BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on July 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler CFP™

***

***

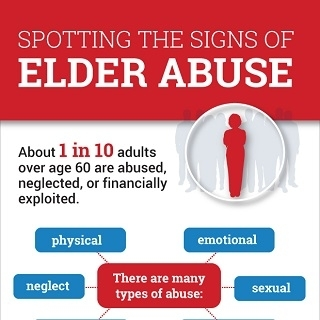

One serious risk to financial wellbeing in retirement that is difficult to talk about is financial exploitation. Someone whose cognitive abilities are declining is vulnerable to harm from both financial predators and their own financial misjudgments. Protecting such clients is a crucial part of a financial advisor’s role.

A little-known but important law, the Senior Safe Act, was enacted in 2018. It encourages financial advisors and institutions to report suspected elder abuse by offering immunity from legal liability when reports are made in good faith and with reasonable care. To qualify for these protections, financial professionals must undergo annual training to recognize the signs of exploitation and know how to act on their suspicions.

In many ways, the Senior Safe Act mirrors the duty of therapists to report when clients are threats to themselves, such as when a client becomes suicidal. Just as a therapist must balance confidentiality with the moral and legal responsibility to protect their client from harm, a financial advisor must weigh privacy against the need to prevent financial exploitation. Both roles rely on professional judgment, training, and the courage to act when the stakes are high.

Financial advisors, accountants, and attorneys are often the first to notice troubling signs that someone is being taken advantage of financially. These might include sudden large withdrawals, changes to account ownership or beneficiaries, or a newly and overly involved friend or family member. Behavioral shifts like confusion, anxiousness, secretiveness, or uncharacteristic deference are also red flags. These patterns are unsettling and demand attention, even when stepping in is uncomfortable.

Reporting possible elder abuse isn’t always straightforward, especially if the suspected abuser is a family member. As an advisor, I worry about misunderstandings, potential conflicts with the family, and even the possibility of damaging a relationship with the client. None of this is easy, But when the signs of exploitation become clear, staying silent could mean allowing harm to continue. That’s a risk I can’t take.

One of the tools I started using decades ago is the trusted contact disclosure form. This simple but powerful document allows clients to name someone my firm can contact if they notice unusual activity, such as a suspicious withdrawal or transfer. The trusted contact does not have control over the client’s account but serves as a resource to verify their well-being and ensure that their financial decisions align with their long-term goals. If you as a client have not signed such a form, it’s worth discussing with your advisor as a preventative step.

If you are concerned about the financial well-being of an elderly loved one, it’s crucial to alert not only their financial advisor but also other professionals like accountants, attorneys, or bankers. These professionals may have insights or access to information you don’t have, and by sharing your concerns, you provide a broader picture that can help them detect and address issues more effectively. Even if they are already monitoring for red flags, your input can provide valuable context to guide their next steps.

Difficult though it may be, stepping into uncomfortable territory is often essential to protecting vulnerable individuals. Whether it’s a financial advisor detecting exploitation or a therapist intervening in a mental health crisis, the goal is the same—to prevent harm while respecting the person’s autonomy.

The Senior Safe Act is a reminder that sometimes the most impactful safeguards work quietly behind the scenes. Taking simple steps like completing a trusted contact form or encouraging your loved one to work with a reputable, fiduciary advisor can make all the difference. Vigilance is an act of care that helps protect someone’s financial assets as well as their dignity and well-being.

Posted on July 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants LLC

***

***

On June 9th, 2025, Oregon’s governor signed into law the country’s strictest corporate practice of medicine (CPOM) prohibition. Senate Bill (SB) 951 will severely curtail the involvement of private equity firms and other corporations in the state’s medical practices.

This Health Capital Topics reviews the bill and discusses the implications on the healthcare industry. (Read more…)

Posted on July 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Medical doctors, dentists, and podiatrists have to undergo extensive training before they can practice medicine independently. Once they receive training, there are opportunities to increase pay and prestige in the medical field through a series of promotions. As a doctor, how much training, experience and skills you have can determine your ability to move upward in these levels. But, personal branding strategies may even be more vital in today’s social media age?

***

Physician, medical and healthcare branding is more than just the creation of logos, taglines, or specific brand messaging. It’s about creating a meaningful connection between your mission, vision and values and the people served – from patients and their families to local and global communities.

While there are many different types of branding strategies in marketing science, they all share key elements that serve as the foundation for the strategy. These 9 elements for all physicians and medical professionals include the following:

Brand purpose: The reason the physician is in practice and what he/she is trying to achieve.

Brand vision: The ideas and goals behind the dentist which serve as inspiration for practice growth.

Brand values: The osteopaths beliefs and what they stand for.

Target audience: The demographic(s) and patient targets that the podiatrist is aiming to reach.

Market analysis: An analysis of the marketplace that identifies gaps where the chiropractor has an opportunity to position him/her self based on a unique value proposition.

Awareness goals: The initiatives the doctor will take in order to reach a target market patient demographic.

Brand personality: The human-like attributes of the physician that will help build relationships with patients, consumers and other physicians and practitioners.

Brand voice: The language and tone the doctor uses to communicate with patients, physicians and consumers.

Brand tagline: A memorable slogan that sums up the physician and their medical offering in a few choice words.

And so, physician branding is the development of a easily recognizable identity for a medical practice, clinic or healthcare organization that helps to shape perception by current and prospective patients and the wider world.

Posted on July 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets wrapped the trading day with another win thanks to a shockingly strong jobs report this morning. Both the S&P 500 and the NASDAQ hit new record highs.

A brand is a name, term, design, symbol or any other feature that distinguishes one seller’s goods or service from those of other sellers. Brands are used in business, marketing and advertising for recognition and, importantly, to create and store value as brand equity for the object identified, to the benefit of the brand’s clients, patients, customers, its owners and shareholders. Brand names are sometimes distinguished from generic or store brands.

Brand management, also known as Marketing, is responsible for the overall management of a brand. This includes everything from product or service development and marketing to advertising and public relations. All of these aspects work together to create a particular image or reputation for a brand. The goal of brand management is to create a robust and positive reputation for a brand that will result in increased sales and market share.This process helps companies create a unique identity for their products or services in the marketplace. A successful brand management strategy can build client, patient and customer loyalty .

Branding is essential for financial advisors, doctors and businesses because it involves creating a unique identity for a company’s products, offerings and services. It can also help build customer, client and patient loyalty and emotionally connect with the practitioner. Branding can be complex, but it is essential to understand the basics before starting a brand strategy.

Thus, doctors, podiatrists, dentists, CPAs, insurance agents, financial advisors and their practices need to understand the different aspects of branding and brand management to create a strong brand identity.

Posted on July 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Power station: Crude oil prices reversed as tensions in the Middle East cooled, but AI likely raises electricity demand over the longer term, creating investment opportunities and risks.

Oil supplies now exceed demand, noted Michelle Gibley, director of international research at the Schwab Center for Financial Research, in her latest analysis, though “AI is transforming the energy sector,” raising power shortage concerns.

Solar stocks got a reprieve today after the Senate dropped the excise tax on clean energy projects. Sunrun soared 10.51%, EnphaseEnergy rose 3.18%, SolarEdgeTechnologies popped 7.16%, and ArrayTechnologies climbed 12.54%.

Apple tumbled this summer after investors were disappointed by its AI rollout, but rose 1.29% on the news that the company may pivot to using Anthropic or OpenAI in iPhones instead of building something in-house.

Wolfspeed, the best name for a company that makes computer chips, exploded 98.09% after the company officially filed for Chapter 11 bankruptcy.

