BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

“What is good for the goose is good for the gander”

By Rick Kahler CFP®

There is an old adage that says, “What is good for the goose is good for the gander.”

In today’s urbanized world, most of us probably wouldn’t have the slightest idea what’s good for geese. Yet we still know that this saying reminds us to be cautious about anyone who makes recommendations they don’t follow themselves.

This is especially important when it comes to investment advice.

Duopoly

Have you ever wondered how your investment advisor invests their money? Have you wondered if the agent selling you cash value life insurance as a retirement investment is investing their retirement in the same? Or whether an advisor recommending a specific mutual fund, stock investment, or bond issue buys the same for their own portfolio?

Ask

My suggestion is to stop wondering and ask. I rarely have a client or prospective client ask me whether I invest my own money in the same way I invest the funds of clients. Most people think it is just too personal to ask how an advisor is investing their own funds and that the advisor may take offense.

Yet knowing how anyone offering investment advice to you invests their own funds is highly relevant. It’s especially wise to ask this if someone is trying to sell you on an “exciting opportunity” that sounds too good to be true. An evasive or vague answer is an obvious red flag. But even with a fiduciary advisor, I believe asking how they invest their own money is a legitimate question. I for one am happy to answer it. Yes, the investment vehicles and strategies I recommend for clients are the same ones I use for myself.

If an advisor is recommending a strategy or investment for you that they don’t subscribe to or invest in themselves, then it’s a good idea to ask another question.

Why not?

Certainly, there are good reasons why an advisor would not have the same asset allocation that they recommend for you. They may be significantly younger or older, or they may have a significantly more aggressive or adverse tolerance for risk. But if your advisor outsources your investments to SEI but uses Vanguard for themselves, I would want to explore that. Or if your advisor is about the same age as you are, but has a significantly different asset allocation and uses none of the investments she recommends that you invest in, I would want to know why.

If an advisor suggests that you put 35% of your investment funds into a private REIT but they don’t own a private REIT, what’s the reason? Or if they are recommending you own a managed futures limited partnership but they don’t own that same partnership or any managed futures funds. Or, maybe they are recommending the A shares of an actively managed mutual fund but themselves purchase passively managed institutional shares.

If you don’t feel comfortable or knowledgeable enough to ask questions like these about specific investments, it’s still important to find out about an advisor’s broader approach to investing. Do they recommend that you “buy and hold,” yet they actively time the market with their own portfolio? Or maybe they actively trade your portfolio while following a “buy and hold” strategy themselves.

Assessment

While portfolio specifics might vary, I want any investment advisor to buy into the same investment philosophy they are recommending to me. If they are going to be timing the market with my funds, I want them to be making the same market moves with their own funds.

If a “sauce” isn’t good enough for the advisor personally, it isn’t good enough to recommend to clients.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Posted on October 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The SPX fell 1.74 points (–0.03%) to 5,808.12 to end the week down 0.96%; the $DJI lost 259.96 points (–0.61%) to 42,114.40 to end the week down 2.68%; and the $COMP rose 103.12 points (0.56%) to 18,518.61 to end the week up 0.16%.

The 10-year Treasury note yield (TNX) added three basis points to 4.23%.

The CBOE Volatility Index® (VIX) climbed sharply to 19.95, nearing recent highs. The 20 level is an area to watch next week, as it traditionally signals more volatile markets.

Pick a direction already: On Wednesday, Spirit Airlines soared 30% on news of a possible merger with Frontier. On Thursday, shares plunged 21% as investors took their profits. Today, shares are back up 15.05% after Spirit announced it will cut jobs and sell planes in an effort to boost profits.

Texas Roadhouse sizzled like a porterhouse T-bone, rising 3.58% after announcing that earnings rose 32% last quarter.

Deckers Outdoor popped 10.57% thanks to soaring demand for Hoka shoes, helping the footwear company beat earnings estimates and raise forecasts.

Newell Brands may not be a household name, but they make household goods like Sharpies, Elmer’s Glue, and Crock-Pot—all things that people bought a ton of last quarter, which is why shares soared 21.59% today.

Apple is just fine, thanks: The Market Cap King got a rare analyst downgrade from KeyBanc, which is worried about lower demand from China. Shareholders were unfazed, and the stock rose 0.36%.

STOCKS DOWN

AutoNation hasn’t shaken off the aftereffects of a major cyberattack in July just yet, which is why revenue and earnings both missed estimates last quarter. Shares fell 4.46% today.

Colgate-Palmolive announced a beat-and-raise quarter, but it wasn’t enough to impress shareholders, who pushed the consumer staples giant down 4.14%.

Mohawk Industries was the worst-performing stock on the market at one point today, falling 13.70% after the flooring manufacturer reported disappointing earnings and lowered its fiscal forecast.

Online education company Coursera got an F from shareholders after the company lowered its revenue guidance for the full fiscal year. Shares dropped 9.83%.

Newmont had its worst day in over a decade yesterday after the gold miner reported shockingly bad earnings, with higher costs offsetting the rising price of gold. Shares continued to fall 1.69% today.

Posted on October 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Applications to MBA programs are up 12% in 2024 after declining for two years, according to the Graduate Management Admission Council, which surveys business school admissions offices.

Apple and Goldman Sachs were ordered to pay $89 million by the Consumer Financial Protection Bureau for failing to address thousands of consumer disputes of Apple Card transactions.

Apple is cutting production of Vision Pro due to slow sales. The tech giant is scaling down production of its $3,500 Vision Pro VR headset and might halt assembly of new ones next month,

UPS delivered a strong earnings report, with revenue beating analyst expectations for the first time in two years. Shares popped 5.28%.

ServiceNow rose 5.41% to a new all-time high thanks to a beat-and-raise third-quarter earnings report powered by higher AI demand for the enterprise software company.

