BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on May 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Classic Definition: In our hemisphere, there is the mystery of the Cuban health care paradox.

Modern Circumstance: This small island country whose economy produces about $6,000 in goods and services per person annually, a mere fraction of U.S. economic activity, lacks access to many commonly used drugs. Specialty medical care is scarce, and obesity rates are high and growing.

Paradox Example: Yet Cuba paradoxically boasts a life expectancy that surpasses the U.S. by six months. So, could this finding be explained by their diet, too, one that is rich in fresh produce, but low in saturated fats?

Question: Or, might it be related to their accessibility to primary care services and high compliance rates of childhood vaccination?

COMMENTS APPRECIATED

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on May 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

BREAKING NEWS

***

***

UnitedHealth Group just announced the exit of CEO Andrew Witty and suspended its 2025 forecast due to surging medical costs, sending its shares down more than 10%. Chairman Stephen Hemsley will become CEO, effective immediately.

The fourth-largest U.S company big revenue in 2024, Minnetonka-based UnitedHealth has experienced a turbulent year that saw the shock killing of United Healthcare CEO Brian Thompson in New York City, and a cyberattack that affecting an estimated 190 million people and cost the company an estimated $3.1 billion dollars.

Virtual chronic care provider Omada Health has filed to go public in the United States, the latest in a string of healthcare listings expected this year. Omada did not disclose the details as to how much it plans to raise from its IPO.

The San Francisco, California-based company, which last raised $192 million in a Series E funding round in 2022, reported a 38% increase in revenue to $169.8 million for 2024, according to its IPO paperwork. For the first quarter of 2025, the company posted a 56.6% year-on-year jump in revenue to $55 million. Omada has applied to list its common stock on the NASDAQ under the symbol “OMDA”.

Healthcare IPOs on U.S. exchanges have fetched $7.1 billion in 2024, compared with $2.8 billion a year earlier, according to data compiled by LSEG.

Posted on May 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

I’ve received emails from readers asking my thoughts on DeepSeek. I need to start with two warnings. First, the usual one: I’m a generalist value investor, not a technology specialist (last week I was analyzing a bank and an oil company), so my knowledge of AI models is superficial. Second, and more unusually, we don’t have all the facts yet.

But this story could represent a major step change in both AI and geopolitics.

Here’s what we know:

DeepSeek—a year-old startup in China that spun out of a hedge fund—has built a fully functioning large language model (LLM) that performs on par with the latest AI models. This part of the story has been verified by the industry: DeepSeek has been tested and compared to other top LLMs. I’ve personally been playing with DeepSeek over the last few days, and the results it spit out were very similar to those produced by ChatGPT and Perplexity—only faster.

This alone is impressive, especially considering that just six months ago, Eric Schmidt (former Google CEO, and certainly no generalist) suggested China was two to three years behind the U.S. in AI.

But here’s the truly shocking—and unverified—part: DeepSeek claims they trained their model for only $5.6 million, while U.S. counterparts have reportedly spent hundreds of millions or even billions of dollars. That’s 20 to 200 times less.

The implications, if true, are stunning. Despite the U.S. government’s export controls on AI chips to China, DeepSeek allegedly trained its LLM on older-generation chips, using a small fraction of the computing power and electricity that its Western competitors have. While everyone assumed that AI’s future lay in faster, better chips—where the only real choice is Nvidia or Nvidia—this previously unknown company has achieved near parity with its American counterparts swimming in cash and datacenters full of the latest Nvidia chips. DeepSeek (allegedly) had huge compute constraints and thus had to use different logic, becoming more efficient with subpar hardware to achieve a similar result.

In other words, this scrappy startup, in its quest to create a better AI “brain,” used brains where everyone else was focusing on brawn—it literally taught AI how to reason.

Financial Advisor, Planner and Insurance Agent Information

By Staff Reporters

***

***

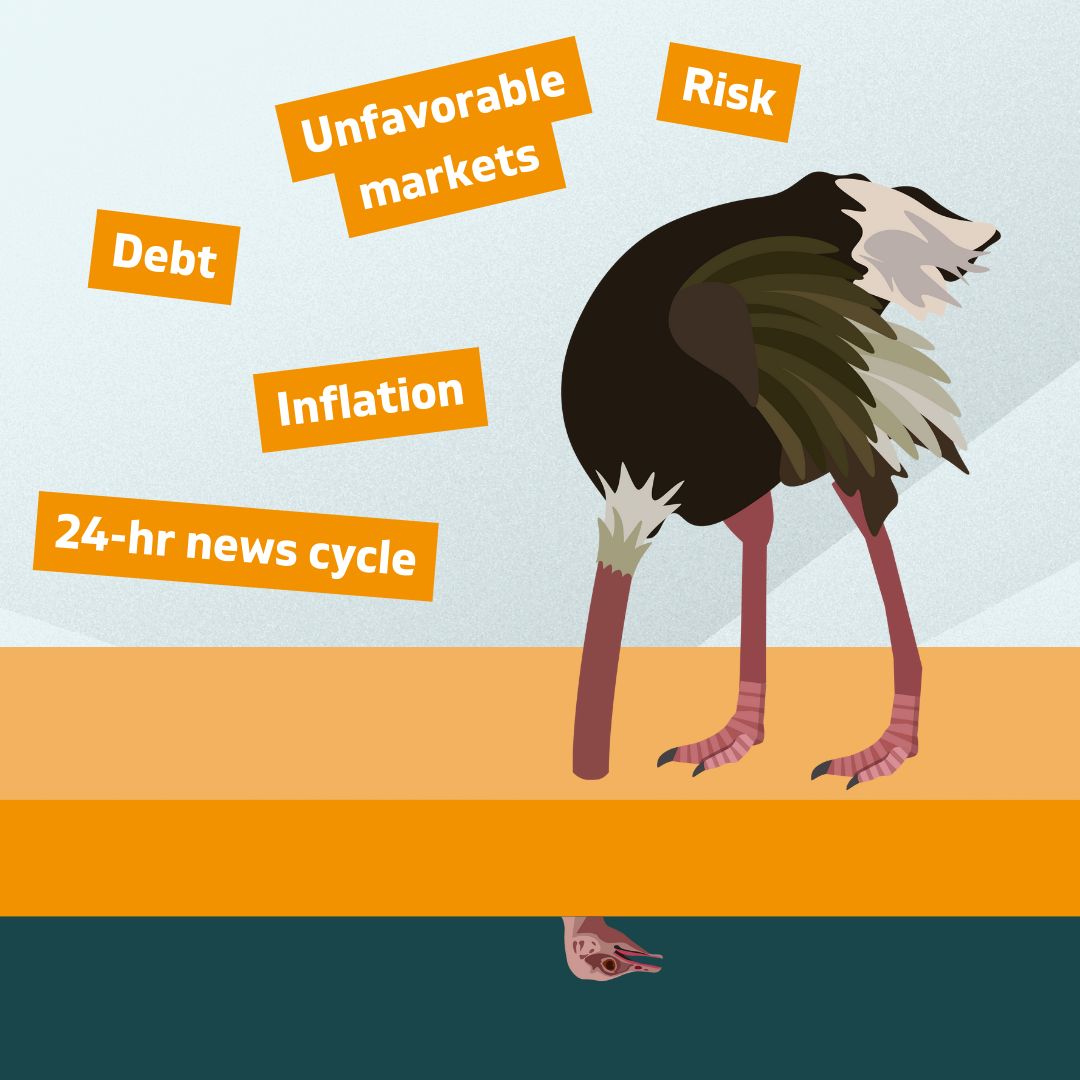

Ostrich Bias is a behavioral phenomenon describing the tendency of individuals to avoid or ignore information that they perceive as negative or threatening. This term is derived from the popular but inaccurate belief that ostriches bury their heads in the sand when faced with danger, even though they do not exhibit such behavior.

Evidence: There is neuro-scientific evidence of the ostrich effect. Sharot et al. (2012) investigated the differences in positive and negative information when updating existing beliefs. Consistent with the ostrich effect, participants presented with negative information were more likely to avoid updating their beliefs; wills, estate plans, investment portfolios, and insurance policies, etc..

Moreover, they found that the part of the brain responsible for this cognitive bias was the left IFG – inferior frontal gyrus – by disrupting this part of the brain with TMS – transcranial magnetic stimulation – participants were more likely to accept the negative information provided.

