BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

There are two distinct forms of financial analysis investment strategies often used by medical colleague investors who desire to pursue an active investment strategy.

Technical Analysis: Technical analysts, sometimes referred to as chartists, use historical price data and transaction volume data to identify mis-priced securities. A key belief shared by technical analysts is that stock prices follow recurring patterns and that once these historical patterns are identified, they can be used to identify future security prices. The heart of technical analysis is identifying significant shifts in the macro/micro economic supply and demand factors for a particular securities investment.

Skeptics of technical analysis generally subscribe to the notion that the markets efficiently and accurately price securities. In fact, the weak form of the Efficient Market Hypothesis [EMH] is based on the view that investors cannot consistently earn superior returns using historical data and technical analysis alone.

Fundamental Analysis: In contrast to technical analysis – which relies on historical market returns / transactions data – fundamental analysis focuses on the underlying company’s assets, earnings, risks, dividends and intrinsic security factors to identify mis-priced securities.

Furthermore, investors using fundamental analysis can use either a top-down or bottom-up approach:

The top-down investor starts with global economics, including both international and national economic indicators. These may include GDP growth rates, inflation, interest rates, exchange rates, productivity and energy prices. They subsequently narrow their search to regional / industry analysis of total sales, price levels, the effects of competing products, foreign competition and entry or exit from the industry. Often they refine their search to the best business in the area being studied.

The bottom-up investor starts with specific businesses, regardless of their industry / region, and proceeds in reverse of the top-down approach. Bottom-up investing is an approach that focuses on analyzing individual stocks and de-emphasizes the significance of macroeconomic and market cycles. In other words, bottom-up investing typically involves focusing on a specific company’s fundamentals, such as revenue or earnings, versus the industry or the overall economy. The bottom-up investing approach assumes individual companies can perform well even in an industry that is under performing, at least on a relative basis.

And so, a medical professional utilizing fundamental analysis is attempting to find securities that are trading at market prices below their intrinsic value. Skeptics suggest this is difficult or almost impossible to achieve.

Thus, while technical analysis focuses on market price history, a security’s intrinsic fundamental analysis is determined independent of the security’s market value. Of course, a combination of both fundamental and technical analysis can also be considered.

Check back periodically for practical updates. Our catalogue library of major books, texts, case models and dictionaries is suggested for additional financial, economic, business and medical practice management information and education.

One relatively recent performance evaluation approach that was developed to help improve the relevance of comparisons is the separation of stock universes and managers by style. This classification method attempts to distinguish between stocks or manager philosophies based upon general financial characteristics of the investments.

The Managers

In very general terms, a manager is often a growth manager if the investment approach that the manager uses focuses on stocks showing growth and momentum in its earnings and price.

A value manager is generally considered to be a manager that attempts to identify under-valued securities based upon fundamental analysis of the company. A stock may be considered either “growth” or “value” based on a given set of valuation measures such as price-to-earnings, price-to-book value, and dividend yield.

The Style

The goal of style-based performance comparisons is to take some of the biases of the market environment out of the comparison, since a portfolio’s returns will ideally be evaluated versus a universe of alternatives that represent similar investment characteristics facing the same basic market environment. Thus, if the environment is one in which investors in stocks with strong past earnings and price momentum have generally performed better than those using fundamental analysis to find under-valued stocks, comparing the growth/momentum portfolio to a growth index or universe should help eliminate the bias.

Style-based universes can help the medical professional better understand the basic environment captured over a given performance time period.

However, there are significant limitations with the various approaches to constructing style-based stock and manager universes that should be understood if they are to be used in direct performance comparisons. Taking style-based stock universes separately from style-based manager universe, one of the most significant issues regarding the categorization of stocks by “growth” and “value” styles is the lack of agreement in the specification of what a growth stock is versus a value stock. With some universes divided by price-to-book value, others by price-to-earnings and/or dividend yields and some by combinations of similar variables, stocks are often classified very differently by two different stock universes. Further, stocks move across a broad spectrum as their price and fundamentals change, resulting in stocks constantly moving between growth and value categories for any given universe. If there is ambiguity in the rating of a given stock, then the difficulty is only compounded when we attempt to boil what may be complex investment processes of an investment manager or mutual fund portfolio manager to a simple classification of growth or value. A beaten down cyclical stock that no self-respecting growth/momentum manager would purchase may be classified as “growth” because it has a high price-to-earnings ratio (i.e., from low earnings) or a high price-to-book value (i.e., from asset write-offs). Value managers are not the only ones to own low valuation stocks that have improving earnings.

***

***

The second problem with style categorization is that managers are often misclassified or they purposefully “game” the categorization of their own process in order to appear more competitive. As an example, if a manager that typically looks for relatively strong earnings/price momentum is lagging in a period when “growth” managers are outperforming, the rank of the manager can be improved simply by claiming a “value” approach. Morningstar’s “style box” classification of mutual funds by size and style of the current portfolio highlight this problem for any given fund by showing how their portfolio has changed its classification annually.

Current Events

The stock market has been booming lately. Up almost 100% since March 2009, after being down almost 50%. And so, perhaps this is a good time to re-evaluate the performance of your investment portfolio[s].

Assessment

However, this leads to an interesting question for the medical professional or his/her advisor: If a manager is still using the same basic investment philosophy and disciplines, but their “style” category has changed according to the ratings service, should you fire them? If the answer is “yes”, then the burden of monitoring and the cost of manager turnover are an inevitable part of narrow style based performance comparisons.

But, if the answer is “no,” then it is easy to see the difficulty of fitting every management approach into a simple style box. The more reasonable alternative is to use style-based stock and manager universes as a tool for understanding the environment, rather than an absolute performance benchmark.

Conclusion

And so, your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed: And, credible sponsors and like-minded advertisers are always welcomed.

Modern Portfolio Theory approaches investing by examining the complete market and the full economy. MPT places a great emphasis on the correlation between investments.

DEFINITION:

Correlation is a measure of how frequently one event tends to happen when another event happens. High positive correlation means two events usually happen together – high SAT scores and getting through college for instance. High negative correlation means two events tend not to happen together – high SATs and a poor grade record.

No correlation means the two events are independent of one another. In statistical terms two events that are perfectly correlated have a “correlation coefficient” of 1; two events that are perfectly negatively correlated have a correlation coefficient of -1; and two events that have zero correlation have a coefficient of 0.

Correlation has been used over the past twenty years by institutions and financial advisors to assemble portfolios of moderate risk. In calculating correlation, a statistician would examine the possibility of two events happening together, namely:

If the probability of A happening is 1/X;

And the probability of B happening is 1/Y; then

The probability of A and B happening together is (1/X) times (1/Y), or 1/(X times Y).

There are several laws of correlation including;

Combining assets with a perfect positive correlation offers no reduction in portfolio risk. These two assets will simply move in tandem with each other.

Combining assets with zero correlation (statistically independent) reduces the risk of the portfolio. If more assets with uncorrelated returns are added to the portfolio, significant risk reduction can be achieved.

Combing assets with a perfect negative correlation could eliminate risk entirely. This is the principle with “hedging strategies”. These strategies are discussed later in the book.

