BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

SELL IN MAY – AND GO AWAY

By Staff Reporters

***

***

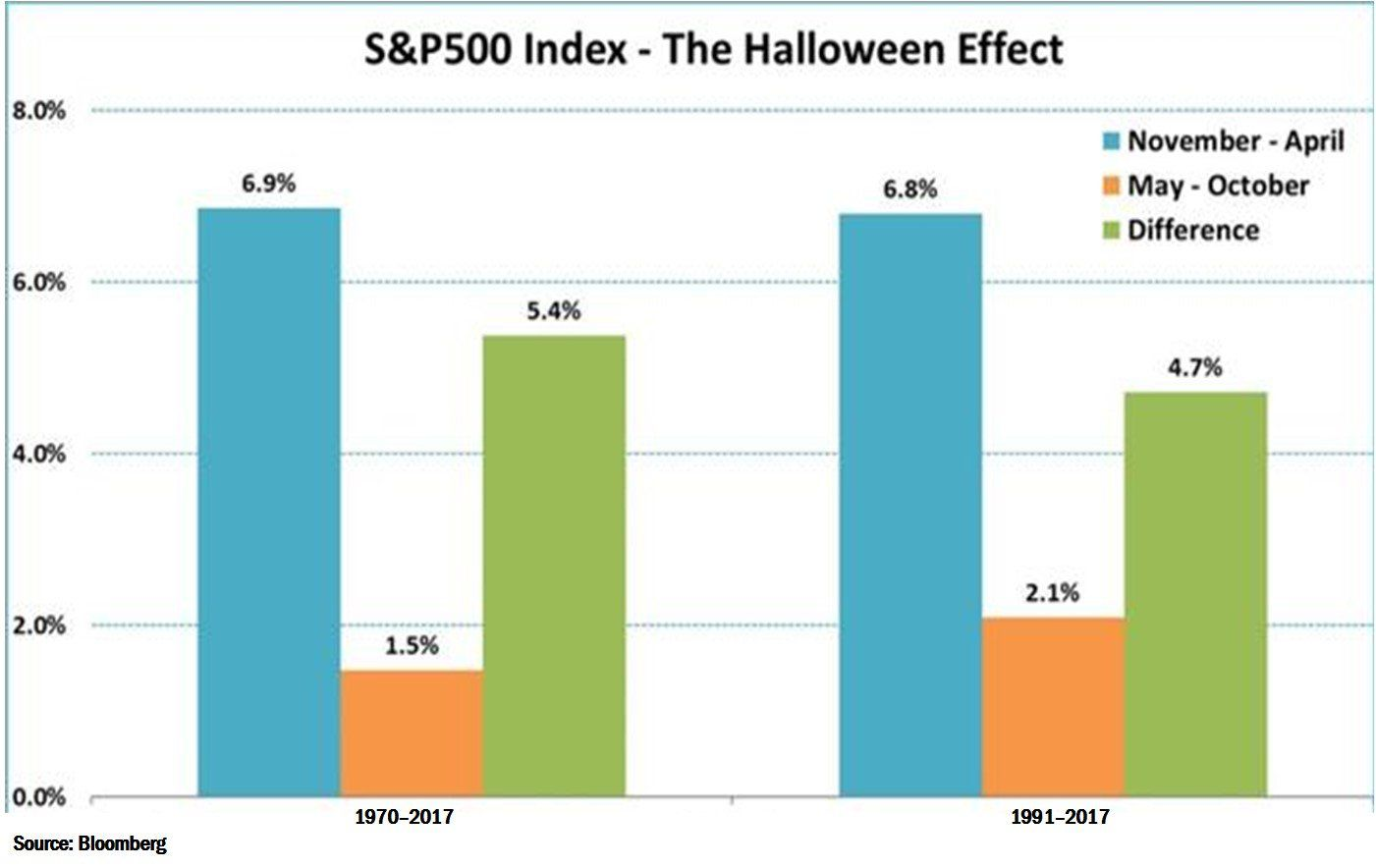

Essentially, the HALLOWEEN INDICATOR is a market-timing strategy. It argues that, by buying into the stock market after Halloween and selling at the end of April, investors would generate a better annual return on their portfolio than if they had remained invested throughout the year. Sell in May and go away is an investment strategy for stocks based on a theory that the period from November to April inclusive has significantly stronger stock market growth on average than the other months

The practice of abandoning stocks beginning in May of each year is widely thought to have its origins in the United Kingdom. The privileged class would leave London and head to their country estates for the summer months, where they would largely ignore their investment portfolios. To this day, many stock market watchers have postulated that the corresponding impact of summer vacations on market liquidity and investors’ risk aversion is at least partly responsible for the difference in seasonal returns.

In what is considered to be a seminal piece of research on the subject, “The Halloween Indicator, ‘Sell in May and Go Away’: Another Puzzle,” authors Sven Bouman and Ben Jacobsen were among the first to document a strong seasonal effect in global stock markets. In 36 of the 37 developed and emerging markets they studied between 1973 and 1998, the authors found returns in the November through April period to be, on average, significantly higher than those in the May through October period, even after taking transaction costs into account. What puzzled the authors was the fact that, while the anomaly was widely known and seemed to offer considerable economic rewards, it had not been arbitraged away.

More recently, Jacobsen partnered with Cherry Zhang on a follow up study, titled, “The Halloween Indicator: Everywhere and All the Time,” and extended the research to 108 stock markets using all historical data available. The result was a sample of 55,425 monthly observations (including more than 300 years of UK data), which helped to rebut any criticisms of data mining and sample selection bias. The results were compelling, as the November through April “winter” period delivered returns that were, on average, 4.52% higher than the “summer” returns. The Halloween effect was evident in 81 out of 108 countries. The size of the Halloween effect varied across geographies. It was found to be stronger in developed and emerging markets than in frontier markets.

Posted on October 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelsen CFA

***

***

One of the biggest hazards of being a professional money manager is that you are expected to behave in a certain way.

One of the biggest hazards of being a professional money manager is that you are expected to behave in a certain way: You have to come to the office every day, work long hours, slog through countless emails, be on top of your portfolio (that is, check performance of your securities minute by minute), watch business TV and consume news continuously, and dress well and conservatively, wearing a rope around the only part of your body that lets air get to your brain. Our colleagues judge us on how early we arrive at work and how late we stay. We do these things because society expects us to, not because they make us better investors or do any good for our clients.

Somehow we let the mindless, Henry Ford–assembly-line, 8:00 a.m. to 5:00 p.m., widgets-per-hour mentality dictate how we conduct our business thinking. Though car production benefits from rigid rules, uniforms, automation and strict working hours, in investing — the business of thinking — the assembly-line culture is counterproductive. Our clients and employers would be better off if we designed our workdays to let us perform our best.

Investing is not an idea-per-hour profession; it more likely results in a few ideas per year. A traditional, structured working environment creates pressure to produce an output — an idea, even a forced idea. Warren Buffett once said at a Berkshire Hathaway annual meeting: “We don’t get paid for activity; we get paid for being right. As to how long we’ll wait, we’ll wait indefinitely.”

