BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The phrase “sell in May and go away” suggests that investors should sell their stocks in May and avoid the market during the summer months, as historical data indicates poorer stock performance during this period.

***

It’s Friday morning, so you’re probably clocking out once you’re done reading this ME-P. And who could blame you, after such a wild month of watching your portfolio zig & zag with every headline.

In fact, why not just sell all your stocks and walk away entirely? You’ve got to admit, it’s tempting. After all, markets have completed an incredible round trip since Liberation Day—you could just call it even, start celebrating Cinco de Mayo a bit late, and maybe check your portfolio again sometime around August.

“Sell in May and go away” might sound like appealing advice these days, especially considering that the market usually spends the next six months under-performing: The S&P 500 gains just 1.8% on average from May through October, the worst-performing stretch of the year historically.

These ‘worst six months’ have gained in eight of the last 10 years,” he recently wrote. He continued: “Not to mention the month of May has been higher nine of the past 10 years, so maybe we should call it,

Posted on May 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

Today, we’re diving into two thought-provoking questions:

What’s a famous investment rule I don’t agree with? Which key characteristics should a good investor have? Again:

What’s a famous investment rule I don’t agree with?

Which key characteristics should a good investor have?

A Famous Investment Rule I Don’t Agree With: “Buy and Hold”

Buy and hold becomes a religion during bull markets. Then, holding a stock because you bought it is often rewarded through higher and higher valuations. There’s a Pavlovian bull market reinforcement – every time you don’t sell (hold) a stock, it goes higher.

Buying is a decision. So is holding, but it should not be a religion but a decision. The value of any company is the present value of its cash flows. When the present value of cash flows (per share) is less than the price of the stock, the stock should not be “held” but sold.

WarrenBuffett is looked upon as the deity of buy and hold.

Look at Coca Cola when it hit $40 in 1999. Its earnings power at the time was about $0.80. It was trading at 50 times earnings. It was significantly overvalued, considering that most of the growth for this company was in the past.

Fast-forward almost a quarter of a century – literally a generation. Today the stock is at $60. It took more than a decade to reclaim its 1999 high. Today, Coke’s earnings power is around $1.50–1.90. Earnings have stagnated for over a decade. If you did not sell the stock in 1999, you collected some dividends, not a lot but some. The stock is still trading at 30–40x earnings. Unless they discover that Coke cures diabetes (not causes it), its earnings will not move much. It’s a mature business with significant health headwinds against it.

“Long-term” and “buy-and-hold” investing are often confused.

People should not own stocks unless they have a long-term time horizon. Long-term investing is an attitude, an analytical approach. When you build a discounted cash flow model, you are looking decades ahead. However, this doesn’t mean that you should stop analyzing the company’s valuation and fundamentals after you buy the stock, as they may change and affect your expected return. After you put in a lot of analytical work and buy the stock, you should not simply switch off your brain and become a mindless buy-and-hold investor.

This doesn’t mean you shouldn’t be patient, but holding, not selling, a stock is a decision.

Posted on May 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler CFP™ MSFP

***

***

DECLINE OF THE DOLLAR

On-again, off-again tariffs. Rising prices. Dramatic market swings. The anxiety-producing headlines come so fast it’s hard to know what to worry about first. Meanwhile, one serious consequence of all this chaos is going almost unnoticed. That is the decline of the dollar.

Since the start of this year, the value of the U.S. dollar has slipped more than 10% against other major currencies. That drop is not just an economic statistic. It affects all Americans’ daily lives.

People are feeling the pinch of rising prices at checkout lines, gas stations, and shipping counters. But there isn’t a full understanding of why. Tariffs are only half the story. The weakening dollar amplifies those price increases even further.

For years, the dollar remained strong even as the national debt ballooned. It benefited from its reputation as a safe haven, from global demand, and from U.S. interest rates. But much of that strength, as we now see, was fragile—propped up more by perception than fundamentals. In April, sweeping tariffs triggered a sharp market correction, and the dollar suddenly fell to its lowest point in over three years. Market confidence vanished overnight.

This was more than a market reaction. It signaled a collapse in trust—not just in policy, but in principle. It is no longer a given that the U.S. will act with consistency, reason, and long-term responsibility. What’s unraveling is both our country’s financial credibility and the moral foundation that underpinned it.

When a currency represents a nation, its value reflects more than economics. It reflects governance, accountability, stability, and integrity. When the dollar stumbles, it speaks to who we are, and whether we can still be counted on.

Yet, most people aren’t talking about the decline of the dollar. This may come from being overwhelmed, choosing to ignore even more bad news, or actually believing that this is a necessary step in making things better. It is not.

We all respond differently to financial uncertainty. Some lean into hyper-vigilance—tightening budgets, tracking every headline. Others shut down, turning toward distraction. Still others press on as if nothing has changed. These are all natural human reactions.

They are not the same as leadership. And leadership—internal and external—is what’s needed now. Not panic. Not blame. Just the courage to face where we are and the willingness to start again from there.

But leadership is in short supply in Washington, where many in both parties remain silent. Some fear political retribution from the administration, others fear backlash from increasingly extreme and vocal constituencies. That silence costs us all.

A respected government official recently told me that, while some of the domestic damage to our economy could be repaired within a few years, rebuilding global confidence in the United States may take a generation. That is a reflection of the rapid erosion of trust that has already happened in the last three months. Trust that took decades to build has been unwound in a matter of weeks. Even if we reversed every policy decision tomorrow, the damage is done.

We cannot change what’s already happened. We can still choose to show up. To pay attention. To have the hard conversations. To lead our own financial lives with more clarity, integrity, and intention than before. That kind of personal leadership may not fix the dollar. But it can help rebuild what underlies its value: trust, steadiness, and the moral grounding we’ve begun to lose.

Because the dollar’s decline is more than an economic headline.

It’s a story about who we are—and whether we’re ready to live with open eyes in a world where the old assumptions no longer hold.

Posted on May 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

The technology at the core of the mania is different every time. What doesn’t change over time is human emotion – the fear of missing out and then the fear of loss.

AI has a feel of “this time is different.” Optimism rarely erupts about the same technology twice; this is why history doesn’t repeat but rhymes. The technology at the core of the mania is different every time. What doesn’t change over time is human emotion – the fear of missing out and then the fear of loss, in that order.

Humans are an optimistic bunch. We need it; it’s essential to our survival and progress; but eventually, we take our optimism too far. The graveyard of financial ruins is full of these stories.

I have beat the dotcoms and Nifty Fifties to death, so let’s go to back another century. My friend the brilliant Edward Chancellor wrote about the railroad boom and bust in England in the 1800s. Here he is, edited for brevity:

The first railway to use steam locomotives opened in 1825 and was designed to carry coal, not passengers. Railway promoters simply did not appreciate the potential demand for high-speed travel. The successful launch of the Liverpool and Manchester Railway in 1830, however, demonstrated the commercial viability of passenger travel. By the early 1840s, Britain’s railway network stretched to more than 2,000 miles. Railway companies were delivering acceptable, if not spectacular, returns for investors.

Then railway fever suddenly gripped the nation. Enthusiasts touted rail transport not just for its economic benefits, but for its benign effects on human civilization. One journal envisaged a day when the “whole world will have become one great family speaking one language, governed in unity by like laws, and adoring one God.” In the two years after 1843, the index of rail stocks doubled.

Investment peaked at around 7% of Britain’s national income. Railway enthusiasts predicted that rail would soon replace all the country’s roads and that “horse and foot transit shall be nearly extinct.”