EXAMPLE: The Ostrich Bias can cause someone to avoid looking at their bills, because they’re worried about seeing how far behind they are on home mortgage payments, credit cards, education or auto loans, etc.

COMMENTS APPRECIATED

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on May 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

As of 1998, May 8th was designated as National Student Nurses Day, to be celebrated annually. And as of 2003, National School Nurse Day is celebrated on the Wednesday within National Nurses Week (May 6-12) each year.

***

***

The nursing profession has been supported and promoted by the American Nurses Association (ANA) since 1896. Each of ANA’s state and territorial nurses associations promotes the nursing profession at the state and regional levels. Each conducts celebrations on these dates to recognize the contributions that nurses and nursing make to the community.

The ANA supports and encourages National Nurses Week recognition programs through the state and district nurses associations, other specialty nursing organizations, educational facilities, and independent health care companies and institutions.

Posted on May 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

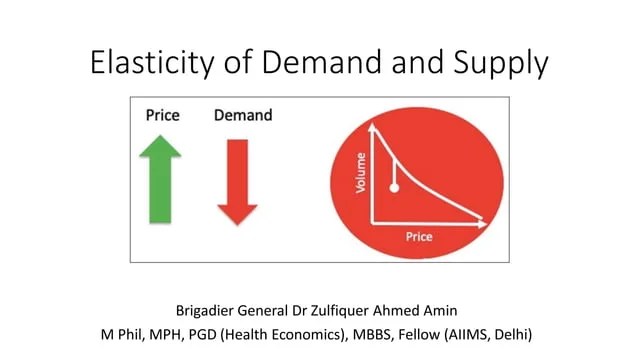

Classic: Despite a wide variety of empirical methods and data sources, the demand for health care is consistently found to be price inelastic

Modern: If you are sick, you will not be very price sensitive. There are exceptions to this rule (e.g., elective surgery such as plastic surgery, purchases of eyeglasses) but most studies find that patients are fairly insensitive to changes in health care prices.

Examples: For instance, the RAND Health Insurance Experiment found that the price elasticity of medical expenditures is -0.2.

***

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on May 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

If getting answers from ChatGPT makes you feel dystopian, you may not want to hear about OpenAI CEO Sam Altman’s other co-founded venture, now rolling out stateside. It scans your eyeballs in exchange for cryptocurrency.

What in the Demolition Man? The device, which creates a unique user ID for your scan, is meant to address a problem that Altman had a hand in creating: how to verify identities and confirm humanity in a world full of artificial intelligence.

The project, called World (formerly Worldcoin), went live in other countries in 2023. Its US expansion, announced this week, featured retail outlets in five cities where you can get your eyes scanned:

Tools for Humanity, the company behind the orbs, says 12+ million people around the world have participated so far.

It claims to keep your data private, but authorities in more than a dozen places have suspended World’s operations or investigated its data practices, per the WSJ.

Some retired people live on a fixed income and many of them live right on the edge of their financial capability. At some time in their life, they may have to make a choice regarding many purchases.

In this case, we will illustrate “choice” using a couple’s purchase of Long-Term-Care Insurance [LTCI]. Of course, economics is the study of choice; wants, needs and scarcity, etc. In our case, if they decide to make the purchase they commit to a lifetime of premium payments. The financial tradeoff is this; if they make the commitment to purchase LTCI, they must give up something else.

EXAMPLE: In order to maintain a monthly premium of $100 ($1,200per year), an elderly patient, retired layman or couple must essentially relegate about $30,000 of financial assets to generate the $100 necessary to make an average premium payment (assumes a 7% rate of return with 4% withdrawal rate) or [4% X $30,000 = $1,200 year]. Thus, if the monthly premium cost is $500 per month, the elder must give up the use of $150,000 of retirement asset just to generate enough cash flow to pay for the LTC insurance.

***

***

The married elder couple has to make the Hobson’s Choice decision among lifestyle (dinners, vacations, gifts to children, prescription drugs, medical care or food and shelter) versus paying an insurance premium to provide for nursing home coverage for a need, which may be very real, but will not occur until sometime in the ambiguous future.

And so, when faced with such a tough economics Hobson’s Medicine Choice, neither of which delivers peace of mind or a respectable solution; many will simply decide that, in either case, they may already end up impoverished. Thus, many will often opt for the better lifestyle now … while they can enjoy it … together.

Cite: Anonymous Health Insurance Agent, Norcross, Georgia

COMMENTS APPRECIATED

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on May 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The National Nurses in Business Association (NNBA) is the premier nursing organization for nurse entrepreneurs, and a springboard for nurses transitioning from employees to entrepreneurs and business owners. The NNBA is an invaluable resource for existing nurse business owners seeking to expand, and maximize their business success.

Members’ resumes include thousands of nurse owned businesses, local, national and international awards, and millions of dollars in revenue. The experience, knowledge and impact of the NNBA community is amazing, as well as the support provided to fellow nurse entrepreneurs and aspiring entrepreneurs.

As the forerunner of the nurse entrepreneur movement, the NNBA provides valuable business information customized for nurses on how to start, plan, expand and grow your nurse owned business. They provide expert guidance, marketing and promotional opportunities, and continuing education in professional growth and career development.

Phantom equity is an increasingly popular tool within businesses, particularly startups and private companies, for incentivizing employees without diluting ownership. It allows firms to reward key personnel by linking compensation to the company’s performance, aligning employee interests with those of shareholders.

Basic Mechanisms of Phantom Equity

Phantom equity operates as a contractual agreement offering employees a simulated stake in the business without issuing actual stock. This arrangement appeals to companies aiming to maintain control over their equity structure while providing performance-based incentives. The benefits mimic stock ownership, such as dividends and capital appreciation, without the complexities of transferring actual shares.

The company establishes a phantom equity plan that defines terms such as vesting schedules, performance metrics, and payout conditions. Vesting schedules, often ranging from three to five years, encourage employee retention. Performance metrics may include revenue growth, profit margins, or other financial indicators aligned with strategic goals. Once vested, employees receive cash payments based on the value of the phantom shares, determined by the company’s valuation at payout.

Valuations, often conducted through third-party appraisals or internal financial metrics, directly affect payouts. If the company grows significantly, the value of phantom shares increases, resulting in higher payouts. Conversely, if performance declines, the value of these shares decreases, reducing compensation.

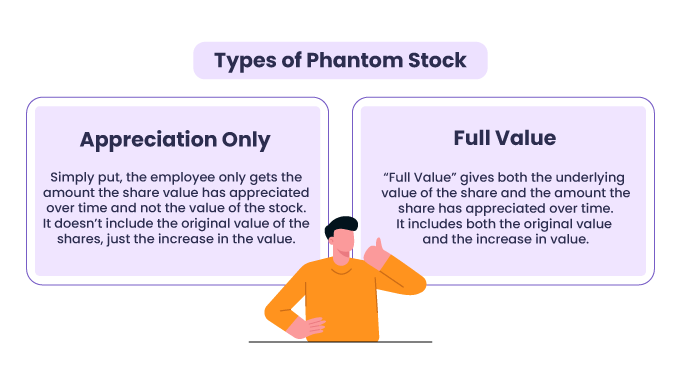

Types of Phantom Equity Plans

Phantom equity plans can be customized to suit a company’s goals, with two primary types being most common: appreciation-only arrangements and full-value arrangements.

Appreciation-Only Arrangements

Appreciation-only arrangements reward employees for the increase in the company’s value over a specified period. Employees are granted phantom shares that reflect the appreciation in the company’s valuation from the grant date to the payout date.

For instance, if phantom shares are initially valued at $10 each and the valuation rises to $15, the employee receives a payout of $5 per share. This structure ties employee rewards to company growth without affecting equity. Companies must rely on precise valuation methods, often adhering to GAAP or IFRS, to ensure fairness and compliance.

Full-Value Arrangements

Full-value arrangements provide payouts equivalent to the full value of phantom shares at vesting or payout. This includes both the initial value and any appreciation.

For example, if phantom shares are initially valued at $10 and later rise to $15, the employee receives $15 per share. While offering greater potential rewards, full-value arrangements require a larger financial commitment from the company. Careful financial planning and adherence to standards like ASC 718, which governs share-based compensation, are essential for managing these plans effectively.

