. Lululemon Athletica Inc. and Nike Inc., among companies with manufacturing ties to Vietnam, were both down more than 9%. Target Corp. and Dollar Tree Inc., retailers whose stores are filled with products sourced outside of the US, dropped more than 10%.

The tech-heavy NASDAQ Composite (^IXIC) led the sell-off, plummeting 6%. The S&P 500 (^GSPC) sank nearly 5%, while the Dow Jones Industrial Average (^DJI) tumbled 4%. The Dow’s 1,700-point drop was the fifth-worst in its history.

Posted on April 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS – MARKET VOLATILITY

By Staff Reporters

***

***

US stocks nosedived on Thursday, with the Dow tumbling more than 1,200 points as President Trump’s surprisingly steep “Liberation Day” tariffs sent shock waves through markets worldwide. The tech-heavy NASDAQ Composite (IXIC) led the sell-off, plummeting over 4%. The S&P 500 (GSPC) dove 3.7%, while the Dow Jones Industrial Average (^DJI) tumbled roughly 3%. [ongoing story].

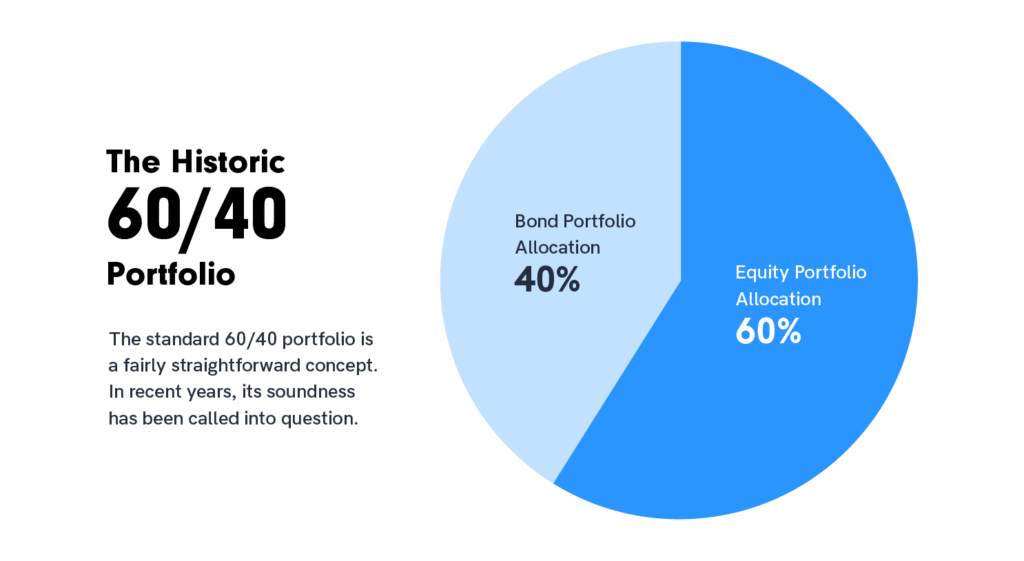

So, does the traditional 60 stock / 40 bond strategy still work or do we need another portfolio model?

***

The 60/40 strategy evolved out of American economist Harry Markowitz’s groundbreaking 1950s work on modern portfolio theory, which holds that investors should diversify their holdings with a mix of high-risk, high-return assets and low-risk, low-return assets based on their individual circumstances.

While a portfolio with a mix of 40% bonds and 60% equities may bring lower returns than all-stock holdings, the diversification generally brings lower variance in the returns—meaning more reliability—as long as there isn’t a strong correlation between stock and bond returns (ideally the correlation is negative, with bond returns rising while stock returns fall).

For 60/40 to work, bonds must be less volatile than stocks and economic growth and inflation have to move up and down in tandem. Typically, the same economic growth that powers rallies in equities also pushes up inflation—and bond returns down. Conversely, in a recession stocks drop and inflation is low, pushing up bond prices.

***

But, the traditional 60/40 portfolio may “no longer fully represent true diversification,” BlackRock CEO Larry Fink writes in a new letter to investors.

Instead, the “future standard portfolio” may move toward 50/30/20 with stocks, bonds and private assets like real estate, infrastructure and private credit, Fink writes.

Here’s what experts say individual investors may want to consider before dabbling in private investments.

