BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on July 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stocks: Investors cheered the news of an EU & US trade deal over the weekend, pushing the S&P 500 above 6,400 for the first time ever. But the index gave up most of its gains late in the day as attention turned to a huge week of data ahead (more on that in a minute).

Trade: Today was the first day of discussions between US and Chinese negotiators in Stockholm to keep the trade war truce alive. Elsewhere, President Trump foresees a baseline 15% to 20% tariff rate for the rest of the world.

Commodities: Gold fell as trade deal hopes heightened investors’ risk appetite, while oil spiked higher after Trump gave Russia a 10- to 12-day deadline to sign a truce with Ukraine.

According to Bloomberg, 83% of the S&P 500 companies that have reported earnings have outpaced Wall Street’s estimates, putting the index on pace for its best season of beats since the second quarter of 2021.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Classic Definition: Research from Ernst-Young [Nikhil Lele and Yang Shim] uncovered a chasm between how consumer patients think they’re doing financially, and the actual state of their finances. Even more striking, their study suggested that improving consumers’ financial health will become one of the top imperatives in reframing consumer financial services.

Modern Circumstance: For example, the study asked consumers to rate their own financial health, and 83 percent rated themselves “good,” “very good” or “excellent.” Now, contrast this figure with what is known about their actual situation:

60 percent of Americans say they are financially stressed.

56 percent of Americans have less than $10,000 saved for retirement.

40 million American families have no retirement savings at all.

40 percent of Americans are not prepared to meet a $400 short-term emergency.

Paradox Example: Fortunately, even though the vast majority of consumers rate themselves as financially healthy, the study found that most still want to improve. Importantly for health economists, the attractive 25-34 and 35-49 year-old age groups were most likely to be extremely or very interested in improving their financial and economic health.

Paradox Example: Massively affluent consumer patients are even more interested in improving this paradox than their mass market counterparts.

Posted on July 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: President Trump said there’s a “50/50 chance” of a deal with the EU ahead of next week’s deadline. Investors decided they like those odds, and pushed the NASDAQ and S&P 500 to yet another new closing record high—in fact, the S&P 500 set a new record every day this week. Meanwhile, trade deal talks with Brazil have reportedly stalled.

Commodities: Oil fell to a three-week low today as Iran signaled a willingness to come to the negotiating table with European powers for nuclear talks.

Hopes of trade deals and less need for a safe haven investment pushed gold prices lower.

Medpace isn’t a meme stock, but it still soared 54.67% yesterday. It was all thanks to a seriously impressive beat-and-raise earnings report for the clinical researcher.

It was also a great day for healthcare stocks: IQVIA climbed 17.92% after beating Wall Street forecasts last quarter.

DR Horton popped 17.02% after the homebuilder crushed Q3 earnings expectations.

It was also a great day for other homebuilders: Pultegroup rose 11.52% despite lower home closings last quarter, and management is optimistic that sales will bounce back next quarter.

NorthropGrumman gained 9.41% after a strong quarter, including an 18% increase in international sales for the defense contractor.

What’s down

LockheedMartin dropped 10.81% after the legacy defense contractor revealed big losses in its classified aeronautics program.

It wasn’t that great a day for defense contractors in general: RTX fell 1.58% after the company cut its earnings guidance.

General Motors may have beaten earnings expectations last quarter and kept its fiscal forecast intact, but investors didn’t like to hear about the $1.1 billion in tariff costs. Shares of the automaker stumbled 8.12%

Coca-Cola lost 0.59% after strong European sales helped the soft drink titan beat earnings estimates, but shareholders weren’t happy about weakness everywhere else.

Equifax tumbled 8.18% thanks to disappointing guidance for the current quarter from the consumer credit company.

Stocks: The multi-day rally wavered this afternoon as investors turned their attention to big tech earnings tomorrow. The S&P 500 closed at a record high, while the NASDAQ finally broke its hot streak.

FOMC: Treasury Secretary Scott Bessent sees no reason for Jerome Powell to step down, while President Trump tempered his outrage against the Fed chair. Instead, well-known economist Mohamed El-Erian took up the gauntlet.

Trade: Bessent said China may get an extension to make a true trade deal, while promising a “rash of trade deals” in the coming days. Speaking of, Trump declared the US has made a deal with the Philippines capping import levies at 19%.

Posted on July 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets lost steam late in the trading session yesterday as investors awaited more earnings announcements, with the DJIA tumbling into the red. But the S&P 500 managed to end the day above 6,300 for the first time ever, while the NASDAQ enjoyed its sixth consecutive record close

FOMC: Over the weekend,President Trump disputed reports that Treasury Secretary Scott Bessent talked him out of firing Jerome Powell. Meanwhile, Bessent said that the entire Federal Reserve should be put under review.

Trade: Commerce Secretary Howard Lutnick reiterated that August 1st will be the “hard deadline” for countries to make a deal with the US. Both negotiations and tensions with the EU are ramping up as Trump threatens to slap the bloc with 30% levies.

Posted on July 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP™

***

***

When Maria needed $400,000 for a down payment on a new home, her broker at a large Wall Street firm offered a solution: “Don’t sell investments and trigger capital gains. Just take out a margin loan.”

A margin loan is a line of credit from a brokerage firm, secured by the client’s investment portfolio. It offers quick access to cash with no immediate tax consequences and minimal paperwork. But the convenience comes at a cost. As of mid-2025, margin loan interest rates range from 6.25% to over 11%.

Margin loan recommendations are often presented by brokers as tax-savvy strategies that allow clients to access “tax-free” cash while keeping their portfolios intact. In many cases, however, the math benefits the advisor more than the investor. The cost of borrowing often exceeds what an investor is likely to earn by holding on.

For example, let’s assume an interest rate of 7.5% on Maria’s $400,000 margin loan. While borrowing delayed the payment of $20,000 in capital gains tax, she will eventually have to pay that tax anyway unless she holds the investments until her death. Two years later, with portfolio returns of 4% annually, she had earned around $32,000 from the $400,000 in investments she might have sold. Meanwhile, she had paid $60,000 in interest—leaving her some $28,000 worse off. That’s without factoring in ongoing interest payments, or the risks of a margin call if the investments securing the loan drop in value.

Why do advisors keep recommending margin loans? Because selling investments reduces the portfolio size and the advisor’s fee. Borrowing keeps the portfolio intact and the compensation unchanged—while the firm receives additional income from interest on the loan. In some cases, advisors suggest using margin loans to buy more investments, increasing both the portfolio and the fee they collect.

None of this is illegal. But when the borrowing cost is higher than expected returns and the advisor benefits financially, the ethics are questionable. The client takes the risk, while the advisor keeps the revenue.