Posted on April 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Consumer sentiment is a statistical measurement of the overall health of the economy as determined by consumer opinion. It takes into account how people feel about their current financial health, the health of the economy in the short-term, and the prospects for longer-term economic growth. It is widely considered to be a useful economic indicator.

Consumer sentiment emerged as an economic statistic during the mid-20th century and has since become a barometer that influences public and economic policy. It is considered a lagging indicator because it takes people several months to notice and feel the effects of changes in economic activity.

American consumers are Worried about the Economy

Consumer sentiment dropped 8% from March to April amid worries about inflation, according to the University of Michigan’s closely watched survey. Though sentiment edged up slightly from an even lower reading earlier in the month, inflation expectations climbed to their highest since 1991 as consumers fret about the potential impact of tariffs.

And even beyond possible rising prices, things could be about to get rougher for consumers: Major retailers have warned that unless President Trump’s tariff policy toward China changes, they’re likely to encounter empty store shelves in a few weeks.

Posted on April 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

FUNDAMENTAL INDUSTRY CHANGES

By Staff Reporters

***

***

Index Funds

An index mutual fund or ETF (exchange-traded fund) tracks the performance of a specific market benchmark—or “index,” like the popular S&P 500 Index—as closely as possible. That’s why you may hear people refer to indexing as a “passive” investment strategy.

Instead of hand-selecting which stocks or bonds the fund will hold, the fund’s manager buys all (or a representative sample) of the stocks or bonds in the index it tracks.

***

Quantum Computing

Unlike traditional computers that use bits, quantum computers utilize qubits. These qubits are capable of being in a state of superposition, where they can represent both 0 and 1 simultaneously, enabling the processing of multiple calculations at once. This could allow quantum computers to outperform classical computers in solving certain complex problems. However, the field is still overcoming challenges such as qubit stability and decoherence; especially in these three areas:

Quantum computing could fundamentally alter healthcare by accelerating drug discovery and improving individualized medicine. Rapid analysis of enormous volumes of biological data allows quantum computers to find trends that might guide the creation of more potent treatments. In addition to accelerating drug development, this will enable customized treatments tailored to unique genetic profiles.

Faster and more accurate financial models produced by quantum computing will transform the banking sector. Through real-time analysis of intricate financial systems, it can help investors to control risk and make better decisions. More precise market forecasts will help maximize portfolio management and trading strategies.

Through greatly enhanced medical diagnosis and patient care, quantum computing can transform the healthcare industry. Quantum computers can remarkably accurately find trends and possible health hazards by analyzing enormous volumes of medical data in a fraction of the time. Early diagnosis and more customized treatment alternatives follow from this.

B–QTUM Index Fund

Index Description: The BlueStar® Machine Learning and Quantum Computing Index (BQTUM) tracks liquid companies in the global quantum computing and machine learning industries, including products and services related to quantum computing or machine learning, such as the development or use of quantum computers or computing chips, superconducting materials, applications built on quantum computers, embedded artificial intelligence chips, or software specializing in the perception, collection, visualization, or management of big data.

Posted on April 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler CFP™

***

***

Lately, I’ve been hearing the same question from clients and readers alike: “Is Social Security even going to be there in five years?” Fueling this concern is a recent viral comment from Elon Musk, who told Joe Rogan that Social Security is “the biggest Ponzi scheme of all time.” That quote has been repeated in every corner of the internet, stirring up uncertainty and fear.

Elon Musk is a genius, but his brilliance in technology and innovation doesn’t automatically translate into expertise in public policy. When it comes to Social Security, he’s outside his lane. Calling it a Ponzi scheme may make for a great soundbite, but it’s a fundamental mischaracterization.

Social Security is not a Ponzi scheme. Not even close.

A Ponzi scheme is a form of financial fraud that lures investors with the promise of high returns. Instead of earning those returns through legitimate investments, the scheme pays earlier investors using money from newer ones. Eventually, the model collapses when there aren’t enough new participants to keep it going, leaving most people with significant losses. This is what happened to those who trusted Bernie Madoff, operator of one of the worst Ponzi schemes in history. Ponzi schemes are illegal, deceptive, and doomed from the start.

Social Security, in contrast, is a government-run, pay-as-you-go tax program. It’s fully transparent; you know exactly where your money is going. The payroll taxes you and your employer pay are used to provide income to today’s retirees, people with disabilities, and surviving family members of deceased workers. This isn’t a con, it’s a social contract.

So why the confusion? Part of the issue is that Social Security does, on the surface, resemble the flow of a Ponzi scheme: money coming in from the young to support the old. But similarity in structure doesn’t make it fraudulent. The program does not promise high returns, it promises a modest, inflation-adjusted benefit to support people as they age.

Social Security does face challenges. The trust fund reserves, built up during years when payroll taxes exceeded payouts, are projected to run dry around 2033. If Congress does nothing, benefits will need to be cut by about 20%. That’s serious, but it’s a solvency issue, not a scam.

And the solvency issue is fixable. There are numerous bipartisan proposals to shore up the system for the long term, from raising the payroll tax cap to gradually adjusting benefits. These aren’t radical ideas, they’re common-sense repairs. A bipartisan mix of 100 CFPs in a room could work out a solution in two days.

When clients ask me if the system will be around in five years, what they’re really asking is: Can I trust it? Can I trust the government? Can I trust that my years of work and tax payments will mean something in retirement? These are not just policy questions. They are emotional questions based on fear of scarcity and a desire for security. When someone with Elon Musk’s influence wrongly calls Social Security a Ponzi scheme, his attention-grabbing soundbite shakes the emotional foundation of that trust.

If we’re serious about preserving Social Security, let’s start by calling it what it is: a commitment to our elders. A tax-supported promise to care for one another across generations.

Social Security is not a fraud, it’s a shared responsibility based on the kind of society we want and woven into the fabric of American life. Yes, it needs some adjustments, but it’s not broken. Rather than eroding public trust with misleading comparisons, we should be focused on debating public policy and how we can strengthen and sustain the program for future generations.

***

ME-P NOTE: An increase in Social Security benefits is on the horizon, providing a potential financial cushion against rising inflation. The Cost of Living Adjustment (COLA) for 2025 is set at 2.5% monthly, translating to an average annual increase of approximately $600 for beneficiaries. This adjustment is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers. While not guaranteed annually, COLA has historically been implemented in most years due to persistent inflationary trends.

Posted on April 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants LLC

***

***

On April 7, 2025, the Centers for Medicare & Medicaid Services (CMS) published their 2026 Rate Announcement for Medicare Advantage (MA) and Medicare Part D Prescription Drug Plans.

For 2026, the payment rate to MA plans will increase 5.06%, the largest increase in the past ten years, and up significantly from the 2.2% rate increase proposed by the Biden Administration.

This Health Capital Topics article will review the Rate Announcement.(Read more…)

Posted on April 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler CFP™

***

***

On January 21, 1980, in what I thought was a brilliant financial move, I bought gold. At what was then an all-time high of $873 an ounce.

Fast forward 45 years, and here we are again. Gold is on a tear, priced just over $3,000 an ounce at the time of this writing. It needs to rise another 16% to reach its inflation-adjusted record and many analysts think it might just get there.

What’s driving this gold rally? The same thing that drove it in 1980—fear.

Back then, the U.S. was grappling with rising inflation, double-digit price increases, and interest rates in the high teens. Investors feared that the dollar and stock market would collapse, that their hard-earned savings would erode into oblivion, and that gold was a safe haven. Sound familiar?

Today, inflation is less dramatic and the stock market would have to go a long way down to even register as a bear market, but it’s still a major concern. Central banks are buying gold at record levels. Gold-backed ETFs, which had been seeing years of outflows, are finally pulling investors back in.

For most, gold isn’t just an investment, it’s an emotional hedge against uncertainty. Back in 1980, I wasn’t thinking about long-term strategy. I was reacting to fear. Inflation had hit 14%, and like many others, I was convinced the dollar would soon be worthless. Gold, I thought, was my best shot at preserving wealth.