In 1845, Britain’s railways carried nearly 34 million passengers. If the 8,000 miles of newly authorized railways were to deliver their expected 10% return, then the industry’s total revenue and passenger traffic would have to climb five fold or more – all within the space of just five years. “This should have alarmed observers by itself … But they were deluded by the collective psychology of the Mania”, writes Odlyzko.

In 1847 a severe financial crisis broke out, induced in part by the diversion of large amounts of capital into unprofitable railway schemes. It turned out that the revenue projections provided by so-called “traffic takers” were wildly overoptimistic. Railway engineers underestimated costs. The vogue for constructing direct lines between large urban centers proved mistaken, as most traffic turned out to be local. As a result, Britain’s rail network was plagued with overcapacity. By the end of the decade, the index of railway stocks was down 65% from its 1845 peak.

The railroad bubble in England is just one example; there are hundreds of similar stories across market history. They all share this theme:

A new technology appears on the horizon. In the early stages, investment is rational, but then at some point excitement, imagination, and optimism take over, leading to overinvestment (usually creating a financial bubble). Investors make a lot of money until most lose it all. When the dust settles, only a few companies survive.

This AI boom reminds me of the telecom sector in the 1990s. The internet was going to change the world, and it did, but first we had tremendous overcapacity in global fiber and telecom equipment.

One could say that telecommunications companies overestimated demand for broadband and underestimated changes in technology, and that would be true. But there was a more nuanced dynamic at play, what economists call the fallacy of composition.

What’s true for one participant isn’t necessarily true for the group.

Posted on May 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

“Any time you make a bet with the best of it, where the odds are in your favor, you have earned something on that bet, whether you actually win or lose the bet. By the same token, when you make a bet with the worst of it, where the odds are not in your favor, you have lost something, whether you actually win or lose the bet.”

– David Sklansky, The Theory of Poker

Over a lifetime, active investors will make hundreds, often thousands of investment decisions. Not all of those decisions will work out for the better. Some will lose and some will make us money. As humans we tend to focus on the outcome of the decision rather than on the process.

On a behavioral level, this makes sense. The outcome is binary to us – good or bad, we can observe with ease. But the process is more complex and is often hidden from us.

One of two things (sometimes a bit of both) can unite great investors: process and randomness (luck). Unfortunately, there is not much we can learn from randomness, as it has no predictive power. But the process we should study and learn from. To be a successful investor, all you need is a successful process and the ability (or mental strength) to stick to it.

Several years ago, I was on a business trip. I had some time to kill so I went to a casino to play blackjack. Aware that the odds were stacked against me, I set a $40 limit on how much I was willing to lose in the game.

I figured a couple hours of entertainment, plus the free drinks provided by the casino, were worth it. I was never a big gambler (as I never won much). However, several days before the trip I had picked up a book on blackjack on the deep discount rack in a local bookstore. All the dos and don’ts from the book were still fresh in my head. I figured if I played my cards right I would minimize the house advantage from 2-3 per cent to 0.5 per cent.

Wanting to get as much mileage out of my $40 as possible, I found a table with the smallest minimum bet requirement. My thinking was that the smaller the hands I played, the more time it would take for the casino’s advantage to catch up with me and take my money.

I joined a table that was dominated by a rowdy, half-drunken blue-collar worker who told me several times that it was his payday (literally: he was holding a stack of $100 bills in his hand) and that he was winning. I played by the book. But it did not matter. Luck was not on my side and my $40 was thinning with every hand.

Meanwhile, the rowdy guy was making every wrong move. He would ask for an extra card when he had a hard 18 while the dealer showed 6. The next card he drew would be a 3, giving him 21. Then the dealer would get a 10 and then a 2 (on top of the 6 that already showed), leaving him with 18. The rowdy guy barely paid attention to the cards.

Posted on May 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

If getting answers from ChatGPT makes you feel dystopian, you may not want to hear about OpenAI CEO Sam Altman’s other co-founded venture, now rolling out stateside. It scans your eyeballs in exchange for cryptocurrency.

What in the Demolition Man? The device, which creates a unique user ID for your scan, is meant to address a problem that Altman had a hand in creating: how to verify identities and confirm humanity in a world full of artificial intelligence.

The project, called World (formerly Worldcoin), went live in other countries in 2023. Its US expansion, announced this week, featured retail outlets in five cities where you can get your eyes scanned:

Tools for Humanity, the company behind the orbs, says 12+ million people around the world have participated so far.

It claims to keep your data private, but authorities in more than a dozen places have suspended World’s operations or investigated its data practices, per the WSJ.

Posted on May 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants LLC

***

***

During the first 90 days of the Republican Party’s government trifecta (controlling the White House, Senate, and House of Representatives), both the Trump Administration and Congress have laid the groundwork for seismic change to the U.S. healthcare industry.

In an attempt to track the latest actions of the federal government’s legislative and executive branches affecting the healthcare industry since the first installment in our February issue, this Health Capital Topics article summarizes recent events in Washington and the impact of these changes on providers and patients. (Read more…)

Some retired people live on a fixed income and many of them live right on the edge of their financial capability. At some time in their life, they may have to make a choice regarding many purchases.

In this case, we will illustrate “choice” using a couple’s purchase of Long-Term-Care Insurance [LTCI]. Of course, economics is the study of choice; wants, needs and scarcity, etc. In our case, if they decide to make the purchase they commit to a lifetime of premium payments. The financial tradeoff is this; if they make the commitment to purchase LTCI, they must give up something else.

EXAMPLE: In order to maintain a monthly premium of $100 ($1,200per year), an elderly patient, retired layman or couple must essentially relegate about $30,000 of financial assets to generate the $100 necessary to make an average premium payment (assumes a 7% rate of return with 4% withdrawal rate) or [4% X $30,000 = $1,200 year]. Thus, if the monthly premium cost is $500 per month, the elder must give up the use of $150,000 of retirement asset just to generate enough cash flow to pay for the LTC insurance.

***

***

The married elder couple has to make the Hobson’s Choice decision among lifestyle (dinners, vacations, gifts to children, prescription drugs, medical care or food and shelter) versus paying an insurance premium to provide for nursing home coverage for a need, which may be very real, but will not occur until sometime in the ambiguous future.

And so, when faced with such a tough economics Hobson’s Medicine Choice, neither of which delivers peace of mind or a respectable solution; many will simply decide that, in either case, they may already end up impoverished. Thus, many will often opt for the better lifestyle now … while they can enjoy it … together.

Cite: Anonymous Health Insurance Agent, Norcross, Georgia

COMMENTS APPRECIATED

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on May 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants LLC

***

***

While the healthcare industry has been dealing with high employee turnover since the start of the COVID-19 pandemic, that turnover was largely among clinical staff.

However, a recent survey found that significant healthcare leadership turnover may also be on the horizon. AMN Healthcare subsidiary B.E. Smith found that nearly half of healthcare executives plan to leave their organization in the next year.

This Health Capital Topics article reviews the survey and the reasons behind the intended exits. (Read more…)

Posted on May 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Caterpillar eked out a 0.54% gain after raising its fiscal 2025 revenue forecast, but the construction giant warned that it will eat about $350 million in extra tariff-related costs.

What’s down

Super Micro Computer plunged 11.50% after reporting terrible preliminary earnings and warned of weaker results still to come.

Etsy beat revenue expectations last quarter, but fell 5.74% after missing profit forecasts as the number of buyers and sellers using its platform continued to fall.