How you get ideas is up to you. I am not a professional writer, but as a professional money manager, I learn and think best through writing. I put on my headphones, turn on opera and stare at my computer screen for hours, pecking away at the keyboard — that is how I think. You may do better by walking in the park or sitting with your legs up on the desk, staring at the ceiling.

I do my best thinking in the morning. At 3:00 in the afternoon, my brain shuts off; that is when I read my emails. We are all different. My best friend is a brunch person; he needs to consume six cups of coffee in the morning just to get his brain going. To be most productive, he shouldn’t go to work before 11:00 a.m.

And then there’s the business news. Serious business news that lacked sensationalism, and thus ratings, has been replaced by a new genre: business entertainment (of course, investors did not get the memo). These shows do a terrific job of filling our need to have explanations for everything, even random events that require no explanation (like daily stock movements). Most information on the business entertainment channels — Bloomberg Television, CNBC, Fox Business — has as much value for investors as daily weather forecasts have for travelers who don’t intend to go anywhere for a year.

Yet many managers have CNBC, Fox or Bloomberg TV/Internet streaming on while they work.

Nepo babies often go broke due to a mix of financial mismanagement, lack of resilience, and the illusion of inherited success. Their privileged upbringing can mask the need for discipline, adaptability, and long-term planning—traits essential for sustaining wealth.

The term nepo baby—short for nepotism baby—refers to children of celebrities or influential figures who benefit from family connections to launch careers, especially in entertainment, fashion, or media. While these individuals often start with significant advantages, including wealth, fame, and access, many struggle to maintain financial stability over time. The reasons are complex and rooted in both personal and systemic factors.

First, many nepo babies lack financial literacy. Growing up in environments where money flows freely, they may never learn budgeting, investing, or the value of money. Without these skills, they’re prone to overspending, poor investments, and unsustainable lifestyles. Lavish purchases—designer clothes, luxury cars, expensive homes—can quickly drain even sizable inheritances if not managed wisely.

Second, the illusion of guaranteed success can be dangerous. Nepo babies often enter industries where their family name opens doors, but that doesn’t guarantee longevity. Fame is fickle, and public interest can fade. If they don’t develop their own talents or work ethic, they may find themselves unemployable once the novelty wears off. This overreliance on family reputation can lead to complacency, making it harder to adapt when challenges arise.

Third, many nepo babies face identity crises and public scrutiny. Constant comparisons to their successful parents can erode confidence and create pressure to live up to unrealistic expectations. Some rebel by distancing themselves from their family’s legacy, while others try to prove themselves in unrelated fields. Either way, this struggle can lead to erratic career choices and unstable income streams.

Fourth, fame without privacy can fuel destructive habits. The entertainment world is rife with stories of young stars—many of them nepo babies—falling into substance abuse, reckless behavior, or toxic relationships. These issues not only affect mental health but also lead to legal troubles and financial loss. Without strong support systems or accountability, it’s easy to spiral.

Finally, inherited wealth can disappear quickly without proper estate planning. Trust funds and inheritances may be mismanaged or depleted by taxes, lawsuits, or poor financial advisors. Some nepo babies assume the money will last forever and fail to plan for long-term sustainability. Others are exploited by opportunistic friends or partners who take advantage of their naivety.

In contrast, those who succeed often do so by acknowledging their privilege, developing their own skills, and surrounding themselves with trustworthy mentors. They treat their inherited platform as a launchpad—not a safety net—and work to build something lasting.

In short, nepo babies go broke not because they lack opportunity, but because opportunity without discipline is a recipe for downfall. Wealth and fame are fleeting without the grit to sustain them. The lesson here isn’t just about celebrity—it’s a universal truth: success inherited must still be earned.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on October 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Insurance Basics for Medical Professionals

By Jeffrey H. Rattiner, CPA, CFP®, MBA via iMBA, Inc.

After determining the need for insurance and the amount to purchase, the doctor-client and financial planner’s next task is to match those needs to the client’s objectives to determine what type of policy the client should purchase. The life insurance industry features more products today than ever before. One reason for this change is that, clearly, the insurance industry has expanded its product base to become more competitive. Another reason is that clients’ needs are constantly changing and the insurance companies must keep up with those needs or run the risk of having funds withdrawn from their companies. New and different types of life insurance products are here to stay. Since life insurance represents a significant part of a client’s risk-management program, planners have to be versed in the specifics of the varied product base.

Term Insurance Alternative

Whole life insurance was introduced as an alternative to term insurance. Whole life is often called cash value insurance or permanent insurance to distinguish it from term insurance. The cash value in whole life insurance arises because of the level premium system and the need to account for prepaid premiums. Whole life insurance offers permanent protection at a level premium for the entire lifetime of the insured. Premiums remain fixed and are paid throughout the insured’s entire lifetime. The premium level can remain constant throughout the life of the policy because premiums are higher during the early years. The excess charge in the early years makes it possible to build up a reserve, which will be needed, together with interest earned, to keep premiums level throughout the life of the policy. Older clients then pay the same premium in later years as they did when they were younger.

Cash Value

The cash value of a whole life policy serves a variety of purposes:

• It can be used for collateral for an insurance company loan.

• If the insured decides to terminate the policy, he or she can elect to receive the policy’s cash value at that time.

• The cash value balance can be remitted to the insurance company to purchase a reduced paid-up insurance policy. This will provide coverage until the funds are insufficient to pay the premiums. This cancellation feature is also referred to as a non-forfeiture value.

• If the policy is not canceled, the accumulated cash value becomes part of the death benefit paid upon the insured’s death (which makes this type of policy similar to a decreasing term policy). It can reduce cash flow by taking some of the investment results out of the contract either through dividends or through policy loans.

General Accounts

With a whole life policy, the insured does not control the investment vehicle. Policies are invested in the insurance company’s general account through the purchase of long-term bonds and mortgages. As a result, during a period of decreasing interest rates, whole life products can be expected to produce superior results since rates can be locked in when interest rates in general are higher. In contrast, rates in an increasing environment are locked in to their portfolios until maturity. There is no flexibility within a whole life policy. Premium payments, type of investment vehicle, and change in death benefit are all fixed. The safety of cash value is high, but the potential rate of return is low to moderate. If interest rates are rising, the price of the policy is declining, and you may want to suggest replacing the policy. (See Planning Issue 10.)

If the premiums paid to the insurance company turn out to be more than the company needs because expenses are lower than expected, the company’s portfolio investment return will be larger than the company expected. As a result, the company will then return some of the excess premium to the policyholder as a dividend or excess interest. Life insurance dividends are not taxable as income because they represent an excess of premium.

Premium Payments

The premium consists of mortality charge, policy expense, and a cash value. When the insured reaches 100 years of age, the policy endows with the face amount of the policy collectible by the insured. Since mortality tables end at age 100, the insurer considers the client dead and pays the face amount of the policy.

Whole life policies are packaged in a variety of ways. One policy, a limited-pay whole life policy, is a whole life policy with a death benefit continuing through age 100. The only difference between this and the traditional whole life policy is that premiums are paid only for a specified period, for example, seven years. In other words, the policyholder prepays the policy. A policy is considered to be fully paid up when the cash value of the basic contract plus the value of the dividend additions or deposits equals the net single premium for the policy in question at the insured’s attained age. The premium-paying period influences the cash value buildup in the policy. This is accomplished by using part of the investment return or dividends from long-term bonds and mortgages to pay the mortality and the expense charges on the policy for the rest of the policyholder’s life.