Hasbro got a nice 4.29% bump thanks to Goldman Sachs analysts, who are big old nerds who think Magic: The Gathering will boost the toymaker’s sales.

Ford popped 4.61% after the automaker reported an impressive 14% increase in sales last quarter.

Casino stocks soared on the news that gaming revenue in Macau rose 19% in June. WynnResorts climbed 8.85%, Las Vegas Sands added 8.95%, and MGMResorts gained 7.24%.

What’s down

AMC Entertainment tumbled 9.03% after the one-time meme stock announced its new debt restructuring plan.

ProgressSoftware sank 13.03% after the business application software company reported mixed results last quarter, beating on profit but missing on revenue.

JobyAviation fell 7.01% after traders took profits following the air taxi company’s big pop yesterday.

AeroVironment dropped 11.42% after defense contractor announced it’s offering $750 million in common stock and $600 million in convertible senior notes to pay off its debt.

Diabetes device makers tumbled on the news that the government may change the reimbursement rate for glucose monitors and insulin pumps. Insulet lost 4.52%, Dexcom fell 4.25%, and BetaBionics sank 4.26%.

Stocks: The S&P 500 and the NASDAQ started the second half of the year on the wrong foot, while the Dow climbed despite investors’ trepidation about conflict in Congress. But the Senate passed its version of the big, beautiful bill this afternoon, potentially getting us one step closer to ending all the drama.

Bonds: 10-year Treasury yields fell to their lowest level in two months this morning ahead of Jerome Powell’s appearance at a central banking conference today. There, Powell demurred on the possibility of a July rate cut, reiterating his wait-and-see approach.

Safe havens: The US dollar gained ground after a terrible first half of the year, while gold rose as investors braced themselves for the big jobs report on Friday.

The S&P 500 closed within a hair of a new record yesterday marking an enormous comeback that followed the April announcement of “Liberation Day” tariffs.

Despite a persistent vibe of uncertainty related to US economic policy and geopolitics:

The S&P 500 closed less than 0.1% away from a record high which it notched in February before cratering nearly 20% in April. The index has regained ground in fits and starts since then and briefly surpassed its record in intra-day trading yesterday.

On Monday, the tech-heavy NASDAQ 100 one-upped the broader market and logged its highest-ever close. It came after President Trump said Israel and Iran agreed to a ceasefire, which eased investors’ concerns about a potential oil crisis.

According to Morning Brew, between unresolved geopolitical conflicts and President Trump’s still-unfolding tariff policies, a portfolio manager with Capital Wealth Planning, Kevin Simpson, told CNBC that he was “surprised by the magnitude of the rebound.”

Deals: Stocks popped at the open yesterday on the news that Canada has rescinded the digital services tax in order to lure the US back to the negotiating table. Meanwhile, Bloomberg reported that the EU will accept a 10% universal tariff in exchange for some key concessions.

Stocks: The S&P 500 and the NASDAQ both hit new record highs today, with the S&P 500 wrapping up its best quarter since Q4 20

The Fed: President Trump published a handwritten note asking Jerome Powell to cut interest rates, even as the White House considers new ways to replace the Fed Chair. Meanwhile, Goldman Sachs now sees the chances of the Fed cutting interest rates in September as “somewhat above 50%.”

Posted on June 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants; LLC

***

***

On May 22, 2025, the U.S. House of Representatives moved President Trump’s budget proposal forward, sending to the Senate a budget reconciliation bill (with a one-vote margin) – the One Big Beautiful Bill Act of 2025 – that renews expiring tax cuts and enacts new ones at a cost of almost $4 trillion. These costs would largely be paid for by cuts to other programs, including to federal healthcare programs, which cuts will have significant ramifications for the healthcare industry.

This Health Capital Topics article reviews the current status of the budget bill and healthcare industry implications. (Read more…)

Posted on June 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

CBOE Volatility Index

***

***

There’s a lot of confidence in markets these days, and nowhere is that more apparent than in the VIX, aka the CBOE Volatility Index, aka aka the Fear Index.

According to Brew Markets, the VIX literally measures the market’s expectation of volatility based on S&P 500 index options, but it’s become a shorthand way of quantifying investors’ fear or confidence. Any time the VIX rises above 30, it’s taken as a sign of some serious trepidation in the market—but anytime it falls below 20, the market is calm, cool, and collected.

The VIX skyrocketed to over 50 on Liberation Day as investors fretted over what tariffs meant for their portfolios, but it’s been gradually falling ever since. As the chart above shows, the VIX just fell below its key support level of 17—a mark it has failed to break below recently, and a move that underlines investors’ confidence that the good times will keep rolling.

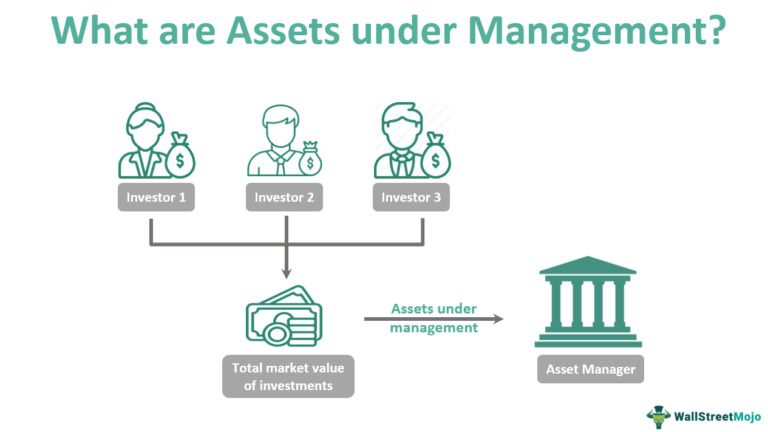

Assets under advisement refer to assets on which your firm provides advice or consultation but for which your firm does either does not have discretionary authority or does not arrange or effectuate the transaction. Such services would include financial planning or other consulting services where the assets are used for the informational purpose of gaining a full perspective of the client’s financial situation, but you are not actually placing the trade.

Assets under advisement could also be those which you monitor for a client on a non-discretionary basis, where you may make recommendations but where the client is the party responsible for arranging or effecting the purchase or sale. A common example of this AUM scenario is when an advisor reviews a participant’s 401(k) allocations. If the adviser does not have the authority or ability to effect changes in the portfolio, these assets are likely considered assets under advisement rather than regulatory assets under management.

Assets under advisement are permitted to be disclosed on Form ADV Part 2A as a separate asset figure from the assets under management. There is no requirement to disclose the assets under advisement figure, but some advisors opt to include the figure to give prospective clients a more complete picture of the firm’s responsibilities. If you choose to report your assets under advisement, be sure to make a clear distinction between this figure and your regulatory assets under management.

***

D. E. Marcinko & Associates Core Operating Values

9. We act with honesty, integrity and are always straightforward. 8. We strive to be innovative, creative, iconoclastic, and flexible. 7. We admit and learn from mistakes and don’t repeat them. 6. We work hard always as competitors are trying to catch up. 5. We treat others with dignity and respect. 4. We are the onus of consulting advice for the fiduciary well being of others. 3. We fight complacency as former success is in the past. 2. The best management styles are timeless, not timely. 1. Our clients are colleagues and always come first.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on June 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Markets: That feeling when you have a $10 trillion rally. To wit:

The S&P 500 closed at a record high this week despite a brief dip as trade tensions with Canada ratcheted up. That puts the index about 20% up from its April low, when the broad tariff announcement sent it spiraling, and up ~5% for the year.