Snap tumbled 12.43% after the social media stock warned that economic uncertainty could hurt its advertising business and refused to issue a fiscal forecast.

Chili’s parent company BrinkerInternational fell 1.89% despite posting solid earnings as investors worry about slowing consumer spending.

Norwegian Cruise Line sank 7.77% after missing earnings and warning of a slowdown in demand.

Stat: $228 million. That’s how much Sacramento-based Sutter Health—one of the largest health systems in the US—agreed to pay to settle allegations of inflating insurance premiums. (Reuters)

Read: Here’s what some say the new Medicare director, a former tech CEO, is likely to focus on. (Stat)

Posted on April 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Consumer sentiment is a statistical measurement of the overall health of the economy as determined by consumer opinion. It takes into account how people feel about their current financial health, the health of the economy in the short-term, and the prospects for longer-term economic growth. It is widely considered to be a useful economic indicator.

Consumer sentiment emerged as an economic statistic during the mid-20th century and has since become a barometer that influences public and economic policy. It is considered a lagging indicator because it takes people several months to notice and feel the effects of changes in economic activity.

American consumers are Worried about the Economy

Consumer sentiment dropped 8% from March to April amid worries about inflation, according to the University of Michigan’s closely watched survey. Though sentiment edged up slightly from an even lower reading earlier in the month, inflation expectations climbed to their highest since 1991 as consumers fret about the potential impact of tariffs.

And even beyond possible rising prices, things could be about to get rougher for consumers: Major retailers have warned that unless President Trump’s tariff policy toward China changes, they’re likely to encounter empty store shelves in a few weeks.

Posted on April 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Coca-Cola rose 0.84% after the beverage behemoth beat earnings expectations. Not only that, it also doubled down on its forward-looking guidance, saying that revenue will grow 5% to 6% while comparable earnings per share will jump 2% to 3% in 2025. Tariff mania may raise some costs, but the company said it would be “manageable,” putting it a step ahead of arch-rival PepsiCo.

Pfizer jumped 3.28% today after the pharma giant announced that it expects to cut costs by about $7.7 billion by the end of 2027 thanks to advances in AI and automation. Despite lower sales in Q1, the company managed to keep its 2025 revenue guidance of $61 billion to $64 billion intact. While that forecast takes into account the $150 million blow from tariffs, it does not include any future tariffs (which President Trump has threatened to slap on the pharma industry).—LB

Meta Platforms gained 0.85% after the social media giant announced it will launch a standalone AI app to compete with ChatGPT. Expect more details in its earnings call tomorrow.

JetBlue Airways may have pulled guidance, but investors like the airline’s lower-than-expected loss last quarter so pushed shares 2.70% higher.

Speaking of fintech, PayPal climbed 2.14% thanks in no small part to a 20% pop in Venmo revenue.

Honeywell International gained 5.40% thanks to strong earnings and sales for the manufacturing conglomerate.

Deutsche Bank climbed 4.08% after Germany’s largest lender reported a 39% increase in profit last quarter.

Sherwin-Williams may have missed on revenue last quarter, but the paint company beat earnings estimates and kept its forward guidance intact, so shareholders pushed it up 4.80%.

Royal Caribbean eked out a 0.02% despite reporting record bookings and boosting its profit outlook, a rare move these days amid tariff uncertainty.

Leggett & Platt may not be a household name, but it sells household goods—and the bedding company’s solid earnings and strong fiscal guidance sent shares 31.73% higher.

What’s down

General Motors fell 0.64% after the automaker beat on top and bottom line estimates but warned that it will have to pull its forward guidance and suspend stock buybacks.

Spotify dropped 3.04% despite active monthly users rising 10% last quarter. The problem, believe it or not, was lower guidance.

Regeneron lost 6.87% thanks to disappointing sales for its hit eye drug Eylea.

NXP Semiconductors may have beaten analyst estimates last quarter, but management’s lower-than-expected earnings guidance disappointed investors, and pushed shares 6.94% lower.

The Zweig Breadth Thrust may sound like an extremely difficult yoga position, but it’s actually a bullish technical indicator with an extraordinary record of 100% accuracy that was just triggered.

Created by investment advisor and author Martin Zweig, the indicator takes the 10-day moving average of the number of advancing stocks across the market and divides it by the number of advancing stocks plus the number of declining stocks. When the resulting percentage rises from below 40% to above 61.5% in 10 trading days, it’s a sign that stocks are rapidly going from oversold to overbought.

The math is a bit complicated, but Carson Research’s Chief Market Strategist Ryan Detrick certainly thinks highly of it.

According to the chart that he just posted on X, the Zweig Breadth Thrust has a perfect record of predicting market gains 6 and 12 months after it appears.

With the indicator triggering on Friday, here’s hoping that we can continue to trust the Zweig Thrust.

If you looked at how stocks were doing yesterday morning and then looked away, we’ve got good news.

After a rough start to the day—especially for tech companies, whose earnings are due out soon—stocks mostly turned things around, with the S&P 500 and the Dow ending the day in the green.

***

***

IBM plans to invest $150 billion in the US over five years. That includes $30 billion earmarked for R&D for manufacturing its mainframe and quantum computers in the US. It’s not the only tech company to announce a big commitment to spend in the US since President Trump took office and unveiled steep tariffs on imports from abroad.

Nvidia and Apple have each separately said that they plan to spend $500 billion stateside over the next four years. Companies in other industries, including pharmaceuticals, have also committed to increased US investment.—AR

Posted on April 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler CFP™

***

***

Lately, I’ve been hearing the same question from clients and readers alike: “Is Social Security even going to be there in five years?” Fueling this concern is a recent viral comment from Elon Musk, who told Joe Rogan that Social Security is “the biggest Ponzi scheme of all time.” That quote has been repeated in every corner of the internet, stirring up uncertainty and fear.

Elon Musk is a genius, but his brilliance in technology and innovation doesn’t automatically translate into expertise in public policy. When it comes to Social Security, he’s outside his lane. Calling it a Ponzi scheme may make for a great soundbite, but it’s a fundamental mischaracterization.

Social Security is not a Ponzi scheme. Not even close.

A Ponzi scheme is a form of financial fraud that lures investors with the promise of high returns. Instead of earning those returns through legitimate investments, the scheme pays earlier investors using money from newer ones. Eventually, the model collapses when there aren’t enough new participants to keep it going, leaving most people with significant losses. This is what happened to those who trusted Bernie Madoff, operator of one of the worst Ponzi schemes in history. Ponzi schemes are illegal, deceptive, and doomed from the start.

Social Security, in contrast, is a government-run, pay-as-you-go tax program. It’s fully transparent; you know exactly where your money is going. The payroll taxes you and your employer pay are used to provide income to today’s retirees, people with disabilities, and surviving family members of deceased workers. This isn’t a con, it’s a social contract.

So why the confusion? Part of the issue is that Social Security does, on the surface, resemble the flow of a Ponzi scheme: money coming in from the young to support the old. But similarity in structure doesn’t make it fraudulent. The program does not promise high returns, it promises a modest, inflation-adjusted benefit to support people as they age.

Social Security does face challenges. The trust fund reserves, built up during years when payroll taxes exceeded payouts, are projected to run dry around 2033. If Congress does nothing, benefits will need to be cut by about 20%. That’s serious, but it’s a solvency issue, not a scam.