In the real world, negative correlations are very rare

Most assets maintain a positive correlation with each other. The goal of a prudent investor is to assemble a portfolio that contains uncorrelated assets. When a portfolio contains assets that possess low correlations, the upward movement of one asset class will help offset the downward movement of another. This is especially important when economic and market conditions change.

As a result, including assets in your portfolio that are not highly correlated will reduce the overall volatility (as measured by standard deviation) and may also increase long-term investment returns. This is the primary argument for including dissimilar asset classes in your portfolio. Keep in mind that this type of diversification does not guarantee you will avoid a loss. It simply minimizes the chance of loss.

In the table provided by Ibbotson, the average correlation between the five major asset classes is displayed. The lowest correlation is between the U.S. Treasury Bonds and the EAFE (international stocks). The highest correlation is between the S&P 500 and the EAFE; 0.77 or 77 percent. This signifies a prominent level of correlation that has grown even larger during this decade. Low correlations within the table appear most with U.S. Treasury Bills.

Posted on April 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson, CFA ***

***

Something weird happened to me on Twitter a few months ago. A “follower” started lashing out at me about a stock we own. When people attack me for my views it doesn’t bother me (I wrote several chapters in Soul in the Game on this topic). I don’t let personal attacks get to me, unless people start attaching bricks to their 280 characters.

This person’s lambasting of me was different. He was upset about the decline of a stock I had never publicly discussed in any of my newsletters or talks. This person was not a client. I didn’t know who he was; I had never met him. I was really confused why a stock my clients and I personally owned was so important to him. It’s like someone being upset about the color my wife chose to paint our kitchen.

Once gently confronted, he apologized, said he was a big fan, and explained that he had read my 13F (a form we have to file with the SEC 45 days after the quarter end, where we have to report our holdings in US stocks). He saw that the stock was one of our top holdings, and he bought it. Because I owned it, he made it a disproportionately large position.

I was truly upset about this incident. One of my principles in life is to have a net positive impact on the people I touch. If every single stock I discussed only went straight up, I wouldn’t have to worry about it. But this is not how life works.

Written by doctors and healthcare professionals, this textbook should be mandatory reading for all medical school students—highly recommended for both young and veteran physicians—and an eliminating factor for any financial advisor who has not read it. The book uses jargon like ‘innovative,’ ‘transformational,’ and ‘disruptive’—all rightly so! It is the type of definitive financial lifestyle planning book we often seek, but seldom find. —LeRoy Howard MA CMPTM,Candidate and Financial Advisor, Fayetteville, North Carolina I taught diagnostic radiology for over a decade. The physician-focused niche information, balanced perspectives, and insider industry transparency in this book may help save your financial life. —Dr. William P. Scherer MS, Barry University, Ft. Lauderdale, Florida This book was crafted in response to the frustration felt by doctors who dealt with top financial, brokerage, and accounting firms. These non-fiduciary behemoths often prescribed costly wholesale solutions that were applicable to all, but customized for few, despite ever-changing needs. It is a must-read to learn why brokerage sales pitches or Internet resources will never replace the knowledge and deep advice of a physician-focused financial advisor, medical consultant, or collegial Certified Medical Planner™ financial professional. —Parin Khotari MBA,Whitman School of Management, Syracuse University, New York In today’s healthcare environment, in order for providers to survive, they need to understand their current and future market trends, finances, operations, and impact of federal and state regulations. As a healthcare consulting professional for over 30 years supporting both the private and public sector, I recommend that providers understand and utilize the wealth of knowledge that is being conveyed in these chapters. Without this guidance providers will have a hard time navigating the supporting system which may impact their future revenue stream. I strongly endorse the contents of this book.—Carol S. Miller BSN MBA PMP,President, Miller Consulting Group, ACT IAC Executive Committee Vice-Chair at-Large, HIMSS NCA Board Member This is an excellent book on financial planning for physicians and health professionals. It is all inclusive yet very easy to read with much valuable information. And, I have been expanding my business knowledge with all of Dr. Marcinko’s prior books. I highly recommend this one, too. It is a fine educational tool for all doctors.—Dr. David B. Lumsden MD MS MA,Orthopedic Surgeon, Baltimore, Maryland There is no other comprehensive book like it to help doctors, nurses, and other medical providers accumulate and preserve the wealth that their years of education and hard work have earned them. —Dr. Jason Dyken MD MBA,Dyken Wealth Strategies, Gulf Shores, Alabama I plan to give a copy of this book written ‘by doctors and for doctors’ to all my prospects, physician, and nurse clients. It may be the definitive text on this important topic. —Alexander Naruska CPA,Orlando, Florida

Health professionals are small business owners who need to apply their self-discipline tactics in establishing and operating successful practices. Talented trainees are leaving the medical profession because they fail to balance the cost of attendance against a realistic business and financial plan. Principles like budgeting, saving, and living below one’s means, in order to make future investments for future growth, asset protection, and retirement possible are often lacking. This textbook guides the medical professional in his/her financial planning life journey from start to finish. It ranks a place in all medical school libraries and on each of our bookshelves. —Dr. Thomas M. DeLauro DPM,Professor and Chairman – Division of Medical Sciences, New York College of Podiatric Medicine

Physicians are notoriously excellent at diagnosing and treating medical conditions. However, they are also notoriously deficient in managing the business aspects of their medical practices. Most will earn $20-30 million in their medical lifetime, but few know how to create wealth for themselves and their families. This book will help fill the void in physicians’ financial education. I have two recommendations: 1) every physician, young and old, should read this book; and 2) read it a second time! —Dr. Neil Baum MD,Clinical Associate Professor of Urology, Tulane Medical School, New Orleans, Louisiana

I worked with a Certified Medical Planner™ on several occasions in the past, and will do so again in the future. This book codified the vast body of knowledge that helped in all facets of my financial life and professional medical practice. —Dr. James E. Williams DABPS, Foot and Ankle Surgeon, Conyers, Georgia

This is a constantly changing field for rules, regulations, taxes, insurance, compliance, and investments. This book assists readers, and their financial advisors, in keeping up with what’s going on in the healthcare field that all doctors need to know. —Patricia Raskob CFP® EA ATA, Raskob Kambourian Financial Advisors, Tucson, Arizona I particularly enjoyed reading the specific examples in this book which pointed out the perils of risk … something with which I am too familiar and have learned (the hard way) to avoid like the Black Death. It is a pleasure to come across this kind of wisdom, in print, that other colleagues may learn before it’s too late— many, many years down the road. —Dr. Robert S. Park MD, Robert Park and Associates Insurance, Seattle, Washington

Although this book targets physicians, I was pleased to see that it also addressed the financial planning and employment benefit needs of nurses; physical, respiratory, and occupational therapists; CRNAs, hospitalists, and other members of the health care team….highly readable, practical, and understandable. —Nurse Cecelia T. Perez RN, Hospital Operating Room Manager, Ellicott City, Maryland