NVIDIA also hit an all-time high, and it keeps edging closer to becoming the first company to hit a $4 trillion valuation.

Posted on June 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Deals: The US and China revealed the details of their trade deal framework, easing restrictions on rare earth metals and semiconductor chips. Commerce Secretary Howard Lutnick promised up to 10 more deals are on their way ahead of the July 9th tariff-pause deadline, but that probably won’t include Canada: President Trump ended all trade discussions with the country thanks to a dispute over the digital services tax.

Stocks: Indexes climbed at the open thanks to the deal with China, but they tumbled on news of a fallout with Canada. Still, the S&P 500 managed to post its 1,245th new all-time high, while the NASDAQ booked its own record close. The Dow trundled higher as well, though it’s still about 1,600 points below its previous record.

Posted on June 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

A June 11th report from global professional services firm Alvarez & Marsal (A&M) predicts that more beneficiaries might soon ditch insurance coverage for options like short-term, limited duration plans or healthcare sharing ministries (HCSMs), which aren’t regulated like health insurance and aren’t required to comply with ACA protections like covering maternity care or pre-existing conditions.

Nvidia extended its winning streak to five days, rising another 1.73% as the AI trade continues to recover.

EchoStar climbed 13.16% after the parent company of Dish TV disclosed that President Trump did in fact prod the FCC to make a deal.

Cyngn soared another 20.07% following a big day of gains after the company that makes self-driving tech for industrial vehicles announced a partnership with Nvidia.

Strong earnings from Nike (more on that later) propelled sporting goods stocks higher today. ONHoldings rose 1.74%, while Dick’s Sporting Goods climbed 3.59%.

Domestic power producers popped on reports that Trump is planning to issue an executive order increasing energy production to meet AI demand. Vistra gained 2.44%, GE Vernova climbed 2.54%, and Vertiv added 2.71%.

What’s down

Coinbase Global ended its winning streak, tumbling 5.77% after GENIUS Act hype propelled the crypto stock skyward all week long. Traders took profits in Circle as well, pushing the stablecoin stock down 15.54%.

Chinese EV maker LiAuto fell 1.93% on its weaker-than-expected deliveries forecast for the second quarter.

Fellow Chinese EV maker Xiaomi stunned markets with reports that it received 240,000 orders for its new SUV within 18 hours of its debut, but shares still sank 4%.

Pony.ai lost 6.31% on a report that Uber is considering helping its founder Travis Kalanick fund his acquisition of the US subsidiary of the Chinese autonomous vehicle company.

Gold miners tumbled while the price of the precious metal fell as investors took a risk-on stance. Newmont lost 4.11%, BarrickMining fell 3.44%, and KinrossGold shed 6.18%.

Today’s trade deal reopens the door for Chinese rare earth imports, bad news for US producers like MPMaterials (down 8.59%) and USA Rare Earth (down 12.14%).

Posted on June 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

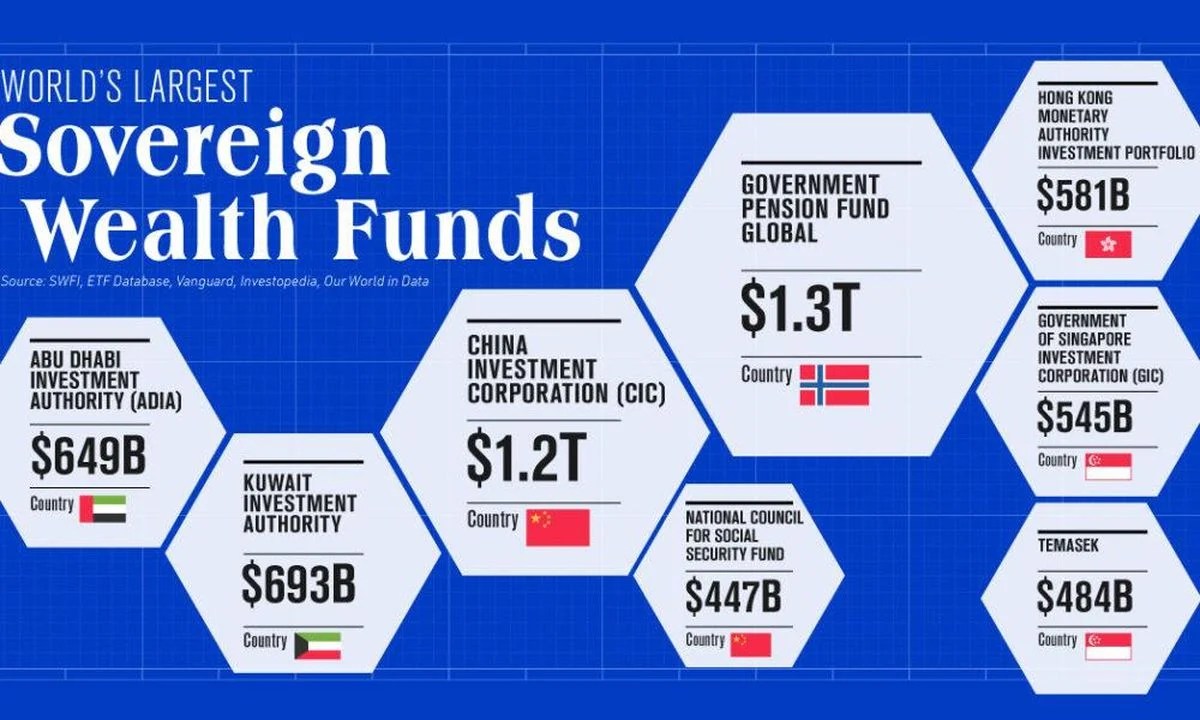

A SWF is essentially an investment fund run by the government. Similar to how a hedge fund or a private equity firm operates, the government would set aside a pot of money and invest it in assets such as stocks, bonds, startups, or real estate.

The idea of the US establishing a sovereign wealth fund akin to Norway’s or Abu Dhabi’s gained momentum recently across the political spectrum. Former President Trump endorsed the concept during a speech on his economic policy agenda for a second term, and the Biden administration has been quietly cheffing up a proposal for a wealth fund over the past several months, Bloomberg reported.

Trump and Biden officials described the fund as a key tool the country could deploy to win the global technological arms race and better compete against geopolitical rivals like China.

For example, the wealth fund could finance capital-intensive sectors such as shipbuilding, nuclear fission, and quantum cryptography that don’t offer near-term ROI for private investors.

However, disadvantages of a SWF include:

Non-Guaranteed Returns, with the Risk of Total Loss

Influence on Foreign Exchange Rates, Introducing Uncertainty

Potential Mismanagement of Funds Due to a Lack of Transparency

Dependency on Global Economic Conditions, Impacting Fund Performance

Challenges in Maintaining Accountability and Addressing Ethical Concerns

Posted on June 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BY A.I.

***

***

Stocks: The S&P 500 briefly traded a few cents above its February all-time closing high yesterday afternoon, but couldn’t sustain the gain and fell just short at the end of the day. The NASDAQ remains inches away from its record high as well.

Deals: The end of the 90-day tariff pause is less than two weeks away, but the White House said that the July 9th deadline “is not critical.”

Meanwhile, the Treasury Department is doing everything it can to make the dreaded “revenge tax” in the big, beautiful bill irrelevant.