And the solvency issue is fixable. There are numerous bipartisan proposals to shore up the system for the long term, from raising the payroll tax cap to gradually adjusting benefits. These aren’t radical ideas, they’re common-sense repairs. A bipartisan mix of 100 CFPs in a room could work out a solution in two days.

When clients ask me if the system will be around in five years, what they’re really asking is: Can I trust it? Can I trust the government? Can I trust that my years of work and tax payments will mean something in retirement? These are not just policy questions. They are emotional questions based on fear of scarcity and a desire for security. When someone with Elon Musk’s influence wrongly calls Social Security a Ponzi scheme, his attention-grabbing soundbite shakes the emotional foundation of that trust.

If we’re serious about preserving Social Security, let’s start by calling it what it is: a commitment to our elders. A tax-supported promise to care for one another across generations.

Social Security is not a fraud, it’s a shared responsibility based on the kind of society we want and woven into the fabric of American life. Yes, it needs some adjustments, but it’s not broken. Rather than eroding public trust with misleading comparisons, we should be focused on debating public policy and how we can strengthen and sustain the program for future generations.

***

ME-P NOTE: An increase in Social Security benefits is on the horizon, providing a potential financial cushion against rising inflation. The Cost of Living Adjustment (COLA) for 2025 is set at 2.5% monthly, translating to an average annual increase of approximately $600 for beneficiaries. This adjustment is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers. While not guaranteed annually, COLA has historically been implemented in most years due to persistent inflationary trends.

Posted on April 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants LLC

***

***

On April 7, 2025, the Centers for Medicare & Medicaid Services (CMS) published their 2026 Rate Announcement for Medicare Advantage (MA) and Medicare Part D Prescription Drug Plans.

For 2026, the payment rate to MA plans will increase 5.06%, the largest increase in the past ten years, and up significantly from the 2.2% rate increase proposed by the Biden Administration.

This Health Capital Topics article will review the Rate Announcement.(Read more…)

Much like a springy inflatable structure often resembling a four-sided building and used by children for jumping for sport and fun, stocks staged a much-needed bounce-house back week on hopes that the trade war would de-escalate, with the S&P 500 climbing for four straight days to close 4.6% higher.

Whether the rally continues this week may depend on the Magnificent Seven earnings on tap—each of those Big Tech stocks has fallen at least 6.5% this year, shedding a combined $2.5 trillion in market value, per the Wall Street Journal.

The fourth market is defined as private transactions made directly between large medical investors, institutions such as banks, mutual funds, and insurance companies, without the use of a securities firm. In other words, fourth market trading is usually one institution swapping securities in its portfolio with another large institution.

From the stock broker’s viewpoint, there is one problem with the fourth market. Since no broker/dealer is involved, no registered representative is involved and there is no commission to be earned. These trades are reported on a system called Instinet.

This is advantageous to larger medical foundations or institutional investors.

What Is Instinet?

Instinet is a global financial securities service that operates an electronic securities order matching, trading, and information system which allows members, primarily institutional traders, and investors, to display bids and offer quotes for stocks, and conduct transactions with each other.

Instinet is an example of a dark pool of liquidity, a private exchange for trading securities that is not accessible by the investing public. The name implies a lack of transparency. and it facilitates block trading by institutional investors who do not wish to impact the markets with their large orders.

According to the SEC, there were 74 registered Alternative Trading Systems, or dark pools, as of February 2024.

Posted on April 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler CFP™

***

***

On January 21, 1980, in what I thought was a brilliant financial move, I bought gold. At what was then an all-time high of $873 an ounce.

Fast forward 45 years, and here we are again. Gold is on a tear, priced just over $3,000 an ounce at the time of this writing. It needs to rise another 16% to reach its inflation-adjusted record and many analysts think it might just get there.

What’s driving this gold rally? The same thing that drove it in 1980—fear.

Back then, the U.S. was grappling with rising inflation, double-digit price increases, and interest rates in the high teens. Investors feared that the dollar and stock market would collapse, that their hard-earned savings would erode into oblivion, and that gold was a safe haven. Sound familiar?

Today, inflation is less dramatic and the stock market would have to go a long way down to even register as a bear market, but it’s still a major concern. Central banks are buying gold at record levels. Gold-backed ETFs, which had been seeing years of outflows, are finally pulling investors back in.

For most, gold isn’t just an investment, it’s an emotional hedge against uncertainty. Back in 1980, I wasn’t thinking about long-term strategy. I was reacting to fear. Inflation had hit 14%, and like many others, I was convinced the dollar would soon be worthless. Gold, I thought, was my best shot at preserving wealth.

The problem? Inflation eventually cooled; it had dropped to an average of 3.5% by the mid-1980s. Gold prices tumbled along with it. Investors who, like me, bought at the peak, 45 years later still haven’t broken even on an inflation-adjusted basis. (My $873 purchase price, adjusted for inflation, equates to $3,580 today.) If I had stuck with a well-diversified portfolio, I likely would have fared much better over time.

Over the years, I’ve come to realize that our financial decisions aren’t just about numbers. They’re deeply influenced by our Internal Financial System™, a framework that helps explain why we handle money the way we do. I now see that my decision to buy gold was a battle between different financial “parts” of myself.

One part panicked, convinced that money was about to become worthless. Another saw gold prices soaring and didn’t want to miss out. Yet another part convinced me that buying at the peak was still a smart move. Had I paused and examined these internal voices, I might have made a different decision.

My gold purchase shows why emotionally driven investment decisions rarely lead to great financial outcomes. Instead of asking, “Is gold a smart long-term investment?” I was asking, “How do I make sure I don’t lose everything?” Those are two very different questions.

If you’re thinking about buying gold, I urge you to consider these questions:

“Am I investing from a place of fear or strategy?” If you’re rushing in because you’re scared of inflation, pause and reassess.

“How does gold fit into my broader financial plan?” Gold can be a great hedge—if held in appropriate amounts in a diversified portfolio. It is best viewed as catastrophic financial insurance, rather than an investment.

“Am I reacting to headlines or making a well-thought-out decision?” The financial media loves a good gold rally. But remember, markets move in cycles. Today’s rally may be history repeating itself.

Back in 1980, fear persuaded me that gold was a sure thing. I forgot an essential caveat—there are no sure things in investing. If bad market timing were an Olympic sport, I’d have taken home the gold (pun intended) for least profitable performance.

In a discussion of competitive healthcare economic models, assumptions must include normal demand quantities, many fully informed patients and the fact that physicians cannot directly influence demand for medical care. These assumptions, although fluid, also preclude that patient buyers are large enough to have any influence over price and result in the following”:

In a “pure monopoly”, there is only one provider with a unique service. The doctor is a “price maker” and charges whatever s/he wishes.

In an “oligopoly”, there are a few physicians who provide similar services. For example, when it becomes clear to Dr. Smith and Dr. Jones that neither can win their price war, oli-gopolists return prices to prior, but still inflated levels!

In “monopolistic competition”, there are many providers with differentiated services. For example, should Dr. Jones decide to have evening hours, she may charge a premium for her fees if Dr. Jones doe not follow suit.

Finally, when “pure competition” occurs, there are many physicians, providing providing similar and substitutable services. Marketing and advertising does not affect fees, and prices are determined by supply and demand. The doctors become “price takers” by accepting fees arrived at by practicing competitively.

COMMENTS APPRECIATED

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on April 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

Tesla market value of $780 billion mostly reflects Elon’s future dreams, not car sales. The reality? Only $100-180 billion tied to the actual vehicle business.