The problem? Inflation eventually cooled; it had dropped to an average of 3.5% by the mid-1980s. Gold prices tumbled along with it. Investors who, like me, bought at the peak, 45 years later still haven’t broken even on an inflation-adjusted basis. (My $873 purchase price, adjusted for inflation, equates to $3,580 today.) If I had stuck with a well-diversified portfolio, I likely would have fared much better over time.

Over the years, I’ve come to realize that our financial decisions aren’t just about numbers. They’re deeply influenced by our Internal Financial System™, a framework that helps explain why we handle money the way we do. I now see that my decision to buy gold was a battle between different financial “parts” of myself.

One part panicked, convinced that money was about to become worthless. Another saw gold prices soaring and didn’t want to miss out. Yet another part convinced me that buying at the peak was still a smart move. Had I paused and examined these internal voices, I might have made a different decision.

My gold purchase shows why emotionally driven investment decisions rarely lead to great financial outcomes. Instead of asking, “Is gold a smart long-term investment?” I was asking, “How do I make sure I don’t lose everything?” Those are two very different questions.

If you’re thinking about buying gold, I urge you to consider these questions:

“Am I investing from a place of fear or strategy?” If you’re rushing in because you’re scared of inflation, pause and reassess.

“How does gold fit into my broader financial plan?” Gold can be a great hedge—if held in appropriate amounts in a diversified portfolio. It is best viewed as catastrophic financial insurance, rather than an investment.

“Am I reacting to headlines or making a well-thought-out decision?” The financial media loves a good gold rally. But remember, markets move in cycles. Today’s rally may be history repeating itself.

Back in 1980, fear persuaded me that gold was a sure thing. I forgot an essential caveat—there are no sure things in investing. If bad market timing were an Olympic sport, I’d have taken home the gold (pun intended) for least profitable performance.

In a discussion of competitive healthcare economic models, assumptions must include normal demand quantities, many fully informed patients and the fact that physicians cannot directly influence demand for medical care. These assumptions, although fluid, also preclude that patient buyers are large enough to have any influence over price and result in the following”:

In a “pure monopoly”, there is only one provider with a unique service. The doctor is a “price maker” and charges whatever s/he wishes.

In an “oligopoly”, there are a few physicians who provide similar services. For example, when it becomes clear to Dr. Smith and Dr. Jones that neither can win their price war, oli-gopolists return prices to prior, but still inflated levels!

In “monopolistic competition”, there are many providers with differentiated services. For example, should Dr. Jones decide to have evening hours, she may charge a premium for her fees if Dr. Jones doe not follow suit.

Finally, when “pure competition” occurs, there are many physicians, providing providing similar and substitutable services. Marketing and advertising does not affect fees, and prices are determined by supply and demand. The doctors become “price takers” by accepting fees arrived at by practicing competitively.

COMMENTS APPRECIATED

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on April 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A thought experiment is an imaginary scenario that is meant to elucidate or test an argument or theory. It is often an experiment that would be hard, impossible, or unethical to actually perform. It can also be an abstract hypothetical that is meant to test our intuitions about morality or other fundamental philosophical questions. The German term Gedankenexperiment was utilized by physicist Ernst Mach

***

Mary is a brilliant scientist who is, for whatever reason, forced to investigate the world from a black and white room via a black and white television monitor. She specializes in the neuro-physiology of vision and acquires, let us suppose, all the physical information there is to obtain about what goes on when we see ripe tomatoes, or the sky, and use terms like ‘red’, ‘blue’, and so on.

Question: What will happen when Mary is released from her black and white room or is given a color television monitor? Will she learn anything or not?

***

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on April 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and Lawrence Rosenberg

***

***

Cold calling is a term that is typically applied to telesales, but most new business relationships actually begin with a “cold” contact of some kind. Whether through social media, email over the phone or door-to-door, “cold calling” lives up to its name; you are contacting prospects (hopefully decision makers) sans introduction and without warning. In some, if not many cases, you will be presenting to customers who have never heard of you, your firm, or your product/service prior to you getting a hold of them. You will also find yourself coming up against the palace guards (secretaries and personal assistants) whose most important job is to run interference for the boss and thwart any and all attempts that an unfamiliar caller might make to reach them. But, as the sales game will readily teach anyone with the fortitude to last long enough to learn the lesson, the more resistance one faces in the pursuit of a successful outcome, the bigger the payoff will be if one can muster the grit necessary to tough it out.

However difficult the road to riches, cold calling allows for a complete leveling of the playing field. Those that sweep the streets could tomorrow talk with billionaires; a man of little status or worth could enter into a contract with the founder of a blue chip, multinational firm — all with a single, unexpected phone call. The sheer daring of such an approach, its impromptu nature, works for so many reasons, not least of which is that it opens doors. From the intrigue and urgency the suddenness of the call implies, to the instant access a bold overture provides, cold calling is the great equalizer among executives, and a path to achievement open to all, no matter one’s experience, education or connections. Not that there ever were any truly insurmountable barriers to climbing the corporate ladder or accessing its highest rungs that a motivated self-starter could not overcome, but with the advent of the telephone and the brashness of the cold sell perfected, the most entrenched and frustrating of impediments, bureaucracy and fraternalism, ceased to be an obstacle. Yesteryear’s power elite traditionally only did business with friends, acquaintances and family (or perhaps a member of their local country club or lodge), but at the very least, those that connected in business were routinely introduced through a referral. However, the audacity of the unscheduled contact, the inspired notion of a “cold call,” and the realization that it worked, that a person of great esteem or importance was willing to do business with an unusually forward individual, made the glad-handing salesman who relied on his father’s rolodex obsolete.

With ivory towers toppled, etiquette overturned and tradition tossed out, ambitious men ignored propriety and custom and cold canvassed the board of directors and senior executive staff of companies both large and small. The old boy’s network, favoritism, and the “it’s not what you know, but who you know” principle of doing business crumbled in one fell swoop. The ramparts guarded by all manner of gatekeepers and middle men were trampled the moment the CEO became connected by wires to the outside world. Using nothing more than a telephone, a Horatio Alger-type work ethic and a well-rehearsed voice, the business world was invaded by those without patronage, underdogs and unknowns swarmed the gates. The cold call allowed the unfiltered, unapproved spirit of the upstart, unfettered by lackeys and administrators, to enter the inner sanctum of a chieftain and with the power of speech alone, win hearts and minds.

But, can one’s voice really move mountains? Must one not support the message with documentation and material, nurture relationships with lunches and meetings and personally shake hands to set the wheels of industry in motion? Is one unannounced, unsolicited, unscreened call enough?

The human voice is the master manipulator of sound and when paired with the right words it has a potent and intoxicating effect on behavior. Although some people react more favorably to stimulation of the other five senses, sound on its own can evoke them all. Those that study the science of suggestion will note the immense influence of other stimuli, such as that which affects sight and sensation, on how we make sense of our experiences, on how we make decisions, but it is the way in which such sensory bias is communicated (via the written word, and more powerfully, through speech) that truly tells the tale. The combination to unlocking the interests of many a man’s mind are often verbalized in the common yet telling replies to intriguing, thought provoking questions or action demanding requests.

***

***

It is all a matter of deciphering the code, the clue-laden language:

“What you said really touched me.”

“I see the light!”

“You can smell his fear.”

“Let’s give that guy a taste of his own medicine.”

“You are coming across loud and clear.”

The way in which we describe our observations provides the key to how we interpret data, how that data impacts us, and through what primary pathway we process such information. It is our use of language that exposes how we perceive the world around us, how the gears of our minds are moved, and which of the five senses most effectively winds the springs that turn them.

Many times a prospect will request to have a look at your proposition in writing before moving forward, others will react positively based solely on their impression. Some say seeing is believing, but if it soundsexciting and beneficial, they will take action regardless because it just feels right.

All our senses come alive when the brain is stimulated, some more than others depending on the man and the moment, but the terms, phrases and idioms that we use when speaking (their quality, nuance and character) and the way in which they are expressed, have the power to move us in life-changing ways — the spoken word, when used properly, can play us like a piano.

Whether impacted more by sight, olfaction or incitement of the somatosensory system (the way things feel physically), one can induce the imagery and kinesthesia necessary to motivate and influence a prospect from afar with voice alone. Provocative descriptions, the proper use of tone and inflection, and the strategic interweaving of silence (of which sometimes nothing can be more deafening or exert more pressure) can activate or set in motion all manner of action. Practiced speech can lighten the heaviest heart or wrest tears from the coldest stare, it can conjure up a dream state or snap you back to reality. Never underestimate what a skillful performer can do with the right vocabulary and properly trained vocals. Charlton Heston could inspire awe, Orson Welles conjure intrigue, and Luciano Pavarotti demand devotion with nothing more than the weight and timbre of their words.