Personal financial success in the PP-ACA era will be more difficult to achieve than ever before. It requires the next generation of doctors to rethink frugality, delay gratification, and redefine the very definition of success and work–life balance. And, they will surely need the subject matter medical specificity and new-wave professional guidance offered in this book. This book is a ‘must-read’ for all health care professionals, and their financial advisors, who wish to take an active role in creating a new subset of informed and pioneering professionals known as Certified Medical Planners™. —Dr. Mark D. Dollard FACFAS, Private Practice, Tyson Corner, Virginia As healthcare professionals, it is our Hippocratic duty to avoid preventable harm by paying attention. On the other hand, some of us are guilty of being reckless with our own financial health—delaying serious consideration of investments, taxation, retirement income, estate planning, and inheritances until the worry keeps one awake at night. So, if you have avoided planning for the future for far too long, perhaps it is time to take that first step toward preparedness. This in-depth textbook is an excellent starting point—not only because of its readability, but because of his team’s expertise and thoroughness in addressing the intricacies of modern investments—and from the point of view of not only gifted financial experts, but as healthcare providers, as well … a rare combination. —Dr. Darrell K. Pruitt DDS, Private Practice Dentist, Fort Worth, Texas This text should be on the bookshelf of all contemporary physicians. The book is physician-focused with unique topics applicable to all medical professionals. But, it also offers helpful insights into the new tax and estate laws, fiduciary accountability for advisors and insurance agents, with investing, asset protection and risk management, and retirement planning strategies with updates for the brave new world of global payments of the Patient Protection and Affordable Care Act. Starting out by encouraging readers to examine their personal ‘money blueprint’ beliefs and habits, the book is divided into four sections offering holistic life cycle financial information and economic education directed to new, mid-career, and mature physicians.

This structure permits one to dip into the book based on personal need to find relief, rather than to overwhelm. Given the complexity of modern domestic healthcare, and the daunting challenges faced by physicians who try to stay abreast of clinical medicine and the ever-evolving laws of personal finance, this textbook could not have come at a better time. —Dr. Philippa Kennealy MD MPH, The Entrepreneurial MD, Los Angeles, California Physicians have economic concerns unmatched by any other profession, arriving ten years late to the start of their earning years. This textbook goes to the core of how to level the playing field quickly, and efficaciously, by a new breed of dedicated Certified Medical Planners™. With physician-focused financial advice, each chapter is a building block to your financial fortress. —Thomas McKeon, MBA, Pharmaceutical Representative, Philadelphia, Pennsylvania An excellent resource … this textbook is written in a manner that provides physician practice owners with a comprehensive guide to financial planning and related topics for their professional practice in a way that is easily comprehended. The style in which it breaks down the intricacies of the current physician practice landscape makes it a ‘must-read’ for those physicians (and their advisors) practicing in the volatile era of healthcare reform. —Robert James Cimasi, MHA ASA FRICS MCBA CVA CM&AA CMP™, CEO-Health Capital Consultants, LLC, St. Louis, Missouri Rarely can one find a full compendium of information within a single source or text, but this book communicates the new financial realities we are forced to confront; it is full of opportunities for minimizing tax liability and maximizing income potential. We’re recommending it to all our medical practice management clients across the entire healthcare spectrum. —Alan Guinn, The Guinn Consultancy Group, Inc., Cookeville, Tennessee Dr. David Edward Marcinko MBA CMP™ and his team take a seemingly endless stream of disparate concepts and integrate them into a simple, straightforward, and understandable path to success. And, he codifies them all into a step-by-step algorithm to more efficient investing, risk management, taxation, and enhanced retirement planning for doctors and nurses. His text is a vital read—and must execute—book for all healthcare professionals and physician-focused financial advisors. —Dr. O. Kent Mercado, JD, Private Practitioner and Attorney, Naperville, Illinois

Kudos. The editors and contributing authors have compiled the most comprehensive reference book for the medical community that has ever been attempted. As you review the chapters of interest and hone in on the most important concerns you may have, realize that the best minds have been harvested for you to plan well… Live well. —Martha J. Schilling; AAMS® CRPC® ETSC CSA, Shilling Group Advisors, LLC, Philadelphia, Pennsylvania I recommend this book to any physician or medical professional that desires an honest no-sales approach to understanding the financial planning and investing world. It is worthwhile to any financial advisor interested in this space, as well. —David K. Luke, MIM MS-PFP CMP™, Net Worth Advisory Group, Sandy, Utah Although not a substitute for a formal business education, this book will help physicians navigate effectively through the hurdles of day-to-day financial decisions with the help of an accountant, financial and legal advisor. I highly recommend it and commend Dr. Marcinko and the Institute of Medical Business Advisors, Inc. on a job well done. —Ken Yeung MBA CMP™, Tseung Kwan O Hospital, Hong Kong I’ve seen many ghost-written handbooks, paperbacks, and vanity-published manuals on this topic throughout my career in mental healthcare. Most were poorly written, opinionated, and cheaply produced self-aggrandizing marketing drivel for those agents selling commission-based financial products and expensive advisory services. So, I was pleasantly surprised with this comprehensive peer-reviewed academic textbook, complete with citations, case examples, and real-life integrated strategies by and for medical professionals. Although a bit late for my career, I recommend it highly to all my younger colleagues … It’s credibility and specificity stand alone. —Dr. Clarice Montgomery PhD MA,Retired Clinical Psychologist In an industry known for one-size-fits-all templates and massively customized books, products, advice, and services, the extreme healthcare specificity of this text is both refreshing and comprehensive. —Dr. James Joseph Bartley, Columbus, Georgia

My brother was my office administrator and accountant. We both feel this is the most comprehensive textbook available on financial planning for healthcare providers. —Dr. Anthony Robert Naruska DC,Winter Park, Florida

Posted on March 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

You don’t have to worry about the market and its crazy valuations. That’s your neighbor’s problem, not yours. In building your portfolio, we are aiming for resilience.

About twelve years ago the South Dakota Investment Council combined two of their asset classes, domestic and international stocks, into one, global stocks. While this move didn’t make the nightly news, it did signify a growing trend.

Many investment managers no longer view the US stock market as a separate asset class from the rest of the world’s stock markets.

Today they view it as one component of a global asset class of stocks.

Diversify

For the same reason you don’t want to own just one company’s stock in your portfolio, it makes no sense for an individual investing for retirement to own just US stocks. It’s as important to diversify among countries as among companies.

The question then becomes how much of a global stock portfolio should be in US stocks and how much in international stocks. For many years the standard thinking of portfolio managers was still to over-allocate to the US. It was, and to some degree still is, common to see 80% of a portfolio’s equity allocation in US stocks.

That over-allocation has never made a lot of sense to me, considering that the US accounts for far less than 80% of the global market capitalization. In the 1980’s, US companies accounted for about 65% of the global capitalization. Accordingly, I weighted my stock portfolios with 65% US and 35% international. By 1999, the US had slipped to 50%. I adjusted my portfolios accordingly.

The latest statistics from Dimensional Fund Advisors show the US still accounts for around 50% of the global capitalization. Investors who want to maintain a true global diversification of their stock portfolios will need to seriously consider reducing their US allocation.

***

***

Which, Where and How to Invest

Which international stocks, then, should you add? Developed regions and countries like those of Europe, Australia Pacific, and Japan account for about 40% of the total global capitalization. Emerging market countries, many in Southwest Asia and Latin America, make up the remaining 10%. Weighting your portfolio accordingly gives you a well-diversified stock portfolio that has a high probability of withstanding the inevitable rise and fall of equity markets.

How do you invest globally? There are mutual funds that invest in specific countries, in regions, internationally, or globally. I don’t really like the country funds, as I don’t know which countries I should be underweighting or overweighting. Besides, creating a global index using country funds can be a lot of work and expense.