***

Tesla has a market capitalization as of this writing of $780 billion. It made around $14 billion of profit in 2023 and $7 billion in 2024. A good chunk of profit comes not from selling cars but from regulatory credits. It sold fewer cars in 2024 than in 2023. Unless we see a significant shift change in battery capacity, speed of charging, and improved quality and availability of charging infrastructure, we have reached peak EV penetration (I wrote about this earlier).

However, today Tesla is not trading based on car sales but on future dreams of self-driving robo-taxis, robots, semis, and whatever else Elon dreams up. The car company may be worth $100–180 billion; the rest is what investors are willing to pay for Elon’s dreams.

Quick thoughts on each dream:

Self-driving: I would not trust my life or my kids’ lives to a car company that only uses cameras. They are passive sensors that have limited range and are easily impacted by bad weather. I’ve used Tesla self-driving software – it is great most of the time, except when it’s not – and then it might kill you or others.

Robo-taxis: They may work in geo-fenced areas, but they pose a huge reputational risk to Tesla. One death and this business is done. That’s what happened to Uber’s self-driving business, and why Google’s Waymo has taken a much more conservative route. It uses radar/lidar and launched the service in geo-fenced areas first.

Semis: They were announced in 2017 and were going to hit the road the next year. They are still not out there. I suspect Elon is waiting for a breakthrough in battery technology.

Robots: Exciting, huge market, but this will be a crowded field.

New competition: There are lots of Chinese EVs invading Europe and the rest of the world. BYD looks like a real competitor.

China looked like a great opportunity for Tesla, but may turn into a liability if the trade war intensifies.

Finally, though at times he seems superhuman, Musk is constrained by the number of hours in the day. As of today he is running Tesla, SpaceX, Twitter (x.com), xAI (the maker of Grok – a ChatGPT competitor), The Boring Company, Neuralink, and oh, yes, DOGE. The EV market is getting more, not less, competitive.

Posted on April 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Alphabet has been declared a monopoly for the second time in under a year. Analysts will have plenty of questions about the repercussions of the most recent ruling, but don’t expect a breakup of Google’s many businesses just yet.

And, the best business unit of them all these days is YouTube, which has seen a stunning surge in popularity lately that the search company will likely try to capitalize on, while it continues to tinker with its Gemini AI model. Consensus: $2.02 EPS, $89.25 billion in revenue.

***

***

Intel seems like a bit of an also-ran in the AI race these days, with shares down over 40% in the last 12 months. But to bulls, that just means the stock is cheap, while the company itself has plenty of opportunities for growth ahead, including partnerships with Nvidia and TSMC.

And, don’t forget that Intel’s status as a dark horse lets it slip below the tariff radar—the domestic chip producer dodged the latest round of restrictions that hit Nvidia and AMD. Shareholders will be hoping to hear more good news ahead. Consensus: $0.09 EPS, $12.31 billion in revenue.

***

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on April 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and Lawrence Rosenberg

***

***

Cold calling is a term that is typically applied to telesales, but most new business relationships actually begin with a “cold” contact of some kind. Whether through social media, email over the phone or door-to-door, “cold calling” lives up to its name; you are contacting prospects (hopefully decision makers) sans introduction and without warning. In some, if not many cases, you will be presenting to customers who have never heard of you, your firm, or your product/service prior to you getting a hold of them. You will also find yourself coming up against the palace guards (secretaries and personal assistants) whose most important job is to run interference for the boss and thwart any and all attempts that an unfamiliar caller might make to reach them. But, as the sales game will readily teach anyone with the fortitude to last long enough to learn the lesson, the more resistance one faces in the pursuit of a successful outcome, the bigger the payoff will be if one can muster the grit necessary to tough it out.

However difficult the road to riches, cold calling allows for a complete leveling of the playing field. Those that sweep the streets could tomorrow talk with billionaires; a man of little status or worth could enter into a contract with the founder of a blue chip, multinational firm — all with a single, unexpected phone call. The sheer daring of such an approach, its impromptu nature, works for so many reasons, not least of which is that it opens doors. From the intrigue and urgency the suddenness of the call implies, to the instant access a bold overture provides, cold calling is the great equalizer among executives, and a path to achievement open to all, no matter one’s experience, education or connections. Not that there ever were any truly insurmountable barriers to climbing the corporate ladder or accessing its highest rungs that a motivated self-starter could not overcome, but with the advent of the telephone and the brashness of the cold sell perfected, the most entrenched and frustrating of impediments, bureaucracy and fraternalism, ceased to be an obstacle. Yesteryear’s power elite traditionally only did business with friends, acquaintances and family (or perhaps a member of their local country club or lodge), but at the very least, those that connected in business were routinely introduced through a referral. However, the audacity of the unscheduled contact, the inspired notion of a “cold call,” and the realization that it worked, that a person of great esteem or importance was willing to do business with an unusually forward individual, made the glad-handing salesman who relied on his father’s rolodex obsolete.

With ivory towers toppled, etiquette overturned and tradition tossed out, ambitious men ignored propriety and custom and cold canvassed the board of directors and senior executive staff of companies both large and small. The old boy’s network, favoritism, and the “it’s not what you know, but who you know” principle of doing business crumbled in one fell swoop. The ramparts guarded by all manner of gatekeepers and middle men were trampled the moment the CEO became connected by wires to the outside world. Using nothing more than a telephone, a Horatio Alger-type work ethic and a well-rehearsed voice, the business world was invaded by those without patronage, underdogs and unknowns swarmed the gates. The cold call allowed the unfiltered, unapproved spirit of the upstart, unfettered by lackeys and administrators, to enter the inner sanctum of a chieftain and with the power of speech alone, win hearts and minds.

But, can one’s voice really move mountains? Must one not support the message with documentation and material, nurture relationships with lunches and meetings and personally shake hands to set the wheels of industry in motion? Is one unannounced, unsolicited, unscreened call enough?

The human voice is the master manipulator of sound and when paired with the right words it has a potent and intoxicating effect on behavior. Although some people react more favorably to stimulation of the other five senses, sound on its own can evoke them all. Those that study the science of suggestion will note the immense influence of other stimuli, such as that which affects sight and sensation, on how we make sense of our experiences, on how we make decisions, but it is the way in which such sensory bias is communicated (via the written word, and more powerfully, through speech) that truly tells the tale. The combination to unlocking the interests of many a man’s mind are often verbalized in the common yet telling replies to intriguing, thought provoking questions or action demanding requests.

***

***

It is all a matter of deciphering the code, the clue-laden language:

“What you said really touched me.”

“I see the light!”

“You can smell his fear.”

“Let’s give that guy a taste of his own medicine.”

“You are coming across loud and clear.”

The way in which we describe our observations provides the key to how we interpret data, how that data impacts us, and through what primary pathway we process such information. It is our use of language that exposes how we perceive the world around us, how the gears of our minds are moved, and which of the five senses most effectively winds the springs that turn them.

Many times a prospect will request to have a look at your proposition in writing before moving forward, others will react positively based solely on their impression. Some say seeing is believing, but if it soundsexciting and beneficial, they will take action regardless because it just feels right.

All our senses come alive when the brain is stimulated, some more than others depending on the man and the moment, but the terms, phrases and idioms that we use when speaking (their quality, nuance and character) and the way in which they are expressed, have the power to move us in life-changing ways — the spoken word, when used properly, can play us like a piano.