You too can affect people, positions and outcomes with sonant spirit and verbal substance. Invest in the greatest tool for success a deal maker has, your lexicon, your locution and your delivery.

Posted on April 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

OpenAI would be open to buying Chrome if Google is forced by a federal court to sell the web browser, the company’s ChatGPT head said yesterday.

The FDA suspended milk quality tests in some dairy products due to reduced capacity stemming from federal workforce cuts, Reuters reported.

Roche, the Swiss pharmaceutical giant, is investing $50 billion in US manufacturing to circumvent President Trump’s tariffs, the company said yesterday.

Rite Aid is preparing to sell itself in pieces ahead of a possible second bankruptcy, Bloomberg reported.

Oklo gained 8.60% after OpenAI CEO Sam Altman announced he’s stepping down as chairman of the board of the nuclear power startup.

Duolingo popped 10.01% after Morgan Stanley initiated coverage of the language learning company, calling it a “best-in-class consumer internet asset.”

Cava climbed 6.29% due to an upgrade from analysts at Bernstein, who think the bowl slop stock will not only survive but thrive in an economic downturn.

Amphenol rose 8.21% thanks to impressive earnings for the high-speed cable company, coupled with a solid fiscal outlook.

Vertiv Holdings jumped 8.60% after the data center company posted an impressive quarterly profit and raised its fiscal forecast.

Stocks surged first thing this morning after President Trump said the media blew things out of proportion and that he has “no intention” of firing Jerome Powell. He also said he would be “very nice” to China in tariff negotiations.

Treasury Secretary Scott Bessent also did some damage control, touting the opportunity for a “big deal” between the US and China.

The combination sent a relief rally sweeping through markets, and while the euphoria faded by mid-afternoon, all three indexes ended the day in the green.

Gold fell and bitcoin rose as investors took on more risk (see below), while oil dropped on reports that OPEC+ may hike its crude output after its meeting next month.

An annuity is a contract between you and an insurance company. When you purchase an annuity, you make a lump-sum contribution or a series of contributions, generally each month. In return, the insurance company makes periodic payments to you beginning immediately or at a pre-determined date in the future. These periodic payments may last for a finite period, such as 20 years, or an indefinite period, such as until both you and your spouse are deceased. Annuities may also include a death benefit that will pay your beneficiary a specified minimum amount, such as the total amount of your contributions.

The growth of earnings in your annuity is typically tax-deferred; this could be beneficial as you may be in a lower tax bracket when you begin taking distributions from the annuity.

Warning: A word of caution: Annuities are intended as long-term investments. If you withdraw your money early from an annuity, you may pay substantial surrender charges to the insurance company as well as tax penalties to the IRS and state.

***

***

There are three basic types of annuities — fixed, indexed, and variable

1. With a fixed annuity, the insurance company agrees to pay you no less than a specified (fixed) rate of interest during the time that your account is growing. The insurance company also agrees that the periodic payments will be a specified (fixed) amount per dollar in your account.

2. With an indexed annuity, your return is based on changes in an index, such as the S&P. Indexed annuity contracts also state that the contract value will be no less than a specified minimum, regardless of index performance.

3. A variable annuity allows you to choose from among a range of different investment options, typically mutual funds. The rate of return and the amount of the periodic payments you eventually receive will vary depending on the performance of the investment options you select.

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

A Certified Public Accountant (CPA) is a licensed professional who has passed an examination administered by a state’s Board of Accountancy. State CPA exams are created under guidelines issued by The American Institute of Certified Public Accountants (AICPA). The Uniform CPA Exam can only be taken by accountants who already have professional experience in the field and a bachelor’s degree.CPAs are not fiduciaries.

Not all accountants are CPAs. Accountants who are CPAs are licensed by their state’s Board of Accountancy after passing the Uniform CPA Exam. CPAs prepare reports that accurately reflect the business dealings of the companies and individuals that hire them. Many prepare tax returns for individuals or businesses and advise them on ways to minimize taxes. Obtaining the CPA designation requires a bachelor’s degree, typically with a major in business administration, finance, or accounting. Other majors are acceptable if the applicant meets the minimum requirements for accounting courses.

Enrolled Agent

Although not a CPA, an Enrolled Agent [EA] is a person who has earned the privilege of representing taxpayers before the Internal Revenue Service [IRS]. This is done by either passing a three-part comprehensive IRS test covering individual and business tax returns, or through experience as a former IRS employee. Enrolled agent status is the highest credential the IRS awards. Individuals who obtain this elite status must adhere to ethical standards and complete 72 hours of continuing education courses every three years.

Certified Managerial Accountant

A Certified Management Accountant (CMA), which is issued by the Institute of Management Accountants (IMA), builds on financial accounting proficiency by adding management skills that aid in making strategic business decisions based on financial data.

Oftentimes, the reports and analyses prepared by certified management accountants (CMAs) will go above and beyond those required by generally accepted accounting principles (GAAP).

For example, in addition to a company’s required GAAP financial statements, CMAs may prepare additional management reports that provide specific insights useful to corporate decision-makers, such as performance metrics on specific company departments, products, or even employees.

Certified Financial Analyst

A Certified Financial Analyst [CFA] is a globally-recognized professional designation offered by the CFA Institute, an organization that measures and certifies the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management, and security analysis. From 1963 through November 2023, more than 3.7 million candidates had taken the CFA exam. The overall pass rate was 45%. From 2014 through 2023, the 10-year average pass rate was 43%.1

CFA Institute. The CFA Institute was formerly the Association for Investment Management and Research (AIMR).

The CFA charter is one of the most respected designations in finance and is widely considered to be the gold standard in the field of investment analysis. To become a charter holder, candidates must pass three difficult exams, have a bachelors degree, and have at least 4,000 hours of relevant professional experience over a minimum of three years. Passing the CFA Program exams requires strong discipline and an extensive amount of studying.

There are more than 200,000 CFA charter holders worldwide in 164 countries.The designation is handed out by the CFA Institute, which has 11 offices worldwide and 160 local member societies.

Posted on April 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

OFTEN CONFUSING TO ALL

By Staff Reporters

***

***

A vehicle typically has two prices: the manufacturer’s suggested retail price (MSRP) and the invoice price. The MSRP is the sticker price, while the invoice price is what the dealer paid the manufacturer for the vehicle. The MSRP includes a hefty profit, so that’s what dealers want you to focus on. However, your goal should be to get the invoice price and focus on that for your negotiations.

However, finding invoice pricing on new cars can be difficult when going through the dealer. Dealers don’t want their invoice price on a vehicle to be public knowledge because that gives customers more leverage when it comes to negotiations. Just like any company, car dealers are in the business to make money. They can’t make money if they give you a huge discount on a car.

What is a Vehicle Invoice Price?

When it comes to the car buying process, there are several other terms and types of pricing you should understand. One of them is the vehicle invoice price. This is also known as the dealer cost, or what a car manufacturer charges the dealer for that specific vehicle. Freight charges are typically included in this total.

However, the numbers on the invoice may not be the true price the dealer paid for the vehicle, because it has hidden profits already built-in. Dealers are often given manufacturer rebates, allowances, discounts, and other incentives for selling a car. The invoice price on a vehicle may range from several hundred to several thousand dollars below its sticker price, which is why service will help you determine what the real numbers look like.

So, once you determine the car invoice price, you have added leverage when it comes to negotiating the best price possible with the auto dealer.

In finance, a “Dead Cat Bounce” is a small, brief recovery in the price of a declining stock.

Derived from the idea that “even a dead cat will bounce if it falls from a great height“, the phrase, which originated on Wall Street, is also popularly applied to any case where a subject experiences a brief resurgence during or following a severe market decline.

