BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on August 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler; MSFP CFP™

***

***

This month, the U.S. government demanded a direct cut of a company’s foreign sales as the price for letting those sales happen.

Tech companies Nvidia and AMD had been stuck in regulatory limbo over selling their newest AI chips to China. According to an August 12, 2025, Reuters article by Karen Freifeld, Nvidia CEO Jensen Huang had even received a public “green light” for the company’s H20 chip, but the Commerce Department would not issue the export licenses.

The stalemate ended only after Huang met with President Trump and agreed to a deal: the licenses would be granted, but the U.S. Treasury would get 15% of all H20 revenue from China. AMD agreed to identical terms for its MI308 chip. Two days later, both companies had their licenses.

The numbers are staggering. Bernstein Research estimates Nvidia could sell $15 billion worth of H20 chips in China this year, and AMD about $800 million of MI308s. That is more than $2 billion flowing straight to Washington, not as taxes but as a contractual price for market access. The legality of this arrangement is questionable, and the deal also raises security concerns.

It is worth noting the administration first asked for 20% before “settling” on 15%. This was not a polite request but a “take it or leave it” demand. From a behavioral economics standpoint, the decision was predictable. The pain of losing an entire market is far greater than the pain of losing a fraction of it.

How is this any different from a tariff? A tariff is a standardized, legally defined tax that applies broadly to certain goods and is collected under public trade policy. This 15% cut is a one-off, privately negotiated condition aimed at just two companies, tied to export license approval. It is taken from gross revenue, not profit, meaning the government gets paid on every dollar of sales before the companies cover a single expense.

“Tax farmming” is an old practice where the state sold the right to collect taxes for a fixed sum, allowing the collectors to keep the rest. Its use in France made some people enormously rich, made everyone else furious, and eventually helped spark the French Revolution. Similar systems appeared in Ottoman Egypt, Qing China, and the early Dutch Republic until abuses finally brought them down.

The Nvidia/AMD deal is not exactly tax farming, but it is a similar dynamic. The government’s role is no longer just regulating. It is stepping in as a business partner, taking a direct share of private sales. Supporters might call it a smart use of national leverage. Critics will see a step away from free-market capitalism toward something more political and transactional.

Nor is this deal a one-off. In June, the administration approved foreign investment in U.S. Steel only after securing a “golden share” that gives it veto power over strategic corporate decisions. History teaches us that once a government finds a way to take a cut, it rarely stops with one sector. Today it is steel and AI chips to China. Tomorrow it could be pharmaceuticals, energy, or consumer goods.

What is the likely impact for average Americans? Money flowing to the U.S. Treasury from a source other than taxpayers may seem like a benefit. Yet any company required to give away 15% of its gross revenue, which could equal its entire profit, has to compensate in some way. The most likely result is higher prices. Hiking prices on computer chips sold to China may not seem to be a big deal—until you consider that many of the products that use those chips are sold to U.S. consumers.

Posted on August 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

Stocks: The final trading day of the summer was bad as a selloff in technology stocks took indexes down from recent all-time highs.

Fed drama: A judge did not issue a ruling on Fed Governor Lisa Cook’s bid for a temporary restraining order against President Trump, delaying it a few more days and leaving Cook in limbo.

Commodities: Gold hit a new all-time high as traders worried about the possibility of the Federal Reserve losing its independence.

A silent, non-directed, ghost, blind, faux, or “mirror” PPO, HMO, or other provider model is not really a formalized managed care organization [MCO] at all. Rather, it was simply an intermediary attempt, and Ponzi-like scheme, to negotiate practitioner fees downward, by promising a higher volume of patients in exchange for the discount.

Of course, the intermediary [discount-broker] then resells the packaged contract product to any willing insurance company, HMO, PPO or other payer, thereby pocketing the difference as a nice profit. Sometime, these virtual organizations are just indemnity companies in disguise.

NOTE: The term indemnity insurance refers to an insurance policy that compensates an insured party for certain unexpected damages or losses up to a certain limit—usually the amount of the loss itself. Insurance companies provide coverage in exchange for premiums paid by the insured parties.

These policies are commonly designed to protect professionals and business owners when they are found to be at fault for a specific event such as misjudgment or malpractice. They generally take the form of a letter o indemnity.

***

As part of a silent PPO scheme, insurers try to pass off the discount as legitimate on Explanation of Benefit [EOB] forms. Physicians should not fall for this ploy, since pricing pressure will be forced even lower in the next round of “real” PPO negotiations!

Medical providers should also be on guard for silent HMOs, MCOs and any other silent insurance variation, since these virtual organizations do not exist, except as exploitable arbitrage situations for the middleman.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Types of investments

Once a physician [MD, DO, DPM or DDS] has a brokerage account, the young doctior will need to decide what to invest in. There are lots of options, and each comes with different benefits and drawbacks. Here are some of the most common options for new physician investors.

Stocks are the first thing most people think about when they are considering investing, but they are not the only option. The prices of stocks change daily, sometimes by large amounts, as the market adjusts to news and various cycles. For that reason, it’s important to do your research. If you’re just beginning with a retirement account, you could also consider the longer-term products listed below.

Index funds and mutual funds.

Index funds attempt to replicate the performance of an un-managed market index. The performance of mutual funds [open and closed] varies. You can often get involved for a lower initial investment, and they can provide good diversification,which makes your portfolio better equipped to handle market fluctuations [active and passive].

For that reason, many financial experts say they should form the core of your retirement portfolio. While they have many similar characteristics, there are important differences. Read more about some of the differences in index funds and mutual funds.

These technically aren’t investment products; they are a contract between you and an insurance company. However, they work to accomplish a similar goal. There are immediate annuities that convert some of your existing savings into lifetime payments, but if we’re talking about saving for retirement, a deferred income annuity is the closest comparison. You make premium payments into the deferred annuity on a regular or irregular basis depending on the contract terms, and when you reach retirement age, you annuitize those savings and receive payments for the rest of your life. They can make a valuable addition to a retirement savings strategy.

Other investments.

There are many other types of investments and financial vehicles: bonds [local, state or US], money market funds, certificates of deposit through a brokerage account or investment apps. Even the cash value of life insurance can play a part. They are all designed to address different needs and have benefits and drawbacks and may be important to your overall strategy.

Crypto.com is a cryptocurrency company based in Singapore that offers various financial services, including an app, exchange, and noncustodial DeFi wallet, NFT marketplace, and direct payment service in cryptocurrency. As of 2024, the company reportedly had more than 100 million customers and more than 4,000 employees.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The so-called money factor (abbreviated as MF on invoices) is a number in a decimal form that dealers use to calculate the APR of a car lease. It’s a major part of your monthly payment and dealers are known to jack up the money factor to pad their profits.

Most doctors don’t ask to see it because they’re not aware of it or don’t know how to calculate it. Ask to see the money factor, then multiply it by 2,400.

For example, if the money factor is .00150, you multiply it by 2,400 to get 3.6%. If that’s higher than the prevailing rate, you have room to talk them down.

How to reduce it

So how do you get a good interest rate when you lease a vehicle? The same way you do when borrowing for any other reason, whether it’s buying a home or applying for a personal loan: by having good credit. This may reduce your interest rate because you’ll represent a lower risk to a lender.

A high residual value on the car could also help you get a better interest rate. A higher residual value means you’d have lower monthly payments because there would be less depreciation on the vehicle. Since interest is applied to your monthly payment, a lower monthly payment would equate to reduced interest charges.

The money factor is one of the many numbers you may want to learn about when leasing a car. It’s one of the transactional costs that come with leasing, and allows dealers and finance companies to make a profit on every lease they execute. As a consumer, it’s a smart idea to learn the financial implications of this number and how it’ll affect your overall costs over the course of a multi-year lease.