This kind of conflict appears more often in portfolios where compensation is tied to asset volume and the company’s primary culture rewards gathering assets over delivering unbiased advice. By contrast, fee-only financial planning and investment advisors typically operate on simpler hourly, flat, or tiered fee structures. Their compensation doesn’t depend on whether a client borrows, sells, or holds. The culture of the firm focuses on conflict-free advice aligned with the client’s best interest.

Wall Street brokers are often held to a fiduciary standard, but structure still matters. In 2024 the SEC reported their examinations of brokers would continue to focus on advisor recommendations unduly influenced by the company’s compensation and incentives.

There are rare situations where a margin loan may be appropriate. A client with large unrealized gains might use a short-term margin loan to minimize taxes. An elderly investor might borrow tax-free rather than sell assets that will receive a step-up in basis at their death. Even in those cases, the math must be exact and the client must clearly understand the risks, including the possibility of a margin call.

If your advisor recommends a margin loan, especially to buy more investments, ask strong questions. What’s the interest rate? What return is realistic? What are the tax consequences of selling? How does this affect the advisor’s income?

In a high-rate, low-return environment, margin loans rarely favor the client. The exceptions are narrow. The risks are significant. And the conflict of interest is measurable.

Sometimes the smartest move is the simplest: sell what you need, pay the tax, and leave leverage out of your plan.

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial planning and investment decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just a few weeks ago.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

Assessment

QUESTION: How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.” In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.

Posted on July 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

The GENIUS Act is the law of the Land

President Trump signed the bill into law Friday, setting up a framework for regulating stablecoins—digital currency pegged to traditional assets—that are linked to the US dollar. It’s a big win for the crypto industry, and Trump said it was a “giant step to cement American dominance of global finance and crypto technology.”

The law could help push stablecoins into the mainstream, and major companies like Walmart and Amazon have been said to be considering launching their own, according to Morning Brew.

Markets: Stocks slid lower today even as a preliminary survey revealed that consumer sentiment hit its highest point since February, while inflation expectations fell to pre-tariff levels. The selloff deepened on reports that President Trump wants 15% to 20% tariffs against the EU, though the NASDAQ managed to eke out a win.

Crypto: Although bitcoin fell after the president signed the GENIUS Act into law, ether rose to its highest price in six months today, while enthusiasm for the new legislation pushed total crypto assets above $4 trillion.

Yes, you can contribute to both a Roth IRA and a 401(k), provided you don’t exceed annual contribution limits for each account.

Determining whether to contribute to a Roth IRA, 401(k), or both can be an important step in planning for your retirement. Here are the key differences, including tax advantages, employer contributions, and investment options.

Eligibility requirements are the first consideration when contributing to a Roth IRA and a 401(k). For Roth IRA contributions, your eligibility is determined by your income. Specifically, if your modified adjusted gross income (MAGI) exceeds certain thresholds, your ability to contribute to a Roth IRA may be reduced or eliminated. However, there are no income limits for contributing to a 401(k), making it accessible to anyone with earned income.

IRS rules do allow for contributions to both a Roth IRA and a 401(k), provided you adhere to the annual contribution limits for each account.

This means you can take advantage of the higher contribution limits of a 401(k) while also benefiting from the tax-free growth of a Roth IRA. This dual approach can be a strategy for maximizing your retirement savings. The advantages to contributing to both accounts present some key benefits, such as:

Tax diversification in retirement, allowing for better management of taxable income.

Potential reduction of overall tax burden.

Maximization of savings potential by taking full advantage of the benefits each account offers.3

Balancing contributions between a Roth IRA and a 401(k) requires careful planning. You might start by contributing enough to your 401(k) to receive the full employer match, which is essentially free money, if your employer offers this. Once you’ve secured the match, consider maxing out your Roth IRA contributions, if you’re eligible.

Stocks: Markets started the day on a high note thanks to a fifth straight decline in weekly initial jobless claims and surprisingly strong monthly retail sales. The NASDAQ hit its 10th record closing high of 2025 and the S&P 500 hit its ninth high.

Commodities: Lithium prices popped around the globe after the Chinese government ordered domestic producer Zangge Mining to halt operations. Plus, the US is reportedly set to impose 93.5% tariffs on Chinese imports of graphite, a key component.

The Fed Drama: A White House official said President Trump will likely fire Jerome Powell soon. Stockssank at the thought of the Fed head being shown the door, offsetting the pleasant surprise of a flat wholesale inflation reading.

Markets: Stocks managed to recoup their losses after Trump said it’s “highly unlikely” that he will fire Powell, but bonds remained shaken.

Crypto: Bitcoin bounced higher after the crypto bills currently under consideration in the House of Representatives cleared a key hurdle.

Also called “qualified” or “statutory” stock options, ISOs are considered tax-advantaged stock options based on U.S. tax law. With ISOs, the spread (the difference between the award price and the fair market value) will count as income for the alternative minimum tax (AMT) in the year you exercise your options.

Example: If you exercise and hold the shares for more than one year past the exercise date and more than two years past the original grant date, the sale of the stock becomes a qualifying disposition, and any realized profit is typically taxed at the long-term capital gains rate. If you sell earlier, the spread will be taxed at your ordinary income tax rate.

ISOs vs. NSOs: What’s the difference?

There are two types of employee stock options: statutory and nonstatutory. They can also be referred to as qualified and nonqualified, respectively. ISOs are statutory (qualified) and differ from nonstatutory (nonqualified) stock options (NSOs) in a few key ways:

Eligibility. ISOs are issued only to employees, whereas NSOs can be granted to outside service providers like advisors, board directors or other consultants. Typically, mainly senior executives or key employees are given ISOs, as a company is not required to offer ISOs to all employees.

Tax perks. ISOs have more compelling tax treatment compared with NSOs.

Posted on July 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets shrugged off President Trump’s weekend threat of 30% levies against the EU and Mexico, as well as his proposed 100% secondary tariffs against Russia today. Stocks eked out a win across the board, with the NASDAQ climbing to a new record close.

Commodities: Oil prices fell while gold took a breather, but the big winner was orange juice futures, which hit a four-month high thanks to Trump’s promise of 50% tariffs on all imports from Brazil. Coffee prices also climbed.

Overconfident Investing Bias happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. This causes the results of a study to be unreliable and hard to reproduce in other research settings.

Example: Data convincingly shows that people and financial planners/advisors and wealth managers who trade most often under-perform the market by a significant margin over time. Active traders lose money.

Example: Overconfidence Investing Bias moreover leads to: (1) excessive trading (which in turn results in lower returns due to costs incurred), (2) underestimation of risk (portfolios of decreasing risk were found for single men, married men, married women, and single women), (3) illusion of knowledge (you can get a lot more data nowadays on the internet) and (4) illusion of control (on-line trading).