Commodities: Gold and oil had muted moves upward but copper climbed to a three-month high after Goldman Sachs analysts warned of shortages ahead

Posted on June 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Stocks: The S&P 500 and NASDAQ started the day inches away from their all-time highs, but the market rally faltered in mid-afternoon as relief from an Israel/Iran ceasefire faded and investors turned their attention to Friday’s PCE report.

Economy: Speaking of inflation, Jerome Powell stuck to his guns during his second day of congressional testimony, endorsing a wait-and-see mentality. President Trump is apparently tired of waiting, and says he has “3 or 4” candidates in mind to replace Powell.

Commodities: Oil bounced back after posting its biggest two-day decline since 2022.

Here is a list of the most common and helpful investment terms you’ll come across and should know.

Ask. The price that someone looking to sell stock wants to receive.

Bid. The price that someone is willing to pay for stock.

Buy. To acquire shares and thereby take a position in a company.

Sell. To get rid of shares whether because you’ve reached your goal or to prevent losses.

Bull market. Market conditions in which investors expect prices to rise.

Bear market. Market conditions in which investors expect prices to fall.

Dividend. A portion of a company’s earnings paid to shareholders.

Blue chip stocks. Shares of large and well-recognized companies that have a long history of solid financial performance.

Earning per share. A company’s net profit divided by the number of outstanding common shares.

Mutual fund. A collection of investments — stocks, bonds, commodities, and more — bundled together and held in common by a group of investors.

Asset. Something you own that could generate a return in the form of more assets.

Asset allocation. Your investment strategy, essentially — the mix of assets you choose to put your money into, whether that be cash, bonds, stocks, commodities, real estate or something else.

Broker. A person or firm — or robot — that arranges transactions between buyers and sellers in exchange for a commission (that is, a fee).

Capital gain (or capital loss). The money you make (or lose) on the sale of an asset.

Diversification. Investing in a variety of sectors, such as health care, energy and IT as well as across different geographic locations.

Dow Jones Industrial Average. A price-weighted list of 30 blue-chip stocks. It’s often used to help get a sense of the overall health of the stock market, even though it only reflects a small portion of the players.

Index fund. A type of mutual fund or exchange-traded fund that allows you to invest in a portfolio that mimics a market index, which is basically a list that tracks the performance of a group of investments either for a specific sector or the overall market.

Hedge fund. A type of investment partnership. Partners pool money from investors and try out a few different investing strategies. Generally, hedge funds will make riskier investments than your typical investor. They’ll also often use leverage (that is, borrowed money) or place bets against the market to get bigger returns. They make their money by charging their investors management fees based on a percentage of their profits.

Expense ratio. The percentage-based fee that mutual fund managers charge you to manage your investments.

Market price. How much it would cost right now to buy or sell an asset or service.

Securities and Exchange Commission (SEC). An independent government body that was created to protect investors and the national banking system. The SEC enforces laws that maintain orderly, fair and efficient markets.

Short selling. A tactic available to investors who predict a stock’s price is about to drop. An investor borrows a quantity of shares through a broker and then sells them, intending to repurchase them later, at a lower price, and return them to the lender.

Stock exchange. A place buyers and sellers come together to buy, sell and trade stock during set business hours. The New York Stock Exchange (NYSE) is the most important stock exchange in the world, but there are a total of 16 exchanges around the world.

Stock market. Refers in general to the collection of markets and exchanges where the buying, selling and trading of investment vehicles takes place.

Price per share. A simple way of calculating a company’s market value at a given moment. To find the price per share, you take a company’s most recent share price and multiply it by its total number of outstanding shares.

Prospectus. A legal document that contains in-depth information about anything you might be planning to invest in: stocks, bonds or mutual funds.

Posted on June 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

SPACs, or special purpose acquisition companies, are shell companies that are created just to acquire or merge with an existing company, allowing that company to enter public markets without going through an IPO. The catch, however, is the SPAC sponsors have a small window of time—usually within two years—to find a suitable company to acquire.

Carnival popped 6.91% after the cruise line reported impressive earnings and reiterated its healthy financial guidance.

If you can’t beat ‘em, join ‘em: Mastercard rose 2.80% on the news that it will integrate Fiserv’s new stablecoin into its products. Fiserv gained 1.24%.

Lyft gained 6.09% after TD Cowen analysts upgraded the stock, calling the ride-sharing company their “Best SMIDcap Idea for 2025.”

Falling oil prices helped airline stocks soar today: Frontier Group jumped 7.56%, JetBlue Airways rose 4.15%, and American Airlines added 4.31%.

Ambarella soared 20.61% on reports that the chip designer may be exploring a sale.

Nektar Therapeutics exploded 156.29% thanks to strong results in the Phase 2 trial of its new eczema treatment.

Crypto miners rose as investors took on more risk following a ceasefire in the Middle East: CleanSpark climbed 13.45%, Riot Platforms rose 8.09%, and MARA Holdings gained 4.94%.

What’s down

Oil prices fell on news of a ceasefire between Israel and Iran, pulling oil stocks down with them: Exxon Mobil lost 3.04%, Chevron dropped 2.25%, and Occidental Petroleum fell 3.34%.

The ceasefire also sent defense contractors tumbling: Lockheed Martin lost 2.59%, RTX dropped 2.72%, and Northrup Grumman fell 3.20%.

Krispy Kreme fell 0.76% on the news that its deal with McDonald’s has fallen apart due to rising costs.

Posted on June 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Stocks: Markets rose tentatively to start the week after the US bombed three nuclear facilities in Iran over the weekend. The rally gained steam in the afternoon after Iran launched a missile strike against a US airbase in Qatar, leaving no US casualties and keeping a path to de-escalation intact.

Safe havens: The US dollar rose to its highest level in nearly a month this morning, up from a three-year low last week, as investors sought safety. Meanwhile, gold inched higher despite pressure from a stronger dollar, a sure sign of investor tension.

Crypto: Bitcoin fell dangerously close to the key support level of $100,000 before recovering later in the day as traders took a risk-on stance.

Posted on June 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Markets: Stocks climbed yesterday as oil prices fell, with investors reacting positively to what appeared to be limited retaliation from Iran in response to the US bombing its nuclear facilities over the weekend.

Meanwhile, Tesla had its biggest jump in two months following the successful, albeit limited, rollout of its robotaxi service in Austin.

Posted on June 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

As economist Jason Furman pointed out, 250 years ago the Continental Congress created a brand-new currency and authorized the printing of $2 million worth to help George Washington pay his soldiers and procure weapons and supplies for the war effort.

Markets: Until now, Wall Street has mostly shrugged off the Israel–Iran conflict in the Middle East, with the S&P 500 and NASDAQ closing just a hair lower for the week on Friday. But, investors’ thinking might—or might not—change this coming week, after the US entered the war on Saturday with strikes on key Iranian nuclear infrastructure.

And, eyes are on oil prices, which, due to the war, are having their most volatile stretch since Russia invaded Ukraine in 2022.

Consumer Fraud in the Health Insurance Marketplace

Don’t be a Victim of Consumer Fraud in the Health Care Marketplace

Beware of…

People asking for money to enroll you in Marketplace or “Obamacare” insurance. Legitimate enrollment agents will NOT ask for money.

High-pressure visits, mail solicitations, e-mails, and phone calls from people pretending to work for the government. No one should threaten you with legal action if you do not sign up for a plan. Always ask for identification if someone comes to your door.

People you did not contact who request personal information. They may be trying to steal your identity. No one from the government will call or email you to sell you an insurance plan or ask for personal identifying information. Be careful when giving out personal information, such as credit card, banking, or Social Security numbers.

Sham websites. Always look for official government seals, logos or website addresses.