Whether impacted more by sight, olfaction or incitement of the somatosensory system (the way things feel physically), one can induce the imagery and kinesthesia necessary to motivate and influence a prospect from afar with voice alone. Provocative descriptions, the proper use of tone and inflection, and the strategic interweaving of silence (of which sometimes nothing can be more deafening or exert more pressure) can activate or set in motion all manner of action. Practiced speech can lighten the heaviest heart or wrest tears from the coldest stare, it can conjure up a dream state or snap you back to reality. Never underestimate what a skillful performer can do with the right vocabulary and properly trained vocals. Charlton Heston could inspire awe, Orson Welles conjure intrigue, and Luciano Pavarotti demand devotion with nothing more than the weight and timbre of their words.

You too can affect people, positions and outcomes with sonant spirit and verbal substance. Invest in the greatest tool for success a deal maker has, your lexicon, your locution and your delivery.

An annuity is a contract between you and an insurance company. When you purchase an annuity, you make a lump-sum contribution or a series of contributions, generally each month. In return, the insurance company makes periodic payments to you beginning immediately or at a pre-determined date in the future. These periodic payments may last for a finite period, such as 20 years, or an indefinite period, such as until both you and your spouse are deceased. Annuities may also include a death benefit that will pay your beneficiary a specified minimum amount, such as the total amount of your contributions.

The growth of earnings in your annuity is typically tax-deferred; this could be beneficial as you may be in a lower tax bracket when you begin taking distributions from the annuity.

Warning: A word of caution: Annuities are intended as long-term investments. If you withdraw your money early from an annuity, you may pay substantial surrender charges to the insurance company as well as tax penalties to the IRS and state.

***

***

There are three basic types of annuities — fixed, indexed, and variable

1. With a fixed annuity, the insurance company agrees to pay you no less than a specified (fixed) rate of interest during the time that your account is growing. The insurance company also agrees that the periodic payments will be a specified (fixed) amount per dollar in your account.

2. With an indexed annuity, your return is based on changes in an index, such as the S&P. Indexed annuity contracts also state that the contract value will be no less than a specified minimum, regardless of index performance.

3. A variable annuity allows you to choose from among a range of different investment options, typically mutual funds. The rate of return and the amount of the periodic payments you eventually receive will vary depending on the performance of the investment options you select.

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

A Certified Public Accountant (CPA) is a licensed professional who has passed an examination administered by a state’s Board of Accountancy. State CPA exams are created under guidelines issued by The American Institute of Certified Public Accountants (AICPA). The Uniform CPA Exam can only be taken by accountants who already have professional experience in the field and a bachelor’s degree.CPAs are not fiduciaries.

Not all accountants are CPAs. Accountants who are CPAs are licensed by their state’s Board of Accountancy after passing the Uniform CPA Exam. CPAs prepare reports that accurately reflect the business dealings of the companies and individuals that hire them. Many prepare tax returns for individuals or businesses and advise them on ways to minimize taxes. Obtaining the CPA designation requires a bachelor’s degree, typically with a major in business administration, finance, or accounting. Other majors are acceptable if the applicant meets the minimum requirements for accounting courses.

Enrolled Agent

Although not a CPA, an Enrolled Agent [EA] is a person who has earned the privilege of representing taxpayers before the Internal Revenue Service [IRS]. This is done by either passing a three-part comprehensive IRS test covering individual and business tax returns, or through experience as a former IRS employee. Enrolled agent status is the highest credential the IRS awards. Individuals who obtain this elite status must adhere to ethical standards and complete 72 hours of continuing education courses every three years.

Certified Managerial Accountant

A Certified Management Accountant (CMA), which is issued by the Institute of Management Accountants (IMA), builds on financial accounting proficiency by adding management skills that aid in making strategic business decisions based on financial data.

Oftentimes, the reports and analyses prepared by certified management accountants (CMAs) will go above and beyond those required by generally accepted accounting principles (GAAP).

For example, in addition to a company’s required GAAP financial statements, CMAs may prepare additional management reports that provide specific insights useful to corporate decision-makers, such as performance metrics on specific company departments, products, or even employees.

Certified Financial Analyst

A Certified Financial Analyst [CFA] is a globally-recognized professional designation offered by the CFA Institute, an organization that measures and certifies the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management, and security analysis. From 1963 through November 2023, more than 3.7 million candidates had taken the CFA exam. The overall pass rate was 45%. From 2014 through 2023, the 10-year average pass rate was 43%.1

CFA Institute. The CFA Institute was formerly the Association for Investment Management and Research (AIMR).

The CFA charter is one of the most respected designations in finance and is widely considered to be the gold standard in the field of investment analysis. To become a charter holder, candidates must pass three difficult exams, have a bachelors degree, and have at least 4,000 hours of relevant professional experience over a minimum of three years. Passing the CFA Program exams requires strong discipline and an extensive amount of studying.

There are more than 200,000 CFA charter holders worldwide in 164 countries.The designation is handed out by the CFA Institute, which has 11 offices worldwide and 160 local member societies.

Posted on April 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

OFTEN CONFUSING TO ALL

By Staff Reporters

***

***

A vehicle typically has two prices: the manufacturer’s suggested retail price (MSRP) and the invoice price. The MSRP is the sticker price, while the invoice price is what the dealer paid the manufacturer for the vehicle. The MSRP includes a hefty profit, so that’s what dealers want you to focus on. However, your goal should be to get the invoice price and focus on that for your negotiations.

However, finding invoice pricing on new cars can be difficult when going through the dealer. Dealers don’t want their invoice price on a vehicle to be public knowledge because that gives customers more leverage when it comes to negotiations. Just like any company, car dealers are in the business to make money. They can’t make money if they give you a huge discount on a car.

What is a Vehicle Invoice Price?

When it comes to the car buying process, there are several other terms and types of pricing you should understand. One of them is the vehicle invoice price. This is also known as the dealer cost, or what a car manufacturer charges the dealer for that specific vehicle. Freight charges are typically included in this total.

However, the numbers on the invoice may not be the true price the dealer paid for the vehicle, because it has hidden profits already built-in. Dealers are often given manufacturer rebates, allowances, discounts, and other incentives for selling a car. The invoice price on a vehicle may range from several hundred to several thousand dollars below its sticker price, which is why service will help you determine what the real numbers look like.

So, once you determine the car invoice price, you have added leverage when it comes to negotiating the best price possible with the auto dealer.

Posted on April 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Meta’s antitrust trial resumes: The FTC is accusing CEO Mark Zuckerberg of purchasing Instagram and WhatsApp to gain an unfair monopoly in the social media space, while the defense is expected to argue that the success of those apps is a product of Meta’s acquisition. Testimony will continue this week, with one Vanderbilt law professor telling Quartz that she expects to hear more expert testimony: “Judges tend to put a lot of stock in expert opinion in antitrust cases, especially when it comes to market definition and monopoly power.”

Netflix rose 1.57% on a strong vote of confidence from Wall Street pros: After last week’s earnings blowout, the streaming service received price target upgrades from JPMorgan, Wells Fargo, Goldman Sachs, Evercore ISI, Morgan Stanley and Piper Sandler today.

Discover Financial Services climbed 3.53% after its merger with Capital One got the greenlight from regulators. Capital One rose 1.54%.

MicroAlgo exploded 74.93% after the tech holding company became the latest hot penny stock du jour.

Gold miners continue to mint big gains as the hot commodity broke yet another record. Barrick Gold gained 1.39%, while AnglogoldAshanti climbed 2.13%.