***

***

If the interest rate is too high, you may need to shop around for a better rate, negotiate with the dealer or lender to lower the money factor, or consider leasing another vehicle that’s more in line with your budget. Either way, make sure you explore all your financial options before taking a car off the lot.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

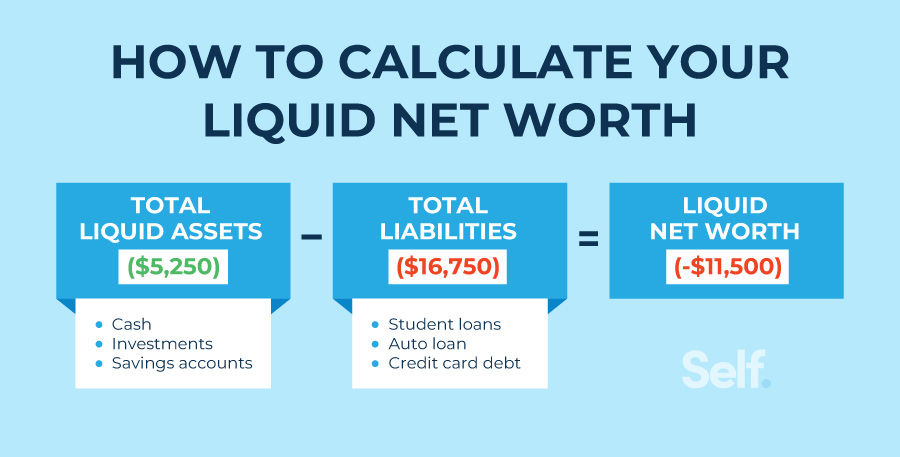

Net worth is everything you own of significance (Assets) minus what is owed in debts (Liabilities). Assets include cash and investments, real estate, cars and anything else of value.

How is net worth calculated? Assets – Debt = Net Worth. Net worth is calculated by adding all owned assets (anything of value) and then subtracting all of your liabilities.

Is net worth yearly? No, net worth is not yearly. Net worth isn’t inherently yearly but is often tracked on an annual basis to assess financial progress year over year.

What net worth is considered wealthy, rich and upper class? In the U.S. salary average is around $59,000, and only 20% of Americans have a household income of $100,000 or more.

Is net worth the same as net income? No, net worth is not the same as net income. Net income is what you actually bring home after taxes and payroll deductions, like Social Security and 401(k) contributions.

Can one measure their net worth if they don’t have many assets or a high income? Yes. Knowing your net worth isn’t about the amount you have; it’s about understanding your financial position. It helps you track your progress, informs your financial decisions, and motivates you to improve your financial health, regardless of where you start.

Stocks: The stock markets rose today after Jerome Powell opened the door to interest rate cuts. The Dow soared to a new all-time high, while small-cap stocks in the Russell 2000 had a banner day.

Bonds: Yields fell while the chances of a rate cut after the Fed’s next meeting in September rose to 83%.

Commodities: Gold rose on rate cut hopes while oil fell as peace talks between Ukraine and Russia stalled. But the biggest winner is coffee: prices have risen for six straight days to cap off its biggest weekly gain since 2021.

A SPECIAL MEDICAL-EXECUTIVE-POST GUEST PRESENTATION

***

What Is a Special Purpose Vehicle (SPV)?

A special purpose vehicle is a subsidiary created by a parent company to isolate financial risk. It’s also called a special purpose entity (SPE). Its legal status as a separate company makes its obligations secure even if the parent company goes bankrupt. A special purpose vehicle is sometimes referred to as a bankruptcy-remote entity for this reason.

These vehicles can become a financially devastating way to hide company debt if accounting loopholes are exploited, as seen in the 2001 Enron scandal.

Posted on August 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Technology: Fears of an A.I. bubble continue to climb after MIT published a report that 95% of companies using generative A.I. programs have nothing to show for it, despite pouring billions of dollars into this space.

Stocks: Another day of technology stocks selling off pulled the S&P 500 and NASDAQ lower yesterday, with investors rotating out of some of the hottest names and sectors in the market.

FOMC Drama: President Trump demanded the resignation of Fed Governor Lisa Cook for allegations of mortgage fraud. Meanwhile, the minutes from the July FOMC meeting revealed a growing divide between central bankers.

US government mulls 10% stake in Intel as Softbank invests $2b.

According to Morning Brew, Bloomberg and the Wall Street Journal reported recently that the government is considering becoming one of the beleaguered chipmaker’s biggest shareholders by converting grants the company was given under the Biden-era Chips Act into an equity stake.

At Intel’s current valuation, a 10% stake would be worth ~$10.5 billion—though the exact size of the stake and whether the government will move forward with the plan remains to be determined.

Meanwhile, over in the private sector, Softbank agreed to buy $2 billion worth of Intel stock, giving it a ~2% stake. Intel has been trying to turn itself around after losing ground to other semiconductor companies

Posted on August 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

In today’s dynamic economic landscape, the concept of a “side hustle” has evolved from a mere trend to an essential component of personal financial strategy for many individuals; even doctors.

A side hustle is a way to earn extra income outside of your primary job or main source of employment. It typically involves part-time work, freelancing, small businesses, or gig-based activities that can be pursued flexibly in your free time. Unlike traditional employment, side hustles often offer more autonomy, creative freedom, and the potential to monetize skills, hobbies, or passions.

***

***

Doctor Gigs?

So, if you’re a doctor, dentist or podiatrist considering a side hustle, focus on something sustainable and long-term. Ask yourself: What am I already good at? What do people already ask me to help with? The best side hustles don’t require reinventing the wheel — just monetizing the one you’ve already been pushing uphill.

But, avoid gigs that require a huge upfront investment or promise overnight success. Instead, look for something that offers flexibility, ideally something that works with your schedule, not against your sanity.

Track your earnings and how much time you’re putting in. Side income should support your goals, whether that’s paying off debt, saving for a trip or just breathing easier when office rent comes due.

But, if it’s draining your energy from your medical practice with little to show for it, it might be time to rethink the hustle.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