Stocks: The major Wall Street stock indexes languished. The S&P pulled back from its record high to close the week just a bit lower, but the NASDAQ managed to post a gain across the week.

Crypto: Bitcoin hit a new high-water mark above $118,000. Next week, July 14th, Congress hosts “Crypto Week” to discuss regulating the industry in a growth-oriented manner.

Commodities: Silver rose to its highest level since 2011, and it’s been even hotter than gold. The metal is up ~27% this year. Oil, meanwhile, ticked higher on speculation that President Trump will place more sanctions on Russia early next week.

Bitcoin notched another all-time record yesterday, beating the previous record that was set two days ago.

Goldman Sachs plans to ask junior bankers to certify their loyalty every three months in order to prevent poaching by private equity firms, Bloomberg reported.

Stocks: Jobless claims came in lower than expected, the 30-year US bond auction met with strong demand, and Delta Airlines unofficially kicking off earnings season with a solid report. The S&P 500 and the NASDAQhit record highs.

Crypto: Bitcoin reached a record high for the second day in a row, hitting $113,863.31 today. The crypto’s price has stayed above $100k for 60 consecutive days.

Commodities: Coffee futures in New York climbed as much as 3.5% in response to President Trump’s threat to slap 50% tariffs on Brazil, which is the top producer of higher-end arabica coffee.

Posted on July 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler CFP™

***

***

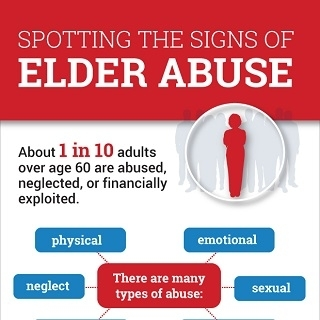

One serious risk to financial wellbeing in retirement that is difficult to talk about is financial exploitation. Someone whose cognitive abilities are declining is vulnerable to harm from both financial predators and their own financial misjudgments. Protecting such clients is a crucial part of a financial advisor’s role.

A little-known but important law, the Senior Safe Act, was enacted in 2018. It encourages financial advisors and institutions to report suspected elder abuse by offering immunity from legal liability when reports are made in good faith and with reasonable care. To qualify for these protections, financial professionals must undergo annual training to recognize the signs of exploitation and know how to act on their suspicions.

In many ways, the Senior Safe Act mirrors the duty of therapists to report when clients are threats to themselves, such as when a client becomes suicidal. Just as a therapist must balance confidentiality with the moral and legal responsibility to protect their client from harm, a financial advisor must weigh privacy against the need to prevent financial exploitation. Both roles rely on professional judgment, training, and the courage to act when the stakes are high.

Financial advisors, accountants, and attorneys are often the first to notice troubling signs that someone is being taken advantage of financially. These might include sudden large withdrawals, changes to account ownership or beneficiaries, or a newly and overly involved friend or family member. Behavioral shifts like confusion, anxiousness, secretiveness, or uncharacteristic deference are also red flags. These patterns are unsettling and demand attention, even when stepping in is uncomfortable.

Reporting possible elder abuse isn’t always straightforward, especially if the suspected abuser is a family member. As an advisor, I worry about misunderstandings, potential conflicts with the family, and even the possibility of damaging a relationship with the client. None of this is easy, But when the signs of exploitation become clear, staying silent could mean allowing harm to continue. That’s a risk I can’t take.

One of the tools I started using decades ago is the trusted contact disclosure form. This simple but powerful document allows clients to name someone my firm can contact if they notice unusual activity, such as a suspicious withdrawal or transfer. The trusted contact does not have control over the client’s account but serves as a resource to verify their well-being and ensure that their financial decisions align with their long-term goals. If you as a client have not signed such a form, it’s worth discussing with your advisor as a preventative step.

If you are concerned about the financial well-being of an elderly loved one, it’s crucial to alert not only their financial advisor but also other professionals like accountants, attorneys, or bankers. These professionals may have insights or access to information you don’t have, and by sharing your concerns, you provide a broader picture that can help them detect and address issues more effectively. Even if they are already monitoring for red flags, your input can provide valuable context to guide their next steps.

Difficult though it may be, stepping into uncomfortable territory is often essential to protecting vulnerable individuals. Whether it’s a financial advisor detecting exploitation or a therapist intervening in a mental health crisis, the goal is the same—to prevent harm while respecting the person’s autonomy.

The Senior Safe Act is a reminder that sometimes the most impactful safeguards work quietly behind the scenes. Taking simple steps like completing a trusted contact form or encouraging your loved one to work with a reputable, fiduciary advisor can make all the difference. Vigilance is an act of care that helps protect someone’s financial assets as well as their dignity and well-being.

Posted on July 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants LLC

***

***

On June 9th, 2025, Oregon’s governor signed into law the country’s strictest corporate practice of medicine (CPOM) prohibition. Senate Bill (SB) 951 will severely curtail the involvement of private equity firms and other corporations in the state’s medical practices.

This Health Capital Topics reviews the bill and discusses the implications on the healthcare industry. (Read more…)

Posted on July 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets wrapped the trading day with another win thanks to a shockingly strong jobs report this morning. Both the S&P 500 and the NASDAQ hit new record highs.

Posted on July 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Power station: Crude oil prices reversed as tensions in the Middle East cooled, but AI likely raises electricity demand over the longer term, creating investment opportunities and risks.

Oil supplies now exceed demand, noted Michelle Gibley, director of international research at the Schwab Center for Financial Research, in her latest analysis, though “AI is transforming the energy sector,” raising power shortage concerns.

Solar stocks got a reprieve today after the Senate dropped the excise tax on clean energy projects. Sunrun soared 10.51%, EnphaseEnergy rose 3.18%, SolarEdgeTechnologies popped 7.16%, and ArrayTechnologies climbed 12.54%.

Apple tumbled this summer after investors were disappointed by its AI rollout, but rose 1.29% on the news that the company may pivot to using Anthropic or OpenAI in iPhones instead of building something in-house.

Wolfspeed, the best name for a company that makes computer chips, exploded 98.09% after the company officially filed for Chapter 11 bankruptcy.

Hasbro got a nice 4.29% bump thanks to Goldman Sachs analysts, who are big old nerds who think Magic: The Gathering will boost the toymaker’s sales.

Ford popped 4.61% after the automaker reported an impressive 14% increase in sales last quarter.

Casino stocks soared on the news that gaming revenue in Macau rose 19% in June. WynnResorts climbed 8.85%, Las Vegas Sands added 8.95%, and MGMResorts gained 7.24%.

What’s down

AMC Entertainment tumbled 9.03% after the one-time meme stock announced its new debt restructuring plan.

ProgressSoftware sank 13.03% after the business application software company reported mixed results last quarter, beating on profit but missing on revenue.