Whirlpool climbed 11.20% after announcing solid earnings and reiterating guidance for the rest of the fiscal year, reassuring worried shareholders.

Molina Healthcare soared 17.67% after beating both top and bottom line estimates in the third quarter, thanks to the health insurer reaping the rewards of higher Medicaid payouts.

STOCKS DOWN

IBM dropped 6.17% on disappointing third-quarter results, missing on both top and bottom line forecasts thanks to lower consulting and infrastructure revenue.

Peloton pedaled higher yesterday after Greenlight Capital’s David Einhorn declared that the company was undervalued while he was pedaling on a Peloton. The stunt only worked for a quick sprint, though, with shares back down 2.07% today.

TKO Group Holdings got hit with a piledriver after the owner of the WWE and UFC announced it is acquiring several entertainment companies, including Professional Bull Riders. Investors bucked shares off 8.69%.

Keurig Dr. Pepper fizzled 4.80% thanks to lower sales last quarter, though the company is trying to bolster revenue by acquiring energy drink maker Ghost.

Air taxi startup Lilium crashed 61.50% on the news that its main subsidiaries have run out of cash and are filing for insolvency.

The S&P 500® index (SPX) rose 12.44 points (0.21%) to 5,809.86; the $DJI fell 140.59 points (–0.33%) to 42,374.36; and the NASDAQ Composite® ($COMP) added 138.83 points (0.76%) to 18,415.49.

The 10-year Treasury note yield fell four basis points to 4.20%.

The CBOE Volatility Index® (VIX) was about flat at 19.18.

PRUDENT BUYER: The efficient purchaser of market balance between value and cost.

PRUDENT MAN RULE: An 1830 court case stating that a person in a fiduciary capacity (a trustee, executor, custodian, etc) must conduct him/herself faithfully and exercise sound judgment when investing monies under care. “He is to observe how men of prudence, discretion and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent distribution of their funds, considering the probable income as well as the probable safety of the capital to be invested.” Allows for mutual funds and variable annuities.

PRUDENT INVESTOR RULE: A fiduciary is required to conduct him/herself faithfully and exercise sound judgment when investing monies and take measured and reasonable investment risks in return for potential future rewards. Allows for mutual funds, stocks, bonds, variable annuities asset allocation & Modern Portfolio Theory.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives.4 A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.

NOTE: Dr. Marcinko is a former Certified Financial Planner and current Certified Medical Planner™. He has been a medical management advisor for more than a decade. He is the CEO of http://www.MarcinkoAssociates.com

The authors acknowledge the assistance of Mackenzie H. Marcinko PhD in the preparation of this article.

Posted on October 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Yep – Even the Smart Folks!

By Lon Jefferies MBA CMP® CFP®

Dr. David Edward Marcinko MBA MEd CMP®

In the Business Insider, Mandi Woodruff describes nine mental blocks that cause smart people to do dumb things. Review the list and itemize the factors that have negatively impacted your finances.

The Factors

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia (or nearsightedness) makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Confirmation bias causes us to place more emphasis on information that supports the opinion we already have. Consequently, we tend to ignore or downplay opinions that don’t mirror our own, leading us to make uninformed decisions.

NOTE: An interesting example of the confirmation bias is the case of David Rosenberg, who is one of the most well-known perpetual bears on Wall Street. In October, Mr. Rosenberg’s analysis forced him to warm to the current investment environment. His fans and followers, rather than appreciating his research and ability to adjust to new information, criticized him for changing his opinion.

As it turned out Mr. Rosenberg had fans not because of his expert analysis, but because he added intellectual heft to his followers pessimism and quasi-political desire for the system to collapse. Their view was that things were in permanent decline and his analysis, charts, and voice added respectability to their pre-existing bias. Mr. Rosenberg has now lost his fan base not because he was wrong for the last four years, but because he changed his mind.

Loss aversion affected many investors during the crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often underperform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Assessment

The good news is that being aware of these tendencies can help us avoid mistakes. We’ll never be perfect, but avoiding detrimental decisions based on mental prejudices can give us an advantage in our financial and retirement planning efforts.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on October 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

CVS Health may be breaking up…with itself. The board of directors at CVS Health—the parent company of CVS Pharmacy, pharmacy benefit managerCVS Caremark, and insurance unit Aetna—are working with a group of bankers to review the company’s strategy, which according to Reuters, may lead to a split between its pharmacy division and Aetna.

Apple climbed 1.23% on a Bloomberg report that iPhone 16 demand has been shockingly strong in China.

Verizon Communications will purchase $1 billion worth of US Cellular’s wireless spectrum licenses. Verizon rose just 0.34%—but it’s a huge deal for US Cellular, which popped 7.22%, and Telephone and Data Systems, which owns 82% of US Cellular, and soared 15.40%.

Intuitive Surgical rose to a new all-time high, climbing 10.01% on strong earnings powered by sales of its da Vinci device.

Lamb Weston, the company behind the french fries you overindulge in every time you go out to dinner, is being pushed by activist investor Jana Partners toward exploring a sale. Shareholders rejoiced, and the stock rose 10.17%.

Stocks Down

CVS Health sank 5.23% on the news that CEO Karen Lynch will be replaced by David Joyner after three years at the helm of the struggling pharmacy/retailer. Joyner ran the company’s pharmacy service business for the last two years.

WD-40 seems like the staple of all consumer staples, but the company missed on both revenue and earnings estimates last quarter. Shares fell 4.79% on the news.

American Express dropped 3.15% after the credit card company reported a rare miss today, beating bottom-line estimates but missing revenue forecasts last quarter.

MGP Ingredients makes all the booze you drink under different brand names, but people aren’t drinking enough. The beverage maker issued preliminary earnings that included a 24% drop in sales. Shares tanked 24.16%.