A Supply Chain Management Strategy

By Staff Reporters

***

***

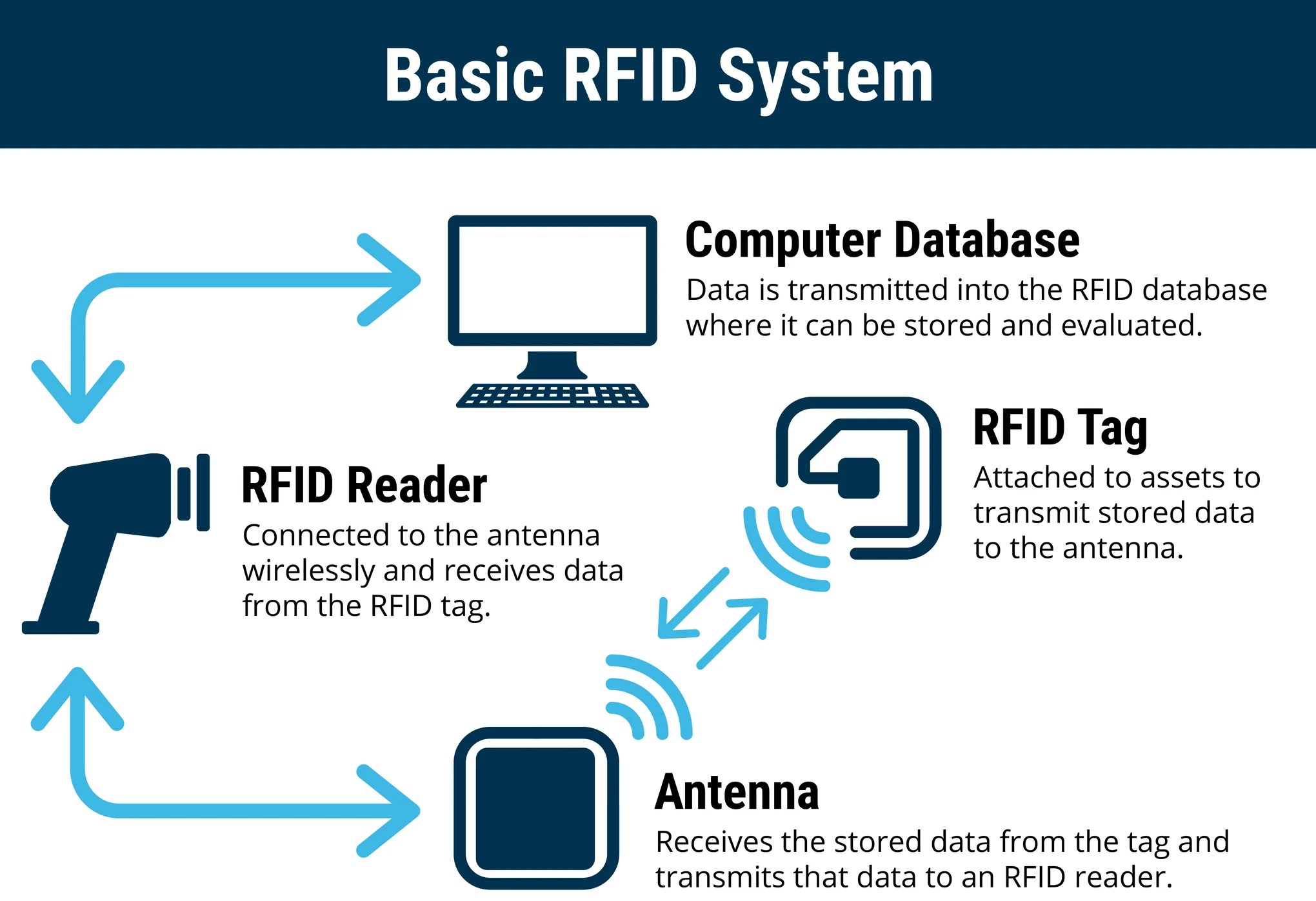

RADIO FREQUENCY IDENTIFICATION

RFID refers to a device attached to an object that transmits data to an RFID receiver. A device can be a large piece of hospital hardware the size of a small book like those attached to ocean containers, or a very small device inserted into a label on a package. RFID has advantages over bar codes such as the ability to hold more data, and to change the stored data as processing occurs. Moreover, it does not require line-of-sight to transfer data, and is very effective in harsh environments where bar-code labels will not work. RFID is not without its own problems, however, as RF signals can be compromised by materials such as metals and liquids.

Although RFID technology is receiving much current attention, it still tends to be cost-prohibitive for some hospital inventory tracking applications. As chip prices go down, there will be continued growth in the application of RFID, but, as in the case of 2D bar codes, many hospital warehouse applications simply do not require this added functionality. The low-cost 1D bar code may continue to be the technology of choice for many hospital inventory tracking applications in the short term.

Smart labels are labels with integrated RFID chips. The idea is to produce labels (probably with bar codes) as well as programming the RFID chips embedded in the label. This would provide all current functionality (human- and machine-readable text and bar codes) as well as adding RFID functionality.

Slap-and-ship describes an approach to complying with vendor requirements for physical identification of shipped goods. More recently, slap-and-ship has been used to describe complying With RFID requirements (such as those from large health care systems); however, it is also applicable to any compliance labeling requirement (such as compliance bar-code labels). Slap-and-ship implies meeting the customer’s requirement by applying the bar-code labels or RFID tags, but not utilizing the technology internally.

Finally, anti-skimming bills were first approved by California and Washington State relative to RFID privacy and are focused on making it illegal for criminals or businesses (or criminal businesses) to read and use personal information from RFID-enabled items such as driver’s licenses and credit cards without the owner’s consent.

UnitedHealth Group soared almost 12%, its biggest one-day gain in nearly five years, after getting the “Buffett Bounce.” Buffett’s Berkshire Hathaway revealed it bought ~5 million shares worth nearly $1.6 billion, giving a much-needed vote of confidence to the struggling health giant.

The White House is considering buying part of Intel, Bloomberg reported this week, which would be the latest big business deal the president pursues on behalf of the government. The Trump administration might acquire a stake in the struggling computer chip-maker using CHIPS Act funding—nearly $11 billion of which was already earmarked for Intel.

Saudi Arabia’s Public Investment Fund took an $8 billion write-down on five mega-projects it’s building, due to lower oil prices and higher costs.

Pimco, the asset management giant, warned that President Trump’s plan to IPO Fannie Mae and Freddie Mac could push mortgage rates higher.

Posted on August 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: The Dow climbed thanks to UnitedHealth and Warren Buffett while the rest of the market sank as the stock rally slowed. But, despite Friday’s decline, both the S&P 500 and NASDAQ wrapped up winning weeks.

Bonds: Both 10-year and 2-year Treasury yields continued to climb after Thursday’s PPI reading and Friday’s consumer confidence and retail sales data.

Commodities: All eyes were on Anchorage, Alaska as President Trump concluded talks with President Putin—discussions that will be crucial for crude’s future.

An important component of hospital credit analysis is essentiality. Hospitals are unusual businesses that many times possess some form of essentiality to their communities. Health care is important to the economic vitality of every community. Many hospitals have served their communities for many years; it is not uncommon to find hospitals that have been continuously operating for more than 100 years in the same community.

Most hospitals are not-for-profit. In not-for-profit hospitals, no private party actually “owns” the hospital; control is vested in various boards, but no one explicitly owns a not-for-profit hospital. In a broad sense, communities own not-for-profit hospitals. They are considered “charities” with a “charitable purpose.” Though a not-for-profit hospital may not have owners, it has many “stakehold-ers,” parties that have vested interests in the continuing success of the hospital.

Many hospitals have broad and vast webs of stakeholders. Stakeholders are why hospitals rarely close or are shut down. Too many stakeholders have interests in the continuing successful operation of hospitals.

Another dimension of the essentiality analysis is service analysis. How significant are the hospital’s services? If the hospital shuts down, what population segments would suffer? How significant is the population that would suffer? How much would they suffer?

And so, hospital stakeholder relationships need to be considered in the analysis of essentiality. How strong are these relations? How many are there? How important is the continuing success of this hospital to these stakeholders?

Analysis of hospital’s stakeholders and services should provide a credible view of the degree of essentiality associated with a hospital. Higher degrees of essentiality suggest higher likelihoods that hospitals, one way or another, will meet their commitments, particularly their payment commitments.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

According to Wikipedia, Phantom debt or zombie debt is a debt that is old, defaulted, or not owed and is somehow still being pursued for collection to be paid by the presumed debtor. It generally refers to debt that is more than 3 years old, is long forgotten about or belonged to someone else – like someone with the same name or a deceased parent. The amount owed can grow to hundreds or thousands of dollars more than what was originally owed.

An example of this is from George Miller. George missed an 11 cent Verizon bill and seven years later it had grown to $4,000.00.

Sometimes it was never owed, was owed by a deceased parent, or that was previously owed by the presumed debtor, but was previously paid in full, settled, discharged via bankruptcy or a dismissed court case, is beyond the statute of limitations, or is otherwise not legally collectible, but that a collection agency or other similar service is aggressively attempting to collect, often fraudulently.