Advantages and DisAdvantages

Advantages of a whole life policy include lifetime coverage for the insured, a forced savings element, loan privileges, and a variety of premium payment plans. Over time, the cost is lower than term, the rate of return if the policy is kept until death is quite reasonable, and the policy will do a better job than universal life in keeping up with inflation. Disadvantages include a higher cost of death protection, a low rate of return, lack of flexibility, and incompatibility with inflation.

Assessment

Whole life policies are most appropriate for people who want or need a forced savings arrangement and for people who want lifetime coverage. As interest rates increased during the late 1970s, the returns received from insurance companies on long-term bonds and mortgage portfolios of whole life portfolios declined. As a result, in order to prevent policyholders from borrowing their cash reserves and investing these funds in other financial products, the insurance industry offered the following incentives:

• Existing policyholders were given the option to have their policies upgraded to reflect current market rates. Policies were upgraded through higher interest rates on cash values and higher future dividends and rates on policy loans.

• New types of policies were introduced—such as universal life, which tied cash value to short-term money market rates.

• Variable life insurance and universal variable life insurance were introduced, which segregated policy assets into a separate account.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on October 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Cryonics is a scientific and philosophical endeavor that seeks to preserve human life by freezing individuals at ultra-low temperatures after legal death, with the hope that future medical advancements may allow for revival and healing. Though still a speculative and controversial field, cryonics has captured the imagination of futurists, scientists, and ethicists alike.

What Is Cryonics?

Cryonics involves the process of cryopreservation—cooling the body, or sometimes just the brain, to -196°C using liquid nitrogen. The goal is to halt all biological activity, particularly decay, immediately after death. This is not the same as freezing; rather, it involves vitrification, a process that turns bodily fluids into a glass-like state to prevent ice crystal formation, which can damage cells. Once preserved, the body is stored indefinitely in a cryogenic chamber until such time that revival is theoretically possible.

***

***

Scientific and Technological Challenges

Despite its futuristic appeal, cryonics remains highly experimental. No human has ever been revived from a cryopreserved state, and current technology cannot reverse the damage caused by the preservation process itself. While scientists have successfully frozen and revived small biological samples like sperm and embryos, scaling this to entire human bodies presents enormous challenges.

The hope lies in future breakthroughs in nanotechnology, regenerative medicine, and artificial intelligence that could repair cellular damage and cure the diseases that led to death in the first place.

Turning 50 with little to no savings can be daunting, especially for a doctor who has spent decades in a demanding profession. Yet, all is not lost. With strategic planning, discipline, and a willingness to adapt, a broke 50-year-old physician can still build a solid retirement foundation by age 65.

First, it’s essential to confront the financial reality. This means calculating current income, expenses, debts, and any assets, however small. A clear picture allows for realistic goal-setting. The target should be to save aggressively—ideally 30–50% of income—over the next 15 years. While this may seem steep, doctors often have above-average earning potential, even in their later years, which can be leveraged.

Next, lifestyle adjustments are crucial. Downsizing housing, eliminating unnecessary expenses, and avoiding new debt can free up significant cash flow. If possible, relocating to a lower-cost area or refinancing existing loans can also help. Every dollar saved should be redirected into retirement accounts such as a 401(k), IRA, or a solo 401(k) if self-employed. Catch-up contributions for those over 50 allow for higher annual deposits, which can accelerate growth.

Investing wisely is non-negotiable. A diversified portfolio with a mix of stocks, bonds, and alternative assets can provide both growth and stability. Working with a fiduciary financial advisor ensures that investments align with retirement goals and risk tolerance. Time is limited, so the focus should be on maximizing returns without taking reckless risks.

Increasing income is another powerful lever. Many doctors can boost earnings through side gigs like telemedicine, consulting, teaching, or locum tenens work. These flexible options can add tens of thousands annually without requiring a full career shift. Additionally, monetizing expertise—writing, speaking, or creating online courses—can generate passive income streams.

Debt reduction must be prioritized. High-interest loans, especially credit card debt, can erode savings potential. Paying off these balances aggressively while avoiding new liabilities is key. For student loans, exploring forgiveness programs or refinancing options may offer relief.

Finally, mindset matters. Retirement at 65 doesn’t have to mean complete cessation of work. It can mean transitioning to part-time roles, passion projects, or advisory positions that provide income and fulfillment. The goal is financial independence, not necessarily total inactivity.

In conclusion, while starting late is challenging, a broke 50-year-old doctor can still retire comfortably at 65. It requires a blend of financial discipline, income optimization, smart investing, and lifestyle changes. With focus and determination, the next 15 years can be transformative—turning a precarious situation into a secure and dignified retirement.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on October 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Level-funded health care is an increasingly popular option for small to mid-sized businesses seeking a balance between cost control and comprehensive employee coverage. It blends features of fully insured and self-funded health plans, offering employers greater flexibility and potential savings while minimizing risk.

In a traditional fully insured plan, employers pay a fixed premium to an insurance carrier, which assumes all financial risk for employee claims. In contrast, self-funded plans allow employers to pay for claims out-of-pocket, which can lead to significant savings—but also exposes them to unpredictable costs. Level-funded plans sit between these two models, offering a structured and predictable approach to self-funding.

With level-funded health care, employers pay a fixed monthly amount that covers three components: estimated claims funding, stop-loss insurance, and administrative fees. The estimated claims portion is based on actuarial data and reflects the expected health care usage of the employee group. Stop-loss insurance protects the employer from catastrophic claims by capping their financial exposure. Administrative fees cover third-party services such as claims processing and customer support.

One of the key advantages of level-funded plans is the potential for cost savings. If actual claims fall below the estimated amount, employers may receive a refund or credit at the end of the year. This incentivizes wellness programs and preventive care, as healthier employees lead to lower claims. Additionally, level-funded plans often provide more transparency into claims data, allowing employers to better understand health trends and make informed decisions about benefits.

***

***

Another benefit is flexibility. Level-funded plans can be customized to suit the needs of a specific workforce, offering a range of coverage options and provider networks. This contrasts with the rigid structure of many fully insured plans. Employers also gain more control over plan design, which can help attract and retain talent in competitive job markets.

However, level-funded health care is not without challenges. It requires careful planning and a solid understanding of risk. Employers must be prepared for the possibility that claims may exceed projections, although stop-loss insurance helps mitigate this. Additionally, level-funded plans may not be suitable for very small groups or those with high-risk populations, as the cost of stop-loss coverage can be prohibitive.

Regulatory considerations also play a role. Level-funded plans are typically governed by federal ERISA laws rather than state insurance regulations, which can affect compliance and reporting requirements. Employers should work closely with benefits consultants or brokers to ensure they understand the legal landscape and choose a plan that aligns with their goals.