Using index regional funds is an easier way to invest in international stocks. To allocate according to the global capitalization percentages above, you would include three index mutual funds in your stock portfolio: one broad market US fund, an international fund of developed (non-emerging markets), and an emerging markets fund.

If you want even more simplicity, invest in one good global fund. The difference between an “international” fund and a “global” or “world” fund is that a global fund will include US stocks where an international fund won’t. Vanguard Total World Stock ETF comes to mind as one of the better “one size fits all” global funds that will invest in a mixture of countries, including the US. This one fund holds 7,164 stocks in 47 countries. You really need nothing more in the equity portion of your portfolio.

Assessment

While it isn’t necessary to allocate your stocks strictly according to global capitalization percentages, research suggest you will probably do better in the long run to do so. Whether you decide to own country, regional, international, or global funds, what’s most important is that you diversify your stock portfolio globally. In today’s world, it’s an important component of diversified investing.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Written by doctors and healthcare professionals, this textbook should be mandatory reading for all medical school students—highly recommended for both young and veteran physicians—and an eliminating factor for any financial advisor who has not read it. The book uses jargon like ‘innovative,’ ‘transformational,’ and ‘disruptive’—all rightly so! It is the type of definitive financial lifestyle planning book we often seek, but seldom find.

LeRoy Howard MA CMPTM [Candidate and Financial Advisor, Fayetteville, North Carolina]

The giant accounting firm Grant Thornton LLP is laying off 200 people, its second round of layoffs in the past six months and an indication that the major players in the professional consulting, accounting and advisory business are preparing for an economic slowdown that could squeeze profits across corporate America.

***

Statistics: 7.4%. That’s the percentage drop in students who graduated with a degree in accounting in the 2021–2022 school year than the year before. Low starting salaries, heavy workloads, and uncertainty around AI are driving the exodus of students from choosing accounting degrees. (the Wall Street Journal).

Posted on February 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A stock buyback is when a public company uses cash to buy shares of its own stock on the open market. A company may do this to return money to shareholders that it doesn’t need to fund operations and other investments

Share buybacks can create value for investors in a few ways: Repurchases return cash to shareholders who want to exit the investment. With a buyback, the company can increase earnings per share, all else equal. The same earnings pie cut into fewer slices is worth a greater share of the earnings.

A stock buyback typically means that the price of the remaining outstanding shares increases. This is simple supply-and-demand economics: there are fewer outstanding shares, but the value of the company has not changed, therefore each share is worth more, so the price goes up.

But, the practice has faced criticism from labor unions, the SEC, and even President Biden, who proposed stricter stock buyback regulations for company execs last week.

Nevertheless,

Stock buybacks from S&P 500 companies are expected to pass $1 trillion this year, after hitting a record $882 billion in 2021, according to Goldman Sachs.

In recent years, Starbucks spent $13.5 billion repurchasing shares.

Do you ever wish you could acquire specific information for your career activities without having to complete a university Master’s Degree or finish our entire Certified Medical Planner™ professional designation program? Well, Micro-Certifications from the Institute of Medical Business Advisors, Inc., might be the answer. Read on to learn how our three Micro-Certifications offer new opportunities for professional growth in the medical practice, business management, health economics and financial planning, investing and advisory space for physicians, nurses and healthcare professionals.

Micro-Certification Basics

Stock-Brokers, Financial Advisors, Investment Advisors, Accountants, Consultants, Financial Analyists and Financial Planners need to enhance their knowledge skills to better serve the changing and challenging healthcare professional ecosystem. But, it can be difficult to learn and demonstrate mastery of these new skills to employers, clients, physicians or medical prospects. This makes professional advancement difficult. That’s where Micro-Certification and Micro-Credentialing enters the online educational space. It is the process of earning a Micro-Certification, which is like a mini-degree or mini-credential, in a very specific topical area.

Micro-Certification Requirements

Once you’ve completed all of the requirements for our Micro-Certification, you will be awarded proof that you’ve earned it. This might take the form of a paper or digital certificate, which may be a hard document or electronic image, transcript, file, or other official evidence that you’ve completed the necessary work.

Uses of Micro-Certifications

Micro-Certifications may be used to demonstrate to physicians prospective medical clients that you’ve mastered a certain knowledge set. Because of this, Micro-Certifications are useful for those financial service professionals seeking medical clients, employment or career advancement opportunities.

Examples of iMBA, Inc., Micro-Certifications

Here are the three most popular Micro-Certification course from the Institute of Medical Business Advisors, Inc:

1. Health Insurance and Managed Care: To keep up with the ever-changing field of health care physician advice, you must learn new medical practice business models in order to attract and assist physicians and nurse clients. By bringing together the most up-to-date business and medical prctice models [Medicare, Medicaid, PP-ACA, POSs, EPOs, HMOs, PPOs, IPA’s, PPMCs, Accountable Care Organizations, Concierge Medicine, Value Based Care, Physician Pay-for-Performance Initiatives, Hospitalists, Retail and Whole-Sale Medicine, Health Savings Accounts and Medical Unions, etc], this iMBA Inc., Mini-Certification offers a wealth of essential information that will help you understand the ever-changing practices in the next generation of health insurance and managed medical care.

2. Health Economics and Finance: Medical economics, finance, managerial and cost accounting is an integral component of the health care industrial complex. It is broad-based and covers many other industries: insurance, mathematics and statistics, public and population health, provider recruitment and retention, health policy, forecasting, aging and long-term care, and Venture Capital are all commingled arenas. It is essential knowledge that all financial services professionals seeking to serve in the healthcare advisory niche space should possess.

3. Health Information Technology and Security: There is a myth that all physician focused financial advisors understand Health Information Technology [HIT]. In truth, it is often economically misused or financially misunderstood. Moreover, an emerging national HIT architecture often puts the financial advisor or financial planner in a position of maximum uncertainty and minimum productivity regarding issues like: Electronic Medical Records [EMRs] or Electronic Health Records [EHRs], mobile health, tele-health or tele-medicine, Artificial Intelligence [AI], benefits managers and human resource professionals.

Other Topics include: economics, finance, investing, marketing, advertising, sales, start-ups, business plan creation, financial planning and entrepreneurship, etc.

How to Start Learning and Earning Recognition for Your Knowledge

Now that you’re familiar with Micro-Credentialing, you might consider earning a Micro-Certification with us. We offer 3 official Micro-Certificates by completing a one month online course, with a live instructor consisting of twelve asynchronous lessons/online classes [3/wk X 4/weeks = 12 classes]. The earned official completion certificate can be used to demonstrate mastery of a specific skill set and shared with current or future employers, current clients or medical niche financial advisory prospects.

Mini-Certification Tuition, Books and Related Fees

The tuition for each Mini-Certification live online course is $1,250 with the purchase of one required dictionary handbook. Other additional guides, white-papers, videos, files and e-content are all supplied without charge. Alternative courses may be developed in the future subject to demand and may change without notice.

***

Contact: For more information, or to speak with an academic representative, please contact Ann Miller RN MHA CMP™ at: MarcinkoAdvisors@msn.com [24/7] -OR- 770-448-0769[9:00 – 5:00 EST].