Note: If you are a Medicare beneficiary, you do NOT need to buy insurance in the new Health Insurance Marketplace.

Although many academics argue that value stocks outperform growth stocks, the returns for individuals investing through mutual funds demonstrate a near match.

Introduction

A 2005 study Do Investors Capture the Value Premium? written by Todd Houge at The University of Iowa and Tim Loughran at The University of Notre Dame found that large company mutual funds in both the value and growth styles returned just over 11 percent for the period of 1975 to 2002. This paper contradicted many studies that demonstrated owning value stocks offers better long-term performance than growth stocks.

The studies, led by Eugene Fama PhD and Kenneth French PhD, established the current consensus that the value style of investing does indeed offer a return premium. There are several theories as to why this has been the case, among the most persuasive being a series of behavioral arguments put forth by leading researchers. The studies suggest that the out performance of value stocks may result from investors’ tendency toward common behavioral traits, including the belief that the future will be similar to the past, overreaction to unexpected events, “herding” behavior which leads at times to overemphasis of a particular style or sector, overconfidence, and aversion to regret. All of these behaviors can cause price anomalies which create buying opportunities for value investors.

Another key ingredient argued for value out performance is lower business appraisals. Value stocks are plainly confined to a P/E range, whereas growth stocks have an upper limit that is infinite. When growth stocks reach a high plateau in regard to P/E ratios, the ensuing returns are generally much lower than the category average over time.

Moreover, growth stocks tend to lose more in bear markets. In the last two major bear markets, growth stocks fared far worse than value. From January 1973 until late 1974, large growth stocks lost 45 percent of their value, while large value stocks lost 26 percent. Similarly, from April 2000 to September 2002, large growth stocks lost 46 percent versus only 27 percent for large value stocks. These losses, academics insist, dramatically reduce the long-term investment returns of growth stocks.

***

***

However, the study by Houge and Loughran reasoned that although a premium may exist, investors have not been able to capture the excess return through mutual funds. The study also maintained that any potential value premium is generated outside the securities held by most mutual funds. Simply put, being growth or value had no material impact on a mutual fund’s performance.

Listed below in the table are the annualized returns and standard deviations for return data from January 1975 through December 2002.

Index Return SD

S&P 500 11.53% 14.88%

Large Growth Funds 11.30% 16.65%

Large Value Funds 11.41% 15.39%

Source: Hough/Loughran Study

The Hough/Loughran study also found that the returns by style also varied over time. From 1965-1983, a period widely known to favor the value style, large value funds averaged a 9.92 percent annual return, compared to 8.73 percent for large growth funds. This performance differential reverses over 1984-2001, as large growth funds generated a 14.1 percent average return compared to 12.9 percent for large value funds. Thus, one style can outperform in any time period.

However, although the long-term returns are nearly identical, large differences between value and growth returns happen over time. This is especially the case over the last ten years as growth and value have had extraordinary return differences – sometimes over 30 percentage points of under performance.

This table indicates the return differential between the value and growth styles since 1992.

YEARLY RETURNS OF GROWTH/VALUE STOCKS

Year

Growth

Value

1992

5.1%

10.5%

1993

1.7%

18.6%

1994

3.1%

-0.6%

1995

38.1%

37.1%

1996

24.0%

22.0%

1997

36.5%

30.6%

1998

42.2%

14.7%

1999

28.2%

3.2%

2000

-22.1%

6.1%

2001

-26.7%

7.1%

2002

-25.2%

-20.5%

2003

28.2%

27.7%

2004

6.3%

16.5%

2005

3.6%

6.1%

2006

10.8%

20.6%

2007

8.8%

1.5%

2008

-38.43%

-36.84%

2009

37.2%

19.69%

2010

16.71%

15.5%

2011

2.64%

0.39%

2012

15.25%

17.50%

Source: Ibbottson.

Between the third quarter of 1994 and the second quarter of 2000, the S&P Growth Index produced annualized total returns of 30 percent, versus only about 18 percent for the S&P Value Index. Since 2000, value has turned the tables and dramatically outperformed growth. Growth has only outperformed value in two of the past eight years. Since the two styles are successful at different times, combining them in one portfolio can create a buffer against dramatic swings, reducing volatility and the subsequent drag on returns.

Assessment

In our analysis, the surest way to maximize the benefits of style investing is to combine growth and value in a single portfolio, and maintain the proportions evenly in a 50/50 split through regular rebalancing. Research from Standard & Poor’s showed that since 1980, a 50/50 portfolio of value and growth stocks beats the market 75 percent of the time.

Conclusion

Due to the fact that both styles have near equal performance and either style can outperform for a significant time period, a medical professional might consider a blending of styles. Rather than attempt to second-guess the market by switching in and out of styles as they roll with the cycle, it might be prudent to maintain an equal balance your investment between the two.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on June 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Stocks: Markets kicked off Friday trading on a high note thanks to comments from Federal Reserve Governor Christopher Waller that the central bank could lower interest rates as soon as next month.

Commodities: Oil prices tumbled at the open after President Trump pushed back his decision to involve the US in the conflict between Israel and Iran by two weeks.

Trade: Stocks gave up their early gains on reports that Japan has canceled high-level meetings with the US after President Trump told the country to spend more on defense.

A psychological paradox is a figure of speech that can seem silly or contradictory in form, yet it can still be true, or at least make sense in the context given.

This is sometimes used to illustrate thoughts or statements that differ from traditional ideas. So, instead of taking a given statement literally, an individual must comprehend it from a different perspective. Using paradoxes in speeches and writings can also add wit and humor to one’s work, which serves as the perfect device to grab a reader or a listener’s attention and/or persuade them to action, sales and closing statements. But paradoxes for the financial sector can be quite difficult to explain by definition alone, which is why it is best to refer to a few examples to further your understanding.

One good psychological paradox example is The Paradox of Thrift which suggests that while saving money is generally considered a prudent financial behavior, excessive saving during times of economic downturn can actually hinder economic recovery. When consumers collectively reduce their spending and increase their savings, it creates a decrease in aggregate demand. This reduction in demand can lead to lower production levels, job losses, and ultimately a decline in economic output. In other words, what may be individually rational behavior (financial saving) can have negative consequences for the overall economy.

The following paradoxical contradictions will help financial advisors guide clients to close more sales to the benefit of both.

____

In the intricate world of finance sales, advisors are often at the crossroads of various paradoxes that challenge client decision-making. While the journey towards financial security involves calculated strategies, it’s the nuanced understanding of paradoxes that can help the advisor close more sales.

____

But, what seems trueabout money often turns out to be false, according to colleague Finance Professor John Goodell, PhD from the University Akron:

The more we try to trade our way to profits, the less likely we are to profit.

The more boring an investment—think index funds—the more exciting the long-run performance will probably be.

The more exciting an investment—name your latest Wall Street concoction, Special Purpose Acquisition Company [SPAC] or anything crypto—the less exciting the long-term results typically are.

The only certainty is uncertainty and the only constant is change. Today’s market decline will eventually become a bull market, and today’s market leaders will eventually yield to other stocks.

Big market trends play a huge role in investment results, and yet trying to time macroeconomic cycles or guess which market sectors will outperform is a fool’s errand. Many big market rotations are set in motion by something wholly unanticipated, like a virus pandemic or a war.

To be happy when wealthy, we also need to be happy with far less money. The fact is, above a relatively modest income level, no amount of extra money will change our level of happiness. More money might even make us miserable, as many lottery winners have discovered.