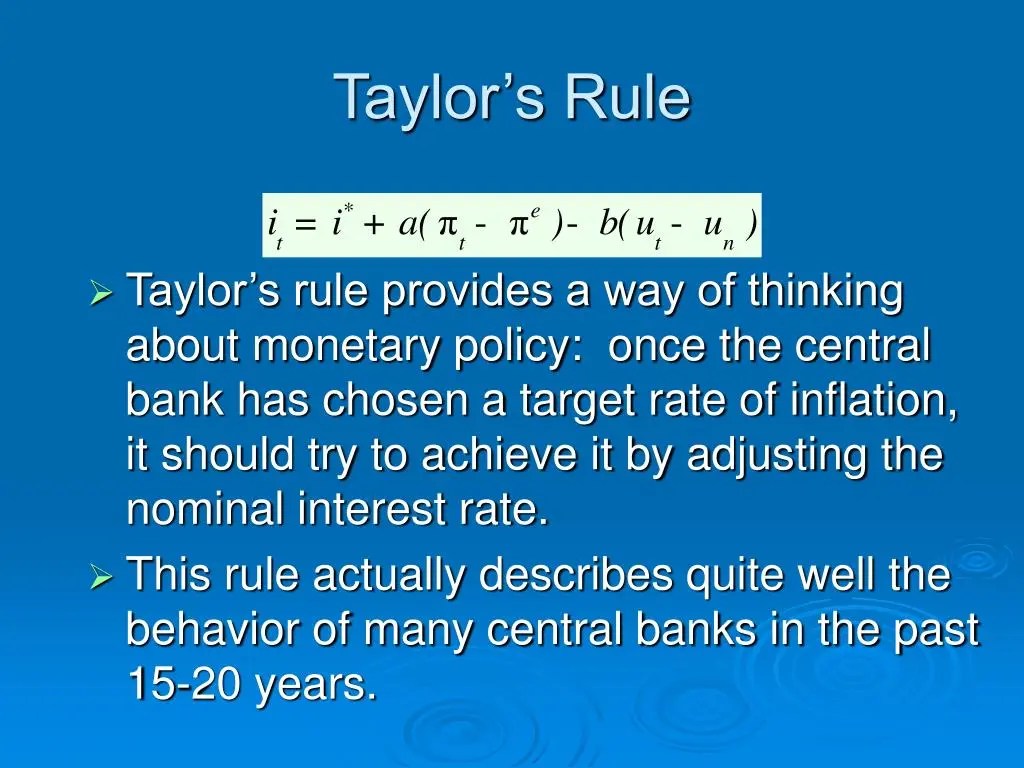

Named for a U.S. economist, the JB Taylor Rule is a mathematical monetary-policy formula that recommends how much a central bank should change its nominal short-term interest rate target (such as the U.S. Federal Reserve’s federal funds rate target) in response to changes in economic conditions, particularly inflation and economic growth. It’s typically viewed as guideline for raising short-term interest rates as inflation and potentially inflationary pressures increase. The rule recommends a relatively high interest rate (“tight” monetary policy) when inflation is above its target or when the economy is above its full employment level, and a relatively low interest rate (“easy” monetary policy) under the opposite conditions.

To illustrate, the monetary policy of the FOMC changed throughout the 20th century. The period between the 1960s and the 1970s is evaluated by Taylor and others as a period of poor monetary policy; the later years typically characterized as stagflation. The inflation rate was high and increasing, while interest rates were kept low. Since the mid-1970s monetary targets have been used in many countries as a means to target inflation.

However, in the 2000s the actual interest rate in advanced economies, notably in the US, was kept below the value suggested by the Taylor rule.

Posted on April 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

According to colleague Dan Ariely PhD, Bereavement Sex is one of those coping mechanisms that sounds strange but makes sense when you think about it. In the face of loss, our brains crave connection and comfort.

Engaging in sex after a significant loss can be a way to feel alive and regain a sense of control. It’s a testament to our complex emotional wiring, where grief and intimacy intertwine.

The VIX soared to 60.13 last Monday before plummeting all the way to 33.76 on Wednesday, the day after the president paused tariffs. But while the VIX has since settled down a bit, investor fear is still high. The VIX closed above 30 for 10 straight trading sessions and the last time that happened was during the bear market back in October 2022, according to MarketWatch—not exactly a comforting comparison.

Then again, just because fear skyrocketed last week doesn’t mean the markets will tank in turn. “Since 1997, there have been 11 times the VIX spiked above 45—and 10 out of 11 times, the S&P 500 was higher four months later by an average of +6.4%,” noted Austin Hankowitz in the latest edition of the Rich Habits newsletter.

Finally, the VIX closed above 30 Thursady as tariff talk and monetary policy pivots keep investors on their toes. But while worries might keep investors on the sidelines, some on Wall Street are taking this opportunity to be greedy while others are fearful.

There’s often a disconnect between physicians, insurance agents and financial advisors and the patients and clients they’d like to serve. Both might ostensibly share the same goal but there’s often a big difference in perspective. Advisors / Physicians and would-be clients / patients likely have different communication styles, especially in an age where technology has greatly changed the way we talk with one another. Their expectations and priorities can also often dramatically diverge. Those structural gaps can hinder collaboration and trust.

To bridge this divide, you must understand how prospective clients and patients think nowadays and be able to adjust your M.A.S. approach accordingly.

THE BASICS

Marketing is the business process of identifying, anticipating and satisfying patient’s, client’s or customers’ needs and wants. It is your unique value proposition or strategic competitive advantage. Marketers can direct product to other businesses or directly to consumers. But, we believe it is actually your strategic competitive advantage [SCA] which differentiates yourself from competitors. It is the “moat” around your business.

Advertising is a marketing communication that employs an openly sponsored, non-personal message to promote or sell a product, service or idea. Sponsors of advertising are typically businesses wishing to promote their products or services. Advertising is communicated through various mass media outlet, including traditional media such as newspapers, magazines, television, radio, outdoor advertising or direct mail; and new media such as search results, blogs, social media, websites or text messages. The actual presentation of the message in a medium is referred to as an advertisement, or “ad” or advert for short. But, we believe that is simply how you disseminate your strategic competitive advantage [SCM] to potential clients.

Sales close the deal and collects money. Sales are activities related to selling or the number of goods or services sold in a given targeted time period. The seller, or the provider of the goods or services, completes a sale in response to an acquisition, appropriation, requisition, or a direct interaction with the buyer at the point of sale. There is a passing of title (property or ownership) of the item, and the settlement of a price, in which agreement is reached on a price for which transfer of ownership of the item will occur. The seller, not the purchaser, typically executes the sale and it may be completed prior to the obligation of payment. In the case of indirect interaction, a person who sells goods or service on behalf of the owner is known as a salesman or saleswoman or salesperson, but this often refers to someone selling goods in a store/shop, in which case other terms are also common, including salesclerk, shop assistant, and retail clerk.

***

***

DERIVATIVE THOUGHTS

Public Relations [PR] is differentiated than advertising from in that an advertiser pays for and has control over the message. It differs from personal selling in that the message is non-personal, i.e., not directed to a particular individual. We pay for advertising but pray for public relations. But public relations are not controllable but it is free, while advertising is not. PR suggests that “good news or bad news”; just spell the name correctly

Change Management is the discipline that guides how we prepare, equip and support individuals to successfully adopt to change in order to drive organizational success and outcomes.

Crisis Management is the precautions and identification of threats to an organization and its stakeholders, and the methods used by the organization to deal with these threats.

MODERNITY NOW

CRM stands for Customer Relationship Management, which is a system for managing all interactions with current and potential customers, clients or patients. The goal is simple: improve relationships to grow your business or medical practice. CRM technology helps companies stay connected to customers, streamline processes, and improve profitability.

When people talk about CRM, they’re usually referring to a CRM system: software that helps track each interaction you have with a prospect, patient or customer. That can include sales calls, treatment plans or service interactions, marketing e-mails, and more. CRM tools can unify customer and company data from many sources and even use Artificial Intelligene [AI] to help better manage relationships across the entire customer – patient lifecycle – spanning departments described in the M.A.S. basics, above.