Here’s where the major stock market benchmarks ended:

The S&P 500® index (SPX)rose 23.20 points (0.40%) to 5,864.67, a new record high close, to end the week up 0.85%; the Dow Jones Industrial Average® ($DJI) added 36.86 points (0.09%) to 43,275.91, also another record high finish, to end the week up 0.96%; and the $COMP gained 115.94 points (0.63%) to 18,489.55 to end the week up 0.80%.

The 10-year Treasury note yield (TNX) fell two basis points to 4.07%.

The CBOE Volatility Index® (VIX) fell to 18.17, the lowest since September 30.

A new survey results may prompt health systems to second-guess some of their future plans. A recent University of Michigansurvey found 74% of adults ages 50+ have “very little or no trust” in health info generated by AI. Maybe it’s not time to roll out chatbots on patient portals just yet.

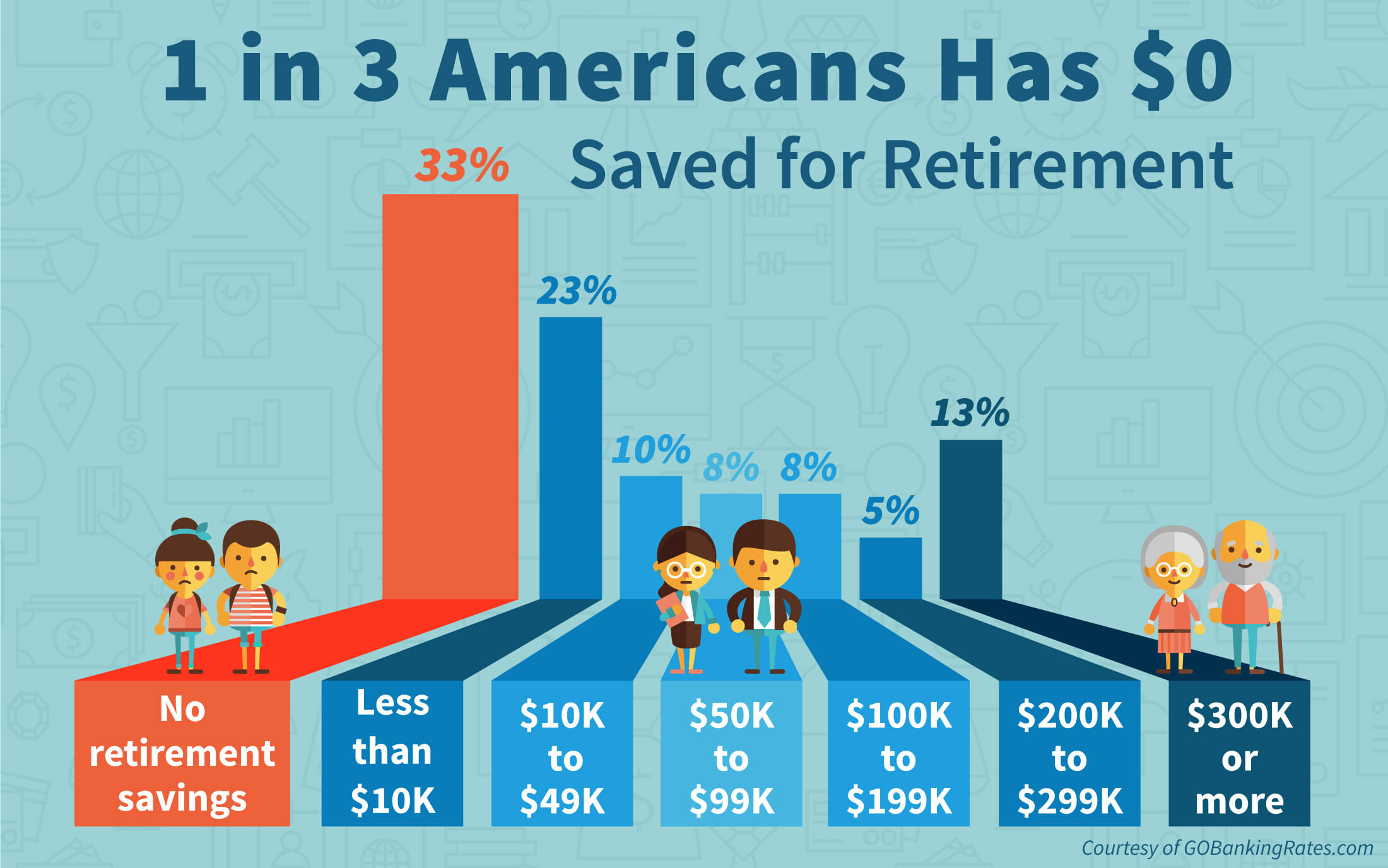

According to the National Institute on Retirement Security, almost 40 million households have no retirement savings at all. The Employee Benefit Research Institute (EBRI) estimates in its 2019 Retirement Security Projection Model that America’s current retirement savings deficit is $3.8 trillion.

What does that mean? Well, the EBRI report aggregates the savings deficit of all U.S. households headed by someone between the ages of 35 and 64, inclusive. In total, those households have $3.8 trillion fewer dollars in savings than they should have for retirement.

For more recent data, Fidelity Investments reported that in the third quarter of 2022 the average account balance for an IRA was $101,900. Employees with a 401(k) averaged $97,200, while those with a 403(b) had $87,400.

Fidelity also estimated that “an average retired couple age 65 in 2022 may need approximately $315,000 saved (after tax) to cover health care expenses in retirement.” Keeping in mind that more Americans are also living longer than ever before, they will face more challenges to cover medical expenses in retirement.