While the concept of phantom debt is quite old, it has gotten a lot of attention since the 1990s.

Very often, collectors of phantom debt use intimidating, abusive, or otherwise illegal tactics in an attempt to collect phantom debt that include frequent phone calls, calls to the victim’s place of employment, or threats of scary consequences against the victim that sometimes include arrest and/or criminal prosecution. In the USA, such tactics violate the Fair Debt Collection Practices Act [FDCPA]

The source of phantom debt may be from collectors who buy the debt from other collectors for pennies on the dollar, some of which take action that is not legal in order to collect that debt. Unlawful techniques used include suing or threatening to sue, re-aging the debt on the victim’s credit report to circumvent limits on reporting, or falsely promising to remove a negative credit report entry in exchange for a partial payment.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets struggled to pick a direction as investors took a wait-and-see approach ahead of today’s CPI reading—even as Wall Street worries about the data’s reliability.

Trade: President Trump asked China, the world’s largest soybean buyer, to quadruple its soybean purchases from the US. He also extended the trade war truce with China by 90 days

Commodities: Gold had its worst day in three months as traders waited for the White House to clarify its new tariffs on the key commodity—only for Trump to announce that it won’t be tariffed at all. Meanwhile, Chinese battery giant CATL halted operations at a mine that produces 4% of the world’s lithium, sending prices of the precious metal soaring.

Posted on August 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On July 2, 2025, the Department of Justice (DOJ) and Department of Health & Human Services (HHS) announced during the American Health Law Association (AHLA) Annual Meeting that the agencies have reestablished a Working Group to “strengthen” their ongoing collaboration, specifically as relates to the False Claims Act (FCA).

This Health Capital Topics article discusses the Working Group’s priorities and the implications for providers. (Read more…)

Posted on August 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.and Staff Reporters

***

***

President Trump is set to sign an executive order allowing alternative assets such as cryptocurrency, private equity investments, and real estate in 401(k) accounts. Those accounts are a veritable gold mine—Americans have stashed approximately $12.5 trillion away for retirement, and alternative asset managers have been chomping at the bit to get a piece of that pie.

According to Brew Markets, the changes have been a long time coming. All the way back in his first term, Trump ordered the Labor Department to review how to incorporate private equity investments into retirement accounts, an effort that was later reversed under President Biden. This latest move expands beyond private equity, coinciding with Trump’s push to bring crypto mainstream.

Proponents argue that alternative assets in 401(k) accounts will enhance investment diversification and could provide retirees with greater profits. Detractors note that these assets are less liquid, less transparent, and generally more risky than investing retirement funds into publicly traded stocks and bonds.

Trump says pharma tariffs could be as high as 250%

The president revealed that he plans to formally announce tariffs on the pharmaceutical industry “within the next week or so” in an attempt to force drug manufacturing to the US, he told CNBC several days ago.

In the early 1980s, Daniel Kahneman and Amos Tverskey proved in numerous experiments that the reality of decision making differed greatly from the assumptions held by economists. They published their findings in Prospect Theory: An analysis of decision making under risk, which quickly became one of the most cited papers in all of economics.

To understand the importance of their breakthrough, we first need to take a step back and explain a few things. Up until that point, economists were working under a normative model of decision making. A normative model is a prescriptive approach that concerns itself with how people should make optimal decisions. Basically, if everyone was rational, this is how they should act.

Amanda, an RN client, was just informed by her financial advisor that she needed to re-launch her 403-b retirement plan. Since she was leery about investing, she quietly wondered why she couldn’t DIY. Little does her Financial Advisor know that she doesn’t intend to follow his advice, anyway! So, what went wrong?

The answer may be that her advisor didn’t deploy a behavioral economics framework to support her decision-making. One such framework is the “prospect theory” model that boils client decision-making into a “three step heuristic.”

According to colleague Eugene Schmuckler PhD MBA MEd CTS, Prospect theory makes the unspoken biases that we all have more explicit. By identifying all the background assumptions and preferences that clients [patients] bring to the office, decision-making can be crafted so that everyone [family, doctor and patient] or [FA, client and spouse] is on the same page.

1. Simplify choices by focusing on the key differences between investment [treatment] options such as stock, bonds, cash, and index funds.

2. Understanding that clients [patients] prefer greater certainty when it comes to pursuing financial [health] gains and are willing to accept uncertainty when trying to avoid a loss [illness].

3. Cognitive processes lead clients and patients to overestimate the value of their choices thanks to survivor bias, cognitive dissonance, appeals to authority and hindsight biases.

CITE: Jaan E. Sidorov MD [Harrisburg, PA]

Assessment

Much like in healthcare today, the current mass-customized approaches to the financial services industry fall short of recognizing more personalized advisory approaches like prospect theory and assisted client-centered investment decision-making.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

THE ADDICTIVE INVESTING / TRADING PERSONALITY OF DOCTORS

Dr. Donald J. Mandell, a pediatrician, always needs to leave the office fifteen minutes ahead of schedule. The reason is because it takes that long to make the necessary number of trips to ensure the front door is truly locked.

Dr. Kamela A. Shaw, a general surgeon, is constantly rushing to the bath room so that she can wash her hands. As far as she is concerned, it is not possible to get one’s hands clean enough considering the COVID pandemic or recent influenza outbreak.

Although the behaviors displayed by these two doctors are different, they are consistent in that each, to some degree, display behavior that might be called an obsessive-compulsive disorder [OCD].

An obsession is a persistent, recurring preoccupation with an idea or thought. A compulsion is an impulse that is experienced as irresistible.

Obsessive-compulsive individuals feel compelled to think thoughts that they say they do not want to think or to carry out actions that they say are against their will. These individuals usually realize that their behavior is irrational, but it is beyond their control. In general, these individuals are preoccupied with orderliness, perfectionism, and mental and interpersonal control, at the expense of flexibility, openness, and efficiency. Specifically, behaviors such as the following may be seen:

Preoccupation with details.

Perfectionism that interferes with task completion.

Excessive devotion to work and office productivity.

Scrupulous and inflexible about morality (not accounted for by cultural or religious identification);

Inability to discard worn-out or worthless objects without sentimental value;

Reluctance to delegate tasks or to work with others.

Adopts a miserly spending style toward both self and others.

Demonstrates a rigid, inflexible and stubborn nature.

Most people resort to some minor obsessive-compulsive patterns under severe pressure or when trying to achieve goals that they consider critically important. In fact, many individuals refer to this as superstitious behavior. The study habits required for medical students entail a good deal of compulsive behavior.

As the above examples suggest, there are a variety of addictions possible. Recent news accounts have pointed out that even high-level governmental officials can experience sex addiction. The advent of social-media has led to what is referred to as Internet addiction where an individual is transfixed to a computer, tablet PC or smart-phone, “working” for hours on end without a specific project in mind. The simple act of “surfing”, “tweeting-X”, “texting” or merely posting opinions offers the person afflicted with the addiction some degree of satisfaction.

Still another form of addictive behavior is that of the individual with gambling disorder (GD).

GD is recognized as a mental disorder in the American Psychiatric Association’s Diagnostic and Statistical Manual of Mental Disorders-V. This is the behavior of an individual who is unable to resist the impulse to gamble. Many reasons have been posited for this type of behavior including the death instinct; a need to lose; a history of trauma; a wish to repeat a big win; identification with adults the “gambler” knew as an adolescent; and a desire for action and excitement. There are other explanations offered for this form of compulsive behavior. The act of betting allows the individual to express an immature bravery, courage, manliness, and persistence against unfavorable odds. By actually using money and challenging reality, he puts himself into “action” and intense emotion. By means of gambling, the addicted individual is able to pretend that he is favored by “lady luck,” specially chosen, successful, able to beat the system and escape from feelings of discontent.

