Dr. David Edward Marcinko MBA MEd

SPONSOR: http://www.MarcinkoAssociates.com

***

***

Milton Friedman, one of the most influential economists of the twentieth century, devoted much of his work to understanding the nature of money and its role in the economy. Although he is best known for his advocacy of monetary policy rules and his critique of discretionary central banking, Friedman also offered a clear conceptual framework for understanding different forms of money. His discussion of the “four types of money” helps illuminate how money functions, how it evolves, and why its various forms matter for economic stability. These categories—commodity money, commodity‑backed money, fiat money, and fiduciary money—capture the historical progression of monetary systems and the institutional choices societies make in managing their currencies.

Friedman’s first category, commodity money, refers to money that has intrinsic value. Gold, silver, and other precious metals are the classic examples. In this system, the money itself is the valuable good; the coin is worth its weight in metal. Friedman appreciated the historical importance of commodity money because it emerged spontaneously in markets without central planning. People gravitated toward commodities that were durable, divisible, portable, and scarce. However, he also emphasized its limitations. Commodity money ties the money supply to the availability of the underlying resource, which can create instability. Gold discoveries can cause inflation, while shortages can cause deflation. For Friedman, the key issue was that commodity money makes the money supply dependent on mining rather than on the needs of the economy. This rigidity, he argued, is not ideal for modern economic systems that require flexibility and predictability.

The second type, commodity‑backed money, represents a transitional stage between pure commodity money and modern monetary systems. In this arrangement, paper notes or coins circulate, but they are redeemable for a fixed quantity of a commodity such as gold. The gold standard is the most famous example. Friedman acknowledged that commodity‑backed systems solved some of the practical problems of carrying and storing precious metals. They also introduced a degree of trust and institutional structure, since governments or banks promised convertibility. Yet Friedman was critical of the gold standard’s constraints. He argued that tying the money supply to gold reserves limited governments’ ability to respond to economic crises. The Great Depression, in his view, was worsened by the Federal Reserve’s failure to expand the money supply because it was constrained by gold convertibility. For Friedman, the gold standard was neither flexible enough nor stable enough to support a growing, complex economy.

***

***

The third category, fiat money, is the system used by most modern economies. Fiat money has no intrinsic value and is not backed by a commodity. Its value comes from government decree and, more importantly, from public confidence. Friedman recognized that fiat money allows for a more adaptable money supply, which can be adjusted to meet the needs of the economy. However, he also believed that fiat money introduces significant risks. Without the discipline imposed by a commodity standard, governments may be tempted to expand the money supply excessively, leading to inflation. Friedman’s famous statement—“inflation is always and everywhere a monetary phenomenon”—reflects his belief that fiat money systems require strict rules to prevent abuse. He argued that central banks should follow predictable, rule‑based policies, such as increasing the money supply at a constant rate, to avoid the destabilizing effects of discretionary monetary decisions.

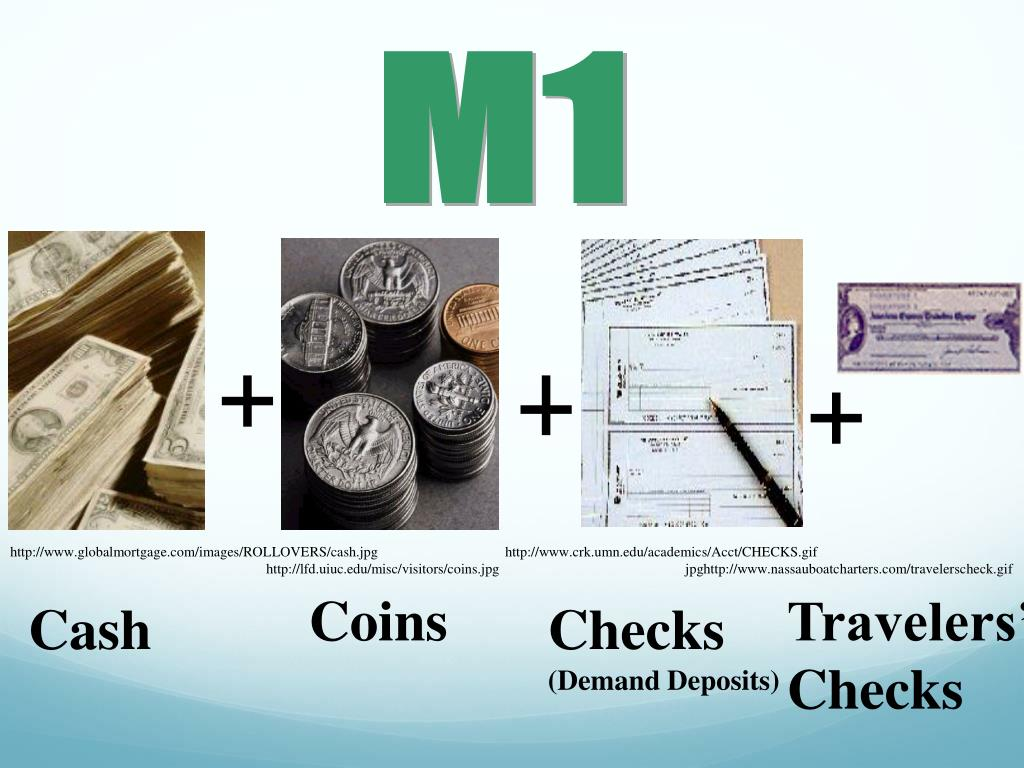

The fourth type, fiduciary money, is closely related to fiat money but emphasizes the role of trust and financial institutions. Fiduciary money includes bank deposits, checks, and other forms of money that exist primarily as accounting entries rather than physical currency. These forms of money rely on the confidence that banks will honor withdrawals and that the financial system will remain stable. Friedman viewed fiduciary money as an essential component of modern economies, but he also saw it as a source of vulnerability. Bank failures, credit contractions, and financial panics can all disrupt the supply of fiduciary money. His work with Anna Schwartz in A Monetary History of the United States highlighted how the collapse of the banking system during the Great Depression caused a severe contraction in the money supply, deepening the economic downturn. For Friedman, the lesson was clear: a stable monetary system requires not only sound government policy but also a well‑regulated and resilient banking sector.

Taken together, Friedman’s four types of money illustrate the evolution of monetary systems from tangible commodities to abstract financial instruments. Each type reflects a different balance between stability, flexibility, and trust. Commodity money offers intrinsic value but lacks adaptability. Commodity‑backed money introduces institutional structure but remains constrained by physical resources. Fiat money provides flexibility but requires disciplined policy to maintain stability. Fiduciary money expands the money supply through financial intermediation but depends on the health of the banking system.

Friedman’s analysis ultimately underscores his broader belief that the key to a stable economy is a predictable and well‑managed money supply. Regardless of the form money takes, he argued that economic stability depends on avoiding large swings in the quantity of money. His framework for understanding the four types of money remains relevant today, especially as new forms of digital and electronic money continue to emerge. By examining the strengths and weaknesses of each type, Friedman provided a foundation for thinking about how monetary systems can best support economic growth, stability, and public confidence.

COMMENTS APPRECIATED

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR- http://www.MarcinkoAssociates.com

Like, Refer and Subscribe

***

***

Share this:

Filed under: "Ask-an-Advisor", economics, Experts Invited, finance, Touring with Marcinko | Tagged: Bitcoin, commoditiy backed money, commoditiy money, david marcinko, economics, economy, fiat money, fiduciary money, finance, four types of money, Milton Friedman, money, money types | Leave a comment »