Financial planning as a concept has been around for a long time, but not as we know it today. When Loren Dunton set up the Society for Financial Counseling Ethics in 1969, or when the first graduating class of the College of Financial Planning graduated in 1973, financial planning was very different. It was centered around selling limited partnerships, which came to end with the Tax Reform Act of 1986.

However, financial planning re-emerged — all thanks to Richard Averitt III. The certified financial planner gave new meaning to financial planning, this time with a focus on who the client is and what their needs are. This approach was purely methodological in nature.

Soon after, financial planning picked up again. According to the Certified Financial Planner (C.F.P.) Board of Standards in Denver, today, there are more than 94,000 C.F.P.s worldwide, including over 48,000 in the U.S. Additionally, there are also organizations that have been set up for C.F.P.s, such as the Financial Planning Association (FPA), which has approximately 22,000 members.

And, don’t forget the emerging Certified Medical Planner™ professional fiduciary designation for physicians, dentists, nurses and allied healthcare clients.

Financial planning, as we know it now, includes investing, tax planning, retirement planning, and basically other ways to get your finances in order and create mindful budgets to ensure a safe and secure future. Getting a step ahead of your spending and finances is beneficial in the long run and Financial Planning Month in October is the perfect time to do that.

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Authors of the seminal textbook Why Nations Fail, Daron Acemoglu, James Robinson, and former International Monetary Fund chief economist Simon Johnson will split the roughly $1 million cash prize for their research, which found a link between a country’s prosperity and the institutions it established during European colonization.

Places developed either “inclusive” or “extractive” institutions based on population density. The former allowed for inclusive governance (i.e., democracy), while the latter extracted resources to benefit a small group of elites.

Countries that developed inclusive institutions have experienced long-term prosperity; those with exclusive institutions haven’t. “Broadly speaking, the work that we have done favors democracy,” Acemoglu said.

Eample: In the twin cities of Nogales, on the US-Mexico border, the north and south parts of the transborder city have the same climate and the same resources, but the section in the US is far richer because of the country’s institutions, according to the researchers.

Critics. Some academics argue the Nobel winners’ premise ignores the effects of culture on prosperity. Others point to an irrefutable counterexample: China continues to experience explosive growth despite having an autocratic government.

Marcinko & Associates is financial guide. We help answer your questions in an empowering way. We educate and guide medical colleagues to understand their financial picture and to make better financial decisions. We strive to simplify everything, clear up confusion, and address specific needs and goals.

Simply put, we’re a financial services company on a mission to empower financial freedom for all healthcare professionals; only. We work with doctors, nurses, medical providers, individuals and all sizes of organizations to offer investment, wealth management and retirement solutions so everyone can have a clear and simple understanding of where their finances and career is today and where it is headed tomorrow.

Whatever your financial situation, we do not shame, criticize, or sell. We enrich, educate and empower. We work only with medical colleagues at every stage of their financial journey [students, interns, residents, practitioners, mid-career and mature physicians], through big life personal changes to annual employment reviews, in order to help them understand, invest, and protect their money and lifestyle.

Assess, develop, and align financial retirement and estate planning goals

Risk Management: Malpractice, home, life, medical, auto and personal indemnity

Life Insurance Need Reviews: whole, universal and term

Business, operations, HR, employment negotiations and medical practice management

Annuity Need Reviews: Indexed and Fixed [Pros and Cons].

***

***

At Marcinko & Associates we discuss specific needs and answer specific questions. We educate and make personalized recommendations that you are free to use, incorporate or disregard. Referrals to trusted specialists and strategic alliance partners then occur if – and as – needed [pro re nata].

According to Wikipedia, Front Running, also known as Tailgating, is the prohibited practice of entering into an equity (stock) trade, option, futures contract, derivative, or security-based swap to capitalize on advance, nonpublic knowledge of a large pending transaction that will influence the price of the underlying security.

Front running is considered a form of market manipulation in many markets. Cases typically involve individual brokers or brokerage firms trading stock in and out of undisclosed, un-monitored accounts of relatives or confederates. Institutional and individual investors may also commit a front running violation when they are privy to inside information. A front running firm either buys for its own account before filling customer buy orders that drive up the price, or sells for its own account before filling customer sell orders that drive down the price.

Front running is prohibited since the front-runner profits from nonpublic information, at the expense of its own customers, the block trade, or the public market.

Scandals

In 2003, several hedge fund and mutual fund companies became embroiled in an illegal late trading scandal made public by a complaint against Bank of America brought by New York Attorney General Eliot Spitzer. A resulting U.S. Securities and Exchange Commission investigation into allegations of front-running activity implicated Edward D. Jones & Co., Inc., Goldman Sachs, Morgan Stanley, Strong Mutual Funds, Putnam Investments, Invesco, and Prudential Securities.

Following interviews in 2012 and 2013, the FBI said front running had resulted in profits of $50 million to $100 million for the bank. Wall Street traders may have manipulated a key derivatives market by front running Fannie Mae and Freddie Mac.

Term Origins

The terms originate from the era when stock market trades were executed via paper carried by hand between trading desks. The routine business of hand-carrying client orders between desks would normally proceed at a walking pace, but a broker could literally run in front of the walking traffic to reach the desk and execute his own personal account order immediately before a large client order.

Likewise, a broker could tail behind the person carrying a large client order to be the first to execute immediately after. Such actions amount to a type of insider trading, since they involve non-public knowledge of upcoming trades, and the broker privately exploits this information by controlling the sequence of those trades to favor a personal position.

Assessment

So, was front-running implicated in the market drop today? OR, a technical correction or Panic selling? Any thoughts.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Posted on October 14, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

U.S. stock markets, including the New York Stock Exchange and the NASDAQ remain open and follow a regular schedule today.

The bond markets will be closed, however.