The more we hate an investing trait—or any trait for that matter—the more likely it is that we’re resisting seeing that trait in ourselves. It’s what Carl Jung MD called the Shadowof Undesirable Personality Aspects that we hide from ourselves. Do prospects get irritated listening to your unsolicited financial advice? There’s a good chance that you often give unsolicited financial advice but don’t like to admit it.

The more we learn about investing, the more we realize we don’t know anything. We should just buy index funds and instead spend our time worrying about stuff we can actually control.

The more an investor is convinced he’s right, the more likely he is to be wrong. Short sellers, in particular, are likely to succumb to this paradoxical trap.

The more options we have, the less satisfied we’ll be with each one. This is the Paradox of Choice; revised. Anyone who has spent hours “optimizing” his or her portfolio knows this all too well. Its close cousin is information overload, another frustration paradox when investing.

The more afraid we are of losing money, the more likely we are to take unwitting risks that lose us money. Sitting in cash seems wise during market selloffs. But the truth is, none of us can reliably time the market. Pull up any chart of the stock market over any period longer than a decade and you’ll see that the riskiest decision is sitting in cash, which gets destroyed by inflation.

The more we think about our investments and look at our financial accounts, the more likely we are to damage our results by buying high because of greed and selling low because of fear. It can pay to look away.

ASSESSMENT

How should you respond to these financial paradoxes? As you plan for your own financial future, as well as your own client prospecting endeavors, embrace the concept of “loosely held views.”

In other words, make financial and client acquisitions plans, but continuously update your views, question your assumptions and paradoxes and rethink your priorities. Years of experience with clients certainly support the futility of trying to help them change their financial behavior by telling them what they “should” know or do.

CONCLUSION

Remember, it is far more useful to listen to client beliefs, fears and goals, and to suggest options and offer encouragement to help them discover their own path toward financial well-being. Then, incentivize them with knowledge of the above psychological paradoxes to your mutual success!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Marcinko, DE and Hetico, HR: Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2016.

Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York. 2006

Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2015.

Assets under management (AUM) is a significant parameter in the financial world. It answers financial questions like – how many investments does a company manage? What is the net value of the investments that the company manages? Finally, how many investors have trusted their assets with the company? The higher the answer to these three questions, the more glory to the company.

A wealthy investor who is not concerned by higher fees but wants maximum returns of their asset will probably choose an asset manager based on its AUM. Thus, the AUM indicates the financial performance of the firm. Also, based on the funds under management, the firm collects fees from other clients.

So, what are the investments which qualify as AUM? Any liquid asset of the investor they have entrusted the asset manager with monitoring and control. For example, bank deposits, cash balances, equity shares, bonds, mutual funds, and other investments.

What are the services an asset manager provides to their clients? The most important function is decision-making. With the constant fluctuations and rapid movements in the market, an asset manager has to make decisions about holding or selling an investment. The firm communicates with the investors and advises them about the necessary action.

Once the decision is taken, the firm acts on the decision, i.e., the investor does not have to enter the field. In addition, the asset management company will buy, sell, and make any other transactions on behalf of the investor. Finally, the firm also renders services like accounting, tax reporting, proxy voting (equity shares), client reporting, and other financial services.

What are Assets Under Advisement?

Assets under advisement refer to assets on which your firm provides advice or consultation but for which your firm does either does not have discretionary authority or does not arrange or effectuate the transaction. Such services would include financial planning or other consulting services where the assets are used for the informational purpose of gaining a full perspective of the client’s financial situation, but you are not actually placing the trade.

Assets under advisement could also be those which you monitor for a client on a non-discretionary basis, where you may make recommendations but where the client is the party responsible for arranging or effecting the purchase or sale. A common example of this scenario is when an adviser reviews a participant’s 401(k) allocations. If the adviser does not have the authority or ability to effect changes in the portfolio, these assets are likely considered assets under advisement rather than regulatory assets under management.

Assets under advisement are permitted to be disclosed on Form ADV Part 2A as a separate asset figure from the assets under management. There is no requirement to disclose the assets under advisement figure, but some advisers opt to include the figure to give prospective clients a more complete picture of the firm’s responsibilities. If you choose to report your assets under advisement, be sure to make a clear distinction between this figure and your regulatory assets under management.

Posted on June 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Stocks: Investors looked past the escalating conflict between Iran and Israel, even as President Trump mulled his options for a US intervention, and stocks rose ahead of today’s Federal Reserve meeting.

Economy: Trump called Jerome Powell “a stupid person” hours before the Fed Chair decided to keep interest rates where they were Stocks fell thanks to the Fed’s prediction that inflation will rise to 3.1% by the end of the year, above previous forecasts of 2.8%.

Commodities: Gold fell just a hair as analysts called the commodity’s top, while platinum climbed to a four-year high.

Much has been written and much has been opined on the topic of health information technology, electronic health records and medical security liability for physicians and healthcare providers in this textbook. But occasionally, we all still get lost in a wide array of acronyms, jargon and terms that are constantly changing in this ecosystem. And so, this brief glossary serves as a ready reference for those who want to know about these definitions in a quick and ready fashion.

Access control: The process of controlling the access of a user

Access security: To allow computer or healthcare network entry using ID / password / secure socket layer (SSL) encryption / biometrics, etc; unique identification and password assignments are usually made to medical staff members for access to medical information on a need-to-know basis, and only upon written authority of the owner of the data.

Access level authorization: Establishes a procedure to determine the computer or network access level granted to individuals working on or near protected health information, medical data or secure health data.

Accredited standards committee: Organization that helps develop American National Standards (ANS) for computer and health information technology; accredited by ANSI for the development of American National Standards; ASC X12N develops medical electronic business exchange controls like 835-Health Care Claim Payment/Advice and 837-Health Care Claim.

Accountability: The security goal that generates the requirement for actions of an entity to be traced uniquely to that entity. This supports nonrepudiation, deterrence, fault isolation, intrusion detection and prevention, and after-action recovery and legal action.

Accounting: Creating an historical record of who was authenticated, at what time, and how long they accessed the computer system.

Administrative simplification: The use of electronic standard code sets for health information exchange; Title II, Subtitle F of HIPAA gives HHS the authority to mandate the use of standards for the electronic exchange of health care data; to specify what medical and administrative code sets should be used within those standards; to require the use of national identification systems for health care patients, providers, payers (or plans), and employers (or sponsors); and to specify the types of measures required to protect the security and privacy of personally identifiable health care and medical information.

Alternative backup sites: Off-site locations that are used for transferring computer operations in the event of an emergency.

American Health Information Management Association: A large trade association of health information and medical data management professionals.

American Medical Informatics Association: An organization that promotes the use of electronic medical management and healthcare informatics for clinical and administrative endeavors.

American Telemedicine Association: Established in 1993 as a leading resource and advocate promoting access to medical care for patients and health professionals via telecommunications technology; membership open to individuals, companies, and other organizations with an interest in promoting the deployment of telemedicine throughout the world.

Anti-virus software: A software package or subscription service used to thwart malicious computer or network attacks, such as: Symantec®, McAfee®, Trend Micro®, Panda Software®, Sunbelt Software®, Computer Associates®, AVG® or MS-FF ®, etc.

ASC X12N: HIPAA transmission standards, specifications and implementation guides from the Washington Publishing Company; or the National Council of Prescription Drug Programs.

Assurance: Grounds for confidence that the other four security goals (integrity, availability, confidentiality, and accountability) have been adequately met by a specific implementation. “Adequately met” includes (1) functionality that performs correctly, (2) sufficient protection against unintentional errors (by users or software), and (3) sufficient resistance to intentional penetration or bypass.