Posted on December 5, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

DEFINITION: Income is the money you receive in exchange for your labor or products. Income may have different definitions depending on the context—for example, taxation, financial accounting, or economic analysis. For most people, income is their total earnings in the form of wages and salaries, the return on their investments, pension distributions, and other receipts. For businesses, income is the revenue from selling services, products, and any interest and dividends received with respect to their cash accounts and reserves related to the business. Economists have different definitions of income and different ways of measuring it, from focusing on earnings, savings, consumption, production, public finance, capital investment or other topics … Maybe?

WASHINGTON (Reuters) – The U.S. Supreme Court is set on Tuesday to consider a challenge to the legality of a tax targeting owners of foreign corporations that could undermine efforts at imposing a wealth tax on the very rich in a case that has already sparked controversy over a call for Justice Samuel Alito to recuse.

The justices are due to hear arguments in an appeal by Charles and Kathleen Moore – a retired couple from Redmond, Washington couple – of a lower court’s decision rejecting their challenge to the tax on foreign company earnings, even though those profits had not been distributed.

The one-time “mandatory repatriation tax” (MRT), which applied to taxpayers owning at least 10% of certain foreign corporations, was part of a 2017 Republican-backed tax bill signed into law by former President Donald Trump.

At issue in the case is whether this levy on unrealized gains is allowed under the U.S. Constitution’s 16th Amendment, which enabled Congress to “collect taxes on incomes.” The Moores, backed by the Competitive Enterprise Institute and other conservative and business groups, contend that “income” means only those gains that are realized through payment to the taxpayer, not a mere increase in the value of property.

Posted on November 14, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

DEFINITION: In the USA shutdowns occur when funding legislation required to finance the Federal Government is not enacted before the next fiscal year begins. In a shutdown, the federal government curtails agency activities and services, ceases non-essential operations, furloughs non-essential workers, and retains only essential employees in departments that protect human life or property. Shutdowns can also disrupt state, territory and local levels of government.

Fortunately, prices held steady for consumers and are growing at a slower pace, the U.S. government just reported Tuesday morning, as overall prices in October were the same as what consumers paid in September.

The Bureau of Labor Statistics says prices in October were unchanged as gasoline prices declined and shelter costs continued to rise. The Consumer Price Index rose 3.2% compared to a year ago, the latest sign that inflation is slowing down as interest rates rise and the job market gives up some of its recent strength.

And, the stock markets rocked upward as Presidents Biden and Xi meet in San Francisco and Congress counts down toward a possible government shutdown. As stocks were a mixed bag yesterday as investors kept their eyes trained on Washington for the latest inflation good news data and to see whether lawmakers can hammer out a budget deal to keep the government from shutting down on Friday.

Yet, Boeing stock took off following reports that China may soon end its freeze on the 737 Max, as well as the announcement of several deals for new aircraft, including Emirates’s $52 billion order for 95 planes.

Do you ever wish you could acquire specific information for your career activities without having to complete a university Master’s Degree or finish our entire Certified Medical Planner™ professional designation program? Well, Micro-Certifications from the Institute of Medical Business Advisors, Inc., might be the answer. Read on to learn how our three Micro-Certifications offer new opportunities for professional growth in the medical practice, business management, health economics and financial planning, investing and advisory space for physicians, nurses and healthcare professionals.

Micro-Certification Basics

Stock-Brokers, Financial Advisors, Investment Advisors, Accountants, Consultants, Financial Analyists and Financial Planners need to enhance their knowledge skills to better serve the changing and challenging healthcare professional ecosystem. But, it can be difficult to learn and demonstrate mastery of these new skills to employers, clients, physicians or medical prospects. This makes professional advancement difficult. That’s where Micro-Certification and Micro-Credentialing enters the online educational space. It is the process of earning a Micro-Certification, which is like a mini-degree or mini-credential, in a very specific topical area.

Micro-Certification Requirements

Once you’ve completed all of the requirements for our Micro-Certification, you will be awarded proof that you’ve earned it. This might take the form of a paper or digital certificate, which may be a hard document or electronic image, transcript, file, or other official evidence that you’ve completed the necessary work.

Uses of Micro-Certifications

Micro-Certifications may be used to demonstrate to physicians prospective medical clients that you’ve mastered a certain knowledge set. Because of this, Micro-Certifications are useful for those financial service professionals seeking medical clients, employment or career advancement opportunities.

Examples of iMBA, Inc., Micro-Certifications

Here are the three most popular Micro-Certification course from the Institute of Medical Business Advisors, Inc:

1. Health Insurance and Managed Care: To keep up with the ever-changing field of health care physician advice, you must learn new medical practice business models in order to attract and assist physicians and nurse clients. By bringing together the most up-to-date business and medical prctice models [Medicare, Medicaid, PP-ACA, POSs, EPOs, HMOs, PPOs, IPA’s, PPMCs, Accountable Care Organizations, Concierge Medicine, Value Based Care, Physician Pay-for-Performance Initiatives, Hospitalists, Retail and Whole-Sale Medicine, Health Savings Accounts and Medical Unions, etc], this iMBA Inc., Mini-Certification offers a wealth of essential information that will help you understand the ever-changing practices in the next generation of health insurance and managed medical care.

2. Health Economics and Finance: Medical economics, finance, managerial and cost accounting is an integral component of the health care industrial complex. It is broad-based and covers many other industries: insurance, mathematics and statistics, public and population health, provider recruitment and retention, health policy, forecasting, aging and long-term care, and Venture Capital are all commingled arenas. It is essential knowledge that all financial services professionals seeking to serve in the healthcare advisory niche space should possess.

3. Health Information Technology and Security: There is a myth that all physician focused financial advisors understand Health Information Technology [HIT]. In truth, it is often economically misused or financially misunderstood. Moreover, an emerging national HIT architecture often puts the financial advisor or financial planner in a position of maximum uncertainty and minimum productivity regarding issues like: Electronic Medical Records [EMRs] or Electronic Health Records [EHRs], mobile health, tele-health or tele-medicine, Artificial Intelligence [AI], benefits managers and human resource professionals.

Other Topics include: economics, finance, investing, marketing, advertising, sales, start-ups, business plan creation, financial planning and entrepreneurship, etc.

How to Start Learning and Earning Recognition for Your Knowledge

Now that you’re familiar with Micro-Credentialing, you might consider earning a Micro-Certification with us. We offer 3 official Micro-Certificates by completing a one month online course, with a live instructor consisting of twelve asynchronous lessons/online classes [3/wk X 4/weeks = 12 classes]. The earned official completion certificate can be used to demonstrate mastery of a specific skill set and shared with current or future employers, current clients or medical niche financial advisory prospects.

Mini-Certification Tuition, Books and Related Fees

The tuition for each Mini-Certification live online course is $1,250 with the purchase of one required dictionary handbook. Other additional guides, white-papers, videos, files and e-content are all supplied without charge. Alternative courses may be developed in the future subject to demand and may change without notice.

***

Contact: For more information, or to speak with an academic representative, please contact Ann Miller RN MHA CMP™ at: MarcinkoAdvisors@msn.com [24/7] -OR- 770-448-0769[9:00 – 5:00 EST].

John English, of the Ford Foundation, once observed that:

[T]he thing that is most interesting to me is that every one of the managers is able to give me a chart that shows me he was in the first quartile or the first decile. I have never had a prospective manager come in and say, ‘We’re in the fourth quartile or bottom decile’.