***

***

Stocks ended last week on a high note, closing out their fifth straight week of gains. The Dow was pushed to yet another new all-time high by strong earnings from JPMorgan, while the S&P 500 was in the green and rose to its own record close, and the NASDAQ clawed its way out of the red by early Friday afternoon.

Bond yields took a breather, falling below 4.1% thanks to a better-than-expected PPI report that helped offset inflation fears that had re-arisen after a worse-than-expected CPI report.

Gold rose as well on PPI news, since the data pointed to a better chance of more rate cuts ahead.

Oil fell a bit but gained over the last two weeks on geopolitical tensions and destruction in the Gulf of Mexico following the two major hurricanes.

The following are some of the most common psychological biases. Some are learned while others are genetically determined (and often socially reinforced). While this essay focuses on the financial implications of these biases, they are prevalent in most areas in life.

[A] Incentives

It is broadly accepted that incenting someone to do something is effective, whether it be paying office staff a commissions to sell more healthcare products, or giving bonuses to office employees if they work efficiently to see more HMO patients. What is not well understood is that the incentives cause a sub-conscious distortion of decision-making ability in the incented person. This distortion causes the affected person – whether it is yourself or someone else – to truly believe in a certain decision, even if it is the wrong choice when viewed objectively. Service professionals, including financial advisors and lawyers, are affected by this bias, and it causes them to honestly offer recommendations that may be inappropriate, and that they would recognize as being inappropriate if they did not have this bias. The existence of this bias makes it important for each one of us to examine our incentive biases and take extra care when advising physician clients, or to make sure we are appropriately considering non-incented alternatives.

[B] Denial

Denial is a well known, but under-appreciated, psychological force. Physicians, clients and professionals (like everyone else) are prone to the mistake of ignoring a painful reality, like putting off an unpleasant call (thus prolonging a problematic situation and potentially making it worse) or not opening account statements because of the desire not to see quantitative proof of losses. Denial also manifests itself by causing human beings to ignore evidence that a mistake has been made. If you think of yourself as a smart person (and what professional doesn’t?), then evidence pointing to the conclusion that a mistake has been made will call into question that belief, causing cognitive dissonance. Our brains function to either avoid cognitive dissonance or to resolve it quickly, usually by discounting or rationalizing the disconfirming evidence. Not surprisingly, colleagues at Kansas State University and elsewhere, found that financial denial, including attempts to avoid thinking about or dealing with money, is associated with lower income, lower net worth, and higher levels of revolving credit.

[C] Consistency and Commitment Tendency

Human beings have evolved – probably both genetically and socially – to be consistent. It is easier and safer to deal with others if they honor their commitments and if they behave in a consistent and predictable manner over time. This allows people to work together and build trust that is needed for repeat dealings and to accomplish complex tasks. In the jungle, this trust was necessary to for humans to successfully work as a team to catch animals for dinner, or fight common threats. In business and life it is preferable to work with others who exhibit these tendencies. Unfortunately, the downside of these traits is that people make errors in judgment because of the strong desire not to change, or be different (“lemming effect” or “group-think”). So the result is that most people will seek out data that supports a prior stated belief or decision and ignore negative data, by not “thinking outside the box”. Additionally, future decisions will be unduly influenced by the desire to appear consistent with prior decisions, thus decreasing the ability to be rational and objective. The more people state their beliefs or decisions, the less likely they are to change even in the face of strong evidence that they should do so. This bias results in a strong force in most people causing them to avoid or quickly resolve the cognitive dissonance that occurs when a person who thinks of themselves as being consistent and committed to prior statements and actions encounters evidence that indicates that prior actions may have been a mistake. It is particularly important therefore for advisors to be aware that their communications with clients and the press clouds the advisor’s ability to seek out and process information that may prove current beliefs incorrect. Since this is obviously irrational, one must actively seek out negative information, and be very careful about what is said and written, being aware that the more you shout it out, the more you pound it in.

[D] Pattern Recognition

On a biological level, the human brain has evolved to seek out patterns and to work on stimuli-response patterns, both native and learned. What this means is that we all react to something based on our prior experiences that had shared characteristics with the current stimuli. Many situations have so many possible inputs that our brains need to take mental short cuts using pattern recognition we would not gain the benefit from having faced a certain type of problem in the past. This often-helpful mechanism of decision-making fails us when past correlations or patterns do not accurately represent the current reality, and thus the mental shortcuts impair our ability to analyze a new situation. This biologic and social need to seek out patterns that can be used to program stimuli-response mechanisms is especially harmful to rational decision-making when the pattern is not a good predictor of the desired outcome (like short term moves in the stock market not being predictive of long term equity portfolio performance), or when past correlations do not apply anymore.

[E] Social Proof

It is a subtle but powerful reality that having others agree with a decision one makes, gives that person more conviction in the decision, and having others disagree decreases one’s confidence in that decision. This bias is even more exaggerated when the other parties providing the validating/questioning opinions are perceived to be experts in a relevant field, or are authority figures, like people on television. In many ways, the short term moves in the stock market are the ultimate expression of social proof – the price of a stock one owns going up is proof that a lot of other people agree with the decision to buy, and a dropping stock price means a stock should be sold. When these stressors become extreme, it is of paramount importance that all participants in the financial planning process have a clear understanding of what the long-term goals are, and what processes are in place to monitor the progress towards these goals. Without these mechanisms it is very hard to resist the enormous pressure to follow the crowd; think social media.

[F] Contrast

Sensation, emotion and cognition work by contrast. Perception is not only on an absolute scale, it also functions relative to prior stimuli. This is why room temperature water feels hot when experienced after being exposed to the cold. It is also why the cessation of negative emotions “feels” so good. Cognitive functioning also works on this principle. So one’s ability to analyze information and draw conclusions is very much related to the context with in which the analysis takes place, and to what information was originally available. This is why it is so important to manage one’s own expectations as well as those of clients. A client is much more likely to be satisfied with a 10% portfolio return if they were expecting 7% than if they were hoping for 15%.