Asymmetric cryptology: The use of two different but mathematically related electronic keys for secure health data and medical information storage, transmission and manipulation.

Asymmetric encryption: Encryption and decryption performed using two different keys, one of which is referred to as the public key and one of which is referred to as the private key; also known as public-key encryption.

Asymmetric key: A half of a key pair used in an asymmetric “public-key” encryption system with two important properties: (1) the key used for encryption is different from the one used for decryption, (2) neither key can feasibly be derived from the other.

Attack tree: An inverted tree diagram that provides a visual image of the attacks that may occur against an asset.

Audio teleconferencing: A multi-simultaneous dual voice communications between two parties at remote locations; two way communications between physician and patient at various locations.

Authentication: The process of verifying and confirming the identity of a user.

Availability: The security goal that generates the requirement for protection against – Intentional or accidental attempts to (1) perform unauthorized deletion of data or (2) otherwise cause a denial of service or data.

Back door: A means to access to a computer program that bypasses security mechanisms, sometimes installed by a programmer so that the program can be accessed for troubleshooting or other purposes.

Back door trojans or bots: Currently, the biggest threat to healthcare and all PC users worldwide according to the MSFT Corporation.®

Bandwidth: The amount of information that can be carried over a communications link.

Bar coding systems: Final FDA ruling issued in February 2004 that required bar codes on most prescription and non-prescription medications used in hospitals and dispensed based on a physician’s order; the bar code must contain at least the National Drug Code (NDC) number, which specifically identifies the drug; although hospitals are not required at this time to have a bar code reading system on the wards, this ruling has heightened the priority of implementing hospital-wide systems for patient-drug matching using bar codes.

Baud: A unit of digital transmission that indicates the speed of information flow. The rate indicates the number of events able to be processed in one second and is expressed as bits per second (bps). The baud rate is the standard unit of measure for data transmission capability; typical older rates were 1200, 2400, 9600, and 14,400 baud; the signaling rate of a telephone line in the number of transitions made in a second; 1/300 sec = 300 baud.

Beta test: The secondary or final stress examination of newly developed computer hardware, software or peripheral devices; site, etc.

Bibliographic database: Indexed computer or printed source of citations of journal articles and other reports in the literature; typically include author, title, source, abstract, and/or related information; MEDLINE® and EMBASE®.

Bioinformatics: The application of medical and biological science to the health information management field.

Biological Information technology: Cross industry alliance of the Microsoft Corporation to enhance the ability to use and share digital health and biomedical data.

Biometric: Personal security identity characteristics, such as a signature, fingerprints, voice, iris or retinal scan, hand or foot vein geometry, facial characteristics, hair analysis, eye, blood vessel or DNA; uses the unique human characteristics of a person as a means of authenticating.

Biometric identification: Secure identification using biometrics that identifies a human from a measurement of a physical feature or repeatable action of the individual (for example, hand geometry, retinal scan, iris scan, fingerprint patterns, facial characteristics, DNA sequence characteristics, voice prints, and hand written signature).

Biopassword: Start-up healthcare IT security pioneer of keyboarding patterns to boost online security through neural network patterns.

Bluetooth® device: Machines, like cell phone with headset, transmitting across communications channels 1 to 14, over time.

Bluetooth® technology: Wireless mobile technology standard built into millions of mobile phones, headsets, portable computers, desktops and notebooks; named after Harold Bluetooth, a 10th century Viking king; healthcare telemetry and rural data transmissions; the Bluetooth Special Interest Group (BSIG) advocates measures aimed at pushing healthcare interoperability for wireless devices and other computers designed for use in the medical field; other wireless stands include: Wi-Fi, ZigBe®, IrDA and RFID.

Buffer: A temporary storage area.

Buffer overflow: A security breach that occurs when a computer program attempts to stuff more data into a temporary storage area than it can hold

Business continuity plan: A plan that outlines the procedures to follow after a business experiences an attack on its security.

California Database Security Breach Act: A state act that requires disclosure to California residents if a breach of personal information has or is believed to have occurred.

Certification authority: An independent third-party organization that assigns digital certificates.

Chain of custody: A process that documents everyone who has had contact with or direct possession of the evidence.

Chain of trust: Suggestion that each and every covered entity and business associate share responsibility and accountability for confidential PHI.

Chain of trust agreement: Contract entered into by two business partners in which it is agreed to exchange data and that the first party will transmit information to the second party, where the data transmitted is agreed to be protected between the partners; sender and receiver depend upon each other to maintain the integrity and confidentiality of the transmitted information; multiple two-party contracts may be involved in moving information from the originator to the ultimate recipient; for example, a provider may contract with a clearing house to transmit claims to the clearing house; the clearing house, in turn, may contract with another clearing house or with a payer for the further transmittal of those same claims.

Children’s Online Privacy Protection Act: A federal act that requires operators of online services or Web sites directed at children under the age of 13 to obtain parental consent prior to the collection, use, disclosure, or display of a child’s personal information.

Cipher lock: A combination lock that uses buttons that must be pushed in the proper sequence in order to open the door.

Clearing house: HIPAA medical invoice, healthcare data transaction exchange and medical data implementation service center that that meets or exceeds Federally-mandated standardized Electronic Data Interchange (EDI) transaction requirements.

Clinger-Cohen Act: Public Law 104-106; Information Technology Management Reform Act (ITMRA) of 1996.

Clinical data: Protected Health Information (PHI) from patient, physician, laboratory, clinic, hospital and/or payer, etc; identifiable patient medical information.

Clinical data information systems: Automatic and securely connected system of integrated computers, central severs and the Internet that transmits Protected Health Information (PHI) from patient, physician, laboratory, clinic, hospital and/or payer, etc.

Clinical data repository: Electronic storehouse of encrypted patient medical information; clinical data storage.

Clinical informatics: The management of medical and clinical data; the use of computers, networks and IT for patient care and health administration.

Clinical information: All the related medical information about a patient; Protected Health Information (PHI) from patients, providers, laboratories, clinics, hospitals and/or payers or other stakeholders, etc.

Clinical information system: A computer network systems that supports patient care; relating exclusively to the information regarding the care of a patient, rather than administrative data, this hospital-based information system is designed to collect and organize data.

Clinical regional health information system: Electronic entity committed to securely share private patient health information among entities like medical providers, clinics, laboratories, hospitals, outpatient centers, hospice and other healthcare facilities; Community Health Management Information Systems (CHMIS), Enterprise Information Networks (EINs), Regional Health Information Networks (RHINs) and Health Information Networks (HINs).

Cold site: An alternative backup site that provides the basic computing infrastructure, such as wiring and ventilation, but very little equipment.

Compact disc – read only memory (CD-ROM): A computer drive that can read CD-R and CD-RW discs.

Compact disc – recordable (CD-R): An optical disc that contains up to 650 megabytes of data and cannot be changed once recorded.

Compact disc – rewriteable (CD-RW): An optical disc that can be used to record data, erase it, and re-record again.

Computer security: A computer or network that is free from threats against it.

Computerized Physician Order Entry System: Automatic medical provider electronic medical chart ordering system that usually includes seven features: medication analysis, system order clarity, increased work efficiency, point of care utilization, benchmarking and performance tracking, on-line alerts and regulatory reporting.

Confidential health information: Protected Health Information (PHI) that is prohibited from free-use and secured from unauthorized dissemination or use; patient specific medical data.