In conclusion, level-funded health care offers a compelling alternative for businesses seeking to manage costs while providing quality coverage. By combining predictability with the potential for savings and customization, it empowers employers to take a more active role in their health benefits strategy. As the health care landscape continues to evolve, level-funded plans are likely to remain a valuable option for organizations looking to strike the right balance between affordability and employee well-being.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on October 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

In the evolving landscape of digital health care, Amazon Pharmacy and GoodRx have emerged as two leading platforms offering consumers affordable and convenient access to prescription medications. While both aim to simplify the process of obtaining prescriptions, they differ significantly in their approach, pricing models, and user experience.

Amazon Pharmacy, launched in 2020, is a full-service online pharmacy that allows customers to order medications directly through Amazon. It offers fast, free delivery for Prime members and integrates with most insurance plans. One of its standout features is RxPass, a subscription service available to Prime members for $5 per month, which covers unlimited eligible generic medications. This model is particularly attractive to individuals who take multiple generics regularly, as it can significantly reduce out-of-pocket costs.

In contrast, GoodRx, founded in 2011, operates primarily as a price comparison and discount platform. It does not dispense medications itself but partners with local and mail-order pharmacies to help users find the lowest prices. GoodRx provides coupons that can be used at thousands of pharmacies nationwide, often resulting in substantial savings—especially for those without insurance. It also offers GoodRx Gold, a paid membership that unlocks deeper discounts and telehealth services.

***

***

When comparing the two, pricing transparency is a key differentiator. GoodRx excels in showing users a range of prices across different pharmacies, empowering them to choose the most cost-effective option. Amazon Pharmacy, while competitive, typically offers fixed prices and focuses more on convenience and integration with its broader ecosystem.

Convenience is another area where Amazon Pharmacy shines. With its streamlined ordering process, automatic refills, and integration with Amazon’s delivery network, it appeals to users who prioritize ease and speed. GoodRx, while convenient in its own right, requires users to present coupons at the pharmacy or use mail-order services, which may involve more steps.

Insurance compatibility also varies. Amazon Pharmacy accepts most major insurance plans, making it a viable option for insured individuals. GoodRx, on the other hand, is often used by those without insurance or with high deductibles, as its discounts can sometimes beat insurance copays.

However, both platforms have limitations. Amazon Pharmacy’s RxPass is restricted to generic medications and excludes certain states due to regulatory issues. GoodRx’s discounts may not apply to all medications, and prices can fluctuate depending on location and pharmacy.

In terms of user experience, Amazon offers a seamless, tech-driven interface with customer support and medication management tools. GoodRx provides educational resources, price alerts, and a mobile app that helps users track savings and prescriptions.

Ultimately, the choice between Amazon Pharmacy and GoodRx depends on individual needs. For those seeking a one-stop solution with predictable costs and fast delivery, Amazon Pharmacy may be ideal. For users who want to shop around for the best deal or lack insurance, GoodRx offers unmatched flexibility and savings.

As digital health continues to grow, both platforms are reshaping how Americans access medications—making prescriptions more affordable, transparent, and accessible than ever before.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

The global healthcare sector faces mounting challenges: rising costs, inefficiencies, limited access, and bureaucratic entanglements. In response, some economists and policymakers have turned to Austrian Economics for answers. Rooted in the works of Ludwig von Mises and Friedrich Hayek, Austrian Economics emphasizes individual choice, market-driven solutions, and skepticism toward centralized planning. But can this school of thought truly “save” healthcare?

At its core, Austrian Economics champions the idea that decentralized decision-making and free-market mechanisms lead to more efficient and responsive systems. In healthcare, this would mean reducing government control and allowing competition to drive innovation, lower costs, and improve quality. Proponents argue that when patients act as consumers and providers compete for their business, the system becomes more accountable and efficient. For example, direct primary care models—where patients pay physicians directly without insurance intermediaries—reflect Austrian principles and have shown promise in improving care and reducing administrative overhead.

Austrian theorists also critique the price distortions caused by third-party payers like insurance companies and government programs. According to them, when consumers are insulated from the true cost of care, demand becomes artificially inflated, leading to overutilization and waste. By restoring price signals—where patients see and respond to the actual cost of services—Austrian economists believe the market can better allocate resources and curb unnecessary spending.

However, critics argue that healthcare is not a typical market. Patients often lack the information, time, or capacity to make rational choices, especially in emergencies. Moreover, healthcare involves significant externalities and moral considerations that pure market logic may overlook. For instance, should access to life-saving treatment depend solely on one’s ability to pay? Austrian Economics offers little guidance on equity or universal access, which are central concerns in modern healthcare debates.

Austria itself provides an interesting case study. Despite the name, Austrian Economics is not the guiding philosophy behind Austria’s healthcare system. Instead, Austria operates a social insurance model with near-universal coverage, funded through mandatory contributions and managed by a mix of public and private actors. While recent reforms have aimed to streamline administration and reduce fragmentation he system remains largely collectivist—contrary to Austrian ideals.

In conclusion, Austrian Economics offers valuable insights into the inefficiencies of centralized healthcare systems and the potential benefits of market-based reforms. Its emphasis on individual choice, price transparency, and entrepreneurial innovation can inspire meaningful improvements. However, its limitations in addressing equity, access, and the unique nature of healthcare suggest that it cannot “save” the system on its own. A hybrid approach—blending market mechanisms with safeguards for universal access—may offer a more balanced path forward.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Valuing a medical practice involves assessing its financial performance, assets, and intangible factors like goodwill and patient loyalty to determine its fair market worth.

Determining the value of a medical practice is a nuanced process that blends financial analysis with strategic insight. Whether you’re preparing to sell, merge, or bring in a partner, understanding how to value your practice ensures informed decision-making and fair negotiations.

There are several recognized methods for valuing a medical practice, each suited to different scenarios. The most common include the income approach, market approach, asset-based approach, and the rule-of-thumb method.

The income approach focuses on the practice’s ability to generate future earnings. This method involves analyzing historical financial statements, projecting future cash flows, and discounting them to present value using a risk-adjusted rate. It’s particularly useful when the practice has stable revenue and predictable expenses. Key metrics include net income, physician productivity, and reimbursement rates.

The market approach compares the practice to similar ones that have recently sold. It relies on data from comparable transactions, adjusted for differences in size, specialty, location, and profitability. This method is ideal when reliable market data is available, though such data can be scarce for niche specialties or rural practices.

The asset-based approach calculates the value of tangible and intangible assets. Tangible assets include medical equipment, office furniture, and real estate. Intangible assets—like patient records, brand reputation, and goodwill—are harder to quantify but can significantly impact value. Goodwill, for instance, reflects the practice’s reputation, patient loyalty, and referral networks.

The rule-of-thumb method uses industry benchmarks, such as a multiple of annual revenue or earnings. For example, a general practice might be valued at 60–80% of annual gross revenue. While quick and easy, this method oversimplifies and may not reflect the unique strengths or weaknesses of a specific practice.https:/https://medicalexecutivepost.com/2025/03/17/medial-practice-valuation-adjustments//medicalexecutivepost.com/2025/03/17/medial-practice-valuation-adjustments/

Beyond these methods, several qualitative factors influence valuation. These include the size and diversity of the patient base, the practice’s specialty, use of technology (like EHR systems or telemedicine), and whether key physicians will remain post-sale. A practice heavily reliant on one provider may be less valuable than one with a strong team and succession plan.