Hertz Global gave up some of last week’s big gains today, dropping 4.98% as investors took profits following Bill Ackman’s hint that the rental car company may team up with Uber.

Speaking of, Uber fell 3.08% after the FTC sued the ride-hailing company for “deceptive billing and cancellation practices.”

Amazon lost 3.11% thanks to a downgrade from Raymond James analysts. They believe the e-commerce titan’s retail and advertising businesses are too exposed to tariffs.

Salesforce stumbled 4.45% on a downgrade from DA Davidson analysts, who say the SAAS company is too focused on AI and not on its core business.

Deutsche Post AG, better known as DHL, announced it is suspending shipments worth over $800 as the international shipping company struggles with tariffs. Shares fell 1%.

Now that the US government is negotiating drug prices directly with manufacturers, states want to get in on the action, too. These efforts vary by state, but generally involve creating a board to review drugs’ affordability and sometimes setting upper price limits (UPLs). While none have implemented UPLs as of April, as the idea gains momentum, there are questions about UPLs and boards’ legality, practicality, and whether they will actually lower costs for patients.

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

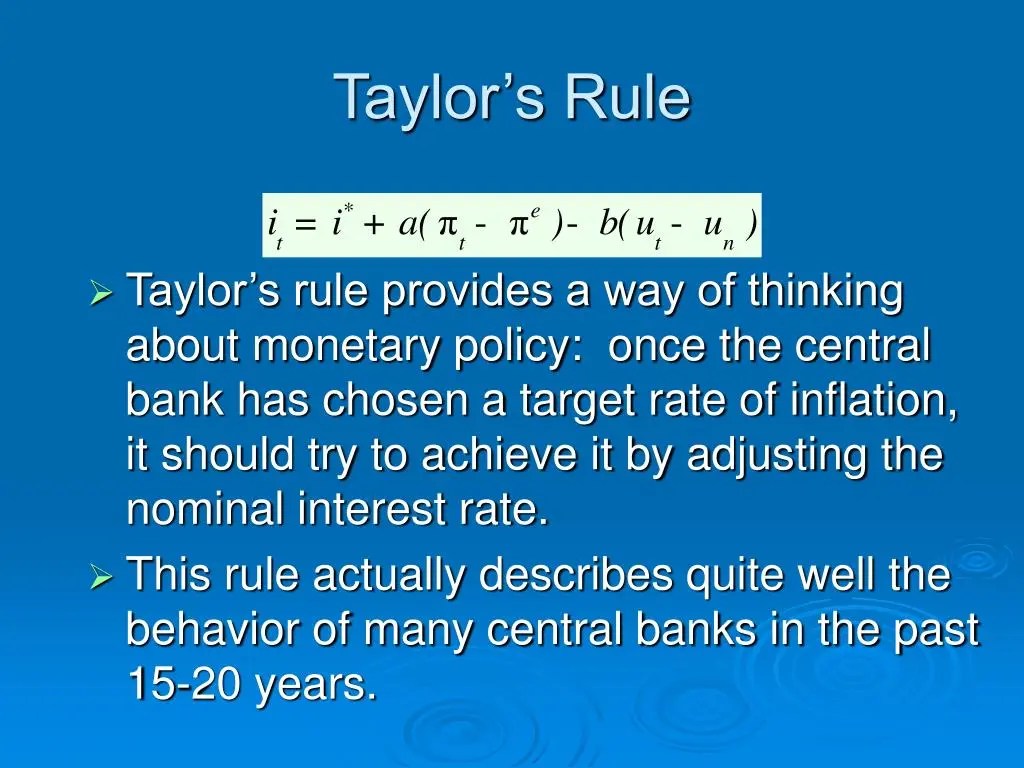

Named for a U.S. economist, the JB Taylor Rule is a mathematical monetary-policy formula that recommends how much a central bank should change its nominal short-term interest rate target (such as the U.S. Federal Reserve’s federal funds rate target) in response to changes in economic conditions, particularly inflation and economic growth. It’s typically viewed as guideline for raising short-term interest rates as inflation and potentially inflationary pressures increase. The rule recommends a relatively high interest rate (“tight” monetary policy) when inflation is above its target or when the economy is above its full employment level, and a relatively low interest rate (“easy” monetary policy) under the opposite conditions.

To illustrate, the monetary policy of the FOMC changed throughout the 20th century. The period between the 1960s and the 1970s is evaluated by Taylor and others as a period of poor monetary policy; the later years typically characterized as stagflation. The inflation rate was high and increasing, while interest rates were kept low. Since the mid-1970s monetary targets have been used in many countries as a means to target inflation.

However, in the 2000s the actual interest rate in advanced economies, notably in the US, was kept below the value suggested by the Taylor rule.

Posted on April 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

Artificial Intelligence Enhanced

***

***

Markets drop as tariff concerns shake the market

Key takeaways (1:30 EST)

The Dow Jones Industrial Average experienced a significant drop of more than 1,100 points, reflecting investor anxiety over tariff policies finance. The S&P was down 150 and the NASDAQ was down 550.

This decline is part of a broader trend affecting the S&P 500 and NASDAQ, as geopolitical tensions and economic uncertainties weigh heavily on market sentiment finance.yahoo.com .

Investors are closely monitoring developments regarding trade policies and their potential impact on the economy, leading to heightened volatility in the stock market

The VIX soared to 60.13 last Monday before plummeting all the way to 33.76 on Wednesday, the day after the president paused tariffs. But while the VIX has since settled down a bit, investor fear is still high. The VIX closed above 30 for 10 straight trading sessions and the last time that happened was during the bear market back in October 2022, according to MarketWatch—not exactly a comforting comparison.

Then again, just because fear skyrocketed last week doesn’t mean the markets will tank in turn. “Since 1997, there have been 11 times the VIX spiked above 45—and 10 out of 11 times, the S&P 500 was higher four months later by an average of +6.4%,” noted Austin Hankowitz in the latest edition of the Rich Habits newsletter.

Finally, the VIX closed above 30 Thursady as tariff talk and monetary policy pivots keep investors on their toes. But while worries might keep investors on the sidelines, some on Wall Street are taking this opportunity to be greedy while others are fearful.

There’s often a disconnect between physicians, insurance agents and financial advisors and the patients and clients they’d like to serve. Both might ostensibly share the same goal but there’s often a big difference in perspective. Advisors / Physicians and would-be clients / patients likely have different communication styles, especially in an age where technology has greatly changed the way we talk with one another. Their expectations and priorities can also often dramatically diverge. Those structural gaps can hinder collaboration and trust.

To bridge this divide, you must understand how prospective clients and patients think nowadays and be able to adjust your M.A.S. approach accordingly.

THE BASICS

Marketing is the business process of identifying, anticipating and satisfying patient’s, client’s or customers’ needs and wants. It is your unique value proposition or strategic competitive advantage. Marketers can direct product to other businesses or directly to consumers. But, we believe it is actually your strategic competitive advantage [SCA] which differentiates yourself from competitors. It is the “moat” around your business.

Advertising is a marketing communication that employs an openly sponsored, non-personal message to promote or sell a product, service or idea. Sponsors of advertising are typically businesses wishing to promote their products or services. Advertising is communicated through various mass media outlet, including traditional media such as newspapers, magazines, television, radio, outdoor advertising or direct mail; and new media such as search results, blogs, social media, websites or text messages. The actual presentation of the message in a medium is referred to as an advertisement, or “ad” or advert for short. But, we believe that is simply how you disseminate your strategic competitive advantage [SCM] to potential clients.