According to Wayne Firebaugh CPA, CFP® CMP™ most medical endowment funds today, even those with internal investment staff, rely heavily upon consultants and external managers.

In fact, a 2006 Commonfund Benchmarks Healthcare Study revealed that 85% of all surveyed institutions relied upon consultants with an even greater percentage of larger endowments relying upon consultants. The common reasons given by endowments for such reliance are augmenting staff and oddly enough, cost containment. In essence, the endowment staff’s job becomes one of managing the managers.

Manager Selection

Even those endowments that use consultants to assist in selecting outside managers remain involved in the selection and monitoring process. Interestingly, performance should generally not be the overriding criterion for selecting a manager. Selecting a manager could be viewed as a two-step process in which the endowment first establishes its initial allocation and determines what classes will require an external manager. The second part of the process is to select a manager that due diligence has indicated to have two primary characteristics: integrity and a repeatable and sustainable systematic process. These characteristics are interrelated, as a manager who embodies integrity will also strive to follow the established investment selection process.

Of Medical-Managers

In medicine, obtaining the best care often means consulting a specialist. As a manager of managers, the average endowment should seek specialist managers within a given asset class. Just as physicians and healthcare institutions gain additional insight and skill in their area of specialty, investment managers may be able to gain informational or system advantages within a given concentrated area of investments.

Assessment

Since most plan managers are seeking positive alpha by actively managing certain asset classes, many successful endowments will use a greater number of external managers in the concentrated segments than they will in the larger, more efficient markets.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Several years ago a group of highly trusted and deeply experienced financial services professionals and estate planners noted that far too many of their mature physician clients, using traditional stock brokers, management consultants and financial advisors, seemed to be less successful than those who went it alone. These Do-it-Yourselfers [DIYs] had setbacks and made mistakes, for sure. But, the ME Inc doctors seemed to learn from their mistakes and did not incur the high management and service fees demanded from general or retail one-size-fits-all “advisors.”

In fact, an informal inverse relationship was noted, and dubbed the “Doctor Effect.” In others words, the more consultants an individual doctor retained; the less well they did in all disciplines of the financial planning and medical practice management, continuum.

Of course, the reason for this discrepancy eluded many of them as Wall Street brokerages and wire-houses flooded the media with messages, infomercials, print, radio, TV, texts, tweets, and internet ads to the contrary. Rather than self-learn the basics, the prevailing sentiment seemed to purse the holy grail of finding the “perfect financial advisor.” This realization was a confirmation of the industry culture which seemed to be: Bread for the advisor – Crumbs for the client!

And so, at D.E. Marcinko & Associates, our informed cadre’ of technology focused and highly educated doctors, nurses, financial advisors, attorneys, accountants, psychologists and educational visionaries decided there must be a better way for healthcare colleagues to receive financial planning advice, products and related management services within a culture of fiduciary responsibility.

We trust you agree with this ME Inc, and Certified Medical Planner™ consulting philosophy, as illustrated on our website.

Did you know that at MARCINKO & Associates, all medical colleagues throughout the United States may contact us when they are considering the sale, purchase, strategic operating improvement, merger, acquisition and/or other financial business or related personal financial planning transaction?

Our difference is “hard” knowledge and insider financial guidance that helps medical colleagues, nurses, private practitioners, clinics, ambulatory surgery, radiology and outpatient wound care centers realize their ultimate economic goals. This typically includes managerial and cost accounting, financial ratio analysis, fair market valuation business appraisals, business plan creation and personal financial planning.

Our “expert witness” business litigation support service and divorce mediation, arbitration, asset division, settlement and second opinion offerings are always available, as well.

And, our “soft” skill professional career guidance and mentoring center includes executive coaching, consulting and mentoring advisory programs for stressed, conflicted or burned-out physicians and medical practitioners.

Most importantly, our professional fees are reasonable and always transparent.

MARCINKO & Associates also serves universities, medical, business, graduate and nursing schools; physicians, dentists, podiatrists, optometrists and legal societies. This includes accountants, financial service providers, wealth and hedge fund managers, emerging entities, hospitals, CEOs and their BODs, the press, media and related organizations.

Did you know that at MARCINKO & Associates, all medical colleagues throughout the United States may contact us when they are considering the sale, purchase, strategic operating improvement, merger, acquisition and/or other financial business or related personal financial planning transaction?

Our difference is “hard” knowledge and insider financial guidance that helps medical colleagues, nurses, private practitioners, clinics, ambulatory surgery, radiology and outpatient wound care centers realize their ultimate economic goals. This typically includes managerial and cost accounting, financial ratio analysis, fair market valuation business appraisals, business plan creation and personal financial planning.

Our “expert witness” business litigation support service and divorce mediation, arbitration, asset division, settlement and second opinion offerings are always available, as well.

And, our “soft” skill professional career guidance and mentoring center includes executive coaching, consulting and mentoring advisory programs for stressed, conflicted or burned-out physicians and medical practitioners.

Most importantly, our professional fees are reasonable and always transparent.

MARCINKO & Associates also serves universities, medical, business, graduate and nursing schools; physicians, dentists, podiatrists, optometrists and legal societies. This includes accountants, financial service providers, wealth and hedge fund managers, emerging entities, hospitals, CEOs and their BODs, the press, media and related organizations.

Posted on August 27, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Jerome Powell: Speaking at the Jackson Hole Symposium, an annual meeting of central bankers from around the globe at a former Wild West outpost, the FOMC chair said inflation “remains too high” and “we are prepared to raise rates further if appropriate” and to keep them high. So, why didn’t the stock market nose-dive like it did after last year’s similarly hawkish Powell speech? It helps that inflation has come down considerably since then (which Powell acknowledged) and that he nodded to the dangers of the Fed doing too much as well as too little.

***

Rite Aid is preparing to file for bankruptcy in the face of costly lawsuits over its sales of opioids, the Wall Street Journal reports.

Wegovy, the weight-loss drug, also helps prevent heart failure, its maker, Novo Nordisk, said after a clinical trial.

Wells Fargoagreed to pay $35 million to settle the SEC’s claims that it overcharged fees on nearly 11,000 investment advisory accounts—claims it neither admits nor denies.

Posted on August 13, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Markets: The NASDAQ is fading and closing lower for the second straight week for the first time all year.

Semiconductor stocks dragged the index down, but investors were also a bit fidgety over an inflation report that showed producer prices grew faster than expected last month.

Posted on July 3, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Investors are coming out of the mid-year investing season enthused and thanks to an Artificial Intelligence fueled stock market rally that turned into an everything rally.

The NASDAQ posted its best H1 since 1983, and the S&P 500 had its best first-half performance since 2019.

But, don’t expect Wall Street fireworks for the next few days. The US stock market will close early today and shut down tomorrow for Independence Day.

Modern Portfolio Theory approaches investing by examining the complete market and the full economy. MPT places a great emphasis on the correlation between investments.

DEFINITION:

Correlation is a measure of how frequently one event tends to happen when another event happens. High positive correlation means two events usually happen together – high SAT scores and getting through college for instance. High negative correlation means two events tend not to happen together – high SATs and a poor grade record.