Greed can also have addictive qualities. In fact, a poll conducted by the Chicago Tribune revealed that folks who earned less than $30,000 a year, said that $50,000 would fulfill their dreams, whereas those with yearly incomes of over $100,000 said they would need $250,000 to be satisfied. More recent studies confirm that goals keep getting pushed upward as soon as a lower level is reached.

Edward Looney, executive director of the Trenton, New Jersey based Council on Compulsive Gambling (CCG) reports that the number of individuals calling with trading-associated problems is doubling annually. In the mid 1980s, when the council was formed, the number of people calling the council’s hotline (1 – 800 Gambler) with stock-market gambling problems was approximately 1.5 percent of all calls received. In 1998 that number grew to 3 percent, and rose to 8 percent by 2012. Today, that number is largely unknown because of its pervasiveness, but Dr. Robert Custer, an expert on compulsive gambling reported, that stock market gamblers represent over 20 percent of the gamblers that he has diagnosed. It is evident that on-line trading presents a tremendous risk to the speculator.

The CCG describes some of the consequences:

Dr. Fred B. is a 43-year-old Asian male physician with a salary above $150,000 and in debt for more than $150,000. He is married with two children. He was a day trader.

Michael Q. is a 28-year-old Hispanic male registered nurse. He is married and the father of one (7 month old) child. He earns $65,000 and lost $50,000 savings in day trading and is in debt for $30,000. He has suicidal ideation.

[B] A Question of Suitability

Since online traders are in it for many reasons, investment suitability rarely enters the picture, according to Stuart Kaswell, general counsel of the Securities Industry Association, in Washington, DC. The kind of question that has yet to be confronted, by day or online trading firms, is a statement, such as: “Equities look good this year. We favor technology stocks. We have a research report on our Web page that looks at the social media industry.” Those kinds of things are seldom considered because they do not involve a specific recommendation of a specific stock, like Apple, Google, Groupon, Facebook or Twitter.

However, if a firm makes a specific recommendation to an investor, whether over the cell-phone, iPad®, fax machine, face-to-face, instagram or over the Internet, or Twitter-X, suitability rules should apply. Opining similarly on the “know your customer” requirements is Steven Caruso, of Maddox, Koeller, Harget & Caruso of New York City. “The on-line firms obviously claim that they do not have a suitability responsibility because they do not want the liability for making a mistake as far as determining whether the investor was suitable or buying any security. I think that ultimately more firms are going to be required to make a suitability, [or eventually fiduciary] determination on every trade”.

[C] On-line Traders and Stock Market Gamblers

Some of the preferred areas of stock market gambling that attract the interest of compulsive gamblers include options, commodities, penny stocks and bit-coins, index investing, new stock offerings, certain types of CAT bonds, crowd-sourcing initiatives, and some contracts for government securities. These online traders and investment gamblers think of themselves as cautious long-term investors who prefer blue chip or dividend paying varieties. What they fail to take into consideration is that even seemingly blue chips can both rise and precipitously drop in value again, as seen in the summer of 2003, the “crash” of 2008, or the “flash crash” of May 6, 2010. On this day, the DJIA plunged 1000 points (about 9%) only to recover those losses within minutes. It was the second largest point swing 1,010.14 points, and the biggest one-day point decline, 998.5 points, on an intraday basis in Dow Jones Industrial Average history.

Regardless of investment choice, the compulsive investment gambler enjoys the anticipation of following the daily activity surrounding these investments. Newspaper, hourly radio and television reports, streaming computer, tablet and smart phone banners and hundreds of periodicals and magazines add excitement in seeking the investment edge. The name of the game is action. Investment goals are unclear, with many participating simply for the feeling it affords them as they experience the highs and lows and struggles surrounding the play. And, as documented by the North American Securities Administrators Association’s president, and Indiana Securities Commissioner, Bradley Skolnik, most day or online traders lose money. “On-line brokerage was new and cutting edge and we enjoyed the best stock market in generations, until the crashes. The message of most advertisements was “just do it”, and you’ll do well. The fact is that research and common sense suggest the more you trade, the less well you’ll do”.

Most day or online traders are young males, some who quit their day jobs before the just mentioned debacles; or more recently with the dismal economy. Many ceased these risky activities but there is some anecdotal evidence that is re-surging again with 2013-14 technology boom and market rise. Most of them start every day not owning any stock, then buy and sell all day long and end the trading day again without any stock – – just a lot of cash. Dr. Patricia Farrell, a licensed clinical psychologist states that day traders are especially susceptible to compulsive behaviors and addictive personalities. Mark Brando, registered principal for Milestone Financial, a day trading firm in Glendale, California states, “People that get addicted to trading employ the same destructive habits as a gambler. Often, it’s impossible to tell if a particular trade comes from a problem gambler or a legitimate trader.”

Arthur Levitt, former Chairman of the Securities and Exchange Commission (SEC) in discussing the risks and misconceptions of investing are only amplified by on-line trading. In a speech before the National Press Club a few years ago, he attempted to impress individuals as to the risks and difficulties involved with day trading. Levitt cited four common misconceptions that knowledgeable medical professionals, and all investors, should know:

Personal computers, tablets, mobile devices and smart-phones are not directly linked to the markets – Thanks to Level II computer software, day traders can have access to the same up-to-the-second information available to market makers on Wall Street. “Although the Internet makes it seem as if you have a direct connection to the securities market, you don’t. Lines may clog; systems may break; orders may back-up.”

The virtue of limit orders – “Price quotes are only for a limited number of shares; so only the first few investors will receive the currently quoted price. By the time you get to the front of the line, the price of the stock could be very different.”

Canceling an order – “Another misconception is that an order is canceled when you hit ‘cancel’ on your computer. But, the fact is it’s canceled only when the market gets the cancellation. You may receive an electronic confirmation, but that only mean your request to cancel was received – not that your order was actually canceled”.

Buying on margin – “if you plan to borrow money to buy a stock, you also need to know the terms of the loan your broker gave you. This is margin. In volatile markets, investors who put up an initial margin payment for a stock may find themselves required to provide additional cash if the price of the stock falls.

How then, can the medical professional or financial advisor tell if he or she is a compulsive gambler? A diagnostic may be obtained from Gamblers Anonymous. It is designed to screen for the identification of problem and compulsive gambling.

But, it is also necessary to provide a tool to be used by on-line traders. This questionnaire is as follows:

1. Are you trading in the stock market with money you may need during the next year?

2. Are you risking more money than you intended to?

3. Have you ever lied to someone regarding your on-line trading?

4. Are you risking retirement savings to try to get back your losses?

5. Has anyone ever told you that spend too much time on-line?

6. Is investing affecting other life areas (relationships, vocational pursuits, etc.)?

7. If you lost money trading in the market would it materially change your life?

8. Are you investing frequently for the excitement, and the way it makes you feel?

9. Have you become secretive about your on-line trading?

10. Do you feel sad or depressed when you are not trading in the market?

NOTE: If you answer to any of these questions you may be moving from investing to gambling.

***

***

The cost of compulsive gambling and day trading is high for the individual medical or lay professional, the family and society at large. Compulsive gamblers, in the desperation phase of their gambling, exhibit high suicide ideation, as in the case of Mark O Barton’s the murderous day-trader in Atlanta who killed 12 people and injured 13 more in July 29th 1999. His idea actually became a final act of desperation.