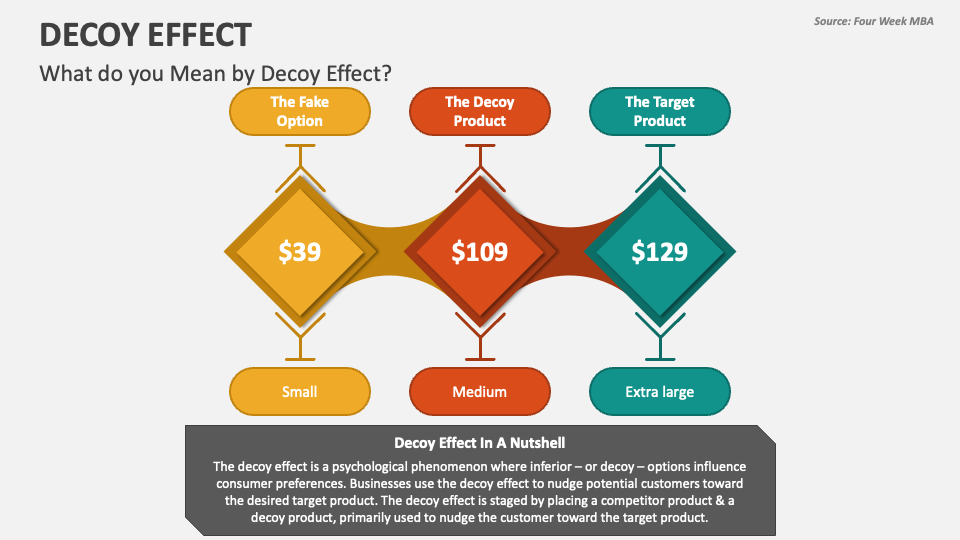

Decoy Bias Effect is a dubious phenomenon in decision-making where the introduction of a third, less attractive option (the “decoy”) influences individuals to change their preference between two other options.

The decoy bias effect describes how, when we are choosing between two alternatives, the addition of a third, less attractive option (the decoy) can influence our perception of the original two choices. Decoys are “asymmetrically dominated:” they are completely inferior to one option (the target) but only partially inferior to the other (the competitor). For this reason, the decoy effect is sometimes called the “asymmetric dominance effect.”

EXAMPLE: This bias is commonly used in financial planning sales; as well as marketing and mutual fund, ETF, REIT, stock broker, insurance agent and financial advisor pricing strategies to manipulate investor choices.

When you buy a share of stock, you are taking ownership in a company. Collectively, the company is owned by all the shareholders, and each share represents a claim on assets and earnings. If the company distributes profits to its shareholders, you should receive a proportionate share of the earnings.

Stocks are often categorized by the size of the company, or their market capitalization. The market capitalization is determined by multiplying the number of outstanding shares by the current share price. The most common market cap classes are small-cap (valued from $100 million to $1 billion), mid-cap ($1 billion to $10 billion), and large cap ($10 billion to $100 billion).

Stocks are also categorized by their sector, or the type of business the company conducts. Common sectors include utilities, consumer staples, energy, communications, financial, health care, transportation, and technology.

***

***

Stocks are often viewed as being in one of two categories — growth or value.

Growth stocks are ones that are associated with high quality, successful companies that are expected to continue growing at a better-than-average rate as compared to the rest of the market.

Value stocks are ones that have generally solid fundamentals, but are currently out of favor with the market. This may be due to the company being relatively new and unproven in the market, or because the company has recently experienced a decline due to the company’s sector being affected negatively. An example of this would be if the federal government was to levy a new tax on all cell phones, thus negatively affecting all cell phone company stocks.

History has shown that, over time, stocks have provided a better return than bonds, real estate, and other savings vehicles. As a result, stocks may be the ideal investment for investors with long-term goals.

Classic: An arrangement by which a patient requests that their health benefit payments be made directly to a designated person or facility, such as a physician or hospital. It is a legally binding agreement between patient and Insurance company asking them to send your reimbursement checks directly to your doctor.

Modern: To accept assignment means that the provider agrees to accept what ever the insurance company allows or approves as payment in full for the claim. The patient signs paperwork requiring his health insurance provider to pay his physician or hospital directly. EXAMPLES:

CMS: The approved amount, also known as the Medicare-approved amount, is the fee that Medicare sets as how much a provider or supplier should be paid for a particular service or item. Original Medicare calls this “assignment.”

Tardiness: When a medical office accepts an assignment of benefits, the insured patients may have to wait several months for their insurance reimbursement to arrive.

Classic: It’s no surprise that people are more honest when they know that they’re being watched. But what about just reminding them of the idea of being watched, without them actually being watched?

Modern: Researchers at the University of Newcastle’s Division of Psychology have an honor (or trust) system where they are requested to deposit payment for coffee in an “honesty box.” There was a note saying how much they should pay.

In 2006, Dr. Melissa Bateson and colleagues decided to do a little experiment: they placed an image above the note. They alternate between two pictures: one week they would use a picture of alleged human eyes and the other week, flowers. After 10 weeks, they plotted the amount of money received versus drinks consumed and found that people paid nearly three times as much for their drinks when eyes were displayed.

“There’s an argument that if nobody is watching us it is in our interests to behave selfishly. But when we think we’re being watched we should behave better, so people see us as co-operative and behave the same way towards us,” — Dr Bateson said

EXAMPLE:

Tax: This has great exemplar potential in things like federal, state and local income tax preparation, etc.

Insight: “It’s a definite that you’re all going to screw up, but it’s not a definite that any of you will learn from that,” declared one of our medical school instructors, years ago. “Cultivate the attitude that allows you to own your mistakes, and then, not repeat them” — reported Monique Tello MD MPH.

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

WARNING – WARNING

By Staff Reporters

***

***

A “retirement account scam” is a type of online fraud that occurs when a third party administrator (TPA) for retirement investment accounts is tricked into authorizing a money distribution to an imposter posing as the true account holder.

The imposter often starts the scam by calling the TPA, identifying himself or herself as an actual account holder, and requesting a withdrawal distribution form. Once the imposter receives the withdrawal distribution form, the imposter returns the completed form to the TPA. The form is completed with the account holder’s real personal identifying information (PII)—often stolen via schemes, data breaches, and other hacking offenses—and bank account information for an account controlled by the imposter or the imposter’s conspirators.

***

***

After the TPA processes the fraudulent request, the request is forwarded to the investment firm responsible for managing the account holder’s investments, and the funds—often the account holder’s life savings—are then directed to the imposter’s designated bank account.

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Natural Disaster Insurance

Protecting accumulated assets by insuring them against the wrath of Mother Nature

Most homeowners’ insurance policies do not cover damages arising from floods or earthquakes. If a home, or any other real property like a vacation home or beach condo, is in an area subject to floods or earthquakes, consider the value of purchasing insurance that covers such catastrophes.

Take the time to review your homeowners’ policy, making sure that it will repair or replace your roof if damaged by hail, and will apply in the event of high winds, rather than only in tornadoes. The key to the maintenance of any type of insurance is to anticipate all of the possible calamities, and then to decide whether you can afford to lose the assets exposed to those calamities.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Beneficiary designations can provide a relatively easy way to transfer an account or insurance policy upon your death. However, if you’re not careful, missing or outdated beneficiary designations can easily cause your estate plan to go awry.

Where you can find them

Here’s a sampling of where you’ll find beneficiary designations:

In several states, so-called “lady bird” deeds for real estate

***

***

10 tips about beneficiary designations

Because beneficiary designations are so important, keep these things in mind in your estate planning:

Remember to name beneficiaries. If you don’t name a beneficiary, one of the following could occur:

The account or policy may have to go through probate. This process often results in unnecessary delays, additional costs, and unfavorable income tax treatment.

The agreement that controls the account or policy may provide for “default” beneficiaries. This could be helpful, but it’s possible the default beneficiaries may not be whom you intended.

Name both primary and contingent beneficiaries. It’s a good practice to name a “back up” or contingent beneficiary in case the primary beneficiary dies before you. Depending on your situation, you may have only a primary beneficiary. In that case, consider whether it may make sense to name a charity (or charities) as the contingent beneficiary.

Update for life events. Review your beneficiary designations regularly and update them as needed based on major life events, such as births, deaths, marriages, and divorces.

Read the instructions. Beneficiary designation forms are not all alike. Don’t just fill in names — be sure to read the form carefully. If necessary, you can draft your own customized beneficiary designation, but you should do this only with the guidance of an experienced attorney or tax advisor.

Coordinate with your will and trust. Whenever you change your will or trust, be sure to talk with your attorney about your beneficiary designations. Because these designations operate independently of your other estate planning documents, it’s important to understand how the different parts of your plan work as a whole.