No correlation means the two events are independent of one another. In statistical terms two events that are perfectly correlated have a “correlation coefficient” of 1; two events that are perfectly negatively correlated have a correlation coefficient of -1; and two events that have zero correlation have a coefficient of 0.

Correlation has been used over the past twenty years by institutions and financial advisors to assemble portfolios of moderate risk. In calculating correlation, a statistician would examine the possibility of two events happening together, namely:

If the probability of A happening is 1/X;

And the probability of B happening is 1/Y; then

The probability of A and B happening together is (1/X) times (1/Y), or 1/(X times Y).

There are several laws of correlation including;

Combining assets with a perfect positive correlation offers no reduction in portfolio risk. These two assets will simply move in tandem with each other.

Combining assets with zero correlation (statistically independent) reduces the risk of the portfolio. If more assets with uncorrelated returns are added to the portfolio, significant risk reduction can be achieved.

Combing assets with a perfect negative correlation could eliminate risk entirely. This is the principle with “hedging strategies”. These strategies are discussed later in the book.

In the real world, negative correlations are very rare

Most assets maintain a positive correlation with each other. The goal of a prudent investor is to assemble a portfolio that contains uncorrelated assets. When a portfolio contains assets that possess low correlations, the upward movement of one asset class will help offset the downward movement of another. This is especially important when economic and market conditions change.

As a result, including assets in your portfolio that are not highly correlated will reduce the overall volatility (as measured by standard deviation) and may also increase long-term investment returns. This is the primary argument for including dissimilar asset classes in your portfolio. Keep in mind that this type of diversification does not guarantee you will avoid a loss. It simply minimizes the chance of loss.

In the table provided by Ibbotson, the average correlation between the five major asset classes is displayed. The lowest correlation is between the U.S. Treasury Bonds and the EAFE (international stocks). The highest correlation is between the S&P 500 and the EAFE; 0.77 or 77 percent. This signifies a prominent level of correlation that has grown even larger during this decade. Low correlations within the table appear most with U.S. Treasury Bills.

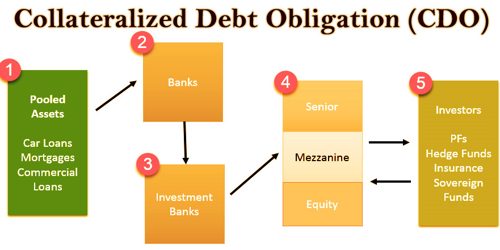

A collateralized debt obligation (CDO) is a type of structured asset-backed security (ABS). Originally developed as instruments for the corporate debt markets, after 2002 CDOs became vehicles for refinancing mortgage-backed securities (MBS).

Like other private label securities backed by assets, a CDO can be thought of as a promise to pay investors in a prescribed sequence, based on the cash flow the CDO collects from the pool of bonds or other assets it owns. Distinctively, CDO credit risk is typically assessed based on a probability of default (PD) derived from ratings on those bonds or assets.

A CMO is a debt security backed by mortgages. These mortgage pools are usually separated into different maturity classes called tranches (from the French word for “slice”). The securities were issued by private issuers, as well as the Federal Home Loan Mortgage Corporation (Freddie Mac). As the mortgages were usually government-guaranteed, CMOs usually carried AAA ratings until their current financial meltdown. The early versions of CMOs were known as “plain vanilla,” but recent developments gave us PACs (planned amortization certificates) and TACs (targeted amortization certificates); among too many others. They were all variations on how principal repayments in advance of maturity date were treated.

Posted on April 11, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Starwood Capital CEO Barry Sternlicht, who has a net worth of $4.6 billion, says inflation is going to drop—and it’s going to drop hard. In an interview with CNBC’s Squawk Box, Sternlicht was asked what he’d say in response to JPMorgan Chase CEO Jamie Dimon’s annual letter to shareholders, in which Dimon writes that current economic conditions “create more risk and potentially higher inflation,” and higher rate hikes.

However, after saying he’s a big fan of Dimon and that he runs “probably one of the best banks in the world,” Sternlicht clarified to CNBC that “we don’t agree on everything.”

The following is a round-up of yesterday’s market activity:

The S&P 500® Index was up 4.09 (0.1%) at 4109.11; the Dow Jones industrial average was up 101.23 (0.3%) at 33,586.52; the NASDAQ Composite was down 3.6 at 12,084.36.

The 10-year Treasury yield was up about 4 basis points at 3.419%.

CBOEs Volatility Index was up 0.54 at 18.94.

Energy and transportation were the strongest-performing S&P 500 sectors, while communications services was the biggest laggard. WTI crude oil futures fell slightly but remained near two-month highs posted last week.

Gold futures fell sharply for the second session in a row. The U.S. dollar index jumped to its strongest level in nearly two weeks.

Posted on April 10, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

Types & Definitions

****

Financial Investing risk is any of various types of risk associated with financing, including financial transactions that include company loans in risk of default. Often it is understood to include only downside risk, meaning the potential for financial loss and uncertainty about its extent.

Although broad investing risks can be quickly summarized as “the failure to achieve spending and inflation-adjusted growth goals,” individual assets may face any number of other subsidiary risks:

Call risk – The risk, faced by a holder of a callable bond that a bond issuer will take advantage of the callable bond feature and redeem the issue prior to maturity. This means the bondholder will receive payment on the value of the bond and, in most cases, will be reinvesting in a less favorable environment (one with a lower interest rate)

Capital risk – The risk an investor faces that he or she may lose all or part of the principal amount invested.

Commodity risk – The threat that a change in the price of a production input will adversely impact a producer who uses that input.

Company risk – The risk that certain factors affecting a specific company may cause its stock to change in price in a different way from stocks as a whole.

Concentration risk – Probability of loss arising from heavily lopsided exposure to a particular group of counterparties

Counterparty risk – The risk that the other party to an agreement will default.

Credit risk – The risk of loss of principal or loss of a financial reward stemming from a borrower’s failure to repay a loan or otherwise meet a contractual obligation.

Currency risk – A form of risk that arises from the change in price of one currency against another.

Deflation risk – A general decline in prices, often caused by a reduction in the supply of money or credit.

Economic risk – the likelihood that an investment will be affected by macroeconomic conditions such as government regulation, exchange rates, or political stability.

Hedging risk – Making an investment to reduce the risk of adverse price movements in an asset.

Inflation risk – The uncertainty over the future real value (after inflation) of your investment.

Interest rate risk – Risk to the earnings or market value of a portfolio due to uncertain future interest rates.

Legal risk – risk from uncertainty due to legal actions or uncertainty in the applicability or interpretation of contracts, laws or regulations.

Liquidity risk – The risks stemming from the lack of marketability of an investment that cannot be bought or sold quickly enough to prevent or minimize a loss.

Posted on April 2, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

All about the Medical Executive-PostBusiness Model

***

One of the questions we receive most often from readers of the Medical Executive-Post is how can we “afford” to give away so much content for free. Or stated another way, “how do we get paid for all of this?”

The simple answer is that we know many (or even most) of you will simply take the ideas that we share and implement them yourself. Do-It-YourSelfers can always simply purchase our texts, books and peer reviewed handbooks redacted in more than a thousand, medical, law, business and graduate schools, as well as the Library of Congress,Institute of Health and Library of Congress.

On the other hand, some of you will realize you need some additional help.