Timing also matters. Economic conditions, regulatory changes, and shifts in healthcare reimbursement can affect practice value. Tax implications and deal structure—such as asset sale vs. stock sale—should also be considered during negotiations.

Ultimately, valuing a medical practice is both art and science. Engaging a professional appraiser or valuation expert can help ensure accuracy and objectivity. They bring experience, access to market data, and the ability to tailor valuation methods to your specific situation.

In summary, a comprehensive valuation considers financial performance, assets, market trends, and intangible factors. By understanding these elements, practice owners can make strategic decisions that reflect the true worth of their medical enterprise.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on October 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Turn Financial A-Ha Moments Into Lasting Change With Memory Re-Consolidation

By Rick Kahler MSFS CFP™

***

***

Have you ever had a light bulb moment about money?

Maybe you leave a workshop, a therapy session, or a conversation with a financial advisor, feeling as if you have finally cracked the code. You understand why you keep overspending. You see the pattern that keeps you procrastinating about saving and investing. You feel the reason you panic about money, even when you know you are okay. In that moment, it all seems so clear.

Yet a week later, you are right back at it. Swiping the credit card. Avoiding the budget. Losing sleep over the same worries you thought you had just solved. What happened to that breakthrough? Why did it not last?

I’ve experienced this myself, more times than I’d like to admit. Recently, I found a book that explains why: Unlocking the Emotional Brain by Bruce Ecker, Robin Ticic, and Laurel Hulley. The authors explain that lasting change happens through something called “memory re-consolidation.” It is the brain’s way of updating emotional patterns we have carried for years—often since childhood.

Most of us have old money stories tucked away in our emotional memory. Suppose, for example, as a child you were scolded for asking a neighbor how much money they earned. This and other similar experiences that left you feeling shamed or dismissed taught you that it was rude to talk about money.

Such early experiences are filed away as emotional truths. They shape what feels true, even years later as an adult, whether or not that “truth” is still relevant.

As an adult, you may have come to understand that talking about money is often essential for your emotional and financial well being. But when the moment comes to have a money conversation, your body still freezes up. That is not weakness. That is your brain pulling up the old file.

Here is where memory re-consolidation comes in. The brain does not update the file just because you think new thoughts. It updates when you have a new experience that feels different. Maybe someone listens without judgment, or you realize you are talking about money and still feel safe. That emotional mismatch tells the brain, “Maybe this file is not true anymore.”

But the update is not finished. To make the change stick, you have to hold both the old belief and the new experience together for a little while. It is like showing your brain two pictures: here is how it used to feel, and here is how it feels now. That moment of holding both is when the rewrite happens.

Even more interesting, the brain keeps the file open for several hours after the shift. What you do in that window can help the change settle in—or not. If you rush back into busyness or distractions, you might accidentally let the old version save itself again.

So what can we do to give those shifts a better chance of sticking? I have noticed that insights gained during a retreat or workshop, with ample time to focus and reflect, are more likely to last. Even in our everyday lives, we can slow down, even for a few minutes, to write about what we felt, check in with our bodies, or talk with someone who supports us. We can protect a little bit of quiet space before diving back into the noise.

The next time you have a money breakthrough, try giving yourself that space. Consciously notice both the old belief and the new experience. Give the re-consolidation time to settle in.

Then, the next time your brain pulls up that old money story, you’ll have access to the updated, more accurate version.

What Medical School Didn’t Teach Doctors About Money

Medical school is designed to mold students into competent, compassionate physicians. It teaches anatomy, pathology, pharmacology, and clinical skills with precision and rigor. Yet, despite the depth of medical knowledge imparted, one critical area is often overlooked: financial literacy. For many doctors, the transition from student to professional comes with a steep learning curve—not in medicine, but in money. From managing debt to understanding taxes, investing, and retirement planning, medical school leaves a financial education gap that can have long-term consequences.

The Debt Dilemma

One of the most glaring omissions in medical education is how to manage student loan debt. The average medical student graduates with over $200,000 in debt, yet few are taught how to navigate repayment options, interest accrual, or loan forgiveness programs. Many doctors enter residency with little understanding of income-driven repayment plans or Public Service Loan Forgiveness (PSLF), missing opportunities to reduce their financial burden. Without guidance, some make costly mistakes—such as refinancing federal loans prematurely or choosing repayment plans that don’t align with their career trajectory.

Income ≠ Wealth

Medical students often assume that a high salary will automatically lead to financial security. While physicians do earn more than most professionals, income alone doesn’t guarantee wealth. Medical school rarely addresses the importance of budgeting, saving, and investing. As a result, many doctors fall into the “HENRY” trap—High Earner, Not Rich Yet. They spend lavishly, assuming their income will always cover expenses, only to find themselves living paycheck to paycheck. Without a solid financial foundation, even high earners can struggle to build net worth.

***

***

Taxes and Business Skills

Doctors are also unprepared for the complexities of taxes. Whether employed by a hospital or running a private practice, physicians face unique tax challenges. Medical school doesn’t teach how to track deductible expenses, optimize retirement contributions, or navigate self-employment taxes. For those who open their own clinics, the lack of business education is even more pronounced. Understanding profit margins, payroll, insurance billing, and compliance regulations is essential—but rarely covered in medical training.

Investing and Retirement Planning

Another blind spot is investing. Medical students are rarely taught the basics of compound interest, asset allocation, or retirement accounts. Many don’t know the difference between a Roth IRA and a traditional 401(k), or how to evaluate mutual funds and index funds. This lack of knowledge delays retirement planning and can lead to missed opportunities for long-term growth. Some doctors rely on financial advisors without understanding the fees or conflicts of interest involved, putting their wealth at risk.

Insurance and Risk Management

Medical school also fails to educate students on insurance—life, disability, malpractice, and health. Doctors need robust coverage to protect their income and assets, but many don’t know how to evaluate policies or understand terms like “own occupation” or “elimination period.” Inadequate coverage can leave physicians vulnerable to financial disaster in the event of illness, injury, or litigation.

Emotional and Behavioral Finance

Beyond technical knowledge, medical school overlooks the emotional side of money. Physicians often face pressure to maintain a certain lifestyle, especially after years of sacrifice. The desire to “catch up” can lead to impulsive spending, luxury purchases, and financial stress. Without tools to manage money mindset and behavioral habits, doctors may struggle with guilt, anxiety, or burnout related to finances.

The Case for Financial Education

Fortunately, awareness of this gap is growing. Organizations like Medics’ Money and podcasts such as “Docs Outside the Box” are working to fill the void by offering financial education tailored to physicians.

These resources cover everything from budgeting and debt management to investing and entrepreneurship. Some medical schools are beginning to incorporate financial literacy into their curricula, but progress is slow and inconsistent.