Counter signature: The ability to prove the order of application of signatures; analogous to the normal business practice of signing a document which has already been signed by another party (ASTM E 1762 -95); part of a digital signature.

Covered entity: 42 CFR § 164.504(e)(2)(i)(B). Any of three broadly defined entities that deal with protected health information (PHI): providers, individuals or group health plans, and clearinghouses.

Cracker: A person who breaks into or otherwise violates the system security with a malicious intent.

Cryptography: The science of transforming information so that it is secure while it is being transmitted or stored.

Cyber-terrorism: Attacks by a terrorist group using computer technology and the Internet to cripple or disable a nation’s electronic infrastructure.

Data backup: The process of copying data to another media and storing it in a secure location.

Data encryption standard: An older health or medical data private key cryptology federal protocol for secure information exchange; replaced by AES.

Data interchange standard: X12 HIPAA health data transmission standard format.

Data interchange standard association: The organization that provides X12 HIPAA transmission standards and formats.

Deadbolt lock: A lock that extends a solid metal bar into the door frame for extra security.

Decision support system: Computer tools or applications to assist physicians in clinical decisions by providing evidence-based knowledge in the context of patient-specific data; examples include drug interaction alerts at the time medication is prescribed and reminders for specific guideline-based interventions during the care of patients with chronic disease; information should be presented in a patient-centric view of individual care and also in a population or aggregate view to support population management and quality improvement.

Decryption: Changing an encrypted message back to its original form.

Definition files: Files that contain updated antivirus information.

De-identified health information: Protected health information that is no longer individually identifiable health information; a covered entity may determine that health information is not individually identifiable health information only if: (1) a person with appropriate knowledge of and experience with generally accepted statistical and scientific principles and methods for rendering information not individually identifiable determines that the risk is very small that the information could be used, alone or in combination with other available information, to identify an individual, and documents the methods and results of the analysis; or (2) the following identifiers of the individual, relatives, employers or household members of the individual are removed.

Denial of service: The prevention of authorized access to resources or the delaying of time critical operations.

Designated record set: Contains medical and billing records and any other records that a physician and/or medical practice utilizes for making decisions about a patient; a hospital, emerging healthcare organization, or other healthcare organization is to define which set of information comprises “protected health information” and which set does not; contains medical or mixed billing records, and any other information that a physician and/or medical practice utilizes for making decisions about a patient. It is up to the hospital, EHO, or healthcare organization to define which set of information comprises “protected health information” and which does not though logically this should not differ from locale to locale. The patient has the right to know who in the lengthy data chain has seen their PHI. This sets up an audit challenge for the medical organization, especially if the accountability is programmed, and other examiners view the document without cause.

Designated standard: HIPAA standard as assigned by the department of HHS

Device lock: A steel cable and a lock used to secure a notebook computer.

Digital certificate: A certificate that binds a specific person to a public key.

Digital imaging and communications in medicine: Technology broadband transmission imaging standards for X-rays, MRIs, CT and PET scans, etc; health IT standard transmissions platform aimed at enabling different computing platforms to share image data without compatibility problems; a set of protocols describing how radiology images are identified and formatted that is vendor-independent and developed by the American College of Radiology and the National Electronic Manufacturers Association.

Digital radiology: Medical digital imaging applied to x-rays, CT, PET scans and related non-invasive and invasive technology; broadband intensive imaging telemedicine.

Digital rights management: The control and protection of digital intellectual property.

Digital signature: Encrypted electronic authorization with verification and security protection; private and public key infrastructure; based upon cryptographic methods of originator authentication, computed by using a set of rules and a set of parameters so that the identity of the signer and the integrity of medical or other data can be verified.

Digital signature standard: Encryption technology to ensure electronic medical data transmission integrity and authentication of both sender and receiver; date and time stamps; public and private key infrastructure.

Digital versatile disc – recordable (DVD-R): An optical disc technology that can record once up to 3.95 gigabytes of data on a single-sided disc and 7.9 GB on a double-sided disc.

Digital versatile disc – rewriteable (DVD-RAM): An optical disc technology that can record, erase, and re-record data and has a capacity of 2.6 GB (single side) or 5.2 GB (double side).

Digital versatile disc (DVD): A technology that permits large amounts of data to be stored on an optical disc.

Disaster recovery plan: A process to restore vital health and/or critical healthcare technology systems in the event of a medical practice, clinic, hospital or healthcare business interruption from human, technical or natural causes; focuses mainly on technology systems, encompassing critical hardware, operating and application software, and any tertiary elements required to support the operating environment; must support the process requirements to restore vital company data inside the defined business requirements; does not take into consideration the overall operating environment; an emergency mode operation plan is still necessary.

Disclosure: Release of PHI outside a covered entity or business agreement space, under HIPAA; the release, transfer, provision of access to or divulging of medical information outside the entity holding the information.

Disc – rewriteable (DVD-RW): An optical disc technology that allows data to be recorded, erased, and re-recorded.

Due care: Managers and their organizations have a duty to provide for information security to ensure that the type of control, the cost of control, and the deployment of control are appropriate for the system being managed.

e-health: Emerging field in the intersection of medical informatics, public health and business, referring to health services and information delivered or enhanced through the Internet and related technologies; characterizes not only a technical development, but also a state-of-mind, attitude, and a commitment for networked, global thinking, to improve health care worldwide by using information and communication technology.

Electronic data interchange: Inter healthcare organization computer-to-computer transmission of business or health information in a standard format; direct transmission from the originating application program to the receiving, or processing, application program; an EDI transmission consists only of business or health data, not any accompanying verbiage or free-form messages; a standard format is one that is approved by a national or international standards organization, as opposed to formats developed by health industry groups, medical practices, clinics or companies; the electronic transmission of secure medical and financial data in the healthcare industrial complex; X12 and similar variable-length formats for the electronic exchange of structured health data. The Centers for Medicare and Medicaid Services (CMS) regulates security and Electronic Data Interchange (EDI).

Electronic data interchange standards: The American National Standards Institute (ANSI) set of EDI standards known as the X12 standards. These standards have been developed by private sector standards development organizations (SDOs) and are maintained by the Accredited Standards Committee (ASC) X12. ANSI ASC X12N standards, Version 4010, were chosen for all of the transactions except retail pharmacy transactions, which continue to use the standard maintained by the National Council for Prescription Drug Programs (NCPDP) because it is already in widespread use. The NCPDP Telecommunications Standard Format Version 5.1 and equivalent NCPDP Batch Standard Version 1.0 have been adopted in this rule (health plans will be required to support one of these two NCPDP formats). The standards are designed to work across industry and company boundaries. Changes and updates to the standards are made by consensus, reflecting the needs of the entire base of standards users, rather than those of a single organization or business sector. Specifically, the following nine healthcare transactions were required to use X12N standard electronic claim formats by October 16, 2003.

Electronic health record: A real-time patient health record with access to evidence-based decision support tools that can be used to aid clinicians in decision-making; the EHR can automate and streamline a clinician’s workflow, ensuring that all clinical information is communicated; prevents delays in response that result in gaps in care; can also support the collection of data for uses other than clinical care, such as billing, quality management, outcome reporting, and public health disease surveillance and reporting; electronic medical record.

Electronic medication administrative record: Electrical file keeping computerized system for tracking clinical medication dispensation and use; integrated with TPAs, PBMs, robotic dispensing devices and CPOEs, etc.

Electronic medical (media) claims: Usually refers to a flat file format used to transmit or transport medical claims, such as the 192-byte UB-92 Institutional EMC format and the 320-byte Professional EMC-NSF.