Less dramatically, for doctors, is a marked increase in subtle illegal activity. These acts include fraud, embezzlement, CPT® up-coding, medical over utilization, excessive full risk HMO contracting, Stark Law aberrations and other “white collar crimes.” Higher healthcare and social costs in police, judiciary (civil and criminal) and corrections result because of compulsive gambling. The impact on family members is devastating. Compulsive gamblers cause havoc and pain to all family members. The spouses and other family members also go through progressive deterioration in their lives.

In this desperation phase, dysfunctional families are left with a legacy of anger, resentment, isolation, and in many instances, outright hate.

[D] Day Trading Assessment

Internet day trading, like the Internet and telecommunications sectors, become something of a investment bubble a few years ago, suggesting that something lighter than air can pop and disappear in an instant. History is filled with examples: from the tulip mania of 1630 Holland and the British South Sea Bubble of the 1700’s; to the Florida land boom of the roaring twenties and the Great Crash of 1929; to the collapse of Japans stock and real estate market in early 1990’s; and to an all-time high of $1,926 for an ounce of commodity gold a few years ago.

Today it is Ask: $3,388.30 USD Bid: $3,367.30 USD

CONCLUSION

To this list, one might again include smart-phone or mobile day trading.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

One of the major concepts that most investors should be aware of is the relationship between the risk and the return of a financial asset. It is common knowledge that there is a positive relationship between the risk and the expected return of a financial asset. In other words, when the risk of an asset increases, so does its expected return. What this means is that if an investor is taking on more risk, he/she is expected to be compensated for doing so with a higher return. Similarly, if the investor wants to boost the expected return of the investment, he/she needs to be prepared to take on more risk.

Harry Max Markowitz (August 24, 1927 – June 22, 2023) was an American economist who was a professor of finance at the Rady School of Management at UCSD. He is best known for his pioneering work in modern portfolio theory, studying the effects of asset risk, return, correlation and diversification on probable investment portfolio returns.

One important thing to understand about Modern Portfolio Theory (MPT) is Markowitz’s calculations treat volatility and risk as the same thing. In layman’s terms, Dr. Markowitz uses risk as a measurement of the likelihood that an investment will go up and down in value – and how often and by how much. The theory assumes that investors prefer to minimize risk. The theory assumes that given the choice of two portfolios with equal returns, investors will choose the one with the least risk. If investors take on additional risk, they will expect to be compensated with additional return.

According to MPT, risk comes in two major categories:

Systematic risk – the possibility that the entire market and economy will show losses negatively affecting nearly every investment; also called market risk

Unsystematic risk – the possibility that an investment or a category of investments will decline in value without having a major impact upon the entire market.

***

***

Diversification generally does not protect against systematic risk because a drop in the entire market and economy typically affects all investments. However, diversification is designed to decrease unsystematic risk. Since unsystematic risk is the possibility that one single thing will decline in value, having a portfolio invested in a variety of stocks, a variety of asset classes and a variety of sectors will lower the risk of losing much money when one investment type declines in value. Thus putting together assets with low correlations can reduce unsystematic risks.

Although broad risks can be quickly summarized as “the failure to achieve spending and inflation-adjusted growth goals,” individual assets may face any number of other subsidiary risks:

Call risk – The risk, faced by a holder of a callable bond that a bond issuer will take advantage of the callable bond feature and redeem the issue prior to maturity. This means the bondholder will receive payment on the value of the bond and, in most cases, will be reinvesting in a less favorable environment (one with a lower interest rate)

Capital risk – The risk an investor faces that he or she may lose all or part of the principal amount invested.

Commodity risk – The threat that a change in the price of a production input will adversely impact a producer who uses that input.

Company risk – The risk that certain factors affecting a specific company may cause its stock to change in price in a different way from stocks as a whole.

Concentration risk – Probability of loss arising from heavily lopsided exposure to a particular group of counterparties

Counterparty risk – The risk that the other party to an agreement will default.

Credit risk – The risk of loss of principal or loss of a financial reward stemming from a borrower’s failure to repay a loan or otherwise meet a contractual obligation.

Currency risk – A form of risk that arises from the change in price of one currency against another.

Deflation risk – A general decline in prices, often caused by a reduction in the supply of money or credit.

Economic risk – the likelihood that an investment will be affected by macroeconomic conditions such as government regulation, exchange rates, or political stability.

Hedging risk – Making an investment to reduce the risk of adverse price movements in an asset.

Inflation risk – The uncertainty over the future real value (after inflation) of your investment.

Interest rate risk – Risk to the earnings or market value of a portfolio due to uncertain future interest rates.

Legal risk – risk from uncertainty due to legal actions or uncertainty in the applicability or interpretation of contracts, laws or regulations.

Liquidity risk – The risks stemming from the lack of marketability of an investment that cannot be bought or sold quickly enough to prevent or minimize a loss.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

On July 14, 2025, the Centers for Medicare & Medicaid Services (CMS) released its proposed Medicare Physician Fee Schedule (MPFS) for calendar year (CY) 2026.

In addition to the agency’s suggested increase to physician payments, the proposed rule also announces a new payment model and more tele-health flexibilities.

According to CMS, the “proposed rule is one of several proposed rules that reflect a broader Administration-wide strategy to create a health care system that results in better quality, efficiency, empowerment, and innovation for all Medicare beneficiaries.” (Read more…)

In order to create and monitor an investment portfolio for personal or institutional use, the physician executive, financial advisor, wealth manager, or healthcare institutional endowment fund manager, should ask three questions:

How much do we have invested?

How much did we make on our investments?

How much risk did we take to get that rate of return?

Introduction to the IPS

Most doctors, and hospital endowment fund executives, know how much money they have invested. If they don’t, they can add a few statements together to obtain a total. But, few can answers the questions above or actually know the rate of return achieved last year; or so far this year. Everyone can get this number by simply subtracting the ending balance from the beginning balance and dividing the difference. But, few take the time to do it. Why? A typical response to the question is, “We’re doing fine.”

Now, ask how much risk is in the portfolio and help is needed [risk adjusted rate of return]. In fact, Nobel laureate Harry Markowitz, Ph.D. said, “If you take more risk, you deserve more return.” Using standard deviation, he referred to the “variability of returns;” in other words, how much the portfolio goes up and down, its volatility [Markowitz, H: Portfolio Selection. Journal of Finance, March, 1952].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stocks: Investors cheered the news of an EU & US trade deal over the weekend, pushing the S&P 500 above 6,400 for the first time ever. But the index gave up most of its gains late in the day as attention turned to a huge week of data ahead (more on that in a minute).

Trade: Today was the first day of discussions between US and Chinese negotiators in Stockholm to keep the trade war truce alive. Elsewhere, President Trump foresees a baseline 15% to 20% tariff rate for the rest of the world.

Commodities: Gold fell as trade deal hopes heightened investors’ risk appetite, while oil spiked higher after Trump gave Russia a 10- to 12-day deadline to sign a truce with Ukraine.

According to Bloomberg, 83% of the S&P 500 companies that have reported earnings have outpaced Wall Street’s estimates, putting the index on pace for its best season of beats since the second quarter of 2021.

ORGANIZATIONAL BEHAVIOR ANDCLASSIFICATION OF RISKS

DEFINITION EMOTIONAL INTELLIGENCE: Emotional intelligence [EI] refers to the ability to identify and manage one’s own emotions, as well as the emotions of others. Emotional intelligence is generally said to include a few skills: namely emotional awareness, or the ability to identify and name one’s own emotions; the ability to harness those emotions and apply them to tasks like thinking and problem solving; and the ability to manage emotions, which includes both regulating one’s own emotions when necessary and helping others to do the same.