Sales close the deal and collects money. Sales are activities related to selling or the number of goods or services sold in a given targeted time period. The seller, or the provider of the goods or services, completes a sale in response to an acquisition, appropriation, requisition, or a direct interaction with the buyer at the point of sale. There is a passing of title (property or ownership) of the item, and the settlement of a price, in which agreement is reached on a price for which transfer of ownership of the item will occur. The seller, not the purchaser, typically executes the sale and it may be completed prior to the obligation of payment. In the case of indirect interaction, a person who sells goods or service on behalf of the owner is known as a salesman or saleswoman or salesperson, but this often refers to someone selling goods in a store/shop, in which case other terms are also common, including salesclerk, shop assistant, and retail clerk.

***

***

DERIVATIVE THOUGHTS

Public Relations [PR] is differentiated than advertising from in that an advertiser pays for and has control over the message. It differs from personal selling in that the message is non-personal, i.e., not directed to a particular individual. We pay for advertising but pray for public relations. But public relations are not controllable but it is free, while advertising is not. PR suggests that “good news or bad news”; just spell the name correctly

Change Management is the discipline that guides how we prepare, equip and support individuals to successfully adopt to change in order to drive organizational success and outcomes.

Crisis Management is the precautions and identification of threats to an organization and its stakeholders, and the methods used by the organization to deal with these threats.

MODERNITY NOW

CRM stands for Customer Relationship Management, which is a system for managing all interactions with current and potential customers, clients or patients. The goal is simple: improve relationships to grow your business or medical practice. CRM technology helps companies stay connected to customers, streamline processes, and improve profitability.

When people talk about CRM, they’re usually referring to a CRM system: software that helps track each interaction you have with a prospect, patient or customer. That can include sales calls, treatment plans or service interactions, marketing e-mails, and more. CRM tools can unify customer and company data from many sources and even use Artificial Intelligene [AI] to help better manage relationships across the entire customer – patient lifecycle – spanning departments described in the M.A.S. basics, above.

When you buy a share of stock, you are taking ownership in a company. Collectively, the company is owned by all the shareholders, and each share represents a claim on assets and earnings. If the company distributes profits to its shareholders, you should receive a proportionate share of the earnings.

Stocks are often categorized by the size of the company, or their market capitalization. The market capitalization is determined by multiplying the number of outstanding shares by the current share price. The most common market cap classes are small-cap (valued from $100 million to $1 billion), mid-cap ($1 billion to $10 billion), and large cap ($10 billion to $100 billion).

Stocks are also categorized by their sector, or the type of business the company conducts. Common sectors include utilities, consumer staples, energy, communications, financial, health care, transportation, and technology.

***

***

Stocks are often viewed as being in one of two categories — growth or value.

Growth stocks are ones that are associated with high quality, successful companies that are expected to continue growing at a better-than-average rate as compared to the rest of the market.

Value stocks are ones that have generally solid fundamentals, but are currently out of favor with the market. This may be due to the company being relatively new and unproven in the market, or because the company has recently experienced a decline due to the company’s sector being affected negatively. An example of this would be if the federal government was to levy a new tax on all cell phones, thus negatively affecting all cell phone company stocks.

History has shown that, over time, stocks have provided a better return than bonds, real estate, and other savings vehicles. As a result, stocks may be the ideal investment for investors with long-term goals.

Posted on April 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

U.S. stock and bond markets will be closed on Good Friday. Many global markets will also be closed Friday. Exceptions include Japan and mainland China, which will be open as usual. U.S. markets will reopen Monday. Many international markets will remain shut to mark Easter Monday, including Australia, Hong Kong, and exchanges in France, Germany and the U.K.

***

YESTERDAY 4/17/25

***

🟢 What’s up

TSMC eked out a 0.10% gain after the semiconductor maker reported a 60% increase in profits last quarter and downplayed the effects of tariffs.

Charles Schwab isn’t just the guy who made $2 billion from market chaos last week. It’s also the brokerage that reported record quarterly revenue, but shares only rose 0.65%.

Hertz climbed another 43.87%, tacking on another day of big wins after Bill Ackman’s Pershing Square Capital took a stake in the rental car company.

Trump Media & Technology Group popped 11.65% after the company asked the SEC to investigate a hedge fund with a $105 million short bet against it.

Chinese tea chain Chagee soared 15.86% in its first day of trading on the Nasdaq.

DR Horton missed analyst expectations last quarter and lowered its fiscal year guidance, but investors quickly forgave the country’s largest homebuilder and pushed shares up 3.16%.

What’s down

Alphabet took a 1.38% hit after a federal judge ruled that Google is a monopoly. This marks Alphabet’s second antitrust loss since last August.

Alcoa fell 6.98% after the aluminum mining behemoth announced it ate about $20 million in tariff-related costs last quarter, noting that this figure could rise to $90 million in the current quarter.

Carried interest accounts for the bulk of private equity fund managers’ compensation. It is calculated as a share of fund profits, historically 20% above a threshold rate of return for limited partners.

In contrast with most other forms of employment compensation and business income, carried interest earned from fund investments held for at least three years is taxed as a long-term capital gain at a rate below the top marginal income tax rate.

Critics of the provision contend it taxes highly compensated private equity managers at a lower rate than comparably paid providers of labor or business services.

Defenders of carried interest argue taxing it as income would be unfair because it represents capital gains even if they’re not derived from recipients’ capital.

Posted on April 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

UnitedHealth stock nosedived 20% in morning trading, falling by $116 per share from Wednesday’s $585 close to $469. The Minnesota-based firm is on track for its steepest daily loss since Aug. 6, 1998.

The losses came after UnitedHealth’s first-quarter financial report was worse than analysts expected across each of the three major quarterly yardsticks: revenue, earnings per share and future earnings outlook.

Furthermore, after the opening bell, the Dow Jones Industrial Average tumbled 1.3%, or around 500 points. The S&P 500 moved up 0.4%, while the tech-heavy NASDAQ composite gained 0.5%.

Abbott Laboratories gained 2.77% after the pharma company missed sales estimates but still beat earnings forecasts.

Gold miners continue to climb as gold keeps hitting new highs. Newmont rose 2.51%, while Gold Fields gained 3.35%.

What’s down

Tesla sank 4.94% after the company’s share of EV sales in California fell below 50% in the first quarter, while export controls threaten plans to produce Cybercabs in the US.

United Airlines fell 0.01% despite reporting its “best first-quarter financial results in five years,” according to management. The airline took the unique measure of providing two different financial outlooks for the year ahead: one for a stable economy, and one for a recession.

Lyft shed just 0.46% on the news that the ride-hailing company is acquiring European taxi app Free Now for $199 million.

Interactive BrokersGroup reported a 47% increase in trading volume last quarter that helped it beat revenue expectations, but the brokerage still tumbled 8.95% after missing profit forecasts.

Palantir gave up some of its recent gains following its big NATO announcement, sinking 5.78% today as investors collected profits.

JB HuntTransport Services’ management team warned that the logistics company sits squarely in the crosshairs of the trade war, pushing shares down 7.68%.

Omnicom Group tumbled 7.28% after the advertising firm missed revenue estimates thanks to economic uncertainty.

Posted on April 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Investors were apparently tired of all the volatility yesterday, leading to a relatively calm day where indexes ever-so-slightly slipped. But it was a big day for Netflix after the Wall Street Journal reported that the streaming giant has plans to double its revenue and reach a $1 trillion valuation by 2030.

***

🟢 What’s up