For example:

Maybe as a financial advisor you’re “stuck” in your financial planning business and recognize that some outside assistance is necessary to help you get to the next level of niche specificity thru our Certified Medical Planner™ chartered certification program designation. Helping physicians of all specialty types in a fiduciary focused manner is the proverbial Win-Win for all concerned.

OR, perhaps you are seeking a glossary of terms and definitions in heath economics, finance, accounting, insurance, managed care, health information technology and security; found in our Health Dictionary Series Wiki Project? Free and print versions are available.

OR, as a doctor maybe your medical practice is growing so much you just hit a wall where you don’t have time to do it all for your patients. After all, with only “so much” time available every day and week, it’s vital to delegate or outsource anything that isn’t really core to your practice and management skill set.

OR, maybe you are even starting, buying or selling your medical practice and need our financial and valuation services. Part (1) – Part (2) – Part (3) Financial, estate, investing and retirement planning services are also available.

OR, you may just need a second informed opinion about a topic not listed; there are a myriad of issues to consider in the competitive ecosystem today.

So, in the meantime, I hope that the ME-P content continues to be helpful food for thought, and perhaps we’ll have an opportunity to cross paths soon at a future conferences or podcasts. Feel free to invite us to speak at your own seminar/podcast online V-log, as well.

TOPIC: Financial Designations and Certifications [Alphabet Soup of Industry Obfuscation and Self-Promotion, or Real Gravitas – You Decide?]

EXCERPT: “Until recently, most financial advisors were regulated by the NASD, the National Association of Securities Dealers. Now the Financial Industry Regulatory Authority or FINRA is the largest non-governmental regulator for all securities firms doing business in the United States. It is a self-regulatory agency comprised of the nation’s brokerage firms. Upon completion of a required exam the FINRA will issue a variety of licenses. The most common are the Series 6, 7, and 24.

The Series 6 is essentially a license to sell packaged products, namely mutual funds. It is most commonly held by insurance agents and bank representatives. It is considered a very easy test. Holding such a license allows the holder to collect commission income through its member firm.

The Series 7 exam is a bit more difficult and includes issues relating to individual securities such as stocks, bonds and limited partnership interests. The pass rate is lower than the Series 6. The probable culprit is the extensive questioning on margin and options, topics most are unfamiliar with prior to entering the securities business.

The Series 24 covers issues of compliance and supervision and is required of Branch Managers of brokerage firms. All registered representatives (the proper name for a broker) must be supervised by someone with a Series 24, also known as a principal’s license.

Checking the background of a registered representative, a branch manager or a member firm is easily done through NASD and/or FINRA Regulation, Inc. NASDR/FINRA maintains the Central Registration Depository (CRD). The CRD can be checked for a description of a disclosed event by phone or by Internet. One should request information on an advisor’s firm as well as the individual. A reputable advisor at a disreputable firm has its own set of potentially dangerous implications.

Regardless of the above, these tests produce licenses to sell financial products. They are not educational achievements. There is virtually no academic barrier to entry for them. Stock-brokers today – hate the term – and prefer “financial advisor”; yet the term has no real meaning other than as a sales license.

Some are college graduates, and beyond; while some other experts argue that too many are not!”

Hence, the need to “raise the bar to fiduciary accountability with deep knowledge of healthcare modernity.”

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on January 15, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Many investors were happy to wave goodbye to 2022, Wall Street’s worst year since 2008. The S&P finished down 19.4%, while the tech centered NASDAQ shed 33.1%. The blue-chip focused Dow Jones did better, losing just 8.8% across the year. Unfortunately, a number of senior investment bankers predict 2023 could bring more stock market woes. Most recently, in fact, Morgan Stanley Chief U.S. Equity Strategist & Chief Investment Officer, Michael Wilson, said he thought the S&P 500 could drop by another 22% in 2023.

Wilson wrote in a note this week that next year’s losses could be more significant than many are expecting. According to Bloomberg, Wilson thinks a peak in inflation would be “very negative for profitability.” He added, “The consensus could be right directionally, but wrong in terms of magnitude.”

Some analysts think that when inflation peaks, the Federal Reserve will ease up on its aggressive rate hikes and the stock market will recover. But Wilson argues this is only part of the picture. He thinks falling prices would have a knock-on effect on company profits, and the subsequent drop in margins would outweigh any benefit from a change in the Fed’s stance.

Wilson also alerted clients to the risk that companies would be caught “off guard” by a combination of falling demand and a catch up in supply. Supply chain issues, caused by a mix of COVID-19 lock downs, labor shortages, and other factors, have contributed to price increases and had a negative impact on production. If the supply chain starts to recover at the same time as recession-induced drops in consumption levels, he thinks the stock market could fall further.

Posted on January 6, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Here are eight things to keep in mind as you prepare to file your 2022 taxes

1. Income tax brackets shifted somewhat

There are still seven tax rates, but the income ranges (tax brackets) for each rate shifted slightly to account for inflation. For 2022, the following rates and income ranges apply:

Taxable income brackets

Tax rate

Single filers

Married couples filing jointly (and qualifying widows or widowers)

10%

$0 to $10,275

$0 to $20,550

12%

$10,276 to $41,775

$20,551 to $83,550

22%

$41,776 to $89,075

$83,551 to $178,150

24%

$89,076 to $170,050

$178,151 to $340,100

32%

$170,051 to $215,950

$340,101 to $431,900

35%

$215,951 to $539,900

$431,901 to $647,850

37%

$539,901 or more

$647,851 or more

2. The standard deduction increased somewhat

After an inflation adjustment, the 2022 standard deduction increases to $12,950 for single filers and married couples filing separately and to $19,400 for single heads of household, who are generally unmarried with one or more dependents. For married couples filing jointly, the standard deduction rises to $25,900.

3. Itemized deductions remain essentially the same

For most filers, taking the higher standard deduction is more practical and saves the hassle of keeping track of receipts. But if you have enough tax-deductible expenses, you might benefit from itemizing.

State and local taxes: The deduction for state and local income taxes, property taxes, and real estate taxes is capped at $10,000.

Mortgage interest deduction: The mortgage interest deduction is limited to $750,000 of indebtedness. But people who had $1,000,000 of home mortgage debt before December 16, 2017 will still be able to deduct the interest on that loan.

Medical expenses: Only medical expenses that exceed 7.5% of adjusted gross income (AGI) can be deducted in 2022.

Charitable donations: The deductions for charitable donations are not as generous as they were in 2021. In 2022, the annual income tax deduction limits for gifts to public charities1 are 30% of AGI for contributions of non-cash assets—if held for more than one year—and 60% of AGI for contributions of cash.

Miscellaneous deductions: No miscellaneous itemized deductions are allowed.

4. IRA contribution limits remain the same and 401(k) limits are slightly higher

The traditional IRA and Roth contribution limits in 2022 remain the same as the prior year. Individuals can contribute up to $6,000 to an IRA, and those age 50 and older also qualify to make an additional $1,000 catch-up contribution. If you’re able to max out your IRA, consider doing so—you may qualify to deduct some or all of your contribution.

However, the 2022 contribution limits for 401(k) accounts have increased to $20,500. If you’re age 50 or older, you qualify to make an additional $6,500 catch-up contribution for this tax year as well.

5. You can save a bit more in your health savings account (HSA)