Conclusion

Medical school equips doctors to save lives, but it doesn’t prepare them to secure their own financial future. The lack of financial education leaves many physicians vulnerable to debt, poor investment decisions, and lifestyle inflation. To thrive both professionally and personally, doctors must seek out financial knowledge beyond the classroom. Whether through self-study, mentorship, or professional guidance, understanding money is as essential as understanding medicine. After all, financial health is a cornerstone of overall well-being—and every doctor deserves to master both.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on October 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

PODCAST: National Prescription Drug Take Back Day

October 25, 2025

By Dr. David Edward Marcinko MBA MEd

***

The National Prescription Drug Take Back Day aims to provide a safe, convenient, and responsible means of disposing of prescription drugs, while also educating the general public about the potential for abuse of medications.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Posted on October 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

What’s a polymath?

The definition of “polymath” is the subject of debate. The term has its roots in Ancient Greek and was first used in the early 17th Century to mean a person with “many learnings”, but there is no easy way to decide how advanced those learnings must be and in how many disciplines. Most researchers argue that to be a true polymath you need some kind of formal acclaim in at least two apparently unrelated domains. And, one of the most detailed examinations of the subject comes from Waqas Ahmed in his book The Polymath, published earlier this year.

Now, despite his many achievements, Ahmed does not identify as a polymath. “It is too esteemed an accolade for me to refer to myself as one,” he said. When examining the lives of historical polymaths, he only considered those who had made significant contributions to at least three fields, such as Leonardo da Vinci (the artist, inventor and anatomist), Johann Wolfgang von Goethe (the great writer who also studied botany, physics and mineralogy) and Florence Nightingale (who, besides founding modern nursing, was also an accomplished statistician and theologian).

What is a savant?

Savant syndrome is an exceedingly rare condition in which individuals with a developmental disorder or an intellectual disability possess extraordinary talents, knowledge, or abilities in a specific area. Savant syndrome may be congenital at birth or acquired later in life and is commonly associated with autism spectrum disorder (ASD). It may also coexist alongside other conditions, such as brain injuries . Individuals with savant syndrome were historically referred to with the term “idiot savant,” but negative connotations of the term “idiot” resulted in its abandonment and is now solely termed “savant.”

Famous individuals with savant syndrome include Kim Peek, who was able to calculate dates for any event hundreds of years into the past or future and inspired the movie the Rain Man. Stephen Wiltshire was mute and communicated through drawings of detailed city landscapes. Approximately 10% of individuals with autistic disorder have savant abilities. Less than 1% of the non-autistic population have savant syndrome. Therefore, not all savants have ASD, and not all persons with autismare savants.

What is a genius?

There is no scientifically precise definition of genius. When used to refer to the characteristic, genius is associated with talent but several authors systematically distinguish these terms. Walter Isaacson, biographer of many well-known geniuses, explains that although high intelligence may be a prerequisite, the most common trait that actually defines a genius may be the extraordinary ability to apply creativity and imaginative thinking to almost any situation.

The plural form of genius can be either geniuses or genii, pronounced [ jee-nee-ahy ], depending on the intended meaning of the word. Geniuses is much more commonly used. The plural forms of several other singular words that end in -us are also formed in this way, such as virus/viruses, callus/calluses, and status/statuses. Irregular plurals that are formed like genii, such as radius/radii or cactus/cacti, derive directly from their original pluralization in Latin. However, the standard English plural -es is often also acceptable for these terms, as in radiuses and cactuses.

Who is Mensa material?

Mensa members range in age from 2 to 106. They include engineers, homemakers, teachers, actors, athletes, students, and CEOs, and they share only one trait — high intelligence. To qualify for Mensa, they scored in the top 2 percent of the general population on an accepted standardized intelligence test.

Note: These descriptions are presented with some thanks to Chat GPT.

According to the Daily Beast, First Lady Melania Trump was allegedly used as “window dressing” in a multi-million-dollar memecoin scheme that deceived investors and enriched its crypto creators, according to a lawsuit filed in federal court. The suit involves the $Melania coin, which the 55-year-old First Lady promoted to her social media on the eve of President Donald Trump’s inauguration in January, writing, “The Official Melania Meme is live! You can buy $MELANIA now.” Many of Trump’s supporters purchased the coin, pushing it to trade at an all-time high price of $13.73 apiece. $Melania was trading at less than 10 cents per coin by Wednesday—a staggering crash in value. Investors in the coin filed a federal class action lawsuit in April against Benjamin Chow, co-founder of crypto exchange Meteora, and Hayden Davis, co-founder of crypto venture capital firm Kelsier Labs, among others, WIRED reported Tuesday.

***

Meme stock prices have shown dramatic volatility, with the Roundhill MEME ETF reflecting sharp swings driven by retail investor sentiment and social media hype.

The phenomenon of meme stocks—equities that gain popularity through online communities rather than traditional financial metrics—has reshaped market dynamics since early 2021. Companies like GameStop and AMC became emblematic of this trend, as retail investors coordinated on platforms like Reddit to drive prices to unprecedented highs. To capture this movement, the Roundhill Meme Stock ETF (ticker: MEME) was launched, bundling popular meme stocks into a single investment vehicle.

The price history of the MEME ETF illustrates the volatility inherent in meme stock investing. In October 2025 alone, the ETF experienced dramatic fluctuations. On October 13, it closed at $10.85, marking a 14.57% gain from the previous day. Just three days later, on October 16, it dropped to $9.97, an 8.95% decline. These swings reflect the influence of social media sentiment, short squeezes, and speculative trading rather than company fundamentals.

Over the past year, the MEME ETF has seen a 74.5% decline, underscoring the risks of investing in stocks driven by hype rather than earnings or growth potential. Despite occasional rallies, the overall trend has been downward, with the ETF trading around $8.93 as of the latest close.

This price history highlights the speculative nature of meme stocks. While they can offer short-term gains, they are highly susceptible to rapid reversals. Investors drawn to meme stocks should be aware of the emotional and social dynamics that drive their prices, and consider whether such volatility aligns with their risk tolerance and investment goals.

In essence, meme stock price history is a story of community-driven market disruption, where traditional valuation models are often sidelined in favor of viral momentum.

The MEME ETF serves as a barometer for this cultural shift, capturing both the excitement and the instability of this new investing frontier.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

So, advice is subject to a fiduciary duty, while product sales (brokerage) activity is not. The ratio of fiduciary advice to brokerage sales is about 1:99. So, what does that tell you?

A Contentious and Complicated Issue

This issue is so contentious and complicated today that lawyers are needed to define each and every term, engagement, transaction, brokerage or advisory contract, etc. It is far too amazingly contorted and complicated for most; including me; and we have even discussed the industry machinations and political double-talk on this ME-P previously; from some vary sharp industry experts, too.

The “work-around” for these rules is industry “dual-registration”. Simply put, just get licensed to do both; as I did. Charge a commission when selling stuff and charge a fee for advice. And ideally, do both at the same time; while getting paid for both sides.

As a naïve luddite, I learned this little truism in financial planning school decades ago, and as a doctor and fiduciary for my patients at all times, almost vomited.

Of course, there were more sophisticated students in our classes who regurgitated the standard industry opinion: “We’ll give the client a financial plan for free IF we can sell commissioned products.”

Ideally this meant a fat and fully commissioned wrap account, whole-life insurance policy, LTCI policy; etc. Or, sell products and collect fat ongoing, and often unrecognizable AUM fees [fee-only], too!