[G] Scarcity

Things that are scarce have more impact and perceived value than things present in abundance. Biologically, this bias is demonstrated by the decreasing response to constant stimuli (contrast bias) and socially it is widely believed that scarcity equals value. People who feel an opportunity may “pass them by” and thus be unavailable are much more likely to make a hasty, poorly reasoned decision than they otherwise would. Investment fads and rising security prices elicit this bias (along with social proof and others) and need to be resisted. Understanding that analysis in the face of perceived scarcity is often inadequate and biased may help professionals make more rational choices, and keep clients from chasing fads.

[H] Envy / Jealousy

This bias also relates to the contrast and social proof biases. Prudent financial and business planning and related decision-making are based on real needs followed by desires. People’s happiness and satisfaction is often based more on one’s position relative to perceived peers rather than an ability to meet absolute needs. The strong desire to “keep up with the Jones” can lead people to risk what they have and need for what they want. These actions can have a disastrous impact on important long-term financial goals. Clear communication and vivid examples of risks is often needed to keep people focused on important financial goals rather than spurious ones, or simply money alone, for its own sake.

[I] Fear

Financial fear is probably the most common emotion among physicians and all clients. The fear of being wrong – as well as the fear of being correct! It can be debilitating, as in the corollary expression on fear: the paralysis of analysis.

According to Paul Karasik, there are four common investor and physician fears, which can be addressed by financial advisors in the following manner:

Fear of making the wrong decision: ameliorated by being a teacher and educator.

Fear of change: ameliorated by providing an agenda, outline and/or plan.

Fear of giving up control: ameliorated by asking for permission and agreement.

Fear of losing self-esteem: ameliorated by serving the client first and communicating that sentiment in a positive manner.

Now, as human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist:

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often under-perform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

A class action lawsuit has been filed in Minnesota against UnitedHealth Group (NYSE:UNH) over allegations that the health insurer and its subsidiary, NaviHealth, used a faulty algorithm to deny rehabilitation care for Medicare Advantage beneficiaries. California-based Clarkson Law Firm filed the lawsuit in the U.S. District Court of Minnesota on Tuesday following an investigative report published by the health-focused news site Stat.

It alleges that UnitedHealth and its subsidiary, NaviHealth, used the computer algorithm named nH Predict to “systematically deny claims” of patients recovering from debilitating illnesses in nursing homes. According to the lawsuit, despite its 90% error rate, the company used the algorithm to deny claims, knowing that only 0.2% would appeal its decision. According to Stat, Humana (HUM), the nation’s second-largest player in the Medicare Advantage market behind UnitedHealth (UNH), also uses nH Predict. UnitedHealth (UNH) denied it used the NaviHealth predict tool to arrive at coverage decisions.

***

***

Ironically, UnitedHealth’s (NYSE:UNH) Optum Rx unit announced plans to move eight insulin products to “preferred” status on formularies to further expand the number of patients benefiting from $35 or less monthly out-of-pocket costs for the lifesaving therapy.

Optum Rx, UNH’s pharmacy benefit manager (PBM), said that effective January 1, 2024, all short- and rapid-acting insulins will move to Tier 1 in commercial formularies, a list of drugs the company maintains to indicate coverage for insured patients.

Posted on October 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

October continues to be a tough month for stocks, with all three major indexes spending yesterday afternoon in the red. The Dow in particular had a horrible day and dropped over 500 points, while major tech stocks were pushed lower by a series of analyst downgrades.

Oil continued its hot streak yesterday, rising above $77 on the back of geopolitical conflict in the Middle East. That helped ensure that, while everything else fell, energy was the only positive sector in the S&P 500.

Gold has often found itself rising in tandem with crude, though it broke that habit, with the shiny safe haven dropping a hair as investors digest the idea that the Fed’s next interest rate cut may be smaller than they thought.

Bitcoin broke above $64,000 for a moment yesterday only to be yanked back down, as crypto traders ride out the recent volatility.

Posted on October 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

IN PRIVATE EQUITY AND MEDICINE

By Staff Reporters

***

***

PRIVATE EQUITY

In private equity, the J curve is used to illustrate the historical tendency of private equity funds to deliver negative returns in early years and investment gains in the outlying years as the portfolios of companies mature.

And, according to Wikipedia, in the early years of the fund, a number of factors contribute to negative returns including management fees, investment costs and under-performing investments that are identified early and written down. Over time the fund will begin to experience unrealized gains followed eventually by events in which gains are realized (e.g., IPOs, mergers and acquisitions, leveraged recapitalizations).

Historically, the J curve effect has been more pronounced in the US, where private equity firms tend to carry their investments at the lower of market value or investment cost and have been more aggressive in writing down investments than in writing up investments. As a result, the carrying value of any investment that is under performing will be written down but the carrying value of investments that are performing well tend to be recognized only when there is some kind of event that forces the PE to mark up the investment.

The steeper the positive part of the J curve, the quicker cash is returned to investors. A private equity firm that can make quick returns to investors provides investors with the opportunity to reinvest that cash elsewhere. Of course, with a tightening of credit markets, private equity firms have found it harder to sell businesses they previously invested in. Proceeds to investors have reduced. J curves have flattened dramatically. This leaves investors with less cash flow to invest elsewhere, such as in other private equity firms. The implications for private equity could well be severe. Being unable to sell businesses to generate proceeds and fees means some in the industry have predicted consolidation among private equity firms.