JobyAviation fell 7.01% after traders took profits following the air taxi company’s big pop yesterday.

AeroVironment dropped 11.42% after defense contractor announced it’s offering $750 million in common stock and $600 million in convertible senior notes to pay off its debt.

Diabetes device makers tumbled on the news that the government may change the reimbursement rate for glucose monitors and insulin pumps. Insulet lost 4.52%, Dexcom fell 4.25%, and BetaBionics sank 4.26%.

Stocks: The S&P 500 and the NASDAQ started the second half of the year on the wrong foot, while the Dow climbed despite investors’ trepidation about conflict in Congress. But the Senate passed its version of the big, beautiful bill this afternoon, potentially getting us one step closer to ending all the drama.

Bonds: 10-year Treasury yields fell to their lowest level in two months this morning ahead of Jerome Powell’s appearance at a central banking conference today. There, Powell demurred on the possibility of a July rate cut, reiterating his wait-and-see approach.

Safe havens: The US dollar gained ground after a terrible first half of the year, while gold rose as investors braced themselves for the big jobs report on Friday.

Named after Monte Carlo, Monaco, which is famous for its games of chance, MCS is a software technique that randomly changes a variable over numerous iterations in order to simulate an outcome and develop a probability forecast of successfully achieving an outcome.

Endowment Fund Perspective

In private portfolio and fund endowment management, MCS is used to demonstrate the probability of “success” as defined by achieving the endowment’s asset growth and payout goals. In other words, MCS can provide the endowment manager with a comfort level that a given payout policy and asset allocation success will not deplete the real value of the endowment.

Divorce from Judgment

The problem with many quantitative software and other tools is the divorce of judgment from their use. Although useful, both mean variance optimization MVO and MCS have limitations that make it so they should not supplant the physician investor or endowment manager’s experience. MVO generates an efficient frontier by relying upon several inputs: expected return, expected volatility, and correlation coefficients. These variables are commonly input using historical measures as proxies for estimated future performance. This poses a variety of problems.

Problems with MCS

First, the MVO will generally assume that returns are normally distributed and that this distribution is stationary. As such, asset classes with high historical returns are assumed to have high future returns.

Second, an MVO optimizer is not generally time sensitive. In other words, the optimizer may ignore current environmental conditions that would cause a secular shift in a given asset class returns.

Finally, an MVO optimizer may be subject to selection bias for certain asset classes. For example, private equity firms that fail will no longer report results and will be eliminated from the index used to provide the optimizer’s historical data [1].

Example:

As an example, David Loeper, CEO of Wealthcare Capital Management, made the following observation regarding optimization:

Take a small cap “bet” for our theoretical [endowment] with an S&P 500 investment policy. It is hard to imagine that someone in 1979, looking at a 9% small cap stock return premium and corresponding 14% higher standard deviation for the last twenty years, would forecast the relationship over the next twenty years to shift to small caps under-performing large caps by nearly 2% and their standard deviation being less than 2% higher than the 20-year standard deviation of large caps in 1979 [2].

Table: Compares the returns, standard deviations for large and small cap stocks for the 20-year periods ended in 1979 and 1999. Twenty Year Risk & Return Small Cap vs. Large Cap (Ibbotson Data).

1979

1999

Risk

Return

Correlation

Risk

Return

Correlation

Small Cap Stocks

30.8%

17.4%

78.0%

18.1%

16.9%

59.0%

Large Cap Stocks

16.5%

8.1%

13.1%

18.6%

*Reproduced from “Asset Allocation Math, Methods and Mistakes.” Wealthcare Capital Management White Paper, David B. Loeper, CIMA, CIMC (June 2, 2001).

More Problems with MCS

David Nawrocki identified a number of problems with typical MCS as being that most optimizers assume “normal distributions and correlation coefficients of zero, neither of which are typical in the world of financial markets.”

Dr. Nawrocki subsequently describes a number of other issues with MCS including nonstationary distributions and nonlinear correlations.

Finally, Dr. Nawrocki quotes Harold Evensky who eloquently notes that “[t]he problem is the confusion of risk with uncertainty.

Risk assumes knowledge of the distribution of future outcomes (i.e., the input to the Monte Carlo simulation).

Uncertainty or ambiguity describes a world (our world) in which the shape and location of the distribution is open to question.

Contrary to academic orthodoxy, the distribution of U.S. stock market returns is far from “normal”. Other critics have noted that many MCS simulators do not run enough iterations to provide a meaningful probability analysis.

Assessment

Some of these criticisms have been addressed by using MCS simulators with more robust correlation assumptions and with a greater number of iterative trials. In addition, some simulators now combine MVO and MCS to determine probabilities along the efficient frontier.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

The S&P 500 closed within a hair of a new record yesterday marking an enormous comeback that followed the April announcement of “Liberation Day” tariffs.

Despite a persistent vibe of uncertainty related to US economic policy and geopolitics:

The S&P 500 closed less than 0.1% away from a record high which it notched in February before cratering nearly 20% in April. The index has regained ground in fits and starts since then and briefly surpassed its record in intra-day trading yesterday.

On Monday, the tech-heavy NASDAQ 100 one-upped the broader market and logged its highest-ever close. It came after President Trump said Israel and Iran agreed to a ceasefire, which eased investors’ concerns about a potential oil crisis.

According to Morning Brew, between unresolved geopolitical conflicts and President Trump’s still-unfolding tariff policies, a portfolio manager with Capital Wealth Planning, Kevin Simpson, told CNBC that he was “surprised by the magnitude of the rebound.”

Deals: Stocks popped at the open yesterday on the news that Canada has rescinded the digital services tax in order to lure the US back to the negotiating table. Meanwhile, Bloomberg reported that the EU will accept a 10% universal tariff in exchange for some key concessions.

Stocks: The S&P 500 and the NASDAQ both hit new record highs today, with the S&P 500 wrapping up its best quarter since Q4 20

The Fed: President Trump published a handwritten note asking Jerome Powell to cut interest rates, even as the White House considers new ways to replace the Fed Chair. Meanwhile, Goldman Sachs now sees the chances of the Fed cutting interest rates in September as “somewhat above 50%.”

Posted on June 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

CBOE Volatility Index

***

***

There’s a lot of confidence in markets these days, and nowhere is that more apparent than in the VIX, aka the CBOE Volatility Index, aka aka the Fear Index.

According to Brew Markets, the VIX literally measures the market’s expectation of volatility based on S&P 500 index options, but it’s become a shorthand way of quantifying investors’ fear or confidence. Any time the VIX rises above 30, it’s taken as a sign of some serious trepidation in the market—but anytime it falls below 20, the market is calm, cool, and collected.