From the stock broker-advisor’s POV, it was “Heads I win – tails you loose” for the client. Now, you know why I am a former or reformed certified financial planner.

The Physics Split

Know that as a pre-medical college student years earlier, I leaned about the Werner Heisenberg Uncertainty Principle, in physics class.

Of course, true Advice – is not Sales … and Sales is not Advice. Both should never be; simultaneously. So, let’s ditch dual registration and decide which to pursue … and then proceed accordingly. Both sales and advice have risks and benefits to client and producer; both have advantages and disadvantages to both; as well.

WHY? Just like the Werner Heisenberg Uncertainty Principle; it shouldn’t [shan’t] be both; at once.

NOTE: In quantum mechanics, the Heisenberg uncertainty principle is any of a variety of mathematical inequalities asserting a fundamental limit to the precision with which certain pairs of physical properties of a particle, known as complementary variables, such as position x and momentum p, can be known simultaneously.

So, in physics, I can tell you where you are -OR- how fast you are going; but not both. Thus, if it is product sales; it is not advice.

Today, since “dual registration” is still allowed, my suggestion to clients is to seek a fiduciary in all matters 24/7/354; get it in writing, and try to avoid arbitration and “best interest” or BICE clauses! Run from [fee-based and fee-only] AUM fees, too.

PS: I am not against Series #7 representatives and product sales. Salesmen/women often provide a valuable service and should be appropriately compensated. I only object when fees, costs, charges and commissions are duplicative, excessive and/or not fully disclosed to the client. Since excessive is an arbitrary term; full disclosure is the key ingredient.

Assessment

So – How am I wrong, mistaken and/or what did I miss? Do tell! Should We – Can We – Ditch Dual Registration [DDR]?

Oh! In the future, I also hope that State fiduciary standards will potentially cover both non-ERISA and ERISA situations, and employee plan participants will have access to full discovery rights, the one thing the industry fears most.

But, that’s a discussion for another day and time.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

President Donald Trump signed a pardon on Wednesday for convicted crypto executive Changpeng Zhao, who founded the Binance crypto exchange, White House Press Secretary Karoline Leavitt said in a statement. “President Trump exercised his constitutional authority by issuing a pardon for Mr. Zhao, who was prosecuted by the Biden Administration in their war on cryptocurrency,” Leavitt said. “In their desire to punish the cryptocurrency industry, the Biden Administration pursued Mr. Zhao despite no allegations of fraud or identifiable victims.”

Zhao was sentenced to four months in prison after reaching a deal with the Justice Dept. to plead guilty to charges of enabling money laundering at Binance, which he ran at the time. The U.S. also ordered Binance to pay more than $4 billion in fines and forfeiture, while Zhao agreed to pay $50 million in fines. A spokesperson for Binance did not immediately respond to a request for comment yesterday.

***

The History of Cryptocurrency: From Concept to Revolution

Cryptocurrency has transformed the global financial landscape, offering a decentralized alternative to traditional banking systems. Its history is rooted in decades of technological innovation, philosophical ideals, and economic experimentation.

🌐 Early Foundations

The concept of digital currency predates Bitcoin by several decades. In 1982, cryptographer David Chaum published a groundbreaking paper on secure digital transactions, laying the foundation for future developments in electronic money. Chaum later founded DigiCash in the 1990s, which introduced the idea of anonymous digital payments using cryptographic protocols. Although DigiCash eventually failed, it was a crucial stepping stone in the evolution of cryptocurrency.

The Birth of Bitcoin

The true revolution began in 2008 when an anonymous figure—or group—known as Satoshi Nakamoto released the Bitcoin whitepaper titled “Bitcoin: A Peer-to-Peer Electronic Cash System.” This document proposed a decentralized digital currency that used blockchain technology to record transactions transparently and securely without the need for a central authority.

On January 3, 2009, Nakamoto mined the first block of the Bitcoin blockchain, known as the Genesis Block. The first real-world Bitcoin transaction occurred in May 2010, when programmer Laszlo Hanyecz paid 10,000 BTC for two pizzas—an event now celebrated annually as Bitcoin Pizza Day.

Blockchain and Beyond

Bitcoin’s success inspired the development of other cryptocurrencies and blockchain platforms. Ethereum, launched in 2015 by Vitalik Buterin, introduced smart contracts—self-executing agreements coded directly into the blockchain. This innovation expanded the use of cryptocurrency beyond simple transactions to decentralized applications (dApps), finance (DeFi), and even digital art (NFTs).

Other notable cryptocurrencies include Litecoin, Ripple (XRP), and Cardano, each offering unique features such as faster transaction speeds, improved scalability, or enhanced privacy.

***

***

⚖️ Challenges and Controversies

Despite its promise, cryptocurrency has faced significant hurdles. Regulatory uncertainty, security breaches, and market volatility have raised concerns among governments and investors. High-profile hacks, such as the Mt. Gox exchange collapse in 2014, highlighted the risks associated with digital assets.

Governments around the world have responded differently—some embracing crypto innovation, others imposing strict regulations or outright bans. The rise of central bank digital currencies (CBDCs) reflects an effort to merge the benefits of crypto with the stability of fiat systems.

🚀 The Future of Crypto

Today, cryptocurrency is more than a niche technology—it’s a global phenomenon. Major companies accept Bitcoin, institutional investors hold crypto assets, and blockchain is being integrated into industries from healthcare to supply chain management.

As the technology matures, the focus is shifting toward scalability, sustainability, and interoperability. Whether it becomes a mainstream financial tool or remains a disruptive alternative, cryptocurrency has undeniably reshaped how we think about money, trust, and digital ownership.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on October 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

NFTs, or Non-Fungible Tokens, are unique digital assets stored on a blockchain that represent ownership of a specific item or piece of content. Unlike cryptocurrencies like Bitcoin or Ethereum, which are fungible and interchangeable, NFTs are one-of-a-kind and cannot be exchanged on a one-to-one basis.

In recent years, Non-Fungible Tokens (NFTs) have emerged as a groundbreaking innovation in the digital world, revolutionizing how we perceive ownership, art, and value online. At their core, NFTs are cryptographic tokens that represent a unique digital item or asset. These tokens are stored on a blockchain—a decentralized digital ledger—which ensures that each NFT is verifiable, traceable, and immutable.

The term “non-fungible” means that each token is distinct and cannot be replaced with another token of equal value. This contrasts with fungible assets like dollars or cryptocurrencies, where each unit is identical and interchangeable. For example, one Bitcoin is always equal to another Bitcoin. However, each NFT has its own metadata, ownership history, and attributes, making it unique and often valuable.

NFTs can represent a wide range of digital content, including artwork, music, videos, virtual real estate, gaming items, and even tweets. Artists and creators have embraced NFTs as a new way to monetize their work, bypassing traditional gatekeepers like galleries and record labels. By minting their creations as NFTs, they can sell them directly to collectors and fans, often earning royalties from future resales thanks to smart contracts embedded in the blockchain.

One of the most popular blockchains for NFTs is Ethereum, which supports smart contracts and has a robust ecosystem for digital assets. Platforms like OpenSea, Rarible, and Foundation have become marketplaces where users can buy, sell, and trade NFTs. These platforms often require users to have a digital wallet and use cryptocurrency to complete transactions.

The rise of NFTs has sparked debates about their environmental impact, speculative nature, and long-term value. Critics argue that the energy consumption of blockchain networks can be significant, especially those using proof-of-work mechanisms. Others worry that the NFT market is driven by hype and may not sustain its current levels of interest and investment. Nonetheless, proponents believe that NFTs offer a new paradigm for digital ownership and creativity, empowering artists and reshaping industries from gaming to fashion.

In conclusion, NFTs represent a fusion of technology, art, and commerce, offering a novel way to own and trade digital assets. As the technology matures and adoption grows, NFTs may become a standard part of our digital lives, influencing how we interact with content, creators, and each other in the virtual world.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

An automobile is one of the biggest purchases after a home; for many physicians and most all of us. But, unlike the typical home, it is usually a depreciating asset – today morning you purchase a car for X-amount of dollars and by the evening it will be worth less. After 5 years it will not be even half-value but still, many folks keep buying cars regularly – buy at 10, sell at 4 & lose 6 (repeat the cycle).

So, here are few financial rules of thumb that you can follow:

The value of a car should not be more than 50% of the annual income of the owner.

Purchase a used car or buy a new & use it for 10 years.

While buying a car with a loan stick to Rule 20/4/10 – Minimum 20% down payment, loan tenure not more than 4 years & EMI should not be higher than 10% of your income.

Note: Equated Monthly Installment [EMI]

Caution: The phrase rule of thumb refers to an approximate method for doing something, based on practical experience rather than theory. This usage of the phrase can be traced back to the 17th century and has been associated with various trades where quantities were measured by comparison to the width or length of a human adult thumb.

Posted on October 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

DEFINED

***

***

A physician practice management corporation (PPMC) is a business entity that provides non-clinical administrative and operational support to medical practices, allowing physicians to focus on patient care while the corporation handles the business side of healthcare.

Physician practice management corporations emerged in response to the increasing complexity of running a medical practice. As healthcare regulations, insurance requirements, and operational costs grew, many physicians found it challenging to manage both clinical responsibilities and business operations. PPMCs offer a solution by taking over the administrative burdens, enabling physicians to concentrate on delivering quality care.

At their core, PPMCs are responsible for a wide range of non-medical services. These include billing and coding, human resources, payroll, marketing, compliance, information technology, and financial management. By centralizing these functions, PPMCs can achieve economies of scale, reduce overhead costs, and improve operational efficiency for the practices they manage. This model is particularly attractive to small and mid-sized practices that may lack the resources to manage these functions independently.

PPMCs typically enter into long-term management agreements with physician groups. In some cases, they may purchase the non-clinical assets of a practice—such as equipment, office space, and administrative staff—while the physicians retain control over clinical decisions and patient care. This arrangement allows for a clear division between medical and business responsibilities, which is essential for maintaining compliance with healthcare regulations like the Stark Law and the Anti-Kickback Statute.

A physician practice management corporation (PPMC) is a business entity that provides non-clinical administrative and operational support to medical practices, allowing physicians to focus on patient care while the corporation handles the business side of healthcare.

Physician practice management corporations emerged in response to the increasing complexity of running a medical practice. As healthcare regulations, insurance requirements, and operational costs grew, many physicians found it challenging to manage both clinical responsibilities and business operations. PPMCs offer a solution by taking over the administrative burdens, enabling physicians to concentrate on delivering quality care.

At their core, PPMCs are responsible for a wide range of non-medical services. These include billing and coding, human resources, payroll, marketing, compliance, information technology, and financial management. By centralizing these functions, PPMCs can achieve economies of scale, reduce overhead costs, and improve operational efficiency for the practices they manage. This model is particularly attractive to small and mid-sized practices that may lack the resources to manage these functions independently.

PPMCs typically enter into long-term management agreements with physician groups. In some cases, they may purchase the non-clinical assets of a practice—such as equipment, office space, and administrative staff—while the physicians retain control over clinical decisions and patient care. This arrangement allows for a clear division between medical and business responsibilities, which is essential for maintaining compliance with healthcare regulations like the Stark Law and the Anti-Kickback Statute.

***

***

One of the key advantages of working with a PPMC is access to capital and advanced infrastructure. PPMCs often invest in state-of-the-art electronic health record (EHR) systems, data analytics tools, and revenue cycle management platforms. These technologies can enhance patient care, streamline operations, and improve financial performance. Additionally, PPMCs may offer strategic guidance on practice expansion, mergers and acquisitions, and payer contract negotiations.

However, the relationship between physicians and PPMCs must be carefully managed. While PPMCs bring valuable expertise and resources, there is a risk that business priorities could overshadow clinical autonomy. To mitigate this, successful PPMCs prioritize physician engagement, transparent governance, and aligned incentives. They work collaboratively with physicians to ensure that business strategies support, rather than hinder, the delivery of high-quality care.

The physician practice management industry has evolved significantly over the past few decades. After a wave of failures in the 1990s due to overexpansion and misaligned incentives, modern PPMCs have adopted more sustainable and physician-centric models. Today, they play a crucial role in helping practices adapt to value-based care, population health management, and other emerging trends in healthcare delivery.

In conclusion, a physician practice management corporation serves as a strategic partner to medical practices, offering the business acumen and operational support needed to thrive in a complex healthcare environment. By offloading administrative tasks and providing access to advanced resources, PPMCs empower physicians to focus on what they do best—caring for patients—while ensuring the long-term success and sustainability of their practices.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Turning 65 is often seen as the gateway to retirement—a time to slow down, reflect, and enjoy the fruits of decades of labor. But for some, including doctors who may have faced financial setbacks, poor planning, or unexpected life events, reaching this milestone without financial security can be deeply unsettling. The image of a broke 65-year-old doctor may seem paradoxical, given the profession’s reputation for high earnings. Yet, reality paints a more nuanced picture. Fortunately, even in the face of financial hardship, retirement is not a closed door—it’s a challenge that can be met with creativity, resilience, and strategic planning.

Understanding the Situation

Before exploring solutions, it’s important to understand how a physician might arrive at retirement age without adequate savings. Medical school debt, late career starts, divorce, health issues, poor investment decisions, or supporting family members can all contribute. Some doctors work in lower-paying specialties or underserved areas, sacrificing income for impact. Others may have lived beyond their means, assuming their high salary would always be enough. Regardless of the cause, the key is to shift focus from regret to action.

Traditional retirement—ceasing work entirely—is not the only option. For a broke 65-year-old doctor, retirement may mean transitioning to a less demanding role, reducing hours, or shifting to a new field. The goal is to create a sustainable lifestyle that balances income, purpose, and well-being.

Leveraging Medical Expertise

Even if full-time clinical practice is no longer viable, a physician’s knowledge remains valuable. Here are several ways to continue earning while easing into retirement:

Telemedicine: Remote consultations are in high demand, especially in primary care, psychiatry, and chronic disease management. Telemedicine offers flexibility, reduced overhead, and the ability to work from home.

Locum Tenens: Temporary assignments can fill staffing gaps in hospitals and clinics. These roles often pay well and allow for travel or seasonal work.