Think twice before naming individual beneficiaries for particular assets. For example, you may establish three accounts of equal value initially and name a different child as beneficiary of each account. Over the years, the accounts may grow or be depleted unevenly, so the three children end up receiving different amounts — which is not what you originally intended.

Avoid naming your estate as beneficiary. If you designate a beneficiary on your 401(k), for example, it won’t have to go through probate court to be distributed to the beneficiary. If you name your estate as beneficiary, the account will have to go through probate. For IRAs and qualified retirement plans, there may also be unfavorable income tax consequences.

Use caution when naming a trust as beneficiary. Consult your attorney or CPA before naming a trust as beneficiary for IRAs, qualified retirement plans, or annuities. There are situations where it makes sense to name a trust — for example if:

Your beneficiaries are minor children

You’re in a second marriage

You want to control access to funds

Be aware of tax consequences. Many assets that transfer by beneficiary designation come with special tax consequences. It’s helpful to work with an experienced tax advisor to help provide planning ideas for your particular situation.

Use disclaimers when necessary — but be careful. Sometimes a beneficiary may actually want to decline (disclaim) assets on which they’re designated as beneficiary. Keep in mind that disclaimers involve complex legal and tax issues and require careful consultation with your attorney and CPA.

Posted on April 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

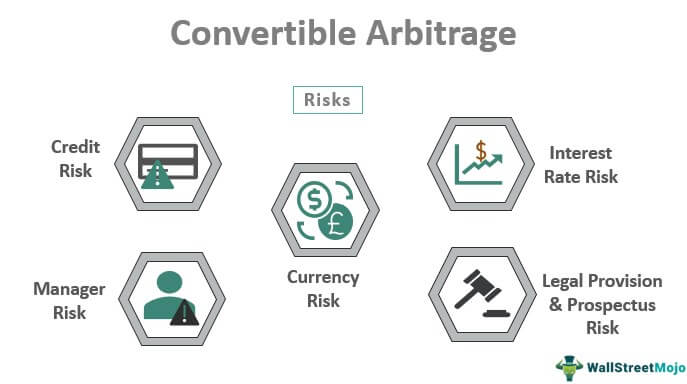

Convertible Arbitrage

Convertible arbitrage is the oldest market-neutral strategy. Designed to capitalize on the relative mispricing between a convertible security (e.g. convertible bond or preferred stock) and the underlying equity, convertible arbitrage was employed as early as the 1950s.

Since then, convertible arbitrage has evolved into a sophisticated, model-intensive strategy, designed to capture the difference between the income earned by a convertible security (which is held long) and the dividend of the underlying stock (which is sold short). The resulting net positive income of the hedged position is independent of any market fluctuations. The trick is to assemble a portfolio wherein the long and short positions, responding to equity fluctuations, interest rate shifts, credit spreads and other market events offset each other.

***

***

Hedge Fund Research (HFR) New York, offers the following description of the strategy

Convertible Arbitrage involves taking long positions in convertible securities and hedging those positions by selling short the underlying common stock. A manager will, in an effort to capitalize on relative pricing inefficiencies, purchase long positions in convertible securities, generally convertible bonds, convertible preferred stock or warrants, and hedge a portion of the equity risk by selling short the underlying common stock. Timing may be linked to a specific event relative to the underlying company, or a belief that a relative mispricing exists between the corresponding securities. Convertible securities and warrants are priced as a function of the price of the underlying stock, expected future volatility of returns, risk free interest rates, call provisions, supply and demand for specific issues and, in the case of convertible bonds, the issue-specific corporate/Treasury yield spread. Thus, there is ample room for relative mis-valuations.

Because a large part of this strategy’s gain is generated by cash flow, it is a relatively low-risk strategy.

Posted on April 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Credit Card Mistakes to Avoid

No number has as far-reaching an impact on your money as your credit scores. Here are some credit card obstacles all physicians, nurses and medical professionals should dodge on the road to financial security

An alternative investment is a financial asset that does not fall into one of the conventional investment categories. Conventional categories include stocks, bonds, and cash. Alternative investments can include private equity or venture capital, hedge funds, managed futures, art and antiques, commodities, and derivatives contracts. Real estate is also often classified as an alternative investment.

QUESTION: But what about a medical, podiatric or dental practice?

***

***

AnAlternate Asset Class Surrogate?

A medical practice is much like an alternative investment [AI], or alternate asset class in, two respects.

First, it provides the work environment that generates personal income which has been considered generous, to date.

Second, it has inherent appreciation and sales value that can be part of an exit (retirement) or succession planning transfer strategy.

Conclusion

So, unlike the emerging thought that offers Social Security payments as a surrogate for an asset classes; or a federally insured AAA bond – a medical practice might also be considered by some folks as an asset class within a well diversified modern investment portfolio.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

The vast majority of physicians and medical professionals major in one of the hard science while in college; biology, engineering, chemistry, mathematics, computer science or physics; etc. Few take undergraduate courses in finance, business management, securities analysis, accounting or economics; although this paradigm is changing with modernity. These course are not particularly difficult for the pre-medical baccalaureate major, they are just not on the radar screen for time compressed and highly competitive students; nor are they needed for medical or nursing school admission, or the many related allied health professional schools.

In fact, William C. Roberts MD, originally from Emory University in Atlanta, and former editor for the Baylor University Medical Center Proceedings and The American Journal of Cardiology, opined just a decade ago:

“Of the 125 medical schools in the USA, only one of them to my knowledge offers a class related to saving or investing money.”

And so, it is important to review some basic principles of economics, finance and accounting as they relate to financial planning in thees two textbooks; and this ME-P.

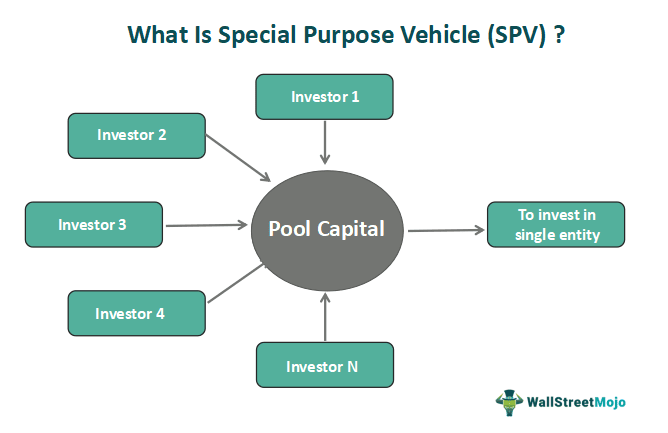

Its purpose is to isolate the parent company from any potential credit or financial risk that may arise from the SPV and is often used to pursue riskier projects, securitize debt, or transfer assets. Since an SPV is separate from the parent company, it isn’t affected by the parent’s performance, and the parent isn’t typically affected by the performance of the SPV. If the parent goes bankrupt and is no longer in existence, the SPV can carry on.

This makes an SPV bankruptcy remote. This also means that the parent company is unaffected by the loss if the SPV fails.

Posted on April 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

THE “FIVE-FIVE” FINANCIAL RULE

By Staff Reporters

***

***

Many of the pros of home ownership will appeal to medical retirees for whom their home is their castle and who appreciate being settled both financially and geographically:

1. Building equity in your home: Each mortgage payment you make brings you closer to owning your house free and clear with no payments. If you can buy a new home or condo outright by selling your current home, you can still build equity in your new home over time.

2. Predictability: If you have a fixed-rate mortgage, your mortgage payments will remain consistent for years and you don’t have to worry about a landlord ever making you move.

3. Tax benefits: You can deduct mortgage interest and property taxes up to certain limits.

4. Customization: You don’t need a landlord’s permission to alter and improve your home.

5. Home appreciation: Homes generally increase in value, so you can increase your net worth by owning a property.

***

***

Renting also has five significant upsides, particularly for physician retirees who want greater freedom to travel and to make bigger moves — potentially across the country or even abroad:

1. Extreme flexibility: You can leave your property after giving notice and go wherever you want much more easily than with an illiquid home you’d have to sell first.

2. Lower upfront costs: You only have to pay first and last month’s rent and a security deposit to move into a rental, not make a large home down payment.