The VIX skyrocketed to over 50 on Liberation Day as investors fretted over what tariffs meant for their portfolios, but it’s been gradually falling ever since. As the chart above shows, the VIX just fell below its key support level of 17—a mark it has failed to break below recently, and a move that underlines investors’ confidence that the good times will keep rolling.

Assets under advisement refer to assets on which your firm provides advice or consultation but for which your firm does either does not have discretionary authority or does not arrange or effectuate the transaction. Such services would include financial planning or other consulting services where the assets are used for the informational purpose of gaining a full perspective of the client’s financial situation, but you are not actually placing the trade.

Assets under advisement could also be those which you monitor for a client on a non-discretionary basis, where you may make recommendations but where the client is the party responsible for arranging or effecting the purchase or sale. A common example of this AUM scenario is when an advisor reviews a participant’s 401(k) allocations. If the adviser does not have the authority or ability to effect changes in the portfolio, these assets are likely considered assets under advisement rather than regulatory assets under management.

Assets under advisement are permitted to be disclosed on Form ADV Part 2A as a separate asset figure from the assets under management. There is no requirement to disclose the assets under advisement figure, but some advisors opt to include the figure to give prospective clients a more complete picture of the firm’s responsibilities. If you choose to report your assets under advisement, be sure to make a clear distinction between this figure and your regulatory assets under management.

***

D. E. Marcinko & Associates Core Operating Values

9. We act with honesty, integrity and are always straightforward. 8. We strive to be innovative, creative, iconoclastic, and flexible. 7. We admit and learn from mistakes and don’t repeat them. 6. We work hard always as competitors are trying to catch up. 5. We treat others with dignity and respect. 4. We are the onus of consulting advice for the fiduciary well being of others. 3. We fight complacency as former success is in the past. 2. The best management styles are timeless, not timely. 1. Our clients are colleagues and always come first.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

If you are just starting out managing your finances and don’t know where to begin, a financial coach may be a good option for you. They are helpful for someone who wants to become proficient in the basics of finance, from learning how to budget or save money to building an emergency fund or creating a plan for paying off debt. If you have short-term money goals, like saving for a big purchase or just practicing better money habits, a financial coach can help you reach them by working with you to create a plan and holding you accountable. Even more for physicians and most all medical professionals.

Pros and Cons of Working with a Financial Coach A financial coach can have a positive impact on your financial well–being and your life in a number of ways:

Financial coaches see the bigger picture of how you relate to money. They can help you develop better habits, resulting in positive personal growth.

By providing education and encouragement, they can reduce financial stress, confusion, and what it is about money that overwhelms you.

Through accountability and support, they can help you accomplish your goals and help you feel more confident in your finances.

Available 24/7/365.

Modest fees.

At you service. Dr. David Edward Marcinko MBA MEd CMP

Posted on June 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Deals: The US and China revealed the details of their trade deal framework, easing restrictions on rare earth metals and semiconductor chips. Commerce Secretary Howard Lutnick promised up to 10 more deals are on their way ahead of the July 9th tariff-pause deadline, but that probably won’t include Canada: President Trump ended all trade discussions with the country thanks to a dispute over the digital services tax.

Stocks: Indexes climbed at the open thanks to the deal with China, but they tumbled on news of a fallout with Canada. Still, the S&P 500 managed to post its 1,245th new all-time high, while the NASDAQ booked its own record close. The Dow trundled higher as well, though it’s still about 1,600 points below its previous record.

If you’re looking at this tab, chances are you are fed up with your financial brokerage accounts, thinking of finances, investing, retirement or all of the above.

And so, we can help

An investment portfolio second opinion, also called a “ portfolio review,” is an analysis of your financial holdings and associated strategies, allocations, fees and performance to determine whether the most effective instruments and methodologies are being utilized to reach your goals.

No Worries! You may have come to the right place.

E-Mail Ann Miller RN MHA CPHQ for an Initial Appointment: MarcinkoAdvisors@outlook.com

The purpose of this initial appointment is for you to ask a lot of questions to make sure you are comfortable with potentially working with us. It also helps if you are prepared to provide a verbal summary of your current situation.

Here are some questions to consider asking us during your first meeting:

1) Can you tell us about your financial qualifications, experience, education and training; if any?

2) Can you provide some information about your current financial advisory team?

3) On what type of investments do you typically purchase and own?

5) How much do pay your financial management firm?

6) How long have you been working with your current financial management firm?

8) What other services does your financial team provide?

Posted on June 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BY A.I.

***

***

Stocks: The S&P 500 briefly traded a few cents above its February all-time closing high yesterday afternoon, but couldn’t sustain the gain and fell just short at the end of the day. The NASDAQ remains inches away from its record high as well.

Deals: The end of the 90-day tariff pause is less than two weeks away, but the White House said that the July 9th deadline “is not critical.”

Meanwhile, the Treasury Department is doing everything it can to make the dreaded “revenge tax” in the big, beautiful bill irrelevant.

Commodities: Gold and oil had muted moves upward but copper climbed to a three-month high after Goldman Sachs analysts warned of shortages ahead

Posted on June 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Nvidia and Microsoft both set new record highs as the AI trade continues to revive. Nvidia rose 0.46%, while Microsoft climbed 1.05%.

CoreScientific exploded 33.01% on reports from the Wall Street Journal that the bitcoin miner may be acquired by AI company CoreWeave.

ServeRobotics gained 9.87% after the delivery robot maker launched its service on the streets of Atlanta today.

McCormick is looking spicy: The consumer goods company rose 5.31% after earnings outpaced analyst forecasts.

PennEntertainment rose 4.94% after the gambling company was upgraded by analysts at Citizens, who think the stock’s underperformance is about to reverse.

Solar stocks may be thrown a lifeline by the Senate, which is considering keeping some clean energy tax credits in the spending bill. EnphaseEnergy popped 12.83%, SunRun rose 6.46%, and SolarEdgeTechnologies climbed 5.11%.

Copper miners popped as prices of the precious metal rose today. Freeport–McMoRan jumped 6.85%, SouthernCopperCorp. climbed 7.79%, and AngloAmericanplc added 7.16%.

What’s down

Micron Technology lost 0.98% despite the chipmaker reporting fiscal third quarter results that beat Wall Street’s expectations.

Kratos Defense and Security Solutions sank 2.36% after the military tech company announced it will sell $500 million worth of stock to raise money for capital spending.

Equinix crumbled another 9.56% after a terrible fiscal outlook pushed Raymond James and BMO analysts to downgrade the internet services company.

Posted on June 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Stocks: The S&P 500 and NASDAQ started the day inches away from their all-time highs, but the market rally faltered in mid-afternoon as relief from an Israel/Iran ceasefire faded and investors turned their attention to Friday’s PCE report.

Economy: Speaking of inflation, Jerome Powell stuck to his guns during his second day of congressional testimony, endorsing a wait-and-see mentality. President Trump is apparently tired of waiting, and says he has “3 or 4” candidates in mind to replace Powell.

Commodities: Oil bounced back after posting its biggest two-day decline since 2022.

Here is a list of the most common and helpful investment terms you’ll come across and should know.

Ask. The price that someone looking to sell stock wants to receive.

Bid. The price that someone is willing to pay for stock.

Buy. To acquire shares and thereby take a position in a company.

Sell. To get rid of shares whether because you’ve reached your goal or to prevent losses.

Bull market. Market conditions in which investors expect prices to rise.

Bear market. Market conditions in which investors expect prices to fall.

Dividend. A portion of a company’s earnings paid to shareholders.

Blue chip stocks. Shares of large and well-recognized companies that have a long history of solid financial performance.

Earning per share. A company’s net profit divided by the number of outstanding common shares.

Mutual fund. A collection of investments — stocks, bonds, commodities, and more — bundled together and held in common by a group of investors.

Asset. Something you own that could generate a return in the form of more assets.

Asset allocation. Your investment strategy, essentially — the mix of assets you choose to put your money into, whether that be cash, bonds, stocks, commodities, real estate or something else.

Broker. A person or firm — or robot — that arranges transactions between buyers and sellers in exchange for a commission (that is, a fee).

Capital gain (or capital loss). The money you make (or lose) on the sale of an asset.

Diversification. Investing in a variety of sectors, such as health care, energy and IT as well as across different geographic locations.

Dow Jones Industrial Average. A price-weighted list of 30 blue-chip stocks. It’s often used to help get a sense of the overall health of the stock market, even though it only reflects a small portion of the players.

Index fund. A type of mutual fund or exchange-traded fund that allows you to invest in a portfolio that mimics a market index, which is basically a list that tracks the performance of a group of investments either for a specific sector or the overall market.

Hedge fund. A type of investment partnership. Partners pool money from investors and try out a few different investing strategies. Generally, hedge funds will make riskier investments than your typical investor. They’ll also often use leverage (that is, borrowed money) or place bets against the market to get bigger returns. They make their money by charging their investors management fees based on a percentage of their profits.

Expense ratio. The percentage-based fee that mutual fund managers charge you to manage your investments.

Market price. How much it would cost right now to buy or sell an asset or service.

Securities and Exchange Commission (SEC). An independent government body that was created to protect investors and the national banking system. The SEC enforces laws that maintain orderly, fair and efficient markets.

Short selling. A tactic available to investors who predict a stock’s price is about to drop. An investor borrows a quantity of shares through a broker and then sells them, intending to repurchase them later, at a lower price, and return them to the lender.

Stock exchange. A place buyers and sellers come together to buy, sell and trade stock during set business hours. The New York Stock Exchange (NYSE) is the most important stock exchange in the world, but there are a total of 16 exchanges around the world.

Stock market. Refers in general to the collection of markets and exchanges where the buying, selling and trading of investment vehicles takes place.

Price per share. A simple way of calculating a company’s market value at a given moment. To find the price per share, you take a company’s most recent share price and multiply it by its total number of outstanding shares.

Prospectus. A legal document that contains in-depth information about anything you might be planning to invest in: stocks, bonds or mutual funds.

Posted on June 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

SPACs, or special purpose acquisition companies, are shell companies that are created just to acquire or merge with an existing company, allowing that company to enter public markets without going through an IPO. The catch, however, is the SPAC sponsors have a small window of time—usually within two years—to find a suitable company to acquire.

Carnival popped 6.91% after the cruise line reported impressive earnings and reiterated its healthy financial guidance.

If you can’t beat ‘em, join ‘em: Mastercard rose 2.80% on the news that it will integrate Fiserv’s new stablecoin into its products. Fiserv gained 1.24%.

Lyft gained 6.09% after TD Cowen analysts upgraded the stock, calling the ride-sharing company their “Best SMIDcap Idea for 2025.”

Falling oil prices helped airline stocks soar today: Frontier Group jumped 7.56%, JetBlue Airways rose 4.15%, and American Airlines added 4.31%.

Ambarella soared 20.61% on reports that the chip designer may be exploring a sale.

Nektar Therapeutics exploded 156.29% thanks to strong results in the Phase 2 trial of its new eczema treatment.

Crypto miners rose as investors took on more risk following a ceasefire in the Middle East: CleanSpark climbed 13.45%, Riot Platforms rose 8.09%, and MARA Holdings gained 4.94%.

What’s down

Oil prices fell on news of a ceasefire between Israel and Iran, pulling oil stocks down with them: Exxon Mobil lost 3.04%, Chevron dropped 2.25%, and Occidental Petroleum fell 3.34%.

The ceasefire also sent defense contractors tumbling: Lockheed Martin lost 2.59%, RTX dropped 2.72%, and Northrup Grumman fell 3.20%.

Krispy Kreme fell 0.76% on the news that its deal with McDonald’s has fallen apart due to rising costs.

Posted on June 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Tesla climbed 8.23% thanks to a successful robotaxi debut in Austin this weekend

NorthernTrust popped 8.01% on reports that Bank of New York Mellon is considering acquiring the financial services company.

The stablecoin adoption wave continues to hit markets, with Fiserv up 4.38% after announcing it made deals with Circle and PayPal to roll out a stablecoin and digital-asset platform for banking clients. Circle climbed another 9.64%.

Nuclear energy stocks climbed on the news that New York will build the first major new US nuclear plant in more than 15 years. ConstellationEnergy rose 3.37%, while CentrusEnergy climbed 1.16% and UraniumEnergy gained 2.01%.

SpartanNash exploded 50.62% higher after C&S Wholesale Grocers agreed to acquire the wholesale grocer for $1.77 billion.

What’s down

Tough first day at work: Stellantis sank 0.48% on the day that new CEO Antonio Filosa took the helm at the struggling automaker.

NovoNordisk lost 5.49% after the pharma giant announced disappointing trial results for its newest weight-loss drug.

Super Micro Computer fell 9.77% on the news that it will raise money by offering $2 billion in convertible senior notes.

Wolfspeed plummeted 31.85% after the chipmaker said it plans to file for bankruptcy.

Although many academics argue that value stocks outperform growth stocks, the returns for individuals investing through mutual funds demonstrate a near match.

Introduction

A 2005 study Do Investors Capture the Value Premium? written by Todd Houge at The University of Iowa and Tim Loughran at The University of Notre Dame found that large company mutual funds in both the value and growth styles returned just over 11 percent for the period of 1975 to 2002. This paper contradicted many studies that demonstrated owning value stocks offers better long-term performance than growth stocks.

The studies, led by Eugene Fama PhD and Kenneth French PhD, established the current consensus that the value style of investing does indeed offer a return premium. There are several theories as to why this has been the case, among the most persuasive being a series of behavioral arguments put forth by leading researchers. The studies suggest that the out performance of value stocks may result from investors’ tendency toward common behavioral traits, including the belief that the future will be similar to the past, overreaction to unexpected events, “herding” behavior which leads at times to overemphasis of a particular style or sector, overconfidence, and aversion to regret. All of these behaviors can cause price anomalies which create buying opportunities for value investors.

Another key ingredient argued for value out performance is lower business appraisals. Value stocks are plainly confined to a P/E range, whereas growth stocks have an upper limit that is infinite. When growth stocks reach a high plateau in regard to P/E ratios, the ensuing returns are generally much lower than the category average over time.

Moreover, growth stocks tend to lose more in bear markets. In the last two major bear markets, growth stocks fared far worse than value. From January 1973 until late 1974, large growth stocks lost 45 percent of their value, while large value stocks lost 26 percent. Similarly, from April 2000 to September 2002, large growth stocks lost 46 percent versus only 27 percent for large value stocks. These losses, academics insist, dramatically reduce the long-term investment returns of growth stocks.

***

***

However, the study by Houge and Loughran reasoned that although a premium may exist, investors have not been able to capture the excess return through mutual funds. The study also maintained that any potential value premium is generated outside the securities held by most mutual funds. Simply put, being growth or value had no material impact on a mutual fund’s performance.

Listed below in the table are the annualized returns and standard deviations for return data from January 1975 through December 2002.

Index Return SD

S&P 500 11.53% 14.88%

Large Growth Funds 11.30% 16.65%

Large Value Funds 11.41% 15.39%

Source: Hough/Loughran Study

The Hough/Loughran study also found that the returns by style also varied over time. From 1965-1983, a period widely known to favor the value style, large value funds averaged a 9.92 percent annual return, compared to 8.73 percent for large growth funds. This performance differential reverses over 1984-2001, as large growth funds generated a 14.1 percent average return compared to 12.9 percent for large value funds. Thus, one style can outperform in any time period.

However, although the long-term returns are nearly identical, large differences between value and growth returns happen over time. This is especially the case over the last ten years as growth and value have had extraordinary return differences – sometimes over 30 percentage points of under performance.

This table indicates the return differential between the value and growth styles since 1992.

YEARLY RETURNS OF GROWTH/VALUE STOCKS

Year

Growth

Value

1992

5.1%

10.5%

1993

1.7%

18.6%

1994

3.1%

-0.6%

1995

38.1%

37.1%

1996

24.0%

22.0%

1997

36.5%

30.6%

1998

42.2%

14.7%

1999

28.2%

3.2%

2000

-22.1%

6.1%

2001

-26.7%

7.1%

2002

-25.2%

-20.5%

2003

28.2%

27.7%

2004

6.3%

16.5%

2005

3.6%

6.1%

2006

10.8%

20.6%

2007

8.8%

1.5%

2008

-38.43%

-36.84%

2009

37.2%

19.69%

2010

16.71%

15.5%

2011

2.64%

0.39%

2012

15.25%

17.50%

Source: Ibbottson.

Between the third quarter of 1994 and the second quarter of 2000, the S&P Growth Index produced annualized total returns of 30 percent, versus only about 18 percent for the S&P Value Index. Since 2000, value has turned the tables and dramatically outperformed growth. Growth has only outperformed value in two of the past eight years. Since the two styles are successful at different times, combining them in one portfolio can create a buffer against dramatic swings, reducing volatility and the subsequent drag on returns.

Assessment

In our analysis, the surest way to maximize the benefits of style investing is to combine growth and value in a single portfolio, and maintain the proportions evenly in a 50/50 split through regular rebalancing. Research from Standard & Poor’s showed that since 1980, a 50/50 portfolio of value and growth stocks beats the market 75 percent of the time.

Conclusion

Due to the fact that both styles have near equal performance and either style can outperform for a significant time period, a medical professional might consider a blending of styles. Rather than attempt to second-guess the market by switching in and out of styles as they roll with the cycle, it might be prudent to maintain an equal balance your investment between the two.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

A psychological paradox is a figure of speech that can seem silly or contradictory in form, yet it can still be true, or at least make sense in the context given.

This is sometimes used to illustrate thoughts or statements that differ from traditional ideas. So, instead of taking a given statement literally, an individual must comprehend it from a different perspective. Using paradoxes in speeches and writings can also add wit and humor to one’s work, which serves as the perfect device to grab a reader or a listener’s attention and/or persuade them to action, sales and closing statements. But paradoxes for the financial sector can be quite difficult to explain by definition alone, which is why it is best to refer to a few examples to further your understanding.

One good psychological paradox example is The Paradox of Thrift which suggests that while saving money is generally considered a prudent financial behavior, excessive saving during times of economic downturn can actually hinder economic recovery. When consumers collectively reduce their spending and increase their savings, it creates a decrease in aggregate demand. This reduction in demand can lead to lower production levels, job losses, and ultimately a decline in economic output. In other words, what may be individually rational behavior (financial saving) can have negative consequences for the overall economy.

The following paradoxical contradictions will help financial advisors guide clients to close more sales to the benefit of both.

____

In the intricate world of finance sales, advisors are often at the crossroads of various paradoxes that challenge client decision-making. While the journey towards financial security involves calculated strategies, it’s the nuanced understanding of paradoxes that can help the advisor close more sales.

____

But, what seems trueabout money often turns out to be false, according to colleague Finance Professor John Goodell, PhD from the University Akron:

The more we try to trade our way to profits, the less likely we are to profit.

The more boring an investment—think index funds—the more exciting the long-run performance will probably be.

The more exciting an investment—name your latest Wall Street concoction, Special Purpose Acquisition Company [SPAC] or anything crypto—the less exciting the long-term results typically are.

The only certainty is uncertainty and the only constant is change. Today’s market decline will eventually become a bull market, and today’s market leaders will eventually yield to other stocks.

Big market trends play a huge role in investment results, and yet trying to time macroeconomic cycles or guess which market sectors will outperform is a fool’s errand. Many big market rotations are set in motion by something wholly unanticipated, like a virus pandemic or a war.

To be happy when wealthy, we also need to be happy with far less money. The fact is, above a relatively modest income level, no amount of extra money will change our level of happiness. More money might even make us miserable, as many lottery winners have discovered.

The more we hate an investing trait—or any trait for that matter—the more likely it is that we’re resisting seeing that trait in ourselves. It’s what Carl Jung MD called the Shadowof Undesirable Personality Aspects that we hide from ourselves. Do prospects get irritated listening to your unsolicited financial advice? There’s a good chance that you often give unsolicited financial advice but don’t like to admit it.