MEDICINE

In medicine, the “J curve” refers to a graph in which the x-axis measures either of two treatable symptoms (blood pressure or blood cholesterol level) while the y-axis measures the chance that a patient will develop cardiovascular disease (CVD). It is well known that high blood pressure or high cholesterol levels increase a patient’s risk.

Paradoxically, what is less well known is that plots of large populations against CVD mortality often take the shape of a J curve which indicates that patients with very low blood pressure and/or low cholesterol levels are also at increased risk.

Posted on September 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Markets: Wall Street life was looking good last week as all the major indexes clinched their third consecutive winning week. Stocks were a mixed bag for Friday, but the Dow Jones scored another record close. Bristol Myers Squibb rose after the FDA approved its schizophrenia drug as the first new treatment for the condition in decades.

Economy: The FOMC’s favorite inflation gauge came in lower than expected for last month, likely clearing the way for Jerome Powell and the Federal Reserve to keep cutting interest rates.

Posted on September 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

Tropical Storm Helene made landfall in Florida last night as a Category 4 hurricane, the strongest to ever hit the state’s Big Bend. It is a huge and powerful storm—with a wind field that could span the distance between tjhe State of Maryland/Washington, DC, and Indianapolis/Chicago—that has already caused historic flooding to some of Florida’s coastal communities.

How bad is it? The Waffle House Index, which has been used by FEMA as an indicator of a storm’s severity, closed all of its locations in Tallahassee, Florida. The Waffle House Index [WHI] is an informal metric named after the Waffle House restaurant chain, headquartered in Georgia, and used by the Federal Emergency Management Agency (FEMA) to determine the effect of a storm and the likely scale of assistance required for disaster recovery.

And, as of 8am EST, Helene has weakened to a Category 1 as it’s moved into Atlanta, Georgia. Nearly 2 million customers are without power across Florida, Georgia, and North/South Carolina. You can get real-time updates here, as we hope everyone in the region is staying safe.

***

Stock market yesterday: The S&P 500 clinched a fresh new record amid GDP data and micro chip stock gains.and Stonk Stocks. Stonk, a deliberate misspelling of stock (meaning “a share of the value of a company which can be bought, sold, or traded as an investment”), was coined in a 2017 meme. The word is often used humorously on the internet to imply a vague understanding of financial transactions or poor financial decisions.

Upbeat GDP data and new stimulus measures in China were largely to thank. One of the day’s big winners was Southwest Airlines, which soared after executives announced plans to revitalize the business.

COMMENTS APPRECIATED

Thank You

***

*** Designated a Doody’s Core Title!

To keep up with the ever-changing field of health care, we must learn new and re-learn old terminology in order to correctly apply it to practice. By bringing together the most up-to-date abbreviations, acronyms, definitions, and terms in the health care industry, the Dictionary offers a wealth of essential information that will help you understand the ever-changing policies and practices in health insurance and managed care today.

Do you ever wish you could acquire specific information for your career activities without having to complete a university Master’s Degree or finish our entire Certified Medical Planner™ professional designation program? Well, Micro-Certifications from the Institute of Medical Business Advisors, Inc., might be the answer. Read on to learn how our three Micro-Certifications offer new opportunities for professional growth in the medical practice, business management, health economics and financial planning, investing and advisory space for physicians, nurses and healthcare professionals.

Micro-Certification Basics

Stock-Brokers, Financial Advisors, Investment Advisors, Accountants, Consultants, Financial Analyists and Financial Planners need to enhance their knowledge skills to better serve the changing and challenging healthcare professional ecosystem. But, it can be difficult to learn and demonstrate mastery of these new skills to employers, clients, physicians or medical prospects. This makes professional advancement difficult. That’s where Micro-Certification and Micro-Credentialing enters the online educational space. It is the process of earning a Micro-Certification, which is like a mini-degree or mini-credential, in a very specific topical area.

Micro-Certification Requirements

Once you’ve completed all of the requirements for our Micro-Certification, you will be awarded proof that you’ve earned it. This might take the form of a paper or digital certificate, which may be a hard document or electronic image, transcript, file, or other official evidence that you’ve completed the necessary work.

Uses of Micro-Certifications

Micro-Certifications may be used to demonstrate to physicians prospective medical clients that you’ve mastered a certain knowledge set. Because of this, Micro-Certifications are useful for those financial service professionals seeking medical clients, employment or career advancement opportunities.

Examples of iMBA, Inc., Micro-Certifications

Here are the three most popular Micro-Certification course from the Institute of Medical Business Advisors, Inc:

1. Health Insurance and Managed Care: To keep up with the ever-changing field of health care physician advice, you must learn new medical practice business models in order to attract and assist physicians and nurse clients. By bringing together the most up-to-date business and medical prctice models [Medicare, Medicaid, PP-ACA, POSs, EPOs, HMOs, PPOs, IPA’s, PPMCs, Accountable Care Organizations, Concierge Medicine, Value Based Care, Physician Pay-for-Performance Initiatives, Hospitalists, Retail and Whole-Sale Medicine, Health Savings Accounts and Medical Unions, etc], this iMBA Inc., Mini-Certification offers a wealth of essential information that will help you understand the ever-changing practices in the next generation of health insurance and managed medical care.

2. Health Economics and Finance: Medical economics, finance, managerial and cost accounting is an integral component of the health care industrial complex. It is broad-based and covers many other industries: insurance, mathematics and statistics, public and population health, provider recruitment and retention, health policy, forecasting, aging and long-term care, and Venture Capital are all commingled arenas. It is essential knowledge that all financial services professionals seeking to serve in the healthcare advisory niche space should possess.

3. Health Information Technology and Security: There is a myth that all physician focused financial advisors understand Health Information Technology [HIT]. In truth, it is often economically misused or financially misunderstood. Moreover, an emerging national HIT architecture often puts the financial advisor or financial planner in a position of maximum uncertainty and minimum productivity regarding issues like: Electronic Medical Records [EMRs] or Electronic Health Records [EHRs], mobile health, tele-health or tele-medicine, Artificial Intelligence [AI], benefits managers and human resource professionals.