DEFINITIONAL ORGANIZATIONAL BEHAVIOR: Organizational behavior (OB) is the study of how individuals, groups, and organizations interact and influence one another. Though it is largely used within the field of business management as means to understand–and more effectively manage–groups of people. The reason businesses look to OB is because it can help organizations increase employee performance, while also creating a positive working environment.

CITE: Eugene Schmuckler; PhD MBA MEd CTS®

***

***

And so, as we review the concept of Emotional Intelligence and Organizational Behavior, it is possible to set up five EI/OB risk classes, based on the economic consequences of the occurrence of specific individual risks:

1. Prevented risks: Risks whose cost of occurrence is higher than their cost of management and whose occurrence may invoke additional legal sanctions. This class would include intentional torts and injuries caused by gross negligence.

2. Normally prevented risks: Risks whose cost of occurrence is greater than the cost of their management but whose occurrence will be considered only as negligent. This class includes most negligent injuries and most types of product liability actions.

3. Managed risks: Risks whose cost of occurrence is only slightly greater than their cost of management. The plaintiff usually has the burden of showing that the defendant owed the plaintiff a special duty to recover for one of these risks.

4. Un-Prevented risks: Risks whose cost of occurrence is less than their cost of management. The classic example of this class is the cost of railroad crossing barriers compared to the cost of people being hit by trains.

5. Un-Preventable risks: Risks whose occurrence is unmanageable. The assignment of a risk to one of these classes is a major problem in medical and healthcare quality control, because the class of a risk determines how much effort must be expended to prevent the risk. The misclassification of a prevented or normally prevented risk as a managed or un-prevented risk can result in large financial losses.

***

For example: A medical clinic that does not update obsolete equipment, such as inaccurate oxygen monitors, would be liable for any injuries attributable to the obsolete equipment. The classifications of risk must be reviewed periodically to determine if the cost of the risk-taking behavior has changed, thereby altering the classification.

***

***

For example: A small hospital in a rural area would not be expected to have the sophisticated equipment as a major hospital in a city. If an accident victim is brought into the rural facility, the hospital’s duty may be to transfer the patient to a better-equipped facility. The patient will face the risk of dying because of the delay in treatment, but the risk of insufficient treatments outweighs the risk of transfer. If the same victim were brought into a hospital in a major metropolitan center, the duty would be to treat the patient without a transfer. The risk of transfer has not changed, but the risk of insufficient treatment has disappeared.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Classic Definition: Research from Ernst-Young [Nikhil Lele and Yang Shim] uncovered a chasm between how consumer patients think they’re doing financially, and the actual state of their finances. Even more striking, their study suggested that improving consumers’ financial health will become one of the top imperatives in reframing consumer financial services.

Modern Circumstance: For example, the study asked consumers to rate their own financial health, and 83 percent rated themselves “good,” “very good” or “excellent.” Now, contrast this figure with what is known about their actual situation:

60 percent of Americans say they are financially stressed.

56 percent of Americans have less than $10,000 saved for retirement.

40 million American families have no retirement savings at all.

40 percent of Americans are not prepared to meet a $400 short-term emergency.

Paradox Example: Fortunately, even though the vast majority of consumers rate themselves as financially healthy, the study found that most still want to improve. Importantly for health economists, the attractive 25-34 and 35-49 year-old age groups were most likely to be extremely or very interested in improving their financial and economic health.

Paradox Example: Massively affluent consumer patients are even more interested in improving this paradox than their mass market counterparts.

Posted on July 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On July 15, 2025, the Centers for Medicare & Medicaid Services (CMS) released the proposed rule for the Outpatient Prospective Payment System (OPPS) and Ambulatory Surgical Center (ASC) Payment System for calendar year (CY) 2026.

Among other items, the agency proposes increasing payments to all outpatient providers, eliminating the Inpatient Only (IPO) List, and changing quality reporting programs.

This Health Capital Topics article reviews the proposed updates and changes to outpatient reimbursement. (Read more…)

Posted on July 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: President Trump said there’s a “50/50 chance” of a deal with the EU ahead of next week’s deadline. Investors decided they like those odds, and pushed the NASDAQ and S&P 500 to yet another new closing record high—in fact, the S&P 500 set a new record every day this week. Meanwhile, trade deal talks with Brazil have reportedly stalled.

Commodities: Oil fell to a three-week low today as Iran signaled a willingness to come to the negotiating table with European powers for nuclear talks.

Hopes of trade deals and less need for a safe haven investment pushed gold prices lower.

Posted on July 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

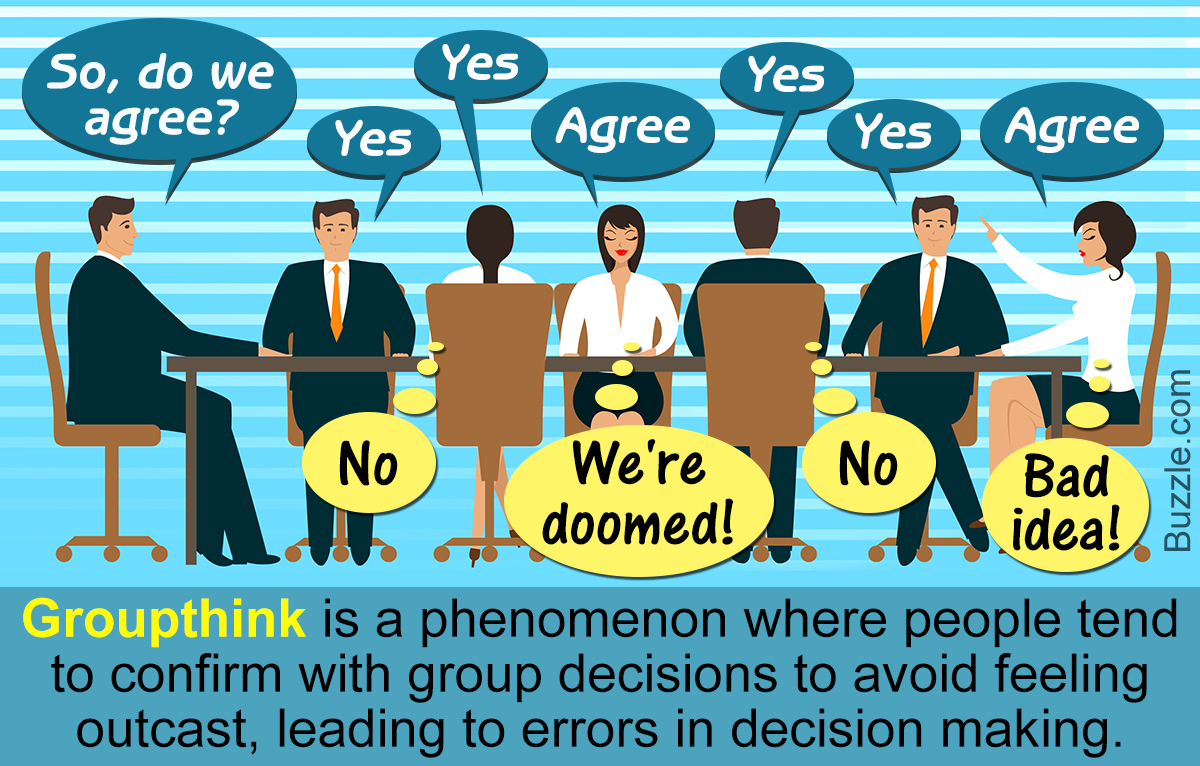

“lemming effect” or “group-think”

By Staff Reporters

***

***

According to psychologist and colleague Dan Ariely PhD, human beings have evolved – probably both genetically and socially – to be consistent. It is easier and safer to deal with others if they honor their commitments and if they behave in a consistent and predictable manner over time. This allows people to work together and build trust that is needed for repeat dealings and to accomplish complex tasks.

In the jungle, this trust was necessary to for humans to successfully work as a team to catch animals for dinner, or fight common threats. In business and life it is preferable to work with others who exhibit these tendencies. Unfortunately, the downside of these traits is that people make errors in judgment because of the strong desire not to change, or be different (“lemming effect” or “group-think”). So the result is that most people will seek out data that supports a prior stated belief or decision and ignore negative data, by not “thinking outside the box”.

Additionally, future decisions will be unduly influenced by the desire to appear consistent with prior decisions, thus decreasing the ability to be rational and objective. The more people state their beliefs or decisions, the less likely they are to change even in the face of strong evidence that they should do so. This bias results in a strong force in most people causing them to avoid or quickly resolve the cognitive dissonance that occurs when a person who thinks of themselves as being consistent and committed to prior statements and actions encounters evidence that indicates that prior actions may have been a mistake. It is particularly important therefore for advisors to be aware that their communications with clients and the press clouds the advisor’s ability to seek out and process information that may prove current beliefs incorrect.

Since this is obviously irrational, one must actively seek out negative information, and be very careful about what is said and written, being aware that the more you shout it out, the more you pound it in.

Stocks: Investors were pleased to hear about the trade deal with Japan yesterday and reports of an agreement with the EU coming soon kept the stock rally alive through market close. The S&P 500 notched its 12th new closing record this year, and the NASDAQ ended the day above 21,000 for the first time.

Bonds: Treasury yields rose a bit after an auction of 20-year notes was met with strong demand, indicating investor appetite for longer-term US debt.

Commodities: Oil inched higher while gold edged lower as investors hedge their bets in anticipation of more trade deals before the August 1st deadline.

Medpace isn’t a meme stock, but it still soared 54.67% yesterday. It was all thanks to a seriously impressive beat-and-raise earnings report for the clinical researcher.

It was also a great day for healthcare stocks: IQVIA climbed 17.92% after beating Wall Street forecasts last quarter.

DR Horton popped 17.02% after the homebuilder crushed Q3 earnings expectations.

It was also a great day for other homebuilders: Pultegroup rose 11.52% despite lower home closings last quarter, and management is optimistic that sales will bounce back next quarter.

NorthropGrumman gained 9.41% after a strong quarter, including an 18% increase in international sales for the defense contractor.

What’s down

LockheedMartin dropped 10.81% after the legacy defense contractor revealed big losses in its classified aeronautics program.

It wasn’t that great a day for defense contractors in general: RTX fell 1.58% after the company cut its earnings guidance.

General Motors may have beaten earnings expectations last quarter and kept its fiscal forecast intact, but investors didn’t like to hear about the $1.1 billion in tariff costs. Shares of the automaker stumbled 8.12%

Coca-Cola lost 0.59% after strong European sales helped the soft drink titan beat earnings estimates, but shareholders weren’t happy about weakness everywhere else.

Equifax tumbled 8.18% thanks to disappointing guidance for the current quarter from the consumer credit company.

Posted on July 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets lost steam late in the trading session yesterday as investors awaited more earnings announcements, with the DJIA tumbling into the red. But the S&P 500 managed to end the day above 6,300 for the first time ever, while the NASDAQ enjoyed its sixth consecutive record close

FOMC: Over the weekend,President Trump disputed reports that Treasury Secretary Scott Bessent talked him out of firing Jerome Powell. Meanwhile, Bessent said that the entire Federal Reserve should be put under review.

Trade: Commerce Secretary Howard Lutnick reiterated that August 1st will be the “hard deadline” for countries to make a deal with the US. Both negotiations and tensions with the EU are ramping up as Trump threatens to slap the bloc with 30% levies.

Posted on July 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP™

***

***

When Maria needed $400,000 for a down payment on a new home, her broker at a large Wall Street firm offered a solution: “Don’t sell investments and trigger capital gains. Just take out a margin loan.”

A margin loan is a line of credit from a brokerage firm, secured by the client’s investment portfolio. It offers quick access to cash with no immediate tax consequences and minimal paperwork. But the convenience comes at a cost. As of mid-2025, margin loan interest rates range from 6.25% to over 11%.

Margin loan recommendations are often presented by brokers as tax-savvy strategies that allow clients to access “tax-free” cash while keeping their portfolios intact. In many cases, however, the math benefits the advisor more than the investor. The cost of borrowing often exceeds what an investor is likely to earn by holding on.

For example, let’s assume an interest rate of 7.5% on Maria’s $400,000 margin loan. While borrowing delayed the payment of $20,000 in capital gains tax, she will eventually have to pay that tax anyway unless she holds the investments until her death. Two years later, with portfolio returns of 4% annually, she had earned around $32,000 from the $400,000 in investments she might have sold. Meanwhile, she had paid $60,000 in interest—leaving her some $28,000 worse off. That’s without factoring in ongoing interest payments, or the risks of a margin call if the investments securing the loan drop in value.

Why do advisors keep recommending margin loans? Because selling investments reduces the portfolio size and the advisor’s fee. Borrowing keeps the portfolio intact and the compensation unchanged—while the firm receives additional income from interest on the loan. In some cases, advisors suggest using margin loans to buy more investments, increasing both the portfolio and the fee they collect.

None of this is illegal. But when the borrowing cost is higher than expected returns and the advisor benefits financially, the ethics are questionable. The client takes the risk, while the advisor keeps the revenue.

This kind of conflict appears more often in portfolios where compensation is tied to asset volume and the company’s primary culture rewards gathering assets over delivering unbiased advice. By contrast, fee-only financial planning and investment advisors typically operate on simpler hourly, flat, or tiered fee structures. Their compensation doesn’t depend on whether a client borrows, sells, or holds. The culture of the firm focuses on conflict-free advice aligned with the client’s best interest.

Wall Street brokers are often held to a fiduciary standard, but structure still matters. In 2024 the SEC reported their examinations of brokers would continue to focus on advisor recommendations unduly influenced by the company’s compensation and incentives.

There are rare situations where a margin loan may be appropriate. A client with large unrealized gains might use a short-term margin loan to minimize taxes. An elderly investor might borrow tax-free rather than sell assets that will receive a step-up in basis at their death. Even in those cases, the math must be exact and the client must clearly understand the risks, including the possibility of a margin call.

If your advisor recommends a margin loan, especially to buy more investments, ask strong questions. What’s the interest rate? What return is realistic? What are the tax consequences of selling? How does this affect the advisor’s income?

In a high-rate, low-return environment, margin loans rarely favor the client. The exceptions are narrow. The risks are significant. And the conflict of interest is measurable.

Sometimes the smartest move is the simplest: sell what you need, pay the tax, and leave leverage out of your plan.

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial planning and investment decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just a few weeks ago.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

Assessment

QUESTION: How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.” In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.

Posted on July 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

The GENIUS Act is the law of the Land

President Trump signed the bill into law Friday, setting up a framework for regulating stablecoins—digital currency pegged to traditional assets—that are linked to the US dollar. It’s a big win for the crypto industry, and Trump said it was a “giant step to cement American dominance of global finance and crypto technology.”

The law could help push stablecoins into the mainstream, and major companies like Walmart and Amazon have been said to be considering launching their own, according to Morning Brew.

Markets: Stocks slid lower today even as a preliminary survey revealed that consumer sentiment hit its highest point since February, while inflation expectations fell to pre-tariff levels. The selloff deepened on reports that President Trump wants 15% to 20% tariffs against the EU, though the NASDAQ managed to eke out a win.