The more we learn about investing, the more we realize we don’t know anything. We should just buy index funds and instead spend our time worrying about stuff we can actually control.

The more an investor is convinced he’s right, the more likely he is to be wrong. Short sellers, in particular, are likely to succumb to this paradoxical trap.

The more options we have, the less satisfied we’ll be with each one. This is the Paradox of Choice; revised. Anyone who has spent hours “optimizing” his or her portfolio knows this all too well. Its close cousin is information overload, another frustration paradox when investing.

The more afraid we are of losing money, the more likely we are to take unwitting risks that lose us money. Sitting in cash seems wise during market selloffs. But the truth is, none of us can reliably time the market. Pull up any chart of the stock market over any period longer than a decade and you’ll see that the riskiest decision is sitting in cash, which gets destroyed by inflation.

The more we think about our investments and look at our financial accounts, the more likely we are to damage our results by buying high because of greed and selling low because of fear. It can pay to look away.

ASSESSMENT

How should you respond to these financial paradoxes? As you plan for your own financial future, as well as your own client prospecting endeavors, embrace the concept of “loosely held views.”

In other words, make financial and client acquisitions plans, but continuously update your views, question your assumptions and paradoxes and rethink your priorities. Years of experience with clients certainly support the futility of trying to help them change their financial behavior by telling them what they “should” know or do.

CONCLUSION

Remember, it is far more useful to listen to client beliefs, fears and goals, and to suggest options and offer encouragement to help them discover their own path toward financial well-being. Then, incentivize them with knowledge of the above psychological paradoxes to your mutual success!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Marcinko, DE and Hetico, HR: Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2016.

Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York. 2006

Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2015.

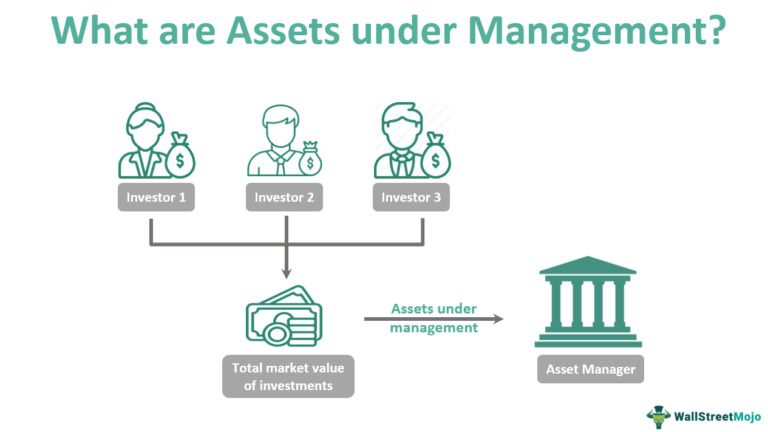

Assets under management (AUM) is a significant parameter in the financial world. It answers financial questions like – how many investments does a company manage? What is the net value of the investments that the company manages? Finally, how many investors have trusted their assets with the company? The higher the answer to these three questions, the more glory to the company.

A wealthy investor who is not concerned by higher fees but wants maximum returns of their asset will probably choose an asset manager based on its AUM. Thus, the AUM indicates the financial performance of the firm. Also, based on the funds under management, the firm collects fees from other clients.

So, what are the investments which qualify as AUM? Any liquid asset of the investor they have entrusted the asset manager with monitoring and control. For example, bank deposits, cash balances, equity shares, bonds, mutual funds, and other investments.

What are the services an asset manager provides to their clients? The most important function is decision-making. With the constant fluctuations and rapid movements in the market, an asset manager has to make decisions about holding or selling an investment. The firm communicates with the investors and advises them about the necessary action.

Once the decision is taken, the firm acts on the decision, i.e., the investor does not have to enter the field. In addition, the asset management company will buy, sell, and make any other transactions on behalf of the investor. Finally, the firm also renders services like accounting, tax reporting, proxy voting (equity shares), client reporting, and other financial services.

What are Assets Under Advisement?

Assets under advisement refer to assets on which your firm provides advice or consultation but for which your firm does either does not have discretionary authority or does not arrange or effectuate the transaction. Such services would include financial planning or other consulting services where the assets are used for the informational purpose of gaining a full perspective of the client’s financial situation, but you are not actually placing the trade.

Assets under advisement could also be those which you monitor for a client on a non-discretionary basis, where you may make recommendations but where the client is the party responsible for arranging or effecting the purchase or sale. A common example of this scenario is when an adviser reviews a participant’s 401(k) allocations. If the adviser does not have the authority or ability to effect changes in the portfolio, these assets are likely considered assets under advisement rather than regulatory assets under management.

Assets under advisement are permitted to be disclosed on Form ADV Part 2A as a separate asset figure from the assets under management. There is no requirement to disclose the assets under advisement figure, but some advisers opt to include the figure to give prospective clients a more complete picture of the firm’s responsibilities. If you choose to report your assets under advisement, be sure to make a clear distinction between this figure and your regulatory assets under management.

Posted on June 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Stocks: Israel and Iran exchanged missile strikes for a fourth day, but investors are betting that the conflict will remain at least somewhat contained. Reports that Iran wants to de-escalate the conflict and even restart nuclear talks seemed to underline that idea, and markets rose strongly throughout the afternoon.

Commodities: Gold fell as hopes of a ceasefire between Israel and Iran made investors more bullish, while Iranian oil infrastructure was spared from the attacks, pushing crude prices lower.

Bonds: A $13 billion 20-year bond auction this afternoon yielded strong demand, rounding out a series of solid auctions over the last few days that seemingly point to renewed investor confidence in US fixed income.

Alternatively Weighted Exchange Traded Funds are designed to track an index that is constructed based on criteria other than market capitalization (the methodology used for most traditional indexes).

Instead, alternatively weighted indexes select and weight securities based on other factors, such as growth, valuation, and price momentum, among others. Examples include:

Invesco S&P 500 Equal Weight ETF (NYSEARCA: RSP)

SPDR Technology ETF (NYSEARCA: XNTK)

First Trust NYSE Arca Biotechnology Index Fund (NYSEARCA: FBT)

Amplify Online Retail ETF (NASDAQ: IBUY)

iShares MSCI USA Equal Weighted ETF (NYSEARCA: EUSA)

Posted on June 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

***

***

Markets: Brace for +/- volatility as US markets reopen this morning, with the escalating Israel–Iran conflict dominating investors’ Bloomberg Terminals.

Stocks fell the most in nearly a month on Friday, and the prospect of an oil supply shock sent crude prices 7% higher, their biggest one-day gain in years. Through it all, the S&P 500 is less than 3% from its record high.

Combined, both the DOW and NASDAQ are up over 750 points, today!