Other Topics include: economics, finance, investing, marketing, advertising, sales, start-ups, business plan creation, financial planning and entrepreneurship, etc.

How to Start Learning and Earning Recognition for Your Knowledge

Now that you’re familiar with Micro-Credentialing, you might consider earning a Micro-Certification with us. We offer 3 official Micro-Certificates by completing a one month online course, with a live instructor consisting of twelve asynchronous lessons/online classes [3/wk X 4/weeks = 12 classes]. The earned official completion certificate can be used to demonstrate mastery of a specific skill set and shared with current or future employers, current clients or medical niche financial advisory prospects.

Mini-Certification Tuition, Books and Related Fees

The tuition for each Mini-Certification live online course is $1,250 with the purchase of one required dictionary handbook. Other additional guides, white-papers, videos, files and e-content are all supplied without charge. Alternative courses may be developed in the future subject to demand and may change without notice.

***

Contact: For more information, or to speak with an academic representative, please contact Ann Miller RN MHA CMP™ at: MarcinkoAdvisors@msn.com [24/7].

Posted on September 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Physician Due Diligence is Important

[By Daniel B. Moisand; CFP®, and the ME-P Staff]

While the merits of hiring the right financial advisor [FA] may be clear, hiring the wrong one can be devastating. Medical professionals still tend to have higher incomes and are an attractive target for most financial institutions and scam artists. This fear is a poor excuse for not getting the assistance necessary. Advice about who to engage for financial assistance comes from a hodge-podge of disjointed sources. This leads to good intentions and bad results. Take caution when using the following as sources of advice.

Relying on Family and Friends

By far more people seek financial advice from trusted family members and friends than any other source. This is only natural. It is essential to trust that you are getting advice from a source that means well. It is also important that you get along well with your advisors. Hesitating to communicate with your advisor, even a great advisor, can cause problems even more problematic that getting bad advice from someone you like. While these sources have a good handle on the essential elements of trust and rapport, it is the competence of the advice that is most often the issue. The life and money experiences of those who are close to you certainly have value, but they are not necessarily relevant to your unique goals and circumstances. THINK: Bernie Madoff.

Media

A few years ago, the dominant media force in consumer oriented financial matters was the print media. Magazines and newsletters proliferated with the bull market. More recently however, television has supplanted print even in the bear market. For example, a study now estimates that 80 percent of what the average American knows about current events comes from TV. Why wait three weeks for the next issue when you can get a commentary instantly on the television? There is nothing wrong with watching shows that cover the markets or subscribing to a consumer finance magazine. It is certainly a good idea to be informed. However, be wary of the quality and applicability of information put out by the media.

The Internet

It is easy to run across an ad for prescriptions drugs on television. Images prance across the screen followed by a litany of potential side effects and the obligatory, “Ask your doctor about”. With the expansion of the information superhighway, more and more companies are going direct to the consumer in some manner or another.

Financially speaking this information can be of great benefit but should also generate more concern. It is very easy to project a particular image via the web. The webmaster controls the interaction from what you see to what you hear. One of the results of this is that the Internet has already garnered a reputation as a breeding ground for new scams. More prevalent, however, is the presentation of information meant to be useful that is simply wrong, misinterpreted, or misapplied. The most terrifying source of misinformation on the net is the chat rooms. Here the entire interaction is clouded by anonymity. Some people enter chat rooms because there is a comfort in anonymity when asking a question. There is also a danger in an anonymous answer. When it comes to something as important as your finances or your health, the prudent course should be to take all the advice with a grain of salt. A great deal of consideration to the quality of the source is in order. It is also essential that one understand the level of accountability a source may possess.

Assessment

Much has been written on financial advisor selection, here on the ME-P and elsewhere; but little on how not to select an advisor. We trust this information will be of assistance to the medical professional in some small increment. Send in your FA stories; both good and bad.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Echoing Elon Musk and my colleague medical Michael Burry MD has warned about American consumers’ debt woes.

Echoing the likes of Tesla’s Elon Musk and “The Big Short” investor Michael Burry, a veteran economist has warned that American households have racked up historic amounts of debt — and the economy will pay the price.

“Consumers are just waking up to the fact that they’re financing their spending by running up their credit cards, and that the interest on those credit cards is over the top, out of control, and off the hook right now,” Carl Weinbergtold CNBC. Record credit-card debt threatens to spark a consumer-spending slowdown soon, Carl Weinberg said.

“That’s going to lead to a retrenchment in consumer spending as we get into the new year” the chief economist at High Frequency Economics said. Weinberg expects the US economy to cool but not slide into recession, and he sees inflation fading.

PS: Mike Burry contributed to our 800 page textbook on investing for physicians.

Posted on September 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

BITCOIN MINER HALVING

By Staff Reporters

***

***

DEFINITION: After the network mines 210,000 blocks—roughly every four years—the block chain reward given to Bitcoin miners for processing transactions is cut in half. This event is called halving because it cuts the rate at which new bitcoins are released into circulation in half. This rewards system will continue until about 2140, when the proposed limit of 21 million coins is reached. At that point, miners will be rewarded with fees for processing transactions, which network users will pay. These fees ensure miners are still incentivized to participate and keep the network going.

And, so, the total value of the world’s most popular cryptocurrency surpassed $1 trillion yesterday for the first time since 2021. The overall crypto market, meanwhile, broke $2 trillion in market cap, fueled by investor confidence. If crypto were a publicly traded company, it would be the fourth-largest in the world behind Microsoft, Apple, and Saudi Aramco.

***

***