It may be time to rethink the traditional 60/40 investment portfolio, according to BlackRock CEO Larry Fink. In a new letter to investors, Fink writes the traditional allocation comprised of 60% stocks and 40% bonds that dates back to the 1950s “may no longer fully represent true diversification.“

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on April 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHA CPHQ CMP™

***

***

Finally … Fiduciary second investing and financial planning opinions right here!

Telephonic or electronic advice for medical professionals that is:

Objective, affordable, medically focused and financially personalized

Rendered by a pre-screened financial consultant for doctors and medical professionals

Offered on a pay-as-you-go basis, by phone or secure e-mail transmission

The iMBA Discussion Forum™ is a physician-to-financial advisor telephone or e-mail portal that connects independent financial professionals to doctors, nurses or healthcare executives desiring affordable and unbiased financial planning advice.

Medical professionals and healthcare executives can now receive direct access to pre-screened iMBA professionals in the areas of Investing, Financial Planning, Asset Allocation, Portfolio Management, Insurance, Mortgage and Lending, Human Resources, Retirement Planning and Employee Benefits. To assist our medical professional and healthcare executive members, we can be contracted with per-minute or per-project fees, and contacted by client phone, email or secure instant messaging.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

QUESTION:Can I invest my Individual Retirement Account [IRA] in a Hedge Fund?

This is up to the manager, but there is no legal restriction on a hedge fund accepting individual retirement account (IRA) assets. IRA accounts are not well suited for funds that make extensive use of leverage, however. In such cases, the fund is likely to generate significant amounts of unrelated business taxable income (UBTI) – profits of the fund attributable to the use of leverage. The holder of an IRA account must pay taxes on UBTI, even if the UBTI was generated in an IRA account.

But, today’s hedge funds may or may not use leverage. Many hedge funds are not hedged at all, but rather are just specialized versions of regular long stock portfolios. If such funds do not use much leverage, IRA investors will not encounter much difficulty with UBTI and should not hesitate in considering these funds.

In considering whether to accept IRA money, hedge fund managers must consider several factors. If the only type of retirement money accepted by the hedge funds is IRA money, then the manager has no limit on how much retirement money the fund can accept. If, however, there are other types of retirement money invested in the fund, such as pension funds, IRA money will be counted towards a total of 25 percent of fund assets that can be invested in retirement accounts before the fund becomes subject to the Employment Retirement Income Security Act of 1974 (ERISA). Funds subject to ERISA regulations face a heavy administrative burden and more restrictions than most fund managers like.

Finally, IRA distributions from a hedge fund are subject to the standard 20 percent withholding unless the funds are directly rolled over to other qualified plans.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Both median and average family net worth surged between 2019 and 2022, according to the U.S. Federal Reserve. Average net worth increased by 23% to $1,063,700, the Fed reported in October 2023, the most recent year it published the data. Median net worth, on the other hand, rose 37% over that same period to $192,900.

You might wonder why the average and median net worth figures are so different. That’s because when you take the average of something, you add together every value in a data set and then divide that figure by the number of individual values.

When calculating a median, you simply look at the middle figure within a data set. That said, an average figure can be significantly higher or lower than a median figure if there are extreme outliers – meaning a group of people with significantly more net worth than the rest of the group can bring the average higher.

Average Net Worth by Age

The average net worth of someone younger than 35 years old is $183,500, as of 2022. From there, average net worth steadily rises within each age bracket. Between 35 to 44, the average net worth is $549,600, while between 45 and 54, that number increases to $975,800. Average net worth surges above the $1 million mark between 55 to 64, reaching $1,566,900.

Average net worth again rises for those ages 65 to 74, to $1,794,600, before falling to $1,624,100 for the 75 and older group. The median net worth within every single age bracket, however, is much lower than the average net worth.

***

***

Physicians [MD/DO]Net Worth by Specialty

A 2023 Medscape report shows the top 10 specialties with the most survey respondents saying they are worth more than $5 million.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

An important concept for all medical professionals to understand is the current rate of return (CCR).

According to this principle, the current rate of a taxable return must be evaluated in reference to a similar non-taxable rate of return. This allows you to focus on your portfolio’s real (after-tax return), rather than its’ nominal, or stated return.

Now, since most medical professionals own a combination of both vehicles, it is important to calculate the average rate of return (ARR), as demonstrated in the following matrix. Usually, this will result in the assumption of more risk, for the possibility of great return.

To compare after tax yields, with taxable yields, use the following formulas: