BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on June 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

A POD (Payable on Death) or TOD (Transfer on Death) account is a type of bank account where the account owner names a beneficiary to receive the account assets when the owner dies.

Key points about these accounts include:

Beneficiaries can be anyone, including minors, non-U.S. citizens, and organizations.

The beneficiary needs to provide a certified copy of the deceased’s death certificate to the bank or brokerage firm.

The assets are transferred immediately upon the account owner’s death.

Probate avoidance: By sidestepping probate, POD and TOD accounts streamline the distribution of assets post-death, allowing beneficiaries to gain access to these funds with greater speed.

Simplicity: Setting up these accounts is generally straightforward, often requiring just the completion of a form at the bank or brokerage firm.

No additional cost: There’s usually no cost to establish these accounts, aligning with the needs of individuals seeking a cost-effective method of transferring assets.

Cons

Joint ownership complexity. When an account is jointly owned, the beneficiary of the account won’t receive the assets until the surviving owner(s) die. The same applies to accounts owned in states with tenancy by the entirety for married couples.

Naming alternative beneficiaries: These accounts do not allow for the nomination of alternative beneficiaries if the primary beneficiary or beneficiaries predecease the account owner. This could lead to the assets being subjected to probate if the primary beneficiary is no longer alive at the time of the account holder’s death.

Transfers only happen after death: These accounts stipulate that the person must pass away before the beneficiary can access the funds – a restriction that could prove troublesome if the beneficiary requires access to these assets during the account holder’s life or if the account owner becomes incapacitated during their lifetime.

Posted on June 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Wall Street is stable right now as the technology trade has come roaring back.

The S&P 500 climbed above 6,000 points for the first time since February, while all three indexes posted their fifth winning week in the last seven. The S&P is now just over 2% from its all-time high.

Meanwhile, recent IPOs are party rocking, especially the stablecoin issuer Circle that went public last Thursday.

Many doctors are surprised to learn of an alternative investment known as a hedge fund, pooled investment vehicle or private investment fund. Unlike mutual funds, they can be structured in many ways. However, these funds cannot be marketed or advertised, but they are far from illegal or illicit.

In fact, physicians were among the early investors in one the most successful hedge funds. Warren Buffett got his start in 1957 running the Buffett Partnership, a hedge fund not open to the public. His first appearance as a money manager was before a group of physicians in Omaha, Nebraska. Eleven decided to invest some money with him. A few then followed into Berkshire Hathaway Inc, now among the most highly valued companies in the world.

And, more recently, Scion Asset Management® LLC, is a private investment firm founded and led by my eloquent colleague Michael J. Burry, MD and featured in the movie, The Big Short. Other hedge fund mangers of note include: George Soros, Carl Icahn, Ken Griffin, David Tepper, John Paulson and Bill Ackman.

A hedge fund is a limited partnership of private investors whose money is managed by professional fund managers who use a wide range of strategies; including leveraging [debt] or trading of non-traditional assets [real-estate, collectible, commodities, cyrpto-currency, etc] to earn above-average returns. Hedge funds are considered a risky alternative investment and usually require a high minimum investment or net worth. This person is known as an “accredited investor” or “Regulation D” investor by the US Securities Exchange Commission and must have the following attributes:

A net worth, combined with spouse, of over $1 million, not including primary residence

An income of over $200,000 individually, or $300,000 with a spouse, in each of the past two years

The hurdle rate is part of the fund manager’s performance incentive compensation. Also known as a “benchmark,” it is the amount, expressed in percentage points an investor’s capital must appreciate before it becomes subject to a performance incentive fee. Podiatrists should view the hurdle rate as a form of protection or the fee arrangement.

The hurdle rate benchmarks a single year’s performance and may be considered mutually exclusive of any other year, or the hurdle rate may compound each year. The former case is more common. In the latter case, a portfolio manager failing to attain a hurdle rate in the first year will find the effective hurdle rate considerably higher during the second year.

Once a fund manager attains the hurdle rate, the investor’s capital account may be charged a performance incentive fee only on the performance above and beyond the hurdle rate. Alternatively, the account may be charged a performance fee for the entire level of performance, including the performance required to attain the hurdle rate. Other variations on the use of the hurdle rate exist, and are limited only by the contract signed between the fund manager and the investor. The hurdle rate is not generally a negotiating point, however.

Example: A fund charges a performance fee with a 6 percent hurdle rate, calculated in mutually exclusive manner. A podiatrist places $100,000 with the fund. The first year’s performance is 5 percent. The doctor therefore owes no performance fee during the first year because the portfolio manager did not attain the hurdle rate. During year two, the portfolio manager guides the fund to a 7 percent return. Because the hurdle rate is mutually exclusive of any other year, the portfolio manager has attained the 6 percent hurdle rate and is entitled to a performance fee.

High Water Mark

Some hedge funds feature a “high water mark” provision known as a ”loss-carry forward.” As with the hurdle rate, the high water mark is a form of protection. It is an amount equal to the greatest value of an investor’s capital account, adjusted for contributions and withdrawals. The high water mark ensures that the manager charges a performance incentive fee only on the amount of appreciation over and above the high water mark set at the time the performance fee was last charged. The current trend is for newer funds to feature this high water mark, while older, larger funds may not feature it.

Example: A fund charges a 20 percent performance fee with a high water mark but no hurdle rate. A podiatrist contributes $100,000 to the fund. During the first year, the hedge fund manager grows that capital account to $110,000 and charges a 20 percent performance fee, or $2,000. The ending capital account balance and high water mark is therefore $108,000. During year two, the account falls back to $100,000, but the high water mark remains $108,000. During year three, in order for the manager to charge a performance fee, the manager must grow the capital account to a level above $108,000.

Claw Back Provision

Rarely, a hedge fund may provide investors with a “claw back” provision. This term results in a refund to the investor of all or part of a previously charged performance fee if a certain level of performance is not attained in subsequent years. Such refunds in the face of poor or inadequate performance may not be legal in some states or under certain authorities.

ASSESSMENT

Managers of hedge funds, like colleague Dimitri Sogoloff MBA who is the CEO of Horton Point investment-technology firm, often aim to produce returns that are relatively uncorrelated with market indices and are consistent with investors’ desired level of risk.

While hedging may reduce some risks overall, they cannot all be eliminated. According to a report by the Hennessee Group, hedge funds were approximately one-third less volatile between 1993 and 2010.

For a podiatrist who already holds mutual funds and/or individual stocks and bonds, a hedge fund may provide diversification and reduce overall portfolio risk. Consider investing in them with care.

2. Burry, Michael, J: Hedge Funds [Wall Street Personified]. In, Marcinko, DE and Hetico, HR: Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

3. Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. Productivity Press, New York, 2015.

4. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on June 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Call for Manuscripts, Articles, Essays, Comments or Opinions

Dear Medical and Financial Services Colleagues, Health Economists, CPAs, JDs, Insurance Agents and Consultants,

The Medical Executive-Post (ME-P), supported by iMBA Inc., with (ISSN 13: 978-1-4665-5873-1] is currently accepting manuscripts for publication.

The ME-P is an open access, multidisciplinary, international, blind peer-reviewed and non-peer-reviewed electronic forum which publishes high-quality solicited and unsolicited research, commentary, opinions, curated news and review articles in English, in all areas of Physician Focused Financial Planning, health economics, finance, accounting, medical practice management, health law, IT, policy and administration. We have over 50 topic channels.

Rapid Response Peer-Review

ME-P is a rapid response forum that publishes daily. One of our objectives is to inform contributors (authors) of the decision on their manuscript(s) within 48 hours of submission. Following acceptance, a paper would be published in the next available issue. The ME-P provides immediate open access to published articles without any barrier.

***

[ME-P Fast Review, Turn-Around and Publishing Time]

***

Broad Exposure Potential

Publishing your news, opinions or comments, essays or articles with the ME-P means that they will be available to millions of readers and researchers because our large and diverse readership base comprises millions of collaborators. Our forum supports the free downloading of published articles by scholars for use as materials for lecture, by government officials for policy making, professors, colleges, universities and educators, and by corporate researchers and FAs to selected firms and organizations world-wide.

Blog Citations

Assessment

Also, ME-P is a member of several local and international organizations, making it possible for the far and wide distribution of published materials. We ask you to support this initiative by publishing your thoughts, comments, articles and original paper(s) 0n this forum, and in our textbooks and white-papers, etc.

WHAT YOU “MUST KNOW“ ABOUT FINANCIAL ADVISORY FEES

Investment fees still matter despite dropping dramatically over the past several decades due to computer automation, algorithms and artificial intelligence, etc. And, they can make a big difference to your financial health. So, before buying any investment, it’s vital to uncover all real financial advisor and stock broker costs.

1. Up-front salesperson commissions. It is easy to ask; “If I buy this investment today and want to get out tomorrow, how much money do I get back?” If the answer is not “all your money,” the difference is probably upfront fees and commissions. These fees may run as high as 30% of the money invested. If you were to earn 5% a year on the investment, it would take 8 years just to break even.

2. Ongoing advisory fees. These are monthly, quarterly, or annual fees paid to advisors for their investment advice and oversight. This includes working with you to pick the asset classes, set diversification, select a portfolio manager, optimize taxes, re-balance holdings and other periodic tasks.

These fees have many names including wrap fee or investment advisory fees. The normal “rule of thumb” is 1% of assets managed, although fees can range from 0 to 7%. Today, it can even be as low as .5%. It can be charged even if the advisor receives an upfront commission. It can be easy to see, or hidden in the fine print.

3. Additional service fees. Find out specifically what services are included financial advisory fees. Additional fees for financial planning or other services are rarely disclosed. They can range from minimal hand-holding focused on your investments to comprehensive financial planning.

4. Ongoing managerial expense ratio fees. These are incredibly well hidden that you may not see them in your statements or invoices. The only way to know is to read the prospectus or other third party analysis, like Morningstar.com. And, they can vary greatly for the same investment, depending on the class of share you buy.

For example, American Fund’s New Perspective Fund’s expense ratio ranges from 0.45% to 1.54%. The average expense ratio of a mutual fund that invests in stocks is 1.35%. Conversely, the average expense ratio of a Vanguard S&P 500 Fund is 0.10%. The difference of 1.25% is staggering over time.

5. Miscellaneous fees. Some advisors charge $50 – $100 a year per account to open or close an account, and even fees to dollar cost average your funds into the market.

6. Transaction fees. Every time you buy or sell a fund, a fee is typically paid to a custodian. These can range from $5 to hundreds of dollars per transaction.

7. Fee Only: Paid directly by clients for their services and can’t receive other sources of compensation, such as payments from fund providers. Act as a fiduciary, meaning they are obligated to put their clients’ interests first

8. Fee Based: Paid by clients but also via other sources, such as commissions from financial products that clients purchase. Brokers and dealers (or registered representatives) are simply required to sell products that are “suitable” for their clients.

A “suitable” investment is defined by FINRA as one that fits the level of risk that an investor is willing and able, as measured by personal financial circumstances, to take on. The Financial Industry Regulatory Authority is a private American corporation that acts as a Self Regulatory Organization (SRO) that regulates member stock brokerage firms and exchange markets. These criteria must be met. It is not enough to state that an investor has a risk-friendly investment profile. In addition, they must be in a financial position to take certain chances with their money. It is also necessary for them to

A hedge fund is a limited partnership of private investors whose money is managed by professional fund managers who use a wide range of strategies; including leveraging [debt] or trading of non-traditional assets [real-estate, collectible, commodities, cyrpto-currency, etc] to earn above-average returns. Hedge funds are considered a risky alternative investment and usually require a high minimum investment or net worth. This person is known as an “accredited investor” or “Regulation D” investor by the US Securities Exchange Commission and must have the following attributes:

A net worth, combined with spouse, of over $1 million, not including primary residence

An income of over $200,000 individually, or $300,000 with a spouse, in each of the past two years

Choose the fee structure. The fee structure should align with your needs. Consider the type of advice you seek, the number of times needed and the complexity of your financial situation. You can always negotiating tactics are free to ask for a better deal.

Compare fees. It is essential to research and compare different fees. Be sure to read the fine print for details or costs that are not a base fee.

Robo-advisors: For simple investment goals, with little specificity, robo-advisors may be a cost-effective option. They charge lower fees than conventional financial advisors and provide an automated, algorithmic approach to managing your investments.

Assessment

The average cost of working with a human financial advisor in 2024 was 0.5% to 2.0% of assets managed, $200 to $400 per hourly consultation, a flat fee of $1,000 to $3,000 for a one-time service, and/or a 3% to 6% commission fee on the product types sold.

When ruminating over financial advisory fees; read and understand the contract with disclosures, do not sign a confidentiality or non-disclosure agreement, and do not waive your right to a lawsuit. According to colleague Dr. Charles F. Fenton IIII JD, forced legal settlements almost always favor the advisor over the client.

2. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

3. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Stocks: The S&P 500 touched 6,000 points for the first time since February and wrapped up its fifth positive week in the past seven following a better-than-expected jobs report. The vibes got even better in the afternoon following a President Trump announcement that the US and China trade teams will meet in London on Monday. STOCKS: https://medicalexecutivepost.com/2025/04/18/stocks-basic-definitions/

Bonds: Treasury yields ticked up in response to the solid May jobs report, a sign that investors were reducing bets on the scale of rate cuts this year. That’s not what Trump wants to hear: He urged Fed Chair Jerome Powell to slash interest rates by a jumbo-sized full point to pour “rocket fuel” on the economy. REVENUE BONDS: https://medicalexecutivepost.com/2024/12/20/bonds-revenue/

Oil: Oil prices have gone sideways for three straight weeks now, trading within a $4 range around $65/barrel since the middle of May. We’ll let you know when something interesting happens. CRUDE OIL:https://medicalexecutivepost.com/2024/08/14/wti-crude-oil/

If you’re looking at this tab, chances are you are fed up, burned out, seeking a better work-life balance, looking for a new non-clinical career, thinking of retirement, or all of the above. Perhaps you are just looking to regain the joy and meaning in your medical career. No worries! You may have come to the right place.

We work only with doctors, dentists, podiatrists, nurses, technicians and healthcare providers who struggle with personal and professional disillusionment, burnout, financial distress and an unbalanced life – all of which can happen at any stage of a medical career.

Through our coaching sessions, medical and healthcare professionals and colleagues can achieve a more meaningful, purposeful, and financially flourishing life.

Posted on June 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

BREAKING NEWS

***

***

Job growth is slowing, but still bigger than expected

US employers added 139,000 jobs last month, government data released yesterday shows—that’s less than the down-wardly revised 147,000 new jobs that were added in April, but more than economists had predicted. Meanwhile, the unemployment rate held steady.

Overall, the highly anticipated jobs report reflects employers growing more cautious in the face of the economic uncertainty brought on by the trade war, but so far, there doesn’t seem to be a steep drop off in the labor market. That could give the Fed reason to stay in wait-and-see mode on interest rates, though President Trump still used the occasion to urge Jerome Powell to cut rates “a full point” on Truth Social.

Posted on June 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Circle Internet Group, the stablecoin issuer,followed up its epic IPO day on Thursday with another banger, soaring 29.80%.

Coreweave closed out a roller coaster week with a 3.78% gain. The recently public AI cloud computing company is up 158% in the past month, and its tie-up with Applied Digital boosted that stock by another 8.54% today.

Rocket Lab (+9.34%) was one of several SpaceX competitors to receive a small boost following Elon Musk’s blowup with President Trump, which could threaten SpaceX’s contracts with the government.

Omada continued the strong run of recent IPOs. The virtual chronic care company jumped 21.05% in its debut on the Nasdaq today.

What’s down

Lululemon plunged 19.80% after cutting its full-year guidance due to the “dynamic macroenvironment” (CEO-speak for tariff uncertainty and people opting for baggier clothes than yoga pants). The company said it will increase prices on some items to offset the tariffs.

Docusign tanked 18.97% after warning that its billings for the year would come in lower than estimates as it transitions to an AI-driven model.

Broadcom failed to live up to exceedingly lofty expectations for its Q3 revenue forecast, causing shares of the giant semiconductor supplier to dip 5%.

Stat: $16 billion. That’s how much an HHS watchdog found in health program overspending, fraudulent billing, and possible cost savings in a six-month span. (Axios)

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

Markets: Stocks fell yesterday as investors readied themselves for today’s jobs report. The May jobs report is expected to show hiring slowed while the unemployment rate held flat. The data release will come as investors closely watch for any further signs of slowing in the US labor market.

The Bureau of Labor Statistics data is slated for release at 8:30 a.m. ET, today. Economists expect non-farm payroll to have risen by 125,000 in May and the unemployment rate to have held steady at 4.2%, according to consensus estimates compiled by Bloomberg.

Posted on June 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Americans are squirreling away a larger percentage of their earnings than ever before. In the first three months of the year, Americans stashed an average of 14.3% of their income in their 401(k)s, up from 13.5% in 2020, according to Fidelity Investments, which manages millions of accounts. That’s a record, and it also nearly approaches the 15% that’s recommended to be able to maintain your lifestyle after a 40-year career, as per the Wall Street Journal.

PlanetLabs exploded 49.37% thanks to the satellite imagery stock beating Wall Street forecasts, posting its first quarter of positive cash flow and record revenue.

MongoDB soared 12.84% after the software company crushed analyst estimates last quarter and projected better-than-expected earnings next quarter.

Five Below continued the trend of discount retailers beating expectations, rising 5.59% on an impressive beat-and-raise earnings report.

Land’sEnd missed revenue forecasts but beat on profits last quarter. Shares climbed 13.02% after the clothing company promised tariffs won’t hurt its bottom line.

Scott’sMiracleGro rose 11.04% after the fertilizer titan reiterated its healthy forward guidance.

What’s down

Tesla fell yet again today, down another 14.26% thanks to a growing rift between CEO Elon Musk and President Trump.

Procter & Gamble fell 1.90% after the consumer goods giant announced it will slash 7,000 jobs over the next two years.

Brown-Forman tumbled 17.92% on poor earnings for the alcohol maker and worse-than-expected forecasts for the coming year.

Kimberly-Clark lost 2.27% due to an agreement to sell a majority stake in its international Kleenex tissue business.

PVH plunged 17.96% after the parent company of brands like Calvin Klein beat earnings estimates last quarter but predicted a much worse quarter ahead.

ChargePoint Holdings plummeted 22.49% thanks to a rough quarter for the EV charging company.

Posted on June 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On April 11th, 2025, the Centers for Medicare & Medicaid Services (CMS) released its proposed rules for the payment and policy updates for the Medicare inpatient prospective payment system (IPPS) and long-term care hospital prospective payment system (LTCH PPS) for fiscal year (FY) 2026.

This Health Capital Topics article will discuss the proposed rule and the implications for stakeholders. (Read more…)

As many medical, dental and podiatric colleagues are aware, Environmental, Social and Governance (ESG) investing refers to a set of standards for a company’s behavior used by socially conscious investors to screen potential investments. Over the last decade, or so, I have seen many investors pursing this laudable aim.

Yet, more than 80% of private equity fund managers have now stepped away from at least one deal due to ESG concerns, according to the 2023 BDO Private Capital Survey. The reasons are complex, and point towards fund managers’ sentiment towards risk-reward in the current economic environment.

This retreat from ESG is due to backlash from conservatives who are critical of the idea that mutual fund managers should be considering any other factor but a company’s share holders in their investment decisions. Accusations of “Greenwashing” have also plagued many ESG funds, which is when an asset management firm charging higher fees or a specific thematic fund without actually delivering a unique investment strategic competitive advantage.

Greenwashing is the process of conveying a false impression or misleading information about how a company’s products are environmentally sound. Greenwashing involves making an unsubstantiated claim to deceive consumers and / or investors into believing that a company’s products are environmentally friendly or have a greater positive environmental impact than they actually do. Greenwashing may also occur when a company attempts to emphasize sustainable aspects of a product to overshadow the company’s involvement in environmentally damaging practices.

According to internationally known linguistics and cognitive science Professor,Mackenzie Hope Marcinko PhD of the University of Delaware, greenwashing is performed through the use of environmental imagery, misleading labels, cognitive biases and tendencies hiding tradeoffs. Greenwashing is also a play on the term “Whitewashing,” which means using false information to intentionally hide wrongdoing, errors or an unpleasant situation in an attempt to make it seem less bad than it really is.

To be sure, uncertainty around ESG regulations in the USA is leading financial deal makers to tread carefully. For example, Jim ClaytonMBA, aprivate equity advisor also from the University of Delaware recently stated:

“We’re a year past when the SEC said they were going to issue ESG reporting standards for public filers which has created more noise in the system.”

“People are nervous about what I would call ESG-intense exposed industries, in other words, those with “heavy carbon footprints”.

And, a federal judge in Texas said that American Airlines violated federal law by basing investment decisions for its employee retirement plan on environmental, social, and other non-financial factors. The ruling in January 2025 by US District Judge Reed O’Connor appeared to be the first of its kind amid growing backlash by conservatives to an uptick in socially-conscious investing. O’Connor said American had breached its legal duty to make investment decisions based solely on the financial interests of 401(k) plan beneficiaries by allowing BlackRock, its asset manager and a major shareholder, to focus on environmental, social and corporate governance (ESG) factors.

Even the State of Florida pulled $2 billion from the investment management firm BlackRock in the largest divestment ever made. Florida Governor Ron DeSantis claimed that by taking ESG standards into account when making investment decisions, the firm isn’t prioritizing the financial bottom line for Floridians.

Assessment

But, for a few years at least, things were indeed good. In 2020 and 2021, ESG funds outperformed the market by ~4.3%.

Conclusion

So, always remember [caveat emptor]: let the buyer beware!

2. Marcinko, DE; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017

3. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on June 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

HealthEquity jumped 8.96% after the health savings account custodian boosted its fiscal guidance for the year ahead.

What’s down

Tesla tumbled 3.55% on weak sales data from China and Germany.

Apple fell 0.22% thanks to a downgrade from Needham analysts, who think the company’s valuation is way too high.

Wells Fargo lost 0.36% after the Federal Reserve lifted its 2018 cap on the bank’s assets.

What goes up must come down: ConstellationEnergy sank 4.31% after Citigroup downgraded the nuclear power provider, warning it’s not getting its money’s worth with Meta Platforms.

Asana plunged 20.47% after the work management software maker announced fiscal forecasts that came in below Wall Street’s expectations.

Flowserve lost 6.27% and ChartIndustries dropped 9.46% after the two industrial manufacturers agreed to an all-stock merger of equals.

50% tariffs on steel and aluminum went into effect today. To celebrate, President Trump hopped on Truth Social to put China’s President Xi on blast ahead of an expected call between the two heads of state. And, Temu lost 58% of its daily users thanks to tariffs.

The president also pushed Jerome Powell to “LOWER THE RATE” following terrible private sector job numbers. Stocks are seemingly immune to tough trade talk and interest rate rants at this point, but bond yields sank on fears of slower economic growth.

The US dollar slipped, propelling gold higher as investors sought safety.

A proxy statement tells you a lot about a company’s management and board of directors, providing details about compensation, large shareholders, and the accounting firm that audits the company books. It also includes information about shareholder resolutions and the board’s responses to those proposals.

Each publicly traded company files a proxy statement with the Securities and Exchange Commission (SEC) every year, and it’s used by shareholders to help cast votes on their proxy ballots. The board may provide recommendations to vote for or against a proposal, but investors should do their best to collect the facts and make a decision on their own.

According to Motley Fool, about once every year, for most companies, you will have the right to vote your shares on a variety of topics related to the companies you own in your portfolio. These are called proxy votes. Regular individual shareholders generally receive one vote per share owned. Some companies have multiple classes of shares, and management and other insiders will have a higher level of voting power (for example, 10 votes per share).

Every year, you will receive a proxy statement in the mail or electronically. This document gives you insight into a variety of important issues to consider and vote on using your proxy ballot.

Quishing, or QR phishing, is a cybersecurity threat in which attackers use QR codes to redirect victims to malicious websites or prompt them to download harmful content. The goal of this attack is to steal sensitive information, such as passwords, financial data, or personally identifiable information (PII), and use that information for other purposes, such as identity theft, financial fraud, or ransomware.

This type of phishing often bypasses conventional defenses like secure email gateways. Notably, QR codes in emails are perceived by many secure email gateways as meaningless images, making the users vulnerable to specific forms of phishing attacks. QR codes can also be presented to intended victims in a number of other ways.

QR codes, or Quick Response codes, are two-dimensional barcodes that can be scanned easily with a camera or a code reader application. The main component of a QR code is data storage. QR codes have the capability to store significant amounts of information including URLs, product details, or contact information. Scanning technology allows smartphone cameras or code readers to easily and quickly access the website to which the URL points.

In a quishing attack, the attackers create a QR code and link it to a malicious website. Typically, the attacker will embed the QR code in phishing emails, social media, printed flyers, or physical objects, and use social engineering techniques to entice the victims. For example, victims might receive an email urging them to access an encrypted voice message via a QR code for a chance to win a cash prize.

Upon using their phones to scan the QR code, victims are directed to the malicious site. The site may prompt victims to enter private information, such as login information, financial details, or personal information. In the example above, the site may request the user’s name, email, address, date of birth, or account login information.

Once this sensitive information is captured, attackers can exploit it for various malicious purposes, including identity theft, financial fraud, or ransomware.

Posted on June 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Ford climbed 2.10% after the automaker reported an impressive 16% increase in sales last month thanks to employee pricing promotions.

Pinterest popped 3.84% thanks to an upgrade from JPMorgan, who applauded the social media site’s recent focus on monetization efforts.

SignetJewelers proved once again that diamonds are forever, rising 12.49% thanks to strong earnings last quarter.

CredoTechnology exploded 14.80% thanks to the high-speed connectivity solutions provider crushing earnings forecasts after it tripled its sales last quarter.

Parsons gained 7.01% despite the defense tech company slashing its fiscal forecast due to uncertainty in the Pentagon.

FergusonEnterprises rose 17.23% on the news that tariffs won’t have much of an effect on the plumbing and heating parts supplier.

MoonLakeImmunotherapeutics soared 17.95% on a report in the Financial Times that it may be acquired by Merck.

Hims & Hers Health fell 3.59% on the news that it will acquire European digital health platform Zava.

Bumble tumbled 6.45% on a downgrade from JPMorgan analysts, who think the dating app is losing market share to Hinge.

EchoStar sank 11.31% after the telecommunications company announced it will not make an interest payment, its second missed payment amid an FCC investigation.

FactSet Research Systems lost 4.83% on the announcement of a new CEO.

Posted on June 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

A recent joint report by the National Association of Accountable Care Organizations (NAACOS) and Innovaccer Inc., a healthcare artificial intelligence (AI) company, found tangible evidence that the U.S. healthcare delivery system is indeed moving toward value-based care (VBC).

Fifteen years after the passage of the Patient Protection and Affordable Care Act (ACA), which promoted VBC through the advent of ACOs and other alternative payment models, there is finally evidence that providers are actually moving in that direction.

This Health Capital Topics article reviews the joint report on “The State and Science of Value-based Care 2025.”(Read more…)

Posted on June 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Meta Platforms popped 3.62% on a report in the Wall Street Journal that the company is going all-in on using AI to create advertisements.

Applied Digital skyrocketed 48.46% after the data center operator announced two 15-year leases with CoreWeave that will bring in $7 billion in new revenue. CoreWeave rose 7.99%.

BioNTech soared 18.05% on news of a multibillion-dollar collaboration with Bristol Myers Squibb to develop cancer treatments. Bristol Myers Squibb rose 1.06%.

Moderna gained 1.84% thanks to the FDA’s approval of its new Covid vaccine, though it’s only for certain patients.

Blueprint Medicines exploded 26.09% after the biopharma company agreed to be acquired by Sanofi for $9.5 billion.

Auto stocks suffered from fears of higher pricing thanks to President Trump’s steel tariff hike. GeneralMotors tumbled 3.87%, Ford fell 3.86%, and Stellantis slid 3.55%.

Sports-betting stocks took a loss after Illinois lawmakers decided to tax the companies $0.25 per wager made on their apps. DraftKings lost 5.99%, and FlutterEntertainment dropped 2.74%.

Advertising stocks sank on Meta Platforms’ announcement of AI advances in its advertisements. Omnicom Group lost 4.02%, and WPP Group fell 2.45%.

Markets: Stocks closed out a winning month Friday with the S&P500 having its best one since 2023. But the markets are still rattled by the trade war, and stocks wavered during the day after President Trump accused China of breaching its recent trade deal with the US. Investors declined to fall into the Gap after the retail chain said tariffs would cost it up to $150 million this fiscal year.

A thought experiment is a mental exercise where you imagine a situation or scenario to explore an idea, test a theory, or examine a problem. It does not involve physical experiments or data. Instead, it uses reasoning, imagination, and logic to draw conclusions or raise important questions.

Sometimes referred to as the Inverted Spectrum Problem or the Knowledge Argument, this thought experiment is meant to stimulate discussions against a purely physical view of the universe, namely the suggestion that the universe, including mental processes, is entirely physical. This thought experiment tries to show that there are indeed non-physical properties — and attainable knowledge — that can only be learned through conscious experience.

Mary is a brilliant scientist who is, for whatever reason, forced to investigate the world from a black and white room via a black and white television monitor. She specializes in the neuro-physiology of vision and acquires, let us suppose, all the physical information there is to obtain about what goes on when we see ripe tomatoes, or the sky, and use terms like ‘red’, ‘blue’, and so on. She discovers, for example, just which wavelength combinations from the sky stimulate the retina, and exactly how this produces via the central nervous system the contraction of the vocal cords and expulsion of air from the lungs that results in the uttering of the sentence ‘The sky is blue’…What will happen when Mary is released from her black and white room or is given a color television monitor? Will she learn anything or not?

Put another way, Mary knows everything there is to know about color except for one crucial thing: She’s never actually experienced color consciously. Her first experience of color was something that she couldn’t possibly have anticipated; there’s a world of difference between academically knowing something versus having actual experience of that thing.

Posted on June 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

Stanley Fischer, one of the most influential economists of recent decades, has died. He was 81. His death was confirmed by the WSJ and Bank of Israel, where he served as governor from 2005 to 2013.

Fischer served as vice chairman of the Federal Reserve from 2014 to 2017. He left his biggest mark in prior decades, as professor of economics at the Massachusetts Institute of Technology, second in command at the International Monetary Fund, and at the Bank of Israel. In those roles, Fischer helped shape how an entire generation of central bankers and economic policymakers do their jobs.

Fischer was born in 1943 in Northern Rhodesia (now the independent country of Zambia) and first came to the U.S. in 1966 to get a Ph.D. at MIT.

After several years at the University of Chicago, he joined the faculty of MIT.

According to wikipedia, the S&P 500 Dividend Aristocrats is a stock market index composed of the companies in the S&P 500 index that have increased their dividends in each of the past 25 consecutive years. It was launched in May 2005.

There are other indexes of dividend aristocrats that vary with respect to market cap and minimum duration of consecutive yearly dividend increases. Components are added when they reach the 25-year threshold and are removed when they fail to increase their dividend during a calendar year or are removed from the S&P 500. However, a study found that the stock performance of companies improves after they are removed from the index The index has been recommended as an alternative to bonds for investors looking to generate income.

To invest in the index, there are several exchange traded funds (ETFs), which seek to replicate the performance of the index.

Posted on June 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and AI

***

***

Positional goods are goods and services that people value because of their limited supply, and because they convey a high relative standing within society.

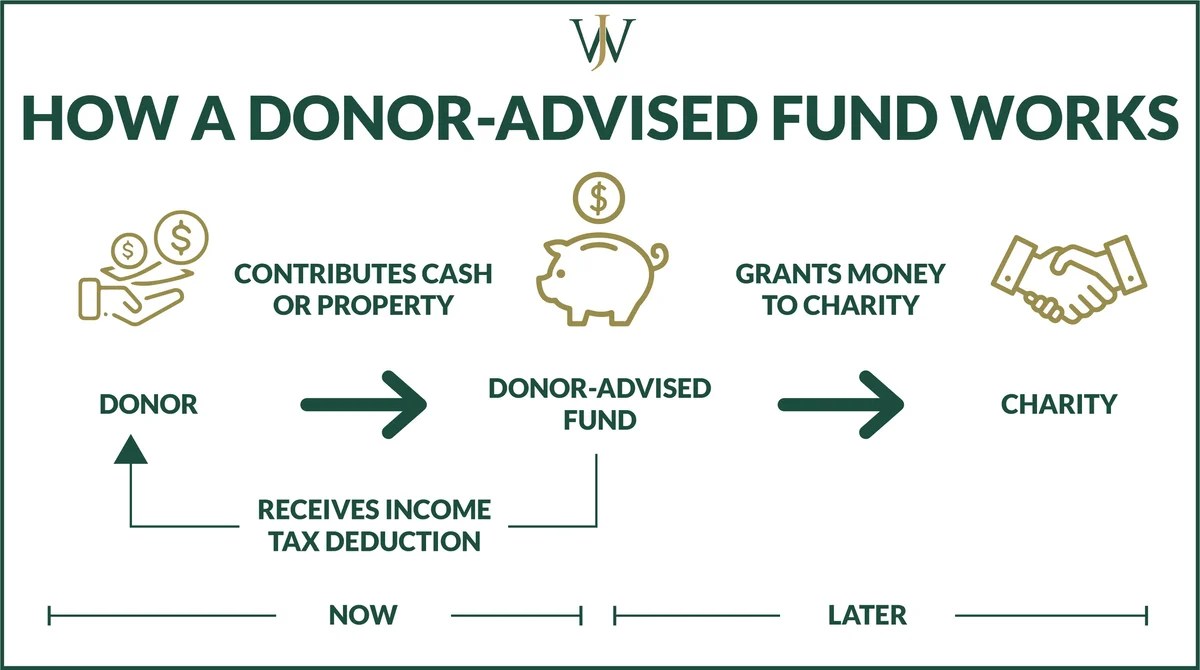

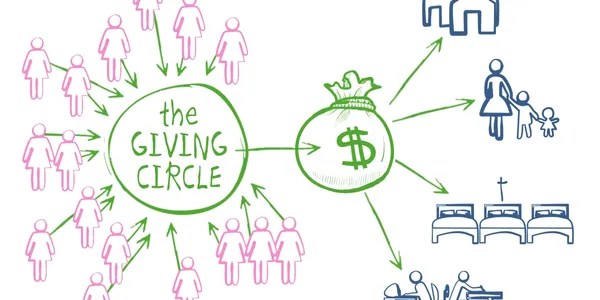

A donor-advised fund is a private account created to manage and distribute charitable donations on behalf of an organization, family, or individual. Donor-advised funds can democratize philanthropy by aggregating the contributions of multiple donors, thus multiplying their impact on worthy causes. Donor-advised funds also have abundant tax advantages.

Donor-advised funds have become increasingly popular, as they offer the donor greater ease of administration while still allowing them to maintain significant control over the placement and distribution of charitable gifts. But, unlike private foundations, donor-advised fund holders enjoy a federal income tax deduction of up to 60% of adjusted gross income (AGI) for cash contributions and up to 30% of AGI for the appreciated securities they donate. Donors to these funds can contribute cash, stock shares, and other assets. When they transfer assets such as limited-partnership interests, they can avoid capital gains taxes and receive immediate fair market value tax deductions.

According to the National Philanthropic Trust’s 2023 Donor-Advised Fund Report, these funds have continued to grow in recent years, despite some headwinds including the Covid-19 pandemic and occasional stock market setbacks. Total grants awarded by donor-advised funds in 2022 increased by 9% to $52.16 billion, while total contributions rose by 9% to $85.5 billion.

Many donor-advised funds accept non-cash assets—such as checks, wire transfers, and cash positions from a brokerage account—in addition to cash and cash equivalents.

Donating non-cash assets may be more beneficial for individuals and businesses, leading to bigger tax bigger write-offs.

Posted on June 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and AI

***

***

Consistency and Commitment Tendency: Human beings have evolved – probably both genetically and socially – to be consistent. It is easier and safer to deal with others if they honor their commitments and if they behave in a consistent and predictable manner over time. This allows people to work together and build trust that is needed for repeat dealings and to accomplish complex tasks.

In the jungle, this trust was necessary to for humans to successfully work as a team to catch animals for dinner, or fight common threats. In business and life it is preferable to work with others who exhibit these tendencies. Unfortunately, the downside of these traits is that people make errors in judgment because of the strong desire not to change, or be different (“lemming effect” or “group-think”). So the result is that most people will seek out data that supports a prior stated belief or decision and ignore negative data, by not “thinking outside the box”.

Additionally, future decisions will be unduly influenced by the desire to appear consistent with prior decisions, thus decreasing the ability to be rational and objective. The more people state their beliefs or decisions, the less likely they are to change even in the face of strong evidence that they should do so. This bias results in a strong force in most people causing them to avoid or quickly resolve the cognitive dissonance that occurs when a person who thinks of themselves as being consistent and committed to prior statements and actions encounters evidence that indicates that prior actions may have been a mistake.

According to colleague Dan Ariely PhD, it is particularly important therefore for advisors to be aware that their communications with clients and the press clouds the advisor’s ability to seek out and process information that may prove current beliefs incorrect. Since this is obviously irrational, one must actively seek out negative information, and be very careful about what is said and written, being aware that the more you shout it out, the more you pound it in.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on May 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

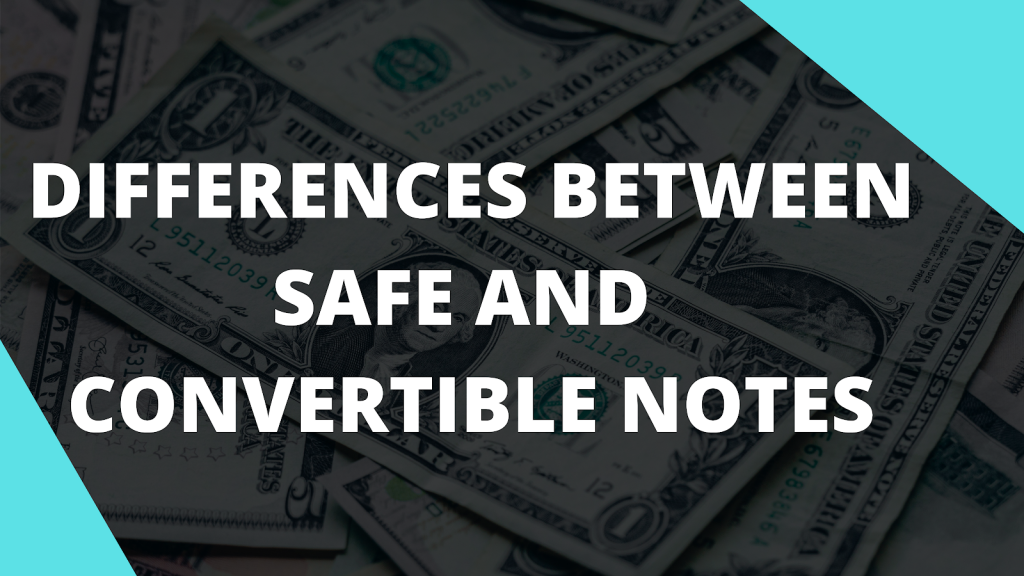

What Is a SAFE Note?

A SAFE note is a type of convertible security that specifies a certain amount of money an investor will pay you as a business owner. In exchange, you agree to give the investor a certain amount of equity in your company at an agreed-upon future date. In other words, a SAFE note confers the right for an investor to purchase shares in your company in a future-priced round.

How SAFE Notes Work

According to ContractsCounsel, a SAFE note works in the following way:

An investor provides funding in exchange for the right to future equity.

You use the funding to grow your business.

After your company grows sufficiently, you secure another investor, and your company receives a “post-money valuation.”

You calculate your company’s price per share.

You convert the SAFE note into the applicable number of shares and distribute them to the SAFE investor. Typically, a SAFE note converts after an equity financing round.

Example of a SAFE Note

An investor purchases a SAFE note with a valuation cap of $20 million. During the next funding round, the value of your company is set at $40 million at $20 a share. Because the SAFE note has a valuation cap of $20 million, its owner can purchase twice as many shares of your company as new investors can. This was the incentive for the SAFE investor to provide funding earlier.

Within venture capital financing, a convertible note is a type of short-term debt financing that’s used in early-stage capital raises. In other words, convertible notes are loans to early-stage startups from investors who are expecting to be paid back when their note comes due. But, instead of being paid back in principal with interest—as would be the case with a typical loan—the investor can be repaid in equity in your company.

You might also think of a convertible note like an IOU. An investor provides you with capital now and the convertible note, acting as a short-term loan, ensures that you give the investor a stake in your startup later. From the investor’s point of view, the benefit in this exchange is that if they give you capital and a vote of confidence early on and you do well, you’ll repay them many times over.

How Do Convertible Notes Work?

Typically, an investor will provide an early-stage startup in need of capital with a loan (with repayment terms in the ballpark of a standard short-term loan, usually a year or two), along with repayment terms. This is the “note.” The note will include a due date at which time it’s mature and the balance will be due, along with interest. Generally, however, the note is not repaid like a normal short-term loan. Instead, you repay the investor for their loan with equity in your company, usually in conjunction with another funding round.

If, however, the maturity date comes along and your startup has not yet converted the note to equity, the investor can either extend the convertible note’s maturity date or call for the actual repayment of the note.

This being said, the whole idea behind convertible notes is that your company is on a strong growth trajectory and that is why the note is being issued—it amasses value for the investor and beelines to a priced round. Ultimately, the point of a convertible note is that the noteholder, or investor, doesn’t want to get their loan paid back— they want their debt to convert into a heavily discounted security in a successful, valuable company that’s growing extremely quickly.

Cons: The major downside of a convertible note is that you will eventually be giving up some control over your business. When the convertible note comes due, the investor will be granted equity in your business. If you’re not ready to split ownership of your business with outside parties, this is not the right financing option for you.

Robert Jarvik, who developed the first artificial heart to be permanently implanted in a human — a breakthrough that captured the world’s imagination even as it triggered debates about medical ethics — died May 26th at his home in Manhattan, NY. He was 79.

Posted on May 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The median homeprice jumped 1.6% YoY last month and is sitting at $431,931. Meanwhile, mortgage rates for a 30-year fixed loan (the most common) are still hovering just under 7%. The chief economist of the National Association of Realtors said lower mortgage rates are the key to getting buyers to buy homes again.

UltaBeauty is sitting pretty, up 11.78% after the cosmetics retailer crushed earnings expectations and raised its fiscal guidance for the year ahead.

CostcoWholesale rose 3.12% after beating Wall Street’s earnings expectations, though same-store sales did slip a bit.

Zscaler climbed 9.79% on strong earnings for the cybersecurity company, including 23% revenue growth.

Palantir popped 7.73% on a report from the New York Times that the Trump administration has asked the company to help the government compile data on US citizens.

What’s down

Nvidia slipped 2.92% as rhetoric between the US and China over semiconductor import restrictions reignited investor fears.

Gap plunged 20.18% after the retailer revealed that tariffs will cost between $100 and $150 million.

RegeneronPharmaceuticals tumbled 19.01% thanks to mixed results for its new respiratory drug in late stage trials. The medication is made in partnership with Sanofi, which also dropped 5.61%.

DellTechnologies sank 2.08% after missing earnings expectations last quarter, though it did manage to beat on revenue.

PagerDuty, which is in fact a cloud computing company and not a seller of 1990s tech, lost 11.43% after issuing lower second-quarter guidance than Wall Street forecast.

Posted on May 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

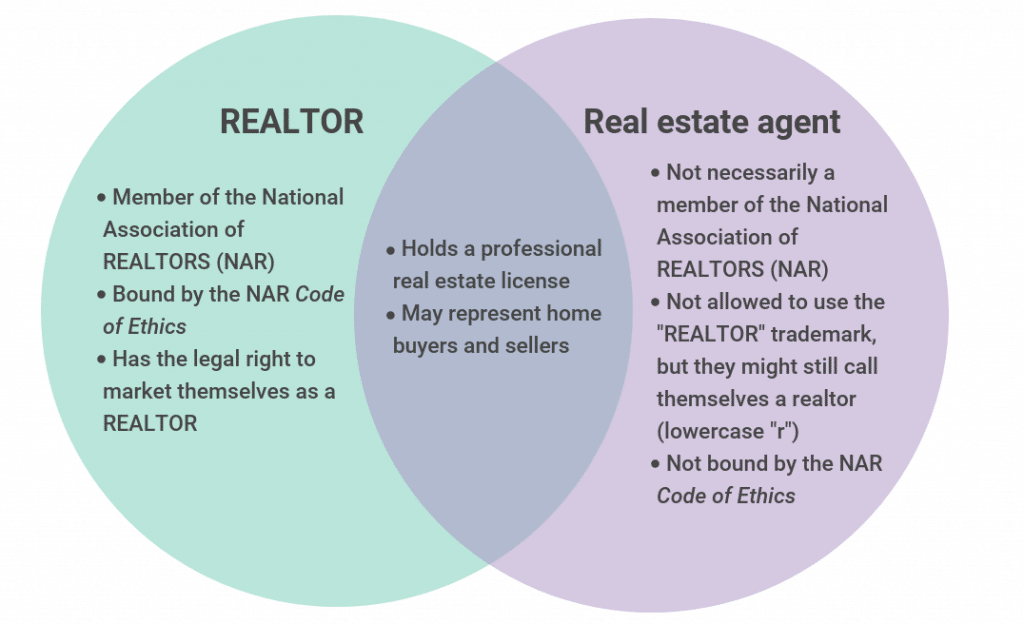

The terms “real estate agent” and “realtor” are often used interchangeably to describe a licensed professional who can help you buy or sell a home. But the terms have different meanings.

A realtor is a licensed salesperson who belongs to the National Association of Realtors (NAR), and must comply with NAR’s code of ethics. The term is capitalized when describing a NAR member, and NAR owns the trademark.

A real estate agent is simply a licensed salesperson who does not belong to NAR, and refers to any individual who holds a real estate salesperson’s license.

Should you hire a real estate agent or a realtor? Agents who belong to NAR aren’t necessarily better than non-member agents. NAR is just a trade association — not a licensing body — so membership is optional.

Posted on May 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

UnitedHealth Group improperly uses workers’ funds to reduce its own 401(k) contributions, according to a lawsuit against the nation’s largest health insurer that is seeking class-action status. The company denies the claims. It’s just one in a string of lawsuits facing the beleaguered company.

Boeing climbed 3.32% after CEO Kelly Ortberg laid out his turnaround plan for the struggling aircraft manufacturer, including ramping up production of its 737 Max.

C3.ai exploded 20.76% higher thanks to a smaller-than-expected loss last quarter and strong revenue growth for the enterprise AI company.

VeevaSystems soared 18.74% after the cloud computing company beat Wall Street estimates on both the top and bottom lines.

E.l.f. Beauty popped 23.58% thanks to better-than-expected earnings, as well as the news that it will acquire Haley Bieber’s beauty brand Rhode for up to $1 billion.

Moderna rose 3.38% despite the Trump administration pulling $766 million in funding for a new bird flu vaccine.

Li Auto climbed 2.11% after beating first-quarter forecasts, though the Chinese EV company issued disappointing guidance.

What’s down

Salesforce posted a beat-and-raise earnings report, but it wasn’t good enough for shareholders, and the software giant sank 3.30%.

HP reported solid revenue last quarter, but missed on profits and issued worse-than-expected guidance for the coming year, pushing shares down 8.27%

Kohl’s fell 0.74% after posting solid sales and a smaller-than-anticipated earnings loss.

Best Buy tumbled 7.27% after beating earnings estimates but missing on revenue and warning that it’s cutting its fiscal forecast and likely raising prices.

SentinelOne fell 11.59% after the cybersecurity company missed revenue estimates and issued a lower sales forecast than Wall Street wanted to see.

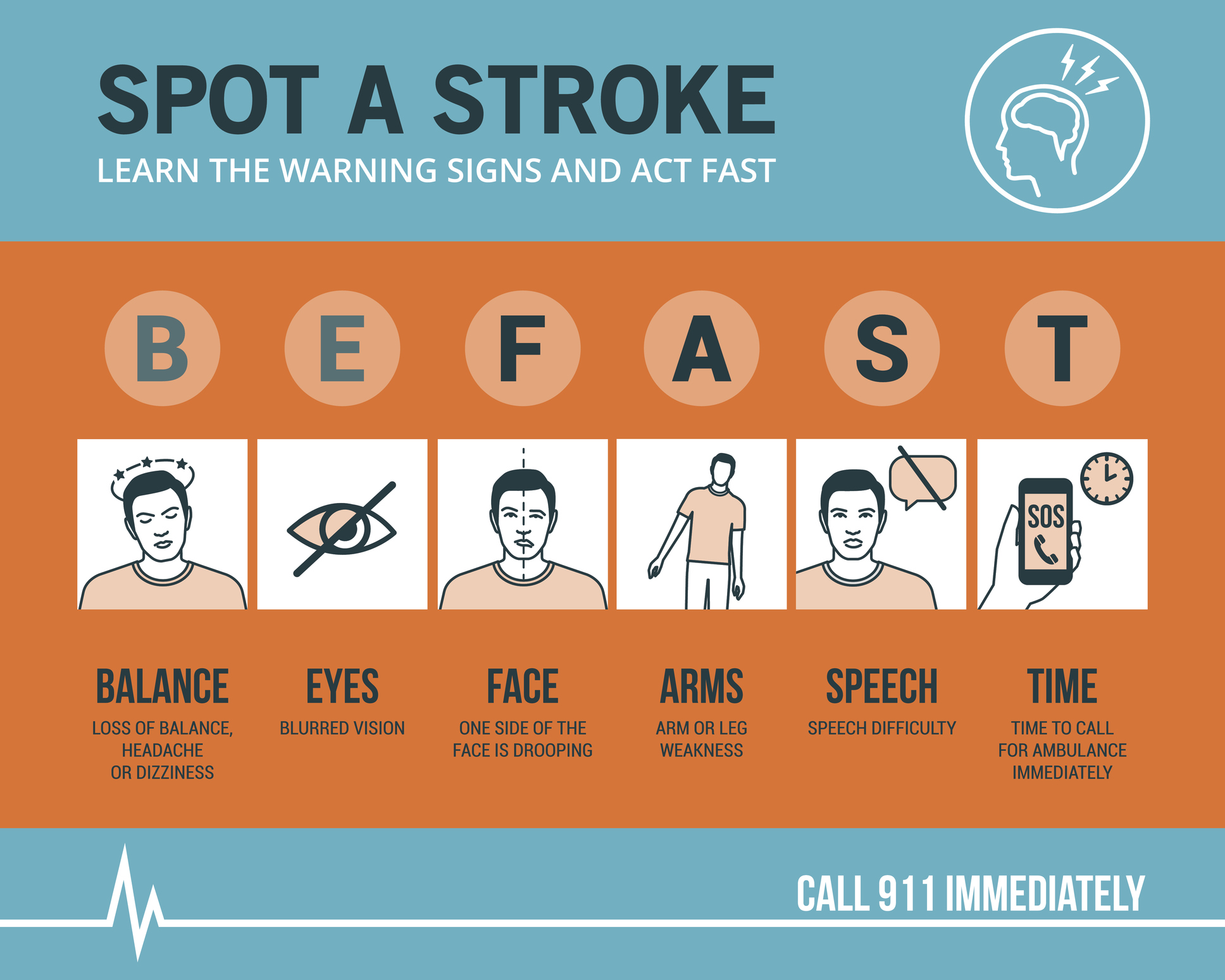

Stroke Impulses are sudden, intense urges that can result from neurological conditions like those following a stroke. It’s like having your brain’s impulse control dial turned way down. These impulses can be surprising and out of character, driven by changes in brain function. Understanding and managing these impulses requires patience and support.

These changes in personality and mood after stroke are common. Impulsiveness, apathy, pseudobulbar affect, anger, frustration and depression can affect a stroke survivor’s quality of life.

So, according to psychologist and colleague Dan Ariely PhD, if you or someone you know is dealing with stroke impulses, remember: it’s a brain thing, not a willpower thing.

Life planning and behavioral finance as proposed for physicians and integrated by the Institute of Medical Business Advisors Inc., is unique in that it emanates from a holistic union of personal financial planning, human physiology and medical practice management, solely for the healthcare space. Unlike pure life planning, pure financial planning, or pure management theory, it is both a quantitative and qualitative “hard and soft” science, with an ambitious economic, psychological and managerial niche value proposition never before proposed and codified, while still representing an evolving philosophy. Its’ first-mover practitioners are called Certified Medical Planners™.

Financial Life Planning is an approach to financial planning that places the history, transitions, goals, and principles of the client at the center of the planning process. For the financial advisor or planner, the life of the client becomes the axis around which financial planning develops and evolves.

Financial Life Planning is about coming to the right answers by asking the right questions. This involves broadening the conversation beyond investment selection and asset management to exploring life issues as they relate to money.

Financial Life Planning is a process that helps advisors move their practice from financial transaction thinking, to life transition thinking. The first step is aimed to help clients “see” the connection between their financial lives and the challenges and opportunities inherent in each life transition.

But, for informed physicians, life planning’s quasi-professional and informal approach to the largely isolate disciplines of financial planning and medical practice management is inadequate. Today’s practice environment is incredibly complex, as compressed economic stress from HMOs managed care, financial insecurity from insurance companies, ACOs and VBC, Washington DC and Wall Street; liability fears from attorneys, criminal scrutiny from government agencies, and IT mischief from malicious electronic medical record [eMR] hackers. And economic bench marking from hospital employers; lost confidence from patients; and the Patient Protection and Affordable Care Act [PP-ACA] more than a decade ago. All promote “burnout” and converge to inspire a robust new financial planning approach for physicians and most all medical professionals.

The iMBA Inc., approach to financial planning, as championed by the Certified Medical Planner™ professional certification designation program, integrates the traditional concepts of financial life planning, with the increasing complex business concepts of medical practice management. The former topics are presented in this textbook, the later in our recent companion text: The Business of Medical Practice [Transformational Health 2.0 Skills for Doctors].

***

***

For example, views of medical practice, personal lifestyle, investing and retirement, both what they are and how they may look in the future, are rapidly changing as the retail mentality of medicine is replaced with a wholesale and governmental philosophy. Or, how views on maximizing current practice income might be more profitably sacrificed for the potential of greater wealth upon eventual practice sale and disposition.

Or, how the ultimate fear represented by Yale University economist Robert J. Shiller, in The New Financial Order: Risk in the 21st Century, warns that the risk for choosing the wrong profession or specialty, might render physicians obsolete by technological changes, managed care systems or fiscally unsound demographics. OR, if a medical degree is even needed for future physicians?

Say, what medical license?

Dr. Shirley Svorny, chair of the economics department at California State University, Northridge, holds a PhD in economics from UCLA. She is an expert on the regulation of health care professionals who participated in health policy summits organized by Cato and the Texas Public Policy Foundation. She argues that medical licensure not only fails to protect patients from incompetent physicians, but, by raising barriers to entry, makes health care more expensive and less accessible. Institutional oversight and a sophisticated network of private accrediting and certification organizations, all motivated by the need to protect reputations and avoid legal liability, offer whatever consumer protections exist today.

Yet, the opportunity to revise the future at any age through personal re-engineering, exists for all of us, and allows a joint exploration of the meaning and purpose in life. To allow this deeper and more realistic approach, the informed transformation advisor and the doctor client, must build relationships based on trust, greater self-knowledge and true medical business management and personal financial planning acumen.

[A] The iMBA Philosophy

As you read this ME-P website, we hope you will embrace the opportunity to receive the focused and best thinking of some very smart people. Hopefully, along the way you will self-saturate with concrete information that proves valuable in your own medical practice and personal money journey. Maybe, you will even learn something that is so valuable and so powerful, that future reflection will reveal it to be of critical importance to your life. The contributing authors certainly hope so.

At the Institute of Medical Business Advisors, and thru the Certified Medical Planner™ program, we suggest that such an epiphany can be realized only if you have extraordinary clarity regarding your personal, economic and [financial advisory or medical] practice goals, your money, and your relationship with it. Money is, after only, no more or less than what we make of it.

Ultimately, your relationship with it, and to others, is the most important component of how well it will serve you.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on May 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Vail Resorts soared 8.84% on the news that it’s bringing back former CEO Rob Katz to turn the company around.

Dick’s Sporting Goods climbed 1.66% thanks to solid earnings, and the retailer also impressed by keeping fiscal guidance intact.

Box jumped 17.23% after the cloud storage company beat earnings estimates and raised its forecast for the coming quarter and full year.

Joby Aviation soared 28.78% after the air taxi startup secured a $250 million investment from Toyota.

What’s down

US chip designers sank on reports that the White House has ordered them to stop selling to clients in China. Cadence Design Systems tumbled 10.67%, while Synopsys lost 9.64%

Okta tumbled 16.16% despite the identity management software company posting solid earnings and standing by its fiscal guidance for the year.

Macy’s fell 0.50% despite beating Wall Street estimates across the board, though it did cut its profit outlook for the year.

Automaker Stellantis dropped 3.15% after revealing veteran exec Antonio Filosa will become the new head of Jeep’s parent company.

Freshpet fell 3.97% on a downgrade from TD Cowen analysts, who think the company’s refrigerated pet food concept doesn’t have much growth potential.

Semtech stumbled 4.56% even though the semiconductor supplier beat earnings estimates and raised its fiscal forecast.

BostonScientific sank 1.56% after it decided to discontinue its artificial heart valve system due to regulatory feedback.

Chevron fell 1.31% a day after the US government declared that it can no longer produce oil in Venezuela.

Posted on May 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP®

***

***

OVER HEARD IN THE FINANCIAl ADVISOR’S LOUNGE

A basic strategy for asset protection is to hold various assets in different entities. Putting real estate, small businesses, and other assets into trusts, corporations, or limited liability companies (LLCs) is effective protection that is relatively easy to put into practice. Not only do I recommend this strategy to clients, I use it myself. Recently, however, I discovered a potential downside.

About 25 years ago, I invested in some rare coins in a corporation I owned and put them into a safe deposit box owned by the corporation. When my business relocated 12 years ago, the safe deposit box billing was not forwarded to the new address and was never paid again. Last year I went to retrieve the coins from the safe deposit box, which I had not visited in 25 years. I discovered the box had been drilled open three years earlier and my collection turned over to the unclaimed property division of the State Treasurer’s office.

I was told getting the coins back would be simple enough. I just needed to verify that I owned the company which owned them by providing the corporation’s tax ID number. However, the corporation no longer existed. I didn’t have a record of its tax ID number. The IRS wouldn’t verify the number without my giving them the address the company had used. That address was a post office box number that I no longer used and couldn’t remember. The state’s position was “no tax ID, no coins.” The only verification of my identity as owner of the corporation was my signature on the bank’s safe deposit box application. Eventually, with the support of bank officers who were willing to swear that I was who I claimed to be, I got my coin collection back. The hassle involved in this process was a reminder of an important component of asset protection. Maintain accurate records so you don’t end up hiding assets from yourself.

***

***

A good start is to create a master file of all the entities that hold your assets. This can be any system that’s easy for you to use: a computer spreadsheet, a set of file folders, or a single paper list. Share it as appropriate with your CPA, attorney, or financial planner. The master list should include the name of each company, its date of incorporation, tax ID number, address, and other relevant information like phone or bank account numbers. Also keep an inventory of the assets each company owns.

Once you’ve created a master list, it’s essential to keep it up to date as you buy or sell assets, close companies, or transfer ownership. Set up a system, as well, to remind yourself of tasks like filing tax returns, completing minutes of annual meetings, and paying the annual safe deposit box rent. Make your record-keeping easier by eliminating unnecessary complications.

For example, you probably don’t need a separate address for each trust, corporation, or LLC. Instead of creating a separate company for each asset, you might consider grouping smaller assets within one entity. I’d suggest first discussing the pros and cons with an attorney or financial planner. For larger assets like real estate, I do recommend holding each one separately.

When I talk to clients about asset protection, I mention that part of the price we pay for it is an increase in paperwork. It’s easy to accept that idea with casual good intentions. The case of my reclaimed coin investment is a good reminder of the importance of keeping up with that paperwork. If we don’t, we might protect ourselves right out of access to our own assets.

Classic: Flat fee paid for a patient’s treatment based on their diagnosis and/or presenting problem. For this fee the provider covers all of the services required for a specific period of time.

Modern: Often characterizes “second generation” managed care systems. After a Managed Care Organization squeezes out costs by discounting fees, they often come to this method. If provider is still standing after discount blitz, this approach can be good for provider and clients, since it permits a lot of flexibility for provider in meeting client needs.

Posted on May 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Bonds breathed a sigh of relief after 30-year Treasury yields fell back below 5% as Japanese central bankers took precautionary measures to shore up their finances.

Gold tumbled as investors continue to throw money at risk assets, while bitcoin maintained its recent gains.

CoreWeave can’t stop, won’t stop: The AI hyperscaler was downgraded by Barclays analysts, who think its near-term upside is limited, but shares still rose 20.66%.

VF Corp., the parent company of The North Face, JanSport, etc, rose 12.92% after disclosing that members of its C-suite splurged on the stock.

SoundhoundAI is a retail trader favorite, and now Piper Sandler analysts like it,too: The AI voice platform jumped 16.05% on an upgrade.

Southwest gained 5.53% on reports that the airline is rolling out $35 baggage fees beginning tomorrow.

Movie theater stocks popped on a record-breaking Memorial Day weekend at the box office: AMC soared 23.77%, Cinemark climbed 3.82%, and MarcusCorp. gained 10.12%.

What’s down

PDD Holdings plunged 13.64% after the Chinese e-commerce retailer reported a hefty 47% decline in profits last quarter.

Trump Media & Technology Group tumbled 10.38% after the company announced it’s raising $2.5 billion to buy bitcoin.

ChampionHomes sank 16.39% after the homebuilder missed Wall Street expectations last quarter by a mile.

RocketPharmaceuticals dropped 62.84% after the biotech reported that a patient participating in a gene therapy trial died over the weekend.

Posted on May 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

Stock markets are coming off their worst week since April as President Trump’s tariff threats on Europe and Apple revived trade war jitters. The president has since delayed tariff threats on the EU, giving European stocks a boost yesterday, while Wall Street had the day off for Memorial Day.

No such relief appears to be coming for Apple, which has fallen 8% so far this month, and is the only Magnificent Seven member in the red for May, per FactSet.

Most individual physician portfolios are simply a list of stocks. Doctors with such lists usually know the cost of each position and when they acquired it. It is not unusual to find inherited low cost stocks in the account that have been held for many years.

When you inherit securities, a new cost basis is established (the price of the stock on the date of death or six months later—the executor of the estate makes this determination). Even though there would be no capital gain liability if the stock were sold immediately after date of death, most people simply don’t do anything, just hold the stock. Of course taxes should be considered when selling securities but the investment merit should be the overriding factor.

***

***

Doctor and Accountant Opinions

In a personal communication, Mr. L. Eddie Dutton, CPA said, “First make an investment decision and if it fits into the tax plan, so much the better. Doctors often wonder where they will get the money to pay the taxes. I say to get it from the sale of the appreciated stock and cry all the way to the bank with your profit.”

Dr. Ernest Duty MD, a very successful private investor advises “Ask yourself this question: If you had the money instead of the stock, would you buy the stock? If your answer is ‘Yes’ then, hold on to the stock but if you say ‘No, I wouldn’t buy that stock today’ then, sell it” [personal communication].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: E-MAILCONTACT: MarcinkoAdvisors@outlook.com